Company & Sector Research

Europe

ResearchGreece

The Greek bank announces an agreement with UniCredit a) to merge their Romanian operations, with ALPHA keeping a 10% stake in the combined entity while pocketing €300m; b) the two sides entering a commercial partnership in asset management and unit linked products, with UCG buying 51% in AlphaLife Insurance; and c) with the Italian bank submitting a bid to buy HFSF’s 9% stake in ALPHA. ResearchGreece considers this to be a win:win for both sides and with the overhang lifted, they upgrade ALPHA to Buy with a TP of €1.84; sees limited downside to current trading of 0.47x TBV.

Alumbra Research

The share price plummets nearly 75% after forecasts are slashed. Earlier this year, Alumbra Research had published a report highlighting numerous red flags in CABP's IPO prospectus. Most notably, they found the timing of its IPO to be highly questionable given 1) 26% of FY22 revenue and up to 51% of EBITDA would likely dissipate very soon due to changes in Nigeria’s currency policy and 2) CABP did not present a credible plan on how it was going to replace this lost revenue / EBITDA. Furthermore, CABP’s growth leading up to the IPO had benefitted significantly from volatility in other African currency corridors, which they believed was unsustainable. Other recent successful shorts from Alumbra include Alstom, Cerence and Doximity.

MYST Advisors

The stock is too cheap to ignore - ENX is the least expensive global exchange trading at ~9.4x EBITDA / ~11.5x EPS. Multi-year growth path with improving fundamentals. Well-positioned to “beat & raise” in a difficult environment. Buying back ~5% of ADV over the next 12 months. Upcoming clearing migrations to accelerate organic growth. Potential for highly accretive M&A within 2 years (i.e., Nasdaq Nordics, BME Spanish Exchange, Euroclear). Asymmetric risk:reward with ~35% upside to €90/share TP (~15x FY24 EPS of €6.00).

the IDEA!

Results were well ahead of market consensus. Furthermore, the sales mix was strong / contained a high contribution from China which resulted in an adjusted gross margin of 48.9% (at the high end of its mid-term guidance range of 46-50%). Order intake was outstanding, especially when accounting for the generally weaker market conditions. This year investments will be at an elevated level (€150-200m) and absorb a large chunk from the net cash from operating activities. However, in the years ahead FCF should accelerate based upon growing revenues, improving profitability and lower capex (€100-180m). Given ASM’s modest valuation and growth potential the IDEA! remains bullish.

Forensic Alpha

While the weak end environment was immediately priced in by the market (the share price fell 18% following the release of Q3 results), Forensic Alpha is more concerned about the fact that absolute inventory has continued to rise (from $148m at the end of Q2 to $158m at the end of Q3) even though revenues are declining. To put this in context, the cost of materials in Q3 was $67m, so this works out at over 7 months of production sitting on the balance sheet as inventory. Management painting this a strategic decision comes across as disingenuous, especially considering their guidance for a sequential revenue decline in Q4 and "limited visibility beyond the current quarter".

North America

280First

10Q / 10K filings analysis

Utilising AI, NLP, data analytics and qualitative analyst oversight, 280First can rapidly glean material / actionable insights from a company's financial reports. Recent alerts include:

Guidewire Software (GWRE) - Contract modifications and customer in-sourcing concerns.

Thor Industries (THO) - Takeover target? More benign competition. Acquisitions outside RV business.

United Natural Foods (UNFI) - Customer retention concerns. Increased margin pressure. Activist shareholders. Less acquisitive.

Walgreens Boots Alliance (WBA) - Dividends at risk. Business model changes. Strategic opportunities.

Hedgeye

Andrew Freedman describes GOOGL's latest results as a classic case of good, but not good enough with expectations high going into the print. While the stock sold off, he does not see consensus numbers going lower for 4Q23 or 2024 off this report (if anything a touch higher). Assuming the Middle East conflict doesn’t escalate, Andrew’s base case continues to be for the ad business to accelerate to 13-15% growth in Q4 (vs. 10-11% consensus). He still sees $7.00-7.50 in EPS in 2024 * 23x (2018/19 average) = $161-173 stock… while downside is $6.50 * 18x = $117 (and that is pushing it). So, with the stock trading at $125, you have less than $10 downside and $40 upside in the next 6-9 months.

Cmind

Cmind predicts that ABNB is very likely to beat its 3Q23 earnings, scheduled to release on 1st Nov. Per their latest prediction, the probability of beating the consensus is 0.91. ABNB exceeds its competitors in high Cash/Operating Profit, EBT/Sales, Gross Profit/Total Assets, Gross Margin change, and Current Assets/Capitalised Expenses; and in low Inventories/Current Assets. In linguistic analysis, ABNB's CEO/CFO have been more positive and bullish on the company’s outlook and less evasive in addressing analysts’ questions.

R5 Capital

The return of Todd Vasos as CEO will not magically make all DG’s problems go away and the Walmart threat is likely to become more of an issue as WMT moves to use its productivity savings from automation / workflow initiatives to lower prices. Walmart+ is also a growing headwind as it makes the service available to more rural communities and discounts the price for lower income households. As of now, R5 has DG’s EBIT margin in the low 5% range over the next few years, yielding mid $6’s in EPS, but this could be optimistic depending on the competitive climate. Assuming a 15 PE multiple, there remains plenty of equity downside.

Singular Research

A hidden gem for investors - ELF’s strategic agility, quick product development and ability to bring prestige-like products to the mass market at an affordable price, positions the group for continued success in the ever-evolving cosmetics industry. Its commitment to staying in touch with consumer preferences and trends, embracing new platforms like TikTok and exploring opportunities in gaming, AI and data analytics further reinforces their low-risk, high-reward innovation strategy. Singular Research initiates coverage with a Buy rating with potential upside of ~40% and a manageable downside risk of 10%.

Boyar Research

GEHC boasts an extremely strong competitive position, including its large install base, proven track record of new product introductions, service capabilities, supply chain and regulatory infrastructure, and IP. 50% of GEHC's revenues are recurring, coupled with minimal capital intensity, provides meaningful cash flow visibility. The healthcare industry in which the company operates currently has a TAM of $84bn, a figure projected to increase to $100bn by 2025. Expanding into adjacencies could increase this number by another $50bn in the coming years. The share overhang associated with General Electric’s retained stake in GEHC should soon be alleviated. TP $95 (45% upside).

Off Wall Street

Another disappointing quarter for ISRG with more of the same - a greater mix of operating leases weighing on Systems revenue, competition pressuring ASPs and GLP-1s clouding the outlook for bariatric procedure growth. While management claims it has not yet seen competitive pricing pressures outside of China, OWS thinks China is the canary in the coal mine. Moreover, it is not a question of whether new systems are “better” than Da Vinci, but rather are they “good enough” and cheaper. As OWS detailed in their initiation report, even share loss of just 5-10% in the next five years would have very significant negative impacts on ISRG’s shipment and procedure growth.

Paragon Intel

John Dietrich is an unconventional pick for CFO because he has never overseen a finance function before, but his pre-existing relationships with the FDX team, general industry knowledge and overall strong execution inspired them to bring him into the C-suite. He is charismatic, humble and approachable, and creates loyalty among those on his team. Dietrich will capably guide the ship through choppy waters as FDX struggles against a shift from a goods economy to a service economy and a post-pandemic e-commerce reset. His primary focus will be on efficiency / cost-cutting and he will lean heavily on his prior experience negotiating with the pilots’ union to extract a favourable deal.

Northcoast Research

Marijuana legalisation - higher accident rates ahead?

With multiple states potentially voting on legality over the next 12 months, Northcoast's analysis points to a material boost in accident rates and collision volumes. Key takeaways include: 1) States in the year of legalisation and the year after legalising either recreational or medicinal marijuana saw average y/y increases in accidents of 3.4% and 4.3%, respectively. 2) In recent years, states which permit recreational use saw higher accident trends compared to the national average of -2.3%. 3) 92% of states with legal recreational use saw positive y/y growth in accident frequency in the year following legalisation vs. the prior year.

Verbatim Advisory Group

According to Verbatim’s latest channel checks, 1Q24 sales trends are significantly stronger on a y/y basis. This strength stems from Cloud migration, ESM projects and Jira Work Management, while larger deal sizes are driving q/q trends. The 2Q24 outlook for TEAM is also stronger on both a y/y and q/q basis. Close rate continues to remain steady according to 100% of their respondents and the flow of new leads is mostly increasing. Also noteworthy, ServiceNow is losing market share to TEAM, but price increases are leading to competition from emerging vendors such as Monday.

Cerundolo Investment Research

Short setup in the Semiconductor ETF (SOXX)

Japan

JapanConsuming

Keeping track of Japan's Retail & Consumer markets

Key stories in this month's issue of JapanConsuming include: 1) Low cost apparel sales keep rising - Shimamura is adapting well despite the competition from platforms like Shein and Temu. 2) Zozo claims the global market for virtual clothes is growing rapidly - and prices suggest it’s probably correct. 3) The next big thing? Seven & I targets first SIP store by Feb. 4) Itochu (and Mizujin) have big plans for Eddie Bauer’s relaunch - hopes to create a major new lifestyle chain for 30s and 40s consumers. 5) Aeon’s new online food store, Green Beans, aims to change shopping habits. 6) Solving the 2024 logistics problem - companies are working hard to come up with solutions to reduce the impact of the new rules re. truck driver working hours.

Emerging Markets

RedTech Advisors

What started out as a promising year for BILI is decidedly less so as we move through 4Q23. Gaming has been stymied following the botched launch of Pretty Derby, its marquee title for 2023, and the recovery in advertising is not strong enough to offset the missing revenue. There is no question that trimming opex and COGS is important for the path to profitability, but a rebound driven by cost-cutting does not generate the same giddy excitement among investors that one gets from new products, new customers and reinvigorating the top line. There is a path to success, but it is narrow and RedTech remains sceptical.

Copley Fund Research

EM Fund ownership surges to highest levels on record - of the 371 funds in Copley’s analysis, 53 increased weights in the oil giant and 10 opened new exposure in the last 6 months. ARAMCO has overtaken both China Petroleum & Chemical and PetroChina in recent months to move to the 5th most widely held stock in the sector. In Saudi Arabia, ARAMCO has overtaken both Al Rajhi Bank and Saudi National Bank over the course of 2023 to become the most widely held stock in the country; no other company has more funds positioned overweight. A stock once shunned by EM managers is seeing a definitive change in sentiment.

AlphaMena

FAB reported significant net profit growth in 9M 2023 (+58% y/y underlying) to AED 12.4bn. Strong investment and corporate & commercial banking businesses (68% of total revenues and 82% of net profit) are the main drivers of FAB’s performance. The bank maintains a strong capital position with RoTE of 18.3% and CET1 at 14.2%, leading to a significant potential for AlphaMena’s intrinsic methods (+48% for the NAV and 52% for the intrinsic value). They expect slower revenue growth pace over 2024-2025 due to stable rates but with no impact on the bank’s equity generation capacity. FAB is shrinking the gap between its GCC peers from a P/B standpoint at 1.26x (vs. 1.16x for its peers).

Galliano's Financials Research

On the back of 3Q23 results, Victor Galliano screens several Thai banks’ core profitability, and their credit quality and coverage, to identify those that are attractive value, have good earnings growth prospects and have the potential to deliver sustainably higher returns going forward. Although he likes Ayudhya, his top pick remains KTB, given its much better CASA ratio and less stretched LDR from its funding metrics, its healthy credit quality coverage and its premium ROE. While KTB's share price performance has been lacklustre recently - perhaps impacted by negative EPS revisions - sound Q3 performance metrics should drive its re-rating supported by undemanding valuations.

Hemindra Hazari

The unlisted parent company of the Indian-listed Vedanta Ltd and Konkola Copper Mines in Zambia, has been in the news due to apprehensions that the company will find it difficult to meet payment of US$3bn bonds maturing in the next two years. Although the media have focused on the dollar bond maturity over the next two years, the company’s own disclosures reveal that in FY24 (year ending 31st Mar), US$4.3bn of bonds will be maturing and a further US$4.1bn in FY25. In fact, a liquidity analysis of the company reveals an even graver situation. According to calculations by Hemindra Hazari, the company has a liquidity shortfall of US$10.8bn in FY24!

Macro Research

Developed Markets

Steno Research

Central banks are insolvent: How do we deal with it?

Yes, you heard right. The Fed is insolvent. The ECB is insolvent. The Riksbank is insolvent. The list goes on… The big question is if it matters and when it matters. Andreas Steno believes the Fed and other CBs will opt to kick the can down the road, running with a “deferred” tax asset that allows them to run operations despite insolvency. The big risk here is markets losing trust in the CB system; there’s a good argument to be had for risk premiums being structurally higher in the post-ZIRP world. Countries with a high degree of insolvency may be attacked by bond vigilantes once push comes to shove and market intervention is needed.

Talking Heads Macro

US: The case for being short bonds (again)

On October 12th Manoj Pradhan took profits on his US positions after a great run, arguing there would be a time to short bonds again – he wasn’t expecting it to come so quickly! He argues there is too little priced into December and for hikes in general; if the Fed does not match the incremental amount of tightening required, then bonds will. He also remarks that the Bank of Canada model is working for the US, commenting on the four elements that forced the BoC to end its April pause and hike in June: labour markets, growth, interest-sensitive spending, and inflation. All of these are highly applicable to the US and point to higher rates – if the Fed doesn’t provide that premium, bond vigilantes will. The Fed is playing with fire and it’s getting burned.

Policy Sonar

Is Germany becoming quintessentially Italian?

News that the current ruling majority in Berlin could change is spreading quickly in Rome. Most Italian politicians are now assuming that Chancellor Scholz is ready to ditch the Greens and the FDP, and to onboard the CDU/CSU. It’s unclear whether this scenario will materialise, or whether it will be an outright switch or more of an embrassons-nous of mainstream parties with the goal of cutting off the AfD and the radical left. The setup in Berlin looks wobblier than in Rome. Moreover, Francesco Galietti doubts that PM Meloni fears a similar turn of events in Italy. Not only were the PD and M5S defeated bluntly and decisively at the latest general elections, they’ve never really recovered. That's not what happened in Germany, where the CDU is doing pretty well in polls these days, and where the CSU in Bavaria just managed to fend off the AfD.

Aitken Advisors

Australia: More hikes needed

James Aitken doesn’t think the RBA will hike next month but believes 1-2 more hikes will be required, suggesting a terminal RBA cash rate closer to 5%. As is the case with Canada, wage settlements continue to head in the wrong direction. Commenting on the RBA’s latest Financial Stability Report, James says it reminds us that inflation is an aggregate demand problem. Hourly wage rates matter for demand, aggregate income matters more. In what remains an interest-rate sensitive economy, it is remarkable that Australian households have been able to respond to the cost-of-living pressures by increasing their supply of labour and generating stronger incomes. James says the Australian labour market is too strong and aggregate demand is too high for the RBA to relax. More work needs to be done to lift the RBA’s cash rate and Governor Bullock knows it.

East Asia Econ

Korea: Exports up, domestic demand down

From an activity perspective, Korea's macro story this year has been one of post-covid recovery of domestic services offsetting export recession. The domestic recovery has recently been starting to look long-in-the-tooth, but Paul Cavey has been looking for signs of an export revival. This month's sentiment surveys from the BOK show both of these trends more clearly falling into place. For now, the weakening of the domestic cycle is clearer, but that doesn't mean a swift change in BOK policy: the sentiment surveys also show inflation holding up.

Ekins Guinness

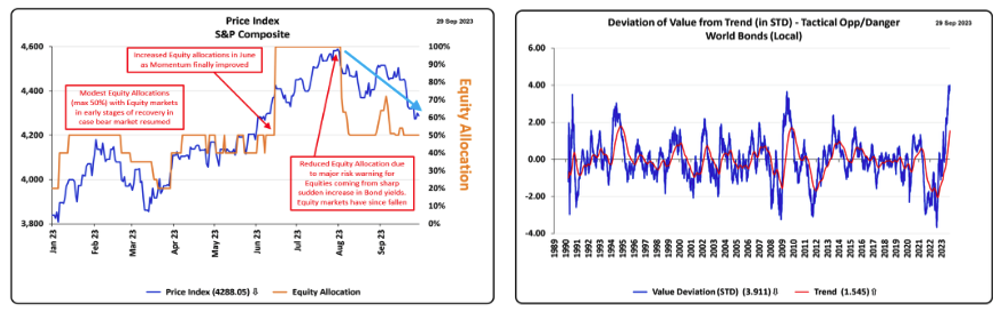

Bonds still pose risk to equity markets

The Ekins Guinness team accurately warned in August that the significant and sudden improvement in bond value yield posed a potential tactical opportunity for bond markets and equity markets. Since then, bond yields have risen further and equity markets have been weak. Chart 1 shows the recent price index for the S&P Composite against their equity allocations. All of the equity price moving averages are now falling, which is a new additional concern; if they continue to deteriorate further, the team will reduce their equity valuations further. It will take time for the risk warning from bonds to dissipate, so the team do not anticipate being fully invested in equities for a while. The difference (in standard deviations) between the bond value yield and its trend line is extreme (chart 2) – in fact, it’s now at the highest level since the 1990s.

Radio Free Mobile

AI regulation should target people, not machines

Governments are moving to impose regulations on AI but a lack of understanding on their part may destroy most of the value that large language models bring. Some of the proposals are focused on topics such as veracity and accuracy, hallucination, and objectivity of AI models – each of which will be very difficult or even possible to effectively fix. Regulation will also impact competition, making it harder for smaller companies and benefitting the likes of Meta, Microsoft and Google. Richard Windsor still believes the machines are still quite dumb, yet they are managing to create a convincing illusion of sentience which leads people to anthropomorphise these systems. This in turn makes them much more capable of being used by bad actors; humans remain far more in danger from other humans than from machines and should be the focus of regulation.

View from the Peak

Strategists’ ideas for 2024

Paul Krake outlines the ideas he believes the sell-side community will emphasise for the year ahead (not his own recommendations). They will be strewn all over the financial media and rapidly become the consensus. They may all be promoted through the medium-term lens of being winners for 2024, but in practice, they are nothing more than trading strategies. Ideas will include: US small cap to outperform; China to rally; mining and climate infrastructure to snap back; KPSI to outperform; large cap banks to outperform the SPX; long US duration; short USD; and long AUD, MXN and KRW.

Emerging Markets

Greenmantle

Markets and the Middle East crises

Following the terrorist attacks on Israel on October 7, U.S. bond prices and Israeli assets weakened while gold and oil rallied. Niall Ferguson analyses seven historical Middle Eastern conflicts involving Israel and finds that most of these conflicts had only limited effects on global markets—with the notable exception of the 1973 Yom Kippur War, which spiked oil prices and led to a crash in equity markets. If the conflict escalates further into a broader conflagration in the Middle East, history suggests there may be larger market moves. However, while Niall urges investors to consider the potential for asset price adjustments comparable with those of fifty years ago, he does not expect an equivalent energy price shock or stock market crash; many of the regional dynamics differ and thus the market reaction is unlikely to be so extreme.

CrossBorder Capital

Reassessing EMs after China’s shock easing

EM liquidity rose higher in September, driven by an uptick in central bank liquidity and by robust CrossBorder flows. Highlights include another huge liquidity injection by the (PBoC). Inflows now exceed RMB 2.6 trillion over two months, pushing Michael Howell’s index up to 80.8. Notwithstanding PBoC liquidity boost, the otherwise resilient EM Liquidity is simply inconsistent with the widespread fears of approaching World recession. EM markets so often get their impetus from buoyant cross-border capital inflows. Here, two things really matter: (1) a stable to weaker (not strong) US dollar and (2) a strong Chinese economy. While the former often drives a regional credit boom, the latter tends to bolster regional commodity markets. The past few months have witnessed a firming US dollar and widespread fears that the Chinese economy is set for structural decline. Mike Howell disagrees.

Deep Macro

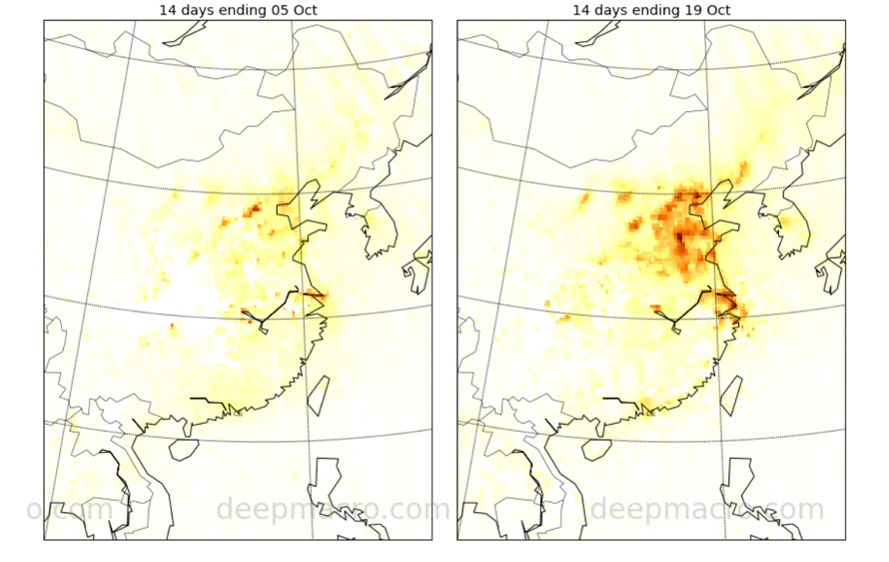

China: Recovery mode

Jeffrey Young points out that sentiment towards China in mid-August was very negative at a time that Deep Macro argued that recovery was on the way: it has now arrived, being led by the industrial sector. This is shown, in part, by concentrations of industrial pollutants (nitrogen dioxide) in the atmosphere, which correlates with industrial production (see chart). Jeffrey also notes that China has now moved from a disinflation state to a reflation state. China's structural challenges do not seem to be impeding the normal movement of economic growth and inflation through their cycles. Even though the domestic factors have turned positive for the RMB, Jeffrey expects a mild depreciation of the RMB over the next month due to global risk factors.

PRC Macro

China: Beijing painting itself into a corner?

One of the key phenomena right now is the US bear steepener, which may have some room to uptick. William Hess believes Beijing is still worried about potential external shocks from dollar strength and a reversal for US equities. He also thinks that technocratic officials are similarly worried about unrealised losses originating from the property sector and quasi-fiscal credit. More developer losses are expected in coming months, which may lead to a state stabilisation fund of some RMB 500bn. The PBoC continues to signal a growth-supportive agenda, but nothing that will trigger a short-term risk-on rally. William discusses Beijing’s overall policy stance, believing it insufficient to revitalise domestic capital markets and reflate domestic asset prices.

Oxford Analytica

China’s economic slump: Will the causes impede recovery?

China’s economy has not rebounded as investors or the government expected. Consumption has been weak. The property market continues to weigh on sentiment. Youth unemployment topped 20% before the authorities decided to stop reporting it. In Oxford Analytica’s latest white paper, the authors consider the causes of the economic slump, policies that are being directed to tackle it and the potential trajectories for the Chinese economy going forwards. Please contact us to find out more.

Alberdi Partners

Argentina: A new surprisingly negative electoral result

The election took a surprising new turn as Sergio Massa went from third in the August primaries (PASO) to first in the presidential election, with 36.7% of the votes. Massa (Union por la Patria, UP) got the most of the participation increase, with 3 million new votes. Javier Milei (La Libertad Avanza, LLA) added 700,000 while Juntos por el Cambio (JxC) lost 400,000 votes. Marcos Buscaglia believes that the result of the run-off election on November 18th is almost a coin toss. Massa seems to have the upper hand, but Marcos thinks that the anti-kirchnerism of most of JxC’s voters are a force to reckon with. He therefore believes it is 55% for Milei and 45% for Massa. Milei took the first steps to get JxC’s voters, saying in the post-election speech that he is willing to make a “tabula rasa” to open himself to these voters.

Teneo

India and the UK: Impasse

India and the UK face a deadlock in their proposed free trade agreement, primarily due to the UK's desire for access to India's legal markets and India's call for more visas for its professionals. Teneo's analysis reveals that India is in no rush to finalise, as the FTA has minimal domestic electoral impact and offers limited economic gains without increased visa access. The Bar Council of India has capped foreign lawyers' activities, and Indian law firms express concerns over market liberalisation. Dairy cooperatives seek relaxed UK food standards, while rice producers aim for UK market access but face political and quality challenges. The auto industry might see import duty reductions. Overall, tariff reductions might benefit certain sectors, but India's strategy suggests limited concessions and a possible impasse on market access and visas, framing the FTA as a non-crucial factor for trade growth.

Emerging Advisors Group

Pakistan: Stuck in a recurring cycle of restructuring and rupee pressures

As Jonathan Anderson suspected, markets have done well tactically in the aftermath of the IMF program announcement. This is due to a combination of IMF funding and progress on bilateral discussions but also serious tightening and demand destruction at home in order to balance the external accounts. However, as before this is emphatically not a structural entry point. Pakistan does not have (and may never have) a sustainable external position, nor does it have (and may never have) a sustainable budget position at home. Until it can achieve meaningful twin surpluses – or manage a “true” default on sovereign obligations – the country remains stuck in a recurring cycle of restructuring and rupee pressures.

ESG

Adelwise

Seafood: The next investment catch?

Aquaculture - the breeding, rearing and harvesting of marine life - offers exciting growth potential. With a growing world population projected to reach 8.6bn in 2030, the demand for aquatic food is only going to rise. This, coupled with higher cost pressure from feed and energy, could see prices rise 33% by 2030. Meanwhile, the percentage of fish stocks within biologically sustainable levels has fallen from 90% in 1974 to 64.4% in 2019. Rebalancing this is where the growth opportunity resides. To help investors navigate the investment decision process, Sophie Biro-Rouillon has devised a - Life below water - scorecard. The scorecard is based on UN SDG 14 targets which she uses to evaluate and score ACWI countries to identify opportunities.

Commodities

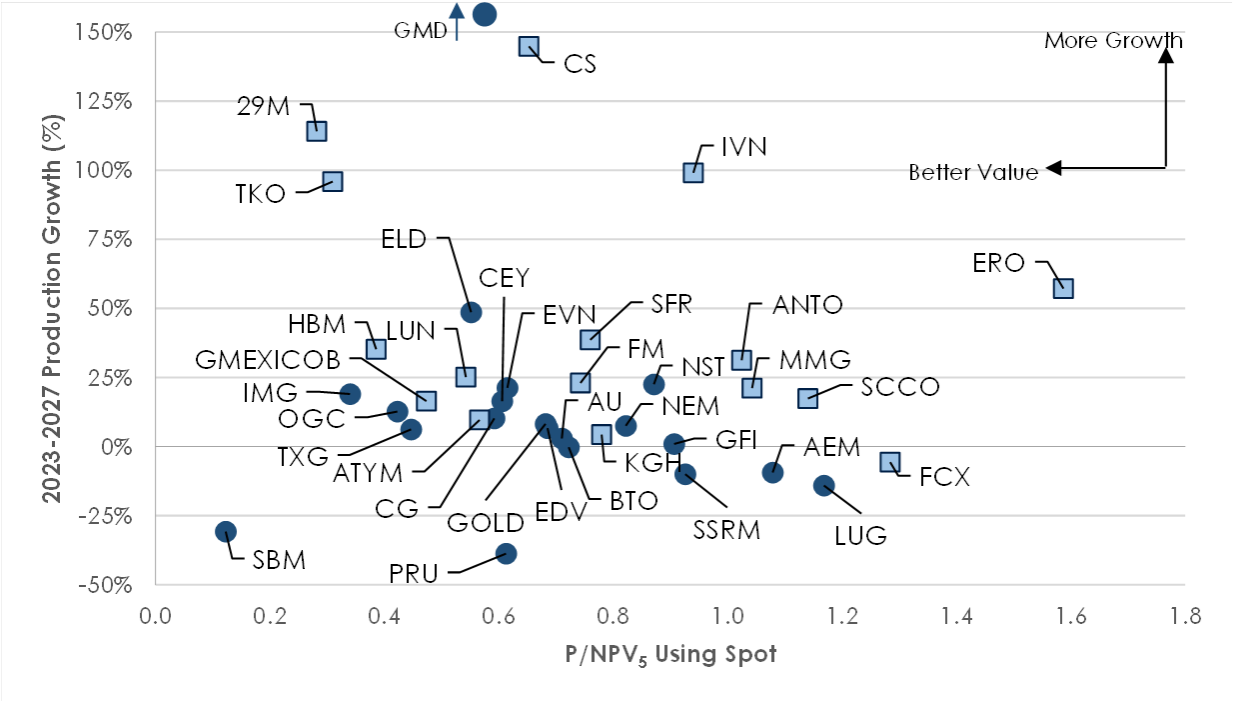

Global Mining Research

Copper vs Gold

Gold has outperformed copper for the past two years, but David Radclyffe comments that the stocks have achieved similar performance. This has resulted in copper stocks trading at a valuation premium, having attracted investor attention for future growth prospects due to the EV thematic. Overall, gold stocks offer better value and yield than copper stocks that are often more growth oriented. Gold has also shrugged off the pessimism of higher interest rates, rallying as a safe-having destination. The high beta of gold stocks to metal price presents an opportunity as the price gains traction. Preferred equities are LUG, GOLD and NST. Copper remains attractive as supply weakness and low inventories are offset by macro concerns. Investors should look towards ATYM and TKO as junior miners, and SFR amongst the mid-to-larger names.

Longview Economics

What does sanctions relief mean for Venezuelan oil supply?

After months of negotiation, the US and Venezuela finally agreed on terms to alleviate sanctions on the country’s oil sector. The oil market’s reaction to the news has been mixed. In the short term, Chris Watling and Harry Colvin expect that projects that are currently operational should quickly increase production to full capacity, which mainly consist of joint ventures between Chevron and PDVSA. There’ll be an increased demand for the country’s heavy crude, especially given the significant premium in the West for such products. In the long-term, expect it to take at least 2-3 years before Venezuelan oil supply meaningfully accelerates; the poor fiscal situation, cautious foreign companies and inadequate infrastructure will hold back supply increases. Expect an increase of no more than 0.2-0.3 mbpd per annum for at least 2-3 years.

CPM Group

Preparing for the next recession with gold and silver

While a recession is not imminent, one is coming. Jeffrey Christian looks at Real GDP, US Industrial Production, as well as the stock and bond market, to determine how we can determine if we’re in a recession. He also looks at some of the steps viewers can take to prepare for a recession with gold and silver, and how the metals have performed relative to other assets during past recessions.

Click here to watch.