Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

Europe

Global Infrastructure stocks offer massive upside

Robert Crimes remains bullish on the Infrastructure sector, citing strong long-term traffic growth, resilient IRRs (averaging 11.3%, +290bps above Insight’s 8.5% Ke) and deep value in listed equities trading ~40% below NAV, despite private market transactions averaging just -3% below NAV over the past decade. The sector shows a weighted average upside of +78%, with notably higher upside in North America (+102%) and Europe (+73%) versus South America (-5%). Credit risk is not a concern, as leverage is manageable, bond yields have plateaued after a sharp 2022 rise and most debt remains fixed at low rates with long durations. Robert's top picks are Ferrovial, Canadian National Railway and Cellnex, each offering over +110% upside.

Fighting Financials reiterates their short thesis on EQT and lowers their TP to SEK205 (~30% downside). EQT continues to lose market share, growing FAUM at +7.8% in 1Q25, materially below sector peers. The firm faces structural headwinds - sticky interest rates are reducing prospective IRRs and volatile markets are preventing easy exit opportunities, while LPs also remain overexposed to private assets, making fundraising more difficult. Rising PE portfolio company defaults (especially in France) and increased distressed credit activity further underscore market stress. In this environment, Fighting Financials prefers the more adaptable alternatives specialists like Apollo and as geopolitical tensions rise, the case for investors hiding in the more “anti-fragile”, defensive financials becomes more compelling.

Insider buying at BNZL has picked up significantly in recent months - Richard Howes (CFO since 2019) bought £300k of shares at an average price of £23.21 in Apr, followed by a £100k purchase at £22.19 on Jun 18th. Peter Ventress (Chair since 2020) purchased £200k on Jun 24th at £23.52. This is his second purchase and four times larger than his Jun 2020 buy at £21.60. Jacqueline Simmonds (Director since 2023) made her second purchase on Jun 23rd, spending £51k at £23.28. Since early Mar, 6 insiders have purchased a total of £2.5m in shares, mostly around the £23 level. Given the breadth and scale of buying, Smart Insider upgrades the stock further to +1 (highest conviction rating).

Boring and beautiful - Pierre-Olivier Essig calls ELIS the best mid-cap to buy in Europe right now. Its mission? Helping hotels, hospitals and other hospitality clients eliminate laundry headaches via its vast footprint, microchip-enabled linen tracking and upgrading the quality of cleaning. With much of the sector still yet to outsource laundry services, the opportunity remains compelling. Growth is predictable: ~2% from volume, 2% from price and 2% from M&A annually. EBIT margins just hit a record 35.2% and management's 38% medium-term target is in sight. With +110% upside to his TP of €50 and trading at just 12x 2025 earnings (vs. 50x for Cintas), ELIS looks insanely cheap.

North America

Special Sits Idea Forum

While all the stocks presented at MYST's latest buyside event could be considered undervalued, many offered significant (i.e. >50%) upside. The most differentiated ideas included: Blackbaud (improving fundamentals more apparent post-EVERFI divestiture; potential M&A target); HealthEquity (new legislation fuelling dramatic TAM expansion + bond portfolio repricing tailwinds); and JBS (multiple to expand as US listing drives increased passive ownership / index inclusion). More familiar names discussed included: Fluor (huge NuScale Power (SMR) monetisation catalyst not reflected in Street estimates); Teva Pharmaceutical (generics cash cow enabling innovative branded portfolio pipeline development); and Warner Bros. Discovery (well positioned for media consolidation wave amid forthcoming business separation).

NBIS plans to establish a data centre in the UK just a week after raising $1bn via a convertible debt offering, underscoring its accelerated capital expenditure strategy. The announcement coincided with media reports of Nvidia's plans to invest in the UK. The growing availability of Blackwells should benefit revenue mix as the year progresses. Hamed Khorsand forecasts revenue to grow from $55.3m in 1Q25 to $292.2m in Q4 for a full year amount of $607.8m. He expects revenue to reach ~$1.5bn in 2026 with NBIS generating adjusted EBITDA of $379.1m. Reflecting this outlook, he raises his target price from $60 to $80, with the shares already up ~80% since his Jan 2025 initiation.

What’s trending in Retail

Each week, The Retail Tracker offers an insightful perspective on retail, fashion and consumer trends and what it means for the stocks. So far this year, Garage is a standout, nailing the “sexy x comfy” aesthetic for teens and taking share from Aerie and Pink. Gap and Old Navy are “crushing it” with consistently strong assortments, offsetting tariff challenges through fewer markdowns. Meanwhile, Urban Outfitters and Nuuly are gaining traction, with Nuuly emerging as a promising rental and tech-driven play. Aritzia is showing good momentum with its best assortment in some time. Department stores may be in free fall, but the best Macy’s stores have never looked better. In contrast, Lululemon is losing its way, expanding beyond its core and diluting its brand identity, while Bath & Body Works' range of new items is exhausting.

Scott Muskin sees WMT as the “Nvidia of Retail” and explains why its equity could be worth a remarkable $250 per share. The upside is grounded in a powerful multi-year strategy driving accelerating earnings growth, supported by automation, expanding e-commerce profitability, surging advertising income, Walmart+ and improving sales mix. Scott draws bullish parallels to his experience in covering Amazon and its journey around enhancing profitability over the last 12+ months, as well as developing a WMT 2034 financial model similar to what he did to appraise AMZN's potential in its North American business. Fixing the “fresh” food offering through improved quality, delivery and in-store experience is also flagged as a critical catalyst for driving frequency, market share gains and a broader halo effect across the entire business.

KCR highlights the strength and diversification of AMGN's commercial portfolio and drug pipeline, which should drive revenue and EPS growth in 2025 despite looming patent expirations on drugs representing 21% of 2024 sales. AMGN also appears well-positioned to absorb potential pricing and trade pressure from anticipated Trump Administration policies. Yet, the shares trade at just 14x 2025 EPS guidance (30% discount to the S&P 500), despite generating $10.4bn in 2024 FCF (nearly $20/share) and offering a 3.4% dividend yield. KCR sees significant upside in a potential re-rating, estimating each P/E multiple point adds ~$20 to the stock. A key catalyst is the MariTide weight-loss drug; successful trials could drive a ~$55 revaluation.

ISRG shares have come under pressure amid rising concerns about competition from remanufacturers. In March, Restore Robotics’ Iconocare Health received 510(k) approval to remanufacture the 8mm Monopolar Scissors (SKU 470179) for the DaVinci Xi system, following similar approval for the DaVinci Si system in 2022. MedMine analysed data from over 1,000 healthcare facilities and found that this SKU represents ~14% of ISRG’s US I&A sales. However, over 98.5% of purchases still come directly from ISRG, with no meaningful signs of remanufactured alternatives gaining traction. While remanufacturing poses a potential long-term threat, MedMine sees no current evidence of hospital adoption and will continue to track the trend closely.

Aerospace & Defence: High-tech growth in disguise

The A&D sector is undergoing a structural re-rating, evolving from a traditionally cyclical industry into a long-duration growth theme with rare earnings visibility. Currently operating at just ~75% capacity (well below historical peaks c.90%), the sector has meaningful room to grow before encountering bottlenecks, supported by strong order flow, rising production and record backlogs. What's more, the rapid adoption of new military technologies - especially in cybersecurity and the escalating global race in space - is blurring the lines between aerospace/defence and the tech sector. Yet, these defence companies still trade at far more compelling valuations. This remains one of David Rosenberg’s highest-conviction investment themes, offering a unique blend of stability and innovation.

Northcoast raises their TP for the stock to $250 (24x 2026 earnings estimate of $10.58), citing strong execution and share gains in HVAC, helped by FERG's focus on dual/multi-trade contractors and leverage to Daikin brands amid R-454B shortages. Management lifted guidance, with gross margins now seen above 30% and higher operating margin expectations, reflecting strong pricing and easing commodity deflation. Despite weak residential markets, FERG’s diverse end-market model is proving advantageous. With private label potential, sales leverage and underappreciated non-residential exposure, Northcoast sees the stock as undervalued and well-positioned to benefit from shifting industry dynamics and eventual recovery in residential demand.

Channel feedback on BOX is turning decisively more positive, according to Sales Pulse Research. BOX has built a strong reputation as an enterprise-grade file storage and content management platform, offering superior security, scalability and cost efficiency vs. OneDrive and Dropbox. The company is well positioned to benefit from AI adoption and growing unstructured data. Its partnership with Nvidia has enhanced Box AI, enabling more powerful and secure enterprise automation. Partners note BOX’s strong integrations, governance tools and alignment with cybersecurity platforms. Several now lead with BOX over traditional solutions, citing better incentives and opportunities for services-led engagements.

IOT trades at 100x forward EPS despite being a mature company with limited history of profitability. The firm continues to rely on low-quality sources of EPS growth to drive earnings beats. In Q1, cash R&D and S&M cuts alone added 6.1 cents to EPS, while stock compensation still exceeds 100% of adjusted EPS and cash flow. Deferred Revenue and Remaining Performance Obligations are growing more slowly than sales and both DSOs are dropping (drawing down DSOs by only 1 day is worth $4m in sales and 0.5 cents in adjusted EPS). With fundamentals increasingly out of sync with valuation, BTN believes even modest signs of slowing growth could trigger significant multiple compression.

TOST’s business model continues to face major challenges in competing for new enterprise customers, with recent wins driven by customer-specific weaknesses and aggressive financial concessions. GPV per average location has declined Y/Y for 7 consecutive quarters, suggesting TOST is either sacrificing payments revenue to support its upmarket narrative or failing to gain real traction. To stay competitive, TOST may need to open its platform to alternative payments processors and 3rd-party point solutions, which could dilute per-location economics or force costly pricing shifts. OWS expects multiple compression as optimism fades, noting TOST currently trades at ~3.2x EV/FY2 Revenues vs. a 2.3x 2-yr avg. TP $24 (45% downside).

Vertical Software: Mid-cap winners in mission-critical markets

Vertical software companies continue to generate superior shareholder returns, supported by durable industry dynamics and deep competitive moats. These firms deliver domain-specific, high-utility solutions that integrate into mission-critical workflows, enabling strong customer retention and product-led growth grounded in sector expertise. Operating in oligopolistic, niche markets with winner-takes-most characteristics, they face limited competitive disruption due to unattractive risk-reward profiles for new entrants. 2Xideas’ in-depth report is structured in 4 parts: a comparison of vertical vs. horizontal software models; a review of the shared operational characteristics of vertical players; a proprietary scoring of 43 mid-cap vertical software names; and 10 highlighted investment ideas including Autodesk, Global-E Online, PTC and Tyler Technologies.

Emerging Markets

Uncovering value in Indonesia

Mike Churchill begins a 3-part series on Indonesia’s overlooked value stocks, starting with heavy equipment, mining and steel names - these stocks all feature in his long-running Classical Insights portfolio (up an extraordinary +5556% since 2002). United Tractors offers the most upside (~75%), trading at 0.8x book and offering a near-10% dividend yield, while coal pricing tailwinds could support a rebound into year-end. Despite a tough 2025, Hexindo Adiperkasa stands out as a 15% dividend-yielding cash machine with 30%+ historical ROEs, trading at 1.5x book. PT Steel Pipe has built a lot of value over the years, looks very cheap and has performed well so far in 2025 with the shares up over 20% YTD.

Tata Motors posted a stable Q4 FY25 performance with flat revenue and margin recovery, aided by strong Jaguar Land Rover (JLR) results. However, the near-term outlook appears weak. JLR is expected to face a sharp decline in wholesale volumes due to high US channel inventory ahead of tariffs. Uncertainty over tariff impact persists. Domestically, Tata is losing share in both passenger vehicles and EVs due to rising competition. In commercial vehicles, market share losses and upcoming AC regulations for trucks will likely keep growth and profitability under pressure.

Saudi market volatility has surged in 2025, with the TASI down 11% YTD amid rising geopolitical concerns. Almarai shares have fallen 10.8% YTD despite strong Q1 results, with net profit up 5.6% Y/Y to SAR731m and revenue rising 5.7% to SAR5.77bn. The company continues to pursue growth, recently acquiring Pure Beverages for SAR1.04bn to strengthen its drinks portfolio and tap high-growth markets. AlphaMena sees 25% upside based on their DCF valuation. With resilient fundamentals, strong brand equity and long-term demand growth in Saudi Arabia and Egypt, the recent stock correction presents an attractive entry point. Almarai now trades at a 17-year low EV/EBITDA of 10.8x.

EM Spreads initiates coverage on CSN with an Overweight rating, favouring the CSN 6.750% 2028s (yielding 8.8%, duration 2.3 years) and 4.625% 2031s (yielding 9.2%, duration 5.0 years). They expect CSN to maintain its BB credit ratings, supported by strong liquidity, stable credit metrics and a clear commitment to deleveraging. Favourable macro tailwinds, including expected rate cuts in Brazil and easing global trade tensions, could lead to spread compression toward the LatAm BB curve. Both bonds trade below par, offering room for price appreciation. EM Spreads' preference is further supported by comparison with similar-rated Brazilian peers such as BEEFBZ 8.875% 2033s and AEGEBZ 9.000% 2031s.

Macro Research

Developed Markets

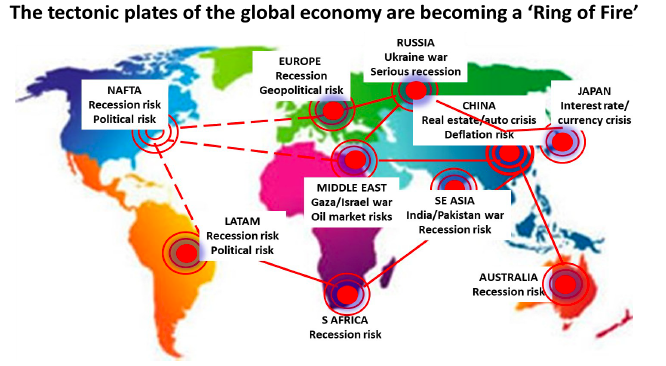

Ring of fire

The latest developments in the Middle East only add to the unfolding risks around the globe and Paul Hodges’ Ring of Fire model is heating up (see chart). He sees Asia as the key risk, with China’s ‘subprime on steroids’ policy since 2008 and Japan’s debt-fuelled ‘3 arrows policies, which Paul discusses in detail in his latest report. The chances of a sequel to 2008 are continuing to rise, but this time the potential for a joint response is very limited; Trump has divided the Western allies and the Tariff wars are more likely to escalate than evaporate. Could we see a repeat of the successful 2009 G20 crisis meeting? It agreed a $5trn boost to the global economy, added $1trn to the IMF’s lending budget and established the Financial Stability Board. The sums involved today would have to be much higher and cooperations appears less likely than ever.

PMs are all in

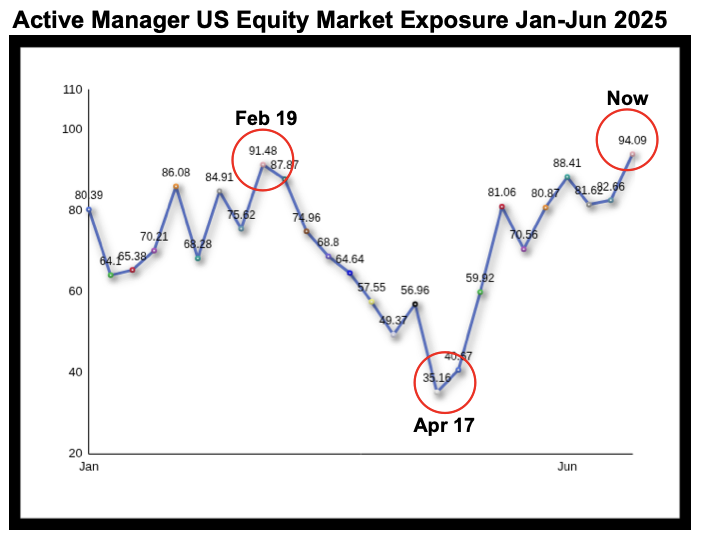

Despite tariffs, wars, soaring oil prices, slowing economy, etc., Michael Belkin points out that stock managers are ultra-committed to the stock market. This isn’t sentiment, it’s positioning, with PMs now more fully invested than at the market's peak. High equity market exposure is a reverse indicator, suggesting they will be dumping stocks into a selloff. Michael also points out the biggest anomaly of the AI bubble: semiconductors. At almost 10% of the index, semis far exceed their 2000 technology bubble peak weighting. Whatever means investors use to rationalise today’s semiconductors mania, the free market always has a solution to over-investment. A weakening economy could soon put the kibosh on grandiose data centre construction plans and lead to the post-bubble scenario of cancelled semiconductor orders. Semiconductor stocks remain a top model sell/short/underperform recommendation.

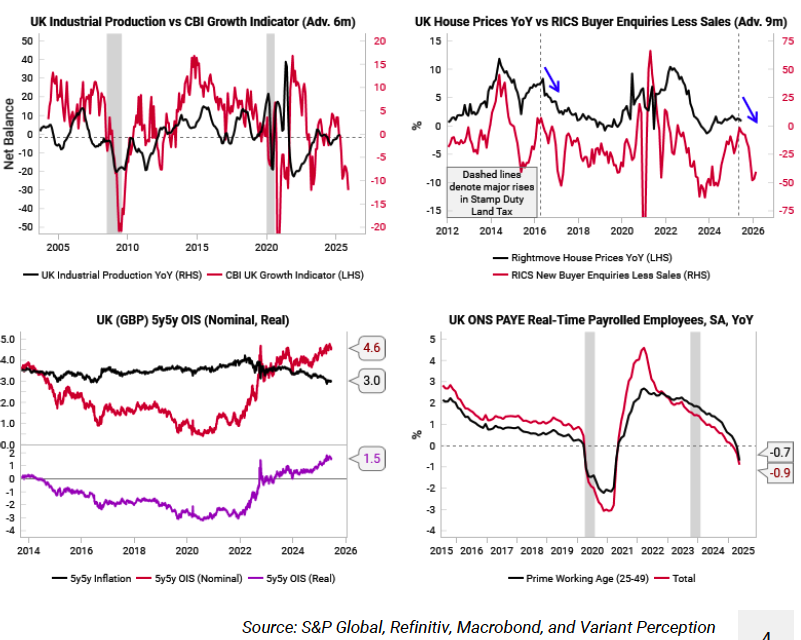

Recession risks mount in the UK

Variant Perception’s growth LEI is turning lower and the CBI Growth Indicator is at lows only seen in prior recessions (top left chart). UK real yields are still too high given signs of housing weakness and other downside risks to growth. The team’s proxy for the neutral rate – 5y5y “real” OIS – is now the highest level in at least a decade (bottom left). Slowing activity and the latest employment tax hikes are already leading to YoY payroll losses in UK ONS data (bottom right), echoing the latest rise in the unemployment rate and company insolvencies. Recession risk is highest in the UK among DM economies. The team expect lower gilt yields and remain short GBP vs long JPY in anticipation of the BoE turning more dovish as growth risks outweigh concerns about still-high inflation.

Germany: Budget does little for structural growth

Germany’s 2026 budget will raise debt-to-GDP from 60-80%, leaving little to no fiscal space for new European debt programmes. Wolfgang Munchau notes that it won’t affect Germany’s fiscal stability in the short-run, but it removes Germany from its post-crisis role as the euro area’s fiscal anchor. He also thinks that the rise in deficits, which will be mirrored by other euro area countries, will drive up interest rates. Germany’s 2026 budget will undoubtedly lead to an increase in GDP growth from 2026 onwards – but Wolfgang sees little in the budget that could help raise structural growth. He says that Europeans should be focusing less on blunt numerical defence spending targets and more on what they're actually getting for their money.

US: Pressure on the Fed intensifies

Danielle DiMartino Booth notes that after a brief reprieve, the slowdown in the US industrial sector has been unrelenting into 2025. Global supply chain slack is deepening, which is manifest in the Philly Fed falling by the most in one month in its history since 1968, the pandemic notwithstanding. At a broader level, aside from a stock market rally that was the sole booster in May’s LEI, the drag via every other component took its diffusion index back to a recessionary reading. Sam’s Club temporarily reducing prices on more than 1,000 seasonal items to combat declining discretionary spending piles on to evidence of disinflationary pressures spreading across the US economy. Danielle says that the Fed’s stance was already out of touch with economic reality and looks to increasingly be intentionally destructive. She reiterates her conviction in a second-half 2025 bull steepener.

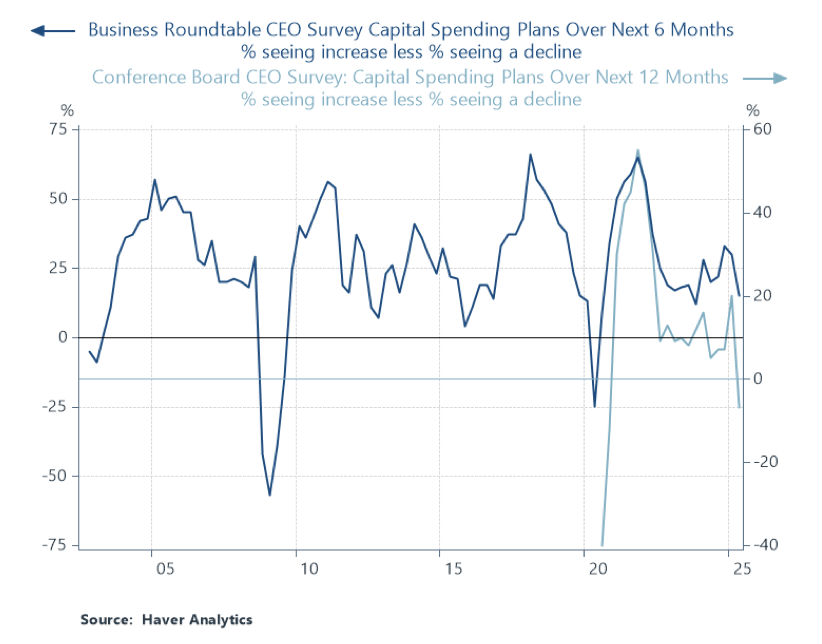

US capex outlook dimming

At the heart of business-cycle dynamics is fixed capital spending, heavily influenced by expectations and animal spirits. The uncertainty created by tariffs may be offset by AI, but the timeline for grand AI projects is unclear. Recent CEO surveys indicate that net hiring intentions have gone from a near-term high of +17% in the fourth quarter to -15% in the second quarter and capex intentions have fallen into negative territory in May and have edged lower this month. There has been a divergence between the hard and the soft economic data and the question is whether the former will follow the latter. While these series on capital spending and employment intentions do not have a long enough history to draw meaningful inferences, they suggest businesses are cautious about the outlook and caution can be a self-fulfilling prophecy.

US: TINA and Treasuries

Andrew Hunt asks: has EZ deficit obfuscation helped maintain US Economic Exceptionalism? He believes it has and that the hurdle for US balance of payments problems is in fact quite high. Unlike its peers, the US is an economy with a positive output gap, strong credit growth and it is experiencing above trend growth at present. The Fed’s current rate strategy is therefore right for the moment, but this strategy will not suit others. The crowded short USD position may not therefore work for a while… US households are long equities but a shift to a fully or overfunded budget deficit would ask questions of their current asset allocation. Ultimately, the outlook for markets rests on two questions: how will the US budget deficit be financed and can the news flow actually overwhelm the TINA effect and lead foreign investors to reduce their acquisitions of USD assets?

US S&P500: A change of view

When the early April tariffs were initially implemented, Adam Parker lowered his earnings estimates, taking the view that a year of growth was removed. With retrospect, Adam now thinks his initial reaction was too punitive, not only because some of the most potentially damaging comments from President Trump were not implemented, but also because of his updated view on some important profit-related dynamics. He is raising his earnings estimates, though he remains below the bottom-up consensus and now forecasts $255 in 2025 earnings, $273 in 2026 earnings and $295 in 2027 earnings. This represents a 3% increase for 2025 vs. his earlier view, but is 3.2% below consensus. Adam’s 2026 and 2027 estimates are 9.2% and 10.6% below the consensus forecasts, respectively.

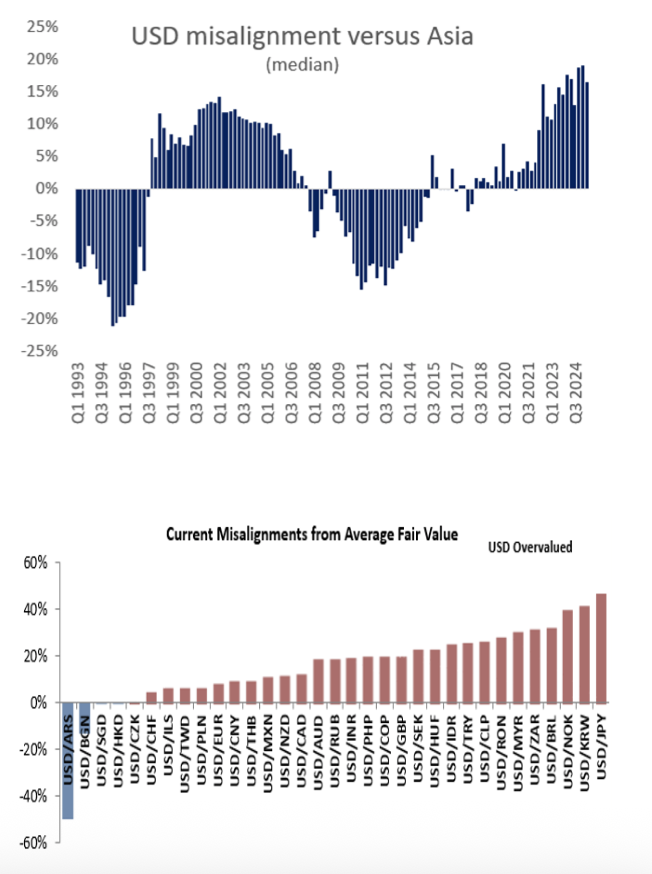

USD: Tumbling further

The USD has moved a long way since the Eurizon team’s early call for weakness, with the consensus U-turning on US exceptionalism. Still, the team see further to run. We are but at the start of a multi-year descent of the USD, a fall triggered by structural weakness in the currency. USD overvaluations are widespread but remain most acute in Asia, where years of CA surpluses have been recycled into USD-denominated investments, mostly unhedged. Investors are vulnerable to the sudden correction (‘avalanche’) in currency markets. A ‘Mar-a-Lago Accord’ will likely take the form of bilateral secret negotiations for the US’ trading partners to facilitate a dollar devaluation. China can and likely will accept a USDCNY near 5.5-6.0. Compared to the G10, the currency is overvalued by 13%, and investors can also expect EUR/USD and USD/JPY to trend towards 120.

Emerging Markets

Trade of the week: USD/MXN

The US strike on Iran has moved the market from a state of uncertainty about whether the US will strike to uncertainty about whether Iran will respond. The trend of reduced Iranian action suggests that their ability to do so is limited. As such the market may refocus on the July 9th deadlines and the slowdown in US data. David Woo sees these events as bearish for equities, although stocks are proving to be resilient, in large part due to retail buying. What may prove to be less resilient on this theme is MXN. Since 2nd April, MXN has traded broadly in line with the S&P but has seen a more significant reversal since Israel first attacked Iran. Unwinding of positions established since 2nd April could easily take USD/MXN to 20 in the short term. David sold the September MXN future at 0.05142. He’ll take profit on a move to 20 in USD/MXN and stop out at 18.90.

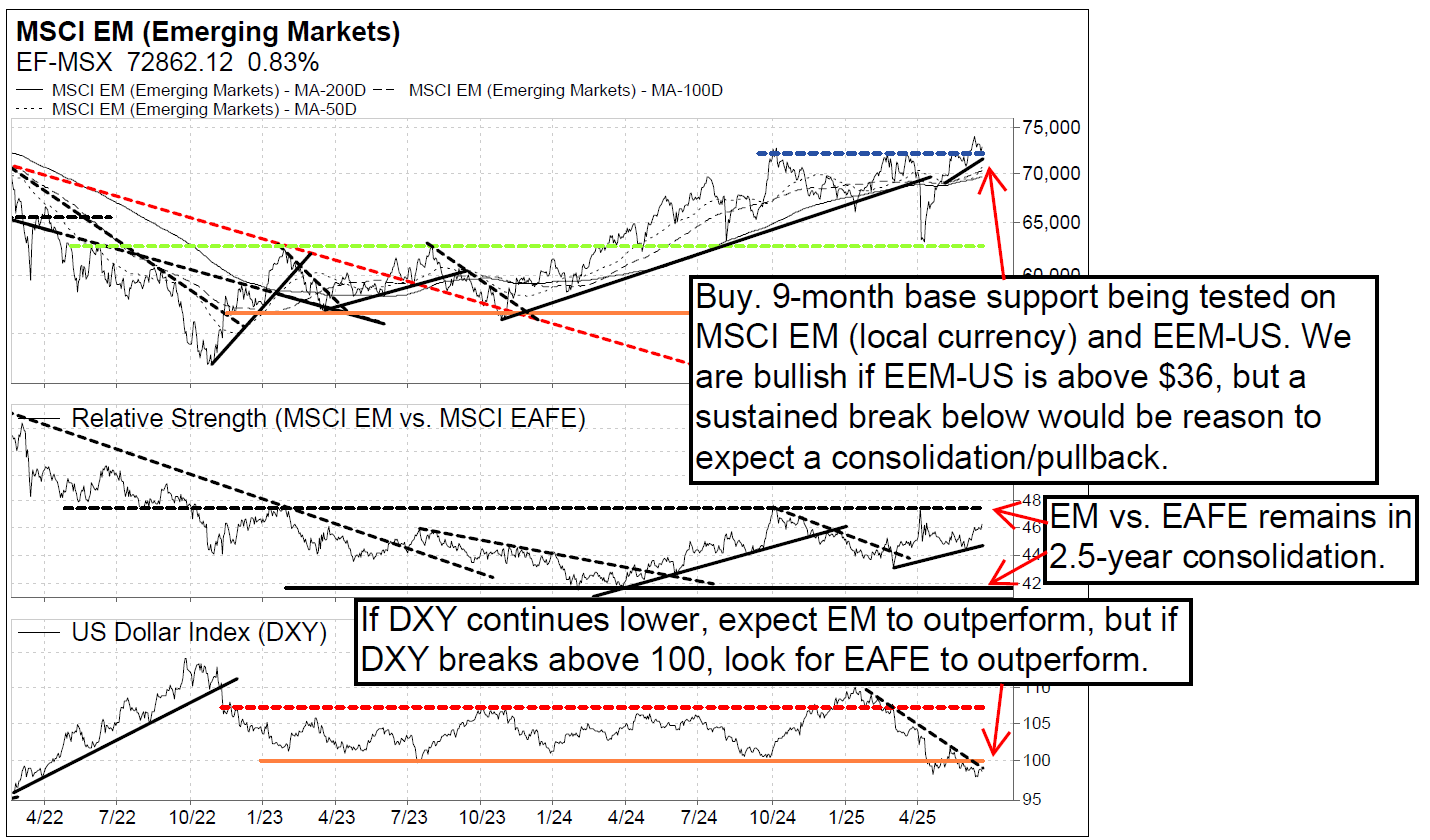

MSCI Emerging Markets: Testing base support

The MSCI Emerging Markets index (local currency) and EEM-US (USD) are holding above their respective base supports, including $46 on EEM-US. The Vermilion team are buyers as long as EEM-US is above $46, but a breakdown below it would indicate a bearish false breakout; if that were to happen, investors should become cautious and expect a pullback/consolidation. Their top EM picks are South Korea and Greece, and are bullish South Africa, Taiwan and Hungary. Defensive EM sectors (staples and utilities) continue to underperform and should be avoided, but the team expect outperformance from MSCI EM tech, energy, industrials, financials and comms.

Brazil: Maintain long equity exposure

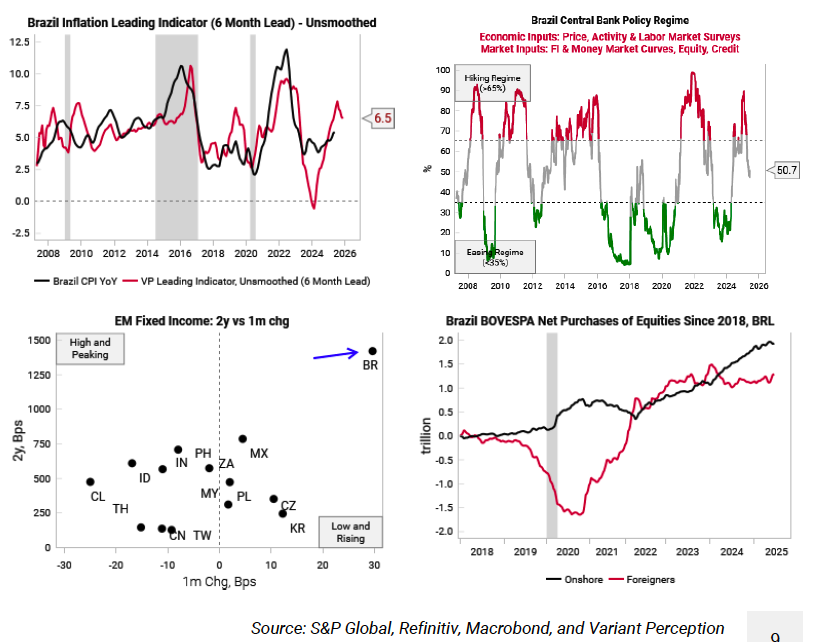

Variant Perception’s inflation leading indicator ticked down again this month, with the unsmoothed 6-month estimate falling to 6.5% YoY (top left chart). Underlying indicators confirm this inflection point, leaving the gap between the Selic rate and inflation the widest since 2005. Brazilian money market futures have also priced in the end of the hiking cycle. Echoing this, the team’s central bank regime model has shifted out of a “hawkish” regime and is now in neutral territory (top right). Meanwhile, the 2-year bond yield in Brazil remains elevated relative to all other EM economies (bottom left). The latest rise in yields over the past month or so is at odds with evidence inflation is rolling over. Investors can expect some lagged negative effects from the tightening cycle, but falling real interest rates are a strong macro setup for domestically-exposed Brazilian equities to move substantially higher from here.

What’s the matter with China’s consumers?

Yes, Trump’s tariffs are hurting China’s economy, but a bigger damper on GDP growth is anaemic consumer spending. China is experiencing deflation and exporting it to the rest of the world. President Xi has tried to revitalise the consumer sector with insufficient measures that don’t get at the root of the problem: Chinese consumers are saving rather than spending because there’s no social safety net, with 61.4% of mainlanders preferring to stuff their mattresses. Moreover, consumer confidence is weak owing to slow wage growth and the property crisis, and Ed Yardeni points out that there’s no signs of improvement. What needs to be done is no secret: the IMF has outlined the ambitious but feasible reforms it would take to revive China’s consumer sector sustainably. Yet, as Trump does his worst to hobble China’s economy, President Xi may be beating him to the punch.

Rhythms of Latin America

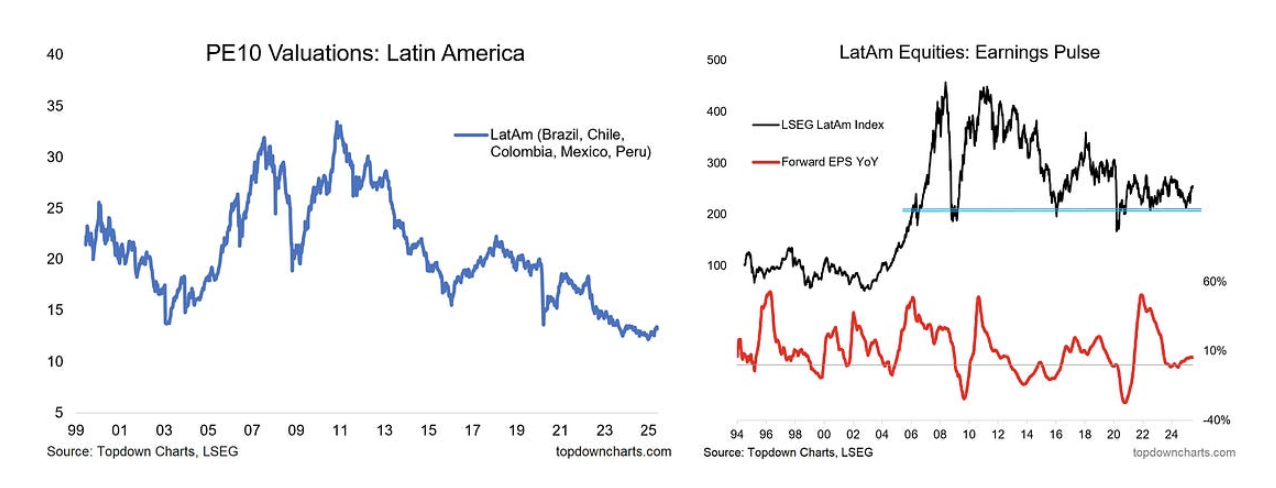

Latin American equities are looking good as the initial rally off long-term support has stuck, positioning has turned up from 10-year lows, earnings revisions momentum moves higher after a big reset and monetary policy overall pulls back from previous shock tightening. By itself this all looks great and Callum Thomas mentions that this is all against a backdrop of extremely cheap equity valuations too (taking an equal weight across Brazil, Chile, Colombia, Mexico, Peru). There’s also extreme cheap FX valuations – which is helpful for LatAm equity returns in USD terms (all-else-equal, a weaker dollar vs stronger LatAm currencies will boost USD returns and likely trigger further performance chasing inflows and easier financial conditions). Remain bullish LatAm equities.

Argentina: Three scenarios for FX and inflation

Inflation in May was below expectations again and core price inflation decelerated. Inflation was 1.5% MoM. Inflation in June will be in the vicinity of 2% MoM, according to Marcos Buscaglia’s estimates. As a result, national inflation may drop below 40% YoY for the first time since March 2021. The government is prioritising the reduction of inflation over other objectives such as the purchase of reserves. With this in mind, Marcos lays out three scenarios for the FX and inflation until yearend. In the baseline scenario (50% probability), the peso weakens but remains inside the target band, in the risk scenario (20% with upside risks) it jumps to the top of the band, and in the government-preferred one (30% with downside risks) it weakens very mildly. In the baseline scenario, inflation remains contained at or below 2.5% MoM, but it stops declining, ending 2025 near 32%.

UAE: The equity market has broken out

Over the past few quarters UAE stock prices have broken the link with crude oil prices and started to rise in line with local bank lending and balance sheet growth - in turn a reflection of strong macro conditions. Jonathan Anderson says there's no guarantee that market outperformance will continue, but he’s clear that this is not a macro bubble a la 2008. The economy has deleveraged dramatically, banks have no funding pressures to speak of and the local property upturn is still in the early stages. As a result, Jonathan is happy to hold the market going forward.

Commodities

Uranium: Glowing again

Uranium (USD75.90) looks to be resuming its secular advance, following a 40% decline in 2024–25. In 2007–16, the market halved three times from the 148.00 peak, the classic signature of the very worst bear markets in equities and also sometimes commodities. Behavioural stuff, remarks Chris Roberts! Indicators at the 2025 low bottomed at higher levels than seen during the 2007–16 Secular Decline, which is what Chris would expect to see in a cyclical bear market. He is alert for a buy setup. One potential way to gain exposure is through Yellow Cake, which Chris is closely monitoring for a buy signal.

Crypto: Feeling stressed

While Bitcoin dominance has surged to a new cycle high, two critical indicators are flashing early signs of broader market stress. Ethereum, once riding a wave of ETF optimism, is now unravelling under the weight of overleveraged futures positions (see chart). Meanwhile, (market-based) liquidity, a silent driver of every rally, has quietly started to dry up. Even stablecoin flows, often overlooked, are painting a telling picture as the summer nears. Some of the market’s biggest buyers are pulling back and key technical levels are now being tested. What’s driving this stall—and what happens if support doesn’t hold? As anticipated, both Bitcoin and Ethereum are undergoing corrections, with each signalling a shift from bullish to bearish trends.

Iran jolts the oil markets

Tensions in the region surged again after the US hit Iran’s three main nuclear sites. Front-month August ICE Brent futures contract settled at $77.10/barrel on Friday, just $1.75 off Thursday’s five-month high. Vandana Hari sees the potential for a surge towards or above $80 in a knee-jerk rush of buying, but expects a swift pullback from these initial peaks. She stresses the importance of distinguishing between rhetorical threats and actual escalatory intent on Iran’s part, and does not see wider Iranian escalation, including a blockade of the Strait of Hormuz. Resuming nuclear negotiations will partially unwind crude’s current $12-14/barrel risk premium that is in place due to the risk of Israel-Iran aerial exchanges.