Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

UBS Group (UBSG SW) Switzerland

Pierre-Olivier Essig believes Switzerland is too small for UBS and now is the ideal time for the bank to split into 3 separate entities: 1) Swiss Retail Bank - to be renamed SBS (Societe de Banque Suisse) and HQ / listed in Zurich. 2) Wealth Management Bank - would keep the UBS label; HQ / listed in London and could extract massive incentives from Rachel Reeves. 3) Investment Bank - rebranded SG Warburg; HQ / listed in New York, enabling it to compete on the same level as US peers; perfect timing given Trump’s promise to cut regulation. UBS shareholders would win from the SOTP and employees would gain from the split. Regulators would be relaxed, with each of the 3 new entities under the supervision of a different jurisdiction.

IMI (IMI LN) UK

Iron Blue initiates coverage on IMI with a score of 26/60, which is top quartile and fertile grounds for shorting. They highlight: 1) Dependence on December revenue recognition. 2) Sustained and elevated stripped out restructuring expense (11% of FY23 PBT adj) & associated use of provisions accounting. 3) Stripped out acquisition software and R&D amortisation (3% FY23 PBT adj). 4) P&L inventories impairment expense reduced to 0% of FY23 PBT adj from 5% in FY20. Iron Blue also notes an internal succession approach for the CEO/CFO roles, sub-optimal controls and many disclosure gaps.

Is the diversified model dead?

GMR recently published a review of the leading mining stocks’ performance over the last five years. For the diversified miners this highlighted weak TSR and overall negative returns stripping out cash payouts. A critical issue facing the group, especially the iron ore-dominated miners, is how to restructure their portfolios for the long-term. GMR reviews six key questions: 1) Is the diversified model dead? 2) Can dividends be sustained? 3) Miners exited coal but should it have been iron ore? 4) Shrinking to greatness might have merit? 5) How to increase EV materials exposure & in which commodity? 6) Is M&A the answer? BHP is their preferred pick, with Glencore second. Vale is very cheap, but it is hard to see a catalyst.

ASML (ASML NA) Netherlands

Kinngai Chan argues that most of the risk for FY25 such as slower than expected demand recovery and expanded export restriction into China have been priced into the stock. He expects the demand for ASML's EUV lithography tools to recover and accelerate through 2025 as he sees higher performance requirements for AI-related applications in both the datacentre infrastructure as well as endpoints products. While there remains some uncertainty about the growth of AI-infrastructure capex in the near-to-medium term due to the discovery of new more efficient LLM model algorithms, Kinngai thinks the AI adoption in the client devices could easily offset the possible weaker WFE spend for infrastructure.

Mid Cap Tech Stocks: Expectations analysis

Revisions across Hardware, Semis and Telco Equipment stocks are poor and getting worse. The median move in consensus Y2 EBIT over the last 3 months is now a cut of 6.0%. There is a wide range of expectations, but median consensus Y3 revenue growth is a remarkable 13% and there are stocks that look to be decent growth and serious value. SeSa stands out. The stock could treble. Meanwhile, Internet and IT Services is the low growth piece of Willis Welby’s Tech coverage. Consensus Y3 revenue growth is only 6.0%, but the median implied to Y3 EBITM ratio is just 49 and revisions remain positive. Indra Sistemas looks interesting. Trading has been good. There is potentially a massive transformation. Finances are strong and the implied to Y3 EBITM ratio means they can see upside of over 100%.

North America

What’s the right beta for your portfolio?

Trivariate analysed the top 500 US equities for five factors beyond the market: size (top 100 vs. 401-500), growth vs. value, high-quality vs. junk, liquidity and momentum. They focused on 3 different portfolios (min-vol, max-Sharpe, max-return) to show a range of outcomes. Over the last 20 years, the “efficient frontier” or optimal beta for a median portfolio appears to be between 0.95 and 1. If you are looking to lower your portfolio beta efficiently, owning high-quality value stocks with relatively low liquidity is a prudent strategy (e.g. Exxon Mobil, Philip Morris, Lowe’s, Medtronic). If you want to take more risk, the optimal factor loadings would be to add to highly liquid growth stocks that are junk quality (e.g. Tesla, Applovin, Micron).

Spin-Off Index up 15% YTD

The sum of the parts is greater than the whole - for over 25 years, Spin-Off Research has been the preeminent independent research service for tracking and analysing the US spin-off space by covering all transactions over $250m from announcement through distribution date and one-year post-completion. You can access the latest edition of their monthly publication by clicking here. This includes coverage of WH Group and Smithfield Foods; Lennar’s REIT spin-off; Aptiv’s tax-free spin-off of its electrical distribution systems business; and Galapagos’ plans to spin off its innovative medicines business.

Regardless of what one thought of FUBO and/or Hulu Live TV separately, the combination of the two - via a merger announced last month - is transformative. It will be the 6th largest pay TV video subscriber platform in the US. Increased scale and Disney’s heft in the marketplace should lead to improved content and distribution deals, bolstering the gross profit margin. Doug Arthur initiates with an Overweight rating and a TP of $6.00 (35% upside). His projected adj. EBITDA estimates are not as optimistic as FUBO’s management. However, he still envisions combined adj. EBITDA of $301m by 2027 and close to $400m by 2028.

Jeff Farmer sees additional beat and raise quarters coming with Chili's SSS and EPS momentum showing little if any signs of slowing. Q2 EPS of $2.80, materially outpaced the $1.80 Street estimate driven by stronger-than-expected Chili's SSS (+31.4%) and a better-than-expected RL margin (19.1%). Menu innovation & value in concert with highly effective traditional and social media messaging have combined to bring customers into Chili's, while investments in food quality, facility improvements and staffing, have kept customers coming back. Jeff’s FY25E EPS increases to $8.43, with EBITDA increasing to $710m and company SSS increasing to +20.1%.

Is 2025 the year NKE’s stock finally breaks back out? Analysts at The Retail Tracker think so. Although for the company to win it needs basketball to be trending again. While timing remains unclear, fashion shifts are turning in its favour. Certain styles are selling well and certain colours are selling out. The Dunk had some very good sellers, the Cortez has been highlighted as a fashion choice for 2025 by a few creators, the group has had some sell-out collaborations and the changes in management have been well received. The Jordan brands turns 40 this year and NKE plans for several drops including the OG Cement. Excitement will start brewing. Investors buying the stock at current levels will be well rewarded.

SAH features as one of the top short candidates in Two Rivers’ Declining Business Model. Sales fell -4.2% last quarter after declining for four quarters and slowing from a post-Covid surge. Sales per employee have rolled over. Gross margins have decreased with EBITDA margins following them down as well. Inventory days turnover has increased to 50 days from 30 days at the post-Covid bottom. Unlevered FCF is falling and has dropped below zero over the past year, on a TTM basis. Leverage has increased to 6.8x net debt to trailing EBITDA. At the last earnings release, the company missed expectations up and down the income statement. The stock trades at historically high multiples.

Despite the disappointing 3Q24 results that VITL reported in Nov 24, the stock has been on a tear the past two months as a severe resurgence in bird flu has driven egg prices to new record highs. Nonetheless, OWS finds increasing evidence their bear thesis is playing out as widely-followed Nielsen and Circana scanner data does not capture the full extent of VITL’s promotional activities. Additionally, while these data sources may present a rosy picture of VITL’s dollar market share, industry participants have repeatedly told OWS that more comprehensive and detailed data available from SPINS reveals steep declines in VITL’s volume market share. OWS considers the stock to be an extremely attractive risk-reward short at this time.

COIN and all other companies in crypto are a waste of time unless you are convinced that crypto itself will go mainstream. Robert Graham-Brown thinks it will, with utility technology waiting for its moment in the sun. His latest report includes key takeaways, such as stablecoins being very important for the likes of COIN and that AI agents and crypto were made for each other. With potentially clearer legislation on the way, especially from a Trump administration, alongside a growing appetite for crypto, Robert sees the likes of COIN being able to generate similar returns to owning crypto, with a potential upside of +55%.

Clinical Labs have been among the least attractive subgroups in Healthcare for a really long time, but fortunately for DGX, Tom Tobin thinks the US is entering a New American Medical Economy where prospects finally look attractive. With just a few weeks under their belt the incoming Trump Administration has been all shock and awe with a clear message that they are serious about reform. Tom sees DGX sustaining a reliably higher revenue and EBITDA growth rate leading to upside to both 2025 and 2026 forecasts, through a combination of excess volume, pricing, efficiency gains and M&A, resulting in a stock >$190.

Healthcare & Trade Tariffs: Rising costs, disrupted supply and industry response

The trade tariffs imposed by the Trump Administration are expected to raise healthcare costs, disrupt the supply chain and make care less affordable for patients. Companies are trying to mitigate these issues through initiatives such as on-shoring manufacturing and sourcing from unaffected countries; however, these measures face regulatory challenges and will require time to implement. Within the medical devices and hospital supply sector, the impact of these tariffs varies among companies. For instance, Johnson & Johnson, Medtronic and Intuitive Surgical have manufacturing exposure in China and Mexico, whereas Boston Scientific and Edwards Lifesciences do not. MedMine monitors spending on medical devices and hospital supplies at ~3,000 hospitals and related healthcare providers across the US, providing valuable insights into the effects of these tariffs.

Retail Real Estate outlook

Kolytics highlights the growing risks to the retail sector from geopolitical tensions, protectionism and declining consumer confidence, even as incomes remain stable and occupancy costs manageable. Tepid tenant demand is offset by a shutdown in new supply, which has stabilised private market valuations and driven REIT pricing off historic lows. Standardising triple net yields (rental income after direct property costs, indirect costs and a capex reserve) and scaling returns to local risk-free rates, they identify divergences across markets to determine the most attractive based on current share prices.

Forensic Alpha sees several new accounting red flags emerging, earning the stock a ‘high risk’ label. The two key areas of concern revolve around an accounting policy change (the point at which INTC can capitalise inventory on the balance sheet seems to have completely changed) and an increase in payables (from $8.6bn to $12.6bn, while other accrued liabilities have risen from $12.4bn to $14.3bn. Combined, these balances now amount to a massive $26.9bn, or 64% of net debt). They expect to see increasing scrutiny of the cash flow statement as restructuring efforts unfold in 2025.

Japan

One of those rare stocks that has changed from a low-priced transformation name to a thematic / growth name and one Asymmetric Advisors has maintained a positive view on for over 10 years. Despite the shares being up more than 60% over the last 12 months, this has become a go-to stock for global funds seeking Japan exposure given its high share in grid transformation and leading position in growing domestic IT DX/AI. Another recent earnings beat still leaves Hitachi with room to overshoot its full year target.

Emerging Markets

The company reported Q3 earnings results on Jan 23rd and the stock declined -20% after the report. From Jan 27th to 29th, 7 officers sold a total of 108k shares at prices ranging from INR 852-958 for gross proceeds of US$1.1m. This follows sales of $1.8m in Dec from 16 officers at an average price of INR 1,350 per share. 3 of the Jan sellers also sold in Dec. It is concerning to see a cluster of selling after a significant decline in the stock price and insiders willing to part with a meaningful % of their holdings at a significantly lower price than they sold just 1 month ago. Smart Insider are ranking the stock -1 (lowest ranking).

China Consumer Sector: High conviction ideas

Laopu Gold (6181 HK) - Has positioned itself as the premier brand in China's traditional handcrafted gold jewellery market; looks poised to capture an increasing share of this expanding market.

Pop Mart (9992 HK) - IP retail, centred around emotional value, will maintain strong global momentum with relatively low competition. If SSS and store expansion remain in a growth cycle, there is a high likelihood of continued earnings outperformance and upward revisions.

Yue Yuen Industrial (0551 HK) - Global leader in sports footwear manufacturing. With ongoing cost optimisation and efficiency improvements, it can target a 10% net profit margin, exceeding market expectations and serving as a positive catalyst for the stock.

Abu Dhabi Commercial Bank (ADCB UH) United Arab Emirates

ADCB’s share price has already risen ~40% since Fighting Financials turned bullish in Jul 24, yet they continue to anticipate further upside. The company last week announced its intention to double profits in the next five years. This doesn't seem unreasonable given it doubled profits in the last five years and has good momentum today, having grown PBT at +26% in FY24 y/y. However, consensus is still modelling only mid-single digit annual EPS growth across FY25e and FY26e. ADCB also benefits from the UAE's dollar peg, low tax, geopolitical neutrality and a higher oil price. Fighting Financials core portfolio was up 15% in 4Q24 and is currently +6% YTD with ADCB a key contributor.

US tariffs and their potential impact on Cemex

Cemex’s credit-positive strategic priorities, commitment to strengthening its credit profile, end-market diversification, solid credit metrics and ample liquidity provide some level of comfort in its ability to navigate tariff uncertainty. However, if the US imposes tariffs on Mexico, EM Spreads expects a meaningful negative impact on Cemex’s operational performance. Credit metrics would deteriorate and this risk is further magnified by the fact that much of the positive outlook has been based on expectations of robust infrastructure and housing spending in Mexico, supported in part by nearshoring and government-led investment. If tariffs lead to a sharp economic slowdown, many of these initiatives could be delayed or scaled back.

Macro Research

Developed Markets

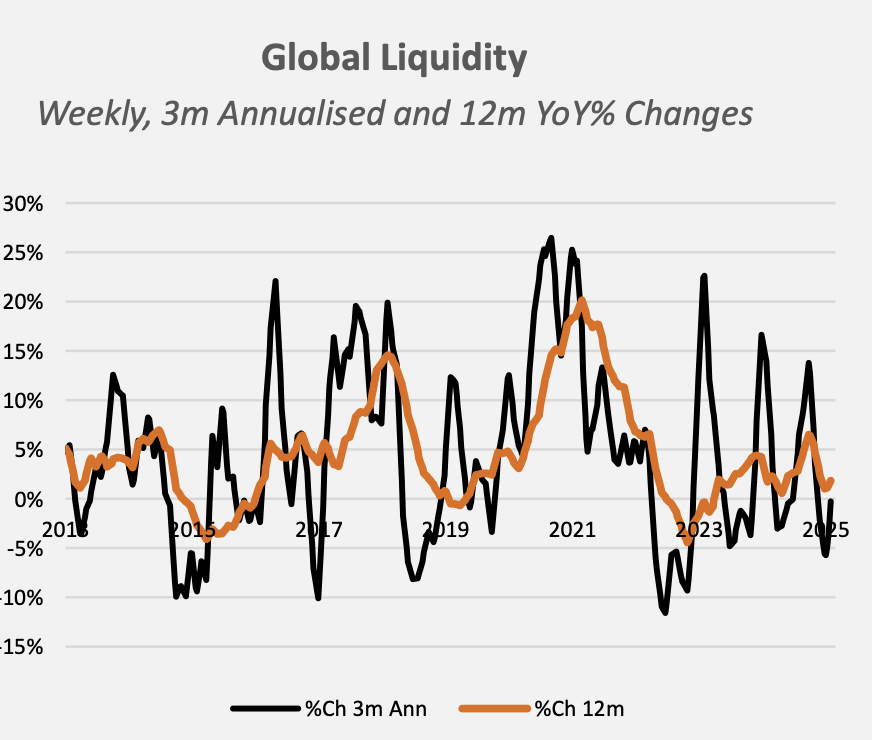

Global liquidity levels have stabilised

Mike Howell points out that global liquidity levels have stabilised following a dip in Q4. He notes that there are four factors underpinning them: (1) Improving Central Bank liquidity, due to the PBoC and ECB. Fed liquidity remains a cause for concern. (2) Collateral values (bonds) which are picking up, in part helped by (3) the loss of momentum in the US dollar. And finally (4), bond market volatility which has retreated from its November peak. Liquidity leads risk asset markets, gold and cryptocurrencies. They recently lost momentum in response to the liquidity slowdown that started in October 2024. Gold and risk assets have recovered in the last week, but Mike fears they may have got ahead of themselves. More liquidity is needed.

Risks in property and bond markets could destabilise equities

Frank Shostak finds that the global growth outlook is very modest with the US having a somewhat better prognosis than the other economies. Japan should suffer a particularly bad year. CPI inflation should continue to decelerate with the risk of deflation, while bond yields continue to manifest a stubborn stickiness. Yield curves should steepen in the US and Europe but not in Japan where inversion is likely. The overall Liquidity that drives stock market momentum is weakening in the US, suggesting a loss of steam in that market, while in Europe Frank still expects some short-term softness to bring markets into line with Liquidity fundamentals which look brighter in the second half. He sees risks in both the property and bond markets which have the potential to destabilise equities, especially as Liquidity declines.

Underlying Inflation

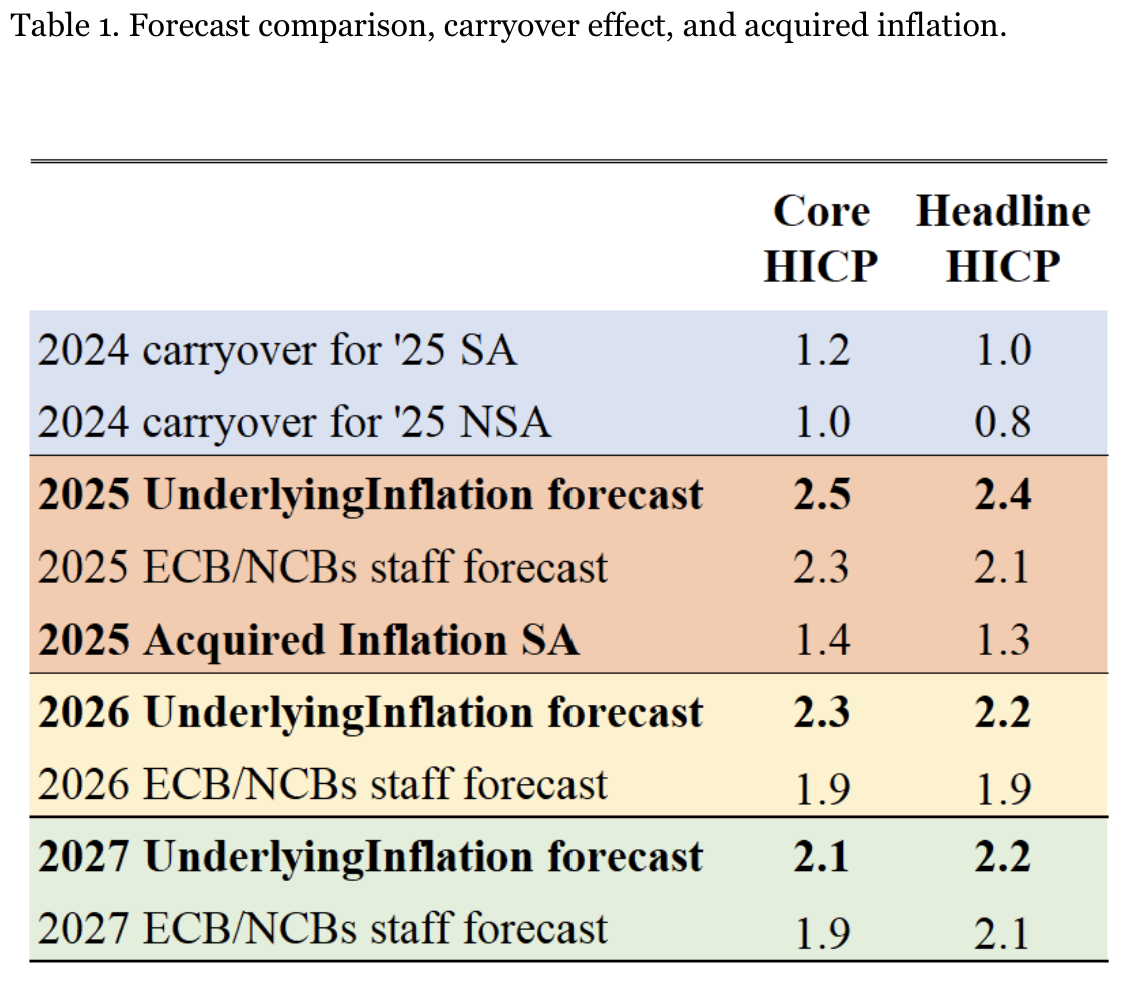

Euro Area Inflation – Core HCIP at 2.5% in January

As expected, Euro Area services inflation remains a concern. The flash release for the HICP (Harmonized Index of Consumer Prices) in January came in as Riccardo Trezzi expected. Riccardo points out that the broader issue remains unchanged: there’s still no sign that services inflation is slowing, having followed its 2023 trajectory throughout 2024 with no signs of the pattern ending yet. Riccardo remains skeptical that a significant slowdown is imminent and he expects inflation to remain sticky in the near term. His models continue to project inflation above the ECB/NCBs staff forecasts. The big picture hasn’t shifted. On one hand, there’s no certainty that it will return to target. On the other, concerns about growth and trade tensions persist—yet the ECB remains focused solely on the latter.

US-EU tariffs: This is going to get bad

Donald Trump's tariffs on Canada should be a worrying premonition for what will happen to us in Europe. According to Wolfgang Münchau, the most straightforward reason for the tariffs on Canada is that it allows Trump to raise revenue without going to Congress. If he can make the executive orders stick legally, it’s one of the few tools he will have at his sole disposal. The tariffs on Canada cast doubt on the possibility that the EU will be able to escape or cut a deal to rebalance the trade relationship. In the longer term, there could be disintegration of the collective west, as trade restrictions now put Europe in the same position as China. Trump also signed an executive order mandating independent assessments of the economic costs of regulation, and a net reduction of those costs – expect this to massively widen the transatlantic growth gap.

US: Animal spirits vs QE’s demise

The old QE-based credit cycle looks to be in its final erratic days – cue higher real bond yields, weak equities and a strong USD. This was the dominant force in markets as 2024 drew to a close. However, Andrew Hunt points out that a new endogenous source of liquidity appeared in the system last week – banks chose to lend more to financials and an animal spirits rally in the credit cycle could offset the demise of the QE-based cycle, thereby holding bonds steady, supporting equities and undermining the USD. In the immediate short term, investors will simply have to see which of these two scenarios prevails over the other. Long term, Andrew’s view is hardening that there will be a further crypto-based leg to the credit boom, something that will make 2025 a lot like 2005 in nature & narrative. On a three-year view, look for higher US inflation, trouble in bonds and a weaker USD.

Anatomy of gross US national product

Ed Yardeni asks: Why is the US economy so strong? Look in the mirror: The consumer is the engine of growth. Yes, technological advancements will continue to buoy GDP, as will Trump 2.0 deregulation and lower taxes. But consumer spending accounts for nearly 70% of real GDP. Ed rejects the notion that consumer spending will slow in the face of depleted savings and other drags; it’s too resilient, which is why the economy is so resilient. Likewise, he doesn’t expect capital spending to slow, notwithstanding a weak Q4; companies still have much to gain from investments in AI and other technological innovations. That’s the linchpin of Ed’s productivity-led roaring 2020s outlook (55% odds) and higher S&P 500 price targets for the rest of the decade.

US: If you can’t find a Trump-proof trade, try a Trump beta-pair

Trump’s decision to club together Mexico and Canada for tariffs is a bit strange. However, out of the two, Mexico has more to offer that Trump wants (immigration flows, border control, manufacturing) and a fully functional government with a mandate to negotiate. Canada’s position is fraught and uncertain. Should further tariff shocks arrive, CADMXN is well protected as long as the countries are lumped together. There are good conditional expressions that can be used to be short CADMXN. With the Dec'25-10y US flattener working well, risk premia are likely to fall. That benefits Mexico much more than Canada. In a (g – r) framework, that is MXN positive.

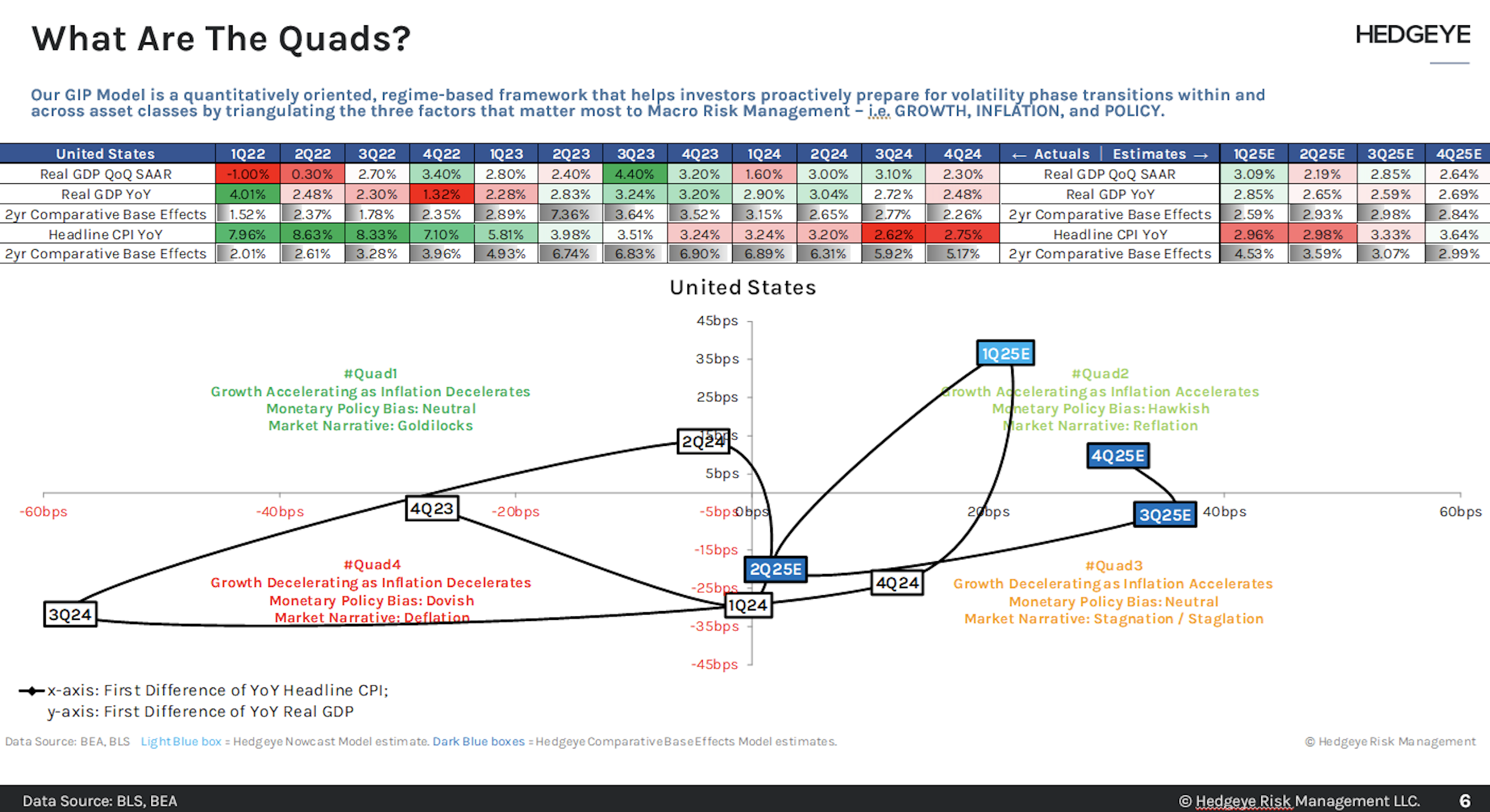

US: Growth forecast for the year ahead

Q4 2024 Real GDP growth of 2.48% Y/Y (2.23% Q/Q SAAR) was a -24bps deceleration from Q3 2024’s real GDP growth of 2.72% (3.04% Q/Q SAAR). The Hedgeye team generally regard ~25bps delta change as the cutoff point for what they consider “shallow” GDP deceleration, putting Q4’s decel just inside the shallow cutoff. Their current Nowcast estimate for Q1 Real GDP growth of +2.85% growth Y/Y marks a healthy RoC acceleration from Q4’s 2.48% growth and equates to 3.05% Q/Q SAAR. Coupled with their estimate for accelerating inflation on a full-quarter basis, this suggests Quad 2 is most likely for Q1 (see graph). Their Q2 and Q3 Real GDP growth forecast estimates call for growth of 2.65% and 2.59%, suggesting Quad 3 is most likely for both Q2 and Q3. Finally, looking forward to Q4, expect growth to reaccelerate to 2.69%, and increase of +10bps in RoC terms. Coupled with expectations for accelerating Q4 inflation, this suggests that Q4 will be Quad 2.

Excellence in FX trading

Triple i Advisors is globally recognised by hedge funds and investment banks, including sovereigns, for capturing exact highs and lows with stalwart accuracy. The architecture to realise this coding achievement involves dissecting volatility, then extending forward into the future price, predicated on each pair’s volatility profile variations. This provides the magnification for directional trades to continue or to pinpoint a new directional initiation with exactness, which can be seen optically in real time by their global clients. This enables Triple i to pre-deliver the following trades' highs and lows in 2024 and 2025: SOLD EUR 1.1214, SOLD GBP 1.3421, SOLD AUD 0.6942, BOUGHT USDJPY 140.85 & 142.01, BOUGHT USDCHF 0.8376, SOLD EURCHF 0.9927, BOUGHT USDBRL 4.76, BOUGHT USDMXN 16.40, BOUGHT USDCNH 6.97 & 7.0140.

Emerging Markets

China: Out with the old, in with the new

William Hess highlights two news items that have sent shock waves through Chinese social media and global markets. The first is the formal nationalization of Vanke, one of China’s largest developers, and the other is the emergence of DeepSeek, an open-source AI model from China. These two developments are relevant because they illustrate the continued divergence between the old and new economies in China. The former showcases Beijing’s resolve to avoid financial defaults for major developers, setting a price floor for old economy assets. This floor may be low, but it avoids the abyss. The latter reveals the upside potential for Chinese tech companies via a new generation of “late developer advantages”, meaning the ability to achieve competitive outcomes with binding budget and resource constraints despite the US tech embargo. Exciting times ahead.

Colombia: Playing hardball with Trump

President Petro’s feud with Trump over repatriation of Colombian nationals may appear to be an impulsive reaction, but the quickly solved impasse has become a campaign issue. Since Petro cannot successfully run on his record as President, he can spur on a national debate over whether voters want a left-wing government defending national pride, or a right-wing government acting as Trump’s “puppets”. In the meantime, growth remains weak, and Marcos Buscaglia expects equally dull conditions throughout 2025. Inflation expectations have stopped falling. With Petro’s appointment of two new directors of the Central Bank, his control over Banrep grows further and casts doubt on a more hawkish central bank during the year. If risks materialise, the local yield curve will steepen.

Ecuador: Election amidst the chaos

Ecuador is gearing up for a presidential election. An ongoing energy crisis and the collapse of the country’s security apparatus amidst drug cartel violence have eroded President Daniel Noboa’s once-stellar popularity. Yet, Niall Ferguson expects him to win what is in effect a rerun of the 2023 presidential race. Perceptions of political risk might increase in the short term, since Niall expects Noboa to face a competitive run-off against a leftist candidate in April, but he should win it in the end. For the first time, Ecuador’s centre-right may achieve a strong bloc in the National Assembly, as Noboa’s party is poised to win 35% of the seats. Expect a strong legislative coalition, which will secure policy continuity, and a stronger mandate for reform. This makes Niall constructive on Ecuador despite the dire domestic security situation, with sovereign debt looking favourable.

South Africa: Ground to a halt

The economy continues to flatline in real terms, with nominal growth is at an all-time low as well. SARB has begun a cautious easing cycle, but real rates are stuck at record highs. Nominal rates are coming down gradually, but real rates and rates/growth gaps are still at record highs. As a result, South Africa's public debt ratio continues to rise rapidly. Unlike Brazil, where the policy onus falls both on the central bank and the treasury, Jonathan Anderson points out that in South Africa the ball is almost completely in SARB's court, waiting for further easing and any measures to help rein in long yields. Until that happens, the main silver lining of the current painful combination of high rates/no growth is that the external balance is back in surplus, the rand is relatively stable, and fixed income and carry returns are very attractive. Jonathan stays all-in on fixed income.

Commodities

US copper continues to atrophy

Political and legal challenges continue with few domestic US copper projects advancing (and some then failing), while existing production continues to mature (see chart). Ultimately, stagnation of US domestic production strengthens the upside case for the copper price. The US has the resource inventory to be self-sufficient, yet it is hard to see any of the key larger projects progressing in the mid-term. By the end of this decade, Global Mining Research sees incremental projects lifting volumes to ~1.3Mt/yr from current production at ~1.1Mt/yr. Preferred US-exposed copper plays are Freeport (upside from leach and Bagdad 2X), Taseko (Florence ISL expected to commence in 2025) and Hudbay (significant resource optionality).

Will silver mine supply peak in the next five years?

Global silver mine production was once buoyant, rising to a peak of 900Moz in 2016. The industry then endured a prolonged decline, falling at an average of 1.4% a year to 814Moz in 2023. In their latest report, the Metals Focus team examine the years ahead for the precious metal. The team expects silver output to rise by 2% y/y to 826Moz in 2024, driven by planned expansions at existing operations. Beyond this, supply will experience staggered growth, rising to a peak of 856Moz in 2027 and plateau thereafter. Of the top five producers, Peru will see the largest growth, leaping from 10Moz to 117Moz. In contrast, production from currently operating mines is expected to fall by 2029 and so output will become increasingly reliant on the successful commissioning of developing projects.