Company & Sector Research

Europe

Pernas Research

As the only vertically integrated brick-and-mortar greeting card retailer in the UK, CARD holds a unique position in the market. Pernas Research believes the company is well placed to continue to gain market share in greeting cards and increase its share in the growing market of celebration essentials and gifts. Like most of the companies they look for, with CARD trading at only ~7.5x EV to normalised FCF, the market perception is that the business is getting weaker when it is, in fact, getting stronger. Pernas expects FCF to grow at low teens over the next five years and the cash flow generation over this period will be greater than the current EV of the firm. Sees 50%+ upside.

Insight Investment Research

Robert Crimes considers the likely early termination of Abertis and ACS’ SH-288 Managed Lanes an isolated process and does not expect TDOT to do the same for FER’s Texas Managed Lanes, which except for NTE-35W, do not have preset compensation, with fair market values far higher and valuable revenue shares would be foregone. Robert reduces his valuation for FER’s 53.7% of NTE-35W from €7.4bn to €4.5bn due to higher than expected revenue shares, recently published by TDOT. His new Managed Lane valuation is €20.0bn, double that implied by the share price.

ResearchGreece

Intends to IPO its US business by early 2025 - using an EV/EBITDA of 9x for the US business and applying 5x EBITDA on non-US operations, yields a targeted total EV at €3.7bn and a targeted equity value of €3.1bn or €40 per share (30% upside). ResearchGreece’s implied targeted 2024 EV/EBITDA of 6.5x and P/E of 10.8x are both below Holcim’s current 8.2x EBITDA and 13.8x EPS, which derives 39% of sales and 31% of EBITDA from the US (vs. Titan’s 58% of sales and 55% of EBITDA) and which also plans to list its North American business in the US (the shares are up c.25% since the announcement in Jan).

Arete Research

The guidance reset follows a well-trodden path by peers this earnings season and will come as no surprise to the market. There has been much speculation around this print and IFX (and the broader autos / industrial semis space) has been a shorting haven vs. a rampaging AI long trade. With the much-awaited cut confirmed, profitability remaining resilient (no gross margin reset back into the mid-30’s) and the trough quarter behind us, Arete thinks the path should now be clear to own IFX for a cyclical recovery, as well as structural growth.

Forensic Alpha

Given the underlying weakness in the advertising business, management has been at pains to demonstrate growth from new revenue streams - in particular what they call “recurring revenues” based on selling premium subscriptions and selling to business customers. However, Forensic Alpha highlights a 25% increase in FY23 in Accounts Receivable from business customers with a sharp deterioration in the ageing profile of receivables. If a customer is overdue on their bills by 4 months, they are unlikely to represent a reliable or recurring revenue stream. As a result, they question whether the growth demonstrated by the company is entirely sustainable.

North America

Deception And Truth Analysis

Outperforming the market with measures of deceptive and truthful language in regulatory filings

Using the Deception And Truth Analysis (DATA) algorithm to select the most truthful companies from among the S&P 500 results in large outperformance for investors. This has now been independently validated twice (click here for details). Not only that, but returns are more consistent and they suffer less downside risk than directly investing in the S&P 500. This result comes from the DATA algorithm which has never seen a stock price, but has seen plenty of management behaviours and is able to consistently select outperforming investments by measuring these behaviours.

Off Wall Street

OWS continues to strongly recommend this short idea to clients with their latest report focusing on three issues: 1) The fundamental takeaways from SSTK's 1Q24 results (which show their AI disruption thesis playing out). 2) Management's intensifying use of accounting shenanigans to distort results, perhaps to keep up appearances long enough for insiders to cash out. 3) Envato, a once-hot startup whose growth appears to have stagnated and now gone negative, and whose acquisition, perhaps a sign of desperation on the part of SSTK management, adds meaningful leverage to SSTK's once-clean balance sheet. Lowers TP to $27 (35% downside).

Hedgeye

The share price has shot up on each of the past two quarterly prints, overtly challenging and even completely ignoring, what Brian McGough thinks is a compelling short thesis. However, CVNA's trends have gone in the opposite direction vs. other used car dealers and Brian is seeing some extremely questionable accounting. Specifically, peak profit per unit while pulling back on virtually all discretionary costs. If the company is going to scale to ~3x the unit volumes, when will it actually deploy incremental capital to do so? This "dream the dream" scenario, which is fully priced into the stock, can only happen if it invests to get there. But it's doing the opposite. Brian sees 90% downside.

Periphery Research Partners

Q1 results confirmed much of Hesham Shaaban’s short thesis - CART’s KPIs and monetisation are working against each other to some degree. Promos are revenue offsets, so while promos can help drive GTV / order growth, it will come at the expense of revenues and potentially to the point where the associated take-rate from the transaction is negative. Hesham suspects CART was pandering to the Street with its 2Q24 GTV guide. He can’t see how it gets there without missing current 2Q revenue estimates, which are likely to increase even further post-print following its strong EBITDA guide.

Gordon Haskett Research Advisors

Discount Stores & Warehouse Clubs: Reading the prints

In terms of set-ups and expectations, GHRA remains most bullish on Target and least optimistic on BJ's Wholesale Club at current levels. For TGT, they increase their 1Q24 SSS view to negative 3.5% and EPS to $2.00 with GHRA’s eyes focused squarely on comp cadence along with category trends in General Merchandise. Conversely, they lower their 1Q24 core SSS view on BJ's to negative 1.0%. They think the Street's $0.83 EPS forecast is too optimistic given that gas profitability has deteriorated, which alongside continued Capital One headwinds could weigh on profits. Looking ahead, they expect BJ's to back its FY24 EPS guidance of $3.75-$4.00, but management could indicate that the lower-band is more appropriate given some of the softness YTD.

Fermium Research

WLK posted a nice 1Q upside though 2024 consensus barely moved; likely a function of its inherent conservatism (Fermium stands 8% higher than consensus). Over the last few years, it has deemphasized the commodity side of the portfolio and materially added to its more specialty B&C products, which peers trade at higher multiples. An upcoming investor event focused on this side of the portfolio may serve to establish more credibility on the sustainability of these results. It's modestly contrarian with only 30% of sell-side at BUY, and lastly, management is considered among the industry’s best.

Lynx Equity Strategies

Apple Silicon in the Cloud

KC Rajkumar thinks through the implications of Apple potentially adapting its client-focused Apple Silicon for AI applications in its data centres. He reasons Apple Silicon in the cloud has several interesting advantages over incumbent Nvidia’s GPU solution. KC thinks the company is taking a major step to diversify away from its dependence on unit volume of Apple products and instead leverage its power-efficient Apple Silicon for delivery of lucrative Gen AI services. Servers based on Apple Silicon in the cloud could quarterback the delivery of Gen AI services to Apple’s c.2.2bn client devices. KC expects a gradual run-up in the stock into the WWDC event next month. TP $220.

Veritas Investment Research

Cybersecurity: Potential SEC investigations

Last October the SEC charged SolarWinds and its chief information security officer with fraud. This report looks at other companies in the cybersecurity industry that may have similar risks to an SEC investigation. Based on Veritas' Freedom of Information Act work, they received confirmations from the SEC pertaining to 15 publicly-listed cybersecurity stocks. Out of the 15 issuers confirmed, 2 attracted SEC scrutiny. Stocks mentioned: Palo Alto, CrowdStrike, Fortinet, Zscaler, Cloudflare, Check Point, Okta, Gen Digital, CyberArk, SentinelOne, Qualys, Tenable, Varonis, Rapid7 and SecureWorks.

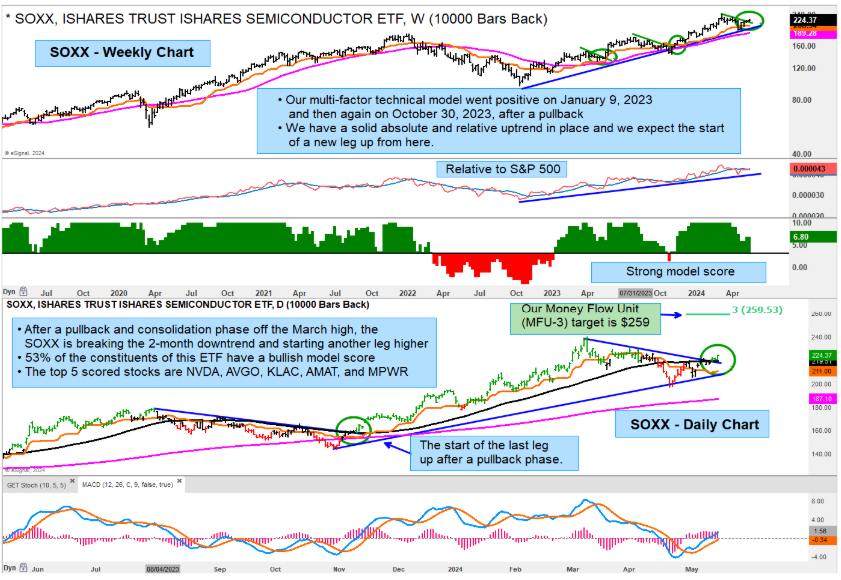

Cerundolo Investment Research

SOXX starting another leg higher

After a 17% pullback from the March high the iShares Semiconductor ETF (SOXX) is emerging from a consolidation phase and about to start another bullish leg higher. Guy Cerundolo scored the constituents of the SOXX and found 53% of the stocks with a bullish multi-factor model score. His top five scoring stocks are: Nvidia, Broadcom, KLA Corp, Applied Materials and Monolithic Power Systems. A full listing and chart review of the constituents is available on request.

MYST Advisors

NRG is the best Cleantech equity in the market and is worth $250/share, according to one of MYST’s clients. Investors are “asleep at the wheel” with the “lazy” data centre derivative thesis. The future of Cleantech is data in the home, which allows NRG to use AI and ML to optimise power consumption / grid load. It has ~8m customers, more data than anyone could dream of and penetration of smart home devices is an easy cross-sell. NRG can shave 1-2% off their power demand at peak, which all falls to the bottom Line. This equates to $1-2bn of “pure margin” that will grow. Meanwhile, the company will generate “insane” FCF to fuel buybacks and incremental growth elsewhere.

280First

AI driven 10Q / 10K filings analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market, ideal for idea generation and portfolio monitoring. Recent alerts include: 1) Johnson Controls - colour on impairment: projections lower than prior forecast. 2) Rambus - customers fail to place orders. 3) Sysco - changing expectation on industry volume growth. 4) Transocean - may seek covenant relief. 5) Wolfspeed - EV products demand moderating? Supply no longer tight?

Japan

Boyar Research

Nintendo has been undergoing a transformation from a lower margin hit-driven cyclical hardware manufacturer to a business that generates most of its revenues from multiple higher margin sources. It is also beginning to aggressively monetise its treasure trove of IP and has a number of hidden assets whose true value is massively understated on its balance sheet. Utilising a SOTP valuation approach, Boyar derives an intrinsic value estimate of USD 20.93/share (50% upside). Ongoing corporate reform in Japan can help unlock shareholder value and they would not be surprised to see Nintendo pursue shareholder-friendly initiatives with its over-capitalised balance sheet.

Asymmetric Advisors

Asymmetric Advisors has been recommending Hitachi for over a decade now and while one could argue that the shares look technically overextended both on chart and PER after the recent rise on the back of its 3/25 forecast being above consensus, they stick with the company as a core Japan holding because 1) earnings are increasingly dictated by IT and DX which should continue to grow and see improving margins over the next few years; 2) grid equipment business has a 2-3 year backlog and rising margins. Meanwhile, analyst consensus has just caught up with the CoE but Asymmetric Advisors sees upside to the earnings.

Emerging Markets

Smart Insider

Zheng Tu (Director since 2019) sells 16m shares at HKD 35.10, reducing his holdings by 50%. This is certainly an abrupt and aggressive % sale from Tu, and his first trade in the shares. Smart Insider ranked the stock -N on May 2nd based on what also appeared to be a very aggressive % sale from Yu He (Director since 2019), who sold all his shares at HKD 32.32. They are now downgrading the stock further, from -N to -1 (lowest ranking).

Propitious Research

The recent slowdown in Chinese retail sales of apparel seems to have been factored into the company’s 1Q24 revenue growth expectations whilst bottom-line growth is supported by margin expansion. With net cash at ~40% of its market cap, the share price should be supported by the ongoing share repurchase programme and its inaugural annual dividend policy. Its 6.6x NTM PE ratio (~4x ex-cash) seems extremely attractive for a highly cash-generative business set to (conservatively) grow earnings at high-single-digits while buying back shares and paying dividends.

AlphaMena

The bank is improving in all of its core businesses - NII (+7% Y/Y in Q1), Islamic financing (+49%) and investment income more than doubled. FAB’s capital ratios are also in a good position with a Tier 1 ratio and ROTE of 15.40% and 17.40%, respectively. In addition, it is benefiting from a healthy asset quality given its cautious loans’ granting policy despite high exposure to the corporate / private sector. The share price has fallen YTD on geopolitical concerns, but AlphaMena believes the stock deserves more attention given its sound fundamentals and its intent to implement a value-added expansion into one of the largest economies like India (FAB is interested in buying SBI’s 25% stake in Yes Bank).

Sandalwood Advisors

Ecopro BM is South Korea's largest producer of cathodes for EV batteries. The company is an important supplier to BMW and Tesla and can be viewed as an early indicator to EV market demand. Recently, Ecopro BM reported a major decline in revenue growth, stating 1Q24 Total Revenue (KRW) at -52% Y/Y and below market expectations. Global investors who closely follow Ecopro and the EV market used Sandalwood’s South Korea data to accurately track this trend.

Radio Free Mobile

Pressure is making life very hard for Chinese semiconductors

While SMIC blamed domestic competition for continued gross margin weakness, Richard Windsor suspects the real issue is to be found at the “leading edge” where it is using a multi-patterning technique to manufacture at 7nm and 5nm. Both Intel and TSMC tried to do multi-patterning for 7nm and abandoned it because the yields were so low that it was not economical to continue. China’s semiconductor industry can make products at much higher cost, but the state will need to support the industry which is becoming increasingly difficult as China’s economy limps along. Furthermore, Chinese technology will no longer be the cheaper option making Western products and standards more competitive in African, South East Asian and Latin American markets.

Macro Research

Developed Markets

CrossBorder Capital

Liquid courage

Global liquidity ticked higher this week yet remains sluggish. Improved collateral values and falling bond market volatility both helped. The missing element remains Central Bank liquidity. Major Central Banks (excluding BoJ) are still holding back. Investors have factored in this lacklustre liquidity backdrop and have been gradually switching to less risky assets in recent months. Michael Howell still expects liquidity growth to pick up through 2H 2024 before peaking in late 2025. Michael’s proprietary risk exposure indexes compare risky assets to safe assets in global portfolios. The latest index value for the World aggregate stands at +16 compared to a YTD average of +23 and a high of +35. The downward adjustment has mostly affected DM, but the UK has emerged as a favourite with a yearly-high of +28.

Aitken Advisors

Let’s talk about UK equities

In 1993, UK pension funds had an 81% allocation to equities, with 33% of this specifically in UK equities. Today, James Aitken remarks, the picture is markedly different, with UK pension funds boasting of a large allocation to global equities but some with only 2% allocated to UK stocks. There’s a tendency to blame the lack of domestic appetite on Brexit; and yet, James points out that there seems to be an announcement every week of a wonderful, yet inexpensive UK listed business due for a foreign takeover. If domestic capital won’t correctly value these great UK businesses, shouldn’t we consider getting involved? If the news flow in the UK goes from awful to even less bad—such as temporary, misplaced euphoria over a new government—then the re-rating of world-class, strategically important UK listed businesses could continue.

High Frequency Economics

UK: BoE’s path to easing isn’t clear

After last week’s MPC meeting, the message from BoE Governor Bailey was that the central bank will likely make monetary policy less restrictive in the months ahead, with the easing being more than market expectations. However, the BoE predicts economic growth will pick up and Carl Weinberg notes that there is little slack in the economy according to HFE’s maths. Why cut rates when the economy is still tight, core prices are rising faster than the target, and GDP growth is accelerating? Furthermore, Carl notes that for equity investors, GDP growth averaging 1% over the next two years leaves little scope for domestic sales growth to boost company profits. For fixed income investors, though, Carl sees scope for gilts to rally in the medium term and for the yield curve to uninvert, if only gradually.

Eurointelligence

Europe’s election dilemma

In the upcoming European election, Wolfgang Münchau argues that the EU is facing a straight choice between focusing on problems of a lack of economic dynamism and global influence, or whether it continues on a path on which form triumphs over substance. Wolfgang says that the metric to look out for is the share of the vote of the centrist coalition that supports the current Commission's agenda. Ahead of the election, the EU's liberals are suffering from weak support, a lack of representation in national governments, and above all, an identity crisis. The Euro group will discuss the French idea of a capital markets union based among a subset of EU member states, based on enhanced cooperation - Wolfgang agrees with the approach, but he doesn't think that the capital market unions thus created will be a success.

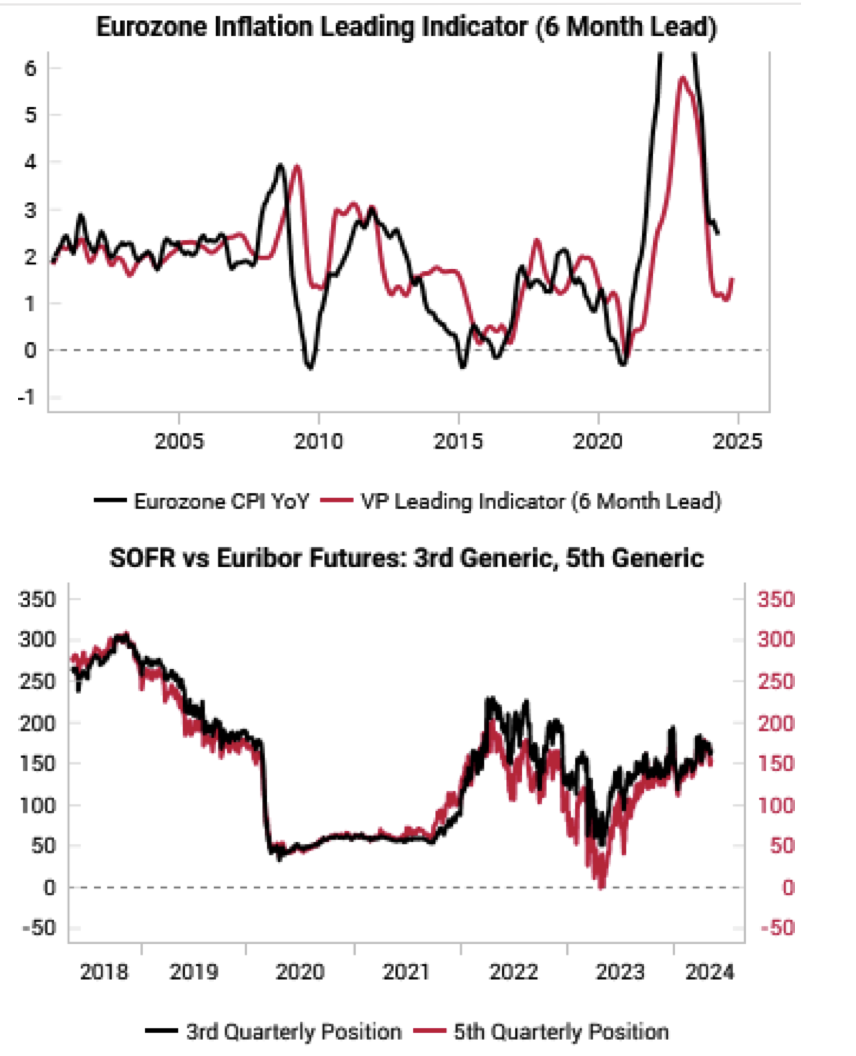

Variant Perception

Eurozone: Inflation LEI bottoms

Variant Perception’s Eurozone inflation leading indicator is bottoming, having correctly foreseen the previous disinflation (chart 1). The spread between Euribor and SOFR futures has widened over the past year (chart 2), pricing in weaker Eurozone growth and disinflation, but this spread is likely peaking. The team also point out that the USD rally looks tactically stretched, with Chair Powell’s comments leaving room for a dovish downside to the dollar. Breadth remains good. Despite the YTD drop in EUR/USD, the EUR cumulative advance decline line vs G10 has actually improved. It’s looking good for a LONG EUR/USD trade.

Talking Heads Macro

An income-led expansion vs labour market crash

The two contradictory themes have shown up repeatedly in recent conversations, but both cannot co-exist. Manoj Pradhan contemplates which one will win out. He doubts a sharp labour market slowdown, since it will require rising layoffs in JOLTS, a worsening of the diffusion of payroll numbers across sectors, and for claims to cross into a 3-handle. With regards to income-led growth, he sees this as a symptom of multiple variables. Rather, the most important thing is the link between the two themes, relating to Manoj’s long-standing heuristic in which richer households have generated jobs for lower-skilled workers. He wonders if a circuit breaker will show up in the form of changing household behaviours or firms laying off workers. Already being received in the rest of the world outside the US vs paid US 5y, a sustained US labour market will help the spread widen.

AAS Economics

No free lunch for the Fed

Frank Shostak suggests that the US Fed does not determine interest rates, but instead only distorts the market interest rates set by individuals’ time preferences. The entire guessing game regarding the Fed’s rate stance is erroneous. What is required is to ascertain the damage that the interest rate policy inflicts on the pool of real savings. When money out of “thin air” is injected into the economy, this creates an exchange of nothing for something. The receivers of the injected money can now divert to themselves consumer goods from the producers. When the central bank attempts to counter the rising interest rate trend by means of injecting money supply, this can make the rising trend steeper because the increase in the money supply creates an exchange of nothing for something, thereby weakening the pool of real savings.

Emerging Markets

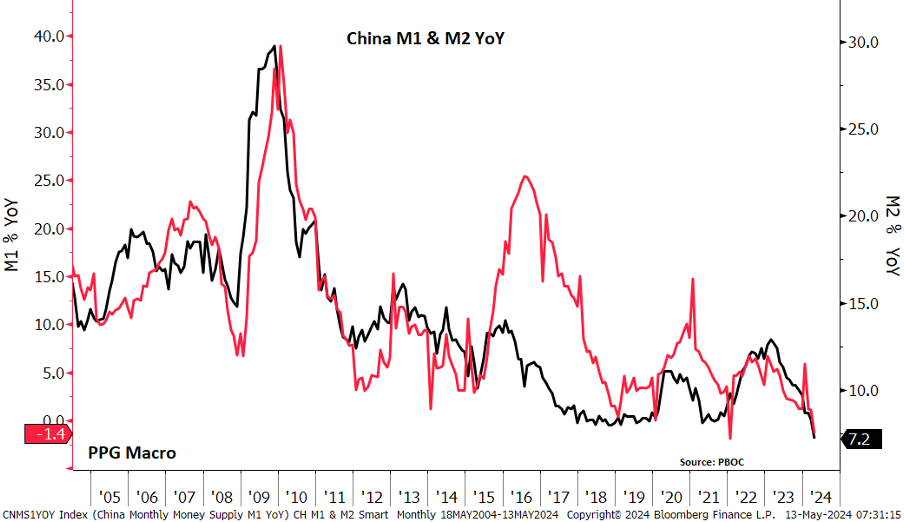

PPG Macro

China: Fighting in the deflationary trenches

In all the time that Patrick Perret-Green has spent looking at China, total social financing year-to-date has never fallen month-on-month…until now. Households remain very cautious, loan growth is at historic lows and contracted over the past three months, and M1 is contracting YoY and M2 growth is down to an historic low of 7.2%. Against this background inflation remains negligible. Headline CPI is just +0.3% YoY, core CPI +0.7% and PPI was lower than consensus at -2.5%. The 17th month in a row in negative territory. With monetary aggregates so weak, the risk is that deflation will become more entrenched and deeper. PPI looks as if it can go lower. The rest of the world will not be able to resist. The scenario is looking like 2014/2015. If PPI heads down towards -5% the pressure for devaluation will become intense.

PRC Macro

China: Credit miss amid the policy void

William Hess thinks the April credit data could indicate that the Q1 fiscal miss is morphing into a Q2 collapse in credit demand. Effective credit demand remains weak and this should give rise to concerns that Beijing will be unable to maintain 5%+ growth with its supply-side led agenda. William’s view is that two related components of the policy agenda are still lacking: 1) there are still expected time lags to the implementation of more effective growth support measures, and; 2) central policymakers have still failed to provide enough policy specifics for key initiatives. Beijing has yet to show us the money, and markets may continue to discount the impact of these programmes heavily, at least in the short-term.

Greenmantle

Argentina: The fight against inflation

President Milei achieved what he needed to in April. Despite the ongoing recession and protests, Milei delivered on his major political promise: disinflation. The passage of the “Bases” bill in the lower house after weeks of patient negotiations shows Milei’s commitment to the actual delivery of structural reforms. This bodes well for the Senate, where Niall Ferguson expects the law to pass in May. He thinks that as long as inflation keeps falling, the recession will be socially tolerated, and Milei’s political authority will not be severely damaged. He is still doubtful whether disinflation can consolidate. The main risk now seems to be of the FX getting too expensive. Yet the direction of travel remains positive: presidential popularity, disinflation, reforms, and fiscal balance. And so, Niall remains constructive.

Alberdi Partners

Colombia and Peru: Credit deterioration

The fiscal stances and institutional qualities have been deteriorating in Colombia and Peru, and Marcos Buscaglia analyses whether this could impact their credit ratings. Running several models, he sees convergence to BB from BB+ for Colombia and expects more downgrades from Moody's. Peru’s S&P rating will remain stable, but Moody’s and Fitch will oversee downgrades, leaving the country on the brink of becoming a fallen angel. On the economic front, Marcos expects Colombia’s GDP growth to outperform consensus at 2% and expects BanRep to deliver another 50bp cut in June. Peru will see similar growth rates, and Marcos forecasts that the BCRP will continue with the easing cycle, with more 25bp reductions and a terminal rate of 4.5%.

Emerging Advisors Group

Food and oil are saving Brazil

Brazil is a failing industrial exporter, with manufacturing exports having declined over the past decade, dramatically underperforming the EM average. Yet, it remains an absolute commodity export tiger, with primary shipments having rocketed upwards, making it one of the few major economies that Jonathan Anderson follows with growing resource export capacity. Oil and foodstuffs are the stars on the scene driving growth. It’s not enough to render Brazil an outright surplus economy, but it’s good enough to keep it out of deficit troubles and thus keep Jonathan invested in BRL carry and local debt.

Krutham (formerly known as Intellidex)

South Africa: The countdown to election

This is a seminal election where the maths of coalitions is going to be exceptionally tight, and Peter Montalto sees no easy routes to magically higher growth or coalition stability. The most likely coalition is an ANC-IFP-smaller party, though this is only moderately probable. The ANC may offer the IFP the KZN Premiership to secure their support. An ANC-DA or ANC-DA-IFP coalition could also be possible, particularly beneficial in provinces like Gauteng. Peter predicts the ANC will fall to 44.8% from 57.5% in 2019, the largest ever fall, driven by a loss in support and the shock of the new MKP party results. Smaller new parties will have mixed results, with MKP performing best. Peter expects a broadly free and fair election but warns about potential instability in KZN if an IFP-DA coalition takes the province.

Commodities

CPM Group

De-dollarisation is a myth

In this presentation, Jeffrey Christian of CPM discusses the misconception that the US dollar is being abandoned in global markets, emphasising its continued strength and dominance as a foreign exchange reserve. He also discusses the myth of "de-dollarisation", highlighting the fact that the value of the dollar has increased significantly since 2011. Jeffrey also points out the stability in the dollar's share of global central bank reserves, which remains between 58%-62%, and how these reserves have continued to grow over time. The presentation concludes with a discussion about what this means for gold, who is buying it, and why.

Click here to watch.

10x Research

Bitcoin: Serious money can be made this year

One big rally is still left this year, but to take advantage of it, investors must time it perfectly; buy-and-hold no longer works in this market. 10x Research’s models should provide a timely heads-up, as they did at the end of September 2023 when the models flagged Bitcoin breaking out while the summer lull still hypnotised everyone else. Expectations of a pro-crypto President will drive a new narrative, and Bitcoin tends to rally +192% on average during election years. The team sees a slide in price towards $52,000/$55,000 by July/August, before the prospect of a Republican win pushes it back to $70,000, hitting a price cap as Mt. Gox distributes 142,000 BTC.

Global Mining Research

Gold: Can higher prices translate into cash?

All too often in the last decade for the gold sector, fully loaded costs have come close to equalling the received price. Therefore, one reason gold equities have likely recently lagged spot prices reflects a degree of market scepticism of the sector's ability to translate higher prices into “cash”. Unfortunately, the senior producers have often been key protagonists, but this isn’t the case for all gold stocks. Herein, David Radclyffe updates the sector cost analysis including highlighting Free Cash Flow (FCF) costs and FCF costs plus dividends, seeking to identify those stocks that could bank the proceeds of higher spot prices in 2024. The notional spot margin after base case dividends in 2024E for Agnico Eagle Mines / Barrick Gold Corp / Newmont is ~US$395/GEO, up from US$200/GEO in 2023. However, the best cash notional margins in 2024E could be delivered by Evolution Mining, Lundin Gold, Centerra Gold, and Barrick Gold Corp.