Company & Sector Research

Europe

New Street Research

Leverage is coming down, dividends to flow. TEL has won a tax case (+NOK2.4bn) and sold its satellite business for an EV of NOK2.4bn, both of which will help with deleveraging. New Street explains why they believe consensus net debt numbers are wrong and have also published a note looking at Thailand; incorporating their new associate dividend assumptions they remain convinced that the group’s dividend will not be cut and can actually grow as OCF grows (EBITDA led). TEL has a 8.5% dividend yield vs. the sector average of 5.1%. Given the positive news flow, any weakness in the share price should be seen as a buying opportunity.

Starling Advisors

Firing on all cylinders - PUM has outperformed its peers over recent quarters through a successful relaunch strategy leveraging on running, performance and lifestyle wear. The company is making strong progress in building up more brand desirability and product heat. It has continued to gain momentum, thanks to its commitment to quality, innovation and the right collaborations with leading athletes and fashion icons. Despite the progress (PUM continues to be well on track for 10% EBIT margin by 2025), the valuation gap vs. adidas has widened on an EV/Sales basis to 31%, which Alex Dwek believes is unjustified. TP €80 (40% upside).

Forensic Alpha

Forensic Alpha has previously raised several accounting flags at BAVA, particularly around inventory and capitalisation of costs. However, publication of the biotech company’s Q3 report saw fresh issues arise, mostly around working capital. The combination of bill-and-hold transactions with rapidly rising receivables (+78% y/y to DKK 1.2bn) is worrying. BAVA is clearly expecting a big ramp up in demand for JYNNEOS into 2024 and this may well override any concerns Forensic Alpha has about phasing. However, investors should at least be aware of the risk that revenues are "pulled forward" from a future quarter.

Insight Investment Research

Robert Crimes increases his valuation of FER’s 55.7% stake in the I-66 by +18% to €5.2bn. Having fully opened 12 months ago, the toll road is beating all forecasts. Robert models revenues of $300m, 35% above Cintra’s estimates in 2024E, due to higher toll prices as a result of good time savings, wealthy users and more trucks. Willingness to Pay will continue to rise with worsening congestion and household income growth. Robert expects I-66 EBITDA growth +6.7% CAGR, driven by average tolls/transaction rising from $7.70 in 2024E by +4.9% CAGR and traffic +2.8% CAGR 2024-66E. His SOTP based TP increases to €68 (120% upside).

ResearchGreece

Trades on 5.5x EPS (ex-cash), 3.5x EBITDA 2023E, with a dividend yield >7%. PPA has produced a strong set of results for Q3 / 9M and the outlook for 2024-2026 is equally impressive. Undemanding growth can push EBITDA to €132m-134m and net income to €85m-86m in 2025-2026; with the valuation dropping to 2.5x EBITDA. More importantly, these numbers imply equity cash flow generation of c.€80m p.a. (15% yield), driving net cash to €285m (€235m incl. leases) or 50% of the current M/Cap. ResearchGreece initiates coverage with a Buy rating and TP €33 (50% upside).

Iron Blue Financials

An Iron Blue score of 28/60 is top quartile (fertile ground for shorting). Red flags include 1) Regular (and higher y/y) use of stripped out restructuring and other one-off costs. 2) Elevated use of provisions accounting, including €39m releases during FY23. 3) Increased client investment capitalisations. 4) Gap between €2.9bn headline net debt (2.4x net debt/EBITDA) and Iron Blue’s preferred calculation (€4.0bn, 2.9x). 5) Extended KPMG auditor tenure (20 years) and above average non-audit fees. 6) Management structure out of line with best practice (combined CEO/chair, non-independent board, shares/votes mismatch, Bellon cross-holding). 7) 41% y/y rise in whistleblower cases.

North America

Trivariate Research

Is quality even a thing for value investors?

Less than 10% of all value stocks are in the highest quality quartile of Trivariate’s proprietary substance model vs. >40% of growth stocks that are in the highest quartile. Within the value universe, there are only 20 mega / large cap. high-quality stocks, making it impossible to be a large cap quality value investor. Among the largest 2000 US equities by market cap., 40% of the top half of quality stocks in the growth universe are in the Tech sector vs. <1% of the top half of quality value being in Tech. On the contrary, >50% of the quality value universe is in Financials, Real Estate, or Utilities, vs. <7% of the quality growth universe. The growth portfolio managers are talking to totally different industry analysts than the value PMs! Signals for investing in value stocks and Trivariate’s top long / short ideas include...

Periphery Research Partners

The upside surprise from CART’s 3Q23 results (order efficiencies) introduces more questions heading into 2024, which is the focal point of Hesham Shaaban’s current short. Investors should remember that the primary source of the company's YTD EBITDA leverage is its Opex cuts, which are not likely to continue into 2024 at a comparable magnitude. In the absence of said Opex cuts, the only real leverage in CART’s model comes from its take-rate, which Hesham expects to be a source of pressure as the group struggles to stabilise its KPI growth.

Verbatim Advisory Group

According to Verbatim’s latest channel checks, Oct sales trends are weaker than Sep and overall Q3 trends. They first noticed weakness within their MCD (US) sample a couple of months ago and now that slowdown has accelerated. Customer count has been negatively impacted by the inflationary environment and higher competition. The average basket size has reduced. Promotions are increasing. The current y/y comparison is tougher both on a one-year basis and on a multi-year basis. In Q3, Verbatim required a bias of positive 170 bps. Based on the tougher multi-year comparison and weaker trends, they are applying a bias of positive 50 bps in Oct. With an Oct Raw Comp of +3.5%, their Oct Comp Estimate is +4.0%.

Bios Research

Healthcare: Top 5 short ideas

Since the spring of 2023 Bios Research has been focused on medtech, commercial biotech, over-hyped AI, and medical supplies and tools. Going into YE23 and 2024 they see several new opportunities for attractive shorts including: 1) $25bn Medical Instruments and Supplies Co. that is up ~50% in the last 12 months but is seeing a decline in revenues (which is expected to continue). 2) $30bn Commercial Biotech with excessive cash burn. 3) $8.5bn Medical Supplies Co. that is grossly overvalued and about to experience deep guidance cuts. 4) $1.5bn Development Biotech in a massively overhyped industry. 5) $1bn Development Biotech that appears on Bios' "Fad, Fake, Fraud" list.

BWS Financial

ARLO's stock has underperformed the fundamentals as investors seem keen on guessing when growth will slow down. The leader in home monitoring IP cameras has maintained its rate of quarterly net subscriber adds throughout 2023 and is poised to cross 3m paid subscribers by the middle of 2024. The introduction of a new security service and lower price camera options should enhance its market share and provide greater ability to generate positive FCF. Management anticipates a record-breaking Q4. Hamed Khorsand continues to believe the stock is being treated more as hardware business than for the recuring service revenue. 12-month TP $17 (85% upside).

Northcoast Research

Recent acquisitions show the two companies increasingly encroaching on one-another - FERG (traditionally stronger in water-related building products) appears to be manoeuvring more aggressively into municipal water works, CNM’s stronghold. Meanwhile, CNM’s push to grow its private label business is increasing its line card overlap with FERG. While such overlap and channel complexity are inevitable by-products of consolidation, Northcoast argues there is ample room for both companies to thrive. In particular, they believe the opportunity remains significant for both firms to deliver structural margin expansion as their leverage with suppliers grows.

Huber Research Partners

Investors are trading the stock as if TRU is in long-term secular decline and / or losing share to a competitor(s). Craig Huber disagrees. He considers the near-term pressure on revenue to be cyclical in nature as the market adjusts to a higher interest rate and weaker macro environment. Meanwhile, management has announced a multi-year transformation effort to reduce costs, accelerate innovation and drive growth. The $120-140m of annual costs savings, and the timing to achieve, fits within the assumptions that Craig had already made. His 2023-2025 EPS estimates are $3.32 / $3.58 / $4.17. TRU continues to be the most mispriced stock he covers.

Valens Research

FIS's three-point turnaround plan begins with selling off Worldpay. As distinct payment processors with different customer bases and needs, their separation aims to reduce operational conflicts. The "Future Forward" initiative is set to cut costs by nearly 10% by 2024's end. Additionally, FIS is strengthening its balance sheet, having paid off billions in debt post-announcement and focusing on reducing debt to pre-merger levels. These strategic moves are designed to reinforce FIS's core competency in serving banks, with potential for significant upside if capital management improves and returns remain steady.

Arete Research

Semis & Hardware: Real-Time Views

Arete’s monthly newsletter covers the latest updates in the global tech hardware and semis markets, with a particular emphasis on foundry, memory, compute, semi-cap, wireless semis, and EV/autos. Highlights from their Nov edition include: 1) Dramatic shift in memory - Q4 price surge signals shift from a buyers’ to a sellers’ market. 2) HBM market dynamics - is AMD diversifying its HBM supplier base with new SK Hynix deal? 3) Why Huawei looks set for a bumper 2024 and US sanctions backfire. 4) Why Apple’s spend at TSMC might be flat in 2024, curbing TSMC recovery. 5) Auto semis - content is king in 2024. 6) Lithium-ion battery outlook - all-time-high earnings amid all-time-low valuations. 7) To infinity and beyond - satellite semis growth in the 2020s.

Japan

Asymmetric Advisors

FP Partner ($730m M/Cap, listed in Sep 22) is growing fast with 9-month operating profit +40% y/y and likely to comfortably beat full year forecasts. PER is 19x 11/24E assuming another +10% y/y growth, though based on the present growth rate, estimates will also need to be guided upwards. As one of the largest insurance sales agencies, FP Partner is benefiting from Japan’s shift from direct insurance product sales by individual insurance companies towards the agency model that dominates in the US.

Azabu Research

Consensus forecasts are divorced from reality - Welcia is so unpopular that analysts expect it to miss its 3-year recurring profit target by 25% and its sales targets by 9%, implying a massive deceleration in outlet expansion and a decline in margins. Mike Allen believes the group’s planning and executions skills are way too good to ever miss by that magnitude, especially given management's major change in policy recently when it comes to cutting costs. Welcia is trading below private-market value (EV/EBITDA has dropped from 18x to 8x). Japan’s drug store market is an active M&A war zone and companies will be bought if they are too cheap.

Emerging Markets

RedTech Advisors

Community Group Buy may have already peaked

RedTech’s latest channel checks show consumers losing interest in buying fresh food from CGB platforms due to quality concerns, even with low prices. CGB was a lifeline for many residents during the lockdowns, but it is not competitive with on-demand delivery from Dingdong and Fresh Hippo or the reliable quality of the local supermarket. RedTech predicted in their Sep 2022 groceries report that CGB would be a transitional model and it seems the transition may come sooner rather than later.

Blue Lotus Research Institute

Downgrades the stock to Sell as BABA backpedals on plans to spin off its cloud business. The malaise today is an aftermath of overexpansion since the group’s IPO in 2014. The resulting conglomerate not only draws ire from the CPC and runs afoul with trustbusters, but also piles up deteriorating assets. So, what needs to occur for Blue Lotus to turn bullish? 1) Taobao / Tmall need capable management to defend against ByteDance, PDD and JD. 2) Needs to resolve its issues with the government on businesses which pose security uncertainties and invite antitrust actions. 3) BABA must be managed by people with high aspiration for success and corresponding incentives.

Copley Fund Research

Fund ownership in the stock continues to fall - average weights slip to 4-year low as managers close out en masse. Between Feb and Oct this year, there were 56 closures (vs. 6 openings), led by growth funds. Ignore the corporate action related declines in Housing Development Finance Corp - the JD.com decline is head and shoulders above all stocks in the EM investible universe over the period. The departure of numerous key investors, paired with the still sizeable base of remaining investors (JD.com is the 16th most widely held stock globally), heightens the risk of an additional sell-off, casting a shadow on any potential share price recovery in the near term.

Sandalwood Advisors

Li Auto, one of Tesla's top EV rivals in China, beat expectations and set a new monthly record with over 40,000 monthly car deliveries in Oct 23. Soon after this new milestone was announced, Li's stock price popped 15%. The China data (Payments & Auto Insurance) from Sandalwood Advisors helped global investors track Li’s deliveries in real-time, and get an early signal on the strong momentum and better-than-expected results. If you never want to miss an inflection point, Sandalwood launched ‘Alpha Seeker’ which alerts clients to all major +/- trends in Sandalwood data.

AlphaMena

ALDAR's development and investment portfolios are growing at a high pace especially with the recent expansion in Egypt, following the acquisition of SODIC. The group reported 21% y/y growth in its 9M 2023 revenue at AED9.763bn and net attributable profit was up 34% y/y to AED2.718bn. Debt is also improving (gearing is expected to be 4.39% on average over 2023-2025 period). Despite the strong performance this year (the share price has risen >30% YTD), ALDAR still offers 8% fundamental potential, mainly supported by the intrinsic methods: +38% for the DCF and +18% for the SOTP.

Macro Research

Developed Markets

Eurointelligence

Eurozone: Will we need the TPI?

Wolfgang Münchau expresses concern about the widening fiscal divergence between Germany on the one side, and Italy and France on the other. He asks whether a situation could arise in which the ECB would trigger the transmission protocol instrument (TPI) in case of an Italian fiscal overshoot. It would not surprise Wolfgang if in the event of a crisis the ECB’s governing council decided by majority vote that the conditions for the trigger of the TPI had been met. Such a crisis isn’t unplausible either, with the country’s ailing real growth rate meaning that even a 3% fiscal deficit target could be a road towards fiscal ruin. The real problem isn’t whether or not the TPI would be triggered, it’s about the potentially massive political impact on European integration.

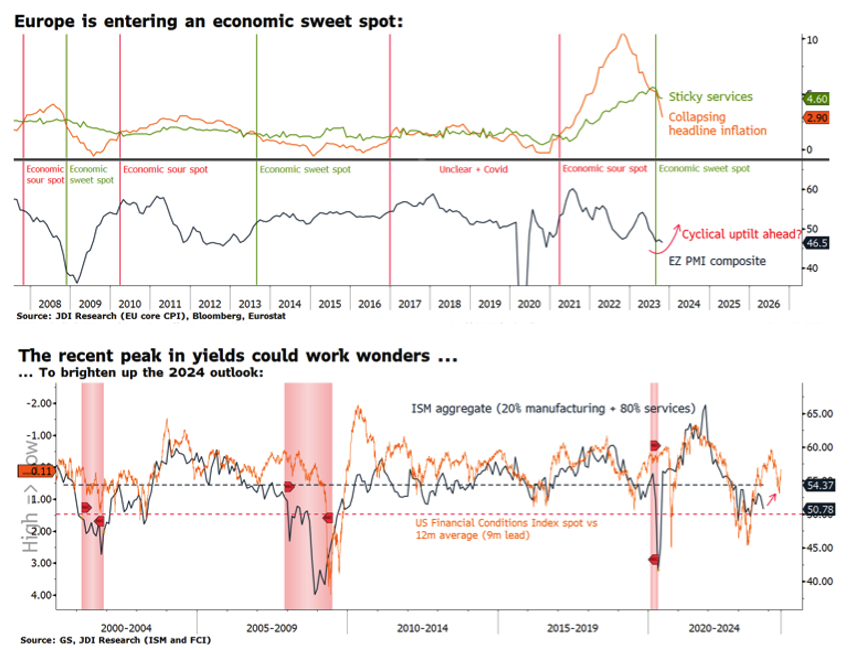

JDI Research

Hit snooze on that hard landing

Alfonso Peccatiello believes there are two main ways to achieve this sought-after outcome: 1) your view is NOT consensus, and you express it through the right asset (no proxy trading); 2) your view IS consensus, but you still pick an undervalued asset to squeeze the remaining juice left. Soft landing is now consensus. If you want to bet against it there are plenty of cheap ways to do that: equity put options are not particularly expensive, and if you think inflation accelerates you can sell bonds pricing in 100+ bps of cuts for next year or buy crude oil which has been slaughtered. If you want a really contrarian way to express the soft landing idea, look at Chinese tech stocks.

The Macro Compass

How do you make money in markets with a directional view?

Alfonso Peccatiellio is of the view there are two main ways to achieve this sought-after outcome: 1) Your view is NOT consensus, and you express it through the right asset (no proxy trading); 2) Your view IS consensus, but you still pick an undervalued asset to squeeze the remaining juice left. Soft landing is now consensus. If you want to bet against it there are plenty of cheap ways to do that: equity put options are not particularly expensive, and if you think inflation accelerates you can sell bonds pricing in 100+ bps of cuts for next year or buy crude oil which has been slaughtered. If you want a really contrarian way to express the soft landing idea, look at Chinese tech stocks.

Hedgeye

US: Colorado court ruling is a mixed bag for Trump

A Colorado state judge ruled that the Fourteenth Amendment disqualification provision does not apply to former presidents, allowing Trump to remain on the Colorado’s primary ballot. However, the findings are ominous, with Trump’s eligibility to hold office now in jeopardy after Judge Wallace determined, as a factual finding, that Trump engaged in insurrection against the Constitution. The case will move quickly to the Colorado Supreme Court, with Judge Wallace’s analysis setting the stage for review of the Trump disqualification issue before the State and US Supreme Court. What we have ahead of us is a monumental, legal battle that will force the US Supreme Court to make the final, absolute call.

Pennock Idea Hub

US: How far can this rally run?

The US equity rally off the bottom in late October is characterised by strong price momentum, resolving itself in a Zweig Breadth Thrust buy signal and four price gaps that likely won’t be filled (see chart). Not only is the price momentum strong, the renewed performance of the price momentum factor also underscores this rally. Ed Pennock suggests a bullish price objective for the S&P500 at 5300.37 and the NASDAQ at 17,152.7. For traders with shorter time horizons, Ed offers a few indicators that can trigger a take profit warning, including keeping an eye on the equity put/call ratio, which at the moment is contrarian bullish but investors should wait for it to fall decisively below its 200dma before taking profits.

Aitken Advisors

Australia: Why isn’t the cash rate moving?

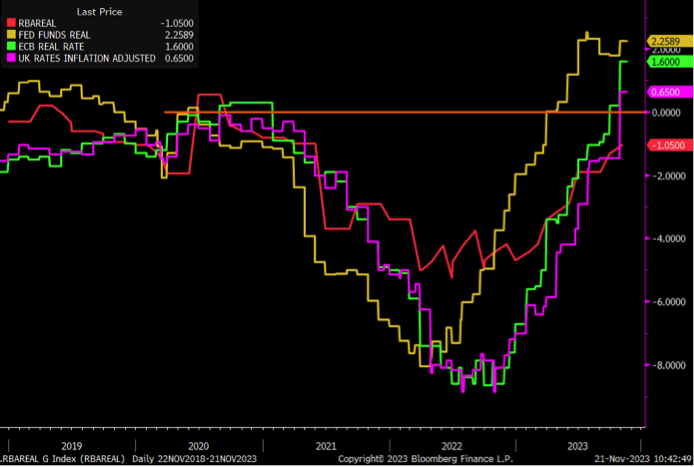

One of these lines is not like the others, says James Aitken. Whereas Fed funds rate is at ~2.25%, ECB depo rate at ~1.6% and BoE bank rate at 65 bp, the real RBA cash rate is still around minus 1. This is amidst a high-pressure economy that is facing a surge in migration, an undersupplied housing market, rising input costs and record super benefits being paid out. Monetary policy is way too loose. The good news is the fairly new RBA Governor Michelle Bullock isn’t mucking around, making her hawkish stance clear. Yet peak RBA cash rates have not moved. It’s quite odd. James has said again and again the RBA cash rate is closer to or even above 5%, and now he says it again but with more conviction than ever.

CrossBorder Capital

Japan: Mrs Watanabe’s threat to world bond markets

Michael Howell argues that Japan’s shifting YCC policy is far from the greatest threat to global bond markets from Asia. A bigger issue is the stability of Japan’s huge household savings pool; the impact of Asian savings has been forgotten but is still meaningful. Currently invested in low yielding deposits, the savings are anchoring low world interest rates, which Michael says may help to explain the tight correlation between the bond term premia across the US, UK, Germany and Japan. However, faster Japanese inflation (already higher than many investors believe) and/or a rapid economic rebound across the Asian economies, could lead to a significant asset shift away from global bonds.

Emerging Markets

Grey Investment

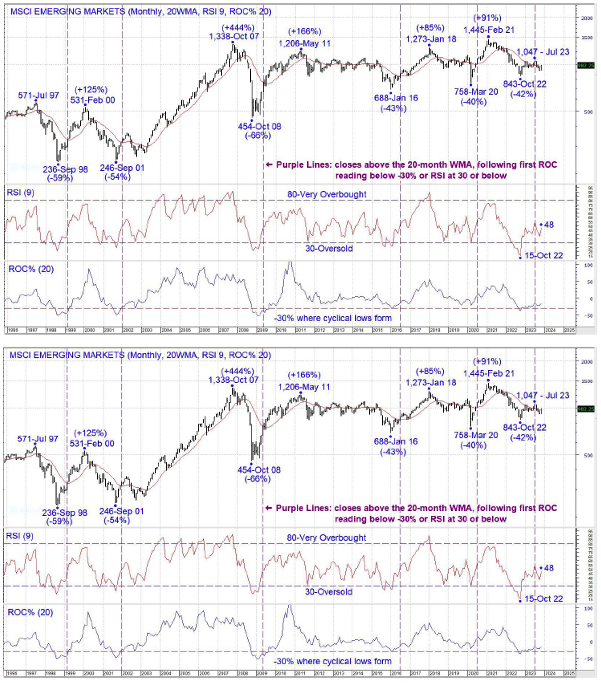

MSCI EM: Time to break free?

Writing about the MSCI EM Index in 2023 feels a bit like a DJ playing a new Earth, Wind and Fire single, but the collective EM is still a thing and looks like it may get more interesting in 2024. The monthly chart shows a peak in October 2007 of 1,338, that is no longer the all-time high but that level marks the beginning of a now 16-year ceiling for the index. On a positive note, the 2008 low of 454 has been followed by a series of rising cyclical lows in 2016, 2020 and 2022. The weekly chart shows an initial 26% rally from the important 2022 low, and the index has now been rangebound for 9 months, forming a potential rectangle. A breakout from the range would signal another cyclical advance, perhaps driven by some improvement in Chinese equities.

Emerging Advisors Group

China: Not out of the woods

Jonathan Anderson points out that consensus has swung firmly to the "green shoots" camp. Most market commentary has the China economy expanding steadily now on a sequential basis, with sustained growth between 4.5% and 5% next year. Underlying data, however, show something very different. When he looks at EAG’s own sequential indicators, they generally show an economy that (i) has been contracting over the past couple of quarters, and (ii) is basically flat today. The main exception is property demand. But it's a very heroic premise to assume that this is directly reflected in GDP. Moreover, Jonathan says there's no sign of meaningful stimulus and neither credit nor fiscal funding figures are moving the needle as of yet. He absolutely does expect more effort in 2024, but this will likely have its main real impact towards the end of next year.

Topdown Charts

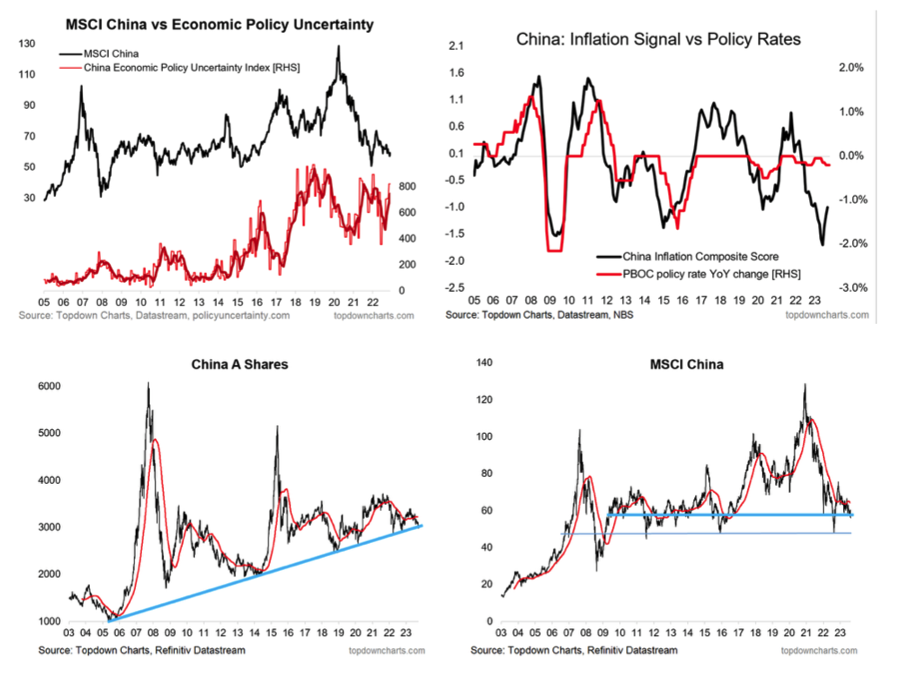

China: Investment opportunity despite policy uncertainty?

Chinese equities are sitting at a precarious point, with macro down drafts, stimulus doubts and the property downturn pushing them down to a key support level. Policy uncertainty is high and policy mistake is a major risk, and the property downturn may result in an inverse goldilocks situation that is the worst of both worlds for equities – a downturn, but not steep enough for stimulus. Yet the valuation backdrop remains supportive, claims Callum Thomas; PE ratios are trading at generally cheap levels and ERP at the top end of the range. He remains cautiously optimistic.

PRC Macro

China: An alternative take on the Xi-Biden tete-a-tete

The consensus takeaway from the Xi-Biden meeting in San Francisco was that the conversation was restorative and put the bilateral relationship on a more stable trajectory. William Hess fundamentally disagrees with this assessment, seeing potential working level re-engagement as papering over a fundamental divergence of respective strategic postures. Xi arrived at the meeting with three key requests, all of which were denied. So why did he turn up? It was to deliver a direct and solemn message about how Beijing interprets the US strategic posture and the potential consequences that will follow, especially on the issue of Taiwan.

Greenmantle

Argentina: A decisive Milei victory

Libertarian maverick is now President-elect, delivering the result Niall Ferguson foresaw and confounding market expectations of a win for Economy Minister Massa. Milei will face an economic mess. In the short-run Niall expects turbulence, including an imminent devaluation of the official exchange rate and a rocky struggle to build a congressional majority. Over the medium run the outlook is more sanguine, particularly if Milei builds a congressional alliance and delays (potentially forever) an asymmetric dollarisation. With the election leading to a more pro-market, open Argentina, investors should re-price Argentinian assets accordingly.

IndiaDataHub

India: Services inflation at current series low

In October, India's headline Consumer Price Index (CPI) inflation eased to 4.9% YoY, declining 15bps from the previous month and marking a 250bps decrease from its peak in July. Notably, core inflation reached its lowest since March 2020 at 4.2%, nearing the RBI's 4% target. Services inflation hit an all-time low at 3.6% YoY, reflecting a benign medium-term inflation trajectory. Despite the overall moderation, a spike in onion prices and subsequent inflation spike in Nov/Dec may delay the RBI’s shift from a hawkish stance. The MPC will wait until this bout of vegetable price inflation plays itself out and signal a change only in Q1/2024, with rate cuts on the way in H1/2024.

Krutham (formerly known as Intellidex)

South Africa: What happens after the election?

There is a significant amount of uncertainty about what will happen post the national and provincial elections. Peter Montalto delves into the key events ahead, which will be important if there is no outright winner. Much of the uncertainty is justified given that there will potentially be modalities for coalitions to consider. Many of these events take place in parliament and include the first National Assembly sitting, election of the president, government formation, coalition formation modalities, passing legislation, removing the president and more. The timeline within which these events must take place is significant as the constitution provides very tight deadlines. In a coalition setting, this may be difficult considering negotiations that have to take place between parties, where Peter believes pre-election day agreements will count for little.

Commodities

Steno Research

Oil: Price always leads narrative

Last week crude oil dropped below USD80, followed by a lot of bearish tones coming from commentators. Andreas Steno doesn’t see reasons for such bearishness with global demand running above projections and TYD having expanded by 2 mbd. Implied gasoline demand shows no weakness yet and the distillate stocks in the US are running well below the 20th percentile. With an implied US gasoline demand of 9.49 mbpd and low stock levels, it can’t be long before we’ll have to see refiners coming into the oil market in size. Go LONG oil. If an outright crude long isn’t your cup of coffee, refiners may be an interesting bet in equity space.

WaveTrack International

Headwinds lessening for precious metals

Precious metals, especially platinum and palladium, completed primary degree and intermediate degree corrections into this month’s lows with sharp upturns since. The USD index has confirmed the end of primary wave 2’s corrective rally that began from last February’s low into the late-October high – a new multi-year downtrend has resumed, and this will remove another headwind for precious metals, in addition to the softening of interest rate expectations. So far, three previous attempts at breaking out of overhead resistance in gold above 2072.00 has failed for good reason – Elliott Wave patterns had correctly anticipated these failures – but the next one is expected to break to new record highs, establishing this uptrend for the next couple of years. Silver will outperform gold, platinum will outperform silver, and palladium will come out on top of them all.

CPM Group

Gold and digital currencies

In this video, CPM Group's Jeffrey Christian debunks the idea that the value of US gold is determined by the Federal Reserve Board. Jeff also debunks the rumour about the New York Fed issuing a "new digital currency." He discusses why that cannot be true, and what the New York Fed actually did.

Click here to watch.