Company & Sector Research

Europe

Arete Research

BT shares are beaten-up and unloved, yet Openreach is making rapid progress on high-return fibre capex, while alt.net rivals are facing uncertain financing, reducing long-term overbuild. BT looks likely to grow revenue, EBITDA and to improve FCF materially as FTTP capex moderates as the build slows post FY26E. Meanwhile, a potential Labour Government looks business-friendly and needs FTTP built; regulatory intervention impacting BT's fibre returns would seem self-defeating. Looking to the mid-term (FY28E), BT shares are implied at only 5x FCF or 7x EV/opFCF. For a business with duration where fibre infrastructure is at the core of the business, this seems remarkably cheap. TP 228p (~90% upside).

Starling Advisors

In the context of slowing economic growth in China and concerns about lower US consumption, the pressure is on UHR. However, the Swiss company has proven to deliver highly desirable products and navigate well in challenging times. In H1, the success of MoonSwatch and strong momentum in own retail - which outperformed the wholesale channel in the US and Mainland China - showed the market the innovation capabilities of the firm. UHR shares have underperformed luxury peers in the past three months and currently trade at below 12x P/E, the cheapest it has been in 10 years. TP CHF321 (35% upside).

Alumbra Research

FCF guidance cut validates Alumbra Research’s concerns - Alumbra initiated coverage on ALO on 2nd May due to €1.7bn of excess working capital liabilities from the Bombardier Transportation acquisition that they believed would represent a significant headwind to the group’s FY24 FCF. Last week, the stock crashed nearly 40% as management warned that FY24 FCF is now expected to be between -€750m and -€500m versus prior guidance for ‘significantly positive’ FCF and consensus expectations for FCF of €300m.

ROCGA Research

BAB appears on ROCGA’s list of undervalued ideas - using their proprietary CFROI based DCF valuation tools, they identify companies on the spectrum ranging from undervalued to overvalued. This list can be easily modified to cover specific geographies, industries, M/Cap... ROCGA currently covers c.2000 companies across Europe and the US. More details on their systematic and interactive valuation tools can be found here. A trial can be arranged on request.

AIR Capital

SAP is guiding for cloud revenues to reach €14.1bn (+25% Y/Y) in FY23, suggesting growth will be far stronger in H2 vs. H1, in total contradiction with the current economic slowdown and competitors’ recent comments. Pierre-Olivier Essig struggles to share management’s bullishness which has led to him downgrading the stock to Sell (from Buy). His new TP is €100 (previously €140).

AIR continues to boast an enviable track record with impressive gains on Buy-rated stocks including Aixtron, Meier Tobler, Novo Nordisk and Rolls-Royce, as well as shorts including Fresenius Medical Care and Grifols.

North America

New Constructs

Where Street earnings are too high & who should miss

Wall Street analysts are too bullish on Q3 expectations for most S&P 500 companies. Although down from record highs set in early 2021, the percentage of companies whose Street EPS exceeds New Constructs’ Core EPS remains high at 71%. Furthermore, 208 companies (>40%) overstate Core Earnings by >10% (Street Earnings are overstated by 24% on average in TTM through 2Q23). New Constructs highlights Bio-Techne as one of the companies most likely to miss Wall Street analysts’ expectations in Q3. Others include Principal Financial Group, T-Mobile, Tesla and Xcel Energy.

Periphery Research Partners

Hesham Shaaban believes the industry is running out of new states for OSB legalisation and DKNG can't lever its marketing spend much further on a now larger geographic footprint with certain states already showing signs of fatigue. Hesham doesn’t see a pathway to consensus 2024 EBITDA estimates. The maths basically translates to an incremental EBITDA margin of >60%, which on a standalone basis seems excessive, even before considering that its incremental gross profit margin has never touched that level. DKNG’s ad budget would need to decline y/y, which hasn’t happened in its reported history, and it would take a leap of faith to assume it could do so and produce consensus revenue growth of +20% at the same time.

Gradient Analytics

SLGN has been added to Gradient’s Greatest Concerns List due to a variety of fundamental and earnings quality issues including: 1) A myriad of top-line headwinds that may pressure sales in 2H23. 2) A relative spike in accounts receivable (surge in 2Q23 represents a marked departure from seasonal norms). 3) Inventory levels have diverged from near-term demand estimates (and appears to be aging unfavourably). 4) Unusual surge in prepaid expenses may represent another margin headwind. 5) SLGN trades at a premium to peers across a wide array of both trailing and forward-looking valuation metrics.

JJK Research Associates

Janet Kloppenburg’s channel checks point to 3Q23 business trends continuing to be very healthy, with total revenues likely tracking above +7% consensus, driven by ongoing momentum in the women’s businesses. Anthropologie’s performance appears to be broad-based, with new customer acquisition fuelling gains with a younger millennial customer. Janet’s product reviews of Free People and FP Movement also reveal highly innovative and fashion directional assortments, which are driving meaningful market share gains. The strength of these brands is more than offsetting the protracted turnaround in UO, resulting in Janet's FY23 / FY24 EPS forecasts of $3.25 / $3.60 being nicely ahead of consensus of $3.16 / $3.33.

J Capital Research

Examining recent financial trends in the company suggests a heightened risk of uncollectable receivables - J Capital believes SLB risks impairments of at least $1.5bn from its Russian and Mexican operations (nearly half its 2022 net income). If operations from these countries are subsequently impaired or ceased, there may also be a downgrade of future revenue growth. From a wider perspective, they are concerned that SLB, in the pursuit of business, is tolerating more risk instead of downscaling it.

Portales Partners

Banks confront interest rates, regulators and credit entering earnings season

Bank stocks sold off on multi-decade highs in long term interest rates last week, while investors prepare for a host of key events over the coming months. Charles Peabody believes banks could rally on 3Q23 earnings results as investors see some relief from regulatory rulings and deposit betas while AOCI and credit deterioration remain front of mind. However, the fundamental trends for banks will continue to deteriorate into 1H24. Markets are differentiating between banks with the capital, liquidity and funding to take advantage of opportunities - and those without. Charles favours JPMorgan, Wells Fargo and PNC, while shunning US Bancorp and Truist Financial.

Paragon Intel

Paragon Intel has published its Executive Diligence memo on RBA's new CEO Jim Kessler, who took on the role in Aug having been COO since 2020. An approachable and grounded executive, he melds strong financial understanding with an excellent ability to execute, which he will leverage while driving legacy RBA results and the integration of the broadly criticised IAA auto salvage acquisition. Paragon’s research includes interviews with 7 former colleagues who worked with Kessler for >27 years combined (5 were positive and 2 neutral) - sources who worked with him at Caliber Collision were the most positive, followed by RBA and then vRide.

Gordon Haskett Research Advisors

Time to take note of Homes.com’s rapid web traffic share gains

While many investors have probably just focused on the Big 3 online real estate portals (Zillow, Redfin & Realtor.com), GHRA believes it's now time to focus on the Big 4 as Costar’s Homes.com has been aggressively growing its web traffic share. Key highlights from their report include: 1) Homes.com accounted for 10.4% of web traffic in Sep, +c.900bps Y/Y. 2) Homes.com's 44% paid mix last month represents a 25-point Y/Y increase, materially above the 1-point increase at both Z & RDFN and 2-point increase at Realtor.com. 3) Homes.com's paid clicks have grown at a significantly faster rate than non-paid clicks (17x vs. 5x).

Singular Research

A premier multifamily rental portfolio - AIV’s development pipeline looks extremely strong, with over 1,000 new units expected to come online in the next 18 months, which will grow stabilised units by close to 20%. Recurring revenue and EBITDA are expected to grow at a materially faster pace than its peer group. AIV also has a rock-solid debt maturity profile, with a weighted average cost of debt, including interest rate caps, of 5.28%. ~66% of the group’s debt service occurs in or after 2029, with no material debt maturities occurring before 2026. Singular Research initiates coverage with a Buy rating and a 12-month TP of $11.20 (85% upside).

Sales Pulse Research

Feedback from channel contacts on the company's core PAM solution continues to be strong, while CYBR is also the standout beneficiary of the MGM breach. Pipeline generation is healthy. Sales Pulse has heard examples of reps “sitting on deals” to push into the next quarter… always a good sign. Some resellers they talked to shared that CYBR encouraged them to get their SE’s trained and certified on the new CYBR Workforce and Identity offerings, but so far these resellers, have not seen much professional services business based on this investment. Elsewhere, CrowdStrike, Palo Alto, Zscaler and Okta all look solid, while Fortinet and Tenable have the softest channel sentiment.

Behind the Numbers

MRVL beats or misses forecasts by only 1-2 cents, but there appears to be several areas for concern: 1) Allowances for discounts and rebates are huge and driving +/- 7 cents of EPS per quarter. 2) Company adds 2.5 cents per quarter by boosting stock pay as a percentage of sales. 3) A new warranty charge appeared for first time last quarter. 4) AI growth is being swamped by weakness in other markets and inventory remains high. 5) It may not use all its contracted shipping and foundry capacity which hurts margins. 6) FCF is overstated because MRVL records technology licensing fees in the financing section of cash flow.

Radio Free Mobile

Preliminary results from Samsung combined with TSMC’s monthly revenue disclosure gives Richard Windsor increased confidence that the inventory correction has come to an end. Of all the component suppliers, QCOM is now trading at the bottom of its peer group in terms of PER ratio which demonstrates just how short-term the market thinks. There is no end in sight to its sales of 5G modems to Apple, it is winning enough deals in automotive to seriously disturb Mobileye and it is very well positioned for the Metaverse when or if it takes off. From a long-term valuation perspective, the shares are on sale.

Emerging Markets

Smart Insider

Rongjun Mu (EVP) sells US$28.9m of stock at HKD113.12 reducing his holding by 6%. His record as a seller has been good, making sales at HKD196.05 in Jun 2022 and at HKD163.7 in Jan 2023 and it's concerning to see him continue to sell into weakness. Xing Wang (Chair & CEO) has also sold $360k of stock, whilst very modest relative to his holding, his record as a seller has also been strong. Compounding matters, both sales follow Nanpeng Shen (Non-Exec), who sold $434m of stock on 31st Aug, reducing his holding by 29%. Stock Rank -1 (lowest rating).

Galliano's Financials Research

China Banks: Deep value despite the NPL challenge

In Victor Galliano’s China banks screen, he focuses on the credit quality headwinds going forward, as well as the returns trends that can absorb potentially worsening cost of risk charges. While China bank shares continue to be poor performers, Victor sees selective contrarian buy opportunities for those banks with deeply discounted valuations and strong balance sheets including credit quality metrics. He upgrades Ping An Bank to Buy and continues to favour Industrial Bank and CCB, although Minsheng remains a Sell.

Insight Investment Research

Exclusive Dubai toll road concession connecting main economic and tourist hubs - minimal capex, high wealth and rising population to generate strong FCF. Op FCF of AED1.49bn, minus capex of only AED5m, to lead to FCF pre-dividends of AED1.44bn in 2024E. Assuming all capex is maintenance related, implies a recurring FCF yield of 5.9% in 2024E. High operating leverage given mostly fixed opex costs, thus additional traffic and inflation highly accretive to EBITDA. Robert Crimes believes SALIK is substantially undervalued by Sell Side consensus. His DDM based equity valuation of AED46.5bn & TP of AED6.21 (91% upside) implies a relatively high EV/EBITDA of 30.7x in 2024E, but this reduces to 19.4x in 2030E due to +7.7% CAGR in EBITDA in 2023-30E. IRR at current share price of 11.8%, 370bps above Insight’s Ke of 8.0%.

Silk Road Research

China Automation: Destocking nearing end, but 2024 expected to be flat Y/Y

SRR’s latest channel checks reveal short cycle orders have bottomed and destocking headwinds have significantly eased Q/Q. The auto industry was cited as an area of strength, while the export market and the electronics sector were highlighted as areas of weakness. The biggest medium-term headwind cited for foreign brands was rising domestic competition. Local automation companies have rapidly moved up the technology curve, while pricing for domestic brands in robotics were estimated to be 10-20% lower than foreign brands, while DCS products were 30-50% lower. Brands mentioned by private systems integrators that have been vulnerable to share loss to domestic brands include Yaskawa, Emerson and Siemens.

Alembic Global Advisors

MENA Chemicals: Earnings misses anticipated

Relatively weak MENA chemical sector share price performance has resulted from a compression in margins on the back of relatively weak product pricing and higher feedstock costs coupled with investor skittishness around the prospects of a recession across several geographies. Hassan Ahmed’s analysis suggests Street expectations for 3Q23 are too high and has lowered his 2023 and 2024 earnings estimates for all seven MENA names that he covers. SABIC is his top pick, as Hassan believes it offers the best blend of earnings resilience and below-sector average valuation.

AlphaMena

EMAAR surfs a 10-year high - Real Estate is seen as a refuge for investors through oil and commodity price volatility. Recent results saw the company's Real Estate revenues fall 18.5%, but this was partly offset by a revival of the other segments with Leasing and retail revenue increasing by 10.6% and Hospitality revenue up 9.7%. Growth was driven by the steady recovery in the tourism industry and strong domestic spending. Margins are also doing well thanks to better operating and financial cost management, while the balance sheet is strong. Finally, AlphaMena flags the recent Credit Ratings upgrade by S&P, Moody’s and Fitch as further proof that the hard times are behind EMAAR.

Macro Research

Developed Markets

Willis Welby

UK: Taking a pause

The Willis Welby team have not always been fans of the Bank of England – the BoE were way off the pace as the UK came out of Covid – but they do think they are getting there. It feels like they are aware of the counting discrepancies and the pause in rate hikes was the right decision. More hikes might be on the way but don’t expect a lot. DB pension schemes will probably still be large sellers but UK equities are cheap and the interest rate and economic backdrop is not yet getting in the way of that view. Indeed, the team’s real time indicators have painted a much more positive view of the UK economy than official stats for a long time.

Teneo

Germany: The rise of the far right

Sunday’s regional elections in the states of Bavaria and Hessen brought the expected rise in support for the far right. The results demonstrate that the traditional narrative of far-right voting as a vague form of political protest, especially in East Germany, no longer holds. Given the magnitude of the political challenges, it is hardly surprising that the parties in Chancellor Scholz’s traffic light coalition are struggling in the polls. More important than the travails of the traffic light coalition is the relative inability of the Christian Democrats (CDU/CSU) to benefit from this more clearly. Sunday’s results and the regional coalition politics demonstrate how the CDU/CSU remains caught between a rock and a hard place. It could move to the right to halt the rise of the AfD but will also need to find centrist coalition partners, most importantly, the Greens.

High Frequency Economics

Trouble in Euroland banks

Carl Weinberg has been watching the results of the ECB’s weekly main refinancing operations (MRO) for signs of increasing stress in the banking system. The number of bidders for short-term cash at these weekly 7-day repo tenders is elevated and rising. The banks that show up here are short of cash to maintain either reserve minimums or capital adequacy, and cannot raise cash uncollateralized on the interbank market. Presumably, banks borrowing here all have problems. Carl’s theory is that the withdrawal of long-term funding for banks via the ECB’s targeted longer-term refinancing operations (TLTRO) lending has put a number of financial institutions below either reserve minimums or below risk-adjusted capital adequacy ratios.

Minack Advisors

Markets are pricing in a soft landing and the start of a new cycle

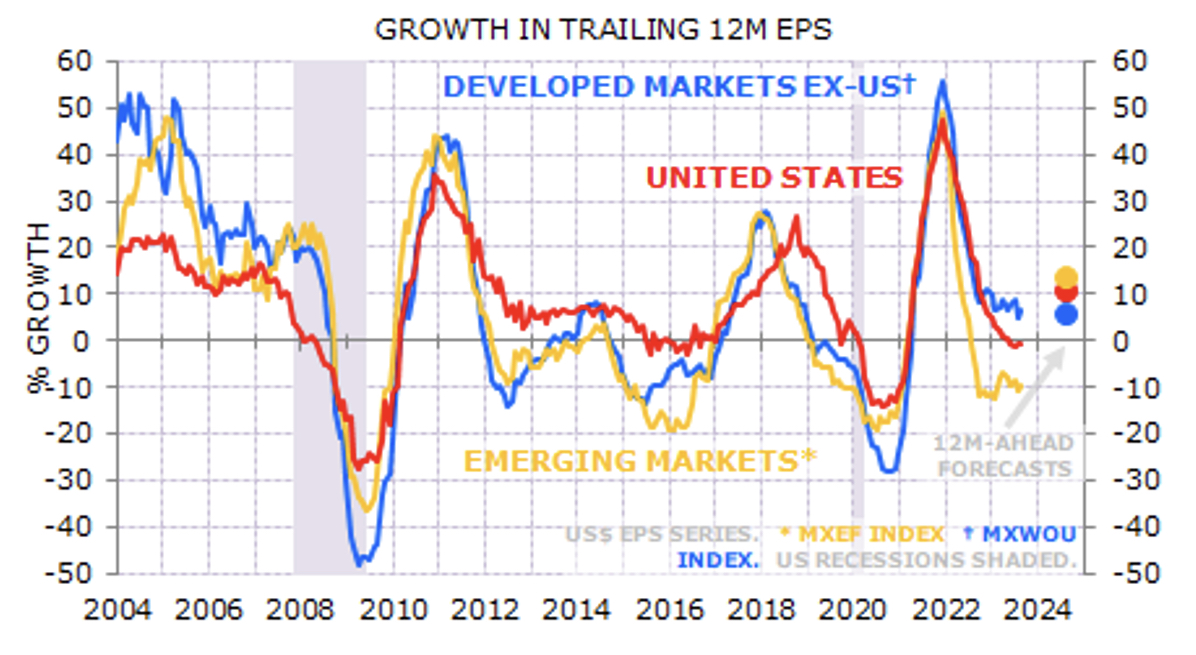

Spiking long-end yields are causing a few bumps for markets. However, there’s no sense that markets are pricing in an increased risk of a recession. Gerard Minack points out that is typical: every hard landing initially looks like a soft landing, and glass-half-full risk markets (such as equities) normally assume the best. That sets up an asymmetry heading into 2024: if the landing is soft, it’s in the price; if it’s hard, it’s not priced. Risk markets are betting on a soft landing and are starting to anticipate the next cycle upswing. If a new cycle is about to start, then the old cycle ended with a feather-soft landing. The cycle low for EPS growth – if we have seen that low – was higher than the mid-cycle slowdown of 2016 (see chart).

Longview Economics

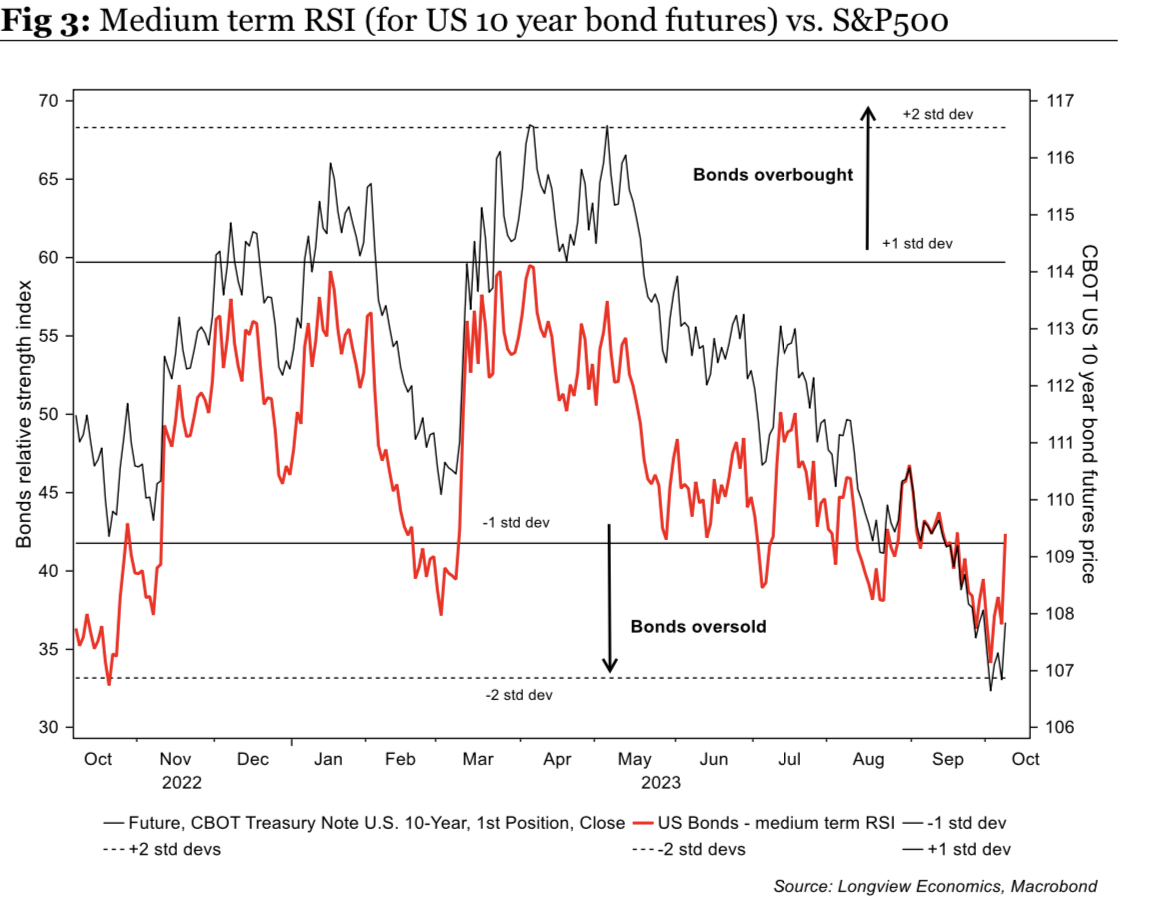

Building weight in troubling times

As the market sold off in recent months, most of Chris Watling’s models have shifted from clear, across the board sell signals onto BUY. Market sentiment and the market narrative has become increasingly troubled (i.e. a typical contrarian BUY signal), especially with the recent bond sell-off. With respect to the market timing tools and risk appetite models, some technical models and the medium-term put-to-call ratio are all signalling that a major local low is likely in the near-term. Bonds are now oversold: if stability occurs in the market, it would likely facilitate a rally in equity markets. Having reduced his tactical underweight equity position at the start of this month, Chris recommends closing it and to start building a tactical OW position.

Belkin Report

Soft landing? No way Jose

Consensus believes that inflation and higher interest rates are the biggest threats to the stock market. Michael Belkin says the exact opposite. The 9% peak CPI inflation rate and 11 Fed rate hikes were blowback from unnecessary, excessive stimulus in 2020-21. When the dust settles, it’ll be clear that overstimulus boosted inflation and subsequent tightening sent economies over a cliff. Stock markets are far from seeing reality, viewing the forthcoming rate cuts as bullish for equities. Nothing could be further from the truth. In the last two major Fed rate cut campaigns (2000-2002 and 2007-2008) the S&P500 fell 50% from peak to trough as the economy and corporate earnings collapsed in recessions. Michael is LONG defensive stocks and SHORT overvalued tech stocks, which currently has him ranked as no.1 out of 175 contributors with their alpha capture hedge fund client.

Heckman Global Advisors

Underweights and overweights across global markets

Dr. Leila Heckman comments on GDP forecasts for the year ahead, with most DM forecasts revised downwards. In the US, with the funding and political issues, sovereign spread risk has risen the most among developed markets, and it continues to be an expensive market. Canada also continues to be underweighted with middle of the road valuations relative to other markets and relatively large downgrades to 2024 GDP forecasts and relatively weak 12-month price momentum. In Developed Asia, Japan continues to be overweighted with its undervalued real exchange rate and strong price momentum. In Continental Europe, Ireland, Italy, Spain, Norway, and Austria continue to be overweighted. Germany and France continue to be underweighted. UK is underweighted based on tight monetary policy and weak 12-month price momentum.

Oxford Analytica

China vs US: Regulating AI

In September 2023, China took a significant step in the AI realm, with 11 companies getting clearance to release their mass-market language models. In Oxford Analytica’s latest White Paper, they examine the risks of AI and how both China and the US are regulating new advancements in technology. Concerns are similar across both nations, but the former is prioritising political stability and social objectives, whereas the latter is instead focussing on the protection of fundamental rights and the maintenance of the free market economy. In the worst-case scenario, such strong focus on competition could breed the development of potentially dangerous AI for purposes of strategic advantage. Please contact us to find out more.

Emerging Markets

Talking Heads Macro

Receive EM and don’t fight the Fed!

Paying rates has been a superb strategy for Manoj Pradhan since April 2020 and especially in the last two months being short bonds. It is not worth fighting the Fed at this point in the hiking cycle. However, the risk-reward is far too symmetric in the US to receive there. EM is another matter. If the Fed is on hold for the time being, EM rates and EMFX have repriced very well in line with Manoj’s pay trades, and China stimulus is coming through exactly as he argued it would. EM is set up very well with an asymmetric risk-reward. So, where to receive in EM? Manoj recommends Korea 2y1y, and 2y in Mexico (+MXN), Czech and Brazil (+BRL). There’s still some risk, but the path of EM central banks is cleaner.

Greenmantle

China: Stabilisation underway

Niall Ferguson is convinced that China’s economy is now entering a period of near-term stabilisation even as its structural growth problems worsen. With most of China having recently been on holiday for the mid-autumn festival and “Golden Week,” Niall believes that the October data will show a moderate—and temporary—boost to consumption. But key structural issues, including local government debt, household consumption, and the real estate slump, will continue to haunt the economy. In this environment, he remains structurally bearish on CNY and Chinese equities and fixed income, including real estate assets, but sees some tactical upside in Chinese tech and consumer-facing equities in the short term.

Capital Alpha Partners

Israel vs Hamas: A full-blown regional war is doubtful

Byron Callan expects that Israel will aim to eliminate Hamas, not just degrade it, in its now-unfolding “Swords of Iron” operation. This could suggest a campaign that lasts through October, with some “then what’s?” to consider. He doesn’t see the possibility of a full-blown regional war with Iran and therefore sees limited impact on defence fundamentals. Israel is likely to repeat “Operation Cast Lead” on a larger and more comprehensive scale, which originally began in 2008 and concluded in 2009 and saw the IDF generally avoid ground conflict in highly built-up urban areas. Hamas very likely learned from its prior conflicts with Israel, including Operation Cast Lead, and may have moved more of its infrastructure into the denser populated parts of Gaza City, Dier al-Balah, Khan Yunis, and Rafah.

Eurointelligence

Israel/Palestine: The wars around us

Hamas' attack on Israel raises a number of important questions for the rest of the world, the most of important of which being whether the conflict will spread. One likely long-term consequence is greater global fragmentation, a trend that has been under way for some time, which accelerated with the Russia-Ukraine war. Wolfgang Münchau makes the observation that many events of the 2020s are the results of unsustainable policies and decisions in the previous decade. This is not a time for analysis and answers but a time for questions. Two key questions that stand out are whether Hamas' incursion marks the beginning of a wider conflict in the Eurasian continent, and whether it will reduce western support for Ukraine as attention turns elsewhere. Attention in Washington will now almost surely shift to the Middle East.

Steno Research

How do markets react to turmoil in Gaza/Israel?

Andreas Stenos has taken a look at the data over the course of the last five stand-offs between Israel and Hamas/Palestine on the back of the atrocious scenes unfolding in the region over the course of the weekend. He considers an escalation involving Iran to be the biggest market risk right now. Before getting to the geopolitics, he allows the numbers to speak for themselves. Expect a slightly stronger USD; higher oil prices; higher broad commodities; better EM than DM equity performance; ok returns in Gold; lukewarm return in bonds.

Emerging Advisors Group

Peru: Six months on

Unrest has faded at the margin, but politics are still impacting local sentiment and activity. The domestic economy is now in recession by all metrics, and the tourist recovery has stalled as well. As before, though, Jonathan Anderson notes that there's no change in Peru's underlying fundamentals. Peru is still an export outperformer by regional standards with relatively solid external and fiscal balances, i.e., there's nothing at risk of falling apart here. The pendulum is swinging towards local carry and fixed income. The weak domestic outlook makes a further equity rally unlikely, but improvement in the external balance and high real rates make local carry and yield attractive.

Commodities

Vanda Insights

Oil and bulls

In Vandana Hari’s mid-Sept report she offered a moderately bullish view for the near-term, expecting prices to grind higher towards $100, which turned out to be spot on. However, heightened uncertainty and a sharp pivot in sentiment from oil supply fears to demand worries has brought prices back down to the mid-$80s. The pullback will strengthen OPEC+’s resolve to keep a tight rein on supply, with the Saudis possibly doubling down if prices look poised for another downward spiral. Vandana outlined a mildly bullish sentiment for this week of a $2-4/barrel rebound, which was also spot on, and expects prices to continue an upward climb to $90/barrel in mid-Oct to mid-Nov.

Global Mining Research

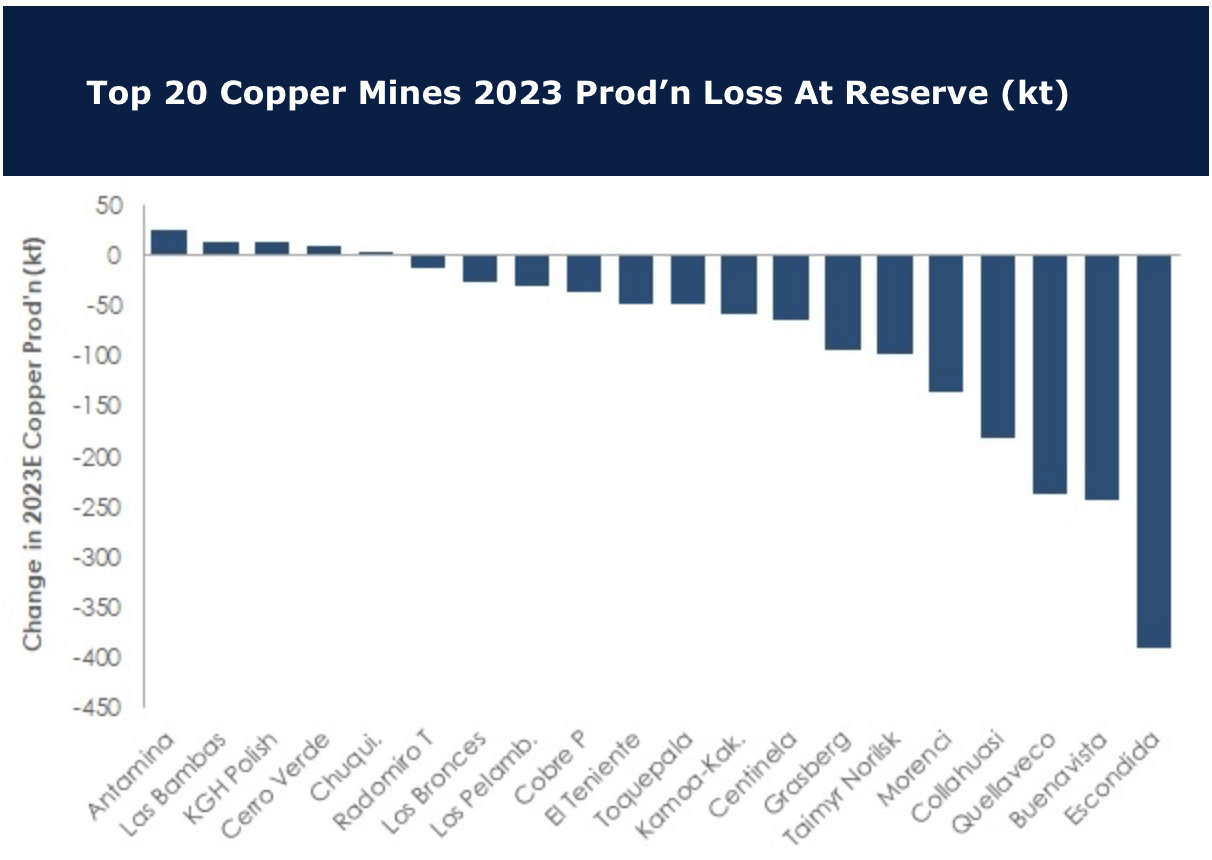

Copper high grading spells trouble

It’s very common practise in the mining industry to high grade operations for as long as possible, explains David Radclyffe. This is especially so in the early years but can run for much longer; take a look at Escondida, which continues to materially high grade despite running for many decades. Out of twenty of the largest and most important copper mines, only a quarter are low grading. What does this mean in practise? Based on 2023 forecasts, if mines were running on reserves, which they ultimately will, we would see a sizeable copper production fall without significant processing plant expansions; the top 20 would produce 1.64Mt copper less, if today’s milling and processing capacity remained unchanged but ore fed through at reserve grade. Some mines will face real trouble (see graph). With this in mind, if the energy transition thematic continues to be pushed we will see a global shortage of copper in the years ahead.

CPM Group

Gold and Silver: Climbing higher

In his latest video, Jeffrey Christian of CPM Group discusses the state of the economy and interest rates, following the release of the latest jobs market report. Jeff shares an updated forecast for Gold, Silver, Platinum, and Palladium as well as his expectations of a recession, and when it may occur.

Click here