Company & Sector Research

Europe

DayByDay

Luxury downside

The MSCI Europe Textiles, Apparel and Luxury Goods Index accelerated to the downside last week - Valérie Gastaldy points out that prices have already fallen below the 38% Fibo since 2022 (at 1325). Should the index correct the rally since 2020, the most reasonable target would be 1207. However, should we be correcting the move since 2009, then the target would be 1020. Re. individual stocks, Hermes is trying to break below its summer lows and the next level where Valérie would consider buying LVMH is at €665. She has set major medium-term support for Moncler at €53.3, but the stock is weaker than the other two and can more easily fall significantly lower if the other two do break equivalent supports.

ResearchGreece

Unfortunately, ELPE does not have a naphtha reformer to take advantage of the huge naphtha-gasoline cracks ($35/bbl in Q2), nor a big enough RES mass (yet) to offset at least part of the weakness in refining. Unless refining margins stay close to $15/bbl beyond 2023, the company’s EBITDA will be going significantly down. With the shares looking expensive in EV/EBITDA terms (8.5x-9.5x 2024-2025E) and the dividend yield not big enough to justify current trading levels, ResearchGreece remains bearish. They now expect clean 2023/2024/2025 EBITDA at €1.03bn/€513m/€547m and see equity cash flow at €140m in 2023 and a negative €65m in 2024.

the IDEA!

Is the business model broken? Analysts at the IDEA! don't think so. The company's clear underperformance against the stock indices is driven by its lacklustre FCF generation that is largely caused by its working capital development or to be more precise by its inventories. When AALB can make real progress getting better control over its inventories / working capital (first signs are already visible) it should be able to recoup most of the lost FCF. the IDEA! models FCF of c.€1.2bn (excl. lease payments) in the period 2023 to 2025. TP €50.15 (~40% upside).

Holland Advisors

Andrew Hollingworth wonders how many AHT observers really understand the financial model of the company and the powerful compounding it will likely result in. If you were offered to invest in a company with a high likelihood of it growing turnover at 13% p.a., EPS at 18% p.a. & receiving a 1.5% p.a. dividend yield, what price might you be prepared to pay? Andrew suggests a 15x multiple offers much value vs. that prospect. These are the growth rate metrics that AHT has achieved in the 8 years between 2015 and 2023 and 15x is the multiple of 3/24 earnings it changes hands for today. The future, of course is different to the past…or is it? He sees a realistic prospect of 20% investor IRR’s.

Copley Fund Research

Ownership levels move to all-time highs in the stock after significant rotation from global managers - a record 26.9% of the global funds in Steven Holden’s analysis now hold a position, pushing the net overweight to a 7-year high. Over the last 6 months, these moves have been among the largest among global Materials sector peers. LIN captured the largest increase in average weight, the largest overweight move and the most funds switching from underweight to overweight. Only Shin-Etsu Chemical saw a larger increase in funds invested. This was most definitely an active rotation.

MYST Advisors

Massive narrative change amid breathtaking earnings miss - risk:reward remains unattractive despite a ~55% drop in ADYEN’s share price. This is a deteriorating business with a disingenuous management team. Payment processing is a commodity and competition is intensifying. Further margin declines are anticipated. Sell-side numbers remain too high. Growth rate is the key KPI - if ADYEN is growing at ~15% (or likely lower) then the stock is worth ~€600/share. Prefers companies trading at legacy multiples with more vertical software.

North America

Cerundolo Investment Research

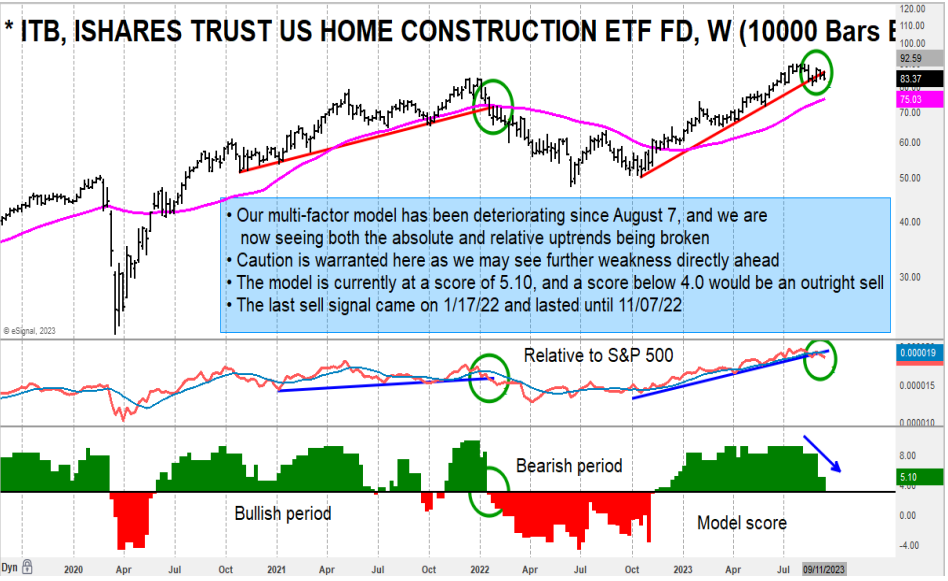

Home Construction ETF (ITB)

Guy Cerundolo ranked and reviewed the constituents of the ITB and found a 10% reduction in the number of stocks with a bullish multi-factor model score from a 1-month look back. At the end of July, he had 79% of the constituents with a positive score compared to 69% now. Some of the stocks had a large negative step size drop in their score and the largest weighted stock in the ETF, DR Horton, is one of them - DHI's share price is beginning to show signs of weakness with both the absolute and relative uptrends being broken.

Verbatim Advisory Group

Weakening trends - Verbatim's HD US Aug Comp Estimate is -3.5% vs. 2Q23 Actual Comp of -2.0%. Traffic levels are declining and customer spending is being negatively impacted by inflation, which is making customers focus more on essential spending. Click here to access the full report which also includes details on HD's inventory levels, promotions, market share and best selling products last month.

JJK Research Associates

Much stronger merchandising execution - CK’s assortments continue to evolve across hero products as well as the development of more compelling wear to work, non-denim bottoms and activewear assortments. JJK sees this as returning to the brand’s minimalist roots, which is better differentiating CK’s positioning with Gen Z and millennial target markets. In addition, TH’s classic positioning has been elevated across the brand’s polo shirt collection, wear to work and now relevant casual / activewear assortments. JJK models +4.5% FY23 revenue and EPS >$10.75 (vs. $10.35 guidance). Looking into FY24 they expect +MSD top line gains and EPS of $12.20 as EBIT margin improves to 10.7%.

Northcoast Research

Improved performance metrics at Burger King US and Tim Hortons Canada, aided by a sizable war chest to recover lost market share should sustain performance improvements going forward. Jim Sanderson believes the current share price does not reflect the long-term potential ahead for QSR, providing an entry-point to invest in this turnaround opportunity alongside veteran QSR executive and company Chairman Patrick Doyle. Jim raises his 2023E non-GAAP EPS to $3.20 (from $3.01) and 2024E to $3.43 (from $3.23). TP $86 (25% upside).

Real Street Retail Research

North American sales trends are increasingly disconnected from the US Beauty market. As inventory mounts in TJX & Costco and once forbidden discounts ramp up on DTC sites and department stores, the prospect of a meaningful turnaround in the medium term is in question. Distribution expansion at Ulta Beauty, Ulta @ Target and Sephora @ Kohl's, has not slowed the share bleed and a new generation of prestige brands has traction in the market. The outlook for this once dominant portfolio of legacy brands in the US is murky at best as the critical Holiday '23 season approaches.

Alumbra Research

The share price declined by 22% last month (and is down 41% since Derek Aherne turned bearish) after DOCS significantly reduced its FY24 revenue guidance. In Derek’s previous reports, he raised concerns that consensus revenue growth expectations appeared overly optimistic considering the firm’s declining NRR rate and net deferred revenue level. In addition, he believed that management’s decision to cease disclosing growth in the average number of modules and brands for its Marketing Solutions customers was a red flag given that they were expected to be key drivers of the company’s revenue growth and growth in these metrics had been deteriorating prior to the removal of the disclosure.

Thompson Research Group

TRG has maintained a bullish view of GVA in the past few years, as the company worked down its Old Risk Portfolio and executed on a low-risk consistent growth strategy. The stock is valued at ~5x EV/EBITDA, which TRG believes is overly punitive and lumps it in with Fluor and Tutor Perini. They believe this is the wrong peer set. Instead, GVA should be compared to Construction Partners and Knife River, who sell at ~10x EV/EBITDA. These three companies have vertically integrated operations (materials producers + contracting services). ROAD and KNF have consistently produced better margins than GVA, but GVA’s 2024 targets show that it can close that gap.

Global Mining Research

ALB sweetens its offer for Liontown to A$3.00/share, a significant premium to its initial reported offer of A$2.20/share in Oct 22. ALB’s persistent interest in LTR points to a long-term plan that would secure stakes in 3 of the top 5 Australian spodumene mines, while it also reduces Chilean exposure and increases US FTA compliant production. However, the downside is that it is a full price being paid, leveraging the balance sheet and likely locking ALB out of other moves, at least for a few years. GMR maintains their Sell rating on the stock.

ETR

Generative AI & Microsoft Copilot

The ETR Insights team recently hosted a Generative AI panel discussing use cases within the enterprise, the extent to which certain companies have already adopted these technologies and the pain points associated with this process. A few key takeaways include: 1) All panellists seemed comfortable with the price points mentioned (e.g., $30 user/month for MS 365 Copilot) and felt confident in their ability to show ROI on these investments. 2) Panellists felt mostly ready to put GenAI to work at scale from an infrastructure standpoint. 3) A few panellists noted substantial overlap between their RPA use cases and their plans for GenAI tools - could GenAI now be leapfrogging RPA?

Ingenuity

Semiconductors: No H2 recovery as foundry outlook worsens

Q2 clearly marked a turning point in the global semiconductor downturn with four out of the eight key segments Ingenuity monitors showing sequential growth and another two (smartphone & server) just barely missing the cut. WFE and Foundry were the outliers with both showing sequential declines. However, before anyone gets too excited about this positive turn of events, it’s important to keep in mind that the y/y comparisons remain in the red across the board. Furthermore, while the silicon wafer and memory segments both showed positive sequential developments, their problems are far from over. Finally, TSMC’s deteriorating FY23 outlook, despite an ongoing Nvidia-driven boost, underscores the reality that there is no H2 rebound on the horizon.

Japan

Asymmetric Advisors

This electrical engineering company is a key beneficiary of investment in new fabs in Japan as the largest proportion is focused in Kyudenko’s home region of Kyushu. Sales recognition from large projects undertaken 3-4 years ago that resulted in low profitability after raw material and labour costs spiked are disappearing and cost pass through means higher margins on newer projects are starting to feed through. Despite a surge in orders since H2 last year, an anticipated step up in earnings and increasing shareholder returns (cash is >¥100bn vs. ¥300bn MCap), the stock trades on a forward PER of <10x - a low valuation for the obvious positives.

Emerging Markets

Crystal Shore Alpha

GTAsia Top 10 Stocks delivers eye-opening returns in falling markets

Asia EM has been clobbered over the past 30 months, down -35% since the mid-Feb 2021 high. Crystal Shore Dashboards (CSD) launched their GTAsia Top 10 Stocks on 14th Feb 2022, right in the middle of this meltdown and have generated a positive return: +10% vs. MSCI EM Asia at -21%. CSD achieved this result by systematically ranking 960 EM Asia stocks on a weekly basis. They then ran a macro overlay on these quintile rankings using their Asia country risk scores. Their top 3 performing stocks today: Aurobindo Pharma (+40% since purchase), Gail India (+14%) and Indian Railway Catering & Tourism (+13%).

AlphaMena

Amid a still-challenging macroeconomic context, STC continues to show strong resilience. The group recorded its highest semi-annual revenues ever in 1H23 at SAR36.506bn (+8.2%). The bottom line also appreciated by 4.2% at SAR6.117bn. STC preserves a generous dividend policy with an attractive regular dividend and high payout ratio which reflects the group’s sound financial position and solid cash flow. STC is a quality stock with a robust business model backed by the company’s leading position in Saudi Arabia, its solid fundamentals and steady investment programme. The group’s recent external growth strategy (e.g., the 9.9% stake acquisition in Telefonica) also provides a positive outlook and will improve shareholder returns in the long run.

Aequitas Research

China’s largest express delivery company aims to raise around US$2-3bn in its H-share listing. Sumeet Singh notes how SFH doesn’t appear to be in an imminent need for cash. However, with several logistics focused companies lining up to list, the company is probably trying to jump the queue before the likes of Cainiao sucks up liquidity. Should SFH decide to go ahead with its H-share listing, it will have to offer a discount, as past A/H listings haven’t had a very great post-listing performance track record. Furthermore, positive trends in revenue growth and gross profit over the last few years (driven by its Supply Chain and International business) have reversed in 2023.

Lynx Equity Strategies

Huawei appears to have adapted its internal 5G modem to a novel 7nm process, one which eliminates the need for the industry-standard usage of FinFET transistors. KC Rajkumar finds it remarkable that SMIC may have been able to control the leakage profile of planar transistors just enough to make it possible for the Mate 60’s 5G modem to operate without obvious issues. The SMIC / Huawei 5G handset demonstrates that the expensive FinFET process may be unnecessary. A few years out, if mid-tier foundries were to duplicate the SMIC planar process, there could be risk to 7nm loading at TSMC.

Macro Research

Developed Markets

Aitken Advisors

A stern test lies ahead for markets

James Aitken is uncomfortable with the idea that we are really close to ‘peak central bank rates’ and still struggles to believe monetary policy is sufficiently restrictive. As such, he believes a stern test lies ahead for markets as a combination of higher real policy rates and higher real yields starts to act as a headwind for markets, and a handbrake on growth. James still believes the market-clearing price for treasury coupons is lower (price down, yields up) and a ten-year treasury at, say, 4.8%/5.0% wouldn’t be wildly out of line with US nominal GDP at a still high 5-7%. He also advises investors to add high FCF oil & gas businesses, short-dated gilts (out to 5 years) and possible longer-dated gilts should better news on growth and inflation come out.

New Normal Consulting

Chemical reaction

Paul Hodges has long viewed chemicals as the best leading indicator for the global economy. Right now, it’s flashing red warning signals. INEOS, a widely-respected company in the industry, confirmed the widespread nature of the chemicals downturn, with lower margins, higher inventory holding costs and lower volumes across their businesses. They’re not alone, with BASF seeing a significant profit fall of more than 75%. It is a situation clearly reminiscent of 2008, when warnings about the risk from the US subprime market were ignored until it was too late. Hopes of avoiding recession are misplaced.

Pennock Idea Hub

Investing in an era of fiscal dominance

The big idea at this year’s Jackson Hole symposium was fiscal dominance, or the problem of big government deficits and skyrocketing debt around the world. For central banks, this presents a problem of potential finance instability as governments will have less fiscal room to deal with the next crisis, requiring monetary policy to step in and do more of the heavy lifting. For investors, this creates an environment of greater cross-asset volatility. Investors may want to re-think how they approach risk in portfolio construction, as estimates based on historical data may no longer be applicable. It is time to recalibrate the effects of diversification and how possible crises may affect cross-asset volatility.

Malmgren Glinsman Partners

US: Daunting fiscal risks

"How will the mammoth US government debt be managed in the 15 months leading up to the 2024 national elections?" asks Harald Malmgren. The US Treasury have announced it expects to borrow another $1,007bn from private markets in Q3, with a further $852bn in Q4. Such numbers are done with the assumption of no recession, yet tax receipts have been declining in recent weeks as economic activity sags. US debt payments are on an unsustainable path (see chart). In his latest report, Harald explores the different paths the future may take which will impact on US spending, with a deep insight into defence spending. Amazingly, some possibilities, such as the US Treasury needing to develop an emergency debt management programme after the US finds itself entangled in an armed conflict, have been given virtually no thought by congress or mainstream journalism.

Steno Research

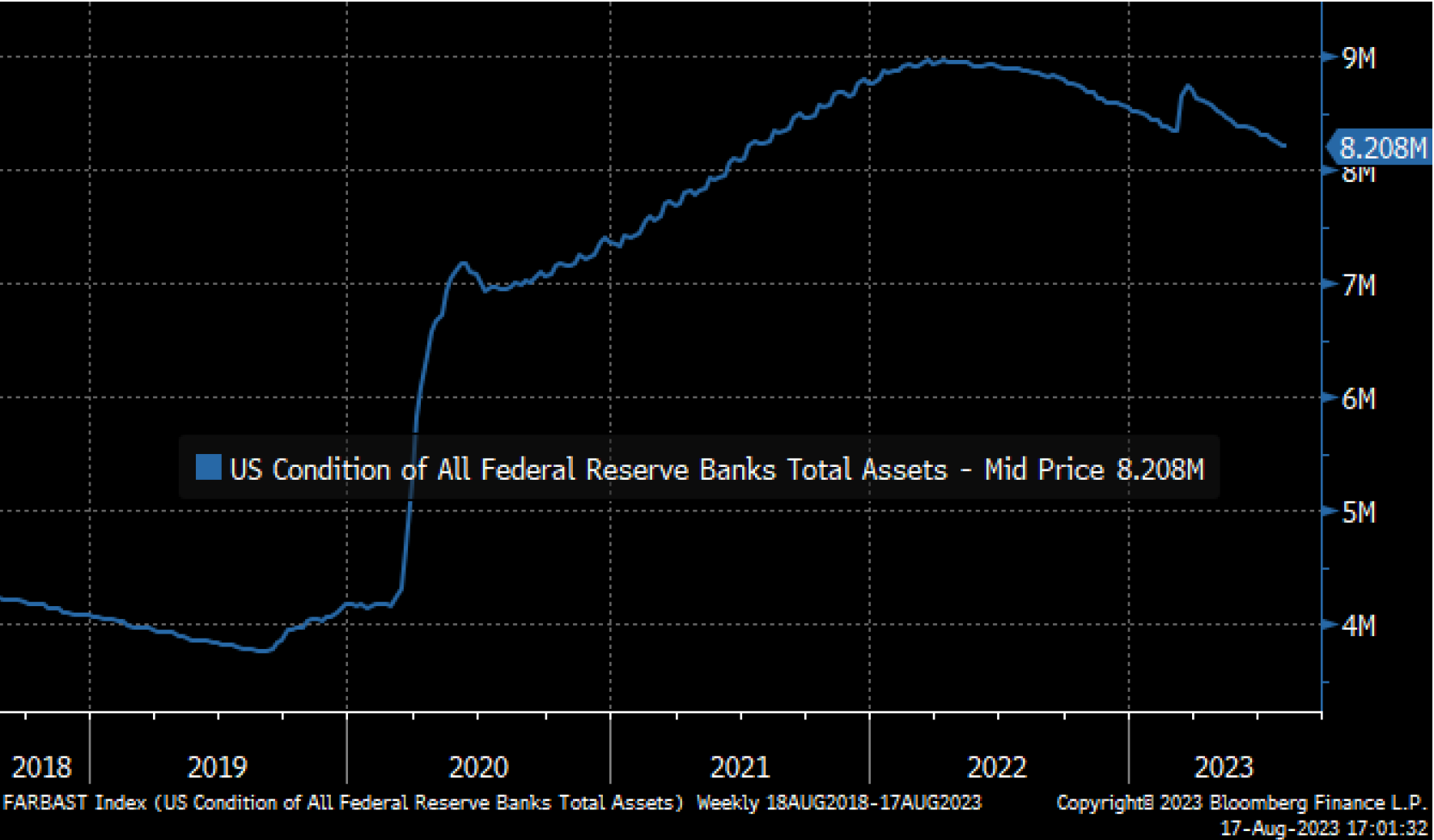

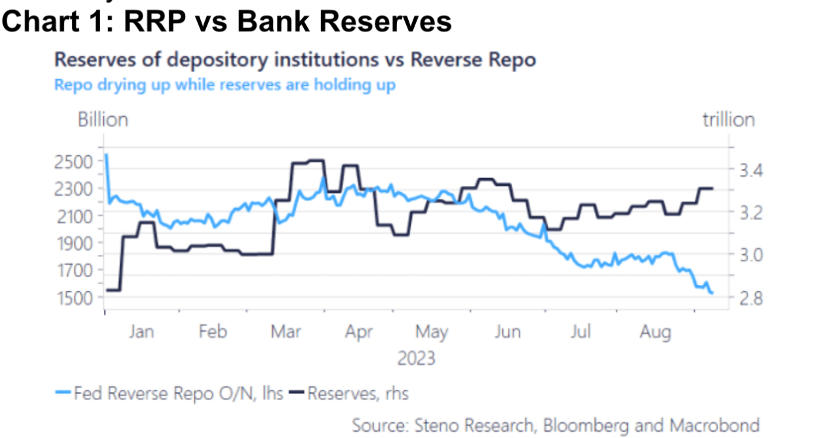

US: Risky business

The Fed released its H4 recently, which bears some interesting insights into the state of the US banking sector. The Reverse Repo facility has been squashed since May while the bank reserves have remained relatively stable. The banks’ continued caution throughout the summer is not at all surprising, and continued risk-averse attitudes will persist in the coming quarters. They are operating under the assumption the risk profile of existing loan portfolios will worsen as the economy cools, and most banks are consequently ramping up their respective allowance for loan and lease losses (ALLL) estimates.

Quill Intelligence

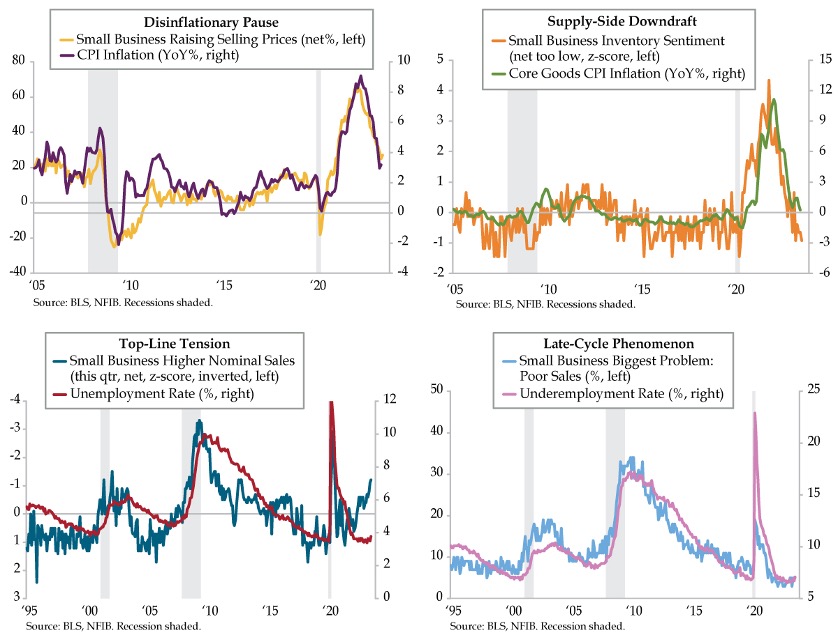

US: Small businesses flag destocking and rising unemployment

Small businesses are pointing to a disinflationary pause in the CPI trend. Nonetheless, a shift from oversupply to undersupply conditions suggests core goods inflation could transition from disinflation to deflation in the coming months. Main Street is also challenging the low unemployment picture with progressively deteriorating results regarding current revenues, while concerns about sales are no longer sitting at cycle lows. The recession narrative continues to be a value trade.

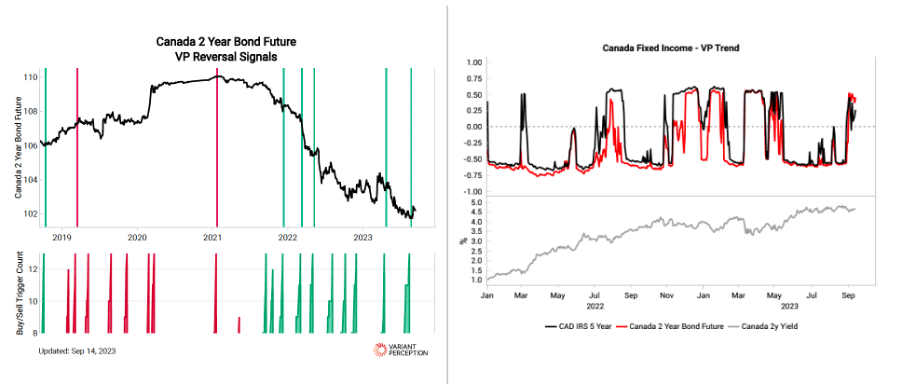

Variant Perception

Canada: Tactical aligns

Variant Perception’s inflation and growth leading indicators continue to drop, and small business delinquencies are picking up showing monetary tightening is starting to gain traction. Cyclical global headwinds for the economy are present. Tactically (1-3mth outlook) both the trend and mean-reversion components in Variant Perception’s Tactical Outlook framework are now bullish (price higher, yields lower) on Canadian front-end and the belly (5y, see chart). In the context of the BoC pause this month, this creates an attractive entry point to buy Canadian front-end & belly or receive in swap space. Cyclically (6-12mth outlook), downside risks are clear.

High Frequency Economics

Japan: No pretty pictures

According to Carl Weinberg, there are no pretty pictures to be found in Japan’s latest economic data releases. Machine tool orders (down 17.6% year-on-year in August) are extending their slump. Most likely, this related to the decline of global demand for everything, as evidenced by the decline in world imports. Increased competition from China and other low-cost manufacturing economies also does not help. On the monetary data, the figures for M2 simply speak for themselves: monetary growth of 2.5% year-on-year cannot possibly accommodate an inflation target of 2% with any economic growth in real terms.

Emerging Markets

Talking Heads Macro

China: Cyclical fundamentals not as bad, policy creeping in

Manoj Pradhan has long been a bear on China, arguing for years that the country’s economy would go sideways at best. Without fundamentals working in tandem, China equities have little upside. Cyclical fundamentals, however, aren’t as bad as markets think. As a result, a massive equity stimulus isn’t necessary to get the economy back to a somewhat sound footing and the steady stream of measures we are now beginning to see should work. Stay LONG China equities as the market still remains oversold. Keep LONG USD/CNH, but switch CNH’s role to a hedge after a superb run from a change in the China view from May.

PRC Macro

China: Beijing all in to avert property and RMB fallout

The PBoC slashed the FX reserve requirement from 6% to 4% in a bid to curb the pace of RMB depreciation, but William Hess sees this only as a down payment and expects the central bank to further escalate intervention before early Q4. He reiterates the view that the previous high for USD/CNY of 7.37 is a line in the sand for the PBoC. Beijing also announced a series of new measures to boost consumption and property demand, which may not be sufficient to stimulate new demand but may tap into pent-up demand. Expect additional measures to bolster property market in September.

Greenmantle

Brazil’s looming China question

Going into 2H23, Niall Ferguson sees an improving outlook for Brazil’s economy. Brazil’s new fiscal framework and the prospect of further interest rate cuts have helped. Further, consumer confidence has reached a nine-year high. There is likely more good news for the economy to come, as the Brazilian Central Bank prepares to cut rates further. In the medium run, Brazil is also well placed, compared to its neighbours, to withstand the impact of a Chinese slowdown. At the same time, Niall is mindful that the Lula administration must overcome significant political stumbling blocks if it is to restore real stability to public finances.

Intelligence Research

Mexico: Draft budget projects continued strength for peso

Mexico’s finance minister has presented the government’s draft 2024 budget to the federal congress. The budget proposal, for some M$9.02trn (US$515bn), represents a 4.3% increase in real terms on that approved for 2023, and is made up of M$6.4trn corresponding to paid programmable spending and M$2.6trn associated with non-programmable spending, which includes the financial cost of the debt, and contributions to states and municipalities. The budget forecasts economic growth of between 2.5% and 3.5% next year, with annual inflation forecast at 3.8%, which would bring it within the target range of Mexico’s central bank (Banxico). The draft budget also estimates the exchange rate for the Mexican peso at 17.10 pesos per US dollar by the end of 2024, signalling continued strength for the currency.

Bondcritic

Thailand: The empire strikes back

The Pheu Thai Party (PTP) decided to betray its voters to cross the aisle to join the conservative side, which will call for turmoil on the street. In the near term, however, the clear political picture is by all means positive for Thai stocks, especially companies which could be subject to reforms proposed by the MFP. PM Thavisin’s past experience should also be positive for real estate, retail and tourism in the near term. The PTP’s populist policy of giving money to every adult next year should give rise to near-term inflation, negative for THB bonds which have remained expensive. Thai politics has entered unchartered territory and Warut Promboon sees this as negative in the long run - the potential surge in Thai stock performance should be the time to de-risk.

Grey Investment

India: Quite nifty

Since 2008, the NIFTY 50 index has advanced in a 15-year up-channel. The new all time high, set last week, should result in another advance into the resistance zone, which starts around 23,400 (see chart 1). The index’s weekly chart shows the index moving away from resistance at 18,350-18,888, a barrier for 20-months. A weekly close above 20,192 would confirm the breakout above the resistance zone, supporting the bullish month chart target of 23,400+ (see chart 2). If that occurs, the support will move up to a weekly close below 19,032. The team remain 50% LONG the BSE 500 in USD terms.

ESG

Metals Focus

Gold ESG Focus 2023

Metals Focus recently published their latest gold mining ESG report, covering 17 of the biggest gold miners from 2014-22. It revealed that combined scope 1 and 2 greenhouse gas emissions fell by 2% y/y in 2022, partly a result of company initiatives to cut emissions and reliance on fossil fuels. The total combined emissions for the gold mining industry as a whole are estimated at 0.3% of global emissions. Water withdrawals fell 7% and water consumption by 3%, but miners need to further improve water management, especially in regions of water scarcity. Spending on community projects rose markedly, seeing a 37% improvement.

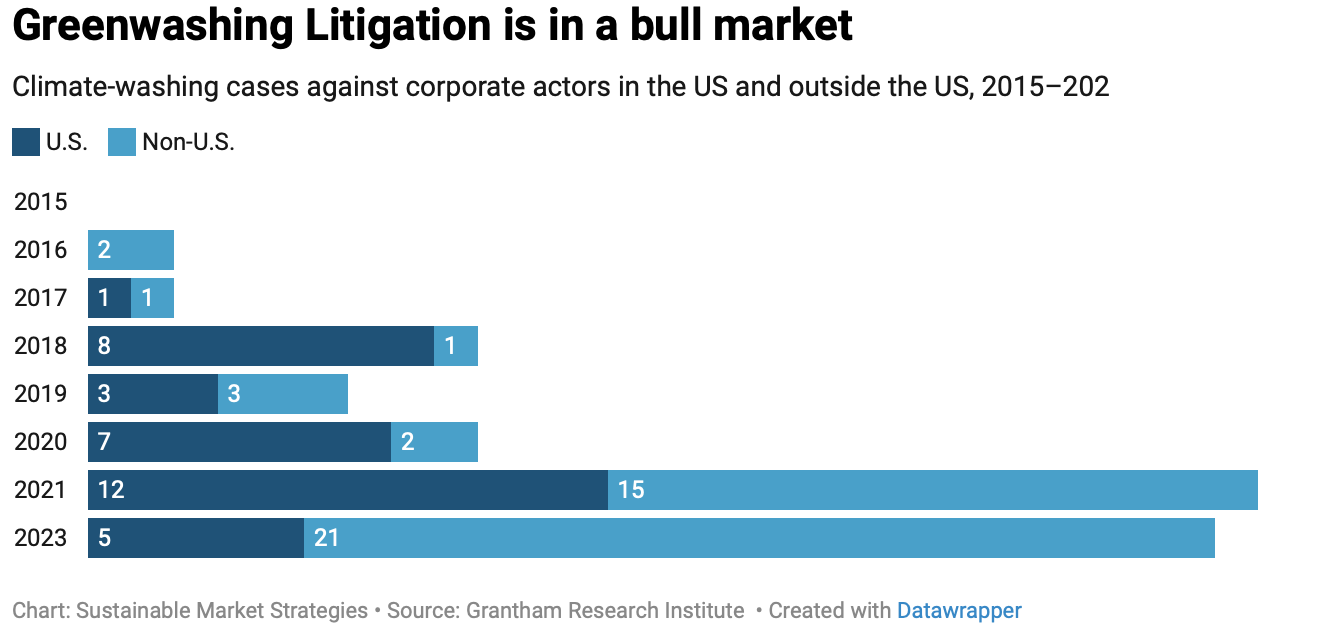

Sustainable Market Strategies

Washing: Beyond green stains

Green – and other colour – washing attempts to mislead consumers into making seemingly sustainable choices that have minimal positive impact and diverts resources away from genuinely sustainable practices. Case studies suggest that today, the net present value of greenwashing is positive: the financial reward for investing in green, fraudulent marketing campaigns is higher than the potential penalty of getting caught. However, a recent surge in litigation as well as broader authority from securities regulators suggest the likelihood of getting caught – and penalised – is growing rapidly (see chart). This implies that washing will become a more material risk to investors.

Commodities

Longview Economics

Natural gas: Winter is coming

Despite popular opinion, high gas stockpiles are not, on their own, enough to insulate Europe against tight energy markets this winter. Total European storage capacity is equivalent to just 30-40% of typical winter consumption. We will see European stockpiles be significantly drawn down by the end of this winter, with stockpiles reduced to ~27% of capacity. This will leave the continent vulnerable to an energy shortage in winter 2024-25. That is, in the absence of stronger production and/or imports, and even in a relatively soft demand scenario in the winter months, there is a potential of an inventory drawdown theoretically to zero by the end of the cold season.

Queen Anne's Gate Capital

China: Property sector’s decline will hit commodities

Whilst China’s economy is the world’s second largest, Kathleen Kelley comments that it represents an outsized portion of commodity demand used in building and infrastructure. With growth slowing and the appetite for stimulus small in comparison to 2008, commodities will take a hit. Expect metals to be the worst hit, with the property market making up 33% of Chinese iron ore demand, 24% of copper, 25% of aluminium and 65% of zinc. Nickel will also suffer. Even the much-hyped energy transition demand isn’t big enough to plug the hole left by the declining property sector. Oil, which has remained immune to the property sector slowdown, and natural gas demand will rise in 2024, but at a much slower rate.

ERA Research

Lumber outlook

Pricing trends were mixed across North American lumber markets last week, with SYP 2x4s increasing by a further $27 w/w to $423, while prices for S-P-F 2x4s, along with most other species and dimensions, drifted lower (-$2 to $418). Sweltering conditions in key US South building markets continue to stymie consumption in the region, while persistently high mortgage rates (hovering around 7%) are expected to put a chill on homebuilding activity through the balance of the year. The ERA team anticipate that lumber prices will be rangebound around current levels until the inventory build-up for next spring’s construction season.