Company & Sector Research

Europe

Insight Investment Research

Transactions indicate high upside for listed Infrastructure

Robert Crimes reviews 138 global infrastructure deals that took place between 2015 and 2023, focusing on the 38 where he had a DCF based NAV. These transactions averaged a -3% discount to Insight NAV but listed valuations trade at a -35% discount. Share prices would need to rise c.50% to close the valuation gap. Robert expects deal flow to continue driven by undervaluation of listed corporates, resilient indexed linked FCF growth and reducing COC. Insight's key Buys to arbitrage from listed to unlisted are Ferrovial, Getlink, Inwit and Cellnex.

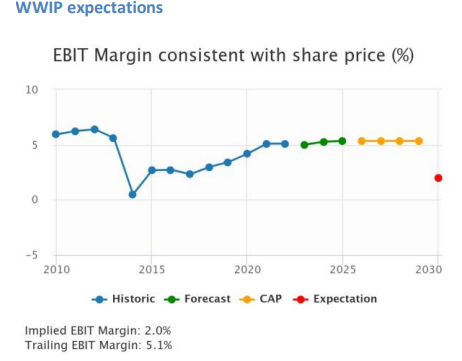

Willis Welby

It feels like the SRP share price is increasingly an anomaly. This was a problem child but looks to have been fixed for a while now and the recent bout of big upgrades has been met with indifference. The consequence is an implied to Y3 EBITM ratio of just 37. Last time Willis Welby ran the numbers, they could still make this share price work at GBP 2.50. They can now make it work all the way up to GBP 3.00 - nearly double the current share price.

Ben Jones Investments

This mining services company provides drilling, laboratory and waste haulage services to blue-chip firms. CAPD boasts higher margins than its competitors and has maintained these margins with significant growth over the last 2 years. Ben Jones forecasts EBT margins of ~20% going forward with FCF yield of 25% by 2025. Current trading is strong, having recently signed new drilling and laboratory contracts which Ben expects to add 11% to revenue growth in 2023 and 17% in revenue growth in 2024. The market is failing to price in this growth leaving a wide gap between CAPD’s M/Cap and Ben’s view of intrinsic value.

Smart Insider

Jens Engwall (Director since 2020, CEO 2018-2020) sells 67,743 shares at SEK 95.95. Smart Insider ranked this stock +1 (highest rating) on 2nd Jun 2023 based on purchases from Engwall as well as David Mindus (Director since 2023) around SEK 60 per share. The stock has risen over 50% and this change in sentiment is not surprising but forces them to downgrade the shares to neutral. Engwall's excellent record as both a timely buyer and seller continues to grow. His last sales were in Jan 2023 at SEK 88 and in Aug 2021 at SEK 142, both of which proved timely.

North America

Your Weekend Reading

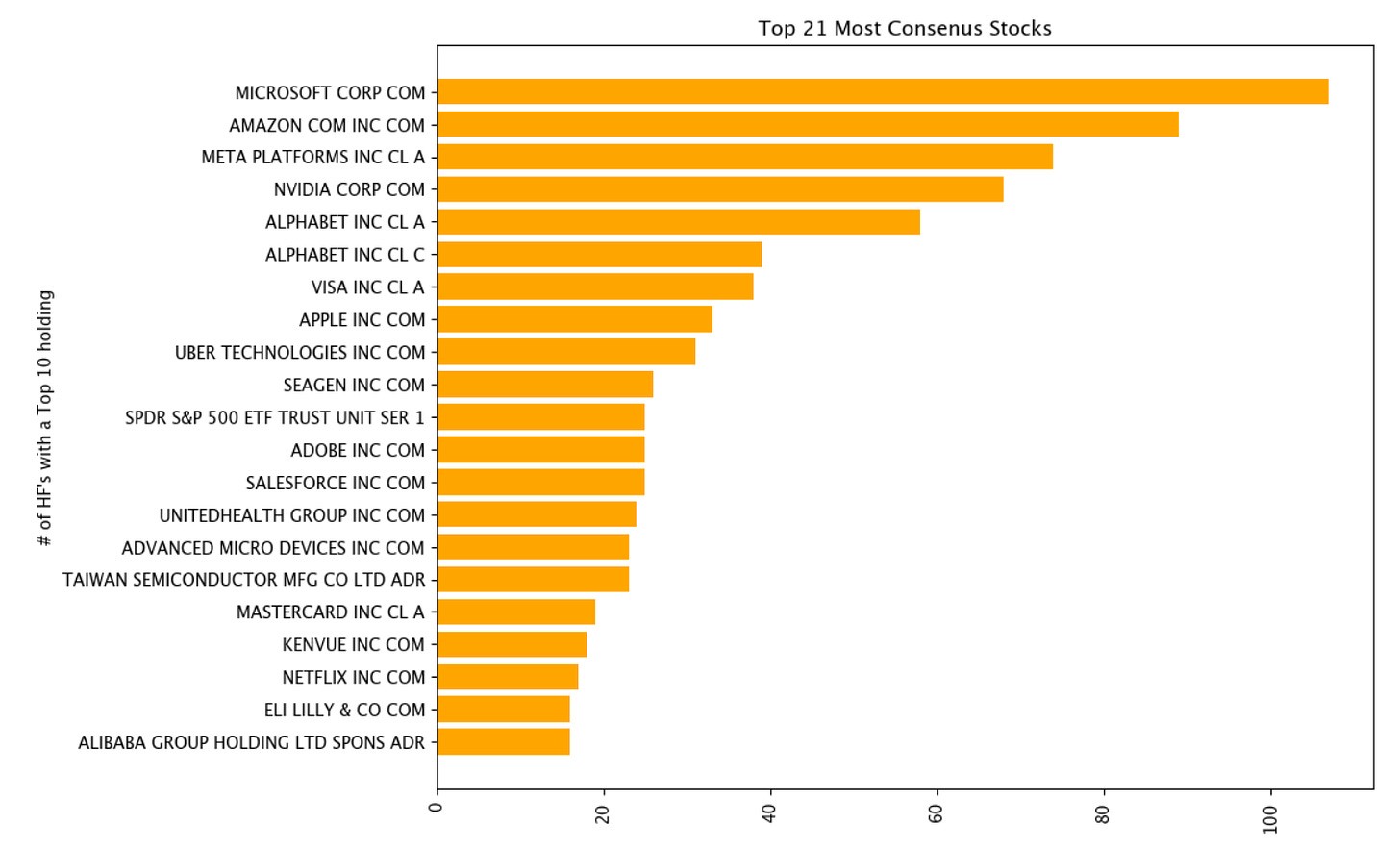

How consensus is your hedge fund?

Erik at YWR analyses $2trn in public holdings at 310 global hedge funds to find the most consensus holdings and the most consensus funds. He has also done the opposite. Who are the most non-consensus funds and what do they like? When you analyse the funds themselves you find the average consensus fund is much bigger with $26.5bn in disclosed equity positions, while the non-consensus funds average $3bn. New York and London are the most popular headquarter locations for consensus funds. Non-consensus funds are more diversified. For all the data as well as the Top 40 non-consensus stocks click here.

MYST Advisors

Hunting For Alpha: Stocks that continue to offer significant downside

MYST hosted 25 formal events in 2023 generating 333 ideas (223 longs and 110 shorts). It was another impressive year with nearly 70% of their highlighted shorts producing positive alpha. Names that remain compelling include:

Aurora Innovation (AUR) - Entering a highly competitive market with an unproven product. TP $0 (100% downside).

Infosys (INFY) - Financials deteriorating amid structural growth slowdown. TP $12.50 (30% downside).

MP Materials (MP) - EV industry pivot away from rare earth materials to cause massive oversupply / pricing collapse. TP $10 (40% downside).

Veeva Systems (VEEV) - Back-end transition could be “worst tech decision since Osborne Computer Corp”. TP $115 (40% downside).

Arete Research

ETSY is once again allowing its platform to be polluted with items which are hardly 'handmade' goods and degrading the quality of its search results, possibly to grab more GMS and boost its flagging growth. While some investors have been celebrating recent headcount cuts, they are overlooking the structural weaknesses in the business. To revitalise its brand, ETSY needs to 1) Guide to far lower sales as part of an effort to clear the marketplace of counterfeit or inappropriate listings. 2) Focus its attention on sellers rather than buyers. Otherwise, its current approach - denying problems and deflecting value criticisms - will inevitably lead to multiple compression for the stock.

Paragon Intel

Tim Cofer will extend his proven track record of growing corporations organically by capturing market trends and creating economies of scale as well as driving profits inorganically through M&A. Paragon Intel interviewed former colleagues who worked with Cofer for more than 30 years combined. Sources gave him the highest rank for his strategic acumen and fitness as a CEO. However, this praise is somewhat offset by the beliefs of some that he lacks transparency and can be arrogant. Paragon likes the appointment. They believe Cofer’s ability to create a very cohesive and forward-looking strategy makes him well suited to lead KDP.

Boyar Research

IBKR has a small account base (~2.5m) with rapid growth (~26% 10-year CAGR) and unique client segments. The online broker’s leading-edge automation generates pre-tax profit margins >60%, substantially above peers. It also boasts a fortress balance sheet (>$9.4bn in excess capital) and an increasing appetite for synergistic acquisitions. IBKR is largely immune to the well-documented challenges surrounding deposit outflows and investments in long-duration fixed-income securities, as well as the effects of the industry transition to “free” trading. Applying a 20x multiple to Boyar’s 2025E EPS, they derive an intrinsic value of $124 a share (40% upside). They would also not rule out a takeover given Mr. Peterffy’s advanced age and large ownership stake.

Periphery Research Partners

Ridesharing will never be a one-horse race - while LYFT may have burned a lot of bridges with consumers (non-refundable cancellations), the one thing that will bring them back is surge pricing on Uber. As far as the next print is concerned, Hesham Shaaban does not see much risk to 4Q bookings or revenue; he suspects LYFT could potentially see a 2-handle on booking growth and double-digit revenue growth (vs. consensus of 3%). For 1Q24, his scenario analysis suggests there are multiple pathways to exceeding consensus bookings estimates even if frequency doesn’t improve and consensus EBITDA estimates don’t appear to be adequately considering LYFT’s YTD Opex cuts.

Behind the Numbers

How accounting for contract costs is impacting the earnings of 70 big software names

BTN continues their review of the software industry with a look at accounting for costs to obtain contracts. In this report they examine 70 software companies with M/Caps of $5bn+ and highlights four different groups: 1) Companies where the earnings benefit of deferring commissions represents a material amount of reported earnings. 2) Ones that may be about to face earnings headwinds from a decline in benefit from deferring commissions. 3) Ones that may be about to enjoy a positive inflection point where falling accruals are leading to lower amortisation relative to the new commissions being deferred. 4) Ones where amortisation is falling relative to deferred commissions which may indicate that new contracts are rising in the mix of new business.

New Street Research

$400bn spent on datacentre AI chips in 2027? Is it possible?!

The mother-of-all sanity checks - Lisa Su (CEO of Advanced Micro Devices) pitched late last year a total addressable market for datacentre AI chips of $400bn, New Street looks to make sense of this number. In the first of what will be a number of pieces on this theme, they estimate the total datacentre capex, the opex required to run such an AI infrastructure, the revenues required to justify the investment, and, last but not least, what industry revenues and capex would need to look like to support all this.

Sales Pulse Research

Tech Trends: Key themes and questions for 2024

Areas of focus for Sales Pulse in the year ahead will include: 1) Cybersecurity - changing end user priorities and competitive dynamics. 2) UC/CC/CP - will a reduction in seat count negate increased ARPU from AI features? How will continued M&A impact this market? 3) Vendors benefitting from the rapid growth in DevOps / DevSecOps. 4) Gap in orders in 1H24 for networking market as end users digest backlog and we await ramp of next generation. 5) Broadcom acquisition of VMware driving end users to look at alternatives, to the benefit of IBM Red Hat and Nutanix. 6) Ramp of funding for Broadband Infrastructure. 7) Impact of CSP Marketplaces on Distributors and VARs.

BWS Financial

Hamed Khorsand initiates coverage of this independent power producer with a Buy rating and TP of $96 (50% upside). TLNE is public after being in private hands for 6 years and filing for Chapter 11 bankruptcy. While the reduced leverage profile of the business creates a valuation appeal, Hamed believes it is the catalyst from what TLNE could achieve at its Susquehanna nuclear plant that could significantly enhance shareholder value. The stock is currently trading on the OTC Markets making it likely that many investors have yet to hear about it. TLNE is not expected to uplist to a national exchange until the middle of 2024.

Japan

Astris Advisory Japan

A surge in the value of Arm Holdings has provided some support for SoftBank shares since an early Dec swoon although the discount has also widened as markets have been hesitant to allocate full value to short-term changes in NAV and (probably) an uncertain yen. Kirk Boodry expects the long-term story for SoftBank will be aligned more with Vision Fund activity, both monetisation and a step up in investment pace, but the discount here provides an attractive entry point (discount to NAV currently stands at 50% - the largest it has been since the Covid sell-off in Mar 20). In Kirk’s latest report he updates his model for Q3 (Dec) including forecasts for the quarter.

JapanConsuming

Top stories from Japan's retail & consumer markets

This month's edition of JapanConsuming includes articles on: 1) Asics - sets its sights on becoming the leading performance running brand in Japan, Europe and the US by 2026. 2) Major food-drugstores like Kusuri no Aoki and Genky DrugStores continue to pressure local supermarket competition. 3) Itochu’s online platform to help retailers procure overseas products. 4) A new luxury digital emporium for the wealthy. 5) Shopping mall development looks set to fall in 2024 as developers favour refurbishment over new builds. 6) New regulations are forcing Japan’s logistics industry to evolve rapidly with many consumers seemingly willing to accept slower deliveries.

Azabu Research

Welcia’s stock dipped 6% in the morning hours following 3Q results, but Q3 is a seasonally small quarter. The Q3 miss amounts to less than a 3% hit to expected earnings for the full fiscal year to 3/24, which Mike Allen argues is trivial compared to the rebound expected in 3/25. Meanwhile, the stock trades below the prices that Japanese drug store typically sell for in the private market - lower in fact, than what Welcia typically pays for its acquisitions. Mike does not see how this is sustainable.

Emerging Markets

RedTech Advisors

China Gaming: A misstep overshadows positives

The Christmas massacre of Tencent and NetEase was another grim reminder of the regulatory exhaustion sapping investor confidence in China. However, RedTech argues that the underlying policy stance is more supportive of gaming than it has been for some years and the introduction of the draft rules was a ham-fisted misfire and not another change in course. The regulator has already hinted that the final draft is negotiable and the companies’ own actions (buybacks) also suggest they are not overly concerned. If the new rules are more bark than bite, then investors should be looking for opportunities instead of the exits.

Blue Lotus Research Institute

Amid the world’s transition to clean energy vehicles, BYD’s middle-of-the-road positioning, strong engineering background in both ICE and battery technology, and long brand track record will allow it to assume the role of Volkswagen or Toyota in the EV era. The US-led protectionism and the rise of Huawei-affiliated EV brands will uniquely help BYD to compete at home with the best and transfer the learnings outwards as a trusted bridge to the world. Both BYD and BYD Electronic International trade near their historical lows in terms of PE band. Blue Lotus initiates coverage with a Buy rating and a TP of HK$350 (65% upside).

Galliano's Financials Research

Big cap GEM Bank investment recommendations for 2024

Victor Galliano favours four longs and one short as his conviction calls for the year ahead. 1) Bank Mandiri (Indonesia) continues to generate improving returns and has strong capital ratios, credit quality and liquidity metrics. 2) KB Financial (South Korea) is a deep value pick. 3) China Merchants Bank is a contrarian pick, which looks well positioned to confront concerns re. Chinese NPLs and also on very attractive valuations. 4) Banco do Brasil screens well re. valuations and returns; its growth potential also looks particularly appealing. 5) Victor’s key sell is Kotak Mahindra Bank (India) as it is richly valued, exposed to low prospective earnings growth and has low credit quality coverage.

CHA-AM Advisors

Shipbuilding: Another industry gets China’ed!

The Chinese are now the mainstream and that is going to change everything in this industry very quickly, according to David Scott. Chinese yards are moving out of their success in bulk into the more “value-added” segments of the industry such as containers and LNG carriers. Ferries and then cruise ships are next. Of course, the pattern is almost the same as we see with EVs, wind turbines, solar panels, etc. 1) The Chinese turns and ratios are already of an order of magnitude better than the incumbents. 2) The gap is widening further as the China industry scales and vertically integrates into its huge domestic clusters. 3) China’s ever more competitive real effective exchange rate is accelerating this whole process. Yangzijiang Shipbuilding looks set to be a big winner.

Macro Research

Developed Markets

Belkin Report

Making profit amidst the coming doom and gloom

Investors believe the economy is in a soft landing crafted by immaculate Fed monetary policy. The truth is probably different, claims Michael Belkin. Markets and the economy have been distorted; first came Covid, then came the huge stimulus created inflation, now the economy has rallied back to the same S&P500 level. What is fresh in investors' minds is inflation and interest rate hikes as the only risks to the stock market. But times have changed, and nobody seems to have grasped that corporate earnings were boosted by inflation, which is now falling and pushing down earnings. Michael forecasts a recession that undermines the entire exaggerated valuation of the market. In the meantime, it’s not all doom and gloom. Sector rotation offers an excellent opportunity to those who are willing to buck the system. The tech and comms services are his favourite SHORTs, and defensive stocks left behind in the 2023 rally (financials, consumer staples, healthcare, utilities) are among his top LONGs.

CrossBorder Capital

Global liquidity levels are rising

Michael Howell’s estimates put aggregate global liquidity at a whopping US$172 trillion, a record high, and this should continue rising before peaking in late-2025. The data further confirms Michael’s view that QT de facto ended in October 2022. Collateral values are trending higher; collateral underpins liquidity and these positive factors are behind the soaring growth rate. Added to this, Central Banks – specifically, the “Big Two”, the US Fed and PBoC – are injecting liquidity into money markets. This should help to settle bond markets, which in turn will underpin collateral values and hence global liquidity. A promising start to the New Year!

Saltmarsh Economics

Will 2024 be the start of significant UK interest rate cuts?

Last week saw the PM Rishi Sunak suggesting an autumn UK general election, consistent with David Owen’s last note on the UK. August could be a pivotal month for the BoE’s MPC, with one further meeting (19th Sept) before a possible Oct 10th poll. In the interim, Deputy Governor Ben Broadbent and Jonathan Haskel - who again voted for a rate rise at the last meeting – will step down and Chief Economist Huw Pill’s and Catherine L Mann’s appointments will likely be renewed. A changing composition at the MPC could also have a bearing on what happens to UK monetary policy later in the year. However, David remains far from convinced that 2024 will be the start of the significant rate cuts priced into the curve. He has written before about the biases in the market and amongst many commentators hoping to see the return of much lower rates.

Trivariate Research

A bull-steepening curve that un-inverts will be positive for stocks

Trivariate’s proprietary macro gauges are mixed. Economic activity has troughed and financial conditions have eased. Industrial activity is close to bottoming. A slowing consumer is the biggest concern. This cycle feels more like a Fed adjustment than a reaction to a crisis (like the accommodations in the TMT bubble, Great Financial Crisis and Covid). The Fed probably won’t cut 6-7x in the next year, unless macro conditions markedly deteriorate. A bull-steepening curve where we un-invert will be positive for stocks. Earnings will slowly expand. Adam Parker’s base case is that earnings grow by 7.2% in 2024 and 6.3% in 2025, below the bottom-up consensus of 10.5% in 2024 and 11.9% in 2025. Nevertheless, he considers the risk-reward for US equities is skewed to the positive for 2024.

Pennock Idea Hub

US: Forecast rate cuts will be disastrous

The FOMC minutes said, “In discussing the policy outlook, participants viewed the policy rate as likely at or near its peak for this tightening cycle…" They went on about "an unusually elevated degree of uncertainty". Ed Pennock says the risk is that the Fed is compelled to cut. Multiple cuts would speak to the Fed seeing something in the economy that he has not factored in, and the forecast of 6 cuts in the 8 meetings worries him greatly - the economy would likely be in a mess. Everybody is still watching the 10-year yield but they should focus on the slope of the yield curve, which is starting to dis-invert. If we can get back to a positive yield curve, the banks will finally do well and capital allocation could go back to optimised returns. That would facilitate the complete broadening out of markets. Investors that have had a tough time looking for value in global small-caps will be a lot happier. Ed recalls that 1995 was a set up for a massive run all the way to 2000.

Talking Heads Macro

Japan: The political economy of wages and rate hikes

Manoj Pradhan discusses the case for the BoJ to back off. He first references the global monetary peloton, directed by the Fed, which is running collectively in the opposite direction to the BoJ and threatens to weaken its fundamentals. He also discusses the politics of real wage declines, which has created political headwinds at a time the government is fighting a corruption scandal. Finally, there’s the fact that both capex and consumption need further support from the BoJ. Since March 2023 Manoj has been LONG Japanese equities, a decision based on an extraordinary move in planned and realised capex. Private non-residential investment remains promising, but much of that depends on profitability, which in turn depends partly on a weaker Yen. The graphs show higher profits feeding into capex intentions… a change in the monetary regime can dislodge capex via a stronger Yen and weaker profits. Manoj recommends staying LONG Japanese equities.

HCWE & Co.

Stocks for the next 10 years

According to David Ranson, what determines the success or failure of a ten-year investment in stocks is not economic growth. Instead, it’s inflation. David says that pessimists about future inflation should minimise their exposure to the stock market – except for equities associated with real assets. He points out that capital markets don’t lend themselves well to long-range forecasts. The so-called “business cycle” has very little relevance to asset performance five or ten years out. Inflation, on the other hand, is a factor that reaches into the future. Indeed, one of the reasons that inflation is so often seen as “stubborn” is that it comes in multi-year waves, resulting in wavelike behaviour in the performance of asset classes that are sensitive to it – including most of the investment categories among which asset allocators have to choose.

Emerging Markets

TenViz

Will 2024 be the year of Asian outperformance?

There are major negative regional demographics, with a contracting labour force and/or low birth rates across the region, but unmatched educational levels, high work ethics, first-class infrastructure and an abundance of high-tech leaders will see the South-East Asia outperform. Not only that, their equities are among the world’s cheapest and industrial production is accelerating across almost all of Asia (ex Japan). Konstantin Fominykh has a BUY on Asia sovereigns since Dec 27th 2023, a BUY on 30Y Australia (which is strategically crucial) since Dec 28th 2023, a BUY on Japan equities since Mar 15th 2023 and a BUY on Taiwan equities since Nov 30th 2023.

Emerging Advisors Group

How to make money in China in 2024

Jonathan Anderson expects local rates and fixed income markets to remain steady this year, as well as a relatively stable exchange rate – but given how compressed yields and spreads are, this isn’t a particularly attractive sector. Nor is Jonathan interested in China-related commodities, which he believes is subject to downside pressures this year. The more interesting market is equities, where (i) both A-share and MSCI China indices are trading at very low multiples, (ii) inherent price volatility is much higher and (iii) returns are historically uncorrelated with either macro or policy activity. Jonathan isn’t buying stocks today, but is ready to enter once he sees sentiment returning. Offshore high-yield dollar bonds are also a rollercoaster market; spreads have narrowed considerably and he worries that pricing is overly optimistic, but he would revisit exposure in a renewed sell-off.

Trivium China

China: Monetary policy is back in fashion

China’s monetary officials aren’t content to sit on the sidelines as the economy limps along. That’s Trivium China’s reading of comments from Zou Lan, director of the central bank’s (PBoC) monetary policy department. In an interview with Xinhua, Zou said the PBoC: “Will strengthen counter-cyclical and cross-cyclical adjustments”. The PBoC will use all its monetary policy tools – including reserve requirements, relending quotas, the medium-term lending facility (MLF), and open market operations – to: “Provide strong support for social financing and the reasonable growth of money and credit”. Until recently the PBoC strove to ensure credit and money supply growth was broadly in line with nominal GDP growth, but it now aspires to match credit and money supply growth with the GDP and inflation targets. This should give credit and monetary growth room to run a little hotter than it has throughout 2023.

PPG Macro

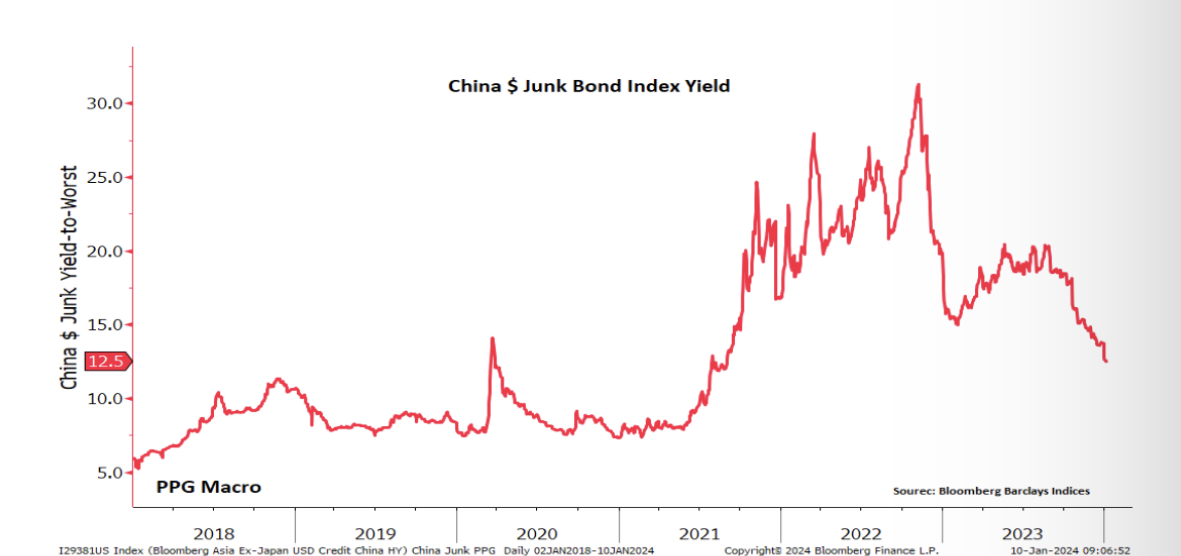

A China surprise?

The China property bust has been a long-running issue – Patrick Perret-Green first wrote about Evergrande back in July 2021. It remains a millstone around the neck of the global economy. Nevertheless, one of the possibilities that’s on Patrick’s radar is that China, relative to expectations, could be an upside surprise. If so, the impact on the global economy and markets could be significant. For all the doom and the gloom, the regime is making progress. One reflection of this is the powerful recovery in Chinese US dollar high yield bonds. There is, however, a big caveat. The fall in yields has been exaggerated by the removal of defaulters from the index, issuance collapsing to non-existent levels and bonds maturing. Over the past year the amount outstanding has fallen from $81.7 billion to $47.4 billion.

PRC Macro

China: Zhongzhi bankruptcy opens door to stimulus

In a pivotal move, a Beijing court accepted Zhongzhi Group's bankruptcy application, a major private financial conglomerate laden with distressed debt and troubled developer projects. Following the nationalisation of Zhongzhi's trust subsidiary in September, a similar fate looms for Evergrande. Onshore investors foresaw these events since their financial licenses were nationalised last September. William Hess sees Zhongzhi's bankruptcy as a positive for property sector policy support, paving the way for broader liquidity injections and demand stimulus for surviving developers. Beijing's shift towards a comprehensive bailout strategy, recognising the inadequacy of selective measures, is noteworthy. Initiatives like Guangzhou's property purchase voucher scheme and Shenzhen's urban village renovation plan aim to de-stock property inventories and rejuvenate construction. William also highlights the PBoC’s commitment to support property sector policies and construction, which – although not directly targeted towards equity markets – will be taken as positive.

Greenmantle

Taiwan votes

Taiwan will soon elect its next president. The front-runner is Lai Ching-te (William Lai), of the DPP. But Hou Yu-ih of the KMT and Ko Wen-je of the TPP both have a shot. Niall Ferguson claims the vote will be closer than the polls suggest. If Lai wins, Niall expects Beijing to ramp up military activity around Taiwan, including air-naval exercises and coast guard exercises to simulate a blockade operation. Unlike Beijing’s response to Pelosi’s visit in 2022, this operation could have multiple stages and persist over weeks or months, disrupting shipping and rattling markets. However, Niall sees volatility or abrupt selloffs resulting from such exercises as a buying opportunity, since Beijing’s goal would be deterrence against Lai, not preparation for invasion. The bigger risk is that Lai, who is prone to ad-libbing statements on sensitive cross-Strait matters, will inadvertently trigger a crisis. If he wins, he could do so at any time in the next four years. If Hou or Ko wins, he expects a relief rally and no military response from Beijing.

ESG

Adelwise

Ocean investing: Momentum builds

The Blue Economy stock universe has a market cap of US$15.2trn and includes over 1000 stocks with a M/Cap >US$500m. The universe is highly concentrated both at the country and sector levels. Almost a third of companies are American, while 72% of the companies are either Industrials or Energy stocks. During 2023, the Blue Economy stock universe rose by 11% thanks to the outperformance of the Healthcare and the Hotels Restaurants & Leisure Industries. Sophie Biro-Rouillon expects stronger performance going forward: earnings growth expectations have turned positive for FY2 and the Blue Economy universe ex-Energy sector has a consensus analyst rating of 3.9 (Hold is 3, Buy is 4).

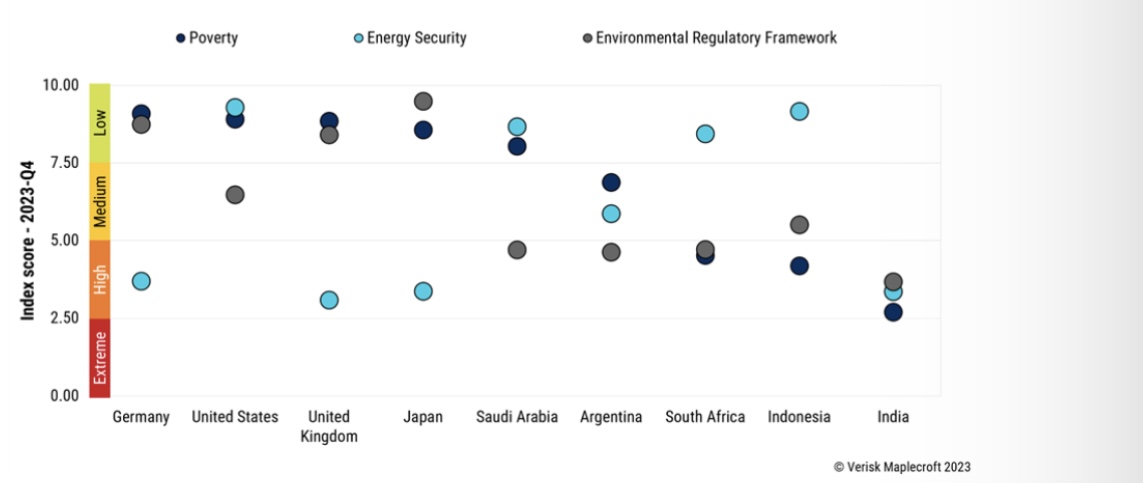

Verisk Maplecroft

The competing goals of the energy trilemma

Maplecroft looks at how DM and EM governments are trying to balance the competing goals of the energy trilemma – the push-and-pull between energy affordability, security and sustainability. From industrialised economies aiming to reduce GHG emissions and manage geopolitical risk, to developing economies trying to balance economic and social development needs against extreme climate risk, this trilemma poses multiple challenges, as summarised in the chart. The selected G20 countries face higher risk on at least one of the indices, underlining the trade-offs and challenges for governments (and their creditors) looking to deliver both an affordable and long-term-secure energy transition. In the coming year, we will need to see more grid investment in EMs to unlock power markets and allow for the scaling of renewable energy sources. In addition, energy security needs will prompt countries to tackle emissions from fossil fuel assets with CCUS tech and carbon market instruments.

Commodities

Steno Research

Bitcoin ETF approved, but does it mean anything?

The crypto industry’s big dream has become a reality, with the SEC’s approval of 11 Bitcoin spot ETFs. Andreas Steno says the approval of Bitcoin spot ETFs was always a matter of “when”, not “if”. The short-term impact of Bitcoin ETF is already factored into the price, but once the market realises the ETFs might not attract as much net inflow in the first few months, a sell-off could be triggered. However, looking at the long run, Andreas as extremely bullish on spot ETFs. They open the floodgates for new capital, allowing institutions, hereunder asset managers and financial advisors, and retail investors to allocate capital to Bitcoin in a cost-effective and well-regulated structure. However, he favours Ethereum, which he believes to be significantly undervalued compared to Bitcoin.

Vanda Insights

Oversupply weighs on crude as Middle East premium ebbs and flows

Crude has begun 2024 exactly where it left off in 2023 — whipsawed by an uneven tug-of-war between a bearish global oil supply-demand balance outlook and a risk premium from fears of Middle East supply disruptions as the region is gripped by growing geopolitical tensions. Crude prices have been hemmed into a relatively narrow band over the past three weeks. Brent futures have been confined to a range of $76-81/barrel from mid-December through the first week of January. While this could be down to an unsettled sentiment mingling with the usual year-end slump in trading activity, Vandana Hari sees this phenomenon persisting. In other words, crude prices may remain jumpy but continue to flit in a small range unless a war engulfs more of the Middle East.

Global Mining Research

Can gold back it up in 2024?

At the time of writing, the spot gold price is US$2,030/oz and well above consensus estimates for 2024 of US$1,925/oz (Factset). David Radclyffe examines whether the drivers behind the price will continue. First, inflation is not likely to be the same factor as it has been in the recent past, and the 3Q23 gold price retreat may have represented a pricing in of lower inflation. There’s also a historical inverse correlation between 10-year US bond rates and gold prices; if rates move back towards the decade average of 2.3%, it should be a positive catalyst for gold. There’s also the US dollar, which often has an inverse correlation to gold and could weaken amidst lower rates and a soft landing. Yet in spite of decade high prices, very few gold miner equities are anywhere near a high level; what will it take for gold equities to price levels closer to spot?