Company & Sector Research

Europe

New Street Research

New Street explores the left-field idea that launching a full takeover of BT could actually help Drahi to increase his liquidity as one option to help support the deleveraging of Altice France by over 1x. They believe that legitimate concerns that Drahi could be a forced seller of his BT shares are acting as an overhang on the stock. While New Street aren’t in any way downplaying the strong opposition and complexity surrounding an offer for BT, they think the maths could just work, so there is the potential that Drahi could surprise the market and attempt to launch a full offer when his current 6-month standstill agreement expires in Nov, as it could raise c.£2.5-3.5bn of additional liquidity.

CHA-AM Advisors

Past the worse - David Scott first recommended the stock back in 2017, highlighting THULE's global leadership and as a great play on the new leisure age / ageing demographics. While it had a fantastic pandemic, the backwash caught it with excessive levels of high-priced inventory. However, David says the reported numbers are starting to show a classic “Positive Divergence”, where the group’s profits are suppressed by de-stocking but its cashflows are restored in the same process. He believes the deep correction in the share price is over.

Willis Welby

There are several manufacturing stocks in Willis Welby’s European Midcap coverage where cautious expectations come with decent growth and strong financial productivity. Two stocks they are particularly keen to highlight: 1) ARIS - the sharp and continuing falls in the share price look to offer a compelling opportunity. Consensus Y3 revenue growth is 5.5% and the implied to Y3 EBITM ratio is now in the high 40s. 2) KRN - H1 trading was good. Orders were strong. Guidance was raised and analysts followed suit. Finances here are seriously strong and an implied to Y3 EBITM ratio of just 39 looks to offer a really interesting opportunity.

Vision Research

Vision’s Apr 23 short report on HTRO focused on exposure to boom-bust Tier 2/3 fibre builders, risk of slowdown in key markets and customers, early signs of small customer stress, balance sheet and channel inventory builds, and widespread signs of moderating telecom capex spend. Management updated sales guidance last week and the shares were down over 20%, pushing the total decline since initiation to over 50%. In the past month, Vision has initiated 3 new European shorts: a $20bn+ consumer staple, a $5bn+ consumer/industrial and a $2bn+ industrial.

Starling Advisors

Growth is far from over - SAP's cloud business is set to grow over 20% p.a. through 2025, driven by a push to migrate on-premise legacy ERP customers to the S/4HANA cloud as well as an increase in cross-selling key solutions including Business Technology Platform (BTP). This momentum will accelerate medium-term sales growth and increase operating profit. Furthermore, the Business AI opportunity is just at its infancy, with enormous opportunity ahead, as generative AI will change the way business run. Alex Dwek believes SAP is well positioned to capture growth in a new AI era and has the potential to re-rate to multiples enjoyed by its 'pure play' cloud peers.

North America

Kailash Capital Research

The refinancing wall looms large - when algebra & optimism collide

KCR’s latest piece focuses on a group of companies that failed the Federal Reserve’s test for financial fragility as defined by interest coverage ratios (ICRs). These are companies that cannot afford to pay the interest on their debt out of operating income. The Fed’s rate hikes have yet to hit the income and cash-flow statements of this $2.2trn group of stocks, but when it does, the impact will be devastating. If you want to ensure you don’t have any of these low-quality stocks sitting in your portfolios, KCR can sort this 507-stock universe on any criteria you might want. Click here to access the full report.

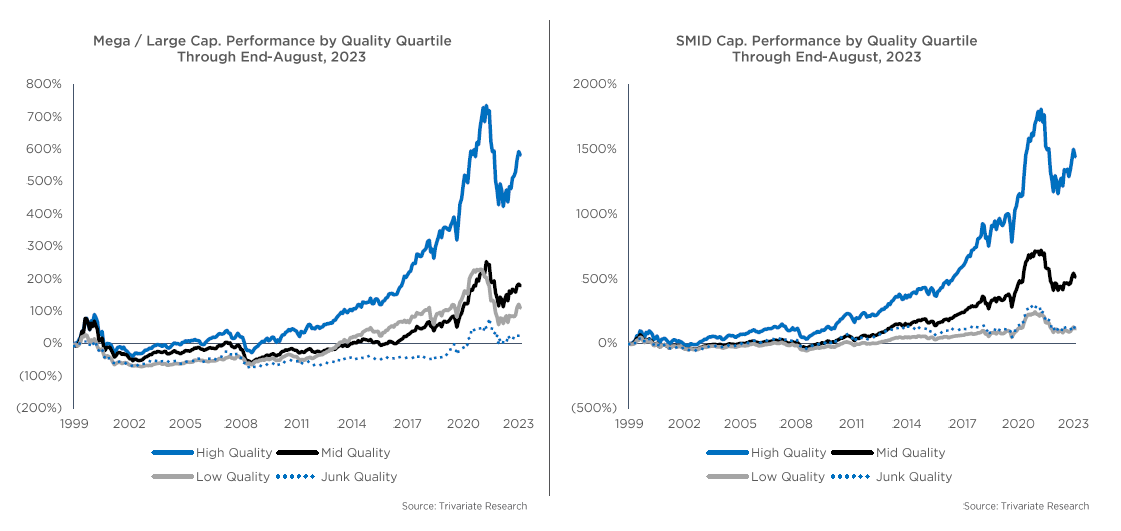

Trivariate Research

You sure you’re a quality growth investor?

Adjusting for the S&P500 performance, only the highest quality quartile of growth has cumulatively generated alpha over the last 25 years. Adam Parker identifies quality growth stocks with the goal of weathering any market pullbacks while also growing through an eroding economic backdrop. Key takeaways include: 1) Given the concentration by industry group, running a mega / large cap quality growth portfolio requires a generalist PM, not individual analysts. 2) Valuation metrics were not effective for quality growth investing. Profitability is most important. 3) Some stocks are highly replicable, some not, some highly idiosyncratic, some not - portfolio construction around these attributes is key. 4) Buying quality growth with gross margin expansion, avoiding those with accruals results in the best performance.

Hedgeye

Andrew Freedman recently turned bullish on the basis that NYT’s transition to a digitally-driven journalism brand has been a success and it has the potential to grow even further in the digital space. Strategic acquisitions have also diversified NYT’s product offerings and an aggressive bundling and promotional strategy will accelerate subscriber growth and drive ARPU expansion. There are also cyclical tailwinds over the next 9-12 months, as anticipated strength in digital advertising and a US Presidential Election cycle are upon us. Andrew sees NYT as the strongest digital journalism brand right now and anticipates 30% upside to its current share price.

Housing Research Center

How can homebuilders sell homes when 30-year mortgage rates are at 7.5%?

HRC has been touring thousands of builder communities since 2006. What they have observed recently is that builders are buying down rates to 4.99%-5.75%. This lowers the payment by over $400-$800/mo or 20%+ enabling buyers to transact. By building move-in ready spec homes, making homes affordable and paying realtors 3%+ when resale inventory is low - builders are achieving a sales pace of 3-4+ sales per community per month.

HRC has called all the major inflection points in housing and has a strong track record of making clients money in bull and bear markets. They are offering new clients a 30-day free trial or 90-day 50% off discounted trial. Request your trial today and find out which builders are outperforming so you can make money regardless of what rates do.

The Retail Tracker

The Retail Tracker felt AEO had been distracted for a while - launching premium denim, promoting aggressively at Aerie, opening Offline stores quickly, buying Quiet Logistics - it felt frenzied. Today, the company seems more focused. Real changes can be seen, not just one season, but more consistently at its core Eagle brand. The denim looks outstanding. The fashion tops are selling. The colours, the merchandising and the marketing are all improved. If AEO can continue this through fall, it is setting up very well for holiday gifting. This should see the stock head back towards $20 before making further progress in 2024.

ERA Research

A long-time industry incumbent with an underappreciated upside story - SON has taken bold steps to reorient its businesses over the past few years under its new leadership team. The businesses have been streamlined, with non-core assets divested, while new, complementary product lines have been added both in North America and Europe. Capital allocation has been investor-friendly, with an unparalleled dividend track record within ERA’s universe and periodic share buybacks. Debt is well-managed at 2.6x with interest coverage of 9.2x. ERA views the current share price as an attractive entry point for investors.

Quo Vadis Capital

Among John Zolidis’ favourite investment themes is a positive trend in unit level ROIC and this has been part of his thesis on YUMC for several years as the company has migrated store formats to smaller and more off-premise oriented locations with lower capex per unit. Cash investment per store has been cut by an incredible 35% per store since 2019. Looking forward, he believes this trend can continue and contribute to better incremental returns and higher margins. The stock is up only 3% YTD, which John attributes to relentless negative media about China. The shares trade at 10x EV/EBITDA (2024).

Foveal Research

There has been much excitement around Merck and MRNA's latest cancer vaccine after ASCO, with data appearing impressive. However, Foveal Research’s latest report suggests otherwise, with the vaccine Keytruda combo performing similar to historic Keytruda alone, along with an unusual underperformance of the control arm that flatters results. Secondary endpoint at ASCO reveal the real concerns over the true treatment effect of MRNA's addon. Dr Amit Roy pitched this idea at our recent Equity Shorting Conference. Click here to listen.

Two Rivers Analytics

Eric Fernandez’s latest short idea was generated from his Breaking Growth Model - in his 29-page initiation report, Eric discusses how 1) OMCL’s customers, the health systems and pharmacies, are under immense financial pressures. 2) Competitors tend to be larger / better resourced and OMCL has been underinvesting in R&D. 3) Sales have slowed and have now started to decline (even in its much-touted Advanced Services segment). 4) Margin declines underscore a fundamental lack of pricing power / uniqueness. 5) Estimates and guidance appear aggressive. 6) Earnings quality issues including questions re. bookings disclosures.

J Capital Research

Although revenue grows, VCEL has lost money every year since 1996 (apart from a measly $2.9m in 2020). By the end of 2022, the accumulated deficit reached $400m - a good indication of the historic value-add from this company. Its cartilage surgery costs $40k+ and is often denied insurance coverage, so the number of surgeries is and always has been small. Executives keep promoting concepts that go nowhere and disappear into corporate silence: a cardiovascular treatment, sales of bone marrow, “arthroscopic MACI”, a China venture. None of this has happened. Meanwhile, management rewards itself with ample share compensation - $37m last year.

Alembic Global Advisors

Given OLN’s impressive return profile and outperformance, relative to peers, during CEO Scott Sutton’s tenure, Hassan Ahmed wonders why the company's Board was unable to strike a deal to retain his services. However, despite Hassan’s frustration over Sutton's upcoming departure, he believes many of the strategies implemented by the outgoing CEO are sustainable. Furthermore, OLN already seems to be trading below trough valuation levels, highlighting the stock's attractiveness. Hassan's 12-month TP is $75 (55% upside).

Radio Free Mobile

Management offers a grovelling apology and waters down its new revenue proposal - Richard Windsor says U's brand has certainly taken a knock and to make matters worse it has been forced to give back more than it took in order to keep developers happy. While he likes the company as it has the potential to solve the most pressing problem in The Metaverse (interoperability), investors are going to have to wait a very long time for that to become a reality. Meanwhile, the stock still trades on over 5x 2023 revenues and 48x 2023 PER - these are lofty numbers for a company that is struggling with growth. It remains one to avoid.

Japan

JapanConsuming

Real insight on Japanese Consumer markets

Top stories from this month’s issue of JapanConsuming include: 1) Seven & I has finally sold Sogo Seibu - it will be pleased to have offloaded a loss-making format it never really understood, but at a cost, it will write off ¥90bn+ in loans. 2) Tsuruha is the latest retailer to come under attack from an activist investment fund. 3) ABC Mart expands its lead in footwear. 4) 3Coins, a variety store run by Pal Group, looks to have a strong future. 5) Frozen Foods becoming mainstream. 6) JapanConsuming’s FOCUS article discusses how the country is witnessing the emergence of a new elite group of department stores who are far ahead even of their big city peers.

Emerging Markets

RedTech Advisors

RedTech’s 3Q23 merchant survey takes a closer look at longer-term growth prospects for Douyin, which is again the most promising destination for online advertising and eCommerce in China. RedTech also asked their merchants several more detailed questions about the strategies they are pursuing on Douyin, as well as how they see things changing and playing out on the big eCommerce incumbents. Douyin is expected to nearly double its share of merchant sales by 2026 to ~19% with Douyin Mall a key driver. While the response to date from Alibaba's Tmall and JD has been lacklustre, opinions on how they should respond are divergent.

AlphaMena

Tunisia’s largest lender posted a modest 6.8% growth in its H1 net profit amid a rising loan loss provisions to comply with the expected change in the regulatory framework (transition toward IFRS requirement from 2023). The solid revenue momentum was helpful to manage the increase in its NPLs rate to 7.2% vs. 6.4% as of 31st Dec 2022. However, the BCT's key interest rate outlook is less favourable with the recent signs of cooling inflation. AlphaMena expects an ongoing impairment in asset quality given the still challenging economic environment. Thus, their earnings targets are expected to decline from 2024 leading to a negative stance on the stock, which is already expensive from a P/B standpoint: 1.44x in 2023 vs. 0.81x average for the Tunisian banks.

India Independent Insight

LTFH faced a substantial INR 26.9bn loss, up to 20% on its FVTPL book, in FY23 due to an accounting policy change involving the reclassification of wholesale loans to fair value. Despite seemingly improving non-performing asset numbers, LTFH's low loss allowance for reclassified loans, coupled with losses on loan sales, raised concerns about its asset quality and disclosure practices. Moreover, inconsistent fair value changes, a puzzling treasury operation and past provisioning flip-flops added to the uncertainty surrounding the company's financial performance and its transition towards retailisation under the banner of Lakshya 2026. The true motivations and hidden costs of this transformation warrants attention!

Macro Research

Developed Markets

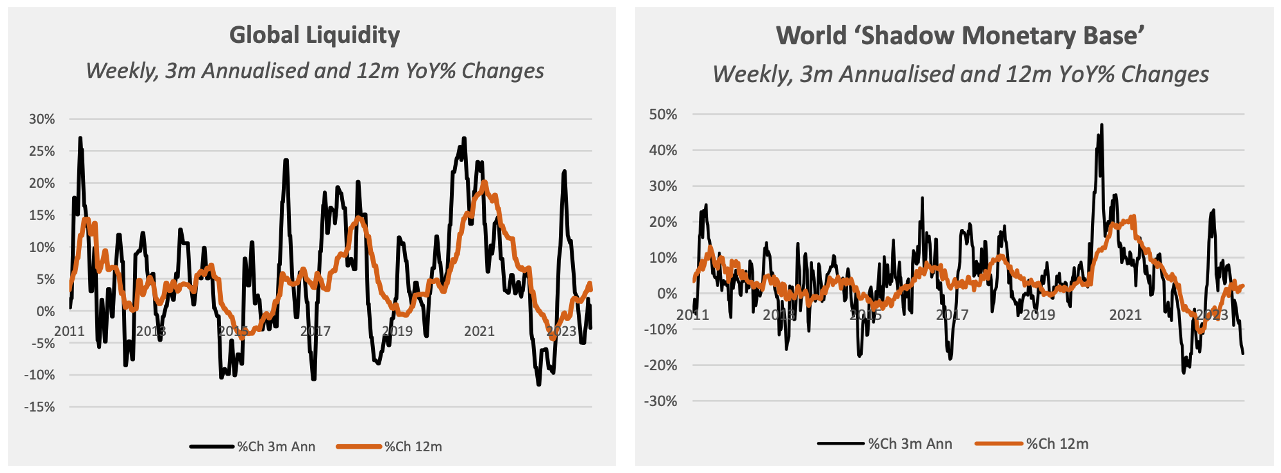

CrossBorder Capital

Faltering liquidity

Global Liquidity conditions falter… again. The root of the problem is weaker shadow monetary base growth, explains Michael Howell. The Fed and Bank of Japan are behind this latest development. This is worrying. Tight liquidity conditions put pressure on financial assets. Already, bond market volatility, as measured by the MOVE, has ticked higher. A rise in the MOVE negatively affects the collateral multiplier, which in turn affects global liquidity. Caution! Near-term developments are not good, but Michael still remains upbeat longer-term and continues to believe the Global Liquidity cycle bottomed last October.

Technical Analysis Group

Is last year’s bear market still ongoing?

Since October of last year, the Wave Principle, per TAG's interpretation, has continued to paint this year’s S&P 500 rally as counter-trend or corrective, moving against an incomplete decline which began in January of 2021. They remain medium term bearish with new trailing stops of 4431.00, and bare minimum downside expectations below last October’s 3491 low. Below 3491 TAG sees a confluence of downside attractions or objectives located near 3250 +/- 50, including the 50% Fibonacci retracement of the rise up off of the 2191 low (March 2020), as well as the equality projection of last year’s decline.

Eurointelligence

Can Sunak’s strategy possibly work?

Sunak has plenty of time to reshuffle political cards ahead of the general election. Wolfgang Münchau sees the beginnings of a Project Fear campaign, designed to expose Starmer’s flip-flopping on Brexit as an indication he’d do the same on his economic promises. Recently, Sunak’s postponement of the UK’s self-imposed climate change targets will be popular amongst Tory voters, but his image still remains the party’s biggest issue: Johnson supporters still regard him as a backstabber who ended up as PM in a typical Westminster coup, and he lacks charisma. Wolfang predicts Labour’s polling lead to fall, but sees an intriguing possibility of a coalition emerging between the party and the Lib Dems. Interestingly, Wolfgang believes that a hung parliament will make it de facto impossible for the Tories to ever return to power as a majority part, with coalitions from then on to eternity.

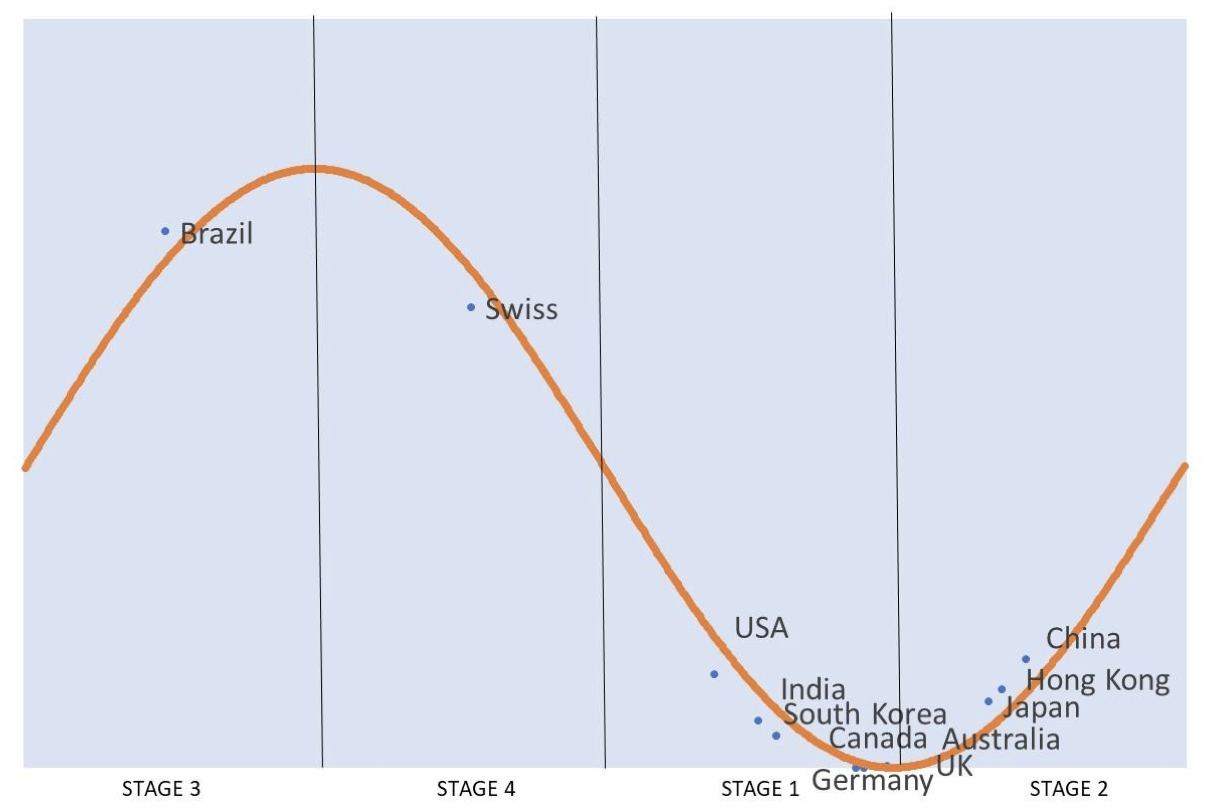

AAS Economics

UK and China: Beneficial, for now

The only changes this month in Frank Shostak’s business cycle sees both the UK and China edge into stage 2 of the cycle, denoting an environment more beneficial for equities. Historically, sectors in the UK that perform well in stage 2 include basic materials, energy and industrials. For China, look towards the likes of consumer discretionary, basic materials and technology. However, Frank points out that in both cases this will be short term as the cycle rotates back into the defensive stage 1 moving into 2024.

Talking Heads Macro

The Fed nails it!

The Fed delivered everything Manoj Pradhan wanted to see – hike(s?), a higher r* and a BoC-type reaction function. He nevertheless remains concerned at the lack of clarity being provided around how inflation will trend after it troughs – as he’s said time and time again, a soft landing is a great exit point for employment in this cycle and an extremely dangerous starting point for inflation in the next. He has no objection to closing the paid March 2024 position but prefers to halve it given that some things have yet to play out, such as the effects of higher oil prices. He also advises investors to remain SHORT bonds, LONG USD (vs SEK and PLN), and SHORT US equities vs Japan and China which both have macro dynamics with some independence from the global cycle.

Belkin Report

US: Overstimulated

The artificial economic and stock market boom ignited by excessive stimulus is over, claims Michael Belkin. Yet somewhat amusingly, markets seem obsessed with a strong economy and the prospect of more Fed rate hikes. The decline in bond markets seems to be preparing a 1987-style collapse setup for the stock market with the TLT TBond etf currently down -18% from its April 6th peak, while the NYFANG+ index is up +22%. Michael’s model also has a reversal forecast for the yield curve inversion. There is no excuse for getting caught in a collapsing speculative bubble when the Fed has been tightening and economy weakening; SELL and SHORT into brief stock market bounces and shift out of tech, consumer discretionary and industrials into ultra-defensive utilities, consumer staples and healthcare.

Greenmantle

Japan: Big changes ahead

As Niall Ferguson expected, the BoJ held policy steady with Governor Ueda’s comments indicating no change in approach. Niall’s base case remains that disinflation’s presence will remain in Japan for several more months, with core inflation stabilising at ~2% next year. Sometime soon, YCC will need to be scrapped, the benchmark rate increased to 0%, and a path fleshed out for the BoJ's massive asset purchase program. More forward guidance is almost certainly on the way in Q4 as Ueda eases the market into pricing in the momentous policy adjustment to come. Niall anticipates a yen rally and the continued steepening of the yield curve in Q4, He also recommends being LONG Japanese banks.

East Asia Econ

Korea: Still no export rebound

The September confidence surveys from the BOK don't give any clear indication of the direction of the cycle. Business sentiment ticked up, but no more than that, and shows no sign of breaking out of the subdued range it fell into early this year. Weighing on overall business sentiment is the continued weakness of confidence in manufacturing. This is important, continuing to suggest no imminent upturn in Korea's export sector. This sluggishness is more in line with Paul Cavey’s short-term model for the regional export cycle, and doesn't validate the decent upturn suggested by some financial market indicators.

Pennock Idea Hub

Is stagflation in our future?

Stagflation is not Ed Pennock’s base-case scenario, but a review of market leadership shows that the risk is rising and needs to be monitored carefully. In addition, stagflation could be exacerbated by disgruntled electorates turning to populist governments, which have shown to depress economic growth. Investors can hedge against such a scenario with a barbell exposure to commodity producers, US megacap growth stocks, based on the theme of buying growth in a growth-scarce world, and value and high-quality outside the US. Don’t be surprised to see a period of more relative weakness or consolidation before growth stocks can become the leadership again.

Emerging Markets

Totem Macro

Best EM alpha opportunities

Whitney Baker sees assets and FX in Brazil, Colombia, Chile and Peru as the most asymmetric EM alpha opportunities. There’s been some tactical inflows into these markets, mainly driven by long-only EM fund managers exiting China overweights and closing EM yielder underweights, but that certainly doesn’t mean the markets are overcrowded. The more structurally sustainable flows that will re-rate these assets still haven’t arrived. These assets have virtually never been cheaper, domestic growth is reaccelerating from sustainable levels, the inflation decline is durable, discount rates are falling, and risk positioning is extremely low. There is an alignment of ways to win in these assets that Whitney favours, and that’s without going into the particulars of flow and positioning drivers that she sees as enhancing this high-level alignment of bullish forces even further.

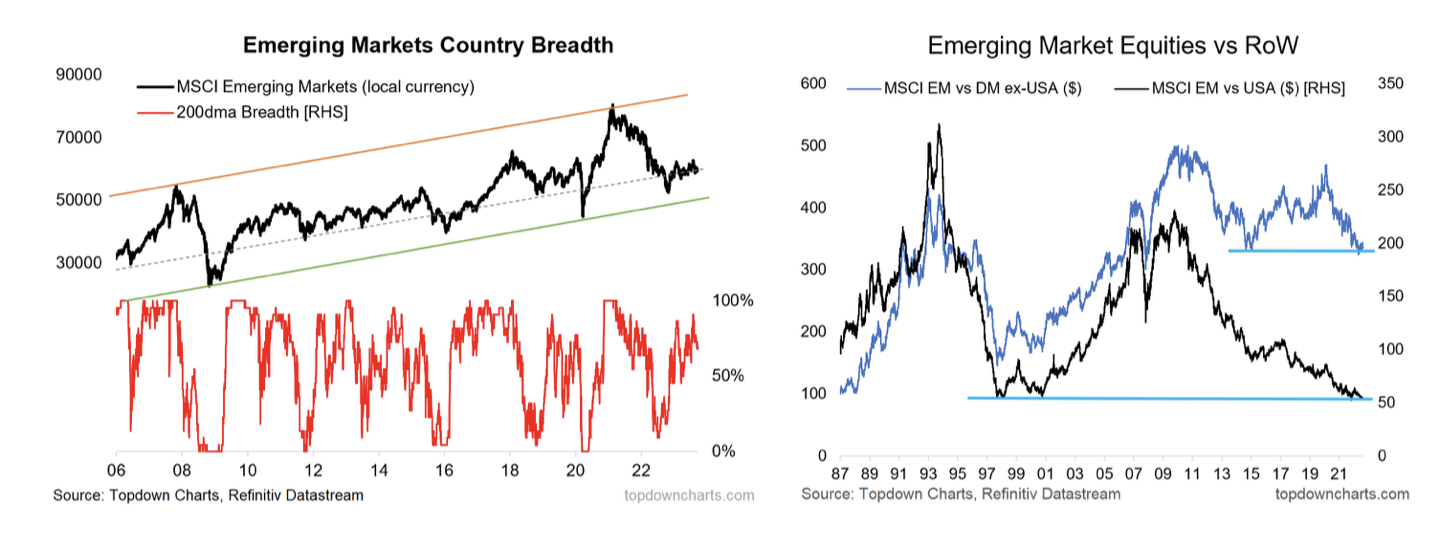

Topdown Charts

EM: Positive on all counts, just waiting for a catalyst

EM technicals have been mixed-to-positive with the MSCI EM index ticking along its long-term uptrend line with reasonably strong breadth, and the relative price line vs DM and US zeroing-in on a major long-term support level. Meanwhile the core case still stands: cheap valuations, bearish sentiment – i.e. contrarian bullish, and monetary conditions turning from previous major headwind as EM central banks pivot. USD remains a double-edged sword, with the YoY figure still negative but the DXY brushing up against a major resistance level. Overall, while technicals/value/sentiment/monetary factors are all improving, the still absent key upside catalyst would likely come in the form of a more meaningful pivot to easing by EM central banks, and ideally a weaker USD.

Eurizon SLJ Capital

China’s local government debt

China's property puzzle has investors on edge, but the picture is brighter than it appears. Local governments hold 54% of GDP in liabilities, while sovereign debt is just 22% of GDP. Managing property sector debt will require fiscal dexterity, with 2.5% of GDP in new local bond issuances annually. Yet with disciplined recovery efforts, the net cost may be only 15% of GDP. Reform, not crisis, awaits. Expect short-term uncertainty as Beijing asserts control over profligate local governments and streamlines their finances. But this is not Japan circa 1990; China's robust GDP and prudent macro policies provide buffers. China's resolute leadership could use this challenge to strengthen local government finances and set the stage for sustainable growth and prosperity.

Teneo

Indonesia: Instructional shortcomings may concern investors

Recent violent protests over land rights signal rising risks for natural resource and manufacturing companies in Indonesia. As the government pushes large projects like Xinyi's $11.5 billion glass complex, ancestral lands are being reallocated, igniting local grievances. Disputes over pay and safety have already turned deadly at some factories. While localised so far, these issues may spread as Indonesia expands minerals processing and manufacturing to attract foreign investors. Inadequate community engagement and resettlement plans risk further unrest. New entrants may be less prepared than established extractive firms to handle social issues. For investors, reputational and operational impacts warrant monitoring, even if national instability appears unlikely near-term. Proactive community and labour relations will be key to realising Indonesia's ambitions while avoiding violent conflicts.

Greenmantle

Polish roulette

Niall Ferguson sees a low probability that the ruling right-wing coalition led by Law and Justice (PiS) will secure a third consecutive majority on its own in the upcoming election. It is more likely that elections will result in a hung parliament. This will set off coalition negotiations, in which the far-right upstart party Konfederacja is likely to play kingmaker. The best outcome for Polish assets is if PiS falls short of an overall majority by a few seats only. In this case, it will persuade a few Konfederacja MPs to join its ranks. The worst outcome is if either PiS or liberal opposition party Civic Platform falls short of a majority by 8-10 seats or more, forcing either party to rely on Konfederacja for outside support. Such an arrangement may collapse quite quickly, leading to snap elections within 12 months.

Emerging Advisors Group

What’s wrong with Vietnam exports?

Vietnam exports have been hit particularly hard the last 12 months – Jonathan Anderson discusses if this is the end of the “new Asian tiger” story. He notes that the drop looks temporary rather than structural. There’s clearly been an unwind of US-bound "China cover trades" this year, but market share data from other trading partners are more sanguine - and new foreign investment continues to pile into the country. Thus, Jonathan is sticking with his growth exposure for now. The local economy and stock market have been a very volatile trade, but he continues to like medium-term exposure for the time being.

ESG

Verisk Maplecroft

Africa’s climate finance shortfall

The inaugural Africa Climate Summit, held in Nairobi, discussed how to close the continent’s finance gap. According to Maplecroft, USD$227bn/yr is needed to meet the continent’s 2030 climate goals, yet annual flows fall short by a staggering 89%. Climate-related investment will increase gradually until 2030, with the African Carbon Markets Iniative (ADMI) one such example. Yet, this falls short of what needs to be done. The continent’s high level of indebtedness and squeeze on financing has left the continent out of international capital markets, rather than project or country-level ESG risks being the cause. Should a balanced, acceptable fund be agreed upon at COP28 that will compensate poor nations for the impact of climate change, it will be an indication that further reforms are possible.

Capital Alpha Partners

The clean energy impact of a government shutdown

Even a brief government shutdown will likely delay key climate initiatives like Treasury guidance on IRA clean energy tax credits, DOE hydrogen hub grants, and administrative regulations. Multiple shutdowns possible until next year would compound delays. Sustainable aviation fuel guidance and hydrogen hub announcements seem particularly at risk. Moreover, with an open 2024 election likely, further regulatory delays increase the risk of Congressional Review Act challenges in 2025. Thus, shutdown-related stagnation could have an outsized impact on climate policy implementation. Even minor disruptions could reverberate given the pivotal policy juncture. Delays may frustrate climate action advocates despite legislative progress, highlighting the critical importance of steady administrative execution.

Commodities

Global Mining Research

Copper vs Gold

Gold miners have traditionally been considered premium rated miners, yet copper stocks covered by GMR have moved to a premium compared to gold and other base metal and bulk miners. Gold stocks are out of favour with valuations underperforming the gold metal price during 2023; the high beta of gold stocks presents an opportunity when the gold price gains traction. Preferred equities include Lundin Gold and Northern Star. Copper stocks remain attractive as supply weakness and low inventories are offset by macro concerns. Preferred stocks are Atalaya Mining and Taseko Mines as junior miners, and Sandfire amongst the mid-larger names.

Totem Macro

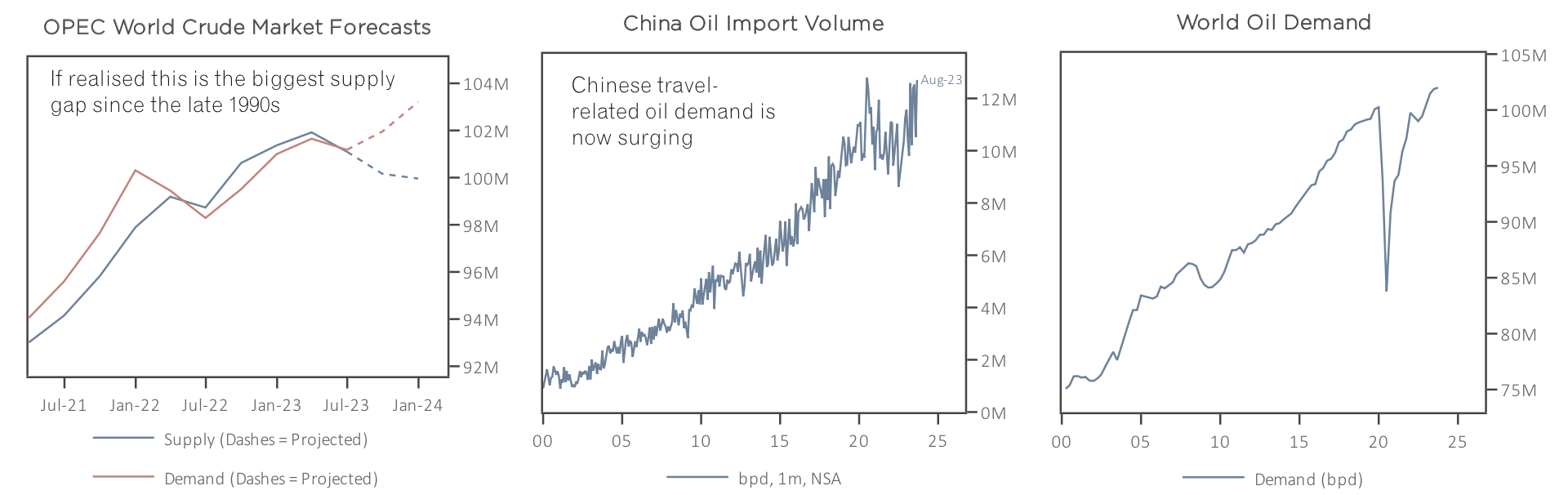

Will oil’s strength continue?

We are in the throes of the oil strength that Whitney Baker expected this year, who believes it’s sustainable. What’s fundamentally happening here is an alignment of bullish forces, from the global economy reaccelerating to extremely constrained incremental oil supply. We’ve also seen China show up to the travel party, driving up related oil demand (see chart). On top of that, oil is both a driver of, and the best hedge against, inflation driven by cyclical overheating, and as prices rise further Whitney expects financial and inflation-hedge oil demand to continue to stoke the fire.

CPM Group

Metals selloff – what’s next?

The Federal Reserve reiterated its view of a stronger economy, and the likelihood that interest rates would stay high. As expected, this announcement was followed by a strong selloff in financial markets including gold, silver, platinum, and palladium. CPM Group's Jeffrey Christian discusses what comes next for the economy and various financial markets. He goes into detail on the historical price movement for gold, silver, platinum, and palladium, as well as CPM Group's expectations for the metals going forward.

Click here to watch.