Company & Sector Research

Europe

Woozle Research

Woozle’s latest channel checks reveal European LFL sales grew DD Y/Y in Q3, driven by improved product availability and heightened demand. North America saw a modest LSD LFL sales growth, with foot traffic increasing but cautious consumer spending. Asia’s LFL sales grew HSD Y/Y, fuelled by big-ticket purchases, notably footwear, despite some stock shortages. Terrace-designed footwear continued to be the top performer. Pricing and discounting have stabilised as inflation eases. Sambas and Gazelles showed no signs of slowing down with most stores reporting strong demand. ADS’ Performance line remains the best-performing apparel category.

Fighting Financials

Fighting Financials have been long-standing buyers of the bonds of IPF. With the 9.75% 2025 SUNs now largely refinanced, the team see value in the 12% 2027 GBP (8.9% YTM-1) and the 10.75% 2029 EUR SUNs (8.5% YTM-1). In FFL’s view, the market is overlooking 1) the anti-fragile nature of IPF’s balance sheet, comprising high-velocity short-term loan assets that have a track record of deleveraging rapidly during economic stress, as well as 2) IPF’s conservative provisions and 3) the benign employment backdrop. Ultimately, credit investors in IPF can still enjoy equity-like returns for what is a defensive and modestly levered (sub-60% LTV) asset. Next key catalyst 3Q24 Trading Update scheduled Thursday 24th October.

Intron Health

Intron has conducted a foundational analysis that investors can refer to over the next 18 months as SAN releases at least 15 P2 & P3 pipeline readouts. They highlight the upside potential from every single readout and show that just 4 drugs could add €18/share. In addition, the likely Consumer Health spin in Q4, the tolebrutinib overhang being resolved and a strong COPD launch sets the group up for a strong 2H24 and even stronger 2025. Intron increases their end-2025 TP to €120.

Global Mining Research

With the Golden Age, when copious amounts of cash was returned to shareholders, now a distant memory, GMR examines where the diversified miners are, in terms of existing and prospective valuations, free cash flows, as well as exposure to preferred commodities. Averages are EV/EBITDA 5.2x, FCF Yield 7.2% and Dividend Yield 4.8% for 2025 on GMR forecasts (iron ore US$115/t, copper US$4.20/lb), with P/NPV10 a reasonable 1.0x. Cash + capex costs range from US$2.49/lb for BHP to US$3.89/lb for South32, on a copper equivalent basis. GLEN is upgraded to Buy, offering reasonable value with good FCF, with AAL reduced to Sell following share price run to £24.

ResearchGreece

The Greek TSO (51% owned by ADMIE) reported strong Q2 results reflecting higher electricity demand and much higher interconnection revenues. Revenues/EBITDA/Net Income grew by +22%/+24%/+30% Y/Y. The strong set of Q2 numbers and growth rate were no different to Q1, but the 45%-60% valuation discount against EUR TSOs remains. The Greek TSO is implementing one of the biggest interconnection capex plans in Western Europe. Therefore, higher RAB and dividends flowing will eventually scatter investor concerns over the corporate structure and regulatory inefficiencies. TP €4.0 (65% upside).

North America

280First

AI driven 10Q / 10K text analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market, ideal for idea generation and portfolio monitoring. Recent alerts include: 1) Broadcom - VMware concerns re. the loss of “significant” customers. 2) Avnet - more benign competitive environment. 3) Guidewire Software - may need to reduce prices or change pricing model. 4) Hewlett Packard Enterprise - more positive on near term growth.

Huber Research Partners

Douglas Arthur raises his Q4 adj. EPS estimate to $1.10 per share (+34% Y/Y). He anticipates significant profit upswings in both DTC and Content (Studios) to more than offset continued weakness at Linear, lower profits at Sports and softness in Parks. In addition, given no Hulu hit in non-controlling interests and expected lower International Parks profits, adj. EPS should benefit from a lower deduction from non-controlling interests. The stock price has broken its lengthy downtrend with Parks weakness largely baked in, while future hotel bookings suggest a turnaround, a few quarters out. Box office results have been very favourable and the slate is strong. DTC is doing fairly well and the upside profit contribution could be significant in FY25E and beyond.

R5 Capital

Amazon's aggressive pricing will likely have implications across retail

Consumer Discretionary / Staples

R5’s online pricing survey between AMZN and Walmart reveals shocking results - its one time purchase price basket was lower than WMT by 9%, which ballooned to 22% when they included all the discounting. With WMT generally considered to be the price leader, when R5 surveys retail stores, the incredibly sharp pricing by AMZN online could easily turn the holidays into a discounting jungle. Their research also reveals continued pressure on consumers and they believe the holiday selling period could be difficult for many retailers both from a revenues and profits perspective. They would exercise caution adding to positions, with the exception of AMZN, as it will likely gain share and it is the aggressor with the price cuts, suggesting that it is accounted for in its guidance.

Kailash Capital Research

Having successfully passed on significant price increases to its customers RL's earnings and cash flow have soared. However, macro concerns about the health of the luxury goods industry have weighed on the company’s valuation which now sits at nearly a 9% FCF Yield, cheaper than 90% of other large cap stocks. If the company could boost its gross margin to the traditional 70%+ range for a luxury retailer there could be significant upside ahead. Specifically, for each 100bp increase above its current 67.2% level, annual EPS would rise by ~$0.75. Using a modest 12x multiple, that would suggest that each 100bp boost in RL’s annual gross margin could cause a $9 increase in its share price. If the firm merely hit parity with peers that gives $27 of upside using what may turn out to be a very depressed multiple.

Cerundolo Investment Research

The stock appears to be in the initial innings of forming a multi-year base with positive money flow.

Paragon Intel

Paragon’s analysis of CEO Bryan Hanson includes interviews with ten former colleagues who worked with him at Zimmer Biomet, Covidien and Medtronic for 110 years, combined. Sources (6 positive, 2 negative, 2 neutral) focused on his strengths as a builder of culture and teams. He begets loyalty in those who work with him, has a high level of transparency and strong communication skills. In fact, his focus on company culture may overshadow other areas, as he and those around him can become absorbed in the excitement of cultural transformation and big-picture ideation at the expense of more disciplined strategy. All the same, Hanson will take a portfolio management approach to SOLV, honing core areas of the business through both divestments and tuck-in acquisitions.

BWS Financial

The slowdown in system placements and acceptance has continued, while the challenges faced earlier this year are not easily fixed, according to Hamed Khorsand. SYM has only added one new site on its location list (Cullman, Alabama) in recent months. Since the company recognises revenue on a percentage of completion basis it is very likely revenue from Cullman was already recognised in prior quarters. As a result, Hamed believes the latest move higher since the stock dropped to ~$18 creates another opportunity to sell as investors realise growth is not what is currently expected by the Street. 12-month TP $10 (60% downside).

Behind the Numbers

The stock features in BTN’s 3Q24 Focus Risk List which contains companies they believe have a higher risk of reporting an earnings disappointment based on earnings quality. ARW is guiding to its lowest quarter in years on adj. EPS of $2.10-$2.30 along with flat sales. BTN sees considerable risks for sales, earnings and cash flow. ARW’s adj. EPS beat of 62 cents last quarter had considerable help from one-time items. It picked up 29 cents by reversing bad debt reserves, another 2 cents from bad debt issues, 7 cents from falling depreciation, 12 cents from interest expense coming in below forecasts and 8 cents from interest rate swaps. This looks like a simple story of some unsustainable earnings drivers.

Sidoti & Company

The strategy to diversify into higher-growth markets is producing sustainably stronger organic growth on top of the company’s historically high revenue visibility and consistent cash flow. Furthermore, the DirecTV / Dish merger provides a new opportunity to gain share for CSG. While Dish is already a long-time customer, DirecTV uses an Amdocs billing platform and as long as AT&T owned DirecTV this was unlikely to change. Sidoti now sees these subscribers as a tangible opportunity for CSG (could double the revenue it currently generates from Dish). Meanwhile, they continue to expect acquisitions to provide an additional catalyst for the stock. TP $74 (55% upside).

Northcoast Research

RCI Rankings: Ohio & Illinois top list with Pennsylvania falling to new low

Since 2011, Northcoast’s proprietary Regulatory Climate Index rankings have provided a valued shorthand for investors seeking to compare regulatory jurisdictions for investor-owned water utilities and their latest update is arguably the most noteworthy yet. Ohio and Illinois top the rankings, while long-time stalwart Pennsylvania dropped to an all-time low and former basket case California jumped to a new high. The 2024 RCI rankings underscore a marked increase in regulatory fluidity, as affordability concerns, volatility in risk-free rates and pitched political division coalesce to drive sharp regulatory divergence.

Japan

Astris Advisory Japan

Shares of NTT have slumped this year as concerns on mobile performance and local exchange profitability weigh on sentiment even as regulatory and political uncertainty lingers. At the company’s recent IR day, management was able to address the former, focusing attention on improvements in mobile and its regional businesses although we will have to wait for the politicians and regulators to address the latter. Large-cap telecom peers have performed much better than NTT, which has expanded the valuation gap with NTT looking much more attractive at 11x FY24e EPS vs. KDDI (14x) and Softbank (17x). NTT has also increased its dividend 12 years in a row and Kirk Boodry does not expect it to stop now. TP ¥207 (40% upside).

Asymmetric Advisors

Billions of dollars needed for PFAS treatment a game changer for Kuraray - the likely explosion of demand for granular activated carbon (GAC) over the next 5 years could transform the company’s prospects. Revenue from its GAC products could rise 2-3x by FY12/30 and generate >¥30bn OP vs. ¥6-¥7bn currently. While the share price has been rising over the last 6 months and is not far off previous highs seen in 2017/18, Asymmetric argues that the scale of the potential benefit to Kuraray is still not well known (if at all). The stock trades on a PER of 11x 12/25E and PBR is 0.87x.

Emerging Markets

Hedgeye

MNSO is a well-managed, tech-infused, Gen Z favourite, global value retailer, so Felix Wang was flabbergasted to hear the company plans to acquire a 29.4% stake in Yonghui Superstores. Is CEO Ye Guofu’s gushing view on Pangdonglai, an innovative new retail concept that Yonghui is experimenting, worth destroying his hard-built global vision for MNSO? At the very least, it throws some uncertainty into its investment story. Felix also thinks consensus forecasts are too high for 4Q24 and 2025. While MNSO will benefit from a rebound in the China consumer, this new deal is an overhang on the stock's valuation, unless the deal is axed by SAMR and / or by shareholders.

EM Spreads

PEMEX bonds an attractive opportunity

Mexico's state-owned oil giant remains highly reliant on government support as it continues to drain cash due in part to the national energy security agenda. With the new administration sworn in, EM Spreads anticipates consistent financial backing and the ruling coalition may be better positioned to implement a financial solution when needed. The potential reclassification as a public company could be a significant positive catalyst, leading to rating upgrades and spread compression. Despite weak 2Q24 results, an unsustainable capital structure and declining oil prices, the prospect of stronger government support makes PEMEX bonds an attractive opportunity.

Galliano's Financials Research

Hana Financial did not make the cut for the Korea Value-up Index announced on 24th Sep as it apparently fell short of the PBV ratio threshold. Despite being excluded from the Index, Hana is Victor Galliano’s core South Korean bank pick for its attractive valuations, low PEG, solid core capital ratio and strong credit quality credentials. He believes it stands out positively on fundamentals and return trends vs. its peers, while there is also potential for its inclusion in a planned rebalancing scheduled in Dec.

Westlake International

Nvidia's H20 remains the top choice for Chinese CSPs

Based on Westlake’s conversations with industry experts, Chinese CSPs remain major customers for the H20 despite Chinese regulators’ guidelines. With speculation the DoC BIS will propose even stricter restrictions on advanced GPU exports to China at its annual review in Q4, Chinese CSPs and leading server ODMs / OEMs are stockpiling H20s in case of potential bans. Contacts estimate the H20 shipment units in China to be ~50k in Q2, ~350k in Q3 and ~400k in Q4, for a total ~800k units in '24. NVDA could potentially see H20 revenue reach $9bn-$9.8bn in 2H24. Chinese CSPs currently rely on NVDA’s GPUs including H20 for training, while deploying a variety of GPUs, e.g. Huawei’s 910B, for inference. Huawei’s Ascend 910B/910C shipments are estimated to grow from 100k-200k in ’23 to 350k-400k in ’24 and 650k-700k in ’25.

Macro Research

Developed Markets

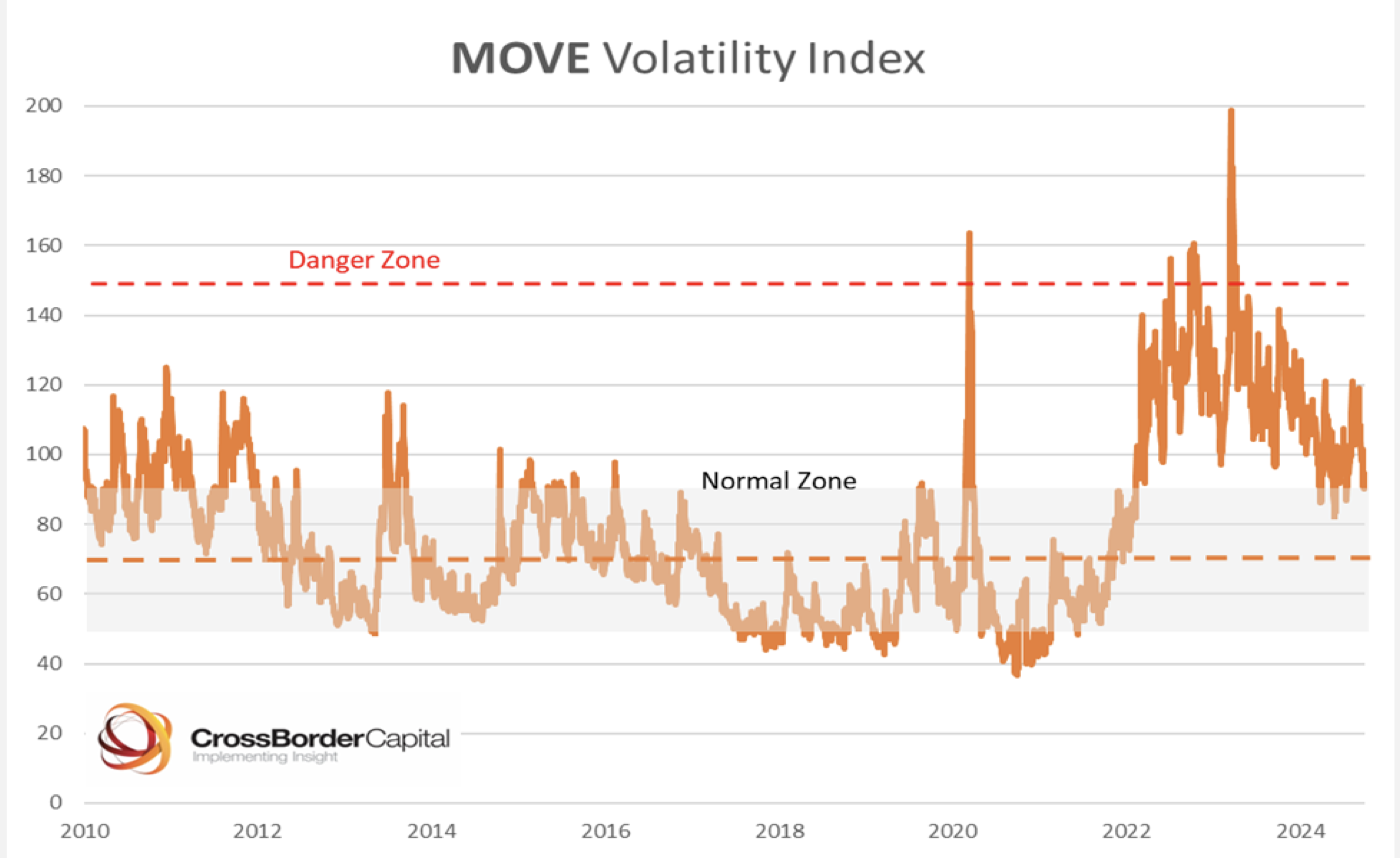

CrossBorder Capital

The hidden driver of global liquidity

Michael Howell’s latest report examines another important source of Global Liquidity, where an increasing multiplier pushes up an expanding collateral pool. He argues that the size of this multiplier is closely tied to falling bond market volatility. Thus, more Global Liquidity drives down the MOVE index of bond volatility, which in turn generates more Global Liquidity in a self-reinforcing loop. Maybe the MOVE index is more important to investors in risk assets than the more popular VIX index?

Aitken Advisors

UK: A rudderless government

To burn all of your political capital within two months of winning the largest majority since Blair’s 1997 victory requires special talent, but Starmer’s government appears to have done it. James Aitken comments that, as a result, hopes for some sort of post-election, end-of-shambolic-Tories re-rating of sterling assets have been dashed. In terms of what this failure means for markets, James tells investors to consider the confusion over the coming UK budget: there have been an equal number of recent briefings on cutting investment versus changing the UK’s fiscal rules. The dysfunction has a whiff of Truss to it. James doesn’t see LDI 2.0 as pending and sees little risk of that, but there’s still a reason why gilts have underperformed since the election. The renewed risk premium on sterling assets is justified; and Bailey’s interview should continue to undermine sterling. Avoid.

Greenmantle

Europe: Budget crunch in Berlin and Paris

In France as well as Germany, upcoming budget negotiations could fracture fragile governments. France’s sovereign risk premium could rise further if Marine Le Pen, the leader of the far-right Rassemblement National (RN), decides to censure Prime Minister Michel Barnier in December. In Berlin, Niall Ferguson expects the Free Democrats (FDP) to exit the three-way coalition of Chancellor Olaf Scholz over budget negotiations this autumn. German snap elections in February or March 2025 would be market-positive. The center-right Christian Democrats (CDU) would most likely emerge victorious and open the door to a slight softening of the debt brake to allow for higher defence spending. In France, however, the risks are to the downside as Barnier braces himself for an exceptionally short term as president.

Eurointelligence

Austria: Kickl’s sweet & sour victory

The far-right FPÖ won the Austrian elections with a solid 28.8%, even more than the polls predicted. In coalition talks, the ÖVP will be the kingmaker: they can choose between a coalition with the far-right or the centre-left. Wolfgang Münchau discusses two likely coalition options: one with the FPÖ, with a prime minister other than Kickl, and a classic grand coalition with the SPÖ and perhaps the Neos. There is also an option of a minority government with a confidence-and-supply agreement in the assembly. For the FPÖ and Kickl, the crucial question could thus turn into a choice between power and principle. If they insist on their Fortress Austria programme with its radical proposals and Kickl as the next prime minister, they won’t get into government. If they open up to compromise, they may lose votes. Power comes with strings attached. The far-right is no exception to this rule.

Quill Intelligence

US: Accept lower rate expectations “promise” at your own risk

A record rise in lower rate expectations has created a burst of euphoria for U.S. households’ short-run economic outlook. However, Danielle DiMartino Booth points out that when a critical mass has formed for future rate cuts, it has historically heralded higher equity volatility, higher unemployment and excess supply conditions, not the other way around. In the University of Michigan’s September data, 55% of consumers expected interest rates to fall in the coming year, a record in data back to 1960, with higher tallies for upper-income and degree holders; notably, five other months have had prints north of 50%, four of which occurred in recession. Prior upswings in UMich lower rate expectations have presaged increases in the VIX, something which has yet to happen in the current cycle; similarly, lower rate expectations cleared 40% in the last three downturns before the unemployment rate began to rise sharply.

Antipodean Capital Management

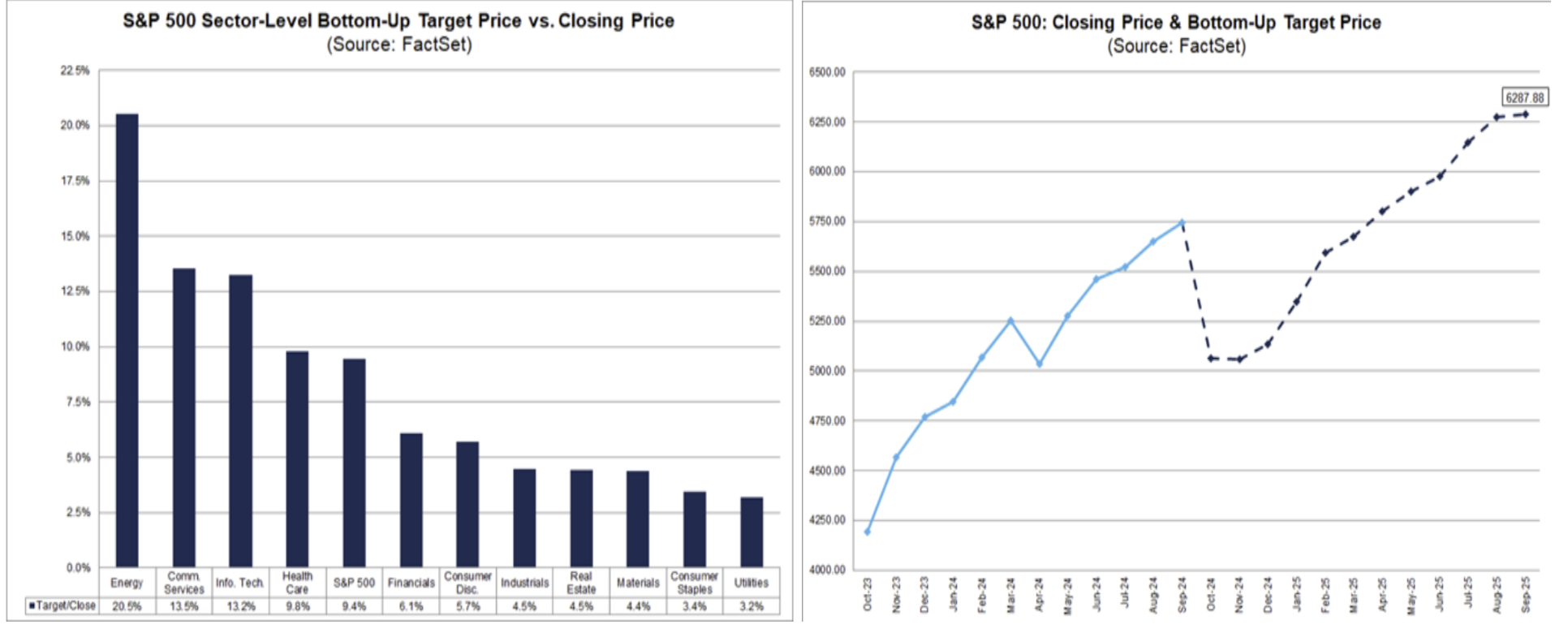

US: Bullish at the wrong time?

Craig Ferguson’s charts highlight the extent of analyst earnings optimism. Chart 1 indicates that analysts expect a 9.4% rise in S&P EPS in the next 12mths, with every sector contributing but energy sector EPS leading the charge rising by over 20%. Is it really possible to see the entire US energy sector record a 20% profit increase in the next 12mths? Global growth has not stopped slowing and downside will only intensify. Furthermore, after holding a 5000 average price target for October 2024, analysts have now jumped well ahead of the S&P’s current level to hold an October 2025 6287 Index target (chart 2). Arguably, right at the wrong time as global growth downside risks accelerate, analysts have increased their bullishness on the S&P to well above current levels. Are they going all in on the soft landing? It certainly looks like it, probably at or near the high.

Emerging Markets

Enodo Economics

China: This ain’t no Japan!

According to Diana Choyleva, Beijing's multi-faceted U-turn on economic policy could mark a watershed evolution of its development strategy towards balanced growth and restored confidence. The demand stimulus includes unleashing greed via equities support and removing dogmatic views towards house price increases. Further fiscal stimulus is expected in October. A holistic strategy aims to address structural demand and confidence issues alongside supply-side reforms. Beijing is signalling that local officials face no negative repercussions if they experiment with policies. China's lack of equity bubble, room for productivity growth and learning from Japan’s mistakes suggest it can avoid Japanification. The growth-focused pivot renews China's appeal to the Global South but won’t change the “uninvestable” narrative in the West. Diana says these structural shifts should provide ongoing support to Chinese equities; the current levels and any market pullbacks are attractive entry points for long-term investors.

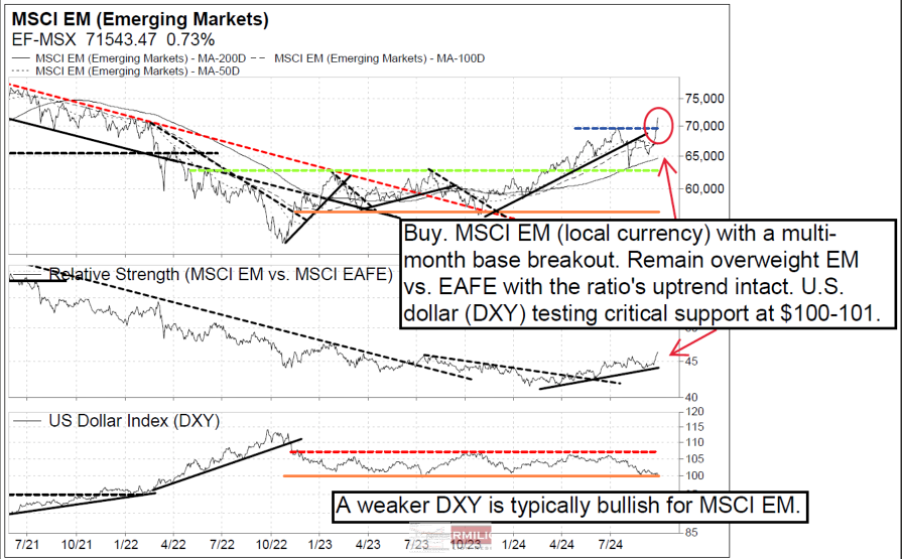

Vermilion Research

MSCI EM breaking out on Chinese stimulus

The MSCI Emerging Markets index (local currency) and EEM-US (USD) are breaking out from their multi-month consolidations thanks to significant Chinese stimulus -- add exposure on pullbacks. The Vermilion team continue to favor EM over EAFE, which has been their view since May. India (SENSEX) remains their lone country overweight, although there continues to be a plethora of countries that are bullish, including South Africa, Philippines, Argentina and Thailand. The Hang Seng is the preferred play on China as it displays a base breakout and RS has been consolidating for all of 2024; the team are monitoring for an upgrade to overweight. Nearly all EM sectors are bullish, with the exception of MSCI EM Energy. That said, the only sectors that display meaningful RS improvement are telecoms, consumer discretionary and real estate, which all have a significant weighting to China.

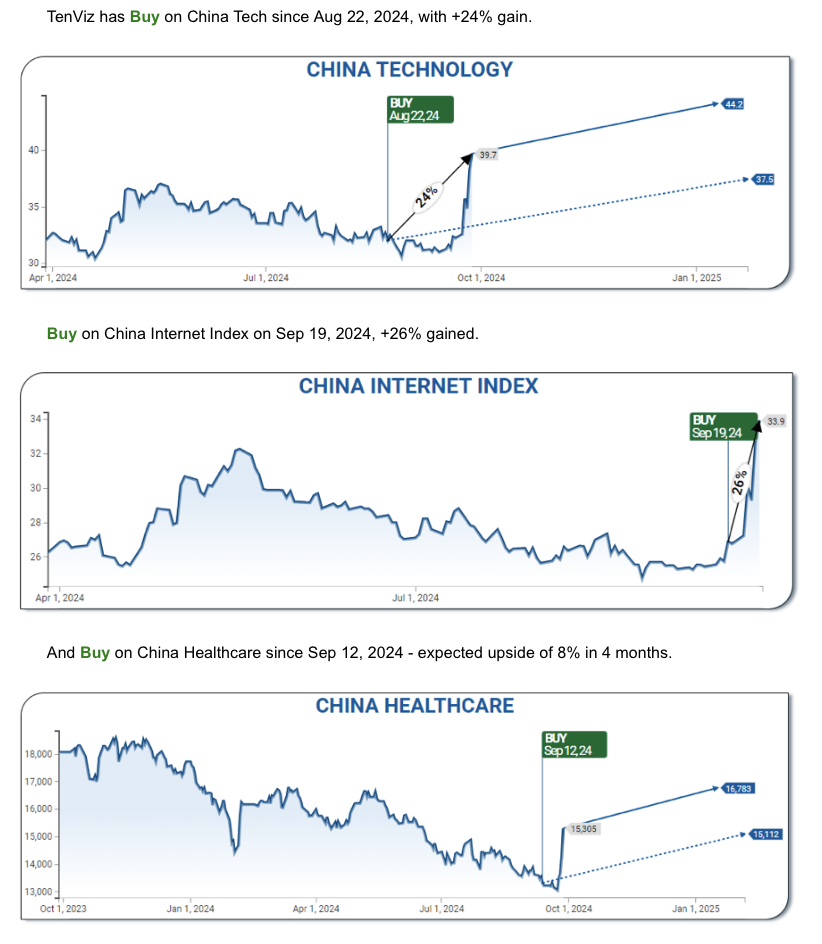

TenViz

China: Unexpected positive developments

Rate cuts and liquidity injections preceded a massive 32% rally within a week. However, Konstantin Fominykh mentions that Chinese stocks were essentially priced for an economic collapse, and capital inflows signaled a turn before the policy shift: BUY on China tech since Aug 22; BUY on China Internet Index since Sep 19; BUY on China Healthcare since Sep 12. Institutional money is flowing not only into major tech names but also into sectors like auto-tech and green energy, highlighting broader market recovery. The rally started within the context of oversold emerging markets. Consistent with a weakening US$, SELL on the trade-weighted USD. Inflows into China align with BUYS on crude oil, uranium ETF, rare earth metals ETF and European luxury stocks.

Pacifico Research

Chile: Slow and steady

Igal Magendzo has modified his base scenario for the path of the monetary policy rate (MPR). While Igal still believes the Central Bank will continue lowering the benchmark rate, he now projects that this will be preceded by a ‘front load’ approach. Nonetheless, he continues to think that from January 2025, the Central Bank will resume a ‘slow and steady’ approach, with pauses, until reaching a neutral rate of 4.25% in June of that year. The Pacifico team has decided to close the monitoring of the tactical paid position in 3m6m CLP/Cámara, as despite having a fair value approximately 15 bps above the market, the current level is almost identical to the entry point, meaning the upside potential is zero.

Emerging Advisors Group

Is Cote d’Ivoire the next Ghana?

Cote d'Ivoire has risen steadily to the top tier of Jonathan Anderson’s macro risk rankings on the back of widening "twin deficits" and an accompanying surge in external borrowing, despite recent export successes. It’s very reminiscent of the situation in neighbouring Ghana a decade ago. Is Cote d'Ivoire at risk of repeating Ghana's subsequent fate of funding crises and forced sovereign default? It’s way too early to tell. Cote d'Ivoire is supported by its latest IMF funding program; export capacity is set to increase further over the coming few years; dollar sovereign spreads were very well-behaved indeed during the market turmoil of 2022-23 that "took out" other EM players, and now we are back in a US Fed easing environment with a weakening dollar, i.e., on balance Jonathan is not looking for significant stresses. But it's worth keeping an eye out.

Greenmantle

Mexico: In AMLO’s shadow

After an unconventional transition, Andrés Manuel López Obrador passed the baton to his successor, Mexican President Claudia Sheinbaum. In a ceremony that highlighted the history of the Mexican left and the battle for gender balance in the country’s politics, Sheinbaum took an oath that did not disappoint her mentor and main supporter. Yet Sheinbaum’s message will fall short in dissipating market uncertainty. She praised AMLO’s legacy and vowed to continue his “national project.” Her key message echoed revered 19th-century reformist president Benito Juárez: “With the people everything, without the people nothing.” Markets will not like this start, even if she is more pragmatic than her predecessor.

ESG

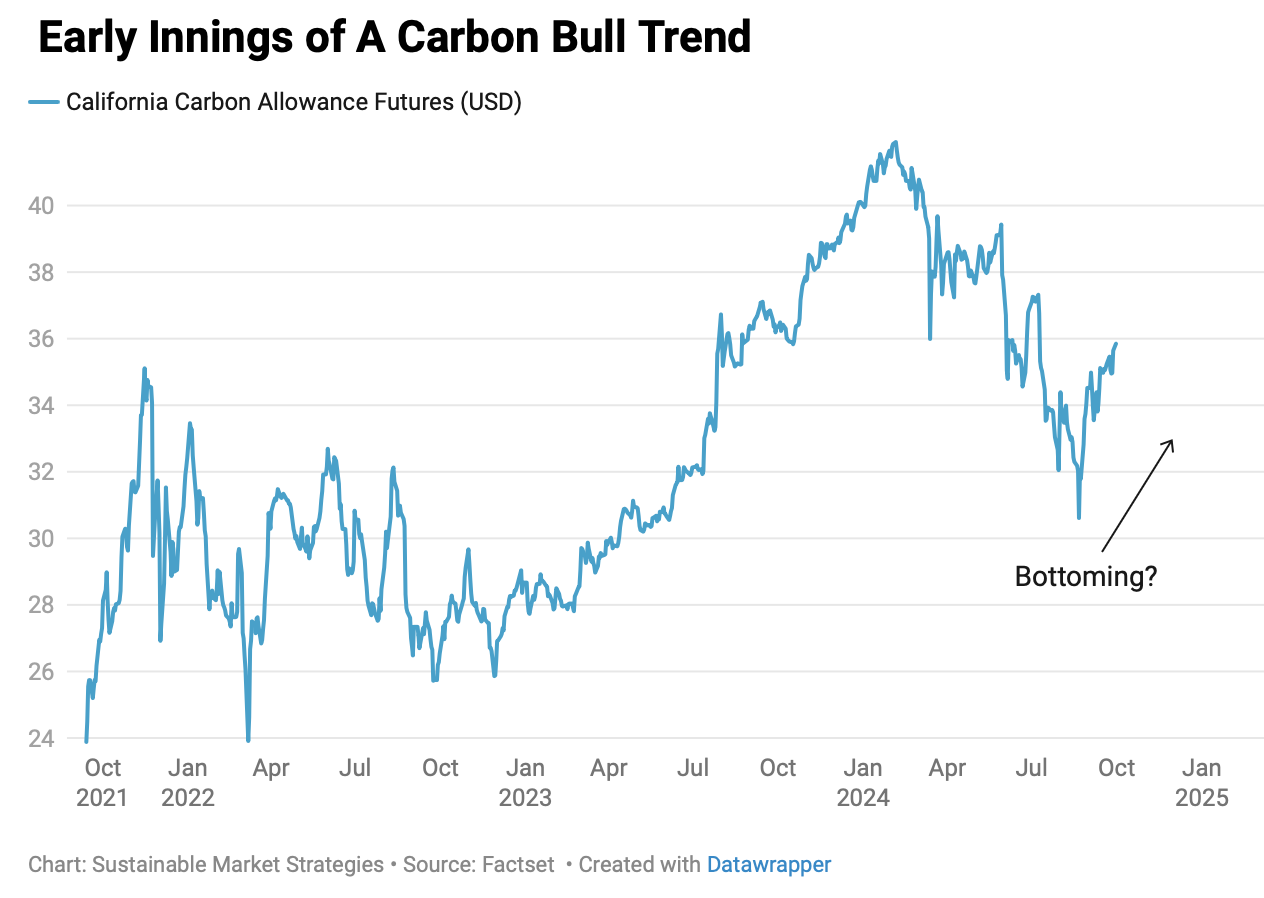

Sustainable Market Strategies

Carbon: The trade of our time

Regulated carbon has proven itself as a liquid and investable asset class. Inflation protection and low correlation to other assets are among the asset’s top financial qualities. Returns over the past year have not been lucrative because a confluence of factors has weighed on prices. Fortunately, most of these headwinds are now reversing, making an excellent entry point, particularly in North America. Carbon investments also offer inflation protection and tend to be uncorrelated to other markets. Ways to get involved in regulated carbon markets include direct participation in quarterly auctions (or via an LP fund) and trading the corresponding futures/related ETFs, such as the Kraneshare California Carbon Allowance Strategy (KCCA).

Commodities

WHB Energy Research

Israel-Iran war unlikely to disrupt oil supplies

William Brown comments that we have arrived at the “moment of truth”, as Tehran has launched multiple long-range missiles into Israel. The odds remain relatively low that oil supplies will be interrupted to any material degree. Famous last words, but this is reminiscent of the Iran-Iraq war where limited damage was inflicted on tankers and international shipping was protected. The price of crude oil actually declined over the course of the war. The international oil industry is extremely resilient. Tanker owners are still willing to carry cargoes into the Arabian Gulf, paying higher insurance premiums. One helpful perspective is to recognize that tankers flows are not actual “flows” that move continuously as if they were pipelines. If a tanker is damaged, that is one “discrete” interruption that can be made up without a material impact on the average MMB/D volume.

WHB Energy Research

Market impact of Saudi production rise grossly exaggerated

William Brown believes the oil market has “overly discounted” the news that Saudi Arabia has abandoned its $100.00 per barrel price target and will increase production to compensate for lower oil prices. Their plan is to begin increasing production by 83 MB/D each month starting in December, boosting output by almost 1.0 MMB/D by December 2025. However, the monthly increment of 83 MB/D is relatively minor, i.e. less than the standard error of estimate of Saudi production. On balance, William believes the market can handle the volumes, and before the end of the year crude oil prices will stage a recovery, assuming economic activity remains on target with his long-standing, moderate growth base case.

CPM Group

Gold: Why is central bank buying down?

In this presentation, Jeffrey Christian of CPM Group discusses the recent practices and policies of central banks regarding gold. He provides a detailed analysis of annual gold purchases and sales since 2000, and the shifts in central bank activity since then. Jeffrey also looks at some of the rumors surrounding central banks' gold activities, debunking claims that they are "aggressively" accumulating gold or planning for a gold-backed BRICS currency. He explains how central banks have actually reduced their gold purchases as prices have risen, reflecting a long-term, price-sensitive approach. The video concludes with a review of recent activity in the gold and silver markets, including CPM Group's expectations for lower prices and buying opportunities in the short-term, and higher prices as the election moves closer and towards the end of the year. Click here to watch. Click here to watch.