Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

90% hit rate on Shorts, while Buy calls also continue to outperform

Since the beginning of 2024, AIR has published 41 Short ideas, 37 of which have generated absolute gains. Standout performers include B&M, LEM Holding, Remy Cointreau, STMicroelectronics, Stellantis and Valeo. In Q1 2025, AIR initiated 6 new Short positions, with LVMH leading the pack, and closed 6 positions, including a 54% gain on Aston Martin. On the long side, AIR’s Top 10 Large Cap Best Ideas returned +7.7% in Q1 this year, outperforming the Stoxx 600’s +5.2% gain. Since inception in 2012, the selection has outperformed the index by nearly 300%. Meanwhile, AIR’s Top 10 Mid Cap Best Ideas Selection delivered +17.3% in Q1, far exceeding the +4.3% return from the Stoxx Europe Mid 200 Index.

Pernod Ricard (RI FP) France

Woozle’s Q1 channel checks reveal a sharper-than-expected revenue and volume decline with clear underperformance vs. Bloomberg estimates and accelerating market share losses. Despite some stabilisation from pricing actions and marketing efforts, underlying consumer demand remains weak, product innovation execution is poor and competitive pressures are intensifying. In North America, organic revenue fell -3.6% Y/Y, with 83% of respondents reporting declining volumes and 50% missing internal targets. In Europe, organic revenue dropped -1.3% Y/Y, with 60% of buyers citing flat or negative growth. Aperitifs and RTDs performed best across North America, while no clear standout category emerged in Europe. Key sub-brands like Suze and Pastis 51 showed strength, whereas Chivas, Olmeca and L’Orbe underperformed.

Smart Insider ranked TSCO +N on Jan 29th based on a £150k purchase from Gerard Murphy (Chair since 2023) at £3.71. The stock has moved lower since, and on Apr 11th, the CEO, CFO and a director combined to purchase £280k worth of stock at around £3.20. Ken Murphy (CEO since 2020) spent £130k and Imran Nawaz (CFO since 2021) spent £50k. Both have only one prior purchase, in Oct 2022 at £2.00, which proved to be very timely. Chris Kennedy (Director since Feb 2025) made his first purchase, spending £100k. Smart Insider are upgrading the stock further, from +N to +1 (highest rating).

Market volatility appears to pose little risk to ENQ’s proposed reverse takeover of SQZ, according to an industry source cited by CTFN. The companies are still figuring out deal terms, especially as “relative share-price movements are a factor” with SQZ’s share price down by 6% and ENQ’s up by over 20% since merger talks were first announced last month. It would be hard for a commodity collapse to dissuade both sides from making a deal given they break even well below $60 a barrel. It also helps that half of SQZ’s business is in gas production, which has held up better than oil in recent weeks. Although the parties are “both keen to proceed”, they have a lot of work to do and the PUSU deadline “may well be extended again”.

Banks vs. Tariffs

TriggerPoint Research is increasingly confident that the SX7P’s 54-month streak of uninterrupted outperformance is well and truly over as macro uncertainty mounts. While the impact of nascent tariff wars on inflation, interest rate policies, trade and by-country GDP is impossible to forecast accurately, one thing is certain: the outlook has dimmed significantly. TriggerPoint’s analysis draws on excerpts from ECB stress test publications to assess how changing macro conditions impact bank credit charges and earnings outlooks, while their report also explores how to approach bank valuation in an environment where earnings visibility disappears and capital return plans face growing uncertainty. Three banks are used as case studies: Barclays, HSBC and Santander.

Dassault Systemes (DSY FP) France

Siemens is acquiring Dotmatics, a US-based SaaS provider for laboratory management, for $5.1bn. The acquisition appears expensive (16.5x EV/sales and 39x EV/EBITDA for FY25) but strengthens the group’s position in the life sciences sector by expanding its digital twin technology and industrial software offerings. Dotmatics adds a new $5.5bn market opportunity, which could grow to $11bn, covering areas like pharma manufacturing, biofuels and chemicals. SIE’s growing presence in this sector will intensify competition where DSY currently leads the market. While GR20 does not expect DSY to respond by going on a buying spree, there could be interesting opportunities for M&A to enhance the 3DExperience platform (on the Biovia side) or Medidata, particularly to align with its recently launched 3D Universes AI-driven environment.

North America

Buy Canada

Analysts at Veritas provide their best ideas for taking advantage of volatile markets. This series of reports features: 1) Veritas President and CEO Anthony Scilipoti providing an overview of why he is more bullish on Canada than the US. 2) Martin Pradier (Materials Analyst) on why he favours gold with Agnico Eagle Mines his preferred play. 2) Darryl McCoubrey (Energy) discusses why he favours pipeline infrastructure with Enbridge and TC Energy his best ideas. 3) Ben Butler (Utilities) looks at valuations in the sector with Fortis his top pick. 4) Liam Gallagher (Communications & IT) on why Quebecor is the best positioned operationally and from a valuation perspective. 5) Shalabh Garg (REITs) covers long-term interest rate trends and why he believes Chartwell Retirement Residences and Granite REIT are best positioned to take advantage of market dislocations.

Looking out over the NTM, whether trade deals are made or not, Brian McGough thinks LULU's earnings power lands closer to $10 than the Street's $17+ and that the current narrative around high growth in China / RoW offsetting North American weakness dissipates, as a +30% revenue growth number gets more than cut in half and the continued weakness in the core US model rears its ugly head. In that context, a peak margin gets slashed, McDonald gets fired and the company sees a major restructuring / cost cutting programme to prop margins and save face… but, not before the stock is trading at 15x a $10 earnings number. Brian still sees 50% downside from current levels.

John Zolidis updates his best Long and Short ideas in Retail and Restaurants to start Q2. This follows a successful first quarter, where his average Short fell 11%, while his average Long was flat. Both compared favourably to his universe, which was down 6%, on average. The key change this quarter sees John turn bearish on TXRH as the business decelerates, margins inflect negatively and consensus forecasts appear too high. Compounding matters, the shares also trade at a premium to historical levels. Additional Short ideas include Cava, Dollarama and Tractor Supply, while on the Long side, he continues to be bullish on names such as Ollie's Bargain Outlet, Sprouts Farmers Market and Walmart.

BTN’s analysis of DOCS’s earnings quality identified several accounting-related factors that have recently boosted growth but appear to be temporary: 1) The boost to sales growth from falling Deferred Revenue may be difficult to maintain. 2) Rising Receivables are helping sales too. With DSOs at historic highs, this growth may be tough to continue. 3) Even with rising revenue, DOCS is still boosting stock compensation as a % of sales which it adds back to non-GAAP EPS. 4) Cash R&D and selling expenses are down as a % of sales and largely flat in dollar terms. 5) Passive interest income added 2 cents last quarter to Y/Y EPS growth. 6) Hefty share repurchases have lapped and taken away this source of 1-2 cents of EPS growth.

NEOG’s share price declined by 29% on April 9th (vs. S&P 500 +9.5%) after the company reduced its FY25 revenue / EBITDA guidance for the second consecutive quarter and the shares have fallen 57% since being added to Alumbra’s high conviction Active List in Jan. In their initiation report, they raised concern that an increase in NEOG’s receivables level combined with a change in disclosure language in the company’s 2Q25 10-Q could be indicative of the company providing extended payment terms to customers in response to intensifying competition. In addition, Alumbra said that NEOG’s margins could be pressured in upcoming periods from the effects of a build-up in inventories combined with ongoing issues ramping up production at its new Food Safety production facility.

Are water industrial stocks defensive? Absolutely not.

Proclamations that the sector is "defensive" and hence a place to hide out in an environment of tariff-induced economic uncertainty are reckless, irresponsible and lack analytical rigour, according to Northcoast Research. Historically, water industrials tend to outperform in bull markets and to underperform in bear markets. Valuation helps to explain why water pure-plays like Badger Meter lag in times of market duress and ahead of a potential downward revision cycle. After all, with the Russell 2000 hardest hit among major indexes, high P/E small caps hardly seem a good place to hide out. A prudent approach for investors looking to play offense is to favour high quality names trading at discount valuations. Examples include Mueller Industries, Advanced Drainage Systems, Gorman-Rupp and Pentair. Meanwhile, investors looking to play defense should look elsewhere.

New CEO Joakim Weidemanis will improve operations and energise growth at JCI, according to Paragon’s analysis which includes interviews with former colleagues who worked with Weidemanis for more than 47 years combined. Sources provided mostly positive feedback (five positive, one neutral, one negative) and agreed that his leadership, integrity, financial acumen and disciplined focus make him an excellent choice to lead the company. Weidemanis actively empowers his managers to succeed and draws on a history of working for global industrial conglomerates to improve operating efficiency, drive growth and divest underperforming assets.

Timber REITs: Timberland holds its value in uncertain times

Timber REITs remain undervalued despite trade policy turmoil, expectations for flat US housing starts and falling consumer confidence. Tailwinds for the year ahead include steady timberland valuations and strong comp sales data, continuing investor interest in US timberland and carbon solutions, and potential increased US wood products manufacturing due to escalating duties (and possible tariffs) on Canadian imports. ERA rates all 3 REITs Outperform, valuing them using a NAV method for land assets and a market-based approach for manufacturing assets. Rayonier and Weyerhaeuser both have target prices of $36, offering ~30% upside, while PotlatchDeltic's TP of $50, offers 25% upside.

ADEA has been swept up in the latest market selling as fears related to tariffs have taken hold even though the company generates its revenue from long-term licensing agreements. ~85% of revenue stems from pay TV and streaming video operators. The remaining portion is from semiconductor companies where tariffs remain an unknown. Q1 was filled with renewals as ADEA tries to leverage last year’s video streaming license with Amazon into new license agreements. Investors are overlooking the resilience of the business and the cash flow ADEA is able to generate this year to further reduce its debt. Hamed Khorsand expects the share price to bounce back when the company reports Q1 results in May. TP $18 (50% upside).

Channel feedback continues to be very positive - identity remains a priority spend and CYBR continues to execute well. SPR has not picked up any hard evidence of customers leaving BeyondTrust over the Treasury Dept breach of compromised API keys. Meanwhile, more channels are confirming increasing instances of Venafi deals in their sales pipelines. This is a change from a quarter ago, when they found interest but less evidence of real sales activity. CYBR’s Zilla acquisition should position the group well to expand into governance and compete with SailPoint and Okta’s OIG solution.

Nvidia’s China outlook clouded by US policy risks

At a time when the market assumed a “grand deal” had been struck between Trump and NVDA, a twist in events again surprised investors with a de facto ban on H20 exports. Meanwhile, Jensen Huang’s visit to China this week appears to continue earning goodwill from Chinese authorities, but ultimately, the company’s future in China lies in the hands of Washington. 86Research takes the cautious view that there is a high probability a full chip embargo will remain in place, even if the two countries eventually reach reconciliation on the tariff front. Given this assumption, the downside risk from an almost total loss of China revenue is likely still not fully priced in.

Emerging Markets

India trumps China

When Team Trump’s “Tariff Liberation Day” exploded across Asia ex-Japan, the impact varied widely from country to country. The worst hit markets were China, Taiwan, Singapore and Vietnam (-20%). But the following markets were relatively unscathed: India (-4%), Indonesia, Thailand and the Philippines. The reason is straightforward: the latter countries have relatively modest exports to the US. Furthermore, some of these countries could stand to benefit from the US-China trade war with a number of companies - like Apple - choosing to relocate their manufacturing away from China. Crystal Shore currently ranks India No.1 in Asia-ex-Japan. A list of their top-ranked stocks (large / mid-cap) is available on request.

The China dividend story

David Scott explores Chinese investors’ growing appetite for dividends. Unlike Japan, where it took a generation for companies to deliver meaningful payouts, China’s path looks very different. The companies are younger and are often still run by the founder who owns a controlling interest. Domestic institutional shareholders are active, rights-conscious, and increasingly reliant on dividends amid falling interest rates and an ageing population. Dividend growth is also seen as a strategic signal - proof that tariffs are not going to derail the business model. Finally, both private and state-linked firms are raising dividends at a surprising pace. David's China dividend plays include Midea Group, BYD, Tencent and CATL.

China Telcos: A rare pocket of resilience

Chinese Telcos saw service revenue return to mid-single digits growth in 4Q24. Despite a blip in EBITDA trend, the industry ended 2024 with 6% earnings growth which translated to higher dividend payouts. Looking ahead, New Street expects further improvements in shareholder remuneration, underpinned by lower capex which has been guided to fall by another 9% in 2025. Amidst the US-China tariff war and thus expected GDP slowdown in China, they view the telcos as being relatively insulated compared to other discretionary industries. For investors who can’t invest in this space, New Street recommends monitoring the developments in China as they see it as a leading indicator for EM telcos more broadly.

RHB Bank (RHBBANK MK) Macedonia, The Former Yugoslav Republic of

The uncertainty in markets has created a buying opportunity in Malaysian banks; unlike China, Malaysia does not seem to be in the “punitive tariff” sights of the Trump administration. Victor Galliano’s top pick is RHB Bank for its deep value credentials and its attractive PEG ratio, combined with the improving post-provision return trend. RHB also scores best on valuation metrics as well as capital adequacy and loan mix, when compared to other Malaysian banks. In terms of balance sheet, RHB has seen improving credit quality trends in its domestic operations even if it has further work to do in its small Thai and Cambodian loan books that account for a disproportionate share of NPLs at group level. RHB’s CoR continued to decline from its 2Q24 peak, with the prospect of credit quality improvements acting as a catalyst for further cuts in CoR.

MediaTek (2454 TT) Taiwan

Richard Windsor says MediaTek’s Kompanio Ultra chip sets a new standard for the high end of the Chromebook market and looks to be merely a stone’s throw from Intel and Advanced Micro Devices facing another newcomer in the PC Market. The biggest winner will be Arm, which will see its penetration of PCs accelerate and it will earn higher royalties from MediaTek which buys the processor design and licences the IP. This is neutral for Qualcomm because competition in this space is healthy and will keep the firm on its toes and push it to continue to lead when it comes to performance. INTC and AMD are the real losers here as the x86 architecture looks increasingly obsolete.

Macro Research

Developed Markets

The rise of the multipolar currency regime

According to Wolfgang Münchau, France and Germany disagree on how to respond to Donald Trump's tariffs, the first risking and the second tempering. France is ready to single out digital services for retaliation, the German outgoing government says everything but digital services. Meanwhile, Friedrich Merz looks for opportunities to conclude trade deals with the US but also other countries around the world. Wolfgang notes that the Trump administration’s sector-level approach to tariffs is proving erratic, which could snarl up supply chains and lead to inflationary pressures. He points out that a world that divides in global tariff zones is not a world in which a single currency will dominate – prepare for the multipolar currency regime.

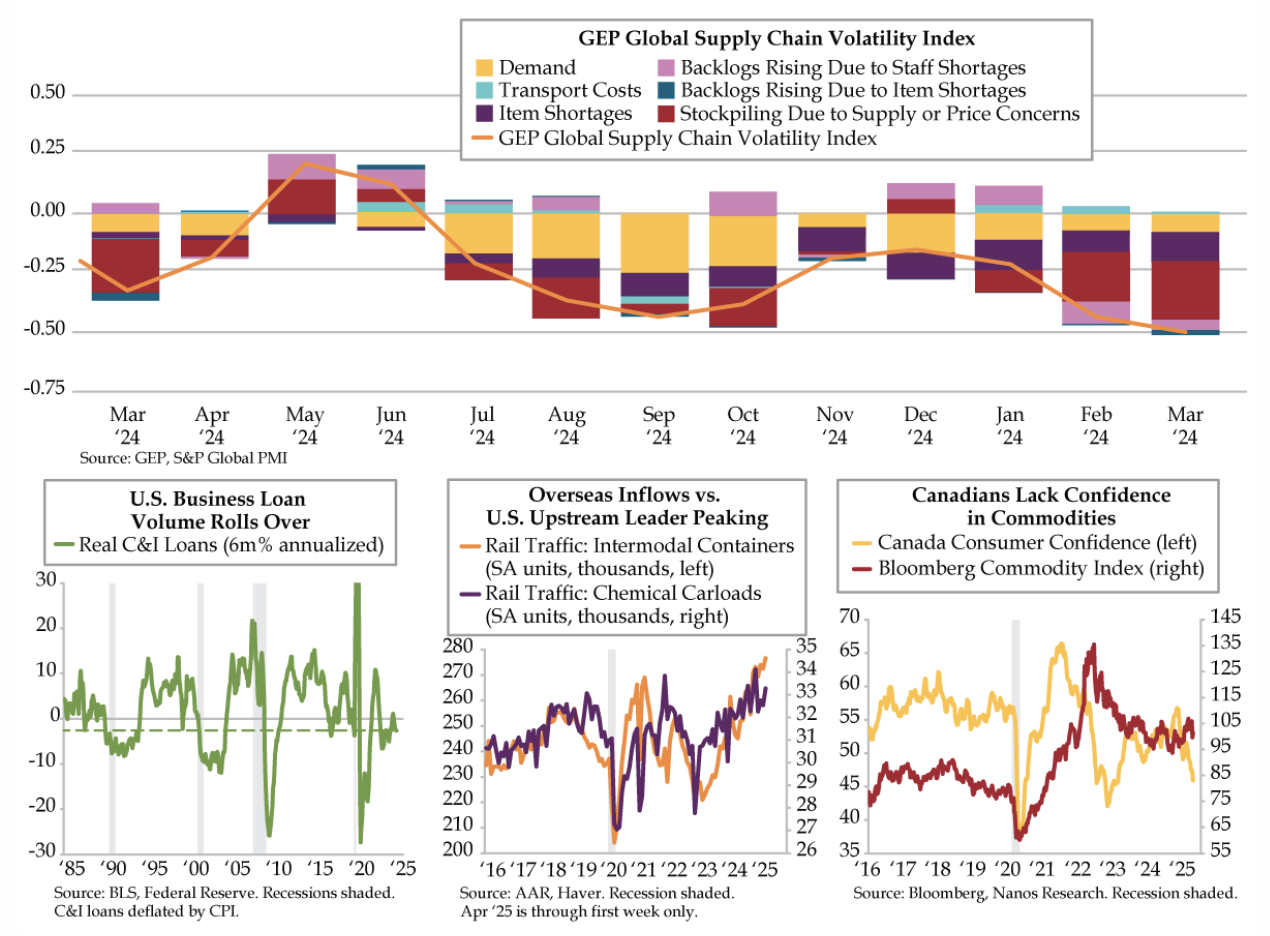

Disinflation despite the tariff terror

March’s Global Supply Chain Volatility Index reflected the most excess capacity since the covid-19 pandemic, declining for a third straight month to -0.51; driving the slowdown was a decline in stockpiling behaviour to levels not seen since 2016 as well as ebbing demand, particularly in North America. Real C&I loan volume channelled the global narrative, with a December topping in upstream chemical rail traffic flagging a cooling in downstream US industrial activity. The precipitous falloff in Canadian consumer confidence—the lowest level in two years—tracking a rollover in Bloomberg’s commodity index, echoed the theme. While Asian supply chains bucked the trend, validated by a boost in incoming US container traffic, that is unlikely to last.

US: Top of the game

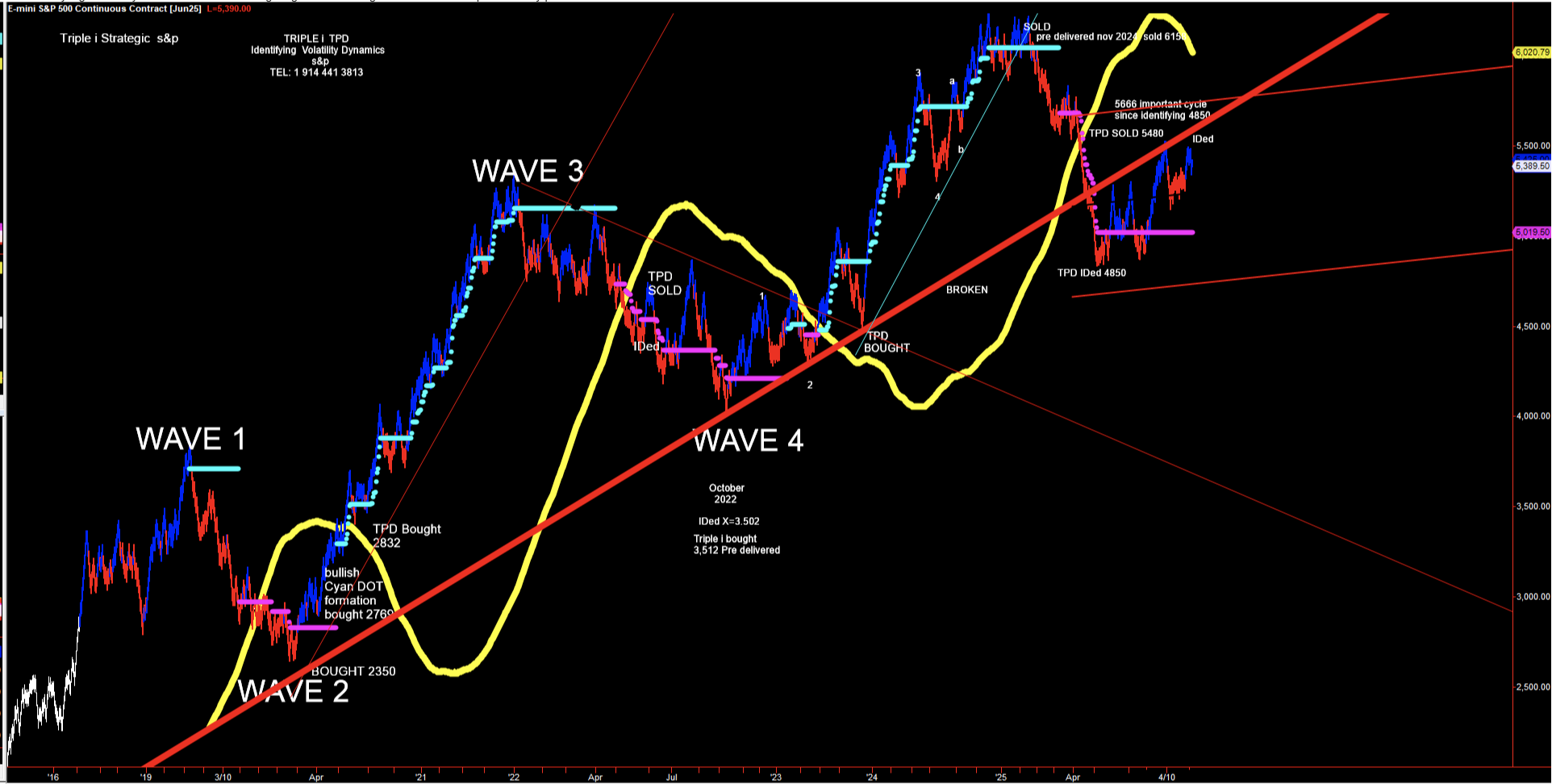

Triple i identified the top in the S&P providing their global clients the acumen to sell 6158, while the market was still accumulating large longs at a generational top. The closing ratio continuously reiterated a zero-value status above 6158, helping to define an initial profit-taking support level at 4850, while the index was trading at 4891. The sells on the way down at 5581 & 5481 ruptured significant multi-year ratios which precisely retested 5528.75 before reversion set in. Additional resistance levels were noted at 5666 (major) and 5780 (significant). Closing beneath 5200 evokes a rechallenge of sub 5k. In currencies, USD/ZAR was one of Triple i’s performing pairs this year. Buy signals at 17.62 and 18.00 targeted 19.94, with price reaching 19.9353.

US: Trump’s permanent tariffs

Like the president’s 10 percent across-the-board baseline tariffs, Stephen Myrow sees sectoral tariffs, expected to be imposed at the 25 percent level, as intended to be permanent rather than leverage points for negotiation. Singling out certain industries aligns with Trump’s long-standing economic vision of reshoring domestic manufacturing in key sectors of interest. Trump has already instituted steel and aluminium tariffs and late last month announced duties on automobiles (in effect as of last week) and automotive parts (set to take effect May 3rd). Pharmaceuticals and semiconductors are poised to be next… Stephen says the line may be different for various sectors. Given the likelihood of these well-telegraphed tariffs being imposed in the coming months, time will tell if and when Trump has had enough medicine (or has run short on it, as the case may end up being due to the pharma tariffs).

US: Why have real yields risen if a recession is being priced in?

Manoj Pradhan ponders the question, going into detail on five hypotheses: plumbing; the structural end of US exceptionalism; the significant dilution of the reserve currency status; a Truss-like shock from fiscal policy (which has Manoj’s full approval as a reason); and an EM-like loss of faith in the administration. He recommends staying long 10y and 30y bonds. His reasoning is that the fiscal news would only show up later in the summer as the fiscal balance/issuance will deteriorate passively as a recession gets priced in and a massive reconciliation budget would be passed only by summer.

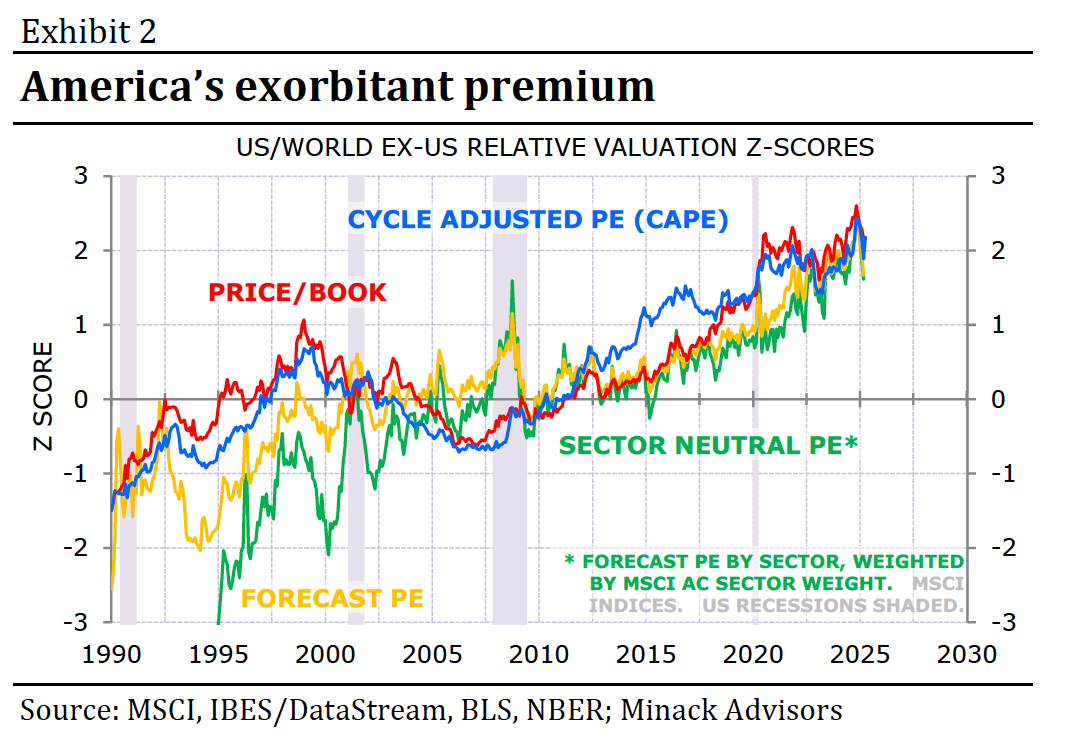

The new Trump trade: US underperformance

Gerard Minack has predicted a major peak in US equity returns relative to the rest of the world. What he hadn’t expected was the Trump Administration to behave in a way so detrimental to America’s own interests. Investors will have little edge trading volatility in the short term unless they’ve accidentally been added to a White House group chat. Gerard expects long-term growth to be harmed by uncertainty, misallocation of capital due to tariffs, lower population growth and attacks on institutions. The US is undergoing an adverse supply shock whereas the rest of the world is seeing a demand shock; whilst other countries can simply loosen policy, the Fed has no clear solution. The US premium is being questioned, especially relating to equities, as the country’s status as the safe haven hegemon. Prepare for an extended period of US asset underperformance.

Japan: Shelving the stimulus

The Ishiba government indicated that it would not pursue a supplemental budget during the current Diet session, in part due to uncertainty about the impact of US trade policy. Although some Liberal Democratic Party lawmakers wanted a stimulus package before upper house elections, shelving a supplemental budget allows Prime Minister Ishiba Shigeru to sidestep a contentious debate about fiscal policy; polls suggest that the public does not necessarily want a stimulus package anyway. Meanwhile, Tobias Harris points out the question of a consumption tax cut — raised as part of the stimulus debate — has divided the opposition, potentially improving Ishiba’s position. With stimulus discussion on hold, the prime minister can now focus on negotiating with the Trump administration; depending on the latter’s demands, Ishiba may still have to engage in some contentious negotiations with domestic constituencies to secure support for concessions, but he has bought himself some time.

Emerging Markets

Argentina IMF deal is as good as it gets

The government and the IMF have just signed an important four-year EFF programme. In a nutshell, the announcement includes the lifting of almost all capital controls, the elimination of the export FX blend, the flexibilisation of the FX access for imports, the introduction of an FX band whose initial ceiling is almost 30% weaker than the current official exchange rate and which includes a free floating regime inside the target band, a restrictive monetary scheme, and a reaffirmation of the fiscal commitment among others. Against these announcements, the IMF provided substantial frontloaded support, which will be supplemented by other IFIs. The programme includes NIR targets as performance criteria. Marcos Buscaglia thinks the programme is as good as it could get in an election year and is thus positive for the credit. The main downside risk stems from the political fallout of the short-term increase in the inflation rate.

Bipolar Cambodia

Jonathan Anderson’s latest report examines Cambodia’s unique banking sector. The dollarised, fast-growing and largely foreign-controlled sector has deepened financial inclusion and credit success, but it has also attracted unusual players due to low barriers and insufficient regulatory scrutiny. The end of the covid-era loan moratorium in 2023 revealed underlying vulnerabilities that had been masked for years and provisioning across the sector remains dangerously low despite visible credit stress. Regulatory decisions also raise concerns over moral hazard and the overall credibility of bank bad asset disclosures. Some investors rely too much on the perceived fail-safe that the banks’ parent companies will step in if needed, but the ownership structures of many of the banks prevent anything beyond limited systemic support.

China: Import ratio now the lowest since the 1990s

Paul Cavey notes that China’s exports through March were solid, but not so strong as to suggest big front-loading. He says that the real standout is the import ratio dropping to a new post-1990s low. The trade surplus upsets Trump. Equally though, weak imports limit China's appeal as a market for others looking for an alternative to the US. On a trend basis, exports are firm. But that is clearer in volume and CNY terms than when calculated in USD. While US exports rose at the end of last year, they have now moderated again. Overall, China's data don't show the lift evident, for example, in Taiwan's trade statistics this year.

Colombia: Rate cuts on the way?

According to Enrico Vicentini, given the sharp movements in external markets—particularly in the US rates market, where significant increases were observed alongside a clear steepening bias—it is notable that IBR swap rates outperformed on a relative basis. In contrast, TES bonds once again experienced upward pressure on their yields, more in line with external developments, which may suggest light positioning in the swap market, typically dominated by offshore investors, judging by the relative price action. As a result, spreads versus USD OIS swaps narrowed considerably, in line with other economies in the region and consistent with the narrative of “US Exceptionalism” losing momentum. On the domestic front, inflation came in slightly below consensus, which could support the case for resuming rate cuts at the next Banco de la República meeting.

Teneo

Ecuador: Noboa under the microscope

With 97% of ballots counted following the presidential run-off, President Daniel Noboa had won 55.65% of the vote, comfortably defeating his leftist rival, Luisa Gonzalez. Noboa therefore secures his first full four-year term having served out the truncated term originally won by Guillermo Lasso. Noboa’s National Democratic Action (ADN) party will have 66 out of 151 seats in the unicameral National Assembly but has supposedly already secured the support of an unconfirmed number of the nine-strong Pachakutik (PK) indigenous bloc and will probably gain additional votes from the Social Christian Party (PSC) and individual legislators. Gonzalez’s Citizen Revolution (RC) party will have 67 seats, but may well experience divisions and disarray after this new defeat. If governability appears more solid than under recent governments, the detail and direction of Noboa’s always-vague policy plans will now come under scrutiny.

Can South Africa catch the critical minerals train?

Despite having an endowment of 30% of the world’s critical minerals, South Africa is at serious risk of missing out on the increased demand due to inadequate planning, policymaking and strategic positioning. There is no coherent critical minerals strategy in place and Peter Montalto cannot see the nation offering anything meaningful to the US when it comes to trade talks. Significant investments, political will and policy reforms are needed to achieve Ramaphosa’s aim of bolstering the country’s raw materials strategy. The next G20 meeting is nearing and the new Department of Mineral & Petroleum Resources (DMPR) needs to move with greater speed in finalising the critical minerals strategy. It must aim to crowd in support and investment from the Global North (including the US) and take advantage of local opportunities such as the SA renewable energy masterplan implementation, the existing project pipeline and the Junior Miners‘ exploration fund.

ESG

Finding green diamonds in the rout

Whilst the world shakes in volatility in the face of the tariff war, the Sustainable Market Strategies team try to find ‘green diamonds’. Their strategy favours stocks with limited exposure to the US and the tariff war, defensive themes that will be less affected by a recession, and names that are focused on services in countries outside of the US. Some of the ideas include NextEra, a stable company operating in the renewable space with long-term PPAs, and First Solar, which does not fit the bill of a defensive company but is one of the few solar manufacturers that does not rely on China. The engineering sector is also of interest; whilst sector stocks recently reacted sharply to recession risks, many of these companies have segments that are relatively recession-proof. Suggested names include AtkinsRealis, Stantec and WSP.

Commodities

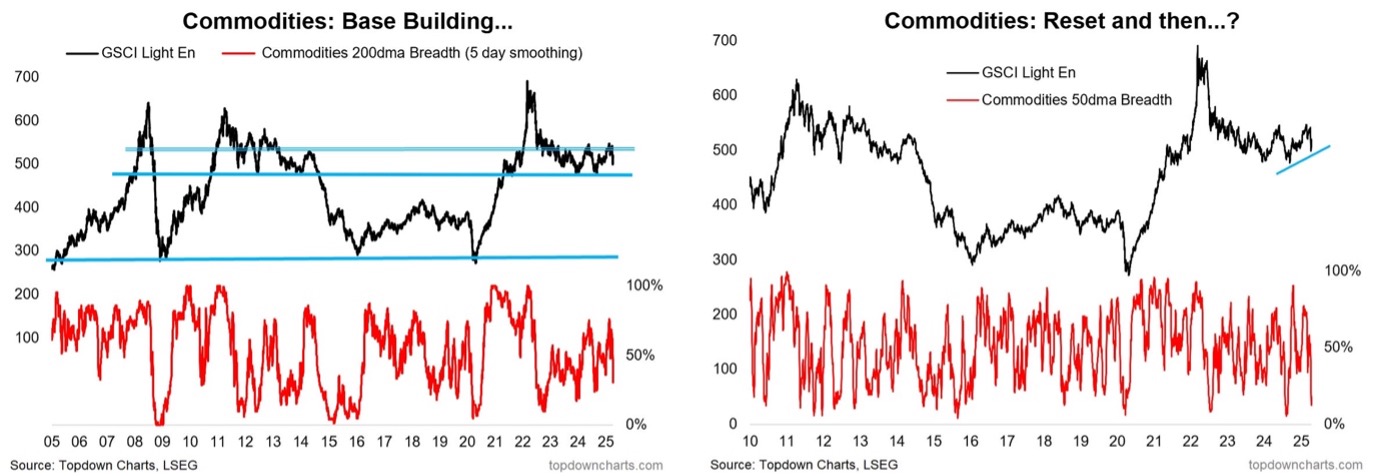

I want to break free

Callum Thomas points out that commodities have pulled back from a key resistance level, yet shorter-term have put in a tentative higher low (from oversold conditions). The bigger picture shows that the cyclical basing process is still in progress (hence, retain a bullish bias). Callum says that one needs to keep a close eye on commodity technicals, particularly in case of global growth surprises at a time where pessimism rules. Meanwhile, tariff tinkering saw commodities initially pulling back from a key resistance level, but for now as of last week's Tuesday low have rebounded from oversold conditions (50dma breadth); and put in a short-term higher low. If commodities can rally from here, it may well set the scene for a breakout from that long-standing trading range.

Iron ore: In the midst of (tariff) war

Despite intraweek price volatility of US$7-8/t swings to the downside and back up again, SGX 62% Iron Ore futures were little changed at US$97.40/t CFR China compared with the previous week. According to Atilla Widnell, there's little else the US administration can do to put direct pressure on the Chinese economy. Sino-centric commodity and financial markets have begun to price-in greater expectations of interest rate & RRR cuts and fiscal stimulus injections. Any nod, hat-tip, wink, and/or indication of expansive fiscal stimulus could send industrial metals soaring; updating Atilla’s short-term target to US$100.50-102.58/t CFR China. Currently he expects that volatility in China-centric industrial metals futures markets will largely be dictated by tit-for-tat trade measures between global superpowers… If global trade measures remain in-situ, Atilla believes this increases the prospect of Chinese authorities revisiting expansive fiscal & monetary stimulus to defend the domestic economy; revising his medium-term outlook to US$95.70-107.84/t CFR China for Q2 2025.

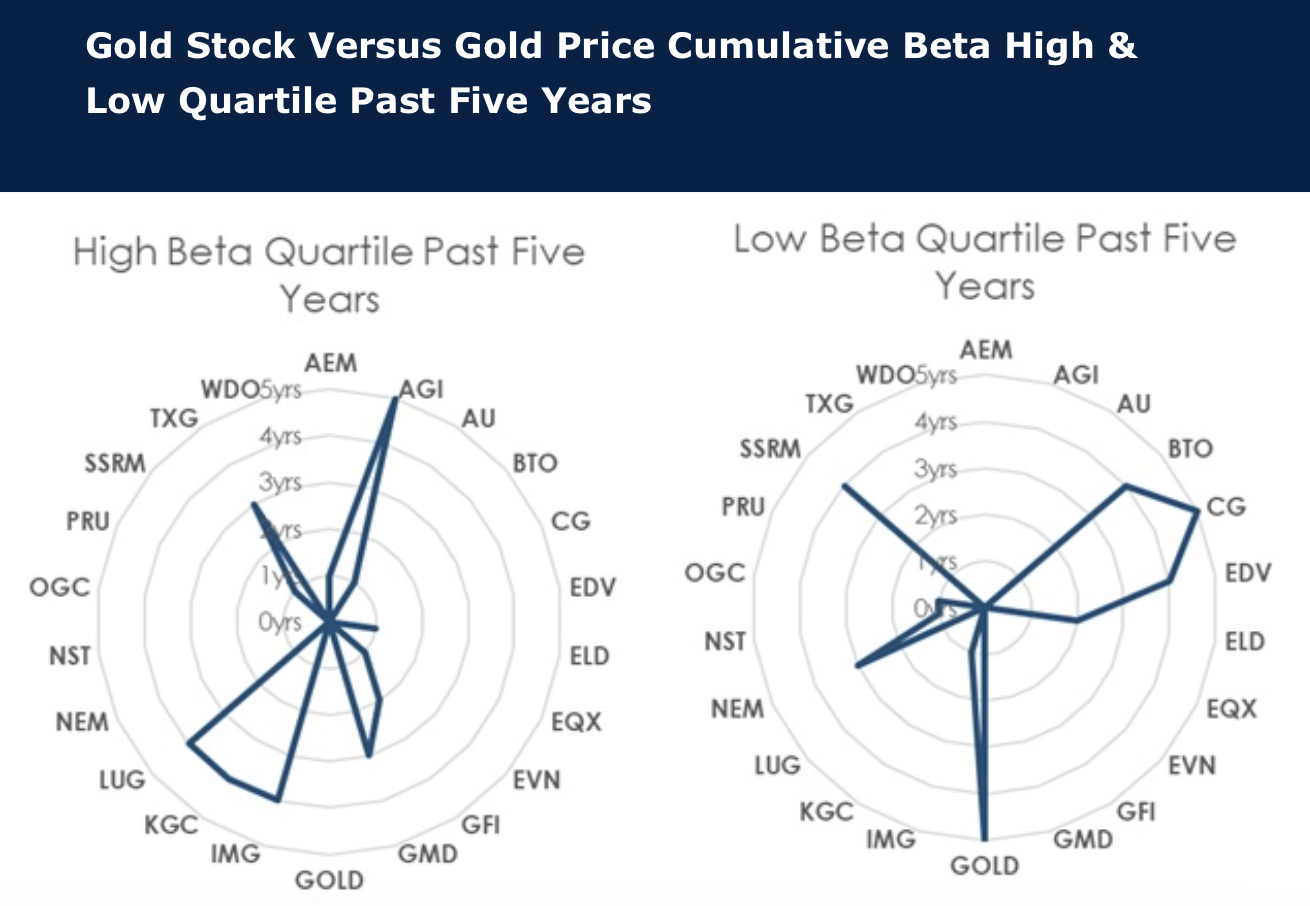

High beta gold stocks outperforming peers

The Global Mining Research team research the correlation of stocks to the gold price and the beta of those stocks. The stocks with consistently high beta to the gold price over the past five years are Alamos Gold, Genesis Minerals, IAMGOLD, Kinross Gold, Lundin Gold and Torex Gold Resources. Stocks with a weak beta to gold price over the past five years are B2Gold, Centerra Gold, Endeavour Mining, Barrick Gold, Newmont and SSR Mining (except 2025), each with mine or management issues, heightened risk or M&A troubles. Market preference for gold stocks appears to be more driven by investor perception rather than quantifiable valuation or sensitivity measures, and investors are preferring stocks with “issues” and aren’t seeking deeply discounted cheap stocks. Preferred gold stocks are BUY-rated Agnico (delivery and lower-risk portfolio), Kinross (risk reduction and execution), Equinox (transitions from project development to cash generation), IAMGOLD (Côté ramp up and derisking) and Lundin Gold (FDN continues to outperform).

Pulp price pessimism

While NBSK pulp import prices have barely budged in China since early March, the futures have been telling a different story. Prices for the dominant Shanghai pulp contract (now July) have plummeted from a $732 equivalent at the end of the Lunar New Year holiday in early February to $638 on Friday 11th April. Prices have not quite reached the lows of 2023, but they are heading there quickly. The ERA team expect import prices to fall in coming weeks. As China is the largest global market for pulp, representing about one-third of World-20 volumes (which are ~80% of global trade), prices in China have typically set the direction for other markets, but it’s unclear if this will be true going forward, as the 145% US tariffs and the 125% Chinese counter-tariffs take effect.