Company & Sector Research

Europe

Willis Welby

Willis Welby remains of the view that the UK has plenty of interesting and growing businesses. IHG features in their latest large cap growth screen - it has great financial productivity and is clearly winning market share. Dollar weakness does not help but the implied to Y3 EBITM ratio is just 84. It is too low. Hilton and Marriott are on 135 and 114, respectively. IHG would make sense GBP20 higher than it is now. Other stocks highlighted include QinetiQ (there is a good fundamental story here alongside some very cautious expectations. Despite a Q2 rerating, the implied to Y3 EBITM ratio is still only 65) and GlobalData (the disposal of part of the Health franchise may prove seminal. Management is talking organic growth >10%, margins drifting higher and accretive roll-ups).

Cerundolo Investment Research

Guy Cerundolo flags ABF’s deteriorating model score and yesterday's (5th Sep) break of a 2-year uptrend is negative for the stock.

CEN-ESG

PFD’s ESG score increases to 58.2/100 - the group maintains a significant lead above the F&B sector median. ESG disclosure was supported by SASB alignment, a formal ESG reporting methodology document and ESG disclosure assurance report. Environmental scoring benefitted from first-time publication of a net zero roadmap and TCFD enhancements including an expanded assessment on the acute and chronic risks associated with the supply of key ingredients. Social disclosure saw the launch of a new supplier engagement plan including supply chain mapping data and a new Human Rights Due Diligence framework. Governance scoring reflected continued alignment with the UK Corporate Governance code. Click here to access the full report.

ResearchGreece

MOH’s Q2 results were much stronger than what benchmark refining margins implied for the quarter. This is thanks to stronger gasoline vol & cracks and the higher naphtha-gasoline spread compared to Q1. ResearchGreece upgrades their rating on the stock to OWN IT with a TP of €28.5. The share price is down -15% since the government imposed another windfall tax on refineries in Jun. At 3.3x clean EBITDA 2024-2025E, there is enough valuation upside (+30%) to compensate for the low refining visibility and enough cash flow to support a solid dividend yield out of 2024 earnings (min. 5%) without raising net debt.

Dragoneye Research

Since Dragoneye's initiation in early Jun, the share price has dropped by over 25%, offering a significant short opportunity. This decline was driven by several factors: persistent cash flow issues, concerns about past management incentives and motivations, and a growing recognition that aggressive accounting practices have inflated profits. These issues culminated in a significant cash downgrade following the first-half results. Dragoneye's exclusive 49-page report highlighted all of these problems. A recent follow-up report, after the first-half results, further emphasizes potential downside risks if more questions are raised about the company's use of factoring. Factoring appears to have boosted an already weak first-half cash flow figure, but this was not disclosed in the company's financial statements.

North America

Kailash Capital Research

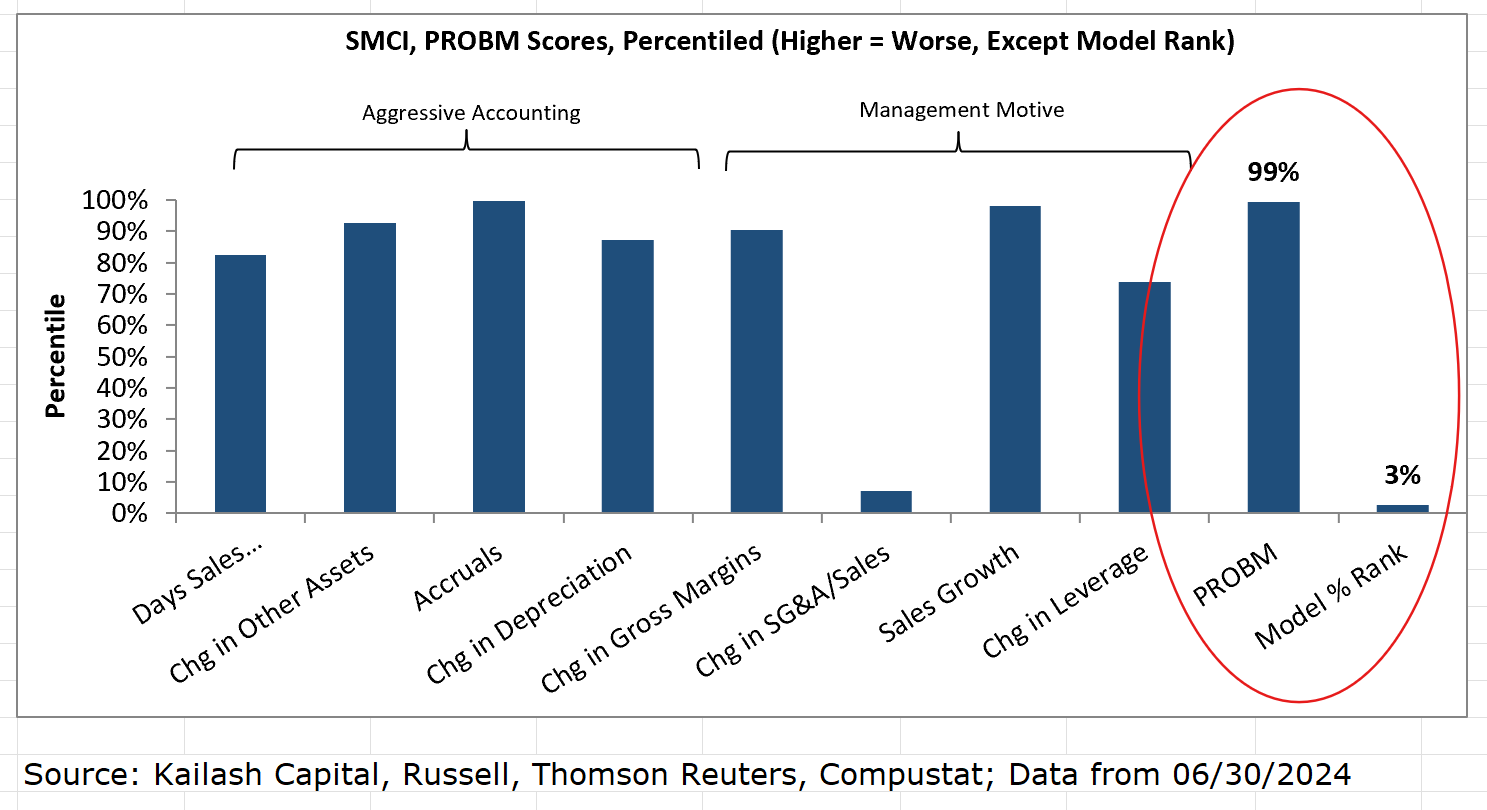

A systematic approach to identifying potential earnings manipulators like SMCI

SMCI shares fell nearly 20% after the company delayed the filing of its annual report and Hindenburg Research alleged “fresh evidence of accounting manipulation”. Interestingly, SMCI features in KCR’s S&P 500 Earnings Manipulator list, which includes stocks in 1) the worst quintile based on academia’s PROBM formula and 2) the bottom 20% of KCR’s ranking methodology. Other companies flagged include Advanced Micro Devices, Tesla, and Xylem, with Block and Emerson Electric added last month. Over the past 14 years, KCR’s Research Short Portfolios have been valuable for spotting potential risk flags and generating short ideas. To access the return summary for these portfolios click here.

Quo Vadis Capital

John Zolidis does not believe that FIVE’s current troubles are caused by deeper structural issues in the market and is confident the company will regain its merchandise discipline. He also applauds management’s decision to slow unit growth, which should lead to better ROICs, increased FCF and enable improvements in execution. Increased labour hours in the store will create pressure on the SG&A ratio, but it is the right thing to do. While the multiple for the stock may not reflate to the historical average of ~18x EV/EBITDA, it currently trades at just 8x. John expects the market to assign a much higher multiple as performance improves and sees 80%+ over the next 12 months.

Verbatim Advisory Group

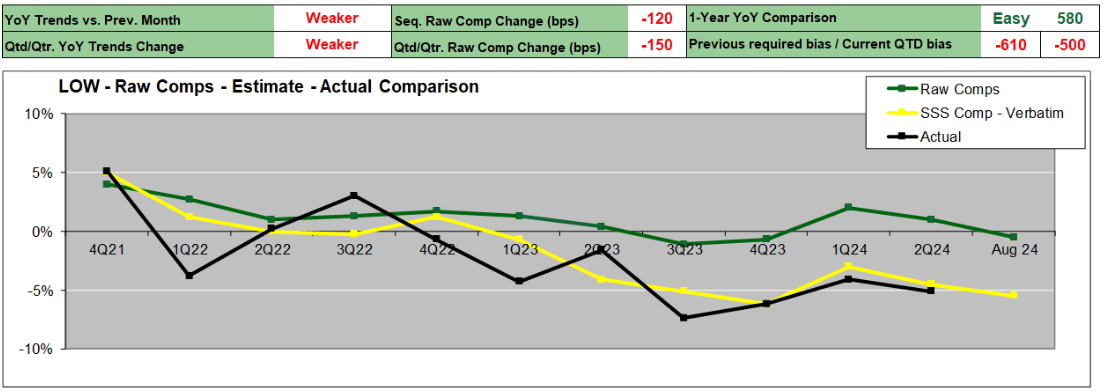

Aug sales trends are weaker than both Jul and 2Q24 trends, according to Verbatim’s latest channel checks. Customers are exercising caution due to economic uncertainty driven by a weak economy and the upcoming elections. To counter this, LOW’s is offering promotional deals and enhancing customer service. Last month’s bestselling products were Halloween related, as well as patio furniture and appliances. Verbatim’s Aug Comp Estimate is -5.5% vs. 2Q24 Actual Comp of -5.1%. Click here to access the full report.

Deep Knowledge Investing

DKI adds a new US Healthcare pick to their portfolio

Working with the same physicians and advisors that led them to Shockwave Medical and a huge exit (>70% in under 4 months), DKI has found another single product company with extremely high revenue growth. They believe that the product is safer for patients and saves Medicare, Medicaid and insurance companies 75% vs. the treatments that are the current standard of care. Like Shockwave, they expect the company to be acquired. DKI's model shows a potential opportunity to make 4-5x their investment in the next 3-5 years.

Northcoast Research

The negative commercial aero demand outlook that Northcoast first communicated in Jun, may turn out to be incorrect after all. The situation appears to be much worse than expected. Global market headwinds are intensifying for upstream aerospace suppliers due to widespread inventory reduction efforts and a sharp drop in tier-one customer orders. Companies levered to titanium, forged products and aero fasteners appear to be in an especially vulnerable position. Northcoast interprets their latest channel insights to be another bearish indicator for HWM still believing CY25 earnings estimates to be overly aggressive and the shares to be overbought heading into a new period of negative headlines.

Hedgeye

Jay Van Sciver sees 50%+ downside as macro and truck fundamentals soften, borrowing costs increase, higher book units are sold into a softer used truck market and leverage tolerance runs dry. Investors are mistaking used equipment price increases for some sort of underlying business change. This is what happened at rental car companies, which also saw the values of their fleets (and stock prices) temporarily soar. Meanwhile, R has never been more richly valued by capital markets. Consensus estimates for 2H24 and 2025 seem disconnected from downcycle realities, with mid-teens EPS (fuelled by debt funded buybacks) less likely than low single digits profits per share as truck gains run dry and competitive intensity compresses margins.

MAPsignals

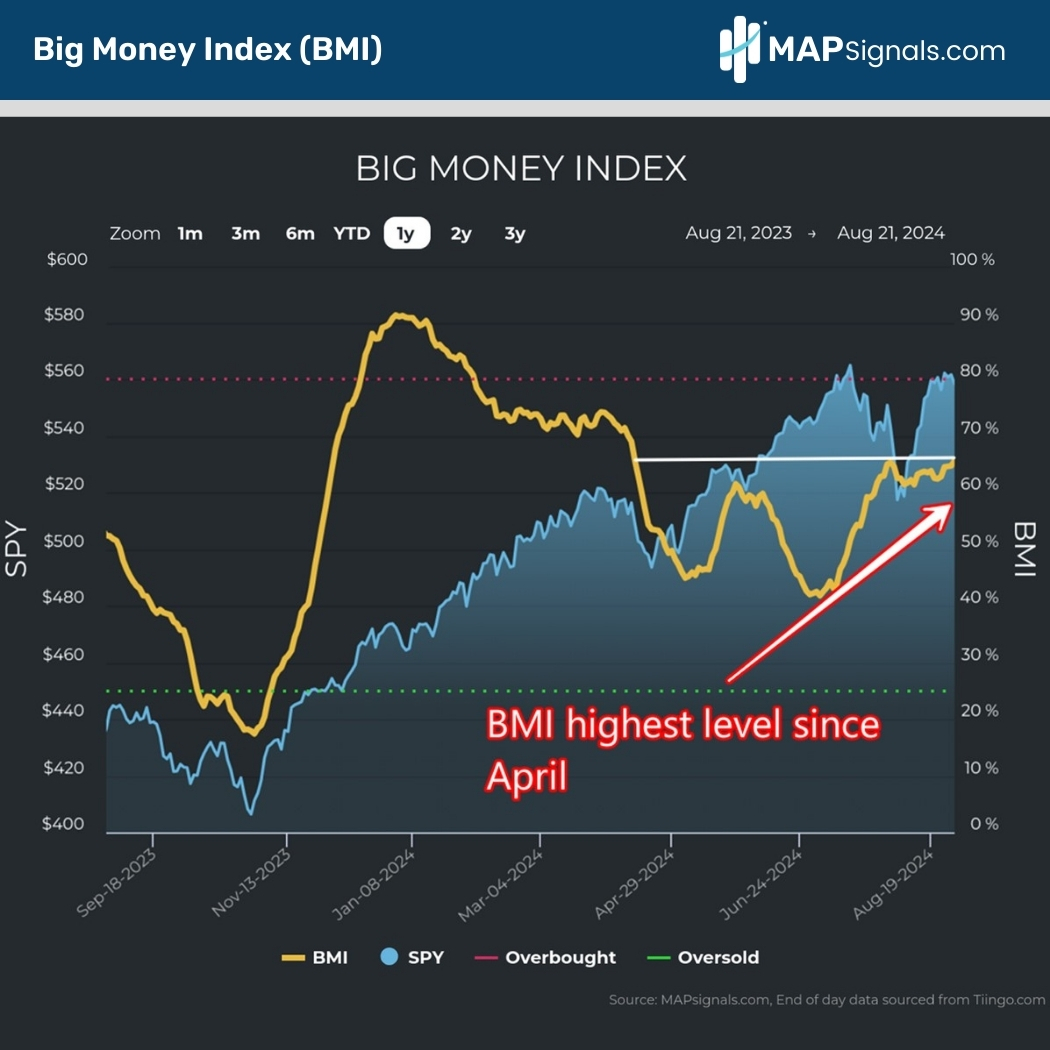

Bullish case to own Real Estate stocks into yearend

The rotation out of Tech is accelerating and one look at MAPsignal’s Big Money Index (see chart) reveals a startling truth: money is being put to work. Since the Jun CPI report, high-yielding REITs have been an easy bet for yield-hungry investors. Lucas Downey has been studying high-momentum periods for the Real Estate sector and found that since 2001, the average return for the iShares Real Estate ETF (IYR) in the months of Sep-Dec is a measly 1.99%. However, when IYR gains at least 9% (it is up +9.25% YTD) in the months of Jan-Aug, the remaining 4 months of the year see market beating average returns of 7.41%. That is a whopping 272% outperformance vs. the typical return!

Arete Research

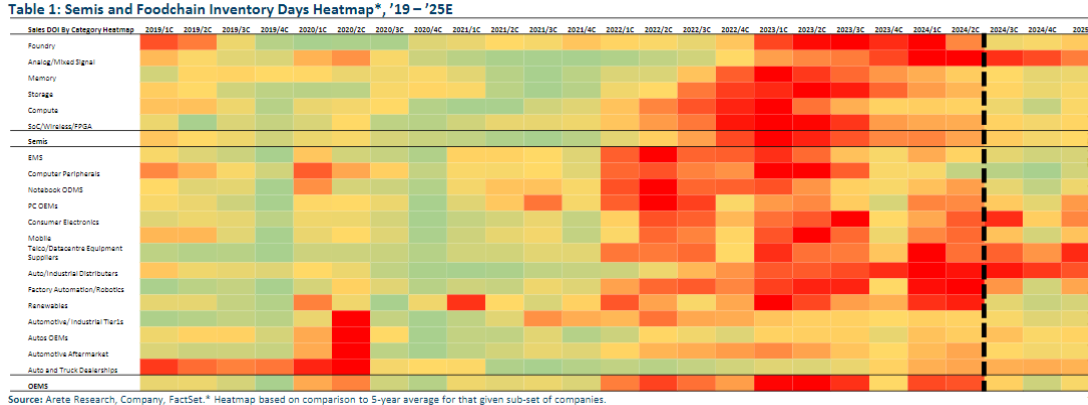

Semis & Downstream Inventory: Different points on the inventory rollercoaster

Arete’s survey covers $630bn of annual semis revenue and $7.8trn of downstream revenue, capturing over 600 companies. Their report highlights 1) Semis inventory across all the sub-sets through 2Q24. 2) The current inventory cycle vs. prior inventory cycles looking back to 2018/19 and 2008/09. 3) Semis customer foodchain inventory through 2Q24 vs. prior cycles across all the main semis end-markets. 4) The correlation between semis inventory and stock prices. 5) Consensus expectations for semis revenue growth over 2024 and into 2025 and what this means for semis inventory reduction.

Sales Pulse Research

Latest channel checks reveal: 1) Demand from telcos remains weak. 2) Demand from hyperscalers and Tier 2 CSPs is reasonably strong. 3) Federal and Enterprise are “OK” but not seeing acceleration. 4) Subsea - CIEN is very well positioned and should see a ramp over the next few quarters. Looking further out industry contacts remain enthusiastic about CIEN’s technology lead and believe they are best positioned to benefit from catalysts that include: 1) Continued growth in bandwidth demand. 2) AI driving higher bandwidth requirements between data centres vs. today’s focus on clusters within data centres. 3) Adoption of 800G and beyond. 4) Ramp in edge computing for AI and other applications. 5) Ramp of BEAD funding.

Corto Capital Advisors

Over the first nine months of its fiscal year, SCSC has experienced softening demand for tech products, macro weakness, elongated sales cycles, muted large enterprise projects and lower sales of barcoding, mobility and POS products. In the most recent quarter, the company’s networking hardware sales also rolled over as customers are still digesting excess prior-period product shipments. Despite these headwinds, shares of SCSC are up >50% over the last year, significantly outperforming the market as well as the company’s key vendors. Corto Capital sees 40%+ downside on multiple compression and the potential for lower than expected revenue guidance for the upcoming fiscal year.

Veritas Investment Research

Veritas highlights the elevated risks inherent in BEP’s business model and explains why strong growth prospects do not always translate into increases in unitholder value. Their analysis indicates that BEP's ROIC and ROE are not sufficient to cover its cost of capital. These returns become considerably lower when gains from asset sales, which have become a material contributor to reported returns, are excluded. With equity returns being driven by asset monetisation, BEP's strategy bears significantly more risk and investors should require an equity risk premium above regulated utility peers.

Japan

Asymmetric Advisors

Shares in MCJ have only recently started to rise having been moribund for 4 years, but with only 1 local broker covering the stock and a lack of detailed English presentation materials, this is a largely overlooked company entering a new growth phase. Its PER is only 11x what is an overly conservative FY3/25CoE calling for sales +5% and OP +6% to ¥18.3bn with a 9.2% OPM. In fact, Q1 sales were +11%, OP +25% with a 11.9% OPM (there is some seasonality, but it is still looking good for an overshoot). MCJ also significantly beat its original profit target in FY24. The group has net cash of ¥37bn (>25% of M/Cap), while mid-term growth in gaming PCs and AI PCs, of which MCJ's Mouse was the 1st in Japan to introduce AI CPU PCs, will be strong tailwinds.

Emerging Markets

86Research

LI's stock price slumped post earnings despite the auto manufacturer delivering better-than-expected Q2 results and providing Q3 guidance in-line with market expectations. However, investors were left disappointed as management failed to offer clear long-term sales guidance or a detailed plan for the development of BEVs. 86Research thinks the market is overlooking the steady growth in LI's EREV sales, excellent cost and expense control, and the strategic capabilities of its management team, which are supporting the long-term development of the company. They view the market concerns as excessive and have been “pounding the table” recommending investors buy the stock at the current price!

Galliano's Financials Research

Bradesco is Victor Galliano’s key pick in big-cap Brazilian / LatAm banks - he believes that post-provision earnings will recover in 2H24, which should drive a meaningful lift in group ROE. It is also looking to squeeze opex, and given its underwhelming efficiency ratio, there is potential to find savings. Bradesco has an attractive earnings yield for lesser political risk than Banco do Brasil, but it is also attractive on its (recovery) growth potential as reflected in the PEG ratio and it has undemanding PE multiples and PBV ratios. NuBank is a digital bank success story, but one that Victor considers has challenges in terms of credit quality and it has potential capital constraints given its fast loan growth.

Crystal Shore Alpha

Nvidia without the drawdowns - TRP has been one of the big success stories of India's stock market. Since 1st Jan 2000, the stock is up 7950% (USD). That compares to MSCI World Health Care (USD) up +650% and MSCI India (USD) up +725%. Crystal Shore purchased TRP in their weekly GTAsia Top 10 Stocks on 2nd Oct 2023. It has been their top performing position, delivering +72% over the past 11 months. Bank Jago Indonesia is their second highest scoring position, with a +33% return (USD) since their purchase just 6 weeks ago.

Creative Portfolios

Within Creative Portfolio’s extensive global equity universe, they screen for the best combined ranked stocks focusing on Valuation, Profitability, Piotroski and Accruals. Paul Hollingworth thinks Universal Scientific Industrial offers a compelling technical-fundamental opportunity. The current valuation only points to a modest pick up in EBIT margin and ROE which he feels is too pessimistic. Furthermore, the company's balance sheet is rock solid and its FCF Yield looks attractive. Using a discounted cash flow model, Paul sees fair value at CNY40.45 (60%+ upside).

Macro Research

Developed Markets

Radio Free Mobile

AI: The race to the bottom

One would have expected Anthropic’s latest innovation to be part of its premium tier, but the fact it is free is a sign that the race to the bottom, kicked off by Meta, is already underway. Richard Windsor sees it as a sign that the company is struggling to attract users to its platform in an already competitive environment. There are still no signs of the promised superintelligence on the horizon. Current expectations and valuations are unrealistic, and we will likely see the reset begin in the venture capital space as start-ups fail to meet their targets and go back to their backers for more money. Against this backdrop, everyone is going to take a hit, but the least pain is likely to be felt by Nvidia and TSMC. Richard prefers adjacencies of inference at the edge and nuclear power as the best way to get exposure to AI.

Talking Heads Macro

The EUR case

According to Manoj Pradhan, the case for being long EUR is that the ingredients for a sustained but typically euro-like dull recovery are in place. More importantly, expectations of euro area growth become so depressed in downturns that they bounce back more sharply when markets are more comfortable about growth – that’s a sound bet for the coming quarters (in the absence of a sharp recession in the US or a further deterioration in China). Manoj addresses three questions in this note: (i) is there a case for being long EURUSD even here? He has been long since April 26th when EURUSD was 1.071. 3.3% in four months isn’t bad, but much of that has come from the recent breakout. (ii) What is the biggest threat to long EUR? (iii) How does long EURUSD coexist with his recommendations to be paid US 2y1y?

Blonde Money

Germany: Misconceptions in the state elections

Between them, the two parties of the far left and the far right took almost half of the votes in the latest German State Elections: 48.6% in Thuringia and 42.4% in Saxony. The scale of their success nullifies a number of misconceptions about each: that the rise of the new party on the far left, the BSW, would eat into the AfD vote and render them less of a threat to the centrist parties; that the BSW was merely a personality cult around its founder; and that neither party would get close to power given traditional parties’ cordon sanitaire around working with any extremists. It also reinforces how hard it is to govern when newer parties reach such a threshold of support. In neither state is a majority of seats for the 'traditional' parties possible.

Yardeni Research

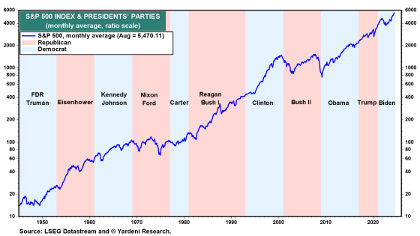

US: What could possibly go wrong in September?

September has a history of being the worst month of the year for the stock market, yet Ed Yardeni believes it’s hard to imagine that it will be a bad one this year since the Fed is widely expected to start its latest monetary easing cycle this month. In addition, the FOMC will release its latest Summary of Economic Projections, which is widely expected to confirm that the Fed intends to cut the FFR several times in coming months. Then again, the S&P 500 is up 18.4% ytd, so it appears to have discounted lots of good news to come. It's certainly too early to discount a bearish political outcome on November 5th. In Ed’s opinion, that would be a sweep for either of the two political parties since the stock market tends to favour gridlock. That said, the market does have a history of performing well no matter which party is in the White House (see chart).

Quill Intelligence

US: Consumer vulnerabilities rising

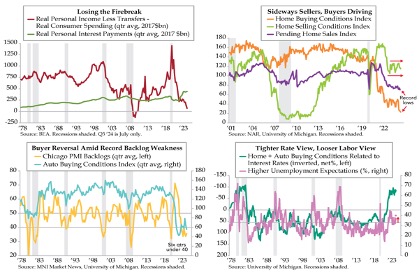

According to Danielle DiMartino Booth, the gap between the source of US consumer spending and the act itself is closing rapidly in 2024. Downside risk to elevated interest payments against this backdrop raises redder flags for household balance sheets given the decimated aggregate saving rate. Record low home buying conditions and 2024’s abrupt reversal in auto buying conditions suggest household budgets are reaching a critical point, especially as it relates to the sensitivity to interest rates. The Fed’s stubbornly tight policy risks a further deterioration in unemployment expectations. Vol is cheap.

Vermilion Research

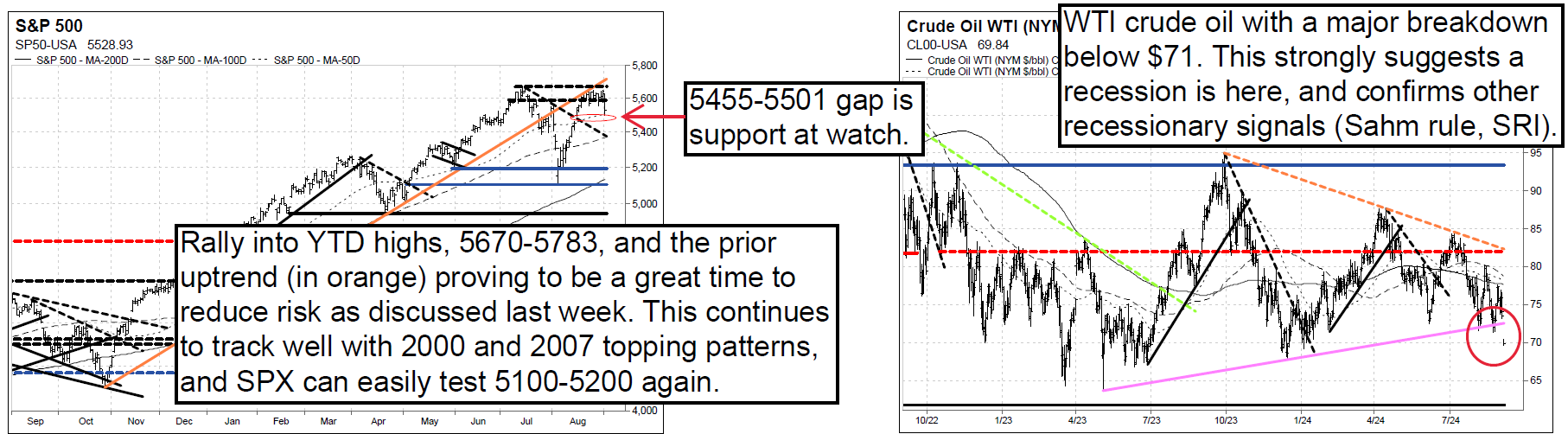

US: Recessionary signals

The Vermilion Research team’s long-term outlook remains neutral on the S&P 500 as of 6 August, after being bullish since early November 2023. The team sees the SPX and Nasdaq 100 as going through a 1- to 4-month pullback/consolidation period, with market dynamics remaining concerning, especially when considering the toppy price action in this bull market’s leaders (Nvidia / SMH) and a major breakdown in WTI crude oil. One of the most bearish things that can happen at this point is if the XLF, XLI, RSP, XLB, and Dow end up being false breakouts, which appears to be happening already with the latter two.

Minack Advisors

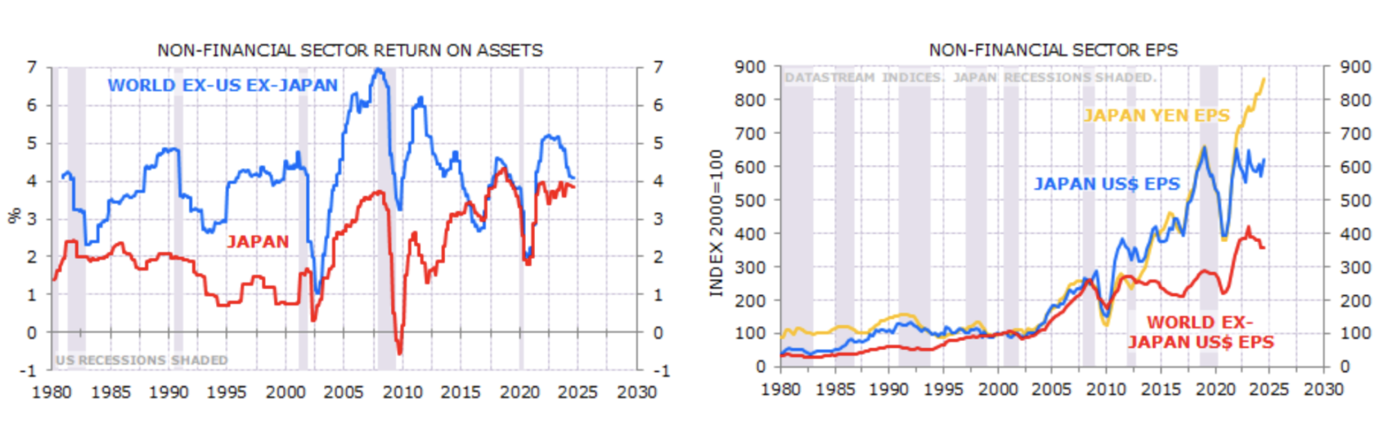

Japan: Bull case still intact

Japanese equity returns have largely been driven by yen weakness over the past decade. The country’s relative performance, in dollar terms, hit a new all-time low in June. However, Gerard Minack comments that the medium-term bull case for Japan remains intact. The market is cheap. Return on assets and margins have risen. US$ EPS growth has been solid, outpacing that of its peers since the GFC (chart 2). Emerging domestic inflation pressures point to rates normalising. And last but not least, if the next cycle is capex-led, as Gerard expects, it will play to corporate Japan’s strengths. The nation’s equity market is perhaps the most cyclical in the world, so with the world slowing down – even if only into a soft landing – now may be the best time to buy the market.

Emerging Markets

Copley Fund Research

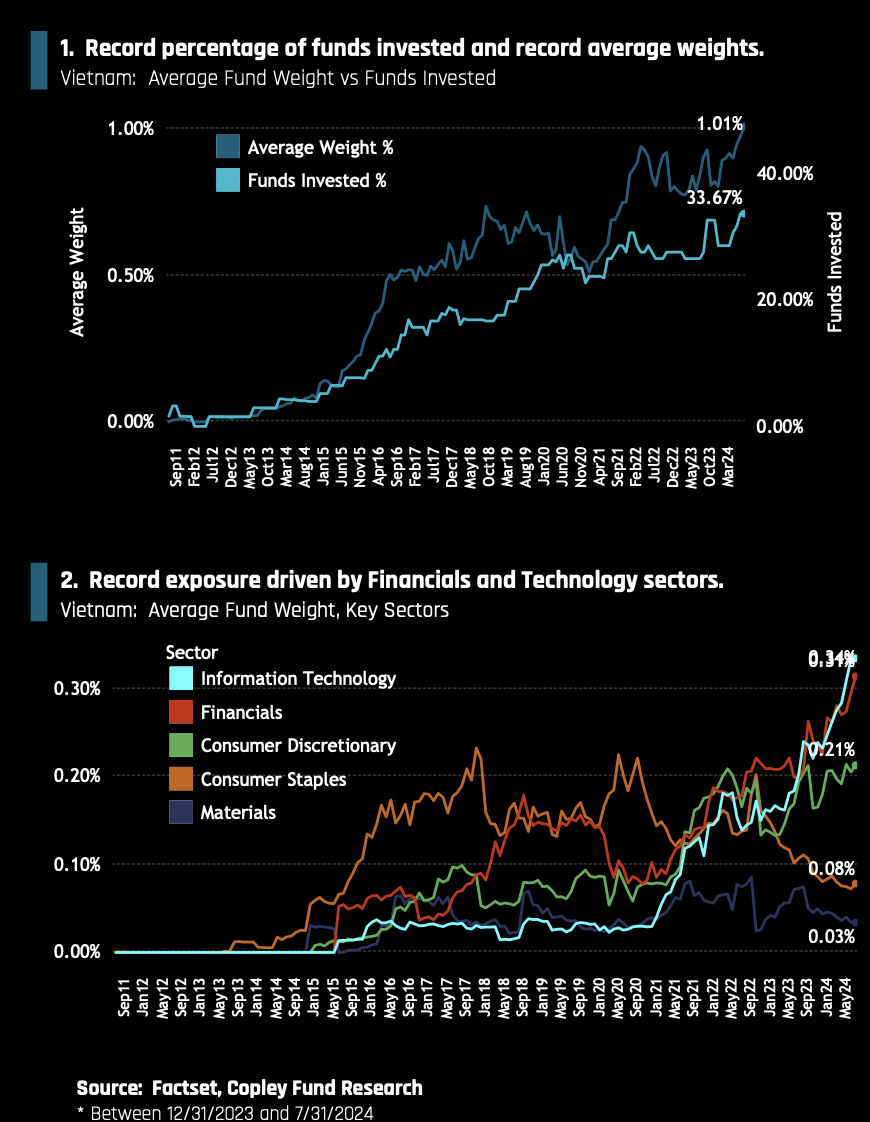

Asia ex-Japan fund positioning insights

Steven Holden’s latest report mentions record fund ownership in Vietnam, with over a third of Asia ex-Japan funds now invested in the country. Average funds have now hit a record high of 1.01%, led by a rotation into financials and tech stocks, and key players such as JP Morgan and Fidelity signalling increased confidence in the Vietnamese market. Another rotation is also underway out of Chinese real estate into Indian equivalents, leading stocks like Phoenix Mills, Macrotech Developers, and DLF Limited to reach new ownership highs. In contrast, fund managers are reducing their positions in Hong Kong Exchanges and Clearing, with the stock falling to the 7th most widely held in the financials sector, reflecting a broader shift towards South Korean financial stocks.

Pacifico Research

Chile: Rates projection

The latest monetary policy rate decision and report align well with the Pacifico team’s previous macroeconomic assessment. They continue to believe that the central bank will be sensitive to short-term events, making it unlikely that a rapid convergence toward neutrality will be guaranteed, as the market is pricing in. The team maintains a bias in favour of UF-denominated instruments, but now with durations in the middle of the curve (5 years) and expects a flattening of the nominal curve relative to USD OIS. They continue to favour bonds over swaps, with significantly higher yields due to an increase in bond issuance and the preference of local pension funds to use these instruments to replicate received positions in long rates due to greater liquidity.

Greenmantle

China: Concerns among the crowd

Niall Ferguson’s team spent two weeks in Beijing and Shanghai speaking with sources in economics, tech, finance, and policymaking. Sentiment has improved marginally since the start of the year, but substantial concerns remain about the property sector and the government’s too-little-too-late approach to policy support. Given the rhetoric from the “Third Plenum” and recent weak 2Q/2024 data, Niall Ferguson expects an announcement around October of another RMB 1trn in central government-issued bonds, as well as another bond quota for local governments to purchase unsold homes and aid the flailing property sector. He expects Beijing to target “around 4.5%” GDP growth next year. Geopolitical tensions may have softened lately, yet Niall urges optimism; regardless of the US presidential election outcome, the Chinese firmly believe that Cold War II will remain the status quo.

WallStreetCourier

China: Sovereign wealth intervention

China's stock market (CSI 300) ended the last week of August week on a high note, driven by significant purchases from a domestic sovereign wealth fund. Despite these gains, the CSI, which tracks the largest Chinese stocks, has plummeted 42% since reaching its peak in 2021. The recent purchases by the sovereign wealth fund serve as a strong fundamental catalyst and align with the growing interest in Chinese stocks among value investors. However, WallStreetCourier’s data still does not provide convincing evidence of a sustainable turning point for Chinese equities. Although Rudolph Koch anticipates no more than a temporary oversold bounce, opportunistic traders may seize the moment as long as his Smart Money Indicator continues to drive prices higher.

Emerging Advisors Group

Nigeria: Keeping promises

Nigeria is keeping its promises on the currency and rates. The NGN rate has remained unified with the black market rate this year, the central bank has kept rates high and the backlog of US dollar orders is clearing. The combination of FX weakening and financial tightening is not great for domestic demand, but it has put the external balance back in surplus, narrowed the fiscal deficit, and is a positive signal for transparency and export investment. Inflation is still high but peaking and likely to come down at the margin, making local rates a bit more attractive—although, as before, Jonathan Anderson is not sure about growth, earnings and equities. He maintains his dollar sovereign position and continues to see value in hard currency debt.

Burumcekci Research & Consulting

Turkey: Recession ahead

In 2Q/2024, GDP grew by 2.5%, below expectations of 2.8%. In contrast, the 2023 growth was revised upwards from 4.5% to 5.1%. When considering the outlook for growth in the upcoming period, leading indicators suggest that GDP growth continued to slow down in 3Q. For instance, Turkey's PMI index averaged 47.5 in July-August, down from the previous quarter's average of 49.2, while the Central Bank’s Real Sector Confidence Index (RSCI) also recorded an average of 98.4 for the same period, which is lower than the previous quarter's 102.1. Consequently, Haluk Burumcekci expects a quarterly contraction in the third and final quarters, leading to a technical recession, and he has revised his growth expectation for this year from 3.5% to 3.0%.

Emerging Advisors Group

Vietnam: Back online

After the painful 2022-23 shocks, Vietnam is back online. The external economy is booming again, with rising exports and tourism flows, record surpluses and continued market share gains. The domestic economy is still weaker, but spending indicators are recovering, the credit cycle is picking up and the corporate bond market has come back to life. So, Jonathan Anderson says he is staying with the equity market. The Vietnam index is no longer underperforming, and he looks forward to renewed structural gains as the country forges ahead as an Asian "tiger".

ESG

Metals Focus

Gold ESG Focus 2024

Metals Focus has recently published its annual report on environmental, social and governance in the gold mining industry, covering the last decade for 17 of the largest gold miners. Key findings include a reduction in combined scope 1 and 2 greenhouse gas emissions by 5.4% y/y in 2023, with Harmony reporting the highest emissions intensity; a rise in payments to governments by 12%, with Barrick leading the way; a fall in community investment by 16%, with Polyus the largest contributor; and the lowest level of fatalities on record amidst improving injury rates. Please contact us to find out more.

Commodities

Grey Investment

Adding to gold longs

Spot gold has continued to set new highs, reaching 2,532 in August (see chart, originally printed 26th August). The breakout from the 41-month rectangle targets a move to 2,650+. Longer-term, Chris Roberts’ base case is for an advance to a minimum of 3,840, double the 12.5-year ceiling formed in 2011-2023. He remains 66% long from 2,102.65 and will add another 10% with 5% at market and 5% at 2,484. A daily close below 2,254 is the stop for all of his long positions.

ERA Research

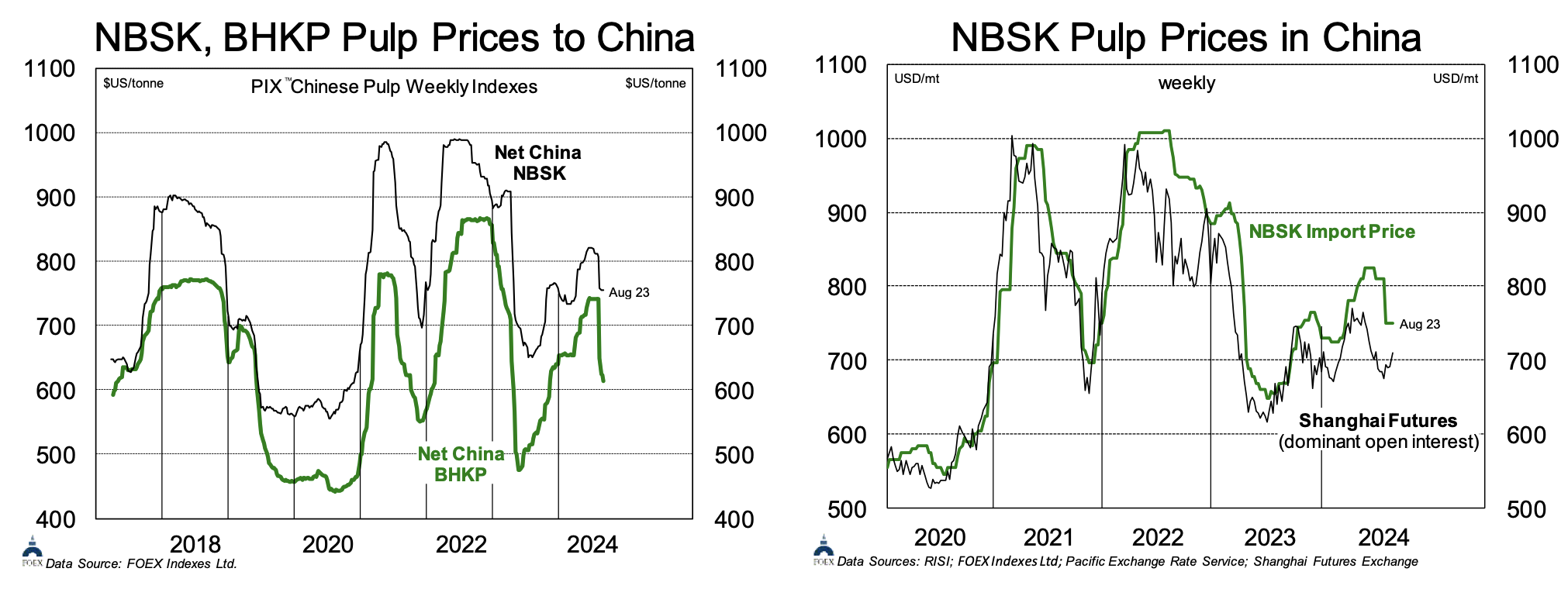

Pulp pricing floor approaching

After an exceptionally steep correction in late July/August, week-over-week price changes for both softwood and hardwood pulps slowed in China (chart 1). Shanghai NBSK futures had been falling for some time, but prices for imported pulp finally began to collapse in early August and have started to climb again (chart 2). The magnitude of the correction has accelerated the pulp pricing cycle and signs indicate that spot hardwood pricing is approaching its trough. For NBSK, the correction has been more gradual and shallower, and new threats to global supply should support pricing in the near term. With 2.0MMmt of mostly NBSK, Mercer is the team’s preferred route to pulp exposure. It is trading at a 3+ year low. While the company has a 2026 maturity to address, it reduced net debt by $45MM in Q2 and expects the same in Q3. The team’s $10 target reflects a 7.0x multiple on 2025E EBITDA of $272MM.

Vanda Insights

Crude flirts with US economic mood, ignoring supply risks

A troika of geopolitical factors erupted on the market at the start of last week in the Middle East, Ukraine and Libya. Brent and WTI futures jumped 3% on Monday yet surrendered most of that premium as the week progressed. Vandana Hari was asked in several television interviews if crude had become immune to geopolitical risk; whilst no market is immune to supply shocks or the risk thereof, there are good reasons why the Ukraine and Gaza wars are not injecting a fear premium in crude. Vandana expects markets to shrug off any worsening of the Gaza situation as long as the hostilities remain confined, and expects the market to do a just-in-time pricing in of a supply risk premium should the Ukraine war impact Russian oil supplies.