Company & Sector Research

Europe

New Street Research

Telcos: Q4 first time ever all EU markets are in positive growth

Service revenue growth remains at record highs (+2.2% Y/Y in Q4, the highest growth rate the sector has achieved over the last 10+ years) and for the first time all markets have positive growth (between +1-5% Y/Y). EBITDA growth also improved, while capex appears to have peaked. OpFCF was +17.5% Y/Y in Q4 and +5.2% for the full year. This was the second quarter in a row of ROCE growth (it is now back above 8% for the first time in 2 years). New Street strongly believes the good service revenue growth will filter through to permanently better FCF and higher ROCE thanks to the improving regulatory environment. Their current top picks are BT, DT, Orange, Telenor, Telia and Vodafone.

the IDEA!

Quality comes at a price - while the size and valuation of the recently proposed Staci acquisition has some analysts and investors concerned, it marks a first credible step aimed at accelerating the transformation of BPOST into a company with a bigger exposure to growth activities and higher margins. Analysts at the IDEA! think the process BPOST is going through shows some parallels with that of the three largest Dutch publishers in the late 1980s and 1990s. In view of the current valuation of the shares (just over 2x EV/adj. EBITDA) they feel that this is beginning to turn into an increasingly compelling investment case.

Radio Free Mobile

ASML really does not want to talk about China. Richard Windsor's biggest concern following the company's disappointing Q1 results is the fact that China made up a colossal 49% of revenues. China is currently buying everything it can get its hands on in anticipation of further restrictions from the US, Japan and Netherlands. This means that demand for equipment is being pulled forward and is setting the equipment industry up for a correction once Chinese buying slows dramatically. The net result is that at 45x 2024 PER and the risk of a miss in 2025, ASML’s shares look far too expensive.

Woozle Research

The majority of DSY resellers / channel partners have reported missing their internal sales targets this quarter, according to Woozle’s latest channel checks. DSY’s core SOLIDWORKS solution had a largely mixed performance with some respondents reporting that they missed sales targets by 20-30% while others reported very minor Y/Y growth. Aggressive promotions were also prevalent. Despite most respondents reporting underperformance throughout 1Q24, this was driven by lingering uncertainty in the market resulting in lengthened deal cycles rather than competitive dynamics, with many hoping that easing macroeconomic conditions should stimulate sales growth.

ResearchGreece

My Big Fat Greek Deal - ResearchGreece downgrades their rating to DO NOT OWN IT (DOI) on the back of the €2bn/2GW solar agreement with Mytilineos. Why? Because the implied cost does not make sense; it is much higher than PPC’s own installations or projects under development; it is higher than any of the recent solar projects they have seen; PPC does not need it and it does not maximise shareholder value. While ResearchGreece’s valuation yields a fair value >€15 per share (+40% upside), their conviction is lower than before the deal. Investors that do not mind uneconomic corporate decisions may find such an upside attractive.

North America

Huber Research Partners

Q1 organic revenue growth beats expectations and management raises the bottom end its 2024 guidance range to +4.0-5.0%, reflecting confidence in the current business performance and outlook. This is on top of 4.1% organic growth in 2023, despite geopolitical and macro uncertainty. Investors who argue that the industry is facing perpetual declining organic revenue growth continue to be proven wrong. This GARP stock looks highly undervalued trading at only 11.6x/10.8x 2024/25E GAAP EPS (43% discount to S&P 500 vs. more modest 25% average discount the prior 10 years using Street consensus estimates), 8.6x/8.2x EBITDA and 10.7x/9.9x FCF.

Gordon Haskett Research Advisors

Home Improvement survey reveals disappointing results

GHRA sees a notable drop in both households planning to undertake a home improvement project and the size / scope of that remodel. 1Q24 survey specifics include: 1) Home improvement plans in the next twelve months moderated ~300 bps sequentially to 53.7% but dropped meaningfully Y/Y from 62.3% in 1Q23. 2) 57.3% of respondents have delayed buying a home (up from 56.0% in 4Q23 and above the long-term average of 51.1%), with 56.7% of them instead planning to reinvest / upgrade their current home (down from 64.3% in 4Q23). 3) The amount consumers are budgeting for home improvement projects moderated sequentially to a 15-quarter low of $5,851, or -24% Y/Y. 4) Home Depot maintained its market share leadership, but the gap to Lowe's narrowed to the slimmest margin yet in GHRA’s survey.

Verbatim Advisory Group

Mar-Apr sales trends are weaker than the Feb-Mar trends, according to Verbatim’s latest channel checks. Overall 3Q24 QTD trends are also weaker than 2Q24 trends. Both DIFM and DIY trends have weakened significantly. Unfavourable weather, rising prices, a weak economy and increased competition are the primary factors contributing to a decline in both Traffic and Ticket levels. Survey feedback also highlights challenges faced by ACDelco brand products due to ongoing labour disputes. Based on weaker trends and an easy multi-year comparison, Verbatim applies a bias factor of negative 250 bps in the current period. With a Mar-Apr Raw Comp of +1.5%, their Mar-Apr Comp Estimate is -1.0%. Their 3Q24 QTD Comp estimate is +0.8%.

R5 Capital

While there has been a lot of optimism around improvements at DG, R5’s latest spot-check of stores does not support this sentiment. Indeed, it was the opposite. They came across similar operating difficulties to those seen over the last few years. There remains a severe inventory overstock problem. Unmanned checkouts and stores only having one employee on a Saturday were also witnessed. Store standards varied, from dirty and messy, to a few being well organised and clean. Scott Mushkin also sees some structural / competitive issues at play that may hamper DG’s longer term growth algorithm even if / when operations improve.

Hedgeye

It is déjà vu all over again - questioning the secular growth of French fries is back. Following LW's recent earnings miss, the stock is trading at its lowest valuation since being spun off from Conagra. However, Hedgeye’s analysis points to an asymmetric risk/reward from current levels. Out year EPS power is between $7-8, meaning the stock can double from here over the next 1-2 years. They believe the current price underestimates the industry’s pricing discipline, underestimates the returns from capacity expansions and overestimates the pricing impact from capacity growth.

BWS Financial

An overhang for drill ship owners has been the energy producers slowing contract activity on the expectation there would be more supply, especially from recommissioning stacked drill ships. However, Hamed Khorsand does not believe this will be the case since many of these assets have been stacked for several years and owners have used them as a source for parts. Supply constraints should persist for the foreseeable future and push day rates above the $500,000 threshold on a consistent basis this year. SDRL would further benefit from such a scenario with 40% of its fleet due for contract renewals next year. Hamed increases his TP to $80 (60% upside).

Foveal Research

Dr Amit Roy provides in depth analysis of all CYTK’s aficamten (oHCM) trials compared to Bristol-Myers Squibb’s Camzyos incumbent. While at first sight, the aficamten data may appear slightly ahead of Camzyos on efficacy and safety, with no cases of low heart strength (LVEF) and so fewer dose interruptions, Amit reveals key differences in patients recruited and how efficacy and safety were assessed, which may portray aficamten headlines in a favourable light. While he sees aficamten approvable, it may not outshine Camzyos when it reaches the market. Amit also assesses the likelihood of the non-obstructive extension market that may be potentially larger, reading out in 2025.

Veritas Investment Research

With its profitability restored, deleveraging substantially complete, no significant growth plans on the horizon and a low likelihood of large-scale M&A activity, AC's choices for capital allocation are increasingly leaning towards shareholder returns. Given its strong performance as of late, Veritas has been fielding questions about the dividend potential for the company. In this note, they attempt to size the airliner's capacity to fund shareholder returns across a range of scenarios. Over the near term, a robust demand environment should enable the company to generate excess cash to support shareholder distributions. However, on a three-year outlook, $4bn worth of scheduled debt maturities and $8bn of new aircraft deliveries will pose headwinds to building cash in the years ahead.

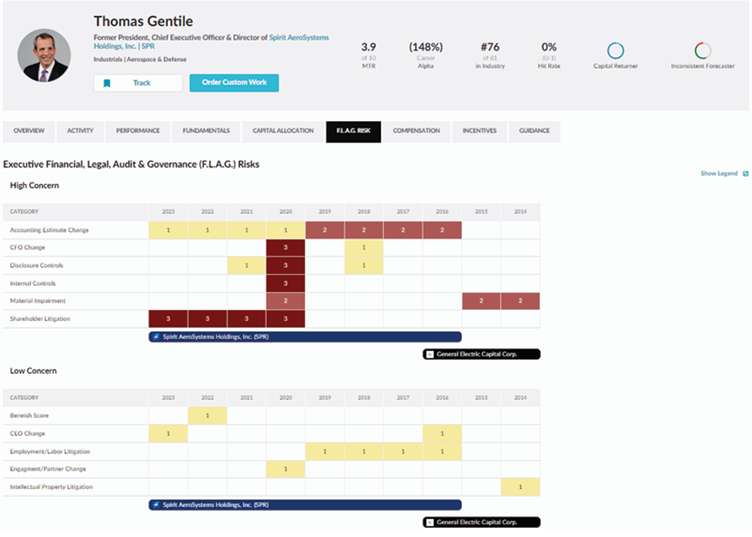

Paragon Intel

Incoming CEO Thomas Gentile appears to be a downgrade to the already under-performing CEO seat at HXL with (147%) career alpha destruction compared to Nick Stanage's (77%). While Gentile brings less "Level 2 & 3" F.L.A.G. Risks than Stanage; his 14 is still considered to be high across all the executives on Paragon’s ManagementTrack platform. Investors should not expect more consistency in trusting guidance from Gentile - he was classified as an “Inconsistent Forecaster” during his tenure as CEO at Spirit AeroSystems. Furthermore, he does not possess a track record as a C-Suite executive of increasing revenue or margins - at SPR revenue declined (26%) and Adj. EBITDA margins declined by (1,470 bps). He left the firm after production problems resulted in the shares declining more than (40%).

MYST Advisors

PCT has developed a patented recycling process which separates colour, odour and contaminants from plastic waste feedstock to transform it into ultra-pure recycled polypropylene (PP) - a massive market with no real direct competition. Industry PP production is forecast to scale to 180-200bn lbs per year. Ironton (PCT’s Ohio plant) is close to achieving long-awaited “critical mass” and lays the groundwork for many larger-scale plant builds over the next 5 years (Ironton is expected to reach 120m lbs per year with each additional plant adding 1bn of new production). Fantastic long-term economics offering ~30% ROIC. PCT can generate $0.60 per Pound of EBITDA. TP (YE24) $17.5 (>200% upside).

ETR

Enterprise IT spend optimism wanes

Based on ETR's data collected from 1,844 IT decision makers, IT spend estimates for 2Q24 are tempered vs. 1Q24, now sitting at +2.5% Y/Y growth. After starting the year more optimistic than the year-end data, respondents’ updated estimates for FY24 spend are less optimistic at an average of +3.4% growth Y/Y vs. 4.3% growth forecasted earlier in the year. Revisions to IT spend expectations are more prevalent in SMEs compared to large organisations. Part of the lower spend estimates can be attributed to a slower roll-out of generative AI projects as more organisations are citing compliance, legal and data privacy as barriers to implement GenAI projects. In addition, slightly more respondents are pulling spend from other areas to support GenAI projects vs. net new budgets being allocated.

Lynx Equity Strategies

Thoughts on Semis going into the earnings season

Semis enter this earnings season precipitously close to an edge. After a hefty run-up, many of the recent winners are perched at or near their 50-day MA - they have not had a pull-back in months. Earnings will need to be clean beat / raise events for stocks to climb higher. KC Rajkumar would let the SOX index, leveraged by rates fears, pull back during earnings prints. However, the underlying strength in the US economy indicates to him that the SOX may have further upside, even as the semis breadth broadens out to include Industrial semis.

Japan

Galliano's Financials Research

The current share price discount to the stated NAV of 53% may seem optically attractive, but Victor Galliano believes this figure will be subject to valuation headwinds going forward. Arm (45% of SoftBank Group’s equity value) is starting to experience limits to its “growth at any price” stock status. It trades at super-premium valuations which are unsustainable, not least as Nvidia trades on less than half the prospective earnings multiple for just slightly lower forward consensus EPS growth. Furthermore, while the JPY’s depreciation is supportive of the group NAV, with the Fed’s hawkish stance well known and BoJ expected to raise interest rates, JPY weakness may be largely done.

JapaneseIPO.com

The bank could see its stock value increase by c.50% over the coming year, according to Yuka Marosek. Key points to her investment thesis: 1) Japanese banks are beneficiaries of interest rate normalisation and investor sentiment recovery. 2) Regional banks are direct beneficiaries of the rebound of the Japanese economy. 3) NIM improvement potential. 4) Solid balance sheet to support growth. 5) Diversified growth plan. 6) Attractive valuation - the bank continues to trade at a modest P/B of 0.44x even after a c.100% increase in its share price over the last 12 months.

Emerging Markets

RedTech Advisors

China: eCommerce forecasts for 2024-2028

Highlights from RedTech’s 22-page report include: 1) Online sales growth will range from ~7-10% from 2024 through 2028, based on ~4-7% overall retail sales growth. 2) High penetration implies slower growth for apparel, while lower penetration suggests more opportunity in electronics / appliances and in groceries. 3) These product dynamics do not favour Alibaba, particularly with more competition. 4) Expects the fastest growth from PDD and even more so Douyin. 5) JD should see gains, but it has been overtaken by newcomers outside of its core electronics and appliances. 6) Alibaba has the most to lose and it will continue losing share.

AlphaMena

This Tunisian brewer announced upbeat 2023 results (net profit +9.5% to TND 281.681m on slightly higher revenue of TND 826.865m), managing to overcome the difficulties of its operational environment (high inflation and sluggish demand). At the current price, the stock trades at 7.08x EV/EBITDA 2024E (vs. 11.6x for its MENA peers) and offers a 5.6% dividend yield. Amidst a declining volume context, SFBT’s ROCE would hover around 25% over the 2024-25 period, thanks to its strong pricing power on a near-monopoly in Tunisia. There is no doubt this is a quality stock and although the share price has rallied +23% in the last three months, it still offers ~50% upside to AlphaMena's target price.

ChartAnalytics

This energy stock is poised for a fresh thrust on the upside - after finding support around the 50-day MA at Rs. 188 in Nov last year, ONGC's stock gradually rose but stalled around Rs. 280 in Feb, undergoing a corrective decline. The decline found support at the 50-day MA, leading to nearly a month of consolidation and forming a symmetrical triangle, a neutral pattern indicating potential continuation. A breakout from this pattern recently occurred with an exceptional volume increase, indicating bullish sentiment. The stock is expected to gain momentum towards Rs. 320. Any price below Rs. 267 suggests exiting the stock.

Macro Research

Developed Markets

Antipodean Capital Management

Inflation surprises

Recent data from the EU, UK and NZ show MoM inflation rising, possibly delaying anticipated rate cuts. It has panned out exactly as Craig Ferguson discussed months ago. The persistence of inflation will suppress economic activity in coming months, possibly hitting equity markets if ongoing corrections come true. The bond market is seeing a strategic shift towards longer durations in anticipation of heightened volatility. Craig adds 10yr macro bond LONGs across the curve and is adding USD Index, USD/JPY SHORTs; and AUD & NZD LONGs (against a strengthening USD) to his portfolio. His growth vs defensive is at 32/68%, with defensives including gold, alts, and extended bond duration.

Aitken Advisors

Should we listen to the central banks?

Investors are growing tired of central bank speak, which James Aitken claims to be performative exactitude peddled as transparency. If you’re in doubt about what’s happening in the world, listen instead to what your best-run portfolio companies are telling you and cross-reference with what you are actually observing. The recent price action – bonds falling more than stocks – could be interpreted as suggesting that despite rising long-end yields, markets are comfortable with strong, perhaps stronger growth to come. That will ensure the best-run companies protect moats & continue to grow earnings in a satisfactory way. Assuming nominal GDP continues to rumble along around 5-6%, bond yields should be higher, with 10yr treasuries soon yielding 5% or more, which will act as headwinds to some stocks that have seen the biggest rallies, such as Super Micro Computer Inc and Nvidia, with marginally profitable, levered businesses struggling. You cannot, however, be out of stocks let alone net bearish: you just need to own different things.

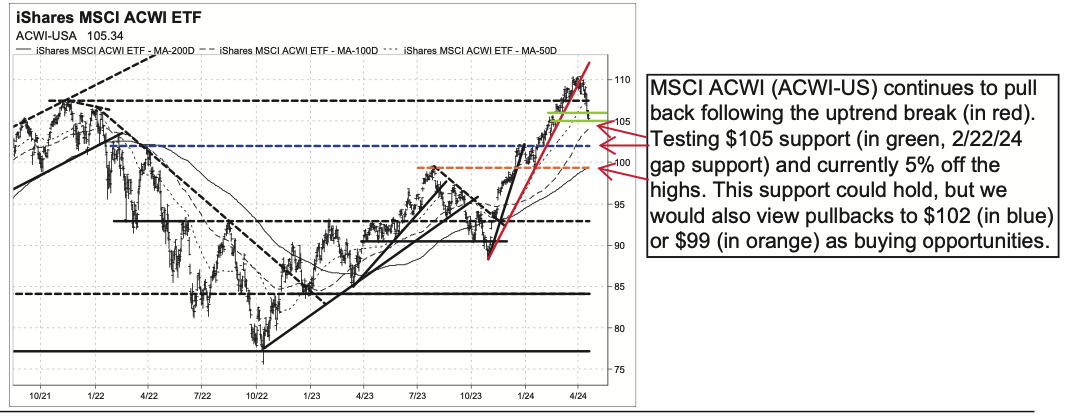

Vermilion Research

Global retreat

A pullback in global equities is underway following steep uptrend violations on the MSCI ACWI further downside may be limited. Several 5-10% pullbacks are to be expected in any given year – particularly after the historic 5-month rallies – so the Vermillion team view this as healthy and normal within the ongoing bull market. ACWI-US is currently testing important support at $105; if this area were to break, next major supports are $102 and $99. A pullback to $102 would be 7-8% off the highs, while a test of $99 would be 10% off the highs. As long as $99 holds on ACWI-US, the team continue to treat pushbacks as buying opportunities.

High Frequency Economics

Resilient global economy? Ha!

Carl Weinberg mentions how IMF WEO staff have failed to predict every economic recession in the past two decades. With their recent assessment of a “resilient” world economy with respect to supply side shocks, monetary distortions and geopolitical risks, Carl can’t help but laugh. Their own data clearly shows declining world exports, commodity prices and more. While the US economy is currently doing well, China’s year is off to a rocky start, the Euroland economy is flat at best, Japan’s declining population is weighing on its economy, and Britain has its own problems. The facts are simple, world GDP is on its way to shrinking this year.

Blonde Money

UK: A summer general election

Helen Thomas points out that the Conservative Party now faces an extinction-level event and that the least-worst option is a summertime election. Opinion polls suggest an electorate ready to euthanise the Conservative brand. The fight back must begin by revving up the party’s long-suffering activists and their disenchanted donors. With the local elections on 2nd May anticipated to be a bloodbath, the rebels are planning to force a no confidence vote in their aftermath. Helen believes there is only one course of action. Before Rishi is removed, he must choose to step aside and anoint a team to lead the party into an immediate election. He can endorse the Leader of the House, Penny Mordaunt, to take the reins. The general election would need to take place immediately. Helen sees the probable election date landing somewhere between 13th June, and 4th July.

Greenmantle

Germany’s peace chancellor

Fearful of entering next year’s re-election campaign with a bleak economic track record, Chancellor Olaf Scholz is looking to boost his popularity. Niall Ferguson expects Scholz’s government to revise implementation of Germany’s debt brake to free up an extra €8 billion (0.3% of GDP) to spend in 2025. Niall also expects Berlin to top up its €100 billion defense fund by 2026 at the latest. In foreign affairs, Scholz is increasingly portraying himself as a ‘peace chancellor,’ whose priority is keeping Germans safe and avoiding escalation in Ukraine, not helping Kyiv win. This is a long-standing strategy of Social Democratic chancellors—but it is made more necessary by the rise of not only the far-right pro-Russian Alternative for Germany (AfD), but also the charismatic left-wing, pro-Russian, and anti-migration populist Sahra Wagenknecht.

Eurointelligence

Europe: Productivity, productivity, productivity

Mario Draghi is urging Europeans to move from a narrow perspective on competitiveness towards a broad concept of productivity. Wolfgang Münchau agrees, but he notes that this is not realistically possible in the EU without a fully-fledged fiscal and capital markets union - it is the resource allocation that is the main problem. Europe must invest in 21st century technologies and create a genuine capital markets union - a real one, not the half-hearted attempts currently underway. There can be no efficient capital markets union without a single European debt security. Fiscal fragmentation is the source of the fragmented resource allocation. Since you aren’t going to get 27 countries to agree on this, you have to start in a smaller group, and maybe not even one that includes Germany to start with.

Steno Research

Is the Fed hiking next?

Steno's proprietary global inflation impulse index has surged back, registering an aggregate Z-score of almost 5. This indicates a substantial positive inflation impulse from each of the five key subcomponents, often resulting in US inflation levels averaging around 4-4.5% after a while. Worryingly, the spread between CPI and PCE prices is rising very fast, typically a strong directional indicator as the CPI is more prone to trend volatility. The financial conditions remain benign and the bottom line is that conditions remain too easy to tame inflation. Powell and the Fed will have to moderately hawk up the stance to try and alter that picture. The Steno Research base case is that they remain on a “soft hold” all the way until the election, but they may move back to an explicitly symmetrical policy stance as early as June or September.

CrossBorder Capital

Watch the dollar

Michael Howell's Global Liquidity Index inched lower in March 2024 to a reading of 27.5, ('normal' range 0-100). This is the weakest index since last November and continues the recent sideways pattern. It's not a surprise, as it aligns with his recent warnings of a coming dip in Global Liquidity. The significant decrease can largely be attributed to Asian economies, notably China, the dominant regional player. With geopolitical tensions and rising gold bullion prices, Howell's main focus this month shifts towards the US dollar. Like in the mid-1980s, the USD's relative strength is defying consensus. Michael predicts US economic acceleration, higher policy rates, and term premia being pushed into positive territory, which will force the 10-year benchmark bond to test yields of 5-5.5%. He continues to favour equities and recommends buying into any setbacks.

Emerging Markets

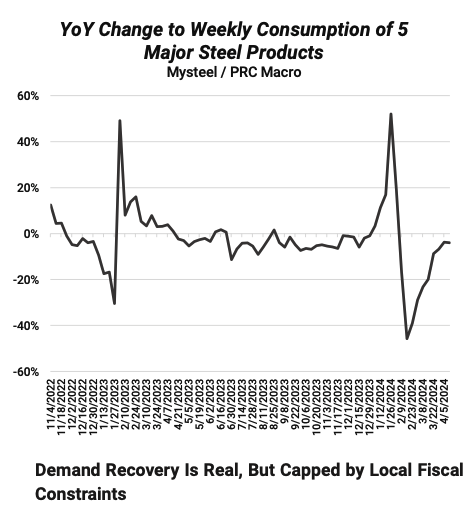

PRC Macro

China: Steel production, not demand, to drive iron ore in Q2

William Hess anticipates the ongoing steel demand recovery in China to peak in May and remain elevated through 2Q/2024. However, the continued slow issuance of local government bonds presents headwinds for this recovery. Consequently, William has revised his 2024 steel demand growth forecast from 1.1% to 0.9%. Contrary to market consensus, he believes that weaker steel demand in China has already been fully accounted for by market participants and is no longer a significant obstacle. A potential game changer for iron ore could be the risk of production cuts. Underreported steel production in Q1 this year might provide the National Development and Reform Commission (NDRC) and steel mills with fewer reasons to reduce production in the second half of the year, which would support better-than-anticipated iron ore demand.

Global Forecaster

Iran’s war on Israel

Based on David Murrin’s extensive human behavioural models, he argues that both the Battle for Ukraine and the Middle East Regional War are being driven by a 112-year entropic cycle, as part of the unfolding hegemonic war of autocracy against democracy. A global war that will only intensify into a 2030 peak. Following the Hamas attack on Israel in 2023, David Murrin warned that it would inevitably escalate into a full-blown Middle East conflict. He points out that this prediction came to pass on 13th April with Iran’s attack on Israel. In his latest Murrination, David assesses what happens next.

Greenmantle

Mexico’s electoral countdown

With the two major presidential candidates now clear, Mexico’s election season has finally begun in earnest. Yet the outgoing president, Andrés Manuel López Obrador (AMLO), is reluctant to relinquish the spotlight. He is leaving his successor a toxic brew of rising debt, uncontained drug violence, a more powerful military and large unfinished infrastructure projects. Niall Ferguson expects whoever wins the election to attempt to avoid the capricious policymaking of the AMLO administration and swiftly address the country’s fiscal imbalance. Mexico’s potential as a site for US nearshoring remains, even as trade tensions between China and the United States are increasing the adoption of protectionist measures. He maintains his view that Claudia Sheinbaum will win the election and gradually distance herself from AMLO’s erratic policies afterwards.

Emerging Advisors Group

Morocco remains a tiger

Moroccan exports continue to boom, driven by rapid growth in vehicles, aircraft parts, consumer electronics and processed fertilizers, making the country a regional "tiger". There isn’t much happening at home. As before the domestic economy is much sleepier, with flattish credit, construction and demand trends. Nevertheless, Jonathan Anderson remains invested in the Moroccan equity market, in line with his long-standing policy of buying exposure to structural export "winners".

Krutham (formerly known as Intellidex)

South Africa: All quiet on the southern front

Q2, on a macro level at least, will be quiet, with most issues not settled until after the elections. A slew of soft Q1 data will be released with inflation risks rising slightly. The National Council of Provinces will be busy finalising legislation before the elections while the pace of reform in the NLCC (logistics) and Necom (electricity) has barely slowed in this peak campaign. Overall, however, everything is subsumed by the election—the campaign, the expected last-minute ANC rally pushing up its vote, the tight timetable and then the dramas of a coalition government. Peter Montalto thinks markets are overplaying risk and uncertainty; the risk is more limited given the high conviction view he has on ANC coalition partner preferences.

Emerging Advisors Group

Sri Lanka: Oh, come on

Sri Lankan debt has rallied sharply. Jonathan Anderson was comfortable with spreads before the new year, but not they’ve tightened another 500bp in the big Q1 high-stress rally. Are things done? There’s some good news: the near-term funding gaps are mostly closed and the government is holding the line on macro discipline. There’s also bad news: equilibrium can only be maintained via painful domestic depression and a complete debt service moratorium. There's no change in the underlying structural imbalances that brought Sri Lanka to this point. As a result, Jonathan believes debt markets are overpriced, with plenty of potential downside exposure to budget and external slippages in 2024-25, and he continues to be cautious on equity and local rates exposure too.

Commodities

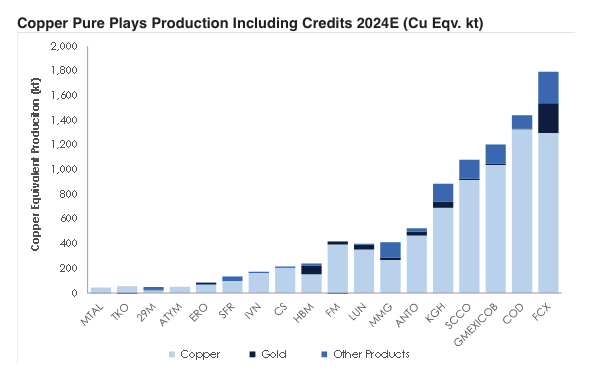

Global Mining Research

Copper sector: Gold credits to shine

Commodity prices are overall moving in the right direction for the copper sector, with spot LME copper now at ~US$4.25/lb. However, many copper miners enjoy important by-product credits, including molybdenum, lead, zinc, silver and gold. Interestingly, precious metal credits have outperformed other by-products with gold at >US$2,350/oz. The sector is expected to generate ~82% of revenues from copper in 2024E with gold the next highest at ~6%. In 2024E, GMR’s copper universe is expected to produce ~2.2Moz of attributable gold production (~0.5Mt Cu Eqv.). However, analysis shows credits do not always correspond to the best position on the cost curve. Many copper miners don’t receive the full impact of higher precious metals credits due to streaming/royalty funding deals. The best way to play this “free kick” is through Hudbay Minerals, KGHM, and Freeport-McMoRan.

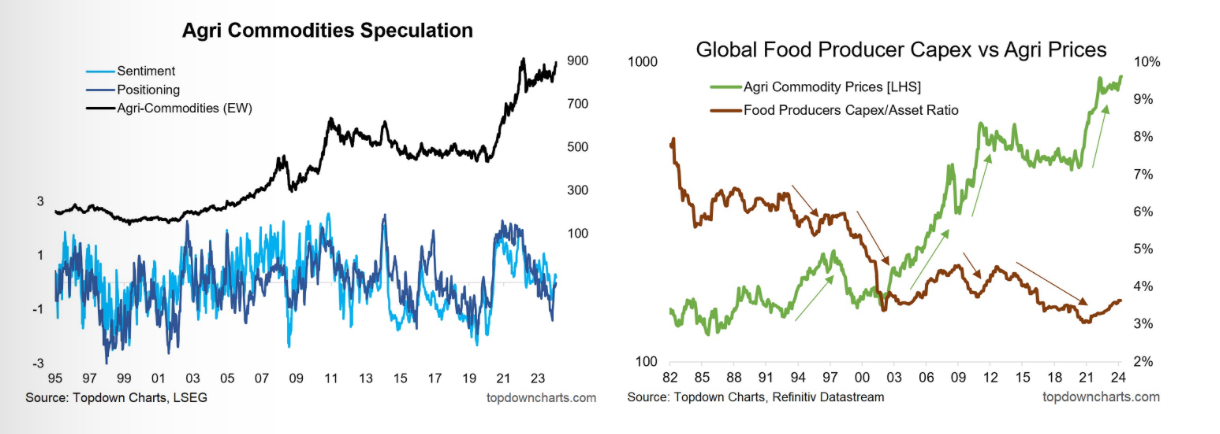

Topdown Charts

Feeling agri

Agricultural commodities have been ticking higher after a period of consolidation following the 2022 peak. There has been some uptick in capex by food producers, but the pace of investment in supply isn’t as strong as in recent years, so Callum Thomas isn’t too concerned about this. Meanwhile, sentiment has collapsed to extreme bearish levels. Grains show similar bearishness; interestingly, the SOI (weather indicator) is ticking up, a characteristic of previous bull moves. It’s a corner of the markets to keep your eye on, especially given the importance of agri/food prices on inflation. Stay alert for upside risk.

CPM Group

Precious metals: What’s next?

In his latest video, CPM Group's Jeffrey Christian discusses the recent price movements in precious metals markets, focusing on gold and silver, while also touching on other commodities including platinum, palladium, copper and oil. Jeffrey reviews the sharp price increases that occurred in precious metals markets as well as the drastic decline that followed. He discusses the reasons behind the rise and fall and draws some historic parallels to further show how this is normal market activity. He also discusses why oil prices have not risen in the face of the Iranian attack on Israel, pointing to oil supply side dynamics. The presentation concludes with CPM Group's short and medium-term projections for gold and silver.

Click here to watch.