Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

Europe

German FTTH deep-dive

While German broadband volume growth is slowing, New Street argues this is outweighed by a more rational market structure taking shape. Fibre overbuild looks set to remain far lower than in most other markets, supporting sustainable pricing and derisking the payback on high levels of FTTH capex per premise. Their report highlights the growing number of wholesale deals emerging; how the MDU market structure is likely to play out given the new draft law amendment; and evolving thoughts on the SDU fibre overbuilder market where they have more visibility on the longer-term wholesale dynamics. New Street also examines the implications for key players including Deutsche Telekom, Tele Columbus and Deutsche Glasfaser.

Consumer stocks poised for a recovery

AIR expects a wave of upward revisions from European corporations in the coming months as tariff clouds thin, China stabilises, infrastructure spend ramps up and European rates remain low. The missing piece is consumer confidence, which should rebound quickly if geopolitical tensions ease. Consumer names like Inditex, Stellantis, LVMH, Diageo, Kering, Adidas, Nestle and Unilever look compelling after steep share price declines, with valuations back to decade-lows. Many of these firms are pursuing clear turnaround strategies focused on FCF generation, deep efficiency gains (utilising AI) and renewed focus on core businesses - supported by a trend toward insider CEO appointments, after a decade of appointing outsiders.

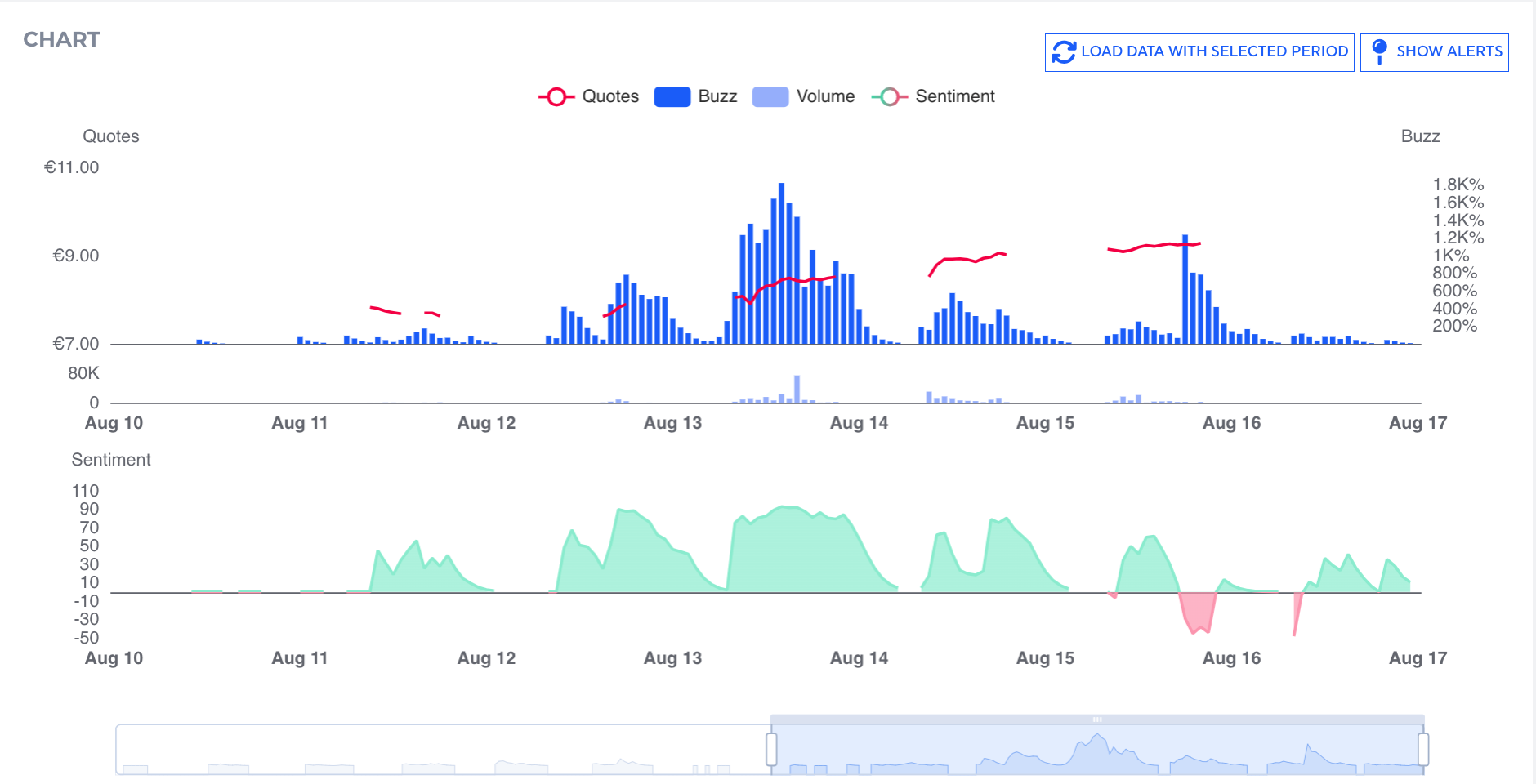

Stockpulse, whose platform provides real-time insights into social media sentiment, highlights a wave of positive attention around TUI. This was particularly apparent on 12th Aug, when the company reported a buzz score of 443% and a sentiment score of 86. This surge in communication and positive mood could be attributed to the company's recent earnings guidance update. Given the significant increase in market sentiment and buzz ahead of the earnings announcement, along with the positive stock price movement and exceeded earnings expectations, TUI's short-term outlook appears bullish. However, the market will need to assess whether this momentum can be sustained in the coming days and weeks.

SBMO delivered another impressive performance in H1 and raised FY25 guidance. The Fast4Ward model is proving highly effective: in the past 7 months, 3 FPSOs with a combined 650kbpd capacity have achieved first oil, with unprecedented time-to-market that sets SBMO apart. While net debt of $5.6bn is still a concern for some investors and came in above consensus, it largely reflects new FPSO construction financing and the IDEA! expects deleveraging to progress as planned. This underpins its $1.7bn dividend / buyback commitment through 2030, with further upside from new orders and two unallocated hulls. Given SBMO’s continued strong performance, the IDEA! reiterates their positive stance.

The shares have risen ~30% YTD (+75% 1Y), reaching Insight’s €75 SOTP-based TP. While recent tariff increases and the successful execution of a major capex programme have supported sentiment, the stock now trades at 8.2x 2026E EV/EBITDA (vs. 7.6x LT avg.) and looks overvalued vs. peers. Structural constraints persist, with Frankfurt’s majority state ownership, unionised workforce and insourced ground handling keeping EBITDA margins low. Aviation returns are weak, with NOPAT/RAB averaging just 3.2% in 2010-19 and only 5.4% by 2040E, still 120bps below Insight’s 6.6% WACC. Tariffs are expected to average just +2.0% p.a. through 2050E, despite high Aviation capex (€390m p.a.). With DPS resuming at only €1.0 in 2025E (1.3% yield), Insight has a Sell rating on the stock, preferring ADP (+75% upside), Aena (+55%) and FH Zurich (+55%).

North America

High-conviction short ideas

Dick’s Sporting Goods (DKS) - the Foot Locker acquisition will go down as one of the most value-destructive deals in retail history. The first time DKS misses a quarter because of perennial weakness at FL, this newco will trade at 3-4x EBITDA.

Best Buy (BBY) - 100% of EBIT comes from extended warranties, credit and membership - all of which are facing cyclical and secular pressure. Tariffs could take margins to zero, spurring a massive round of store closures.

Lam Research (LRCX) - the most complacent name in semicap with 2026 WFE expectations set too high especially in DRAM. P/E now 4.5x turns above 3-yr average despite little growth in 2026. Domestic competition in China intensifying longer-term.

AI driven 10Q / 10K filings analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) Advanced Micro Devices - struck previous wording around the need to discount products, suggesting more confidence in pricing power. 2) Bright Horizons Family Solutions - no longer anticipating expanding operating cash flows. 3) GoDaddy - takeover target? Plus, further colour on international expansion plans. 4) Gilead Sciences - more competitive market for Bulevirtide. 5) Installed Building Products - new change in control agreement prompted by external takeover interest? 6) New York Times - increasing concerns re. competitors gaining market share at its expense.

Assessing the risk of a crash in the Canadian housing market

Veritas’ latest Housing Riskometer update highlights continued stress in the Greater Toronto Area (GTA) and Greater Vancouver Area (GVA) housing markets. Current months-of-inventory levels suggest detached and condo prices in both regions could fall ~10% Y/Y, or at least another 5% from Jun 25 levels. While prices have declined in recent months, a meaningful correction has yet to occur. To contextualise risks, Veritas reviews prior housing busts - GVA in 1981 and GTA in 1989 - where prices dropped more than 25% peak-to-trough, to understand the current resilience better. Specifically, they examine the labour market conditions during the two historical market downturns.

How to play America’s atomic acceleration

The US nuclear sector is at an inflection point. The Department of Energy has launched a program to fast-track the approval of 11 new reactor designs, with first units targeted for approval by 2026, as part of broader plans to quadruple capacity by 2050. Momentum is spilling into capital markets, with developers seeking more than $500m via SPACs and IPO pipelines building. A major step last week saw ASP Isotopes and subsidiary QLE sign an MOU with Fermi America to develop new enrichment capacity at the planned 11 GW HyperGrid campus in Texas. Yet while demand is surging, uranium supply growth remains constrained - leaving the fuel chain as the sector’s hard limit, and where high-conviction opportunities are emerging.

The Genius Act has changed America’s relationship with crypto, making it the most attractive country in the world for stablecoins. Abacus’ latest report notes that while the pace of adoption is still unclear, long-term disruption of financial incumbents appears inevitable. CRCL’s model is attractive if USDC can scale, though Abacus estimates ~10x growth is needed to deliver a reasonable IRR - a challenging hurdle. Blockchains are expected to replace legacy infrastructure, with SWIFT the first casualty. Visa and Mastercard face limited near-term risk, but crypto is the primary long-term threat to their duopoly. Stablecoins have the potential to reach >$2trn m/cap in the next few years vs. $260bn today. Abacus sees CRCL as a compelling risk/reward play, with upside potential of 150% outweighing downside risk of 55%.

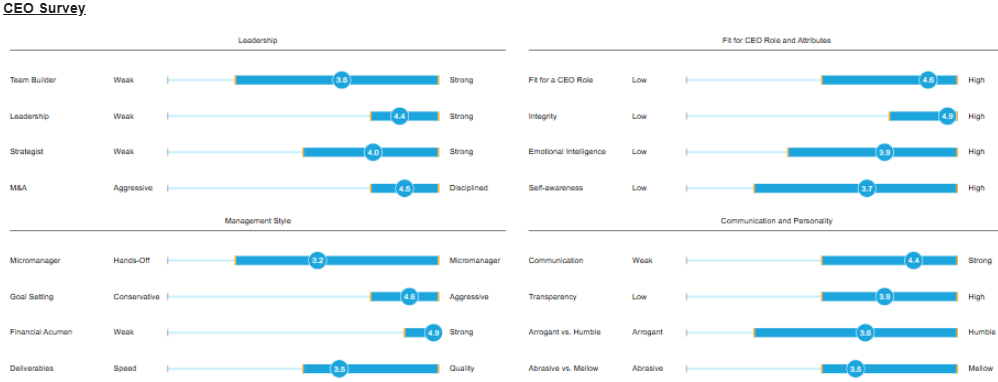

Paragon interviewed 7 former senior executives at ATS who worked with BAX's new CEO, Andrew Hider, for more than 36 years combined. Feedback was universally positive. Hider is a disciplined, process-driven leader who blends Danaher-style operational rigour with strong communication and an ability to scale businesses via organic growth and M&A. At ATS, he drove cultural transformation via the ATS Business Model, delivering margin expansion and shareholder returns, though his intense stretch targets and competitive nature created a high-pressure environment that could limit collaboration and agility. His success at BAX will hinge on whether he can balance his relentless operational focus with greater strategic flexibility and adaptability to the slower-moving, more regulated dynamics of the pharmaceutical industry.

KCR slashes tech exposure

KCR’s evidence-based stock selection process has swung from unambiguously bullish tech to record levels of bearishness. KCR's report (click here to access) shows long exposure in the technology sector across all their Large Cap model portfolios was >50% between 2014-2019 but has since collapsed to a far more modest 32%. Contrarily, 59% of their short model portfolios are now made up of tech stocks. The impact is even more dramatic in KCR's Small & Mid Cap portfolios - only 5% of their long book is in tech, while 58% of their SMID short model portfolios are IT names. KCR’s report also includes their Top 10 Ranked Long and Bottom 10 Ranked Short ideas.

While CDNS appears to be handily beating both sales and earnings estimates, BTN’s analysis shows it is being driven by increasingly aggressive revenue recognition. Recurring revenue growth slowed to 6.5% Y/Y in 2Q25 (vs. mid-teens previously), while upfront revenue has surged >100% Y/Y in the last 3 quarters. BTN cautions comps will toughen significantly in Q4 and even modest declines in upfront revenue would see CDNS lose its EPS beats. Unbilled receivables have doubled in the last 8 quarters and long-term receivables doubled in Q2. Deferred revenue days of sales has also dropped Y/Y for 4 consecutive quarters. Additional red flags include lower bad-debt reserves and an EPS boost from higher stock comp. At >50x forward EPS, there is little margin for error before the stock price could face pressure.

Boyar argues investor fears around FI are overblown. While the loss of a respected CEO, macro uncertainty and competitive pressures in the Merchant business have weighed on sentiment, Boyar sees the past year’s share price swing as a textbook case of exuberance turning into excessive pessimism. The company retains leading market positions, a strong operating track record and a mid-teens earnings growth outlook, yet trades at just ~12x forward P/E - its cheapest valuation in over a decade. Wall Street’s intense focus on Clover's short-term performance overlooks FI’s host of other valuable business lines, which together contribute ~83% of revenue. Applying a 19x multiple to 2027E EPS of $13.33, Boyar values the stock at $253, implying ~90% upside.

Richard Windsor argues that SoftBank’s $2bn investment in INTC, alongside a potential 10% US government stake, may keep the company alive but does little to resolve its strategic paralysis. INTC faces a stark choice: either invest heavily to catch up with TSMC or break up the business - yet under new CEO Mr. Tan, neither path is clear. The board abandoned Pat Gelsinger’s catch-up strategy due to mounting costs, leaving INTC exposed to further share losses in PCs (to AMD and Qualcomm) and in data centres (to Nvidia and AMD). Richard warns that without decisive strategy, customer confidence will erode, competitors will gain share with ease and capital injections alone cannot avert decline. He sees no attractive entry point in INTC shares.

According to Systems Integrators who work with SNOW, they saw strong 2Q25 momentum driven by rapid partner expansion and AI innovation. The company now has over 10,000 partners worldwide reflecting heavy investment in programs that broaden global reach. New AI-driven tools, including Cortex AI, Iceberg tables, and adaptive compute capabilities, enable enterprises to interact with data in natural language and automate pipelines, and are driving revenue. Strategic acquisitions, such as Crunchy Data, further enhance Postgres capabilities and enterprise appeal. To sustain momentum, SNOW is leaning heavily on system integrators, hyperscalers and resellers to drive adoption of next-gen AI offerings.

Japan

Japan’s space capabilities are rapidly expanding

Investor enthusiasm in the country’s space sector is accelerating, underpinned by several IPOs expected in the next couple of years. At SPEXA 2025, this enthusiasm was on full display, led by Toyota’s backing of Interstellar Technologies, which plans a listing and aims to capture the growing low-Earth-orbit launch market. Japan is also positioning itself at the forefront of space-debris removal working with Astroscale and JSAT, targeting an international regulatory framework by 2026. Meanwhile, government ambitions include doubling the space industry to ¥8trn, achieving 30 annual rocket launches by the early 2030s and deepening NASA collaboration, including a Toyota-built lunar rover. Neil Newman sees Japan’s space industry as an increasingly attractive investment theme.

Emerging Markets

China's biotech rally has only just begun

Horizon Insights argues that investors continue to underestimate the sector’s progress as global pharma validation accelerates. Over the past year, BMS, Merck and others have paid billions in upfront licensing fees for Chinese-developed assets. China now leads globally in ADCs and bispecifics, representing 40-50% of pipelines. YTD, MNC-led upfront BD payments total $9.1bn, on pace to double last year’s total. Horizon sees a structural repricing underway, driven by big pharma patent cliffs, supportive policy and rising clinical credibility. If 2018 marked the breakout for China EVs, 2025 could do the same for innovative drugs. Top picks include Innovent Bio, Keymed Biosciences and Akeso.

Lucror maintains a “Buy” on Greentown China’s 8.45% ’28s (102.8/7.1%/2.2Y), citing attractive carry and manageable credit risks. The H1/25 profit warning (~90% y/y decline to CNY 205mn) reflects delivery timing and non-cash impairments rather than underlying liquidity stress. Credit quality is supported by a strengthened capital structure, with short-term debt reduced to <20% of total and Cash/ST debt at a record 2.5x. Access to financing remains solid, backed by parent China Communications Construction Group, demonstrated by successful bond issuances and continued land-banking activities in Tier 1-2 cities. Despite earnings volatility from the absence of recurring income and sector ASP pressure, Lucror’s “Stable” credit bias reflects expectations of continued resilience and relative outperformance.

AceCamp analyses H1 results for these two leading robotaxi companies, focusing on revenue structure, burn rate, strategic focus and commercialisation outlook. They believe WeRide's early-mover advantage in globalisation and Pony.ai's capability for technological mass production represent two divergent industry paths. In the short term, Pony.ai's diversified revenue structure offers greater resilience; in the long run, WeRide's high-growth overseas markets may unlock larger opportunities, though local operational costs remain a challenge.