Company & Sector Research

Europe

Stockpulse

Harness real-time social media sentiment for smarter trading decisions

Stockpulse offers advanced AI-driven data and signals covering more than 70k securities and 40 markets globally. They have developed a series of alerts to help investors stay ahead of the curve including: 1) Buzz Alerts - triggered when real-time buzz around a stock skyrockets, giving you a heads-up that something big might be brewing. 2) Moving Stock Price Buzz Alerts - if buzz is high and the stock price is moving sharply, this alert gives you instant insight into real-time price shifts. 3) Pre-Earnings Buzz Alerts - notice a surge in chatter before an earnings release? This alert tells you that traders are already speculating, so you can prepare. 4) Adhoc News Buzz Alerts - when official news breaks and the buzz jumps, this alert shows that the news is having a significant market impact.

Ben Jones Investments

Ben Jones believes the market is overplaying the significance of rate moves and paying too little attention to the business fundamentals. TW’s current valuation would only be appropriate if volumes and margins never recover. Ever. Ben anticipates a recovery to 14,000 completions p.a. over the next 3 years. TW has near to no debt and still generated >£300m net income and OCF in 2023. Although he expects net income of c.£230m in 2024, Ben sees the homebuilder generating >£500m p.a. under more "normal" conditions. He maintains his view that TW is significantly undervalued.

Iron Blue Financials

Iron Blue initiates coverage on KYGA with a score of 28/60, which is top quartile and fertile grounds for shorting. Accounting concerns highlighted include: 1) A significant increase in stripped out restructuring expense over the past three years. 2) FY23 PPE capex exceeded depreciation by 9% of PBT adj. 3) 12.6% tax rate is lower than suggested by the geographic profit split and could see risk from Pillar Two. 4) Discount rates for pension liabilities and the goodwill impairment test both seem less conservative than average. Re. governance, they note a 21-year average KYGA career within the leadership team, a nationality mismatch with the group’s geographic mix and a CFO who previously was lead auditor on KYGA.

Hedgeye

The company has exceeded its growth targets in recent years, resulting in a premium valuation of 33x EPS and 20x EV/EBITDA. However, the challenge to repeat this success is its most important commodity input, cocoa. To offset further cocoa inflation in 2025, the company plans to raise prices by double-digits. Aggressive price increases are made worse by chocolate being virtually the only food / gift experiencing high levels of inflation. As a result, Daniel Biolsi has added the stock to Hedgeye’s Best Ideas Short list; sees 25%+ downside.

MYST Advisors

SRC was one of the stocks highlighted at MYST’s Top Post-Election Ideas Forum - Trump’s victory is expected to accelerate a potential resolution of the war in Ukraine and the recent closure of SRC’s acquisition of CRH’s Polish lime operations positions the company as a “stealth beneficiary” of reconstruction efforts. The stock trades at just ~5x FY25 EBITDA with a ~13% FCF Yield, a substantial discount to US peers including Martin Marietta, Vulcan Materials and Summit Materials. Notably, SRC's closest comp by size, US Lime & Minerals, trades at ~28x EBITDA. Presenter’s 2-year TP is £1.54 (95% upside), but he sees potential for a 3-to-4-bagger over time.

ResearchGreece

Hurricanes, lower volume, higher pricing and stronger margins. These are the main points coming out of US cement companies in their Q3 updates and all of them are sharing an upbeat outlook for 2025. ResearchGreece believes TITC’s soon-to-be-IPOed US business deserves the 9x-10x EBITDA 2025 multiple of its US cement peers. Valuing what is 55% of TITC's total EBITDA at 9.0x, results in zero value for the company's non-US operations. For 2024-2026 ResearchGreece forecasts EBITDA of €580m-€640m, net income of €295m-€343m, payout at 30%, capex at €250m and FCFE of €170m-€270m resulting in net debt of €160m in 2026 (vs. €483m in 2024). TP €47.6 (25% upside).

North America

Huber Research Partners

The current stock price applies an overly punitive 37% conglomerate discount to NWSA’s valuation, according to Craig Huber’s detailed SOTP analysis. Craig has no doubts the company should be broken up, arguing that management could greatly enhance shareholder value by doing any of the following: 1) Distribute REA shares held by NWSA to existing shareholders, ideally in a tax-free structure. 2) Wait for a much better environment and then sell Move (Realtor.com). 3) Sell / spin-off Foxtel. 4) Spin off Dow Jones. 5) Sell Books operation. 6) Sell Factiva. 7) Shed underperforming assets such as its secularly declining News Media segment. While investors wait patiently for portfolio simplification, fundamentals continue to improve. Craig raises his earnings estimates for both this year and next.

Periphery Research Partners

EXPE has gone to great lengths to showcase its “industry-leading” B2B business, but this segment is only 30% of revenue and y/y growth just slipped below 20% for the first time since 2021, so it can only obfuscate weakness in the group’s core US lodging business for so long. Hesham Shaaban expects core declines to become more evident if his Revenge Travel Hangover theme manifests. He also plans to be short in force into the next print, especially given EXPE has a history of setting aspirational 4Q targets into year-end. It has missed 4Q revenue estimates twice in the past 3 years and the stock has also traded down on 4Q results each of the past 4 years.

Sidoti & Company

While the market still discounts GEF based on its cyclical exposure and legacy focus on containerboard and steel, Sidoti believes the company’s ongoing transformation has created a long runway for growth and margin expansion, particularly in its Global Industrial Packaging segment, and deserves to be valued as such. With a top-tier management team and its “Build to Last” strategy, GEF looks to separate itself from its peers as a specialised and diversified materials company offering high-teens margins and superior FCF conversion. Sidoti’s TP of $93 (30% upside) is based on an 11x price to free cash flow multiple on their FY26 FCF estimate of $400m ($8.44 per share).

Kailash Capital Research

KCR highlights the uncommon relative value available in blue-chip staples stocks. The data is clear: today is one of the best times in 30+ years to buy select names in the sector and KMB appears to be a stock with rapidly improving fundamentals which investors have overlooked. It trades at ~18x projected 2025 earnings, a 10% discount to the S&P 500 and a ~25% discount to peers, despite the strong and consistent earnings and cash flow growth it has reported over the last eight quarters. KMB also trades at a substantially lower multiple of P/FCF (16x vs. 23x-41x for Clorox, Colgate-Palmolive and Procter & Gamble), while offering a materially higher dividend. If the 6x-7x P/E multiple gap were to be cut in half, KMB’s share price could be revalued higher by ~$25.

Portales Partners

Sequencing a surge in capital markets & quantifying benefits of deregulation

Bank stocks are rerating higher in Q4 dramatically outperforming the broader market. The stocks have exceeded their traditional 55% relative P/E ceiling. In Charles Peabody's previous report, he quantified the benefits of tax cuts, robust capital markets, a steeper yield curve and more buybacks, which would result in an 11%-16% rise in bank earnings. This week, after conversations with policymakers, he believes a lighter regulatory touch could improve earnings a further 3% or more. Sequencing is important, as the Trump Administration is intent on taking a blowtorch to the government. There may be serious economic headwinds from attacking the fiscal deficit, followed by more rapid economic growth in the longer term.

Northcoast Research

While LII's management has done a stellar job righting the ship over the past few years, Northcoast balances this view with their dour outlook for the North American residential HVAC market in the intermediate term, which is c.70% of the group's business. In their 36-page industry initiation report titled ‘Hot Air and Cold Realities’, they argue that while market participants appreciate the unit volume headwinds, they do not appreciate the pricing headwinds given the potential for intensifying competitive dynamics. As such, Northcoast initiates coverage of LII with a Sell rating and TP of $475 (30% downside). Other stocks covered include Carrier Global, Comfort Systems and Trane Technologies.

Alembic Global Advisors

APD has underperformed closest peer Linde by over 100% since the two companies hit their Mar 20 lows. The initial underperformance came on the back of compressing EBITDA margins driven by natural gas pass throughs at APD - something that has reversed itself since 4Q22. The recent underperformance has been driven by investors feeling jittery about the capital allocation strategy at the company and associated IRR concerns as well as rising debt and dwindling FCF levels. Hassan Ahmed’s analysis suggests these concerns are being addressed and the share price underperformance should reverse itself. His 12-month TP is $375.

Paragon Intel

Tomer Weingarten’s declining engagement and mercurial behaviour a poor fit for a public company CEO - Paragon’s analysis includes interviews with former senior executives who worked with Weingarten for more than 18 years combined. They described him as volatile and abrasive, lacking integrity and prone to impulsive decision making, which has led to the departure of a previously strong C-suite. Repeated shifts in financial guidance have lowered his credibility with investors, with sources noting the company would be better off acquired or run by a new CEO, although neither option is likely given Weingarten’s control of the board and voting shares.

Japan

Astris Advisory Japan

Potential NTT interest in SBI Sumishin is not far-fetched

SBI Sumishin Bank shares popped 17% on reports that NTT DOCOMO could be a buyer. Kirk Boodry thinks it is an easy story to believe. DOCOMO has already said it is looking at online banking options to solidify its fintech portfolio. And SBI Holdings essentially has two online banks as recently acquired and privatised SBI Shinsei Bank has a minimal offline footprint. It is encouraging that shares of NTT (rated Buy) were up on the news and while Kirk would like to believe that represents an endorsement of higher fintech exposure, it could also reflect hope that NTT may be steering clear of any involvement in a domestic Seven & i counterbid. The price tag could be somewhat steep with SBI Sumishin valued at ¥514bn, but NTT Group has the balance sheet to support a deal.

Emerging Markets

86Research

Multinationals in China: Europe vs. US

Much of what 86Research has heard this earnings season confirms insights they have previously flagged re. the China market, including the strength of Sam's Club, the robust expansion of travel demand and the competitive challenges facing Starbucks and iPhone. More remarkable, however, are the latest moves by several European multinationals, such as Volvo and LVMH, which appear committed to cross-border cooperation in areas relatively insulated from geopolitical pressures. Beneath the broader, probably over-generalised narrative of a multinational exodus, a more nuanced observation points to a potential structural shift in the origins of China-bound investments, with European firms advancing at the expense of their US counterparts.

EM Spreads

EM Spreads continues to view MELI as an attractive emerging market credit story. For EM investors, they prefer MELI 2.375% 2026 notes. These bonds trade wide relative to the EM BBB and LatAm BBB Indices, offering a more favourable risk-return profile than MELI 3.125% 2031 notes. For US investors, MELI's risk-reward symmetry is particularly compelling. The 2031 bonds trade wide to the broader US Index, yielding 1.0 percentage points higher than comparable global e-commerce and fintech peers. EM Spreads believes MELI’s geographic diversification, strong liquidity, healthy credit metrics and positive outlook partially offset the risks linked to its LatAm exposure.

ERA Research

Shandong Chenming Paper forced to idle capacity

News that the company is having to idle 7.1MMmt of capacity due to a liquidity crunch is a seismic event. ERA has been highlighting domestic oversupply of coated ivoryboard for several years, but it has been the loss of the prior export release value (due to high shipping costs as well as increasing trade barriers) that finally destroyed producer pricing power in China. There are several possible paths forward: either the Chenming capacity remains out and other producers succeed in their announced increases, restoring some profitability…or Chenming was only the first shoe to drop and other producers are in similar dire straits and business failures will expand. ERA is inclined to favour the latter, which in turn should lead to pressure on imported pulp demand and prices.

Smart Insider

Smart Insider upgraded the stock in May based on a US$1.2m purchase from Yun Sung Na (Co-CEO) at KRW 31,717. While a minor addition to his holdings of 4.9m shares (13% of the company), it was noteworthy to see him make his first purchase since Dec 2018 and with the stock close to an all-time high. It proved very timely. The stock traded as high as KRW 70,000 in July. Since then, the share price has retraced significantly and Yun Sung Na has recently made additional purchases of US$1m at KRW 33,745. It is interesting to see him add, especially after watching the stock double and roundtrip. Smart Insider renews their +1 rank (highest rating).

Radio Free Mobile

Balkanisation of the Internet has begun

Huawei’s migration of its smartphone business to its home-grown Harmony OS is the first concrete sign that Richard Windsor’s long-predicted splitting of the Internet into two pieces has begun and everyone, not just China, will be poorer because of it. Richard thinks that every technology standard created from here on will have a Chinese version and a Western one which are developed independently and are incompatible. This is why he has been forecasting that the long-term growth of the technology industry will be lower. Huawei is the first to go down this route, but he has no doubt that there will be many others over the next few years.

Macro Research

Developed Markets

GFC Economics

UK: BoE signals caution on rate cuts

The BoE is rightly signalling a more cautious approach to cutting rates, after Labour’s autumn budget. The case for rate cuts was not convincing and the latest inflation data underlined the point. The drop in UK labour productivity in Q3 (-1.8% y/y) should be a warning: without a significant improvement in the supply side of the economy, inflationary tendencies will persist, particularly with such fiscal largesse. With landlord instructions falling relatively sharply in October, the continued imbalance between rising tenant demand and dwindling supply will keep rent inflation elevated, making the 2% inflation target even more challenging. The y/y for the ONS private housing rental index re-accelerated from 8.44% to 8.67% in October. Private medical insurance costs are also climbing sharply, driven by higher demand for private healthcare services, pressure on public healthcare systems and higher levels of claims.

Greenmantle

Germany: Who is Friedrich Merz?

Germans are set to elect a new Bundestag on February 23, 2025. For now, the centre-right Christian Democratic Union (CDU) under party Chairman Friedrich Merz leads in the polls by a large margin. The centre-left Social Democratic Party (SPD) of sitting Chancellor Olaf Scholz could attempt to gain ground by abandoning Scholz and backing the very popular defence minister, Boris Pistorius, as candidate for chancellor. Such a move could upset the race. But even then, Niall Ferguson’s base case remains that Merz will become Germany’s tenth post-war chancellor. Merz would govern with either the SPD or the Greens. His arrival would translate into a loosening of fiscal policy, supply-side economic reforms, more robust support for Ukraine and potentially even the issuance of EU bonds to finance defence spending.

Eurointelligence

Europe’s car industry

The Swedish battery start-up Northvolt has filed for bankruptcy in the US. It is the latest in a series of mishaps to befall Europe’s car industry. Wolfgang Münchau argues that the main problem is not with the new firms like Northvolt, but rather Europe’s dependence on incumbent auto dinosaurs. Compared to Tesla and the panoply of Chinese electric car firms now present, the old incumbent firms are struggling to manage the process. There is also more effective vertical integration, with the new firms building their own batteries instead of relying on smaller new firms. This success stems from a key difference between Europe and both the US & China, the first being more effective capital allocation and the second being a willingness to see new firms pop up, rather than coddling old ones.

Totem Macro

US: The madness continues

For months, Whitney Baker has been focusing on the record dislocations between asset positioning versus cashflows and nominal growth, the leverage used to fund this, extreme risk-positioning and record low cash allocations even by the standards of the most extreme bubbles in history, the increasing evidence of a late-cycle downturn in global and US growth, a synchronised global earnings downswing, and the deflationary collapse rippling outward from China. Yet the market believes the opposite, because it doesn’t understand where we are in the cycle. In light of this, Whitney uses her latest report to debunk several bullish narratives, including a repeat of Trump’s market in 2016 and a US manufacturing renaissance. Meanwhile, in EM, a quiet equity rotation is beginning.

Steno Research

US: Expectation vs reality

One of Andreas Steno’s strongest convictions right now is that the US bond market is not prepared for upcoming macro trends in 2025. The team’s US nowcasting model has been reliable and is now predicting weakness. Although it’s still far from recessionary, markets are all about expectations, and right now they’re heavily tilted towards higher yields and a more hawkish Fed, but the services sector – a key pillar of strength – has started to weaken in their models. Historically, this has been closely correlated with the 10-year yield, suggesting that bonds might soon offer a compelling contrarian trade. Andreas continues to favour US and UK bonds, even as it remains a contrarian stance, and US equities.

Beacon Policy Advisors

US: Tech policy under the GOP trifecta

Despite Silicon Valley’s left-leaning reputation, President-elect Trump made significant inroads in the industry during this election cycle. Silicon Valley can expect a more business-friendly approach to some tech policy issues under the Republican trifecta, such as data privacy and AI. However, that doesn’t mean Big Tech will be left to their own devices; the GOP is likely to deepen scrutiny elsewhere, primarily online speech and section 230. Smooth sailing is not guaranteed. What is perhaps the biggest outstanding question is the president-elect’s selection of anti-trust enforcers, where nominees may come from the traditional pro-business wings of the GOP or the ranks of the ascendent “Khanservatives”, i.e. populist Republicans who are more sympathetic to the relatively aggressive style of anti-trust enforcement pursued by outgoing FTC Chair Lina Khan.

Eurizon SLJ Capital

Will the US fiscal deficit be driven down to 3% of GDP?

According to Stephen Jen, the first ‘3’ of the ‘3-3-3’ policy slogan is to drive the federal fiscal deficit down to 3% of GDP, a stark contrast to a forecast Stephen has seen of 12% of GDP by the end of Trump 2.0 in 2028. Three weeks after the election, he has not yet seen one analyst explicitly including spending cuts in their projections. This is a mistake in market expectations, which presumably were formed by experiences from Trump 1.0 as well as Reagan failing to materially narrow the fiscal deficits despite promising to do so. We will see if the Laffer Curve will work, and if Musk and Ramaswamy’s recommendations will be implemented. Stephen believes so, mainly because of the aligned White House, Congress, business giants like Elon and Vivek, and a very strong consensus across the board against fiscal laxity, yet the market believes otherwise.

Grey Investment

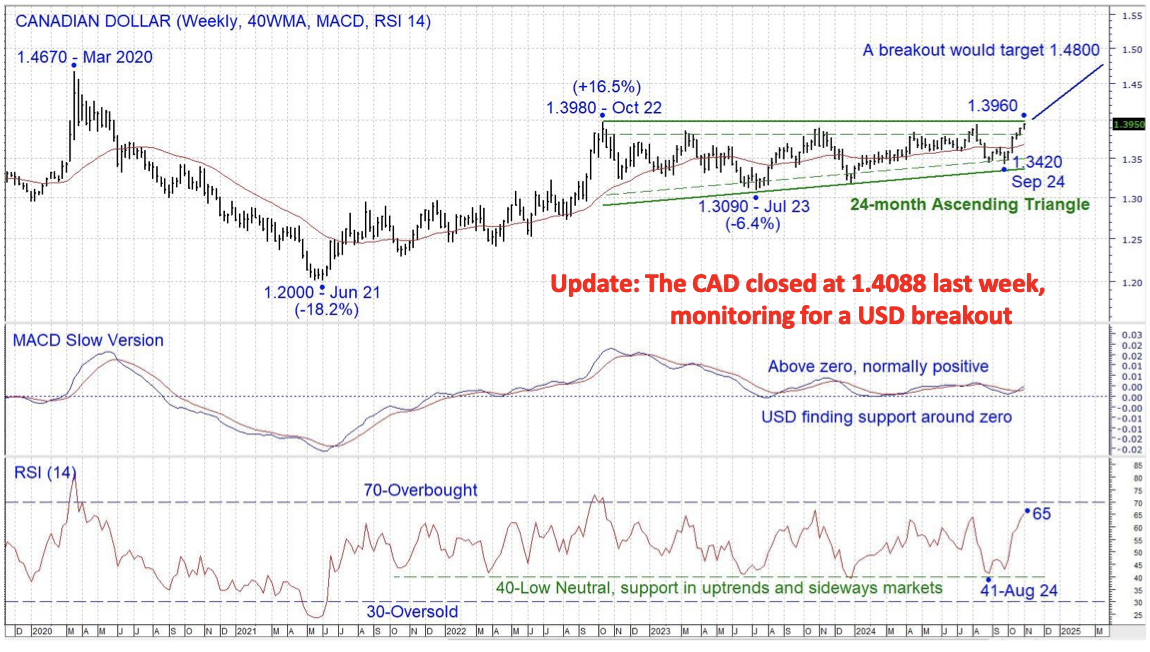

Canada: CAD to test major USD resistance?

The weekly chart of the Canadian Dollar features a potential 24-month ascending triangle. A weekly close much above 1.4150 would likely lead to another test of key monthly resistance at 1.4670+. Chris Roberts would consider a USD long position if a breakout from the Ascending Triangle occurs. Further, he would look to exit USD longs and recommend a short if the CAD reached the top end of the 8.5-year range. MACD has managed to stay above the zero line as the Ascending triangle has been forming, supporting the bullish implications (for the USD) of the chart pattern.

Westbourne Research

Japan: Where to next?

Sharmila Whelan’s latest reports provides a deep insight into the Japanese economy. Currently, business cycle indicators remain broadly positive, underpinning continued economic recovery and corporate earnings growth. The corporate profit cycle is strengthening, the investment cycle is in upswing and so is the credit cycle even though private credit growth is slowing. Mortgage borrowing is picking up strongly, a positive for property-related sectors, potentially consumer discretionary spending. The reality right now though is that spending is moderating despite strong nominal wage growth and slowing inflation. Consumption rather than exports is the biggest uncertainty to the outlook. Sharmila maintains an overweight on equities. Japan’s private equity market also looks interesting. Expect the yen to weaken against the US dollar; go underweight JGBs and hedge against yen weakness.

Emerging Markets

Alberdi Partners

The distant and immediate future of trade in Argentina

One of the greatest tragedies of Kirchnerism is that it killed the export sector. However, Marcos Buscaglia comments that exports will soar in the coming years, with $45bn+ coming before 2030 only from oil and agriculture. In the short term, however, imports will rise faster. Import growth is going to be robust next year. Final goods imports are already rising fast, as an exchange rate-based stabilisation gives rise to strong durable sales. With the elimination of the Impuesto PAIS at the end of the year and a strong ARS, this trend will intensify next year. This will lead to a deterioration of the trade balance and of the current account balance in 2025. In the context of a fixed exchange rate, the accumulation of reserves will hinge on the fate of the financial account.

Enodo Economics

China: Easing the surge

Diana Choyleva expects Chinese equities to rise in coming quarters, with Beijing actively managing the pace to ensure sustainable multi-year gains rather than speculative surges. China placed equities support at the core of its unexpected stimulus package with two new tools: a Rmb500bn central bank swap facility and Rmb300bn re-lending facility. If the policies are successful, the authorities pledged to expand these tools, which could bring the overall size of equity market support to Rmb2.4trn, comparing favourably with the Rmb1.6trn of national team buying in 2015. As Diana argued in September, this is as close to the Chinese authorities saying, "whatever it takes" and will help unleash greed. But the authorities want to attract professional investors and institutional capital, not retail-driven speculative volatility. They appear to have learnt from past boom-bust cycles and are prioritising stable wealth creation over short-term excitement.

East Asia Econ

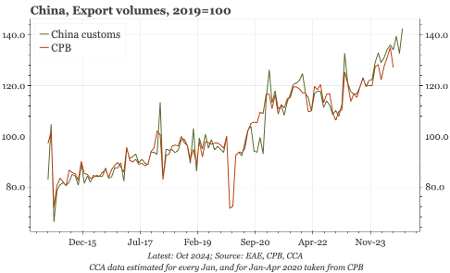

China: Export-led growth continues

Paul Cavey notes that China’s export volume growth remains remarkably strong, in absolute terms, but particularly relative to the sluggishness of world trade. In this relative sense, China's export performance this year is as strong as it was during the boom that followed WTO entry. At the same time, Paul points out that there’s no sign of a revival in imports. Both values and volumes are now falling YoY. Whereas before the pandemic import volumes were growing more quickly than the global average, that order has now been reversed. With the strong growth in export volumes and little change in imports, the real trade surplus is still rising. That will be useful for GDP growth in Q424. But the continuation of export-led growth will be less helpful for relations with the incoming US administration.

Emerging Advisors Group

Nope, still no flood of Chinese goods

Once again China is posting a strong trade surplus and the news flow is all about mainland exporters rushing to ship goods to the US in advance of US tariffs. The reality, according to Jonathan Anderson, is that Chinese exports are broadly flat and just in line with the rest of EM. The true explanation behind high trade surpluses is a big "import crunch"; Chinese import spending has fallen well below the EM-wide trend in recent years...and the gap is increasing. China's merchandise trade surplus is embarrassingly high at roughly US$1 trillion - but the "basic" BOP balance is much lower, less than US$300 billion, and this is the figure that matters for Chinese macro policy. China has been and will continue to restrict imports and other outward spending by all means possible.

Teneo

India: Adani indictment may prompt domestic and geopolitical ripples

The US Department of Justice has indicted Gautam Adani and seven associates for allegedly orchestrating a USD 265mn bribery scheme, raising concerns over transparency and compliance within India’s corporate sector. Domestically, opposition parties have renewed their criticism of cronyism involving the Adani Group, but political complexities make directly blaming the Bhartiya Janta Party-led government difficult. The indictment and its fallout threaten India’s global economic ambitions and could strain India-US relations, adding to existing tensions over trade and geopolitical alignments.

ESG

Verisk Maplecroft

Locating risk, unlocking value

Verisk Maplecroft’s new Area Risk Exposure Analytics (AREA) tool opens up the black box for portfolio managers of asset-level corporate exposure to global climate, environmental, political and human rights risks. AREA combines the locations of 4 million+ corporate assets with industry-leading, geospatial risk data, featuring 85 individual risk issues that are mapped down to subnational levels. AREA has been specifically developed to reveal hidden vulnerabilities and strengths in the global operations of 50,000 publicly listed companies worldwide and provides investors with an entirely new way of assessing the sustainability and resilience of the organisations they invest in. Please contact us to find out more.

Sustainable Market Strategies

Playing the Trump card

The outcome of the US election creates a tough backdrop for ESG strategies, but it is far from being the death knell. Indeed, Trump’s first term was an excellent time for many thematic sustainability funds and many equity sectors moved contrary to consensus expectations – this trend could repeat over the next four years. Companies that have benefitted from deglobalisation, such as those involved in building domestic supply chains, will continue to thrive in the years ahead. Sustainability-focused investors should look for industrial companies that generate most of their revenues within the US and support resource efficiency, climate adaptation and automation, as these will be in high demand (see table for some examples).

Commodities

Stray Reflections

Bitcoin: The speculative craze is over

It’s always risky to call a market top, particularly in crypto. Still, Jawad Milan feels that it’s important to point this out: the current patterns suggest that we are at a pivotal moment. Whether it’s a major turning point or just another phase in Bitcoin’s cycle, it’s something we shouldn’t ignore. Much like the Glencore IPO in May 2011, which marked the end of the commodities supercycle, Coinbase’s public listing in 2021 signalled the top in digital assets. Glencore has since seen a large surge precipitated by a massive fall, and Coinbase followed a similar trajectory, with its stock opening at $381, climbing to $429, then plummeting 92%. It has since rallied 965% to a recent high of $341, reaching the 78.6% Fibonacci retracement level, just like Glencore in 2018. Jawad estimates potential upside levels of $102,000-$116,000. The speculative energy has been exhausted; now we’re in a market with less upside.

ABCG Research

Gold on track to challenge all-time high

Sohail Yousaf points out that the technical structure suggests that gold is on track to challenge its all-time high (ATH) in the first quarter of 2025, given the consistent formation of higher highs and higher lows. Considering both the technical and fundamental outlook, gold's current bullish trend remains dominant, but there are opportunities for strategic positioning. If gold manages to hold the $2,735 resistance level, entering short positions with a target of $2,690 could be a prudent short-term strategy. However, the broader trend remains bullish, and the team recommends aligning with this momentum. Key buying opportunities could emerge around the $2,690 and $2,660 support levels, offering favourable entry points for long-term gains.

CPM Group

The real reasons investors should expect higher gold and silver prices

In this presentation, Jeffrey Christian of CPM Group discusses the latest developments in the precious metals markets, focusing on gold, silver, platinum and palladium. He looks at how global risks and shifting political landscapes, such as the recent election and its aftermath, are affecting investment demand for the precious metals. He also looks at some economic concerns such as recession risks and their impact on commodity prices. The video concludes with a look at open interest for gold and silver and what it could mean for price movement as we move toward the close of 2024. Click here to watch.