Europe

Is it finally time to buy Cyclicals?

At a time when economists are slashing year-end targets for major equity indices, star asset managers are forecasting the dollar’s demise, the collapse of the US economy and gold prices surging further, the real story has already begun and it’s the exact opposite. Recent sector rotation suggests markets are anticipating a brief global GDP contraction, followed by a rapid and robust rebound. Q1 results in Europe are strong. Companies are quickly adjusting supply chains to outmanoeuvre Trump’s tariffs. By early Jun, the tariff story will be old news and business will be almost back to normal. Stop overthinking and trust corporate agility. The real opportunity is in quality cyclicals - cash-rich, order-heavy, sector-dominating companies with rock-solid fundamentals. AIR’s top picks include Airbus, ASM International, Renault, Rexel, Schneider and Vestas Wind.

Communications

Following publication of its FY24 annual report, Iron Blue increases their WPP score by 3pts to 30/60 (now top decile; fertile grounds for shorting). This reflects: 1) Higher stripped out costs (41% of PBT adj vs. 30% in FY23). 2) Re-expansion of the gap between accrued income and deferred income after narrowing the previous two years. 3) Another fall in balance sheet bad debtor impairment provisions. 4) Compression of trade receivables. 5) Reduced disclosures in several areas following change of auditor. 6) Moderated CEO LTIP ROCE and FCF targets.

Financials

Fighting Financials reinitiates coverage of BG with a Buy rating, after first recommending the bank at €66 in Jul 24 and removing it from their active buy list at €98 in Mar 25. They highlight a supportive macro backdrop for NIM-sensitive banks, with sticky inflation and low unemployment in Europe. While BG stands out for the fundamental quality of its business and undemanding consensus expectations. Key risks include potential Austrian bank taxes and legal challenges over retail processing fees. Nevertheless, BG is one of the best positioned names to navigate said challenges given its high level of profitability and substantial excess capital (>6% of the group’s m/cap is available for M&A or special dividends / buybacks).

Materials

Activist investor Jeff Ubben, founder of Inclusive Capital, has urged CRBN’s board to hire external advisors to reassess its strategy, suggesting a split of its health and nutrition division. Analysts at the IDEA! reiterate their positive stance on the stock, with CRBN having made a strong start to 2025 and they believe the company is entering a period of solid growth with improved profitability. In combination with limited capital investments, a considerable improvement in FCF is anticipated. Tariffs are factored into 2025 guidance and are expected to have a relatively small, direct net-impact.

North America

“Baby With The Bathwater” Idea Forum

Given the sharp shift toward macro dynamics, MYST hosted a generalist idea event to identify companies that have been overly penalised amid the recent downturn. All but one of the participants felt the market may hit new lows (S&P 500 ~4,500) as consensus earnings estimates are likely too high. While most of the stocks presented were not far from their 52-week (or much longer) lows, participants highlighted companies with underappreciated earnings resilience (Byrna Technologies, CCC Intelligent Solutions, Six Flags, IMAX, Nvidia) and businesses misperceived as Trump tariff / DOGE losers (Aptiv, KBR, SharkNinja). However, the stock offering the biggest upside (100%+) was Chart Industries (LNG export policy beneficiary with rising recurring revenue / improving leverage profile).

“Hidden” Balance Sheet Shorts

High and volatile inflation, historically, means wider swings in corporate profit margins. Uncertainty rises, companies stockpile more inventory, COGS is more volatile and difficult to manage. We saw this in the 1970s “stagflation”. US corporates are sitting on historically high profit margins today. Will that last? If it doesn’t, one potential source of short ideas are companies that have levered up their balance sheets against unsustainably high profit margins. These stocks wouldn’t look highly levered on a ND/EBITDA basis, but if profit margins start to revert lower, “normalised” leverage might be much higher than investors realise. Names of potential interest using OWS's short screener tool include Constellation Brands, Lincoln Electric, Parker-Hannifin, TransDigm and Union Pacific.

AI driven 10Q / 10K text analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) AZZ - extension of credit to larger customers. 2) Constellation Brands - competitive pricing pressure. 3) DR Horton - changing long term expectation on debt to total capital ratio. 4) Moog - changing order demand in simulation and test products. 5) T-Mobile US - acquisitions of business with international exposure. 6) TriNet - change in stock repurchase expectations.

Communications

New CEO Spencer Rascoff is a high-capacity multi-tasker primed to rebuild consumer trust and female engagement. He served as CEO of Zillow from 2010-2020, scaling the business into the leading US online real estate platform. While not a product visionary himself, he is a detail oriented entrepreneurial risk taker who will inculcate a faster paced culture of innovation at MTCH. Rascoff has a knack for emphasising authentic user experience over monetisation (short-term) with an eye towards building a more trusted relationship with customers. Paragon’s analysis includes interviews with 7 former senior executives who worked with Rascoff for more than 85 years combined.

Communications

META is doubling down on AI infrastructure, raising its 2025 capex forecast to $64–72bn as it accelerates data centre construction amid rising costs. CEO Mark Zuckerberg is committed to making META a leading AI platform and insists on building in-house capacity to avoid reliance on others. While the AI strategy (centred on open source) is progressing well, it comes with a steep price tag, notably the ongoing $4bn+ quarterly burn at Reality Labs. Richard Windsor sees a growing risk of AI infrastructure overbuild, with META, Google, Microsoft and Amazon all ramping up spend - setting the stage for a painful correction. Despite this, META’s core business remains solid, with strong Q1 performance and improved operational efficiency via AI. At 23.5x FY25 PER, META is reasonably valued, but Richard prefers Google, where AI disruption risks from players like OpenAI are, in his view, overstated.

Consumer Discretionary

Northcoast’s latest Auto Parts Price Tracker shows that AZO has taken significantly more aggressive pricing actions than its competitors. By raising prices earlier, AZO may be positioning itself to absorb future tariff-related costs more effectively, limiting the impact on its margins over time. In contrast, AAP does not appear to be taking full advantage of this pricing environment. Not only has it refrained from meaningfully increasing prices, but it has also decreased prices in some categories, despite macro conditions that would typically encourage companies to maintain or raise prices. Northcoast believes this reflects the company’s ongoing struggle to better align its purchasing and pricing strategies. This cautious approach may be limiting its ability to expand margins at a time when passing through higher costs could be both justified and beneficial to the bottom line.

Consumer Staples

Scott Mushkin upgrades UNFI to Buy with a $38 target (40% upside), citing its strong position in the healthy eating trend. He expects revenue to outperform management’s conservative guidance, fuelled by robust store growth at Amazon’s Whole Foods banner, UNFI’s largest customer. Margin expansion should come from the group's adoption of Lean Operation Management - boosting FCF, reducing debt and enabling future buybacks. Assuming a 55% natural/organic sales mix by FY28, EBITDA margins could surpass 2.3%, with earnings exceeding $4 per share. The stock currently trades at a ~12x PE, 5.5x EV/EBITDA on FY26 estimates. If Scott’s projections around growth and margins verify, not only will the company see better than estimated earnings growth, but valuation multiples will increase.

Canadian Banks: Preparing for higher PCLs

Financials

Shalabh Garg attempts to quantify the performing loan provisions that Canadian banks might build over the coming quarters. He uses the banks' response to macroeconomic uncertainty in the early days of the pandemic as a reference point for provisioning built through the reclassification of some Stage 1 loans to Stage 2 under IFRS 9 and an increase in the allowances for credit losses ratio for both Stage 1 and 2 loans. Shalabh believes RBC and TD, followed by Scotiabank and CIBC, will likely undertake substantial performing provisions for credit losses over the coming quarters if trade policy uncertainty persists. He does not expect impaired PCLs to spike in the near term, unless economic conditions deteriorate materially and drive the unemployment rate higher. He believes valuations will come under further pressure only when impaired PCLs ramp up.

A factor model mystery!

Healthcare

Major Pharma and Biotech are surprising inclusions in the top 5 ranked sectors in YWR’s Global Factor Model, which ranks 3,000+ stocks on earnings momentum, valuation and price momentum. In his latest piece, Erik@YWR looks at why these two sectors have started scoring well this year. While valuation and FDA reform explain some sentiment shifts, the real driver appears to be surging prescription volumes in mid-cap firms targeting rare diseases. Deeper analysis links this to a little-discussed Medicare change under the Inflation Reduction Act: a $2,000 annual cap on out-of-pocket drug costs starting in 2025. This structural policy shift has quietly boosted earnings estimates across the space. And the good part is nobody has picked up on this, so the trend will likely continue.

Industrials

AAL reported a disappointing Q1, with modest improvements in unit revenue and load factor offset by poor cost control (especially relative to Delta and United). Despite benefitting from lower fuel prices, AAL failed to retain related savings. Cash conversion deteriorated and over the last 12 months, adjusted OCF is ~33% below 2019 levels (the weakest among the Big Three). Leverage also remains substantially higher than peers. Reno Bianchi forecasts Q2 EBITDA of ~$1.6bn, below consensus estimates. Given increasing macro risk, he believes AAL's credit profile is looking increasingly fragile. Reno continues to recommend avoiding the group's equity and unsecured debt, while the current spread premium among AAL’s long-dated secured obligations is too tight. Investors should focus exclusively among some of the airline’s short-dated, well secured structures.

Materials

Frank Mitsch applauds the action to delay the Ft. Saskatchewan Path2Zero project, which is resulting in an additional $600m in capex savings during 2025. And combined with the Macquarie infrastructure sale(s) and anticipated NOVA litigation proceeds, suggests concerns over dividend sustainability in 2025/26 should diminish. Despite weak sentiment, heavy short interest and near-term pressures (up to $1bn FCF outflow in 1H25), he expects improvement in 2H25 as working capital normalises, maintenance spending falls and new projects ramp up. Trading at ~9.4x EBITDA with a ~9.5% dividend yield and shares back at Covid lows, Frank sees an attractive mid- to long-term risk/reward and upgrades the stock to Buy.

Technology

Kinngai Chan believes STX's HAMR technology HDD will drive further upside to its gross margin into 2H25. Industry checks indicate the current favourable pricing environment and product mix will continue. The company’s HAMR technology will not only allow it to increase its HDD capacity points but will also drive higher ASP and serve as a cost reduction for its mid-to-lower capacity HDDs. While Kinngai understands investor concerns about possible customer pull-ins and the future impact of tariffs on industry demand, he thinks any demand slowdown would be manageable for the storage market and STX. He expects STX will drive its corporate margin to the high-30% range as its HAMR-based HDD ramps through 2H25 and into 2026.

Developed Markets

Narrowing the focus

Although peak uncertainty has passed, risks have not disappeared and the Variant Perception team are narrowing their focus to either extreme market dislocations or seeking out assets they want to own on a 2-3 year time horizon. They still like their long Indian equities trade as the first sign of foreigner inflows starts to resume. They also like JYP 10s30s flatteners as the curve has seen a major price dislocation during the past month. In FX, long ZAR remains their preferred high carry short USD expression, with the rally in gold improving the ZAR’s terms of trade (see chart). The team’s medium-term leading indicator for volatility remains elevated, but they are waiting for market pricing to become more favourable for long vol trades.

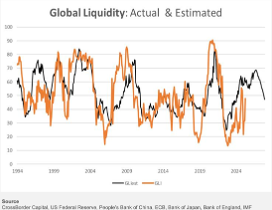

Liquidity taps

The rapidly deteriorating path of the world economy is likely to spur renewed policy ease among world central banks, and the sharp rallies in gold and Bitcoin – two highly liquidity-sensitive assets – have spurred hopes of rising global liquidity. Already, the PBoC has opened the Chinese liquidity taps. This backdrop persuades Michael Howell that the long-slated late-2025 peak in global liquidity will be quickly offset and pushed back into mid-2026. A pending recession makes him reluctant to move back into risk markets yet, even though some rebound looks deserved. Nonetheless, the likely inevitable policy response of more liquidity is a great future omen. It establishes the upward path of persistent monetary inflation that ultimately underpins the value of hedges such as gold, quality equities, prime residential real estate and Bitcoin.

Tariffs vs deficits, hope vs fear

There is no discussion about fiscal policy yet in markets, with Manoj Pradhan claiming that investors have a small window where stagflation concerns vs hopes of tariff de-escalation will dominate market pricing. However, once the discussion of deficits enters the picture, these trades (particularly receiving bonds) will no longer be valid. The window between the two could be as little as three months! To take advantage of the small window between tariffs and deficits, Manoj recommends long Chinese equities and MDAX (to hedge for the possibility of de-escalation), and long MXN/CHF and EMFX vs USD as de-escalation trades. To trade for slowing growth, opt for long US 10y and 30y bonds, full house South Africa incl 10y bonds, and Japan 10y, and receive 2y UK, Euro area, India and Mexico.

UK: GBP testing resistance

The British pound is testing resistance at £1.3125-1.3434 at the top end of a 21-month rectangle pattern. A breakout from the range would have a measured move target of £1.4800+. But Chris Roberts would focus on another test of the £1.4000+ zone, a barrier for almost 9-years. That important £1.4000+ zone must be conquered for a long-term bullish view on Sterling (which would target £1.7000+). The 14-week RSI has reached 68, just below Overbought 70. This may mean some consolidation will occur here. Chris continues to monitor for trade setups.

US: The art of (tariff) war

Donald Trump agreed not to impose a double tariff on foreign car makers. Even so, the US tariff policies will constitute a serious hit for European car makers, and will accelerate their plans to invest in the US. Wolfgang Münchau argues one reason why the US is likely to prevail with its policy shift is the rest of the world's dependence on the US treasury market, which is difficult for the rest of the world to disentangle itself from. There is enough flexibility for investors to rebalance their portfolios away from US overweight to US neutral, but China cannot diversify away from US Treasuries overnight; they have no other currency to diversify into. The euro area does not have a euro bond, and the supply of German debt securities is severely limited. The UK, Australia and Switzerland are far too small to absorb any deluge of outflows away from the US.

How I learned to stop worrying and love the bond

Patrick Perret-Green highlights that while short-end interest rates are now priced close to their lows, 1y1y USD OIS at 2.98% and 2-year yields at 3.59%, the real divergence lies in long-end bonds. Yield curves are steep, with long bonds pricing in long-term fiscal strain, inflation risks, and geopolitical uncertainty, in stark contrast to the recessionary tone of the short end. This "great steepening" now feels stretched. Investors may want to fade long-end pessimism, especially given unsustainable long-term bond yields from a fiscal standpoint. Long-duration shorts may be vulnerable. Patrick questions whether central banks have sufficient oil in the engine to cushion a disinflationary global economy. Investors should consider being flat or cautiously short long bonds, take profits on short-end receive positions, and prepare for future central bank intervention. The Trump effect may further disrupt markets, but the time may be right to stop worrying and love the bond.

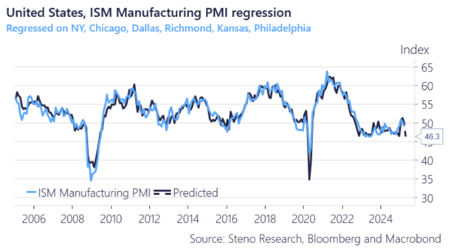

US: The ISM manufacturing playbook

Markets remain too complacent about the risk of weakening US manufacturing, with key assets still priced for a rebound rather than a slowdown. If ISM Manufacturing lowers to 46, investors should consider tactical short positions in the most misaligned assets. These include US Financials, Tech, and Communication Services - high-beta sectors still priced for strong growth. China and Germany also stand out, with massive valuation spreads versus their ISM sensitivity, making them vulnerable in a downturn. In FX, precious metals like Gold and Silver are sharply out of sync with ISM trends, while SEKUSD and AUDUSD look similarly overextended. Conversely, Energy stocks appear to have already priced in manufacturing softness, offering relative safety. Brazil, USDJPY and Turkey also offer more protection if growth continues to decelerate.

US: The next credit cycle problem

Charles Peabody has received considerable feedback on his recent piece on “Parallels with the Panic of 1907”. When asked why he firmly believes that private capital (private equity and private credit) will house the epicentre of the next credit cycle his answer is quite simple. To paraphrase Willie Sutton – “Because that’s where the money went”. When the Fed grew its balance sheet from less than $1 trillion to over $4T following the GFC, Dodd-Frank imposed constraints and massive capital requirements on the banks. When the Fed balance sheet doubled again to $9T following Covid, private capital continued to benefit during the lowest interest rate cycle in history. The economic dislocation from Liberation Day tariffs in 2025 can be equivalent to the San Francisco earthquake and fire that led to the failure of the Knickerbocker Trust in 1907.

Emerging Markets

The systemic risk in China’s SME boom

SME credit continues to expand at a blistering pace, with loans approaching 60% of GDP, much higher than the pre-Covid level of 37% in 2019. That’s bigger than real estate developer and LGFV loans combined. Average SME loan rates have fallen, with many banks offering rates below that of mortgage loans. What was once the highest-risk, highest-yield segment in bank portfolios is now priced among the lowest risk. The SME bad loan recognition moratorium was confirmed in 2024 to be formal policy, with banks expected to maintain loan rollovers and refrain from downgrading troubled SME credit. “Extend and pretend”. Lessons from around the region suggests this will end badly. China's moratorium, now in its fifth year, is longer and larger than that of any other country. The longer it lasts, the greater the underlying risk…

China: Tariff pressures

Horizon Insights interviewed 37 export-oriented enterprises including those specialising in consumer goods, machinery, photovoltaics, batteries and automotives. 62% reported a y-o-y improvement in export orders during March-April 2025, but sentiment around second-quarter order intake has softened notably. Several have reported a decline in direct export orders to the US, with some reporting shipment suspensions. Some enterprises have adopted inventory stockpiling strategies to mitigate the near-term impact of tariffs, with current inventory levels expected to sustain operations for 2-5 months, although pressures are likely to emerge beginning in Q3. Beyond North America—where tariffs and softer demand are evident—and Russia, which is experiencing elevated inventory levels and weaker demand, Southeast Asia has seen a rise in transshipment trade. Meanwhile, robust demand for construction machinery and automobiles persists in emerging markets such as Africa, the Middle East, and Latin America.

Is India now an attractive defensive market?

Jonathan Anderson poses the question: “Is India is now an attractive defensive market?” However, he says that the answer depends on what you mean by "defensive". On the one hand, the good news is that India is far more domestically oriented than other regional players (ex-China), and the economy is still growing at a respectable 4% to 5% pace. But on the other hand, the bad news is that the market is still expensively priced even after the recent retrenchment, and the rupee is not immune to global trends given India's external deficit position. Jonathan concludes that in a "hard" US recession scenario he would be more inclined to take respite in India. In the current environment, however, he still finds other domestic- and external-led stories more appealing at the margin.

Russia: What the future holds

Chris Weafer monitors four possible scenarios covering geopolitics and the conflict and what each may mean for a peace process and sanctions. Chris also considers the implications of each on the economy, the ruble, the business environment and the return to Russia of foreign investors and companies. Chris’s base-case (50% probability) is based on peace talks starting in the summer and concluding by year-end or in 1Q26. In such an event, he sees Ruble-US$ rate trading in the 85-90 range in Q2/2025, moving to 90-95 in H2/2025. Sanctions against MOEX are removed by year end, but the CBR will stick with the OTC rate setting. The slower-engagement scenario (40% probability) assumes a break in Russia-US talks and some additional sanctions applied to Russia, with the process dragging into mid-2026. In this case, expect R/$ to trade in the 95-100 range until year end, rallying to 90-95 in H1/2026.

Turkey: Simsek reaffirms commitment to inflation fight

Report by

Burumcekci Research & Consulting

Treasury and Finance Minister Mehmet Simsek reaffirmed strong political backing for his economic programme, emphasising inflation reduction as the top priority. In an interview, he acknowledged the global slowdown and tighter domestic financial conditions but insisted Turkey remains resilient due to its investment-driven, domestically focused growth model. Simsek downplayed concerns over capital outflows, noting household confidence in the programme and that reserves, though hit, remain adequate. He ruled out any programme changes, maintaining a 24% inflation target and projecting a current account deficit well below 2% of GDP, potentially narrowing further if oil prices and the euro/dollar rate move favourably. Simsek pledged continued fiscal discipline and investment incentives, signalling confidence in medium-term stability. “There is no question mark over the programme,” he said, suggesting that market credibility is returning. Investors, he implied, should see Turkey as positioned for long-term strength once global volatility subsides.

Commodities

Bitcoin: A smash move is coming

According to Markus Thielen, Bitcoin’s market structure, liquidity signals, and technical momentum align for a move higher. With the macro backdrop stabilizing and money flows accelerating, he says that the stage is set for Bitcoin to break above $100,000 — potentially igniting a broader altcoin rally. Markus’ tactical altcoin outperformance indicator continues to favour Bitcoin, although a decline in dominance from 63.3% to 62.6% would trigger a shift in favour of altcoins. Last week his "Bitcoin/SP500: Pay-to-Play Is Back" report highlighted his strategy of buying the $100,000 June calls while selling the $110,000 June calls — a view Markus is growing increasingly confident in as liquidity conditions continue to strengthen and a move above $100,000 appears likely.

China: Nerves of steel

Markets are again speculating that China will cut steel production by 50m tonnes, with traders responding by shorting raw materials and adding long exposure to steel products. There is credibility to the statement, including that NBS revised down crude steel production after being investigated by the government in January. However, William Hess stands by his statement that a 50m cut is unlikely to happen. That said, he thinks a demand air pocket resulting from stimulus and tariff uncertainty will dominate steel production cut narratives before the start of the winter heating season, posing significant downside risk for iron ore. Another policy consideration is the increasing resistance to elevated exports of cheap Chinese steel products in other major economies (ex-US), which remains a risk to current demand forecasts even if no tariffs have yet been placed on Chinese steel.

Hydrogen, it’s a gas gas gas…

Japan’s commitment to hydrogen is gaining renewed attention. As the country’s multi-decade pursuit of a hydrogen society begins to show signs of commercial viability, Neil Newman explores the path ahead and the firms that may be poised to benefit. Among potential exposures is

Chiyoda Corp,

whose SPERA Hydrogen technology enables the stable, long-distance transport of hydrogen via liquid organic carriers.

Iwatani Corp,

Japan’s dominant hydrogen distributor, is another key player. Although rising demand has driven local hydrogen prices as high as ¥1,650 per kg, the firm sees potential for a 77 per cent price reduction through scaling and improved electrolyser deployment.

Panasonic

also stands to benefit through its Ene-Farm residential fuel cell system, over 500,000 of which have already been installed. As Japan develops global hydrogen supply partnerships, accelerates cost reduction, expands into transport and shipping, and leads the way in global standards, investors should watch closely.

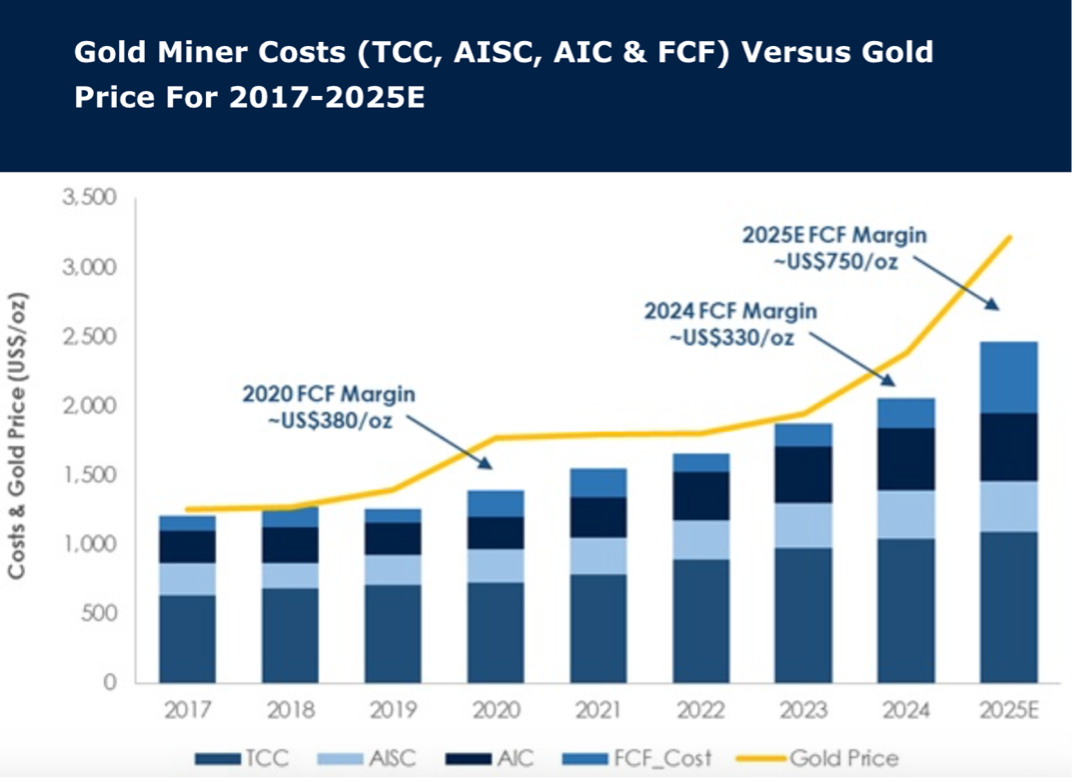

Gold: Higher prices, higher costs

As markets focus on record spot prices in 2025, price-linked costs and general mining inflation are also driving operating costs to record highs. In 2025 gold miner FCF costs are expected to reach a record ~US$2,465/oz, in line with inflation expectations. Positively, gold prices are rising faster and the 2025E FCF spot margin at ~US$750/oz is near double the last high in 2020. Gold miners (covered by Global Mining Research) with the lowest FCF costs in 2025 are

Lundin Gold,

Wesdome,

Kinross and

Agnico.

Stocks with improvement in FCF costs from 2024 to 2025 are

IAMGOLD,

Torex and

Equinox.

Preferred gold stocks are BUY-rated

Agnico (delivery and lower-risk portfolio),

Kinross (risk reduction and execution),

Equinox (transitions from project development to cash generation),

IAMGOLD (Côté ramp up and derisking) and

Lundin Gold (FDN continues to outperform).