Company & Sector Research

Europe

Willis Welby

Plenty of value on offer in Big Pharma

The sharp fall in the median implied to Y3 EBITM ratio for Willis Welby’s Healthcare coverage is all about Pharma. This leaves a median ratio for the subsector of just 94 which gets you good financial productivity, neutral revisions and a median consensus Y3 revenue growth rate of 7.4%. While the share price of Novo Nordisk discounts a lot of success, at the other end of the scale there are some companies where ratios seem to be getting more cautious without much obvious justification. GSK and Sanofi’s share prices are both consistent with a catastrophic future which makes no sense. Roche is not far behind. Given the normal dislocation of Pharma dynamics from wider economic ones this also looks like a major opportunity from a risk management perspective as well as from a value perspective.

MYST Advisors

Although investors have favoured equipment stocks amid a perceived Industrial & Infrastructure Super Cycle in the US, recent 3Q23 earnings results from companies such as ABB and Rexel suggest otherwise as trends are slowing rapidly, with both orders and construction activity worsening as interest rates rise. Investors do not properly appreciate that renters of AHT’s equipment are primarily small businesses that require financing and working capital from small / regional banks. These loans are typically based on adjustable rates and recent NFIB surveys corroborate that credit is drying up. Ultimately, AHT’s margins will be pressured as utilisation rates suffer. TP £30.00 (40% downside).

the IDEA!

Due to several changes in the regulatory minimum wages in the Netherlands and PNL’s high share of workers around the minimum wage level, the company will be confronted with unprecedented high wage inflation in 2024. The fact that both CLAs are set to expire within the next five months can potentially come on top of this. Whereby PNL’s pay scale structure dampened the effect of wage inflation in FY23, this will no longer be the case going forward. The impact of this, in combination with lower volumes, a deteriorating sales mix in mail and the fact that higher mail tariffs offer insufficient compensation, continues to be significantly underestimated by the market.

Holland Advisors

Mr Market changes his mind by 90% in twelve months - the FY23 net profit figure that RYA earlier this week guided to be €1.85-€2bn was expected to be almost half that level this time last year! The un-forecasted driver of the difference was something Andrew Hollingworth has been writing about at length for some time now. i.e., the firmer pricing that comes from a consolidated market and RYA’s ever-growing unit-cost gap with its peers. This company is on its way to making ROE’s of c.30% for many years to come. Doing so in a business model that arguably has a huge low-unit cost moat around it. If it were to again distribute 70% of its profits annually and keep growing, what PE do you think it deserves? It’s not 10x.

North America

Behind the Numbers

DASH reported 3Q23 results that beat consensus but much of this outperformance can be attributed to low-balling forecasts. Furthermore, BTN questions how much of the gain can be sustained given the size of the cuts to key expenses. Adjusted EBITDA was $74m ahead of the high end of guidance, but to get there the company added back an additional $30m in litigation costs, had a sudden $50m drop in G&A costs, a large decrease in advertising, and it appears that employee pay increases have stalled and R&D is flat-to-down. These boosts to EBITDA filter down to earnings. In addition, earnings benefitted from interest income rising by $31m.

Huber Research Partners

3Q23 a seminal quarter? When one considers that: a) the general ad market backdrop is sloppy; b) the news cycle was quiet in Q3; c) NYT remains in an investment / growth mode - results were strong across the board. Net digital adds accelerated. Advertising was stronger than expected buoyed by a surprisingly strong contribution from The Athletic and positive print advertising. Total company revenues accelerated to 9.3% growth vs. 6.3% in 2Q23. Costs were as expected; consequently adj. EBITDA increased a better than expected 30.2%. As an added bonus, net cash has continued to build. Doug Arthur raises his adj. EPS estimates for 2023E and 2024E to $1.40 and $1.62, respectively.

Housing Research Center

A Homebuilder Santa Rally: Will it work again now that the Fed is essentially done?

For investors who trade the builders, this has been a particularly profitable trade - over the past 36 years it has worked 72% of the time (measured from Dec 1st to Jan 31st) and the average rally has been 16%. Over a 3-month period (starting from Nov 1st), the results are even more impressive (75% success and an average gain of 20.5%). Alex Barron sees a compelling opportunity this year as well. The housing market is not as sensitive as investors fear to interest rates. Balance sheets have never been stronger. Public builders are gaining market share more rapidly than ever before. Valuations have not been this low without imminent warning signs. Looking at the current values of builders vs. Alex's mid-price targets, the group offers on average 54% upside over the next 12 months.

Arete Research

GLBE benefits from the ongoing shift to e-commerce, in which brands are accelerating the search for incremental growth in international markets. Arete sees the business at an inflection point with the Sept launch of Shopify Markets Pro; this gives it access to $14bn of SMB cross-border GMV on SHOP. They model GMV growing 5x by 2027. GLBE also benefits from having its two leading partners (SHOP and DHL) as 13% shareholders and has limited competition for its “merchant of record” solution. Arete initiates coverage with a Buy rating and a TP of $58 (55% upside), based on a 9x EV/Sales multiple on 2025 sales of $1.2bn.

CTFN

On 17th Oct Choice Hotels went public with an unsolicited offer for competitor WH. The nearly $10bn enterprise value strategic deal would be one of the largest of the year. However, WH has pushed back on the approach and CHH is now preparing a proxy fight and possibly an exchange offer to land its prey. Exclusive reporting from CTFN has covered the antitrust dimensions of the deal, the tactics likely to be employed and pricing insights. Click here for the full story.

Quo Vadis Capital

What really jumps out here is the disconnect between results, guidance and how analysts are modelling the company. 1) Consensus EPS for 2024 is $2.78, below revised guidance for 2023 of $2.77-$2.81. 2) The Street is modelling EBIT margins down every year going forward. 3) Analysts are modelling ~2% annual comps going forward despite the benefit of more immature stores entering the base and compared to the 3.9% comp produced in 3Q23 on top of a 2.4% increase last year. John Zolidis wonders if analysts have any credibility here. SFM has beaten estimates for 17 consecutive quarters, the stock is up over 30% YTD and zero analysts are recommending it.

Veritas Investment Research

The attractiveness of asymmetry - extreme price volatility often makes this aircraft manufacturer's shares a challenge to hold. Since the start of its turnaround journey 3+ years ago, its stock has appreciated by >350%. Along the way, however, the stock has suffered multiple significant drawdowns. Management has made significant progress in addressing liquidity, reducing leverage, improving its cost structure, operational efficiency and cash generation. Analysts at Veritas see the stock offering gains of between 125% and 220% vs. downside of ~25%. This equates to an upside-to-downside ratio of 5:1 to 9:1, which is an appealing trade-off.

Northcoast Research

It has been a tough 2H23 for GNRC investors. However, there is light at the end of the tunnel as Residential sales benefit from the return of HSB normalised shipments in 2024, success within ecobee, and expansion of the beyond standby product set within C&I that will offset cyclical weakness from equipment rental and telecom customers. The late 2024 rollout of new clean energy products is a free call option on the shares at these levels. Northcoast’s TP of $144 (40% upside) places an 18.5 multiple on their FY24 EPS estimate of $7.78.

Radio Free Mobile

Artificial Intelligence: Lifecycle of a bubble

As more and more models are released by companies, start-ups and open source, the harder they will have to work to attract users, resulting in falling prices. The current mantra (and what companies seem to be raising money on) is that $20 per user/month is the benchmark and at this price, a lot of money will be made. However, Richard Windsor suspects the real price will be no more than $20 per user/year. This means that in 12 months when these new companies need to raise more money, they will have badly missed their targets and the long-term outlook will be lower. This is what pricks the valuation bubble and causes expectations and valuations to reset to reality.

Sales Pulse Research

Sales Pulse's latest channel checks suggests there could be problems with FTNT’s North American sales culture. In early Oct, they reported how the cybersecurity group had pushed out several underperforming salespeople. They are now picking up examples of salespeople, who have been historically successful over a 5+ year period, that are leaving due to increased quotas, reduced territories, etc. This does not bode well since these are the same reps that need to be trained / motivated to focus on management’s new plans to concentrate on the SASE and security operations segments as growth slows in the network security market.

Australia

Rimor Equity Research

Despite WOR's transformational purchase of Jacobs ECR, the share price remains at a similar level to where it was 5-years ago, having underperformed the Australian market by ~20%. Since their initial take on the acquisition, Rimor has published a number of detailed reports on sustainability themes and energy transition with input from industry contacts. In this 58-page report, they highlight the likely extended duration of this up-cycle and WOR’s leverage to investment requirements across a range of end-markets that they expect to become clear in the next 12-18 months. Rimor also believes the importance of the Jacobs acquisition to WOR will become clearer - both in bringing capability and earnings diversity. Opportunities for margin and cashflow improvements are also identified.

Japan

New Street Research

Huge beat as ARPU inflects - KDDI reported a very strong set of Q2 figures with both KPIs and headline numbers inflecting / strong across all business lines. While these numbers can be volatile and Q1 was weaker, net profit growth was 18%, 11% ahead of consensus. New Street continues to argue that Japanese Telcos have entered a Golden Age. KDDI is in a clear uptrend; investors who do not have exposure are missing a strong story. KDDI remains their top pick with a TP of ¥6,500 (+30% upside).

Galliano's Financials Research

YCC relaxation adds fuel to the Japanese banks re-rating

The latest BoJ adjustment to its yield curve control lifts the hard yield ceiling of 1% on 10-year JGBs, making it “a reference” and allowing yields to exceed it. 10-year JGB yields are close to 1%, with Japanese bond yields steepening further which is positive for Japanese banks, especially those with a high share of floating rate credit exposures. In Aug, Victor Galliano identified Resona, Mizuho and SMFG as his picks for a steepening yield curve. In Oct, he added Hachijuni as the deep value buy. Now, he adds Concordia for its high share of floating rate lending.

Emerging Markets

AlphaMena

Most of the GCC equity markets have fallen for the third straight month as the Israel-Gaza war rages on. Almarai, the Gulf’s largest dairy company, is no exception, having seen its share price drop ~20% since the end of Jul. However, this poor performance should not arouse doubts about its solid fundamentals. Almarai recorded a 19.5% y/y increase in its 9M net profits after Zakat and tax to SAR1.678bn with revenues up 5.6% to SAR14.656bn. AlphaMena points to the resilience of the group’s business model thanks to its strong brand image, portfolio optimisation and growing demand. They expect a 6.49% CAGR of revenues and an EBITDA margin average of 29.3% (2023-2025).

India Independent Insight

Whirlpool (WHIRL IN), Aditya Vision (AVL IN), Electronics Mart India (EMIL IN), Eureka Forbes (EUREKAFO IN)

Iii’s Bharat Connect Flash report provides insights, anecdotes and narratives that they pick up as part of their regular on the ground checks and that could potentially emerge as more significant trends or issues, warranting deeper attention. Highlights from their latest note which focuses on consumer durables include: 1) WHIRL’s offline sales are slowing down due to lack of price parity with online sales, lack of company support and flat consumer sentiment. 2) AVL’s competitive advantage is uncertain, with some stores emphasising lower prices and others focusing on service. 3) EMIL differentiates through a better shopping experience and pricing is not a major issue for growth. 4) EUREKAFO hasn't seen a change in the total cost of ownership (TCO).

Smart Insider

Chi Dung Ngo (Chair since 2010) splashes out more than US$55m as he purchases 70m shares in VPB. This is Ngo's fourth reported acquisition, by far his largest and the highest price he has paid. His most recent buy was five years ago in Dec 2018 when he spent US$18.3m below VND 10,000 per share. This is a confident purchase from the Chair, paying roughly twice the price of his prior purchase. Stock Rank +1 (highest rating).

Macro Research

Developed Markets

CrossBorder Capital

Why the USD is strong and why it could get even stronger

Michael Howell argues that the US Dollar is being pushed higher by rebounding US private sector cash inflows alongside the tight control of new liquidity supplies by the Fed. Positive US private sector cash flows, in turn, are partly explained by the persistent stream of foreign capital into US dollar assets, but largely by the Biden Administration’s remarkably loose fiscal policy. A strong dollar is not a consensus trade. However, it could prove self-correcting if the resulting disinflationary pressures compel the US Fed to ease monetary policy in 2024, which could help to underpin markets. Despite the widespread assertion that the US dollar system is threatened, the paradox of a potentially stronger US currency needs to be watched.

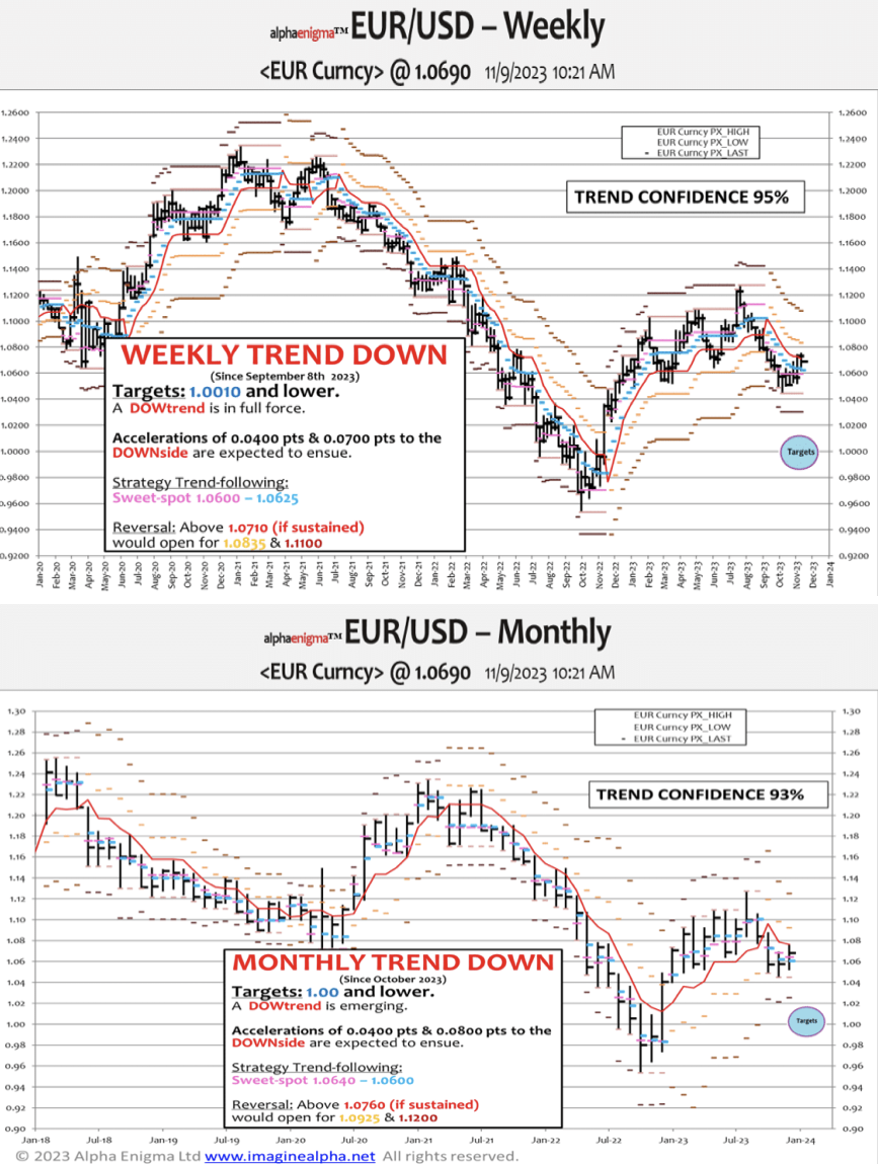

ImagineAlpha

EUR/USD 1.070/60 will resist further favouring 1.00 better than 1.12

The “triple alpha” downtrend was downgraded on October 24th as EUR/USD staged a rally toward 1.0750. That level is very significant as it is a combination of the weekly and monthly timeframes overhead resistance between 1.070 and 1.0760. There is no upside potential for the EUR short of a thrust through that area, explaining the range bound price action that has unfolded recently. In the weekly outlook for the coming 4-13 weeks (chart 1), the timeframe is favouring the downside. In fact, the 1.0700 area is an ideal entry point for intra-quarter traders/hedgers. More work needs to be done for a full reversal. Over the next 3-12 months (chart 2), the overcast resistance is strong (to put it mildly) and 1.00 remains more likely than 1.12 for the time being.

Grey Investment

Portugal: Europe’s Japan

Following a 77.5% decline in 22 years, Portugal now has a positive equity story. The Euronext Lisbon PSI is on the verge of breaking out from a 17-month Ascending Triangle, following a shallow retracement of the 2020-22 bull market (chart 1). A weakly close above 6,560 would be viewed as a breakout, targeting 7,900, after which the Grey Investment team would likely recommend a BUY. Looking at chart 2, the secular bear market is over and the weekly chart breakout would take the index clear of key monthly resistance around 5,800. A long secular decline destroys an equity culture among local investors, but there will be plenty of young investors who will not have the bad memories that come with prolonged market losses.

Quill Intelligence

US: Macro headwinds from trade, inventories and customers

Trade volumes have been supported by the auto sector’s extraordinary run. With the auto runway running out, however, non-auto trade volume and paltry inventory breadth speak to further downgrade risk to near-term US growth prospects. Non-autos fell -3.6% and -3.5% in Q2 and Q3, reversing the typical recession pattern of autos falling first and highlighting the magnitude of the chip shortage-induced catchup. Not to be left out, consumers’ nervousness is rising as they contend with higher delinquencies across the consumer debt spectrum. Rising auto delinquencies in particular point to continued implosion of the used vehicle bubble which will push core consumer goods prices into deflation.

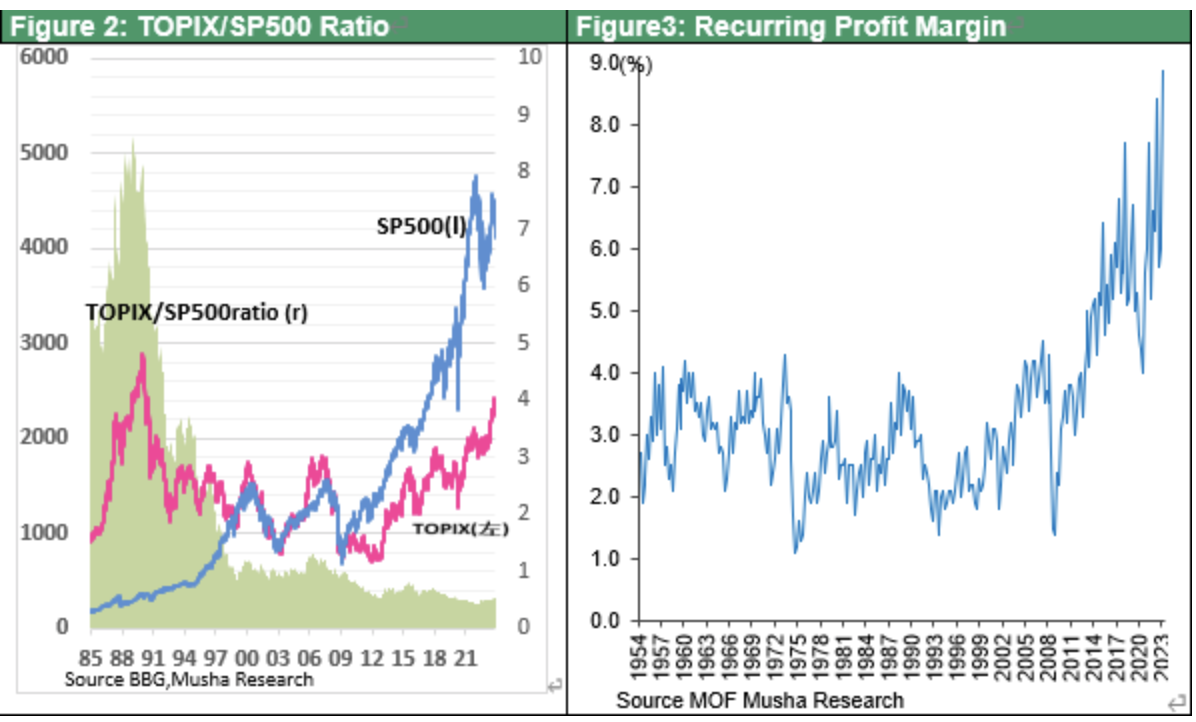

Musha Research

Japan: Land of the rising sun

Japan may be the brightest of major economies in both politics and the economy, according to Ryoji Musha. Even though Kishida administration’s approval rating has fallen, its base of power is solid. The economy’s robust performance stands out amidst the downward revisions in China and the Eurozone. Investors around the world have developed an attitude of neglect for Japan over the last 30 years, that is until recently; the chart shows the multiple of TOPIX vs the S&P500, which has seen a recent and rapid increase to 0.54x. Ryoji points to the transformation stemming from evolving attitudes in initiative-taking and major changes in the geopolitical environment. Japan’s time has come.

Harlyn Research

An underweight in Industrials is rare and often spells trouble

Simon Goodfellow has downgraded the Industrials sector in four regions this week – to neutral in the UK and Pan Europe and to underweight in the Eurozone and Japan. In the last four weeks, it has lost ground in every region. In the 28-year history of Simon’s models, the Industrials sector has had the lowest number of underweight recommendations out of all eleven sectors (incl. Small Caps) and this is normally an indicator that investors are concerned about the onset of a recession. Small Caps have also seen a big reduction in their recommended weight over the same period, which reinforces these fears.

Emerging Markets

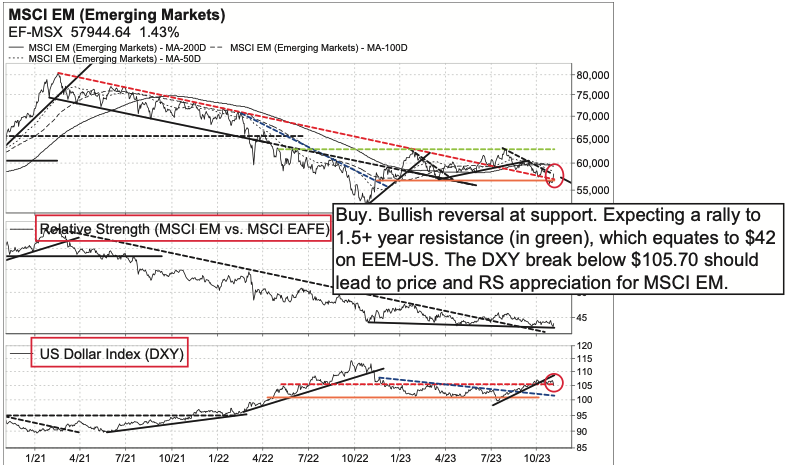

Vermilion Research

MSCI EM Index reversing 3-month downtrend

In Vermillion’s prior EM Strategy, Ross LaDuke discussed that MSCI EM (EEM-US) was again approaching major 10.5-month support at $37-$37.50, which has been their important line-in-the-sand throughout 2023, and that as long as EEM-US is above $37, Vermillion are buyers on this pullback. This support level held and EEM-US now displays a bullish 3-month downtrend reversal as the US dollar (DXY) appears to be breaking below $105.70 – all rather bullish signals suggesting this rally is just getting going -- BUY. Ross is bullish as long as $36.50-$37 support holds on EEM-US. His first target is $42, which is 1.5+ year resistance. Additionally, he remains neutral on EM vs. EAFE; the EAFE vs. EM ratio is moving sideways following the 2.5-year downtrend reversal.

Primaresearch

Through the lens of demographics

Shamil Ismail discusses how demographic shifts could impact investment performance through weakening demand and higher wage costs. He forecasts the number of countries with severe labour shortages to increase dramatically after 2040, so it is imperative for investors to assess the demographic risk to companies and investments. In his latest report he outlines multiple examples, including in the case of Tencent which could see the target market of its games division in China fall by 18.1% by 2030. He also examines the Chinese real estate crisis through the lens of demographics, with the rapid construction of new homes continuing despite the decline in the young adult population, contributing to c.60m incomplete or abandoned apartment units. With the population of the 25-44 years age group set to decline 35% by 2030, the crisis could be protracted.

Greenmantle

China: Policy pivot

Although little has been revealed about the country’s future macro policy direction, Niall Ferguson has detected the beginning of a change in the regime’s economic policy. Over the next few months, he expects more bullish news to come out of China as Beijing focuses on doing more to support the economy, primarily through continued monetary easing and fixed asset investment (FAI) funding. Meanwhile, an apparent relaxation in U.S.-Chinese tensions - culminating in a likely meeting between Xi Jinping and Joe Biden in San Francisco in less than a fortnight - will please Western investors who are not yet reconciled to decoupling. Even as the likelihood of greater policy support has made Niall more optimistic about Chinese assets over the next coming months, he remains bearish about the long-term fundamentals.

Antipodean Capital Management

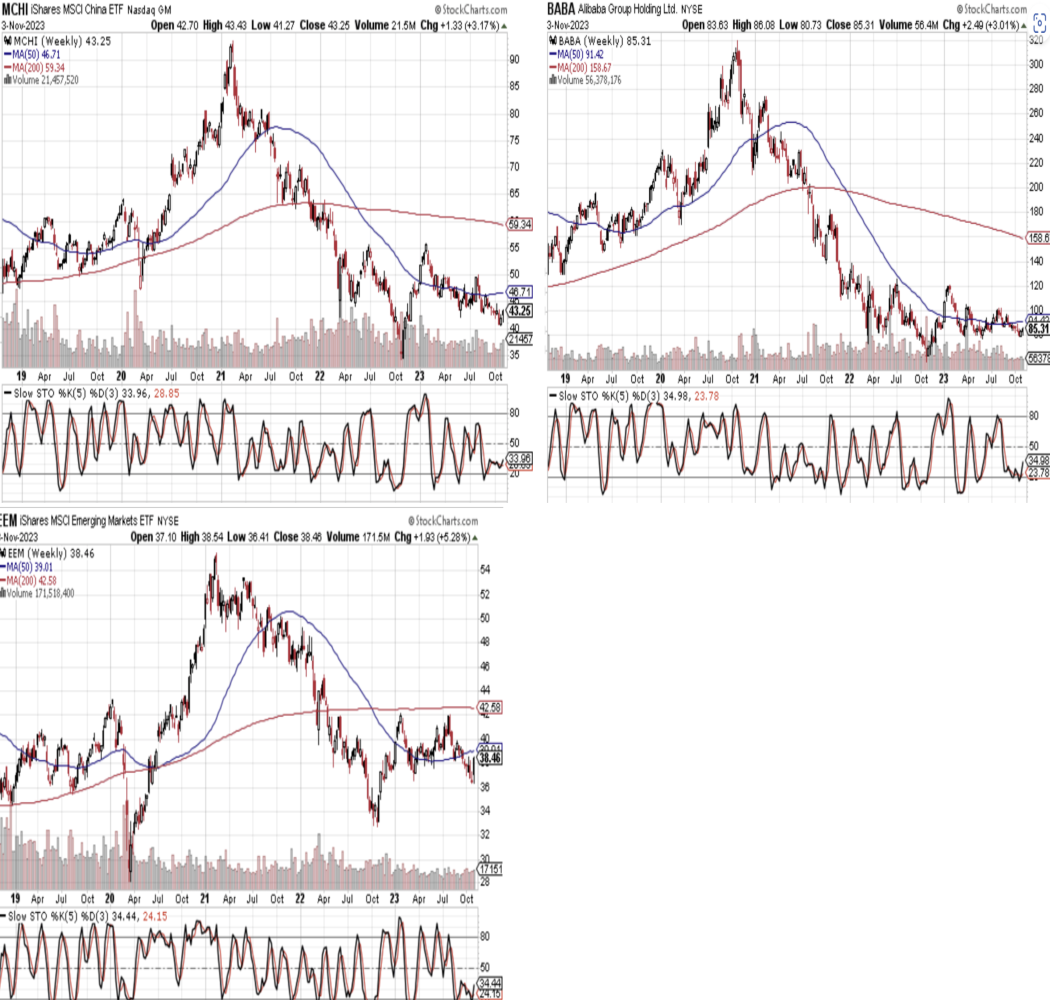

China: Soon to win

Craig Ferguson has recently been advocating LONG EM and China equities, in particular over US equities. The reasons are numerous: monetary policy is easing in China and tightening in the US; fiscal policy is easing hugely in the former; equity valuations in the US are historically extreme at 19x whereas in China they’re exceptionally low at 10x. If Craig is right about global/US yields and the USD cycles peaking, this should be most expansive for EM and China. Craig points to three graphs that outline his view of Chinese outperformance. Chart 1 indicates a head and shoulders reversal base pattern for the broad MCHI China ETF, with expectations of the January 55 high being retested. Similarly, China’s largest firm (chart 2) is basing and may see a rise back to its January high at 120 with a minimum 50% rally. EM gains will come but will be relatively modest, towards 42-46 (chart 3).

Bondcritic

China: Defaults en route

Warut Promboon is of the opinion that the Chinese regulators are usually reactive rather than proactive, but in the face of Country Garden Holding defaulting on its USD bonds, he believes the government will be looking to rescue more developers. Warut sees no sign of recovery in the property market, a worsening credit crisis before the situation improves and limited refinancing prospects that should deter many international investors from China. The domino effect, starting with Evergrande, is continuing and more defaults will be inevitable. The sector is not investable for the general public and only distressed specialists should endeavor any investments in high-yield property developers. He maintains his underweight recommendation on the COGARD complex despite the attractive offers of c.5 cents on the dollar.

Emerging Advisors Group

Egypt without tourists?

Two big pieces of news have come out since September: the further improvement in Egypt’s current account position, and the Israel-Hamas war. Jonathan Anderson believes the best combined outcome of these two factors is to leave the country where he saw it two months ago: heading for inevitable further currency shake-out and eventual sovereign default, with IMF discussions affecting the timing but not the outcome. If things escalate further on the geopolitical front, the downside risk is an acceleration of both FX and default pressures. Jonathan doesn’t see value in local assets and is not inclined to chase what is still in the best case a tactical trade on Egyptian dollar spreads.

Krutham (formerly known as Intellidex)

South Africa: Metro drama

Recent developments indicating an impending termination of the relationship between the ANC and the EFF in municipalities they govern together have reignited an interest in the (in)stability of metros. In addition, the DA is preparing to table a motion to dissolve the City of Johannesburg council. Generally, metros have enjoyed a period of political stability in recent months, despite isolated events which have threatened the incumbency of some leaders. Removing the EFF, however, will leave four major metros in the lurch – though the ANC seems to think the impending dysfunction outweighs the risk of being associated with the EFF (a risky gamble). While attention is presently shifting towards metros as they get caught up in 2024 electioneering, Peter Montalto expects attention to shift away from them once parties start publishing their manifestos.

ESG

Sustainable Market Strategies

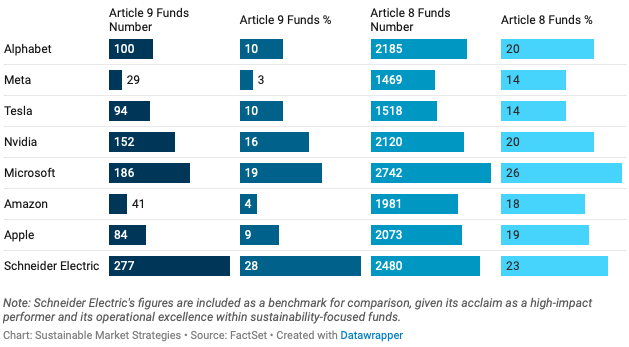

The Magnificent Seven

The impressive growth trajectory of the Mag 7 has been fuelled by AI and cloud computing, as money continues to chase their share prices higher despite pressure from rising bond yields on tech stocks’ long duration and their steep valuations compared to equity benchmarks. As pioneers in innovation, they are increasingly encountering legal challenges, but this has been intensifying as of late. The giants have a noteworthy presence in sustainable investment funds (see chart). However, the Sustainable Market Strategies team see the broad inclusion of these stocks as somewhat dubious. They tout Nvidia and Microsoft as the leaders, although the former is trading on a lot of AI hype and will fall short of growth expectations. Meanwhile, Amazon and Meta should be avoided as long positions in a sustainable strategy.

Commodities

Vanda Insights

Oil: The pendulum continues to swing

Economic sentiment with respect to the US remains fickle, the pendulum swinging between sanguine optimism and recession fears. Vandana Hari notes the impact on crude of the changes, with Brent and WTI being yanked up from 1-month and 3-month lows after Chairman Powell’s recent comments. Tensions in the Middle East continue to run high around the Israel-Hamas conflict and crude will maintain some fear premium as long as it drags on. Should there be an actual supply disruption, crude could well surge into the triple digits, but that is not Vandana’s base case scenario. The 3m b/d of OPEC/non-OPEC output cuts are set to run into the year-end and hold a floor under crude. Vandana is NEUTRAL sentiment for the near-term (to mid-Nov) and mildly BEARISH for H2 Nov – H1 Dec.

J Ganes Consulting

Cotton: Price drop spurred some buying

With the cotton market slipping, buyers stepped up to purchase US cotton. The purchases corresponded with what is normally a seasonal dip in price, suggesting that buyers believe the market is in a bottoming process. While it is encouraging to see a blip up in export sales, the cumulative total for this season remains well below year-ago levels. Consider also that the USDA is expecting global demand to see a sharp gain year over year, this suggests the US is losing market share and isn’t competing well in the global arena. While the market was able to rally from the recent lows on the seemingly positive data, it backed off the initial, more bullish response to export sales. It’s going to be a challenge for the US to compete against Brazil.

Northcoast Research

Titanium: Bubble? What inventory bubble?

The Northcoast Research team are raising their titanium industry demand assumptions to account for a stronger-than-expected commercial aerospace backdrop, rapid inventory depletion and the cell phone redesign contribution. Companies focused on upstream production appear to be well-positioned to realise double-digit unit volume growth over the next year three years. Titanium pricing may have cooled in recent months, but the weakness has been attributed to normal mid-cycle correction factors and will only be a temporary adjustment. This supports the relatively bullish outlooks provided by the likes of BUY-rated ATI Inc..