Company & Sector Research

Europe

Smart Insider

Per Waldemarson (CEO since 2019, joined 2009) has made another purchase, spending €532k on August 2nd at SEK 307.30 and increasing his holdings by 3% to 758,500 shares. He has developed an excellent record when it comes to acquiring stock, based on 12 prior purchases, and qualifies as a "Smart Buyer". Smart Insider ranked the stock +1 on April 25th based primarily on a €444k purchase from him at SEK 258. The stock is up ~20% since that upgrade and it is interesting to see another large purchase from him.

the IDEA!

DSFIR looks to have the turned the corner with 1H24 results showing a clear beat of consensus almost across the board. Results are helped by an acceleration of sales growth in Q2 (vs. Q1) and by cost synergies as well as the impact of the vitamin transformation programme. Particularly impressive were the Y/Y sales growth in P&B and TTH, which accelerated from LSD in Q1 (+1.4% and +3.4%, respectively) to +13.1% (P&B) and +9.6% (TTH) in Q2. While the other two divisions showed positive growth as well. Overall, the results provide the IDEA! with even more confidence that the company is on the right course towards delivery on what it promised at the time of the merger.

Forensic Alpha

Following the publication of its Q2 report, AIXA has moved to Forensic Alpha’s top risk rating. In large part this is due to the sharply rising level of inventory on the balance sheet (€429m = 44% of total assets and represents 17 months of sales). Investors may not have noticed the sheer extent of the increase because it has occurred steadily over several quarters (in 4Q20 inventory was €79m = 13% of total assets and 6 months of sales). Management continues to claim the build-up is due to the anticipation of higher expected volumes. A more troubling explanation is that production has been kept high to maintain gross margins.

Cerundolo Investment Research

Guy Cerundolo provides a basket of long ideas in Europe. These stocks have good and improving multi-factor model scores. In addition to SAP (see chart) he also highlights companies including ASM International, Assa Abloy, CRH, Ferrovial, Philips, Rolls-Royce and Tesco.

North America

Kailash Capital Research

The cardinal sin of artificial intelligence & finance

Having received pushback on a bullish piece KCR had written on Cardinal Health (describing it as a low-quality company that deserved to be cheap), they discovered that the disparity in views was caused by the failure of two separate AI-driven products. Sold to financial professionals and institutions as efficiency tools, both rendered wildly inaccurate calculations for ROIC for CAH. In KCR's latest report, they look to 1) set the record “straight” on CAH; 2) demonstrate that high-quality stocks are as overvalued today as they were in 1999; and 3) show that active management can help investors purchase top-quality stocks at cheap prices.

Real Street Retail Research

Beauty retail disruption

Ulta share losses accelerate as Sephora, TJX and Amazon are set up to win in US Beauty this fall / holiday. Q2 was a bloodbath at Ulta with historical promotional levels and muted traffic vs. Sephora. Amazon Prime Day highlighted new, exclusive product and the migration of prestige & luxury brands. TJX's core beauty presence continues to ramp up as holiday approaches. At the current level of execution, H2 appears bleaker than guidance.

JJK Research Associates

Janet Kloppenburg has been disappointed with LULU's merchandising execution in recent months. Despite management’s confidence that newness would accelerate in Q2 and into 2H24, Janet has not observed any significant new introductions beyond the troubled Breezethrough collection, resulting in bland / basic assortments. She is concerned that the brand may have fallen behind and is chasing the trends, rather than leading as has been the case historically. This lost opportunity may constrain LULU’s North American turnaround, which guidance assumes will emerge in the second half of this year.

Quo Vadis Capital

John Zolidis believes 2Q24 results highlight two facts about YUMC: 1) It has a very powerful set of fundamentals. It is growing units at a DD rate. It is maintaining DD EBITDA margins. The company has $3.1bn in cash net of borrowings (23% of the market value) and John expects $1.5bn in capital return this year. 2) Management continues to impress. YUMC did post negative SSS, but both KFC and Pizza Hut grew transactions. Meanwhile, margins were resilient and above his estimates. At the current price, investors are being offered YUMC's growth and FCF at a significant discount.

Paragon Intel

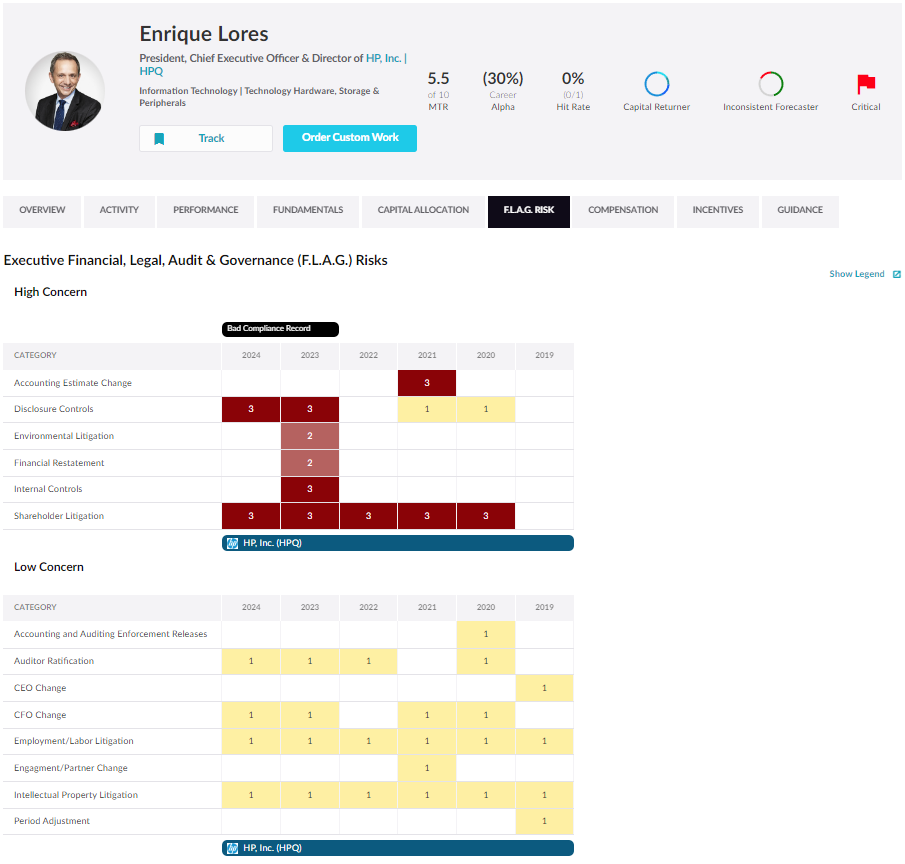

Enrique Lores replaces John Donahoe as Independent Board Chair. Lores has overseen more than 98% alpha destruction as a member of PYPL’s board since he joined in 2021 and has not created alpha as a CEO nor a board member in his career. In 2023 he received a "Bad Compliance Record" tag because of his "Level 3" Disclosure Controls and Internal Controls F.L.A.G. (Financial, Legal, Audit, Governance) Risks at HP Inc. Paragon also cautions about his incentive compensation - after only hitting 56% of his incentive targets from 2020-2022, Lores was able to convince the board to materially lower his 2023 incentive thresholds...and he was able to meet or beat all of those targets last year.

MYST Advisors

Industrials Idea Forum

Despite the uncertain economic backdrop, presenters at MYST's latest buy-side event, once again offered only long ideas. It was also unusual that >50% of the stocks pitched at a generalist industrials event were Transports / Energy-related names. Perhaps this speaks to the recent rotation into early cyclicals. Some of the most compelling ideas include:

Barnes (B) - Aerospace transition story with activist involvement + M&A optionality. TP $60 (60% upside).

Lineage (LINE) - “High tech” cold storage REIT with superior growth / margin profile vs. peers. TP $115 (30% upside).

Proficient Auto Logistics (PAL) - Auto transport rollup poised for strong EPS growth under former Saia “Rockstar” CEO. TP $40 (100%+ upside).

BWS Financial

The share price tanks as Q3 results disappoint after an increase in system costs. During the earnings call, SYM’s management referred to delays in permits and product delivery resulting in people not having anything to do. This is a characterisation of a construction / contracting company and not one developing automated technology. Hamed Khorsand also believes these issues could create additional risks re. its relationship with Walmart. SYM’s share price has already fallen ~45% since he initiated coverage with a Sell rating a few weeks ago, but Hamed stills more than 50% downside.

Fermium Research

Having recently upgraded FMC to Buy following news of Pierre Brondeau's return as CEO, Fermium is heartened by the tangible progress being made on the company's cost reductions. Furthermore, while 3Q guidance was below current consensus (as they expected), the key point is the company’s assertion that 4Q will be materially higher than current estimates, suggesting that the wicked destock since 2Q23 is running its course. Their thesis appears to be playing out. With 2025 set up to be a “normal year”, they remain of the opinion that FMC’s share price will return to more “normal” levels.

Sales Pulse Research

While it is not unusual to hear of CSCO reorganising at the end of its FY, channel chatter is that the upcoming changes are fairly major. CSCO has been one of the companies that SPR hears of replacing senior employees with younger, lower paid staff. Indications are that the only teams that are preforming well are those selling to the public sector. Expectations are low so much of this weakness is baked in, but if investors are expecting signs of improvement, that is not what channels are reporting.

ETR

ETR conducted a CRWD focused flash survey of 100 IT decision makers on the day of the global IT outage to capture the initial impact and reaction to what was unfolding. Nearly 75% of respondents were from large organisations, including 25% from Global 2000 firms. While 56% of respondents were very unlikely or somewhat unlikely to replace CRWD, a similar amount were reconsidering their reliance on the company and expressed disappointment in its testing and response, urging better QA processes and improvement in communication. Since publishing their findings, ETR has gathered CRWD customers who can share how the outage affected their organisations and discuss how it will influence their relationship with the cybersecurity firm moving forward.

Lynx Equity Strategies

Bad news comes in threes. First, there is a new-found realisation that AI returns are not keeping up with massive AI investments. Second, there are macro-related worries. And now third, a report emerged that NVDA’s Blackwell roll-out is being delayed due to “design flaws”. KC Rajkumar is not surprised. In a recent Micron note, he pointed to the potential for heating-related failures of the NVDA GPU-HBM module. His most recent checks now show that NVDA is likely to pause GPU wafer starts at TSMC until yield-issues are resolved. KC expects a hole appearing in NVDA’s 2FH25 product roll-out and revenue ramp. Estimate cuts are on the way. He is looking for the stock to head to the $80 level into the upcoming earnings call. Advanced Micro Devices, on the other hand, could end up being an accidental winner.

Corto Capital Advisors

The share price fell nearly 20% after the company reported worse-than-expected results and is now down over 50% since Zach Shannon recommended shorting ZI in Feb 24, having missed and guided down in each of the subsequent quarters. This week, the company finally cut its full year outlook, wrote off $33m in previously recognised revenue and announced the departure of its CFO. ZI now sees a full-year revenue decline (vs. previous guidance for growth) - something Zach has been flagging all year. In early July, he recommended reducing / covering short exposure on takeover speculation, with a recommendation to re-short into the print.

Emerging Markets

Copley Fund Research

Asia Ex-Japan Funds: Extreme stocks

In this report, Steven Holden screens for stocks at the extreme ends of their positioning or momentum ranges. He synthesises current and historical data on fund positioning with recent manager activity to accurately assess sentiment for each stock within Copley’s coverage. Stocks highlighted include Phoenix Mills and SK Hynix (High Positioning, Positive Momentum); AIA Group and Shenzhen Inovance Technology Co. (High Positioning, Negative Momentum); PT Avia Avian and Wuxi Biologics (Low Positioning, Negative Momentum); New Oriental Education & Technology Group and Shinhan Financial Group (Low Positioning, Positive Momentum).

Your Weekend Reading

The globalisation of WeChat - which has done what Facebook never did - they combined chat, social and payments. And now they are innovating again by going over the top of iOS and Android with Mini-Programs. The Mini-Program combo of apps/social/chat and payments is a superior platform and as businesses outside of China start to realise this Erik@YWR sees users hitting 2bn by 2030. The faster growth of WeChat relative to games and social media will transform the company’s revenue mix. The expanding international customer base will unlock growth in payment fees, advertising and Tencent Cloud. Erik sees EPS over HK$35 in 2028 (vs. HK$20 in 2024). TP HK$1000.

Blue Lotus Research Institute

Online gaming bucks the trend of weak consumption

Blue Lotus’s research suggests game and online video revenues are holding up better than movie theatres and that Tencent, NetEase and Bilibili’s 2Q24 NI will comfortably beat consensus forecasts. Over the past seven years, they have found an inverse relationship between online game and video with offline movie receipts. Gross billings of China’s gaming industry grew by 2.1% Y/Y in 1H24, reversing a decline since 2022. Online video grew by 1.4%. While smaller developers continue to struggle (economies of scale / large companies benefitting from AI investments and acquisitions), Blue Lotus raises their target prices for NetEase and Bilibili. Tencent remains their top pick.

Sandalwood Advisors

Domino's Pizza China's successful store expansion in the country drives better growth than market expectations. Sandalwood’s data highlighted DPC’s outperformance on June 21st and in late July the company published earnings stating total revenue in 1H24 was to improve by no less than +45%, comfortably exceeding the full year consensus of +31-34%. The stock climbed over 10% on the back of this news and also significantly outperformed the Hang Seng Index in June / July.

Horizon Insights

This year, regulation of two-wheeled EVs has intensified, with strict oversight on battery usage, onboard chargers and major component modifications. As the transition period concludes, manufacturers are speeding up the clearance of old vehicle inventories and developing new models that comply with the revised standards. The updated national standard is expected to ease restrictions on speed and vehicle weight but will impose the highest production qualification requirements in history. Consequently, many lower-tier manufacturers will struggle to survive. Horizon Insights believes Ninebot, which has established a strong reputation for its high-end products, looks set to benefit, even at the expense of market leaders including Yadea and Aima.

CHA-AM Advisors

An accident waiting to happen - once the Chinese have finished with the cement industry in Southeast Asia, India will be in their sights next. David Scott’s analysis reveals common characteristics of Indian cement companies to be: 1) Surprisingly low Returns On Equity and On Assets. 2) Extraordinarily high valuations. 3) In a more efficient market the EV/Sales would be a fraction of where they are now. 4) Substantial gearing amongst some of the smaller names. 5) Companies in the sector have been serial share issuers. David dreads to think what happens to UTCEM when the Indian cement boom is over, but sees the whole sector as a Sell.

Macro Research

Developed Markets

Belkin Report

When the tide goes out

Favourite consensus 2024 investment themes hit a brick wall one month ago. Market psychology believed AI was nirvana, the US economy was expanding relentlessly, Japanese and European stocks were must buys, and so on. The mentality is turning out to be wrong, especially highlighted in the recent stock market downturn. Market psychology is also showing signs of changing, with the Nasdaq’s -8% drop while bonds and short-term interest rate futures rallied—until now, any hint of weakness leading to Fed rate cuts was seen as bullish for stocks. Michael Belkin’s model indicates that a long-term global equity bear market has started, with big alpha opportunities in defensive sectors: reits, health care, utilities and staples. Likewise, TBonds have an upward forecast. In an extended bear market, buy-and-hold gets thrashed.

RW Advisory

Behavioural Inflection Reversal: What Next?

Ron William’s prediction (see IRF Podcast here) of a “growing probability of a dramatic ‘flash crash’ risk into Q3, from early August onwards, weighed down by compounding triple whammy headwinds, of momentum extremes, rotation fragility and cycle asymmetric risk” has come true. What next? Despite the sharp oversold reactionary bounce and growing back to normal, soft-landing consensus; RWA remains tactically short in their model portfolio (strategically underweight), with trailing stops, amidst likely elevated volatility, into September, leading to a strategic top in 2025 (see chart mosaic). A barbell strategy is prudent. Keep legacy profits trimmed, hedge further downside risk and build smart portfolio diversification, notably in Gold and other defensive plays.

Steno Research

On credit watch while liquidity is turning nasty

Andreas Steno says everything is about assessing the USD economic cycle and the potential for rate cuts of the magnitude priced in after a crazy week last week. He does have his doubts but is still waiting for potential triggers to bet on it. For now, he sees rates coming even lower as the nasty position squaring “party” is still ongoing. Japan was the most consensus long in the equity space after US tech stocks (until this massive sell-off), while India is third. The Nifty50 is still surprisingly untouched and a potentially vulnerable target for the next position squaring. In the FX space, the CNH is still THE short bet among macro HFs/Multistrats, which is a potential sharp catalyst for a further move lower in USDCNH with contagious spill-overs to the Gold and Silver markets as well.

Andrew Hunt Economics

US: Has the Fed made a fatal error?

Over the last few weeks the budget deficit has jumped, providing a probable stimulus to the economy, and on this basis Andrew Hunt is not forecasting a US recession. The stimulus if successful will trigger higher inflation. However, the budget deficit has not so far been monetised unlike in 2023, which is a crucial difference. The wider deficit is crowding out private sector credit and the NBFI credit boom. If the FOMC wanted to avoid this, it should have cut rates in July; signalling but not enacting a cut actually made the situation worse by implicitly damming the flow of RRP monies into the system. The only way the deficit can be monetised in the near term is by drawing on the TGA. If this is not done, Andrew suspects that the flow of funds to the NBFI boom will fall away, inviting a deflationary contraction that could easily morph into an asset market crash.

Talking Heads Macro

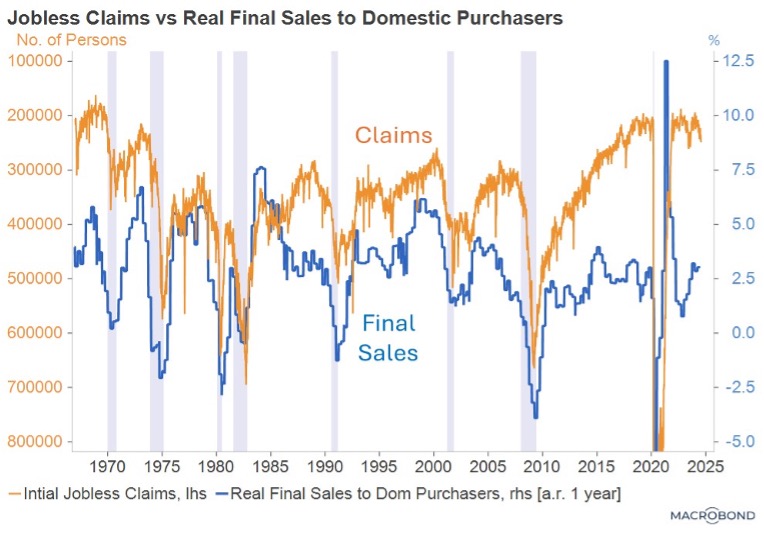

US: Unemployment is an outcome - where’s the fundamental impulse?

In light of the recent broad weakness in the labour market, Manoj Pradhan asks if the deep fundamental drivers suggest a downturn of the market into recession? First, real final sales to domestic producers show similar numbers to 2019, with plenty of resilience in demand and growth. Second, services inflation being higher than goods inflation offers some profit protection to the former industry. Third, real wage growth has only recently turned positive after two years of negative wage growth, and strong monetary and credit tightening has been offset by fiscal policy. This combination is implicitly asking: can labour markets be a leading indicator of the cycle? Manoj closes his long 5y position and opts to pay 2y1y given the 10bps move in Sep already.

Minack Advisors

US: Wild moves say more about the markets than the data

According to Gerard Minack, the reaction to two weak US data prints – manufacturing ISM and non-farm payrolls – says more about market positioning than the economic outlook. Yes, growth is slowing, but there are few signs of recession. The problem is investors had priced a feather-soft economic landing and shrunk risk premia in equity and credit markets. Moreover, the astounding move in dollar-yen hints that a number of inter-connected flows are reversing. This could be a bumpy, soft landing for risk assets. Suddenly, recession fears are back. Most – 75% – Fed tightening cycles end in recession. But Gerard continues to think that a soft landing is more likely than not for three reasons. First, there are no major financial imbalances. Second, the volatile goods sectors – inventories, autos and housing – have been through a cycle. Third, fiscal policy and AI-related investment are likely to remain supportive.

Emerging Markets

Alberdi Partners

Argentina: The ARS overvaluation intensified

Most LatAm currencies weakened against the USD in recent weeks, making the ARS stronger in real terms. Additionally, the country’s Terms of Trade deteriorated. That the peso got stronger does not mean it is overvalued, but Marcos Buscaglia suggests there are many ways to show that it is. One is the Big Mac Index, showing that the currency is almost as expensive as Uruguay’s. There’s also the goods and services imports/exports data and the fact that the central bank is losing reserves, which supports the case of an overvalued peso. Marcos’ model shows that, were capital controls to be lifted, the peso would be overvalued by 33% in real effective terms in 3Q, compared to an overvaluation of 27% in 2Q. For overvaluation to cease in 2025, a strong devaluation or superstrong improvement in productivity and/or the ToT would need to occur.

Emerging Advisors Group

China’s trust sector problems continue to pile up

Over a third of Chinese trust companies are technically insolvent or are on the brink. Jonathan Anderson points out that although the asset quality situation did not worsen in 2024, the longer-term issues look problematic. The core asset quality issues facing trust companies still revolve around the real estate sector, but at the same time an upswell in local government financing vehicles is also causing pain. The good news is that the impending collapse of many trust companies is unlikely to be a catalyst for broader financial contagion. There may also be some good news around the corner, with government efforts to reduce unsustainable deposit inflows beginning to bear fruit. The beneficiary of this shift so far appears to be credit bonds vis inflows into bank wealth management products, but other investment managers will likely benefit.

Trivium China

China: LGFV land grabs create inventory of idle land

Land purchases by local government financing vehicles (LGFVs) have resulted in a massive stock of undeveloped land. Local governments rely on land sales as a key source of revenue, but this has been under pressure as private developers facing financial distress have reduced land acquisitions. In response, local governments have encouraged LGFVs to purchase land. By directing LGFVs to make land purchases, local governments were effectively borrowing this money. However, LGFVs have neither the experience nor sufficient capital to develop properties, and much of their land holdings sit idle. With little prospect of generating income, land purchases have merely escalated financial risks for LGFVs and their government hosts. Reducing their massive and unproductive land stock will require local government buybacks or land transfers to more robust state-owned enterprises. Either approach will require substantial support from the central government.

Burumcekci Research & Consulting

Turkey: Inflation outlook does not support rate cut expectation

In July, the CPI increased by 3.23%, while the annual CPI fell from 71.60% in the previous month to 61.78%. Haluk Burumcekci points out that the upward impact of external factors on inflation is significantly decreasing, and if the moderate trend in exchange rates continues, and no new shocks are observed in wages, administered prices, and commodity prices, the monthly inflation trend could slow again from September onwards. However, the recent hawkish messages from the Central Bank suggest that interest rate cuts are not imminent. In its July MPC meeting, the Central Bank kept the one-week repo rate steady at 50.0%, with the main message on monetary policy stance being that a tight stance will be maintained until a significant and permanent decline in the main trend of monthly inflation is achieved and inflation expectations converge towards the forecast range.

Greenmantle

The history of fraud in Venezuela

After a fraudulent election on July 28th, Nicolás Maduro has been proclaimed Venezuela’s president-elect. As the international community questions the results and the opposition calls on the population to protest, Niall Ferguson reviews previous fraudulent electoral cycles that could serve as a guide for what is to come. Using this applied history framework, he finds that the factors that will determine the ultimate outcome are: a) the cohesion of the Venezuelan armed forces, b) the resistance of the opposition, and c) the ability to coordinate and mobilise civil protests, both inside the country and abroad. Given both Venezuela’s history and the current state of affairs, Niall believes that the military still has incentives to support Maduro at this stage, even if there are some low-level defections. Unless the military supports civil efforts to overthrow Maduro, a transition is unlikely.

ESG

Verisk Maplecroft

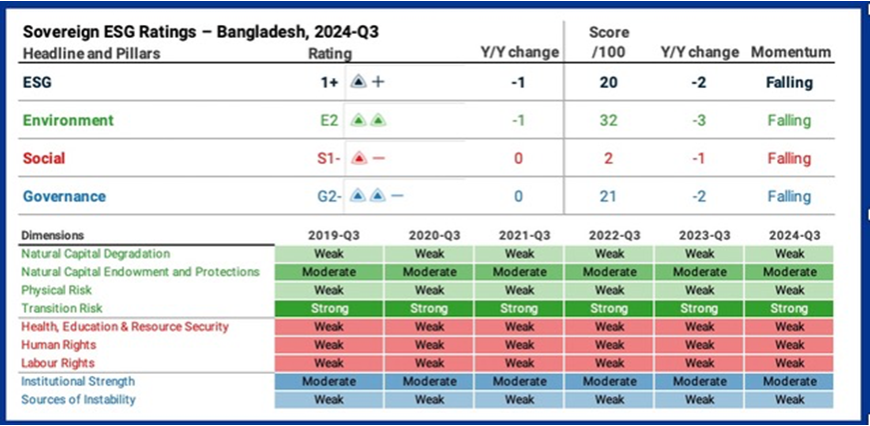

Bangladesh: The end of Hasina

PM Hasina resigned and left the country in response to mass protests. Although Hasina’s reign was marked by a severe crackdown on opposition forces, limiting the space for dissent, Bangladesh’s score on Maplecroft’s Government Collapse Index had consistently registered in the extreme-risk category. Despite stronger economic growth during recent years, the ex-PM’s reign saw little to no improvements across the S and G indices in their Sovereign ESG model. The country also registers in the extreme risk category in the Reserve Adequacy and Import Cover indices, underlying its precarious external debt situation and the potential challenges of upcoming repayment obligations estimated at USD 4.5 billion in 2025-2026.

Sustainable Market Strategies

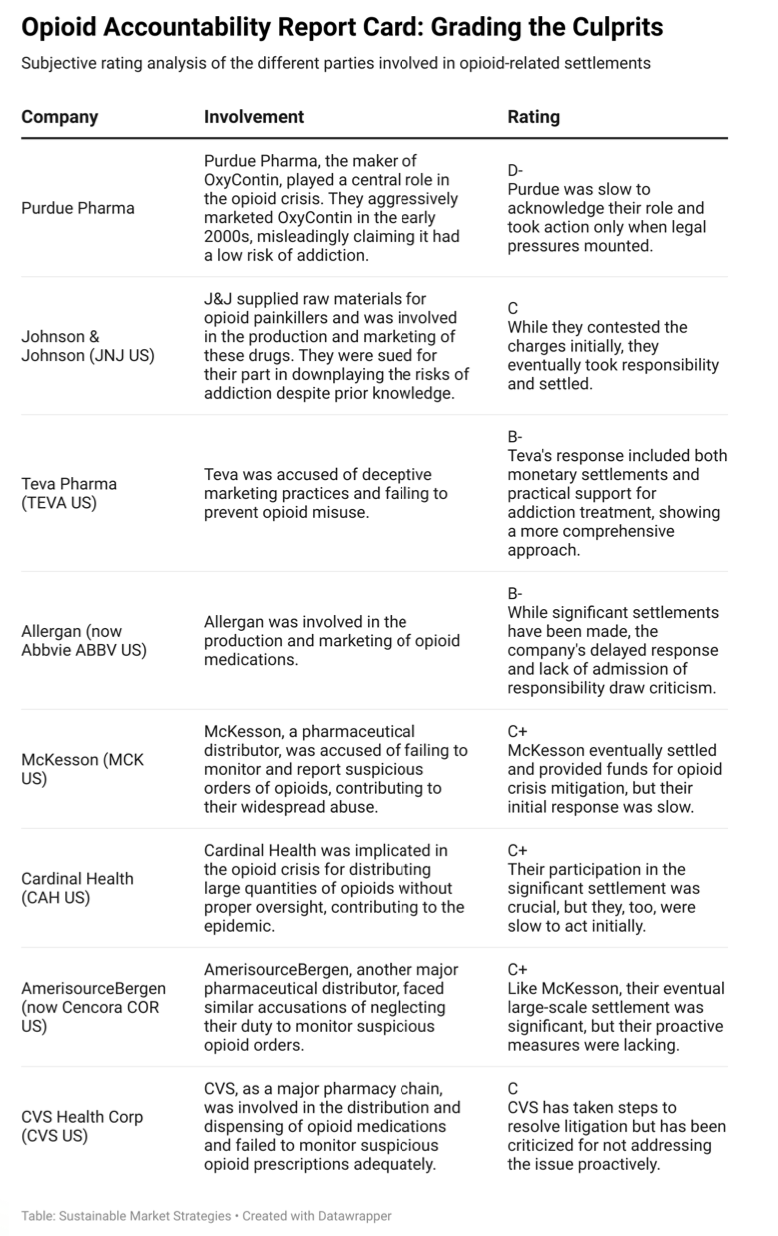

The pain trade: The new frontier of non-opioid treatments

America’s opioid crisis is a major societal issue largely ignored by the financial community, with devastating effects on the US economy and labour force participation. Although a large share of the blame must go to pharma companies that designed, manufactured and promoted the products, other parts of the healthcare sector also share responsibility. Current equity investors should note what role publicly-listed healthcare companies played and how they responded to accusations (see chart). Looking ahead, the implementation of the NOPAIN Act could mark a significant inflection point for investors seeking to address the opioid crisis through strategic capital allocation. Companies such as Pacira BioSciences, Indivior and Vertex Pharmaceuticals are leading efforts to provide alternatives to opioid dependence. By boosting non-opioid alternatives, the Act opens new investment avenues for impact-minded investors.

Commodities

ERA Research

Pulp sellers blink in China

Pulp prices in China have been rangebound since early June, with Chinese buyers and sellers locked in a standoff. Given the huge week over week PIX China pulp price changes (chart), the producers have blinked first. PIX prices dropped $48 and BHK fell by an astounding $91, a correction of a magnitude that would usually take weeks to occur. Expect other international markets to see accelerated price drops as a result. The biggest market-pulp consumers are tissue producers and in ERA’s stock coverage Cascades is expected to benefit the most. Pulp producers are the losers, including Mercer International and International Paper. Expect pulp names to remain under pressure for at least a quarter, or until closures accelerate.

CPM Group

Gold and silver: Future projections

In his latest video, Jeffrey Christian discusses the recent market sell-off and CPM Group's projections for gold, silver, financial markets and the global economy. Jeffrey explains the significance of rising unemployment rates and puts them in historical context, leading to a discussion about whether the current employment and market conditions are as dire as they seem. The video concludes with an updated view of CPM Group's short and long-term outlooks for gold and silver.

Click here to watch.