Company & Sector Research

Europe

New Street Research

New Street recently published two thematic notes looking at Sub-Saharan African telecoms companies. They focused on the potential for market structures and revenues to improve, and especially after periods of currency weakness (which has been notable in Egypt and Turkey). In this note, they go through the consequences of this for VOD and refresh their investment thesis as they believe the upside from the non-European assets could be overlooked by consensus (and talking of non-EU assets, this is New Street’s first VOD report where they highlight the hidden value that might be in satellites as well). TP £1.40 (90% upside).

Revelare Partners

Last week the gambling software company confirmed it was in discussions with Flutter over a possible £2bn Snaitech sale. PTEC was highlighted as a Buy during one of Revelare’s idea events in Nov last year and they think the report is still worth reading. The presenter provided details on the disagreement between PTEC and Caliente. He also discussed a number of levers that he believes could leave the stock being worth c.£43.00 vs. its current price of £6.50!

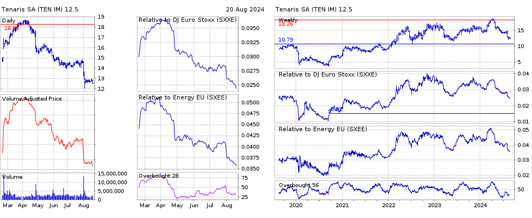

Stockcube

Stockcube opens a short position as TEN's share price reasserts the downtrend and makes new short term relative lows. Their TP is €10.50. The stock was one of the names highlighted in Stockcube’s Daily Europe Top 200 Bulls & Bears report this week, where they also opened a long position in Lonza Group (finds short term uptrends; TP CHF600). Having recently closed shorts in Norsk Hydro (finds short term price and relative support) and Kering (finds long term support at €240), as well as closing their long position in Deutsche Bank (now trades sideways), Stockcube’s portfolio currently consists of 44 open longs and 26 shorts.

ResearchGreece

ResearchGreece was not surprised the bank raised its FY24 RoTE guidance to >24% from >17% following Q2 results (they had been expecting this ever since Q1). Meanwhile, management has announced its decision to list the stock on the ATHEX (and de-list from the LSE) which should improve trading liquidity. ResearchGreece reiterates their OWN IT (OI) rating and raises their TP to €5.8. This comes as the result of their higher estimates in 2024-2026. They expect dividends of €180m-€195m in 2024-2025 on 40% and 50% payout respectively, pointing to a dividend yield of >10% at current prices.

Smart Insider

Sylvie Gregoire (Director since 2015) spent €184k at DKK 913, increasing her holdings by 26%. This is her fourth purchase and her largest. She last bought shares in May 2022 at DKK 395, and before that in Aug 2017 at DKK 144, both of which were timely. Smart Insider ranked the stock +N on Aug 8th based primarily on a €228k purchase from Christina Law (Director since 2022), her largest purchase and the highest price she has paid. Andreas Fibig (Director since 2018) also recently increased his stake in the company. As a result, Smart Insider upgrades the stock further to +1 (highest rating).

Insight Investment Research

Near-term tariff rises at Frankfurt are insufficient to close the gap to its Allowed Reg. Return. Robert Crimes sees Aviation Returns (NOPAT/RAB) of only 3.1% in 2024E and 2.9% in 2025E, c.320bps below Insight’s WACC of 6.2%. In addition to insufficient tariff rises, there are 3 key factors to consider: 1) Weak traffic recovery (lowest of EU peers). 2) High wage rises above inflation (Frankfurt staff costs to rise c.€150m (+19%) in 2024-25E). 3) High expansionary capex. Robert has a Sell rating on the stock given the average upside of Insight’s Global Infrastructure coverage is significantly higher at nearly 100%. Buy rated peers include Aena (TP €369), ADP (TP €234) and Flughafen Zurich (TP CHF330).

Ben Jones Investments

Ben Jones provides his thoughts following solid 1H24 results and believes San Dionisio will be transformative for ATYM, boosting production from 48kt Cu in 2024 to over 100kt CuEq by 2030. The increase in production comes from higher grades alone, Ben expects no change in the mining and processing rates, which allows for strong economics. San Dionisio’s proximity to the existing Cerro Colorado pit and its use of the existing processing facilities also provide extremely strong economics. Masa Valverde and Proyecto Touro are two excellent development assets Ben sees priced as free options. He thinks they are being ignored by the market due to limited information.

North America

Quantitative Partners with Phil Erlanger Research

Tracking the mutual funds tax selling

Geoff Garbacz thinks this might be the most important data point to follow to determine if we continue to see a stock market rally. Stocks vulnerable to tax selling include Boeing, Intel, Rio Tinto, Stellantis and UPS. Click here to watch the video which also includes the key levels to monitor on the S&P 500.

Trivariate Research

The five most important insights that all growth investors should know

1) Owning high-quality growth stocks and avoiding low-quality growth stocks is crucial. 2) To pick stocks among high-quality growth, use improving margins, revenue acceleration and upward revisions. Buying cheap and shorting expensive stocks across the high-quality growth cohort is not effective. 3) Low-beta relative to the growth universe performs far better than high-beta. 4) Combining quality and beta works. Avoiding high-beta and the bottom-half of quality is pivotal for growth investors. Hence, owning low-beta Energy is better than owning high-beta Tech among growth stocks. 5) Combining forecasted revenue growth and beta also works, where lower forecasted growth and low-beta generate excess returns and growth stocks that are both high-beta and have high forecasted revenue growth lose money.

MYST Advisors

Decades of price gouging and significant brand mismanagement was bound to cause Parks to slip up sooner rather than later. DIS will start FY25 with Parks growth flat (at best) and the well-known myriad of headwinds facing the Entertainment division. Warner Bros. Discovery just took a massive write-down on its linear networks. DIS will have to do the same at some point. Most importantly, modelling future EPS growth is only getting more difficult. EPS is topping out around current levels. What to pay for peak earnings? It is not 17x-25x. The new trading range for the stock as it slowly "dies" is $30-$75/share assuming $3.00-$5.00 of EPS and a 10x-15x multiple.

Gordon Haskett Research Advisors

Ahead of the print, GHRA upgrades the stock to Buy and raises their 2Q24 SSS estimate to 4% (vs. guidance of 0%-2%), driving total sales growth of 12.7% to $2.4bn and EPS of $1.00. GHRA’s footfall data has inflected higher on a both a one and two-year stacked basis, while QTD traffic through the first two weeks of 3Q24 has stayed strong (Aug > Jul). Longer-term, they expect BURL's 2.0 Strategy to drive improved comps and margins. The company can close the performance gap to peers and while sceptics will argue that this expectation is largely reflected in the stock and valuation, GHRA thinks investors should barbell higher quality retailers with some turnaround / defensive characteristics to increase alpha.

Hedgeye

How many names in the Consumer space can you point to with under-consumption in its category during Covid while still running below long term trend, idiosyncratic drivers to accelerate unit and comp growth, countercyclical elements as the low-price leader in its space and a flywheel that drives sustained unit growth with stable, high growth in FCF? Cash generation will fuel growth and consistent stock buybacks creating downside protection. These assets are rare and Hedgeye thinks PLNT can easily command a high teens EBITDA multiple for years to come with sustainable mid-teens EBITDA growth and 25%+ EPS growth. That builds to a stock of $130-160 three years out (vs. ~$80 today).

Bios Research

Alpha generating Healthcare shorts

Bios continues to publish strong short ideas and recent earnings has been validating a number of their commercial short theses. They have been focused on medtech, commercial biotech, over-hyped AI, and medical supplies and tools. Recent successful calls include 1) Northwest Biotherapeutics (down 75% since initiation) - its valuation was egregious given the company’s poor financial position and numerous corporate red flags. 2) Recursion Pharmaceuticals (down 46%) - its platform lacked any clinical validation, yielded a limited number of outside partnerships with near-term milestones and demanded significant cash burn. 3) West Pharmaceutical Services (down 26%) - identified as a short because of hype surrounding GLP-1 and other biologic manufacturing.

Northcoast Research

Northcoast’s channel checks continue to reveal a slowing demand growth environment for nickel-based alloys. The average shipment comp reported by nickel-alloy survey participants was up 2-3% Y/Y, compared to +4-5% growth in CY2Q. Drivers behind an increasingly cautious 2H24 outlook include slowing jet engine orders, but the most surprising takeaway from recent checks was a sharp drop in medical-related demand. Contacts reported flat-to-down 1% order growth for CY3Q, which is down from the +7-9% growth range to start the year.

Sidoti & Company

Since CBZ announced its largest ever acquisition and reported 2Q24 results, the share price has fallen c.20%. However, Sidoti sees the Marcum deal as a natural and positive step for the company, adding long-term EPS and FCF growth potential as well as size, scale and service offerings. Their new estimates now imply respective annual EPS growth of 10.0% and 20.6% for this year and next. Sidoti’s FCF per share estimates of $2.88 in 2024 and $3.54 in 2025 imply respective FCF yields of 4.2% and 5.2%. They believe the recent pullback provides an attractive entry point and upgrade the stock to Buy with a target price of $86 based on 27x their 2025 EPS estimate of $3.20.

Alembic Global Advisors

Pete Skibitski turns bullish and increases his target price by $20 (to $48) post 4Q24 results - he raises his terminal valuation by four turns, to 18.5x (~20% premium to the S&P 500 on EV/EBITDA), which, combined with a higher forecast following Q4, drives the increase to his TP. While management still targets only modest sales improvement in FY25, adj. EBITDA margin rate should improve nicely into the low double-digits. Pete also believes mid-term Street expectations are too low, as the firm’s FY24 revenue in radar applications was $110.4m, well below its prior peak of $289.2m in FY21. However, he expects MRCY can return to this level, which should drive attractive HSD organic revenue growth.

Sales Pulse Research

Security Spending: Trends remain healthy

Key takeaways from SPR’s latest field work include: CrowdStrike - seeing some deal slippage, but most respondents believe few customers will actually switch vendors following the global IT outage. SPR has heard of renewal discounts that include buy 3-yr and get 1-yr free. SentinelOne - benefitted from winning more deals at the end of the quarter, assisted by CRWD’s crash. Zscaler - mostly positive input but some concern re. the maturing of the SASE market and possible disruption to sales from the shuffling of sales personnel between ZS to Wiz and from ServiceNow to ZS. Fortinet - industry contacts are positive about its acquisition of NextDLP but less enthusiastic about Laceworks.

Japan

Azabu Research

From zero to hero - NextAge has, in just two short years, moved from No.3 to No.1 in the used car market in Japan. Its market share is still <7% and Mike Allen no longer sees any meaningful obstacle in the company’s path to 30% share within the next 8 years. Yet the stock has underperformed the TOPIX by 60% in the past year and trades at ~11x EPS. Investors have lost faith in the company’s ability to sustain the same level of sales and profitability per unit as it rapidly expands its outlet base. In Mike's 21-page initiation report, he argues the series of events that gave rise to these fears have passed and are already fully resolved. He thinks fair value could be 3x the current price.

Emerging Markets

Copley Fund Research

The percentage of funds invested in BHARTI reaches 15-year highs. Over the past 6 months, ownership increases have been the highest among Indian peers, propelling the telecoms company to the 7th most widely owned stock in India. This has been primarily driven by Growth and Aggressive Growth investors, with other style groups largely absent. 27 funds have initiated new positions, with no closures, and notable new investors include Fidelity, GQG and Morgan Stanley. While BHARTI’s ownership has been steadily increasing for over four years, it remains a net underweight and lags behind other Indian large-cap peers. Even within Copley’s peer group, there are still 87 former holders who are not currently invested. The bull market may not be over just yet!

Blue Lotus Research Institute

BABA’s transformation from China’s eBay to China’s Microsoft continues - the group’s AI strategy involves both the development of its open-source LLM model (Qwen), which has performed well on benchmarks in China, and investment in Chinese AI startups. This strategy has already proven successful with Moonshot and MiniMax developing popular AI applications. BABA provides these start-ups with credits that can be used for training or inference, which has driven growing demand for AI services on AliCloud. Although GPU supply is a constraint, Blue Lotus sees domestic breakthroughs in semiconductor equipment providing BABA with an avenue to expand its supply of AI compute and expects the group (and Tencent) to reinvent China’s software industry.

AlphaMena

The bank has experienced an impressive rally backed by its ongoing strong operational results. NIM has risen from 2.53% in 2021 to 3.59% at 1H24. Recoveries post Covid combined with a favourable economic backdrop in UAE has helped to achieve >50% EPS growth on average over the last three years. A more generous dividend policy was a key catalyst for the stock last year and AlphaMena expects an improved 1.4 AED dividend per share in line with a 5% increase in 2024 EPS. The recent rally has narrowed Emirates NBD’s P/B historical discount from 35% (2019-23) to 12%. Strong momentum implies investor interest towards the stock can continue. TP AED27 (35% upside).

Propitious Research

Following a protracted downturn from 3Q22 to 3Q23, Parade has witnessed a recovery back to positive Y/Y revenue growth. During 1H24 revenue was up +24% Y/Y driven by both its Display Port and its High-Speed Interface Solutions segments, while gross margin has stabilised at c.43%. Parade remains one of the higher-quality EM IT companies and finished Q2 with NT$10.1bn net cash (16% of its Market Cap). In this report, Wium Malan analyses the group’s revenue growth outlook, margin expectations, dividend payout ratio optionality and current valuation level.

Macro Research

Developed Markets

Harlyn Research

Time for the beach

Lesson one, fixed income is not offering many clear signals. Simon Goodfellow points out that there is no sustained relative momentum anywhere along the US Treasury curve. Investment Grade and EM Bonds are not adding to returns or diversifying risk. High Yield continues to do both, which is lesson two. Three, Simon still likes the Technology-related sectors in US equities, but not as much as he used to. Four, Japanese equities are uninvestable until the new PM is confirmed and maybe not even then. Five, Simon is already defensive in his Eurozone equity models and becoming more so in his bond model, all of which is consistent with a rising threat of recession. Six, the UK is his preferred equity region, with its recommended weight approaching a 20-year high. There is a chance it may escape from 25 years of underperformance.

Belkin Report

Sentiment remains weak but positioning remains extreme

Global markets have had the initial plunge from cycle peaks triggered by deleveraging, but retail investors, hedge funds and Cathie Wood are buying the dip, as if the AI bubble is here to stay. Michael Belkin has recently suggested that a bear market has probably started and recommends selling and shorting into brief rallies instead of buying and holding the same investments that worked before the US stock market’s July 16th cycle peak. Banks and financial stocks in Europe and Japan are his top model sell recommendations. Michael also mentions a huge bubble in emerging and frontier equity markets, which no one seems to recognise; India, a favourite long for EM managers, is rolling over and is poised to be a great short, and the likes of Turkey, Poland, Romania, Peru and Argentina are among others that are very inflated and probably headed for a big fall.

Eurointelligence

Germany cuts Ukraine budget

While the western media are focusing on Ukraine’s incursion into the Kursk region in Russia, Wolfgang Münchau feels the much bigger story is that Germany has quietly abandoned its aid for Ukraine. The German government managed to agree a budget deal by cutting out Ukraine aid for the remainder of this year and for next year. Olaf Scholz’s big idea – and a U-turn – is to support a €50bn credit for Ukraine, collateralised by Russian-held reserve assets. Wolfgang argues that this is a thoroughly bad idea that it is likely to prolong the war, raise the costs to the west, and make it ultimately harder to conclude a deal.

Policy Sonar

Italy: Is the honeymoon over for Giorgia Meloni?

Italy’s PM Meloni has exulted in an extraordinarily long honeymoon phase. Externally, the PM managed to convince her allies that she would stick to Draghi's agenda on foreign and fiscal policy. Domestically, she benefited from weakened opposition forces, fed by a strong electoral tailwind. Consequently, no one within the right-wing coalition dared challenge her. According to Francesco Galietti, however, things are now changing. Within the EU, Meloni’s decisive turn against Ursula von der Leyen and the majority that supports her all but promises the end of any grace period for Italy's fragile fiscal status. At home, the PM is still doing well in domestic polls but is nonetheless facing growing pushback within her coalition. This is important, since she cannot marshall a majority on her own and still needs partners to piece together a government and run the country.

Ironsides Macroeconomics

US: A boost in capex?

In this week’s note Barry Knapp reviews the inflation and economic data in detail, marks the monetary policy outlook to market ahead of the Jackson Hole Economic Policy Symposium, offers his thoughts on the evolving political policy outlook and updates his sector and asset allocation views. Broadly, Barry’s medium-term outlook is for a strong capital spending cycle like the ‘60s or ‘90s enhanced by accelerated technology innovation adoption diffusing across a range of sectors, notably healthcare. This secular trend in turn would overcome excessive government spending and deficits as well as Fed intervention into a part of the market they have no business being involved in, namely the setting of longer-term rates. In the near-term, however, Barry has a negative bias because of his concerns about government interventions to stabilise ‘market failings’, mostly making things worse.

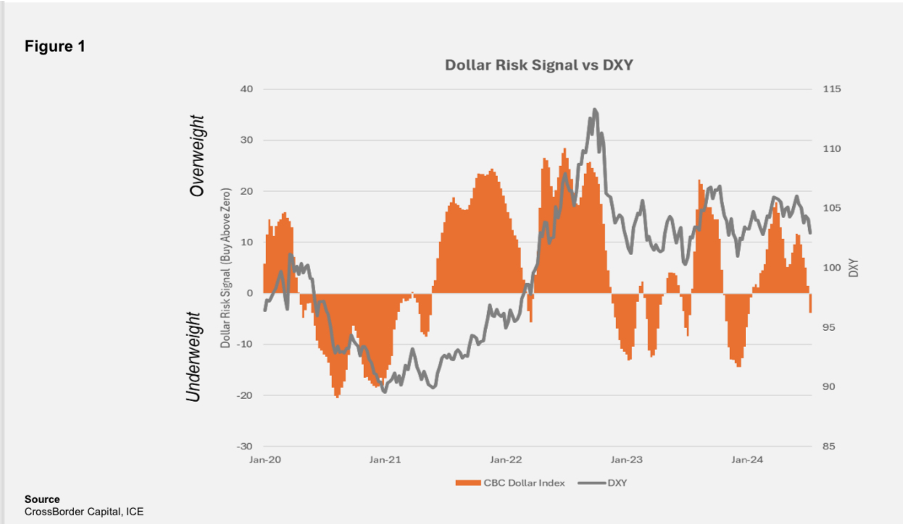

CrossBorder Capital

Has the US dollar turned?

The outlook for the US dollar has turned bearish as previously robust inflows of foreign capital into US assets have decreased, dampening the US real effective exchange rate. Combined with global and domestic economic uncertainties and recent Asian tightening, US liquidity injections have stalled, with bank reserves approaching precarious levels. These structural factors, including instability in cross-border capital flows to the US and increasingly reactive liquidity management by the Fed and Treasury, are poised to weigh on the dollar. Michael Howell suspects that this is a strategic risk-off move in the dollar, with large DM currencies to benefit. He favours JPY, EUR, CHF and GBP over AUD and NZD.

Talking Heads Macro

Australia: A matter of time before the RBA changes its tune

The Australian economy is unremarkable and will slow further, but the RBA’s refusal to ease is an outlier. Manoj Pradhan explains that one of the two has to give. Widespread demand weakness is likely to translate in the classic manner to an already-softening labour market, with only state-sponsored fiscal policy standing in the way. Even the bulwark of immigration has softened and will weaken further. The country’s short-term neutral interest rate, r*, is much lower than the US and most of the G10. He recommends receiving AUS 2y1y (outright or vs US 2y1y, which he’s already paid). Australia 2y1y makes more sense close to 2%, while the US 2y1y needs to edge towards 3.5% without a fundamental trigger for a recession.

GFC Economics

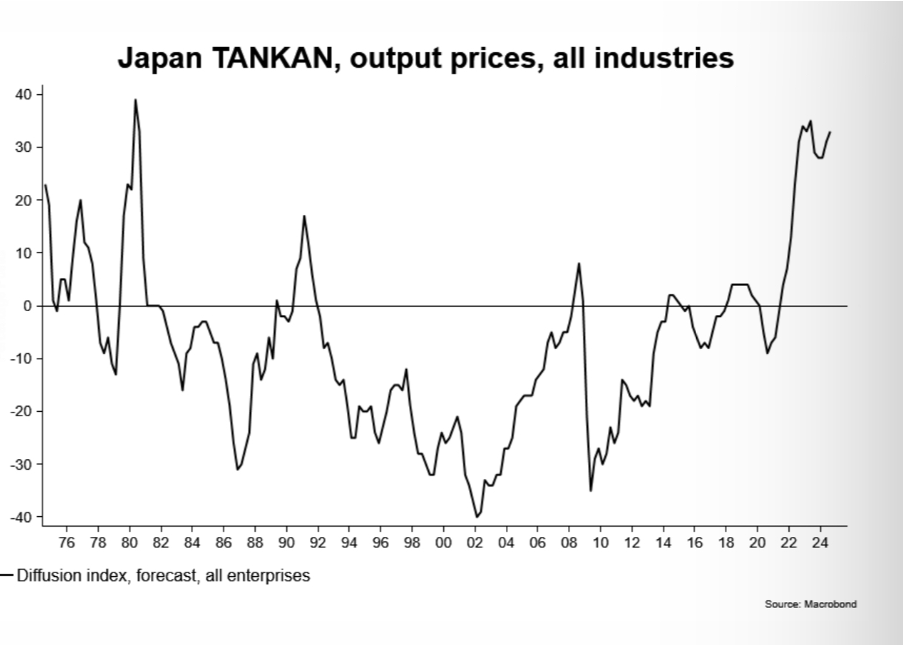

Japan: BoJ could be more hawkish than markets anticipate

Real wages are finally beginning to turn up; employee compensation in Q2 rose 0.8% y/y in real terms. The consumption deflator increased 2.9% y/y in Q2. But cost pressures have been broadening across the economy. The GFCF deflator, for example, climbed 3.7% y/y in Q2. According to the June 2024 Tankan survey, price pressures are forecast to intensify again in the non-manufacturing sector in Q3. The forecast employment diffusion index also fell to a new multi-decade low. The BoJ is still in the early stages of a tightening cycle, while the Fed is cutting. This is rare. This should ultimately be supportive of the yen but the mispricing in JGBs is arguably starker. Demetris Pachnis and Graham Turner believe that the BoJ will be more hawkish than markets currently anticipate. The two-year JGB yield is still just 0.37%, which looks completely out of sync with where Japanese monetary policy is headed.

Greenmantle

Korea: No credit for Yoon

South Korea’s economy remains resilient thanks to continued momentum in exports and reviving private demand. Regardless, President Yoon Suk-yeol and the ruling conservative People Power Party (PPP) face political headwinds, including a wave of impeachments. Niall Ferguson is short South Korean equities, as rates stay higher for longer in 2H24 and Chinese competition seizes exporters’ market shares. A Harris win in the US will leave their relationship with Korea largely unchanged. A Trump success would be a setback for exporters due to potential renegotiation of KORUS and pressure to appreciate the KRW, but his administration would increase pressure on US allies to raise defence spending. Even if this doesn’t happen, the defence industry is faring nicely with healthy profits and limited competition and will benefit from a bipartisan consensus to support the industry. Niall is long the South Korean defence sector.

Emerging Markets

Emerging Advisors Group

All the arguments in Argentina

Jonathan Anderson asks if Argentina is a raging success or looming failure. The Milei administration has put the budget into surplus; external deficits have disappeared and sequential inflation has come down sharply. However, Peso credit and wages are exploding at 230% y/y and rising, banks won't stop lending and the central bank won't stop accommodating. And the main reason monthly inflation has fallen is that the government has artificially re-pegged the peso, while the black market exchange rate continues to depreciate. Jonathan fears that this is a case of failure. In the current environment inflation will almost inevitably pick up again, import pressures will likely resurge and the peso regime faces a strong risk of renewed blow-out, taking Argentina into another round of destabilisation.

PRC Macro

China: More consumption stimulus rumours

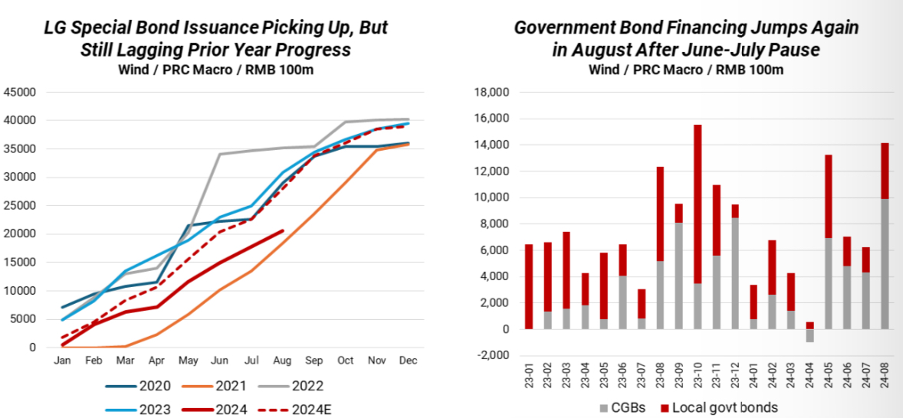

William Hess has very low confidence in rumoured additional stimulus involving either or both RMB 2trn in additional CGBs in H2 and RMB 1trn in consumer vouchers to stimulate consumption. He sees low probability of an increase to the annual deficit, with planners favouring accelerating investment in strategic infrastructure and industrial capacity. However, William does expect a consumer voucher programme for the National Day Holiday, but it will be limited in size and impact. Even without additional stimulus, the acceleration to fiscal spending in H2 will be sufficient to boost growth and base metal demand in Q4 and likely Q1 next year. There are already signs of a re-acceleration to infrastructure project approvals and government bond issuance after May (see chart).

Alberdi Partners

Colombia: More hawkish than it appears

Activity contracted strongly in June, but July’s data shows a better outlook, although Marcos Buscaglia is downgrading his 2024 and 2025 GDP growth forecasts. Headline inflation went under 7% year-over-year for the first time since January 2022, as expectations continue edging down slowly but are still unanchored from the centre of the target band. There is a debate on whether Banrep will accelerate the pace of rate cuts in the last three meetings of the year. Marcos' updated Taylor rule model is more hawkish than consensus for both 2024 and 2025 in both the baseline and alternative scenarios, and he maintains his call that rates will drop by 50bp in the next three meetings, sending it to 9.25% by year-end.

Emerging Advisors Group

Staying put in Mongolia

The macroeconomic environment in Mongolia today remains very positive, with booming export earnings and a favourable external position; the budget is in surplus, the tugrik is appreciating at the margin and sovereign dollar spreads have narrowed. With ongoing investment in export capacity and related infrastructure, Jonathan Anderson expects further gains ahead. The source of downside risk, of course, is China, as the current property market shakeout raises the potential for macro volatility in Mongolia's main (indeed, virtually sole) export market. But on balance Jonathan believes that property woes will have only limited impact on mainland demand for Mongolian coal and copper as we have seen in the past couple of years. As a result, he stays invested in Mongolian equities and dollar credit on the back of medium-term structural growth prospects.

ESG

Sustainable Market Strategies

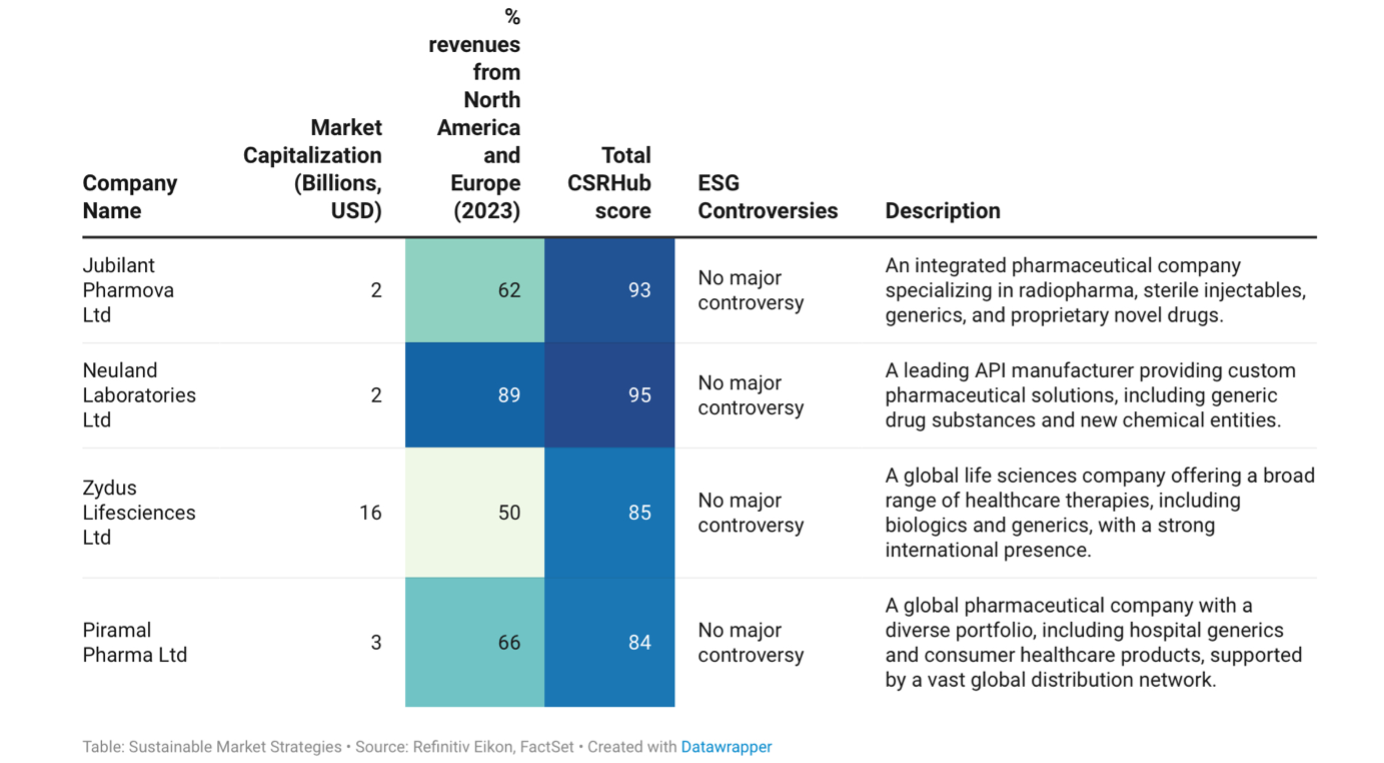

From globalisation to reshoring

In a world shrouded by uncertainty, there is a clear consensus: deglobalisation is taking hold. In Sustainable Market Strategies’ latest note, they evaluate how strong the trend really is and what this means for investors. So far, it has manifested itself as a shift in trading partners rather than a true de-linking of the economy. There are some standout winners, including Mexico, India and Vietnam, but the latter has limited equity investment opportunities due to ongoing ESG issues. The unprecedented shortage of drugs in the US and Europe presents significant opportunities for India’s pharmaceutical industry, and the country’s ESG pharma stocks are poised to climb. Top potential plays include Jubilant Pharmova, Neuland Laboratories, Zydus Lifesciences and Piramal Pharma (see chart). Alongside Indian pharma, the team advise looking at US industrials and Mexico manufacturing to ride the deglobalisation wave.

Commodities

Meridian Macro Research

Cautious optimism for a gold breakout

[Published 17th Aug] Gold jumped more than 3% last week to a record high of $2,508/oz. This following a deluge of (mostly) weak macro updates: PPI was weaker than expected m/m and y/y; CPI y/y also weaker than expected; Retail Sales were still negative y/y on Real basis; UMichSentiment improved a bit but Real Income expectations hit a record low; Housing Starts were weaker than expected, tumbling to April-May 2020 level; Industrial Production turned negative y/y. Additionally: the Dollar (DXY index) finished the week at 7-month lows. Eric Pomboy is cautiously optimistic this week's gold move signals the next leg higher is getting underway. Silver will need to play some real catch-up in coming days to confirm the breakout, plus the metals will need to hold their ground should market risk-off episode(s) return.

ERA Research

Lumber prices remain in uptrend

Lumber prices remained in an upward trend last week, driven by a myriad of supply-side factors, while demand remained steady at best. S-P-F 2x4 prices finished the week up another $10 at $375, while SYP 2x4s were one of the few products that did not see w/w increases and were unchanged at $334. A looming rail stoppage in Canada and an indefinite curtailment announcement by Interfor (a combined 330MMbf of annual capacity at Meldrim and Summerville) caught buyers’ attention, but lumber takeaway was hampered by inclement weather across large parts of the US South. ERA anticipates that prices will continue to grind modestly higher over the coming weeks as builders gear up for the fall construction season, although a more appreciable improvement in demand may remain elusive until spring 2025 as markets await a first Fed rate cut.

Global Mining Research

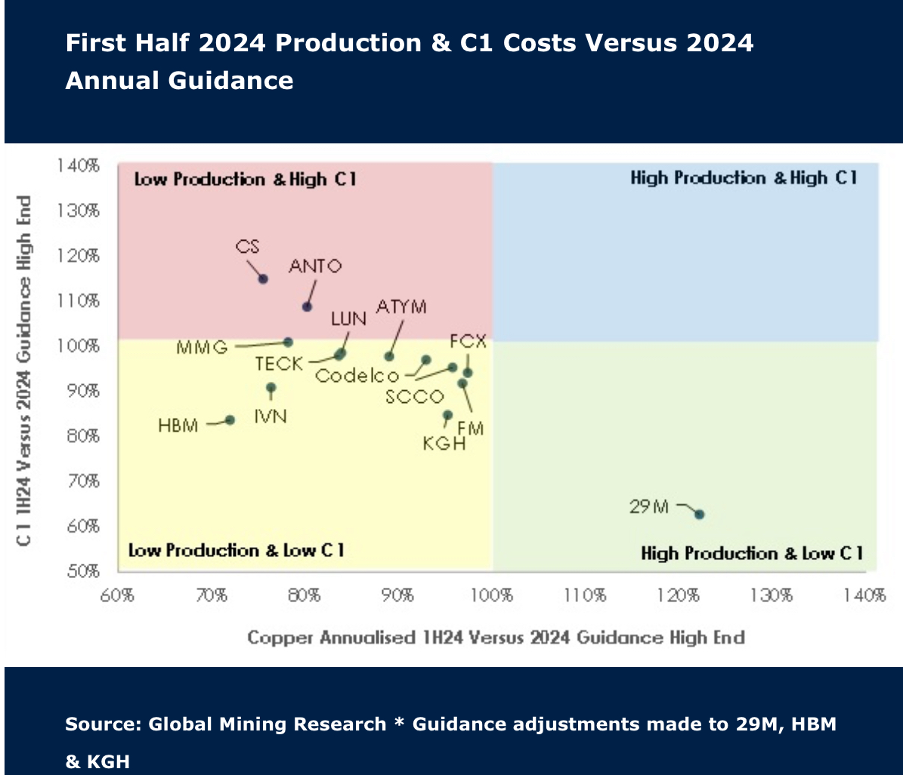

Can copper volumes meet big expectations?

As expected, the first half of the year was met with weaker production, with companies in Global Mining Research’s coverage reporting flat figures of +1.5% and low capex. Costs increased some 4.8%, but this was offset by a ~US$0.60/lb increase in copper prices in the latest quarter. 60% of producers are expecting stronger H2 volumes, but Antofagasta, Ero Copper, Ivanhoe Mines and Capstone Copper are most at risk of missing 2024 guidance. Following the recent pullback and ahead of seasonally stronger Q4 prices, GMR continues to see the sector as attractive. Ratings have been raised for leveraged plays KGHM (to buy) and MMG (to hold).