Company & Sector Research

Europe

New Street Research

Selling Italy to rebrand as Vodakom?! With the sale of Spain and now the announced provisional sale of Vodafone Italy for €8bn, the profile of the group changes dramatically and it increasingly just becomes a German company instead. This might be a sector-wide missed opportunity at 4:3 consolidation, but given the sale price of Italy is above the value in New Street’s 140p target, they are left scratching their heads on the muted share price reaction, since VOD’s implied EU business is now trading on just 3.1x EBITDA and one-time cash returns are likely on the way. The prospect of being a takeover target looms ever larger.

the IDEA!

Bloomberg reported this week that Italian insurer Generali is considering making a large acquisition in Europe and that NN could be one of its potential targets. The news underlines what analysts at the IDEA! have been saying many times before, i.e., that NN shares are cheap (trades at <6.3x 2024 EPS and a P/BV of 0.55x vs. Generali at 9.2x and 1.18x, respectively), whilst offering a very attractive cash yield. The company has returned €10bn+ in cash to its shareholders (2015-2023) by means of dividends and share buybacks. So, even without a takeover, they consider NN to be a very attractive investment case.

Willis Welby

Median consensus Y3 revenue growth for Willis Welby’s mid cap MedTech coverage remains high at 7.3%, but financial productivity is not generally impressive and with a median implied to Y3 EBITM ratio of 145, expectations are almost all too high. However, EKTAB is one stock that does look particularly attractive. Willis Welby likes the product lines here as well as the financial productivity. And this is a standout cheap share (the implied to Y3 EBITM ratio is in the 50s - significantly below sector peers). Yes, investors should be wary of lumpy orders and delivery, but the positive share price reaction to disappointing numbers recently confirms just how nervous the market is. 50%+ upside.

Forensic Alpha

More accounting red flags - PHIA put through a massive €1.7bn of adjustments in FY23 to get from GAAP-based EBITA of €183m to Adjusted EBITA of €1,921m. Restructuring and acquisition-related charges totalled €381m and this figure has been increasing sharply over the last couple of years. The fact that this charge has occurred every year since 2015 should have investors questioning whether this can really be classified as a “one-off”. There has also been some unusually large movements in the Provisions Schedule as well as a decline in Accrued Customer Rebates, where manipulating supplier rebates is notorious as a tool for inflating earnings.

ROCGA Research

ROCGA’s cash-flow-returns-on-investments based online platform provides a systematic framework to compare, value and gain insight into companies. IFX is on a list of undervalued companies, along with others, including Roche and Kering. Apart from their proprietary economic returns and conventional valuation indicators, data points such as EV/IC against ROIC/WACC are also available. Their interactive tools allow you to model and value one of 2000 companies across Europe and the US. A free consultation and trial can be arranged on request.

North America

Off Wall Street

OWS’ thesis is playing out - AI disruption is accelerating and management is turning to aggressive revenue recognition to obscure the problems. SSTK missed 4Q23 revenues on weak e-commerce. Even with the miss, DSOs appeared to soar yet again and FCF halved. The company guided to flat Y/Y revenue and EBITDA in 2024, but this assumes an unrealistic rebound in the stock business. Instead of taking a hard and honest look at the structural challenges it faces, and preparing its investors for a difficult transition ahead, management changed its segment reporting hoping investors would ignore the fine print and gave 2027 “targets” that appear fanciful at best. 40% downside.

Gordon Haskett Research Advisors

EPS north of $10.00 is very much on the cards for FY24 - shares of TGT were up 12% post 4Q earnings and are now up ~20% since GHRA turned bullish in early Feb. In their latest note, they make the case for both earnings upside and multiple appreciation (via traffic gains and business mix diversification). To this end and within their coverage universe, TGT joins the likes of Dollar General, Dollar Tree and Dick's Sporting Goods where this dynamic could play out in the months ahead. Their TP increases to $200 and is based on ~18.5x GHRA’s 2025 EPS of $10.75.

Portales Partners

Bank Stocks: Controlling the narrative (except for credit quality)

Charles Peabody does not believe that the problems at NYCB will prove to be unique. He thinks the credit cycle has further to play out and that it will get a lot worse before it gets better. He expects regulators to find similar problems at other regional banks. It’s just that they may want to “pace” the discovery process so as not to create a systemic crisis. In the meantime, regional banks (a la Columbia Banking System) will be encouraged to build liquidity (at the expense of NIM) so that they might be able to absorb negative fundamental news (either within their own franchise or at a neighbouring bank). The current risk/reward for bottom fishing is simply not worth it.

Veritas Investment Research

BMO reported 1Q24 results that fell short of expectations on weaker net interest margin performance, lower capital markets revenue and higher credit loss provisions. Veritas continues to see upside risk for credit losses for BMO in a recessionary environment on greater exposure to US banking and commercial lending. They expect adjusted EPS to decline by double-digits in FY24 with positive operating leverage supported by cost synergies tied to the Bank of the West acquisition more than offset by an increase in credit losses and lower NIM expansion. TP reduced to C$101.

Behind the Numbers

BTN lowers their earnings quality rating for TEVA to 1- (Strong Concern) - the company gave its lowest FCF guidance in years as it had already stretched payables by 29 days last year ($630m), pulled in more from sold A/R ($378m) and will need to start paying its opioid settlements. TEVA posts small EPS beats. It cut sales allowances to add 18-40c the last 3-years. EBITDA of $4.5-$4.9bn looks overstated as TEVA adds back recurring cash costs for litigation, some R&D, regulatory compliance… BTN sees EBITDA at $3.1-$3.3bn. TEVA’s debt to EBITDA is 3.45x. At $3.2bn and adding the opioid settlements to debt, the ratio is almost 7x.

Two Rivers Analytics

AEIS features as one of the top short candidates in Two Rivers’ ‘Breaking Estimates Model’ - the power electronics industry faces increased competition, pressuring AEIS’ sales and margins. The company posted lower than expected results when it announced earnings last quarter and all four of its business segments have now seen a decline in revenue during both Q3 and Q4. Estimates have been sliding all year but have taken a sharper turn down this past month. Margins have been falling since 2017, yet are forecast to turn on a dime now and increase immediately to 17% adjusted EBITDA. The stock trades at historically high multiples of sales and earnings. Other short ideas include LGI Homes, MP Materials and Xometry.

Northcoast Research

PDC business in the hot seat? BRC’s revenue growth over the past ten quarters has been negatively impacted by 50-100bps on average, as the healthcare segment has underperformed compared to the rest of the company. Management has a history of culling unprofitable SKU's as well as non-core assets; thus, Northcoast believes a sale of the segment (generating $100m+ in proceeds) is not out of the question. They believe the shares are undervalued as investors have failed to appreciate BRC’s ability to drive continuous EPS growth (14% CAGR since 2016) and the resilience of its business model. Even at their TP of $73, the shares would still be trading at a 30% discount to peers.

Thompson Research Group

GVA has already turned the corner, but the Street has not turned the corner on its perception of the group. However, it is only a matter of time, according to analysts at TRG. With low-double-digit EBITDA margin (more comparable to public-traded peers), improving cash flow generation, a conservative balance sheet, and $5.5bn of CAP, there is a credible case for multiple expansion. TRG’s fair value range for GVA is $68-70 based on ~7x (which they view as conservative) their FY25 EBITDA and represents ~40% upside.

The Edge

The unassuming ESG powerhouse that will likely double - spun off from Danaher in Oct 23, VLTO is a global leader in essential technologies dedicated to safeguarding the world's vital resources. With c.55% of its income coming from recurring sources and its favourable margins, the business is in a strong position to capitalise on its leadership in sectors with high growth potential in a very unstructured industry. A promising candidate for long-term growth and a potential future separation (spinoff) of its 2 divisions could see the stock price double within the next 2 years.

Global Mining Research

A copper growth story with significant optionality within the portfolio to >300kt/yr (vs. 164kt in 2023). After a period of heavy investment, FCF is set to turn positive in 2H24 with production from the Mantoverde sulphides project. The balance sheet is much stronger following the recent equity raising, with Net Debt/EBITDA forecast to fall from 3.8x in 2023 to 1.3x this year. However, near term cash flow is expected to be directed to mines, not the shareholders. CS offers an attractive risk / reward with its exposure to copper, scale, growth upside and a balance sheet expected to rapidly de-lever in the midterm. Growth studies in 2024 are likely to be near-term news catalysts.

ETR

Emerging Technology Survey (ETS)

ETR's ETS provides data-driven insight into which private tech companies are gaining traction in global enterprises by tracking evaluation, utilisation and churn metrics for 400+ emerging technologies. Feb’s survey saw participation from 1556 IT Decision-Makers, including 263 Fortune 500 and 369 Global 2000 organisations. ETR has generated 300+ individual vendor data reports for the companies they track.

OpenAI remains the top performer in the ML/AI sector with the highest Net Sentiment score and second highest Mind Share. Information security outperformers include OneTrust, Snyk and Abnormal Security. Docker and PostgreSQL are two of the highest Mind Share vendors. Kubernetes continues to see the highest utilisation rate across the survey universe, followed by Docker, Postman and Figma. Stripe, Grafana, Postman and MURAL saw material improvements off already strong utilisation rate bases.

BWS Financial

TLNE announces the sale of its zero-carbon data centre campus in Pennsylvania to Amazon Web Services for $650m. The transaction value is more than Hamed Khorsand was expecting and includes a power purchase agreement that would create a minimum of $300m of adjusted EBITDA over the next seven years for TLNE. Moreover, the group has additional assets for sale that could further showcase the underlying value of TLNE's current stock price. Further liquidation of assets could lead to the company being sold in pieces as it would have a small operating footprint to remain public. The share price is up more than 30% since Hamed turned bullish earlier this year.

Japan

JapanConsuming

Key stories from Japan's retail and consumer markets

The latest edition of JapanConsuming includes commentary on 1) the proposal to bring Welcia and Tsuruha together to form a new FMCG mega-retailer. Although both are designated drugstores, their expansion into food and general FMCG means the creation of what will be Japan’s single largest retail chain by sales, sending shockwaves across the entire industry. 2) KDDI acquiring 50% of Lawson, making it a partner to Mitsubishi Shoji in running the third largest convenience store chain. It’s a big deal, but no one really knows what KDDI’s aims are. Some more imaginative analysts suggest this could be just the first step towards KDDI merging with Rakuten in order to beat Amazon.

Asymmetric Advisors

Management upgrades FY3/24 forecasts - sees OP +39% Y/Y to ¥19.7bn (27.2% OPM) and puts the PER at 20x. Although Asymmetric Advisors, who were the first to issue a post-IPO Buy note on Daiei Kankyo, expects slower growth in FY3/25, the direction is still positive as mix and volumes will continue to improve driven by the circular dynamics of growth in both incinerator and final disposal capacity. In addition, waste management demand will only continue to grow and investors can expect further steady M&A add-ons from the highly fragmented market which includes many small companies with ageing owners.

JapaneseIPO.com

Are you seeking a secular growth industry that extends beyond the realm of artificial intelligence? While traditionally perceived as cyclical, there are compelling reasons to believe that certain segments within the construction equipment space will experience sustained growth, according to Yuka Marosek. She favours Takeuchi Manufacturing, whose global presence, growing production base and huge TAMs - global urbanisation, coupled with the expansion of the US housing market and a strategic focus on mini excavators, positions it for significant long-term growth. Furthermore, this growth comes with a great value proposition - the company trades at 11x PE and is backed by ROE of 21%.

Singapore

Tabbush Report

Singapore’s banks are an excellent window of credit metrics in both China and Hong Kong

DBS in Hong Kong shows an 8x rise in credit costs in recent periods. UOB’s credit costs in Greater China move from reversals to charges in the past two interim periods Y/Y. Even while OCBC shows declines in NPLs in all regions, it boosted its NPL coverage dramatically over the past year. Yields on financial assets are far lower at DBS than peers and the differential has worsened, which can mean worsening relative asset quality. Over the past several years OCBC has hardly expanded its financial assets, unlike peers, which can mean less seasoning risk. Long-term credit cost data does not favour DBS, where there can be a more volatile delta than peers in FY24 and perhaps in FY25.

Emerging Markets

Smart Insider

Insider sentiment is extremely bullish in China

Last month saw 565 insider buys and just 46 sells (Sell/Buy Ratio 0.08). Smart Insider had previously reported how Jan’s data was “off the charts” bullish and the improvement seen in Feb takes it to a new level. Buying more than doubled MoM, while selling declined -26%. One note of caution - they only upgraded 10 stocks in Feb (including Chengdu Corpro Technology, Lianhe Chemical Technology and Blue Sail Medical) as in many cases the buying was in extremely weak stocks from insiders with mixed or poor records - but if buying continues at this level, they would expect to upgrade more stocks in the month ahead.

Horizon Insights

China's laparoscopic robots sector looks set to benefit from policy updates and hospital procurement. With over 180 certificates expected by mid-2024, tender volumes could double, offering significant growth potential. Domestic manufacturers, including MedBot, are gaining market share with second-generation devices narrowing the gap in stability and cost. Toumai, a product of MedBot with government support and competitive pricing, presents a strong alternative to Intuitive Surgical’s da Vinci system which currently boasts c.90% market share.

Macro Research

Developed Markets

View from the Peak

The age of AI and cheap energy

As Paul Krake pivots his gaze towards the horizon where AI and renewable energy reshape the global economy, it becomes apparent that the most lucrative investment opportunities may not solely reside in the technology creators but significantly in the technology adopters. The impending revolution will likely unfold within sectors like healthcare, banking and retail, which stand to gain immensely from integrating AI into their operations. Meanwhile, the transition to renewable energy presents a canvas for transformative investment in many industries. Companies that embrace renewable energy, not just as an environmental imperative but as a strategic asset for cost reduction and operational efficiency, will likely emerge as leaders.

Eurointelligence

Europe’s leaky boat

Like the Iraq War twenty years ago, divisions over how to support Ukraine militarily now threaten to become a more permanent rupture in European foreign policy. Wolfgang Münchau believes that the recent leaks from the German ministry of defence will worsen the situation, making clear that that the Russians see Olaf Scholz as the weak link. Everyone in Berlin is now calling for an investigation into an unsecure Webex conference call in which four generals discussed technical details about the delivery of Taurus cruise missiles to Ukraine. The leak keeps the pressure on Scholz not to U-turn on his refusal to send Taurus missiles. The Russians are treating Scholz as a useful idiot, which Wolfgang thinks this is far more worrying than the security lapse itself.

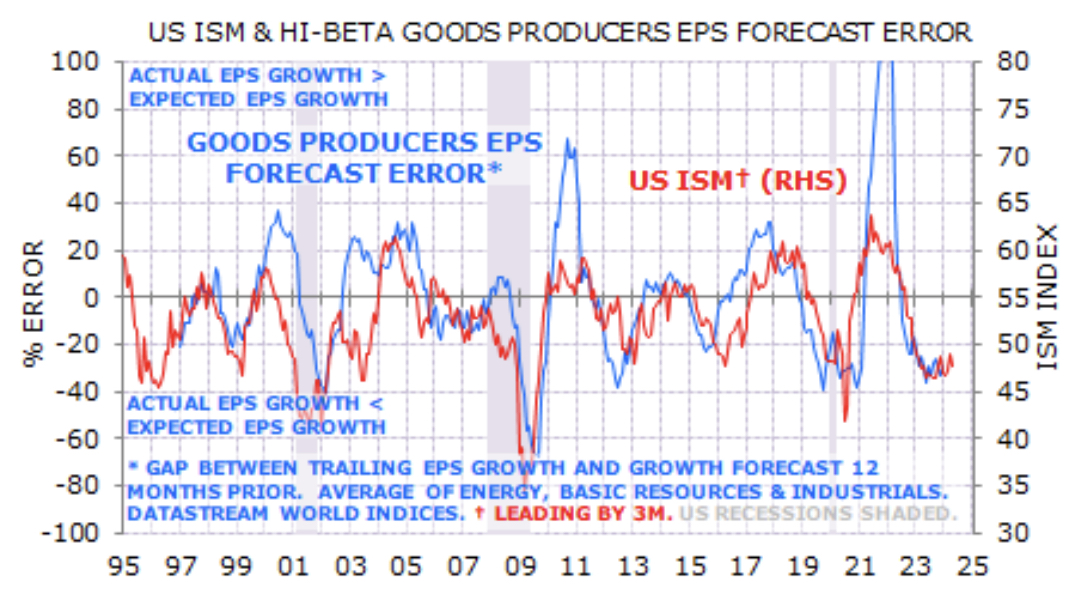

Minack Advisors

It’s a weak, weak world

The world is weak, US exempted. GDP forecasts are inching downwards, inflation is simmering, and it’s only a matter of time before policy rates follow. America’s relative strength points to a stronger USD and equity outperformance, despite the valuation premium. Gerard Minack believes capex will drive the next global cycle where goods makers and their suppliers will do rather nicely. However, these are highly cyclical companies currently experiencing weak EPS levels compared to 2023 forecasts (see chart). With the cycle weak in many places, if you want to invest in the leaders of the next global bull market, wait for a good buying opportunity later in the year.

Aitken Advisors

US: Is the Fed suffering from anosognosia?

James Aitken remarks that there is no urge from the Fed to resolve the apparent cognitive dissonance between underwriting another bubble and the challenges of the inevitable bust. The wider issue is not how many times the Fed cuts, but rather how we get back to a consumption-balancing natural rate without a liquidation of financial assets. For twenty-five years we have produced massive, rolling bubbles of unacceptable and perhaps even illusory wealth from the perspective of society. If one takes Waller’s Q&A at face value, the Fed seems perfectly comfortable with blowing another bubble: if 1995-2000 is the right analogue, then a Fed cut(s) with stocks at record highs means the bubble may just be beginning. There seems to be no reflection that high stock prices could mean real interest rates are too low to contain inflation – with Bitcoin’s breakout, oil reclaiming $80 and the recent rip in gold, it certainly appears to be true.

GFC Economics

US: Policy has become too loose again

Graham Turner points out that new highs in stocks, combined with record house prices, are putting some downward pressure on the labour force participation rate, which saw its recovery peak in August 2023 and has now resumed its secular downtrend. Demographic challenges are ubiquitous across developed economies and interest rate hikes have done little to slacken labour markets. Whether the Fed cuts once or twice is less important than what happens at the long end of the yield curve, which needs to head back towards 5% for conditions to become restrictive again. Long-dated Treasuries have further to fall. If anything, the disconnect between the bond market and the strength of the US economy has grown since the last CPI report. The performance of cryptocurrencies adds to the weight of evidence; monetary policy remains too loose.

Independent Strategy

Has the ECB killed the golden goose?

If the Fed has a new paradigm of low inflation and sustained growth, Europe has discovered low inflation and no growth. The result is a structurally weak Euro. David Roche is now SHORT again. Among his secular themes in his February report, central banks figured largely. The report analysed why the Fed may benefit from a new paradigm. That is sustained growth and low(ish) inflation without incurring a recession or massive layoffs. If so, that would be due to a new relationship between job openings and unemployment. In short, job openings and wage increases could fall in tandem without a massive rise in unemployment. That would avoid hitting household income and risking a recession. And for the nerds, it put a kink in the Beveridge Curve and killed the Phillips Curve dead.

Technical Analysis Group

US 10 year yield outlook

On the first trading day of 2024, TAG called for the next +60 +/- 10 bps to the yield upside. The average rise that followed was +60 bps across 2yy-5yy-10yy-30yy. On February 20th, TAG highlighted the maturing nature of the corrective rise in yields, calling for the next 50-100 bps to come from the yield downside, consistent with their October ‘23 downside projections to 3.55% > 3.15%. TAG now views the February 22nd rebound high to 4.35% as the end of wave ‘B’, now seeking yield downside in wave ‘C’ to 3.29% / 3.28% / 3.12%.

East Asia Econ

Japan: Stronger capex

The outperformer in the Q4 MOF survey data was capex spending, which rose 16.4% YoY, the biggest increase in almost 20 years. Potentially, it also points to rising productivity: while spending on other types of investment also grew in Q4, but the biggest jump was in spending on software, which surged 30% QoQ. Paul Cavey thinks that the size of the bounce at the end of Q4 suggests some one-off factors and points out that previous big rises in software spending haven't been sustained. The rise in software spending is being by led by large non-manufacturing firms. In a sense, that isn't surprising, given services sectors show the most intense labour shortages.

Harlyn Research

Have we missed Japan?

According to Simon Goodfellow, Japanese equities cannot outperform on a sustained basis until Japanese investors start to rebuild exposure to their domestic equity market – something they haven’t for over 25 years. Simon agrees that there have been significant moves to make local companies more investor-friendly, but his models suggest that US equities are still outperforming on a common-currency, risk-adjusted basis. When he runs his standard process, but in yen terms, he finds that Japanese equities are #2 behind the US. There are some sectors where Japan is preferred, but they are small in comparison to the ones where it isn’t. Simon likes Japan on a tactical basis, but there is nothing to suggest that Japanese investors are about to fundamentally restructure their portfolios.

Emerging Markets

Hokenson Demographics

China: Year of the Dragon, Century of the Babyless

The demographic outlook for China has gone from bad to worse. Now, it’s more likely than ever that the country’s 2100 population level will fall short of the UN’s low fertility population projection of 494m. The number of live births has seen a decline for the fifth consecutive year, plummeting by 5.7% in 2023. Richard Hokenson does remark that 2022-23 birth rates could have been depressed by Covid-19 such that we may see a 2024 rebound, but of the past six Dragon years births only increased once. Any rebound is likely to be short-lived. Richard recalls focusing on demographics back in the 90s, with investors gasping when they saw his China chart that showed the country’s demographic path. Now it’s becoming reality.

Greenmantle

China: Stimulus shots, please

The 14th National People’s Congress was marked with an ambitious GDP growth target of ~5%, to be achieved in party by the announcement of a multi-year program of ultra-long term treasury bonds and a greater pledge for central government-led fiscal support. Niall Ferguson thinks the worst has passed for Chinese assets. While markets have yet to respond positively to the announcement, he sees more upside ahead as Beijing will have to do much more than was announced if it is to meet its ambitious growth target – expect more stimulus to come in Q3 in the form of at least an additional RMB 1trn in sovereign bonds. Niall therefore sees a case for onshore equities, bonds and commodities exposed to Chinese manufacturing investment.

PPG Macro

China: Devaluation risk

The Chinese Coast Guard is up to its usual shenanigans in the Philippine Sea. Such behaviour is common, not just at sea but with China’s support for Russia and trading arrangements with Iran. Patrick Perret-Green asks claims we shouldn’t expect anything more when it comes to economic policy; China will do whatever it considers best for itself. This seems to be underpriced in global markets. The market has under-reacted to China’s bond yields hitting record lows. Given interest rate differentials (see chart), why shouldn’t China let the currency go? They can argue they are merely allowing markets to function, which will force the world’s central banks to go back to their playbooks of the mid-teens. Against this background, Patrick remains in the camp that rate cuts are coming.

Emerging Advisors Group

Watch the credit cycle in Hungary

Jonathan Anderson has yet to exit his front-end HUF position, as rates are still relatively attractive, the domestic economy is extremely weak and the external balance has improved accordingly. The thing to watch now is the credit cycle. Barring any unusual rate moves ahead, the key swing vote that would push Jonathan out of the trade is an uptick in lending activity. The equity market has been a big outperformer after the 2022 collapse and earnings are surprisingly strong, but this is a one off tied primarily to commodity prices and not a call for a sustained investment position.

PRC Macro

China: NPC improves fiscal outlook but falls short on monetary policy

William Hess believes the NPC report to be uninspiring but “good enough” as a down payment on the 5% growth target. Based on new inputs from the NPC so far, he has marked up his estimate of implied augmented fiscal expenditure growth for 2024. Overall, the NPC work report retained a familiar supply side bias but acknowledged inadequate demand as the primary impediment to a more credible domestic cycle. Apart from onshore equities (which William guesses were instructed to trade higher), markets were unimpressed by the NPC. The report repeated one of the key policy failings of the past 18 months by omitting specific funding commitments for programs like affordable housing construction, subsidies, and related monetary policy language that implied larger injections of cash/base money.

Burumcekci Research & Consulting

Turkey: Rate cuts unlikely to be soon

In February, CPI increased by 4.53%, higher than the market expectation of 3.98%. As a result, the cumulative inflation was at 11.54% in the first two months of the year. Inflation rose compared to the previous year, influenced by both food and non-food prices. From the indicators monitored in terms of underlying trends; core inflation indicator B index rose to 70.3% and C index to 72.9%, while the annual increase in service prices reached a new historical peak at 94.4%. If the central bank adheres to its guidance, Haluk Burumcekci believes it would be unrealistic to expect an interest rate cut; an interest rate hike may even be possible. In the February MPC meeting, the Central Bank kept the one-week repo rate at 45.0%, stating that the current rate will be maintained until we see a significant and lasting fall in inflation.

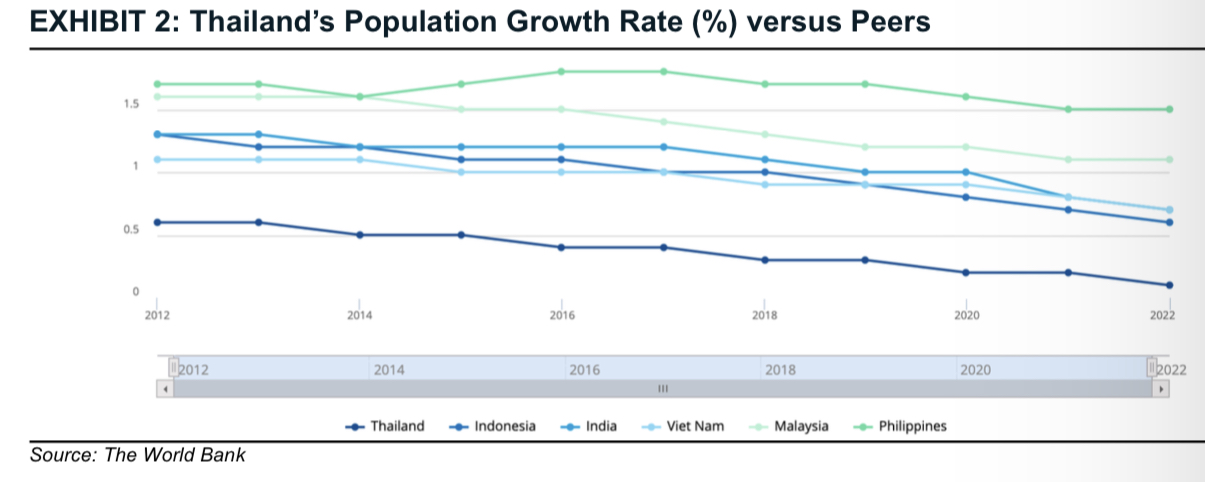

Bondcritic

Thailand: Ageing poor

Thai equities lack growth and innovation, claims Warut Promboon. Big corporations continue to have unfair advantages when it comes to financing and barriers for newcomers are strong. The country’s ageing society is suffering from rising income disparity and a stalling education system. Economic and political restructuring is needed and Warut predicts more unpredictable disruptions and policy blunders that could impair stock performance. He believes the country is unable to correct its course in the near term and is underweight the Thai stock market as a whole.

Commodities

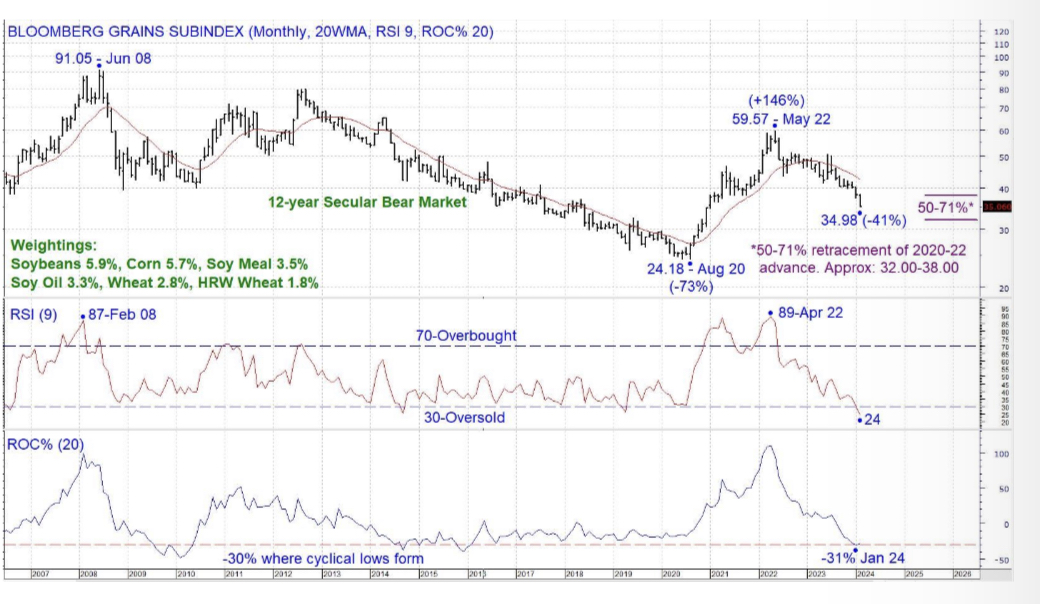

Grey Investment

Grainy prospects

The Bloomberg grains Subindex (35.06) has been one of the worst performing commodity sectors since the broad-based index peaked in 2022. It has retraced around 62% of the 2020-22 surge and is now roughly in the middle of the area where Chris Roberts would anticipate the secular bull market in commodities to resume from. The featured indicators are in oversold territory, where cyclical lows typically form, and Chris is preparing for the resumption of the secular advance.

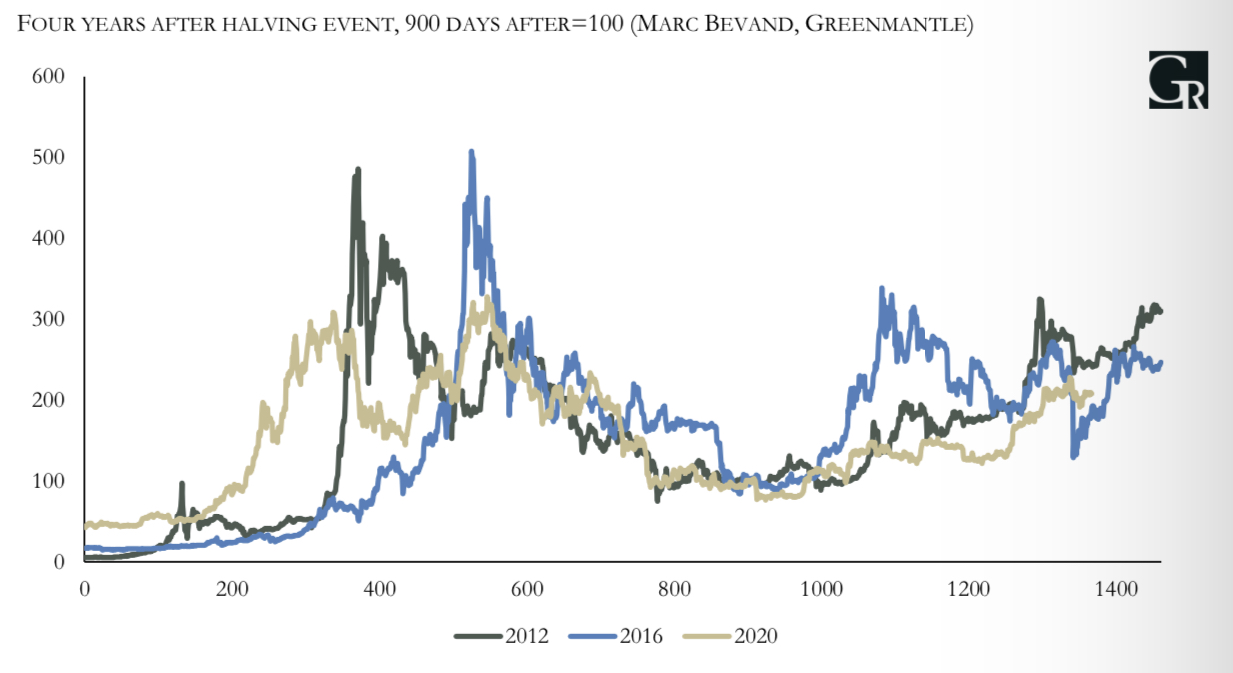

Greenmantle

The other side of Bitcoin

Bitcoin is over a decade old and has gone through several cycles. An asset-pricing literature has developed that explains Bitcoin essentially as a procyclical, high beta risk asset with a tight relation to retail flows. Should the economy hold up—a big “if”— Niall Ferguson remarks that the conditions would be set for a bubble after Bitcoin’s halving event in April lasting until H1/25. However, the increased institutional flows over the longer term should still support Bitcoin prices even without a post-halving bubble. These new inflows driven by recently approved spot ETFs in the US could deliver the bubble-sized gains, but (like the gains delivered by the rise of crypto exchanges) they run counter to Bitcoin’s founding ethos of decentralisation and original use-case as a means of payment. Niall is LONG Bitcoin based on historical patterns.

Steno Research

Commodities are finally moving

Andreas Steno comments that things are finally starting to move a bit in the commodity space, with copper, silver and crude showing bullish improvements in his z-score based overview, but readings are still bearish. The commodity space is the most sensitive asset class to the actual economy, so Andreas asks if this positioning represents early signs of a cyclical comeback, or just noise. Tin, which has the highest beta to ISM manufacturing, has turned very bullish this year, which should speak for the first case. Andreas is net LONG broad commodities and has added additional exposure towards energy in crude and natural gas.

ERA Research

OSB prices moving higher again, further increases expected

After posting modest declines earlier this year, OSB prices have rebounded from the mid-February low of $411 to $439 (chart 1). At the same time, indicators show US structural panel dealers’ sales-to-inventory ratios are moving higher (chart 2). The ERA team suspect that many OSB buyers delayed wholesale inventory replenishment when it looked like prices were set to roll over this quarter. However, when prices abruptly reversed, they were forced to pull out of their PO books, leaving OSB producers in the seat once again. In the near term, further OSB price increases seem assured and whilst the team sees risk of oversupply for OSB in H2/2024, their outlook has become less negative. Trade recommendations are more focused on the next US housing upcycle as opposed to a seasonal trade around spring building. Over the longer-term, the team sees most upside for TSX:Interfor ($26 target price) and NYSE:Weyerhaeuser ($39 target price).