Company & Sector Research

Europe

Woozle Research

Feedback from Woozle's latest channel checks remains positive - estimates Q2 volumes +5% Y/Y and pricing +4%. Several dealerships noted that order books remain full and wait lists are growing. Unsurprisingly, respondents noted that there have been no price cuts or any element of discounting. However, several respondents did note that Ferrari has become more proactive in hosting car events and experiences at dealerships to boost heat around new models. Purosangue models received positive feedback, as did Roma Spider and 296 GTB designs. In regards to hybrid models, initial optimism from respondents during Q1 has started to wane somewhat in this quarter.

Alumbra Research

The share price tanks as management warns FY24 EBIT will be 31% lower than forecast. Alumbra had previously raised concerns that expectations were overly optimistic considering the likely non-recurring prior year benefits from: 1) normalising excess equipment order backlog and 2) low quality sources of EBIT such as higher capitalised R&D, lower inventory impairment charges and lower bad debt expense. In addition, Alumbra highlighted that an increase in related party receivables relative to APAC revenues in Q423 could be indicative of higher channel fill in China and that intensifying competition with STAAR Surgical could also weigh on revenue / margin growth. AFX has fallen 32% since Alumbra turned bearish in Jan 24.

Off Wall Street

Poor performance is primarily the result of fundamental competitive issues and industry headwinds - OWS believes the new management team’s ambitious turnaround targets will not be met. While bulls view SN as a value stock and a turnaround story, the company’s underlying financial position appears to be far weaker than investors appreciate. SN reported adj. EBITDA and “trading cash flow” of $1.3bn and $635m, respectively, in 2023. However, by OWS's calculation, FCF was just $129m in 2023. Hidden behind its heavily adjusted metrics, SN is in a precarious financial position. TP £7.00 (30% downside).

ROCGA Research

ROCGA’s Cash Flow Returns On Investments based online platform provides a systematic framework to compare and value companies. Factor analysis shows Sixt to be undervalued. These include various valuation indicators, ROCGA's proprietary valuation and modelling tools, as well as growth indicators. Apart from their proprietary economic returns and conventional valuation indicators, data points such as EV/IC against ROIC/WACC are also available. ROCGA's interactive tools allow you to model and value one of 2000 companies across Europe and the US. A free consultation and trial can be arranged on request.

North America

MYST Advisors

Special Situations Idea Forum

The majority of stocks presented at MYST’s latest buy-side event had very near-term (<6 months) catalysts to unlock value either through business transformations, fundamental business inflections, M&A / spin-off activities, or “technical” tailwinds. Ideas included:

Core Scientific (CORZ) - Bitcoin mining conversion provides “shortcut” to new data centre capacity. TP $18 (85% upside).

Golar LNG (GLNG) - “Orphan stock” nearing closure of multiple lucrative long-term FLNG vessel contracts. TP $75 (145% upside).

Jacobs Solutions (J) - Long-awaited exit from “deal purgatory” to finally showcase fundamental strength. TP $180 (30% upside).

Teck Resources (TECK) - Coal divestiture creates significant re-rate potential / M&A optionality. TP $65 (35% upside).

Periphery Research Partners

One thing that has seemingly gone unnoticed is that DASH’s take-rate has been topping out on a sequential basis since 2Q23. Hesham Shaaban believes DASH had been reinvesting subscription revenues into promos (revenue offsets) to drive GOV growth. But DASH ended 2023 with only 20% more subs on a y/y basis (vs. 50% in 2022), so it is working with less incremental subscription revenue to offset the promos needed to buoy an even larger GOV basis this year. Collectively, this suggests that take-rates may be under pressure; he is expecting take-rates to flatten out if not decline on a sequential basis this year, while consensus is assuming consistent expansion through 4Q24. Hesham is eyeing 4Q24 for an EBITDA miss on guidance, but suspects 3Q24 GOV or EBITDA guidance could come in light as well.

Arete Research

Arete sees a $4.5-5bn EBITDA improvement from streaming by the end of the decade and thinks that the expected loss of the NBA means that '26E will likely mark the low-point of group EBITDA (at ~$9.4bn), before international streaming growth is sufficient to offset linear declines. The market is clearly not expecting any stabilisation right now, with the stock implied at <3x P/FCF in '25E. Leverage should hit management's 2.5-3 turn target range in '25E and WBD would then be able to buy back stock very accretively. This scenario creates a significant potential upside case, with Arete’s revised TP of $24 implying the shares could more than triple, and yet still trade only at ~10x trough P/FCF.

Sidoti & Company

Better-than-expected 4Q24 results in a challenging operating environment are encouraging and reaffirm Sidoti’s bullish view on the stock. After severe weather-related disruptions in Jan, demand rebounded and LZB benefitted from solid in-store execution, store base growth and record-high conversion rates and gains in average ticket. With initial 1Q25 guidance above forecasts, Sidoti raises their FY25 and FY26 EPS estimates to $3.22 and $3.72, respectively (from $3.08 and $3.58 previously). FCF per share will total $2.64 in FY25 and $3.45 in FY26; the company will use most of the FCF for dividends and share buybacks. TP increased to $45.

Quo Vadis Capital

$1bn retailer of non-discretionary product trading at lowest-ever price and multiple. John Zolidis sees comps improving as 1) replacement cycle revs up, 2) remote medicine initiative adds capacity and 3) maturation from recent store openings. Based on his estimates, investors are getting the unit growth for free. Assuming modest comp recovery and MSD EBIT (consistent with low end of guidance) an 8x EV/EBITDA results in a ~40% return vs. 14% downside over the next 12 months. Over 3 years, John estimates a ~90% return. However, if the multiple even modestly re-rates (e.g. to 10x vs. historical average of 16x) a 3-year return could be >140%.

Tabbush Report

Consumer credit card risks: Buy now, default later?

Monoline companies are seeing dramatically higher credit costs or net charge-offs or both. Many banks are seeing the same. It is often the case that a financial crisis is more visible at the fringes before it is visible mainstream. This may be the situation now with US financials, driven by worsening credit metrics in consumer card loans. With delinquent credit card loans as a percentage of total delinquent loans in the US now higher than in any recent crisis, investors must pay more attention here and not fall prey to myopically focusing on commercial real estate risks. Company-specific data generally suggests figures can worsen considerably, despite an already rapid deterioration.

Abacus Research

RKT is well placed to accelerate market-share gains in the current down market. Smaller non-bank operators are being pushed out of the channel, plus banks are scaling back their mortgage businesses. Basel III could accelerate this. ~30-35% of people employed by the industry have exited and remaining loan officer pay has fallen ~50%. Cyclically mortgage volumes look unlikely to get much worse, especially if we see a rate cut cycle start sometime this year. Based on Abacus’ estimated normalised mortgage industry volume, they see RKT earning $1.10 EPS in 2026-2027 period (vs. 2026 consensus est of $0.82). TP $19.50 (40% upside).

Kailash Capital Research

The drug distributor possesses three of the most prized attributes of any stock 1) strong, predictable growth prospects; 2) low business risk; and 3) normalised FCF generation capability of >$2bn p.a.. CAH trades at only a 13.4x P/E multiple, a ~35% discount to the S&P 500 Index, while also trading at a substantial discount to Cencora and McKesson (avg. P/E 17x), despite having broadly similar growth prospects, cash-generating ability and balance sheet strength. If CAH shares were accorded a P/E multiple in line with the S&P 500, a very reasonable target, the stock would be trading ~50% higher than the current price.

Northcoast Research

Buzzing the tower: A high-speed review of aerospace channel insights

Channel reads through June provide greater backing to Northcoast’s bearish near-term call on the aerospace supply chain. As a result, they maintain their lower investment ratings for the upstream suppliers and the specialty materials group, and they anticipate a reset of estimates to a lower level in the next twelve to eighteen months. Based on the responses from contacts, the survey data clearly shows a negative demand environment (or downward momentum in 2Q24), which is in line with what other channels have said. Early warning signals also seem to be spreading beyond the problem areas Northcoast identified in their last market update, such as jet engine manufacturers, European-based suppliers, the Boeing supply chain and premium forgers.

Hedgeye

Attempts to expand into new areas, such as CRM and developer-focused products, have had limited success, with low penetration rates and integration challenges. Hedgeye does not believe MNDY will successfully bridge the gap from point solution to platform. Meanwhile, in Jan 24, the firm implemented a 20% price increase for customers. This will lead to increased churn/seat reductions and negatively impact win rates on new business. Operating in a highly competitive market with low barriers to entry, MNDY faces rivalry from established players in work management, CRM and devops - ultimately positioning its core product as an add-on solution within a broader ecosystem.

AceCamp International

SMCI's share price has risen over 300% since AceCamp turned bullish in 2Q23. However, their recent analysis suggests a potential inflection point in the company's trajectory. Intensified H100 server pricing competition could lead SMCI non-GAAP EPS to grow only 17%/4% Y/Y to $27.3/$28.3 in FY24/FY25, 30-40% below consensus estimates. Considering margin pressure and growth headwinds, a contraction from the current elevated multiple to a 10-15x FY25 PE range appears increasingly likely, implying over 50% downside.

ETR

Survey data suggests more friction converting customers to SaaS - ETR’s Technology Spending Intention Survey (TSIS) results have shown a 28-point Net Score decline over the past two years and preliminary July Net Score data puts VRNS as the second lowest among publicly traded security vendors. The company has executed its first SaaS transition phase well, but ETR’s data reflects declining spending intentions among existing customers it aims to convert. AI adoption is expected to grow the volume and complexity of enterprise data use, but ETR sees increasing competition from Microsoft, large security platform companies and AI-focused security start-ups.

Japan

Astris Advisory Japan

NTT shares have dramatically underperformed the overall market and peers YTD as a weak Q4 print disappointed investors. However, Kirk Boodry thinks the reaction is overdone with medium-term guidance intact, including a rebound in profitability by FY25. The shares look attractive with >40% potential upside. Kirk assumes compound annual revenue growth of 3% across his forecast period with corresponding 4% growth in operating profit and EBITDA. FCF should grow MSD. His forecasts also include a 7% EPS CAGR through 2030 as consistent share buybacks provide an extra kicker to profit growth.

JapaneseIPO.com

The company has experienced a fivefold increase in book sales compared to 2016, with a consistent rise in sales outside the Covid-period. Operating profit was up 43% Y/Y in FY23, achieving an operating margin of 27.3% - the highest in the Japanese publishing industry. Additionally, the company boasts an ROE of 23% and is debt-free. In her latest report, Yuka Marosek explains why she believes the group's unique “one-source-multi-use-loop system” is set up to ensure a steady stream of likely-big-hit content. The stock trades on a 6.5x P/E multiple (FY25) and P/B of 1.82x.

Galliano's Financials Research

Norinchukin Bank is an outlier not a sector indicator

The bank plans to sell JPY10trn of foreign government bonds, crystallising a chunk of the JPY2.19trn of unrealised bond losses, as it also looks to raise JPY1.2trn. In this note, Victor Galliano explores the bigger cap banks’ foreign bond holding and unrealised gains or losses, including those of Japan Post Bank. He believes Norinchukin is a sector outlier rather than big cap bank canary in the coalmine. Victor sticks with buys on Resona, Mizuho, SMFG and Concordia.

Emerging Markets

Smart Insider

Jiarong Chen (Director since 2020) sells US$18.5m worth of stock at an average price of HKD 2.64, reducing his holding by 68%. This sale is indirect, on behalf Jubilee Prestige Investments Limited, which is wholly owned by the director. It is the lowest price he has ever sold shares. Chen has a short but good record as a seller. He started to sell in Dec 23 at HKD 3.51. It is concerning to see him continuously selling in large absolute size and at a lower price. Smart Insider ranks the stock -1 (lowest rating).

India Independent Insight

Based on Iii’s latest interactions with business partners of Eureka Forbes, it is quite evident that the company is not interested in developing its offline sales channels (i.e. the franchises). Product quality and service-related issues continue to impact referrals, which used to account for nearly 70% of a franchise partner’s source of leads. The increased cost of ownership is causing customers to look for alternatives. The strategy of splitting sales and service franchise partners also does not bode well for the company’s market development. Premiumisation has few takers while the disconnect between ground realities and management is also quite alarming.

AlphaMena

The share price has risen more than 150% post Covid, but AlphaMena still sees over 30% upside. Strong 1Q24 results were reassuring and AlphaMena remains confident about ADCB’s business model based on the expansion of its core businesses powered by digitisation, portfolio de-risking and disciplined cost management. The lender also possesses the highest rating on AlphaMena’s Fundamental Strength Indicator, a set of metrics that help gauge stocks on their financial and operating performance. The stock continues to trade at a discount to its 2019 P/B while the organic capital generation has noticeably improved. Finally, ADCB offers a generous payout (7% dividend yield).

Macro Research

Developed Markets

Totem Macro

Liminal state

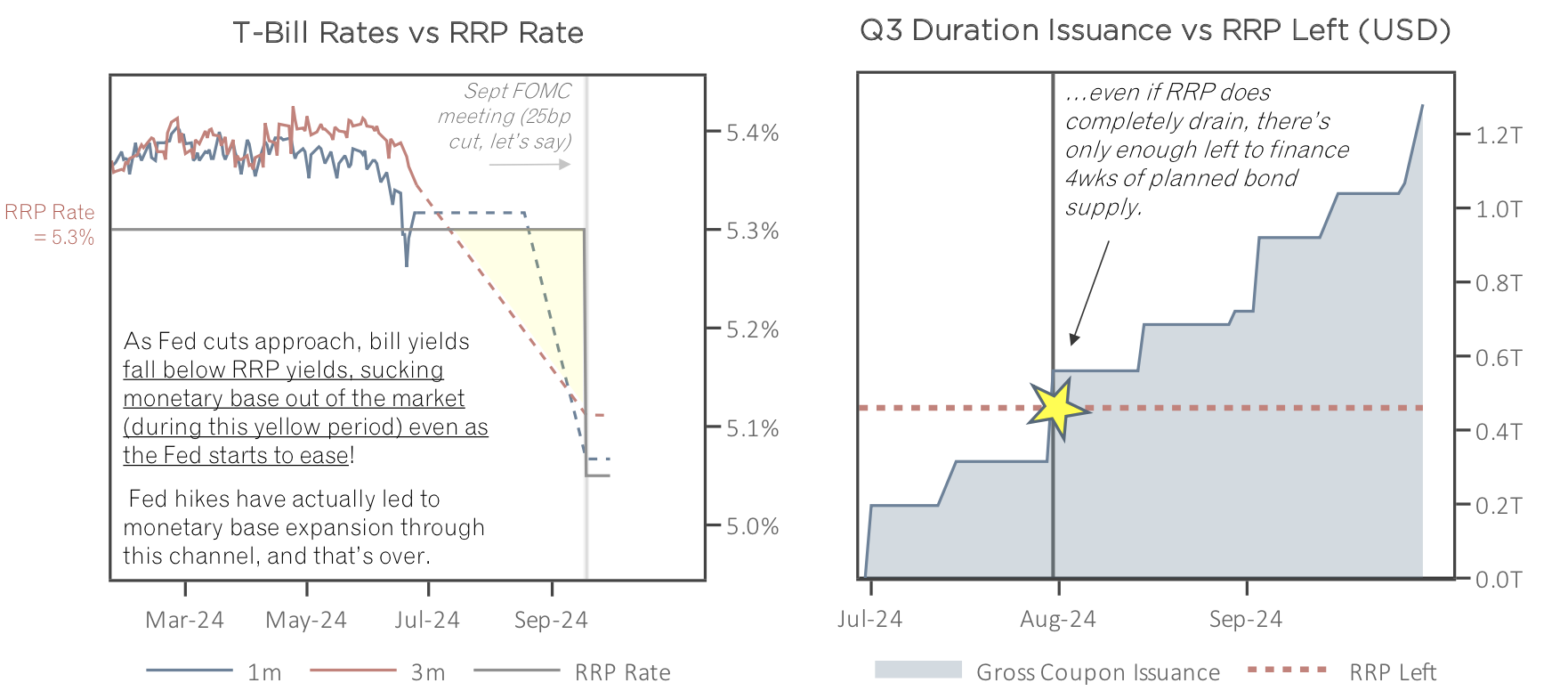

According to Whitney Baker, we are currently in a liminal state of market irrationality and denial. This irrationality peaked recently, spurred on by money printing, which helped big tech to gain "money share" alongside other factors such as wrong-way elections in EMs and Europe, and the US repo squeeze unwinding short-end carry trades. The repo squeeze ended when RRP supplied funds, compressing rates and ending the carry trade unwind. The squeeze was further influenced by Japanese investors ditching US duration as hopes for falling yields were extinguished by recent data. The Asian selling of US duration is upon us and Whitney has been talking about this for years as the ultimate constraint the US will face. Now it’s happening and Whitney discusses the linkages that are coming home to roost, driving systemic financial risk in China, Taiwan, Japan and Korea. The liminal state is ending; reality is now.

Belkin Report

Ultimate euphoria

The Euphoriameter of valuation, sentiment and volatility suggests the US stock market is in a speculative bubble beyond the extremes of the March 2000 TMT bubble peak. Michael Belkin claims the bubble has disguised a deterioration in the US economy, with US retail sales languishing and leading economic indicators remaining negative. Investors need to protect themselves. He recommends LONG Treasury bonds, which are a low-buy investment that could benefit from a risk-off move by asset allocators who sense the approaching recession. This speculative bubble isn’t just confined to the US; European stocks were a consensus must-buy until the French snap election fractured that illusion, and Japan and China were also must-buys that have now rolled over and are being sold.

Willis Welby

UK: Plenty of interest

The Willis Welby team revisits their review of UK growth names they put in place at the start of 2023. They have 104 stocks in their UK coverage with market caps north of USD 2.5bn. Nineteen of them make their screen of consensus Y3 revenue growth in excess of 6%, reasonable financial productivity, and an implied Y3 EBITM ratio of less than 110. The performance of this approach has been okay since May 20, with the mean move of the 18 names at -0.8%, which is ahead of the -2.1% return from the FTSE 350. The team remains of the view that the UK has plenty of interesting and growing businesses. And enough of those names are still available at attractive prices, including the likes of Sage, Convatec and IHG.

Eurointelligence

Frexit through the back door

Would the French parliamentary elections eventually trigger the undoing of the EU? Not immediately of course, but Wolfgang Münchau sees it as a risk that could occur over time. Rassemblement National may no longer advocate Frexit, but their desire to violate the EU’s legal order amounts to the same thing; the party is keen to limit the Schengen free movement area, reduce the country’s contribution to the EU budget and exit the EU power market. All of these mini-Frexits add up to the real thing. France isn’t Hungary, it’s a founding member of the union that relies on the voluntary commitment of member states to respect the rules. Should it decide to opt out, no one in Brussels would be able to stop them and they would end up bringing down the whole house of the EU.

Greenmantle

US: Contentious concentration

The US equity market is top-heavy, expensive and exhibiting high beta returns. The current iteration of the technology rally, the Magnificent 7, is riding the wave of AI hype. Niall Ferguson sees near-term risks in the growing disappointment of cloud or AI product revenues, the size of data centre capital expenditures, or the ability of large AI models to scale with compute. For the moment, none of these risks has materialised. However, given the beta-driven nature of the rally, it is reasonable to expect a harsh market correction when a correction does arrive. The historical example of the Nifty Fifty of the 1970s is relevant, which highlights that a crash is not inconsistent with entrenched firms continuing to have strong revenue growth in the ensuing decades.

CrossBorder Capital

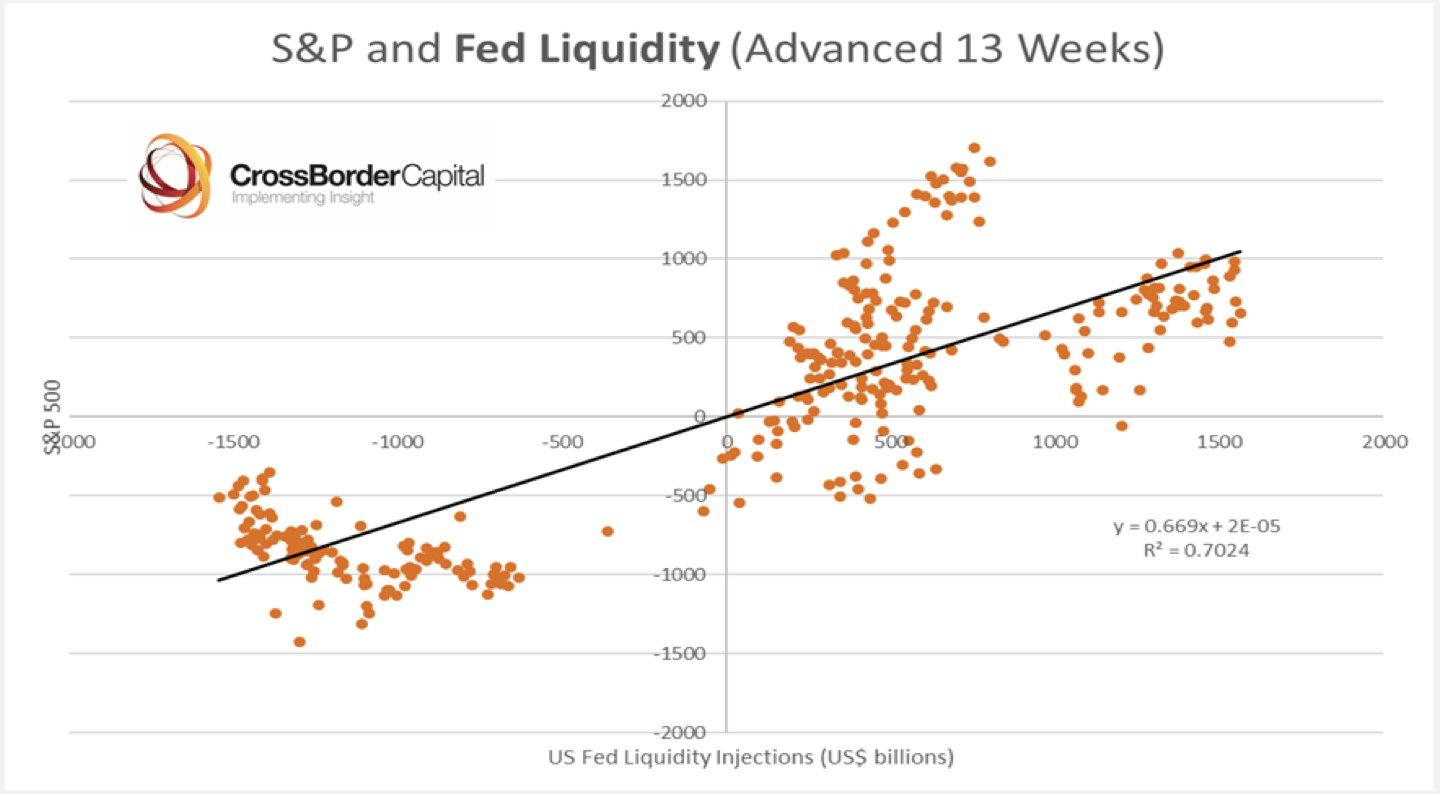

US: Has the Fed lost its power?

More liquidity is coming, but does the US Fed still pack a killer punch? Some argue not. Michael Howell disagrees entirely. There is a hierarchy of World Money and the Fed has become more, not less, important since the 2008/09 GFC. It is also working far more closely with the US Treasury. Arguably, in an era of ‘Fiscal Dominance’, the funding role played by the Fed becomes critically important. There may be limited scope for policy rate cuts, but liquidity provision via changes in balance sheet composition and foreign swap lines are anyway more important both for maintaining financial system stability and driving asset markets. A rough rule of thumb shows that each US$1 trillion of Fed Liquidity boosts the S&P500 by 700 index points.

Yardeni Research

US: Bull tramples even Wall Street’s bulls

The US bull market has stampeded through some of the most optimistic price targets on Wall Street. Whilst Ed Yardeni is sticking with his S&P 500 year-end target of 5400, he is looking forward to the bull run lifting the index to 6000 by the end of 2025 and 6500 by Q4/2026. Q1 earnings beat expectations causing industry analysts to revise upward their consensus estimates for this year and next. Ed lays out his forecast for continued revenues and earnings growth during the Roaring 2020s. The stock market may be in a melt-up, so he revisits the 1990s for some guidance. The S&P 500 Information Technology and Communication Services sectors are as large now as they were during the dot-com bubble, but today they generate a larger percentage of the S&P 500’s earnings.

Emerging Markets

Eurizon SLJ Capital

A rewarding hunt for quality in EM equities

EM equities have not been impressive as of late, generating only a 6% return over the past five years and 13% over the past decade. However, for both EM and China, there are very wide disparities between the top and bottom deciles, with EM countries varying significantly in terms of income, culture, politics and more. EM markets also tend to be more segmented than their European counterparts, increasing the scope for monopolistic conditions. Take a look under the hood and you can find that the top performing stocks in EM and China have in fact outperformed the US; with the top seven performing equity stocks rising by double their S&P equivalents. The potential gains from alpha are substantially greater for EM equities, even if passive index investment strategies may not favour EM.

Horizon Insights

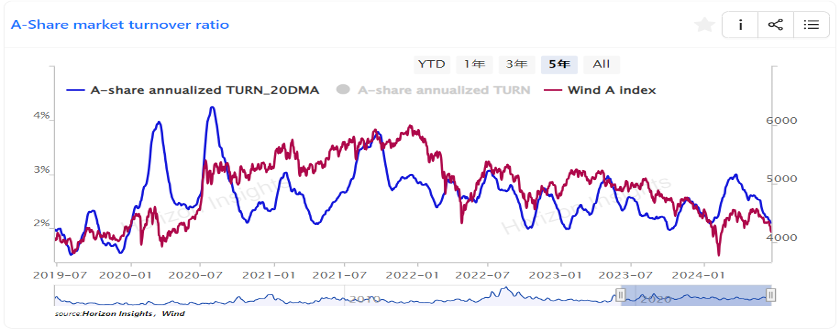

China: Opportunities await, embrace positivity

Although Chinese assets have experienced rapid adjustments in the past 1-2 months, the current stage of market sentiment, the steady improvement in industrial metrics and potential policy support suggest that the outlook for the Chinese stock market should not be overly pessimistic. While the dismal consumer data in May and the lack of improvement following real estate policy changes are significant fundamental concerns, the ongoing increase in policy support and the stabilisation and rebound of the global economic cycle have become key structural variables influencing the market. The pessimistic sentiment surrounding the weakening economy continues in a cyclical manner. As a result, the market turnover rate has reached a significant low. Market sentiment is bottoming out and investors should stay positive.

Talking Heads Macro

Mexico: Watch the fiscal more than social

Incoming President Sheinbaum is drifting towards fiscal discipline after an unambiguous message from markets. The social agenda will absolutely matter, but Manoj Pradhan explains that international investors will not ignore the carry as long as fiscal discipline remains, the path he believes the administration will follow. Given the geopolitical drive against China, US growth and the resurgence of manufacturing, capex can drive Mexico’s agenda and allow Balassa-Samuelson to drive the exchange rate higher without damage to the economy. Back into MXN against JPY or CHF.

Emerging Advisors Group

Colombia: Don't worry, it's fine

Colombia has been caught in the regional FX reversal, but Jonathan Anderson doesn’t see any serious underlying downside risks. As it stands, he’s still very comfortable with the macro adjustment; domestic demand and imports are still holding weaker, the central bank has kept rates high, and both external and fiscal imbalances have narrowed further. The country isn’t as compelling on FX/rates as with regional neighbours. It may have been as profitable as Brazil and Mexico in local currency asset performance over the past year, but its key indicators are less compelling: inflation is still relatively high, real interest rates lower and external debt levels more elevated. This shouldn’t prevent investors from being there, but it does affect Jonathan’s perception of risk/reward at the margin.

Talking Heads Macro

South Africa: Three steps towards structural change

Manoj Pradhan outlined three steps towards structural change in South Africa. Step 1) A coalition to run the economy along with the business-friendly and fiscally conservative DA. Step 2) Following the Treasury’s fiscal guidelines, which are extremely well-run and is a serious signal of intent that will have convinced the DA. Step 3) A resumption and broadening of capex, which Manoj sees as a much bigger story than the election that will encourage corporates to grab market opportunity in a heavily undercapitalised economy. For investors, credit still looks best, followed by the spread between bonds and swaps (for lower risk and macro improvements). Local bonds unhedged are riskier but offer better rewards along with equities.

ESG

Verisk Maplecroft

UK: Starmer’s policy agenda vs fiscal reality

Laurent Balt asks what a Labour victory means for the UK policy environment. He paints a cautious picture of Starmer, in his lawyerly reserve, loathe to do anything untoward on the macroeconomic policy front. Realistically, he cannot avoid trade-offs once in office: the internal pressure for spending will be high and the fiscal situation is poor. Economic growth will be insufficient to plug the fiscal gap in the short term. Ultimately, there is little room to do much without hiking taxes. A possible answer may come in chancellor-in-waiting Rachel Reeves’ plan to ask major institutional investors to pile into the government’s transition strategy. Combined with Starmer’s predictable, ‘softly softly’ approach, markets may be assuaged that a ’quiet revolution’ in Britons’ economic and social wellbeing may be possible without breaking the fiscal headroom.

GFC Economics

Fuelling growth

Fossil fuel consumption continues to rise in absolute terms. Driven by the vast expansion of data centres and the AI boom, global power demand forecasts are being revised higher, in addition to the emergence of “negative feedback loops” where accelerated climate change leads to higher energy demand. Demetris Pachnis and Graham Turner explain that climate change is just one of the many risks facing sovereign bonds in coming years. Some would argue that interest rates need to be slashed to support a faster rollout of renewable energy projects, but the authors suggest that this may not suffice and could result in negative supply shocks as emissions continue to rise and climate change worsens. Dual interest rates for green energy are one potential option. But the bottom line is that technological change is not enough: global growth is far too strong for the world to see enough progress on emissions reductions.

Commodities

Stray Reflections

Crypto: The ultimate Trump trade

In April 2017, Jawad Mian expressed a bullish opinion on Tesla, with the company at the epicentre of Trump’s economic nationalism. This time around, he’s betting on crypto. Trump has made it clear that his administration will support digital currencies, in contrast to the Biden administration’s scepticism. Although crypto assets have performed poorly since the March peak, the legislature appears to be warming up to crypto. New legislation has been passed to provide regulatory clarity for digital asset innovation and the SEC even approved exchange-traded funds for ether. Other positive developments are emerging, including Mastercard’s recent decision to allow users of Binance to make purchases on its network. If Bitcoin is ever going to make a run for $100,000, now is the time.

Veritas Investment Research

Diverging views on oil demand

OPEC recently announced its intention to phase out 2.2 million b/d in voluntary supply cuts this autumn, hoping the market would interpret this as optimism for demand. However, oil prices reacted negatively. Adding fuel to the fire, the IEA released a bombshell report, forecasting a significant oil surplus by the end of the decade. Dan Fong points out that the unfortunate reality is that the two most followed global oil demand forecasts (IEA and OPEC) are both likely biased due to self-interest, which can create volatility when markets take these estimates at face value. Given that oil demand is generally inelastic, Dan prefers to focus on the supply side, in which producer discipline and consolidation, declining US shale quality, and (cautiously) supportive OPEC policy continue to support an oil price range of US$70-90/bbl.

CPM Group

Gold and silver: Spikes and dips

In his latest update, Jeffrey Christian of CPM Group discusses the potential for a brief spike in gold and silver prices due to the upcoming July Comex silver futures roll forward.

Jeffrey also discusses the longer-term outlook for gold and silver prices, and how political and economic factors could drive future market movements.

Click here