Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

Europe

Interim results looked good - revenue was up 11% with Insurance particularly strong. There was a sharp increase in margins and management guided to the top of the range. Analysts have put through some meaningful upgrades for Y1 and Y2, but the share price has fallen markedly since then. Willis Welby continues to be bullish. There is a decent growth model and a good financial model. The balance sheet is strong. The implied to Y3 EBITM ratio of just 50 is too low. They see MONY, along with Next 15 and Team17, as prime candidates to be taken over by Private Equity.

JL Warren Capital

2023 stands to be a year of resetting for luxury brands and the best hope is that 2024 builds on a moderate comp in a stabilised economy.

LVMH - sales in mainland China are estimated to have declined 5-10% Y/Y in Jul (first month of negative comp YTD). Aug decline has accelerated but could narrow as Chinese V-Day approaches. Macau and HK continue to boom on overseas buying by Chinese tourists.

Gucci - China sales have collapsed and the brand lags peers, likely due to its bold and loud design used to attract entry-level, younger shoppers going out of fashion. Gucci's deep double-digit decline could improve in Q4 as its new designer launches a new season and easy comp kicks in. However, the fundamental issue of losing share in a down market is likely to take time to address.

Starling Advisors

Q1 results proved that the long trade into numbers was crowded as the shares fell 10% despite a strong performance. However, Alex Dwek believes the investment thesis remains intact. Cartier and Van Cleef continue to gain market share in a branded fine jewellery category that remains fundamentally attractive. The 1) comeback of the Chinese consumer, 2) strong pricing power and 3) continued luxury consumer appetite for CFR's timeless and iconic jewellery and watches should enable it to navigate well in a period of softening US demand. CFR has shown in the past its ability to anticipate market and regional trends and redeploy efficiently. At 17.9x, the stock currently trades close to 1 SD below its 10-year historical mean P/E.

New CEO Hein Schumacher will have a hard time creating shareholder value as he is stretching beyond his depth during a time of intense household budgetary pressures, rising input costs and pressure from an activist investor. Although Schumacher has global experience, ULVR is several times larger than any business he has previously run and faces specific challenges (margin pressure, a new operating structure and decisions on which long-term brands to own). Paragon’s research includes interviews with Schumacher’s former colleagues; while they gave him the highest rating for financial acumen and integrity, this was countered by his abrasiveness and weak self-awareness.

The bank has reported a super strong set of Q2 results, driven by the wide(r) loan-deposit rate asymmetry boosting NII +21% Q/Q / +164% Y/Y, with clean RoTE at 25% (vs. 21% in Q1). ResearchGreece raises their 2023 RoTE estimate to 19.6% (vs. management guidance of >17%) and reiterates their OWN IT (OI) rating with a TP of €5.9 (100% upside). Unless earnings are hit by a windfall tax, they expect the 30% minimum pay-out guidance to equal a 9% dividend yield next year and rise closer to 10% by 2025; shareholders will be pocketing c.30% of the bank’s M/Cap in the form of dividends during 2023-25.

Reports a mixed set of H1 results with strong top-line growth but weaker margins. Forensic Alpha’s analysis focuses on inventories which continues to rise from what were already-high levels at the end of FY22 (currently stands at $2.4bn). The provision against this inventory balance is now a massive $576m and not surprisingly was identified as a "Key Audit Matter" in KPMG's report for FY22. While management has been very open about this issue, the bull thesis relies on a strong improvement in margins in H2, but this could be derailed in the event the company is forced into making write-downs and / or additional provisions.

North America

According to CTFN’s industry sources, DISH’s merger with satellite communications company SATS is unlikely to face burdensome regulatory hurdles at the US Federal Communications Commission and is expected to be received as an effort by the acquirer to meet its upcoming 5G buildout deadline. The merger will allow both parties to combine the expertise and financial assets of SATS while allowing DISH to raise additional capital. While rival telecom players can be expected to oppose the deal, these concerns will not have much sway at the agencies as the parties involved will argue that DISH is a new entrant in the wireless business trying to compete against incumbents.

Brian McGough sees more cross currents around NKE today and critical questions that need to be answered than at any time in the three decades that he has covered the stock (and worked at the company). His analysis focuses on NKE’s historical “super cycles”, where it comes off an investing period and accelerates market share, which he thinks is happening now. These cycles tend to last 3-5 years. Brian believes NKE will overdeliver on revenue, margins and EPS this year by a wide margin, and that it is a "must own" stock. TP $180 (65% upside).

Deja-vu to Mar 2019 when Chuck Grom first upgraded the stock to Buy - he sees a similar inflection point in the maturation of the business with the company clearly focused on improved profitability all while revenue trends in both e-commerce and home furnishings appear to be now bottoming out (with potential for a return to sustainable sales growth starting in 3Q23). Further, and equally important, as this was a case for his prior Hold-Rating, the company has significantly pulled back on promotional activity from Apr/May levels. Using a 1.0x P/S ratio, Chuck has a TP of $110 (55% upside).

TPL captured more water business in Q2 than ever before leading to revenue and earnings exceeding Hamed Khorsand’s expectations. The stock has been mostly trading with the price of crude oil, but non-oil and gas revenue is nearly 50% of total revenue, creating a business model that has effectively hedged the volatility related to energy prices. Hamed believes this change in revenue mix should lead to a higher valuation. He forecasts FY23 revenue of $619.9m and net income of $383.6m, or $49.83 per share. The increase in the cash balance should lead to more shares being repurchased. TP $2750 (45% upside).

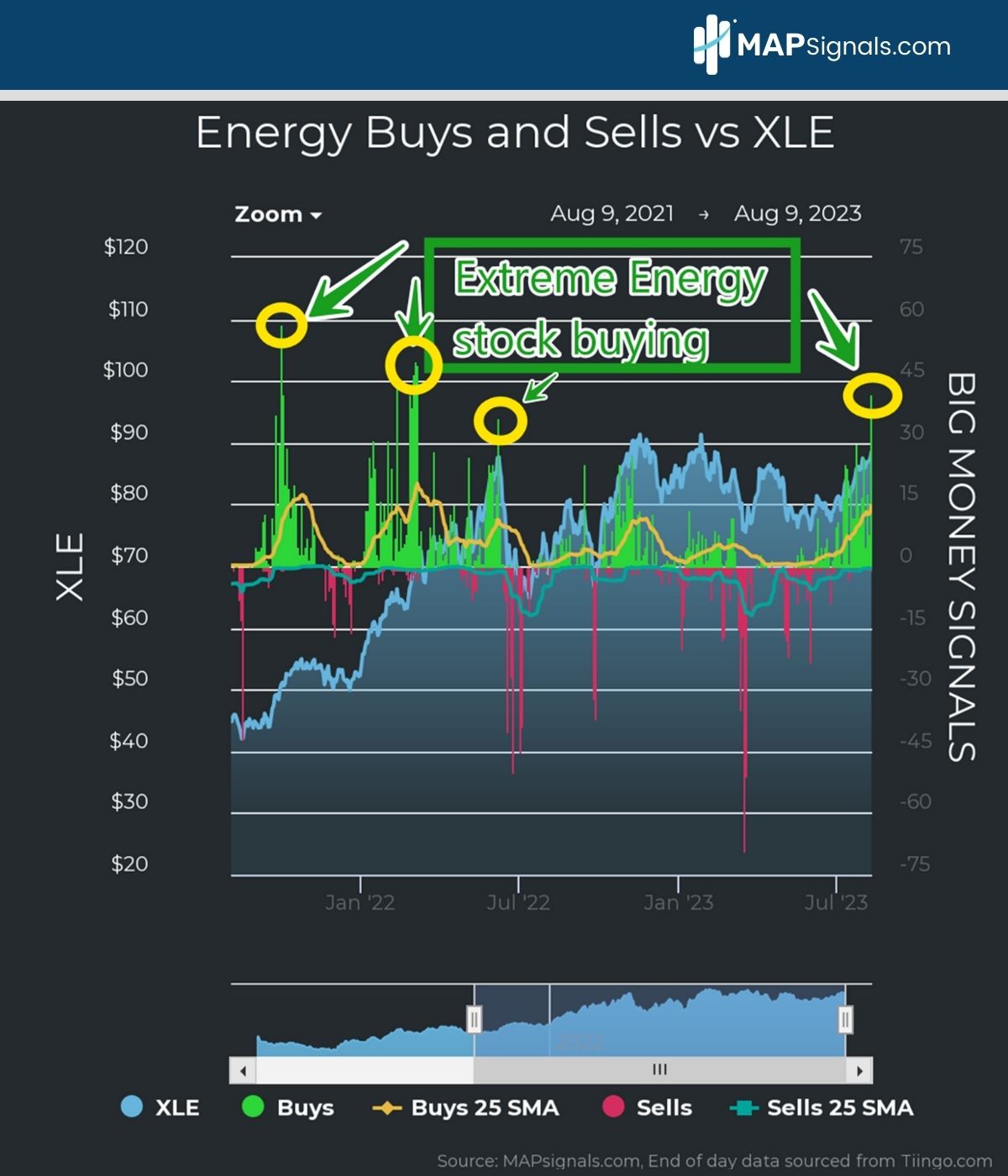

Rare signal points to big upside for Energy stocks

While MAPsignals’ Big Money Index paints a negative short-term picture for the wider market, this healthy sell-off is giving way to a powerful rotation. Money is flowing out of popular high-flying growth stocks and surging into select Oil & Gas names. Lucas Downey's analysis included isolating all days over the past 10 years where >35 Energy stocks were bought. It has only occurred 32 times. Post such an occurrence, 6 month returns for the XLE are 7.6%, while the average gain over 1 year is 15.8%. However, in the post Covid era, 1 year gains amount to a jaw-dropping +35.7%! Adding to Lucas’ bullish view, Energy has now eclipsed Technology as the top-ranking sector in MAPsignals’ data.

USB is capital constrained and is hampered by an under-earning investment portfolio which will pressure earnings for years. Charles Peabody also questions management’s credibility - performance targets unveiled at Investor Days from 2013, 2016 and 2019 all went unmet. More recently, management has been disingenuous about its recent equity capital raise and deposit trends despite obvious balance sheet signs to the contrary. Statements about NII, stock buybacks, positive operating leverage and even the “3.8-year duration” on its AFS portfolio are all questionable. Charles downgrades the stock to Sell and expects the shares to revisit their 52-week lows.

The Psychedelic Revolution

The potential of using psychedelics for therapeutic benefit has taken several steps forward recently. The FDA is getting closer to issuing specific guidance and guidelines for the use of psychedelic drugs to treat mental illnesses - notably for depression and PTSD - as well as for addictions and for use in clinical trials. Psychedelics are gaining cultural awareness and acceptance, with two US states (Oregon and Colorado) legalising controlled uses. Investors are taking notice. By last year, more than 50 psychedelics companies, including Compass Pathways and ATAI Life Sciences, had gone public at a combined valuation of over $2bn.

The stock was highlighted at MYST’s latest Industrial Ideas Forum, with the Presenter claiming that OEM’s “can NOT make planes” without CRS’ specialty metal alloys, putting it in the sweet spot of the aerospace supply chain. While he sees upside to Street estimates and ample room for multiple expansion, he believes CRS also offers substantial “discovery value”, noting that it has relatively limited long only sponsorship and is covered by just 3 Sell-side analysts with stale earnings estimates. Management’s plans to double FY19 operating income by FY27 look conservative. The stock trades at a substantial discount to peers despite having similar scarcity value. TP ~$120 (100% upside).

Poor risk/reward - to justify its current price ($14), MWA must improve its NOPAT margin to 8% and grow revenue by 9% (well above 10-year CAGR of 2%) compounded annually through 2032. In this scenario, NOPAT would equal $236m in 2032, or over 2x its highest-ever NOPAT achieved in 2019. New Constructs considers these expectations to be overly optimistic. Even if the group maintains its NOPAT margin at TTM levels of 7% and grows revenue 5% compounded annually through 2032, the stock would be worth no more than $8 today (40% downside).

Buy the dip even as AI momentum shows cracks - as the semis complex comes under pressure for all the right reasons (disappointments at Apple, loss of momentum in AI, analog inventory, China trade worries), KC Rajkumar believes (near-term) long ideas in semis have become harder to come by. However, he argues the Street has become too negative re. traditional servers and expects investors to gravitate towards AMD despite ongoing worries regarding share gain of its MI300. Over time, KC would not be surprised if up to a third of Microsoft’s AI servers come to be based on an AMD solution vs. the dominant share Nvidia currently enjoys.

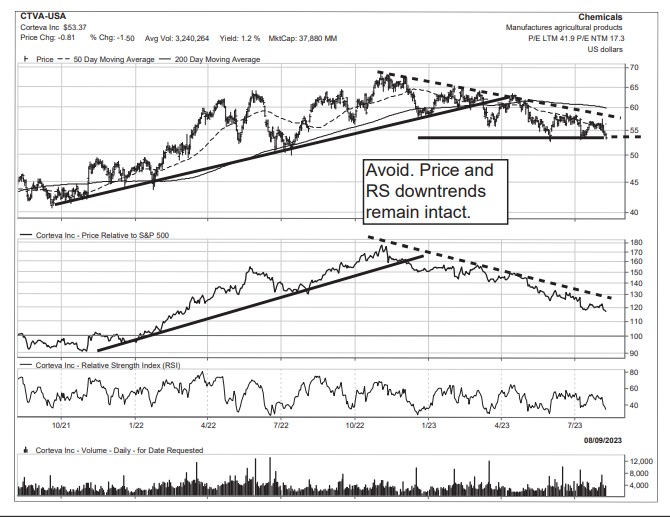

Short Shots

Is a collection of technically vulnerable charts culled from the “Negatively Inflecting” and “Toppy” columns within Vermilion’s Weekly Compass report or from various technical screening processes. The charts contained in this report have developed concerning technical patterns that suggest further price deterioration is likely. For these reasons Short Shots can also be a great source of ideas for investors interested in short-selling candidates.

Charts highlighted include Corteva (see above), Enphase Energy, General Mills, Kraft Heinz, Hershey, MarketAxess, Moderna, Newmont, Penumbra, Roblox, SolarEdge and Valmont Industries.

Japan

Victor Galliano continues to be cautious on SoftBank due to its 1) WeWork exposure (estimated at USD 1.8bn and looks increasingly to be at risk of being written off), 2) the risk of over-valuation of private companies in the Vision Funds (private companies accounted for 64% of SVF1’s fair value with SVF2’s private companies accounting for 84% of the fund’s total equity value) and 3) Masa’s debts to SoftBank (USD 5.1bn). In the near term, the upside potential to equity value rests largely with the Arm IPO, but Victor is concerned that its AI credentials may well be being overstated by SoftBank's management.

Emerging Markets

India IPO Forensics: TVS Supply Chain Solutions, SBFC Finance, Utkarsh Small Finance Bank

TVS SCS - an Indian supply chain firm with a 7% market share; although 70% of operations are international, struggling foreign branches raise sustainability doubts. Additionally, issues like asset impairment, debt-heavy balance sheet, costly acquisitions, asset sales and excessive promoter pay warrant attention.

SBFC - while FY23 saw a robust performance driven by business expansion, efficiency and managed credit expenses, notable concerns like legal disputes, employee turnover and write-offs require careful consideration.

Utkarsh - ranked fifth among India's SFBs, the company exhibited strong advances, deposits and enhanced efficiency recently. Yet, vigilance is advised regarding INR 6bn write-offs in the past two years that aided NPA reduction.

EM Telcos: Are the price wars finally over?

For 15 years, EM Telcos have been engaged in a war for market share, with price the primary weapon. However, peace is now breaking out globally. Mobile prices are rising across global EM (India, Brazil, Indonesia, Thailand among others). In this note, New Street analyses which markets have the greatest potential for recovery, based on 3 criteria: affordability, market structure and challenger returns.

Sigit Prastowo (Finance Director since 2020) purchased ~730k shares on Aug 15th at IDR 5,852, increasing his holdings by +14% to 5.9m shares. This is Prastowo's sixth purchase, his largest and the highest price he has paid. His first purchase was in Mar 2022 at IDR 3,938 and he has steadily added to his holdings since. Smart Insider ranked this stock +N on Aug 10th based on purchases from Agus Dwi Handaya (Compliance & Human Resource Director) and Tim Utama (IT Director). There are now three key operating officers buying shares while the stock is near an all-time high. Smart Insider upgrades the stock further, from +N to +1 (highest ranking).

Copley Fund Research

China: Construction Materials slump

Ownership levels among active China A-Share funds in the sector are approaching their lowest levels on record. Since the last peak in ownership (Feb 2022), Construction Materials have been the victim of some aggressive manager rotation. All 4 of Steven Holden’s ownership measures fell over the period, most notably the percentage of funds invested (-21.6%) and average weights (-0.54%), both among the largest moves of any industry group. Stock ownership is spread across 13 companies, though exposure is heavily skewed towards the top 2 names. Despite heavy selling, Anhui Conch Cement and Beijing New Building Materials account for >60% of the total industry allocation.

3Q23 guidance misses expectations due to intensified pricing competition in smartphone OLED driver IC and AceCamp’s industry surveys reveal Chinese peers could gain additional market share as a result of accelerated localisation of smartphone components. Compounding matters, Samsung will also soon begin selling its OLED driver IC to Chinese smartphone makers. AceCamp believes Novatek could have only 15-20% unit market share in Apple’s OLED driver IC orders in 2024 (vs. consensus estimates of 30-40%). Their 2024/25 EPS forecasts are 30-40% below consensus; valuing the stock at 10-13x 2024/25 PE, implies 40%+ downside.

Macro Research

Developed Markets

The problem with bonds

Michael Howell believes that we face not so much a credit crisis (at least not yet) involving private debt, but instead a duration crisis affecting public debt. Put another way, it is not so much risky assets, MBS and junk bonds that are selling off, but ‘safe’ asset government notes and bonds. If this is true, the entire base of the financial system and the trajectory of Global Liquidity are at risk, and policy makers may need to pump in even bigger volumes of Central Bank liquidity to bail the system out and will be forced to act on cap yields. US Treasuries look vulnerable because term premia are extremely low, and yields could test 5%. There are structural debt supply issues affecting bond markets, already upset by the change to Japan’s YCC. Watch out.

Improvement in bond value now poses tactical threat to equities

The Ekins Guinness team believe that the significant improvement in World Bond Value Yield has now reached a level (in terms of extent and speed) that there is a potential tactical opportunity in bond markets. It remains “potential” since there is not yet any meaningful improvement in price behaviour for bond markets, so the team is not yet allocating to Bonds. Nevertheless, a tactical Value opportunity in bonds poses a risk to Equity markets, and their models have mitigated risk by reducing the equity allocation. It is several decades since such a rapid rise in inflation, followed by a sharp fall, and investors need to be quick to react.We are living in a period in which important signals are given and that asset allocations decisions have to be fluid.

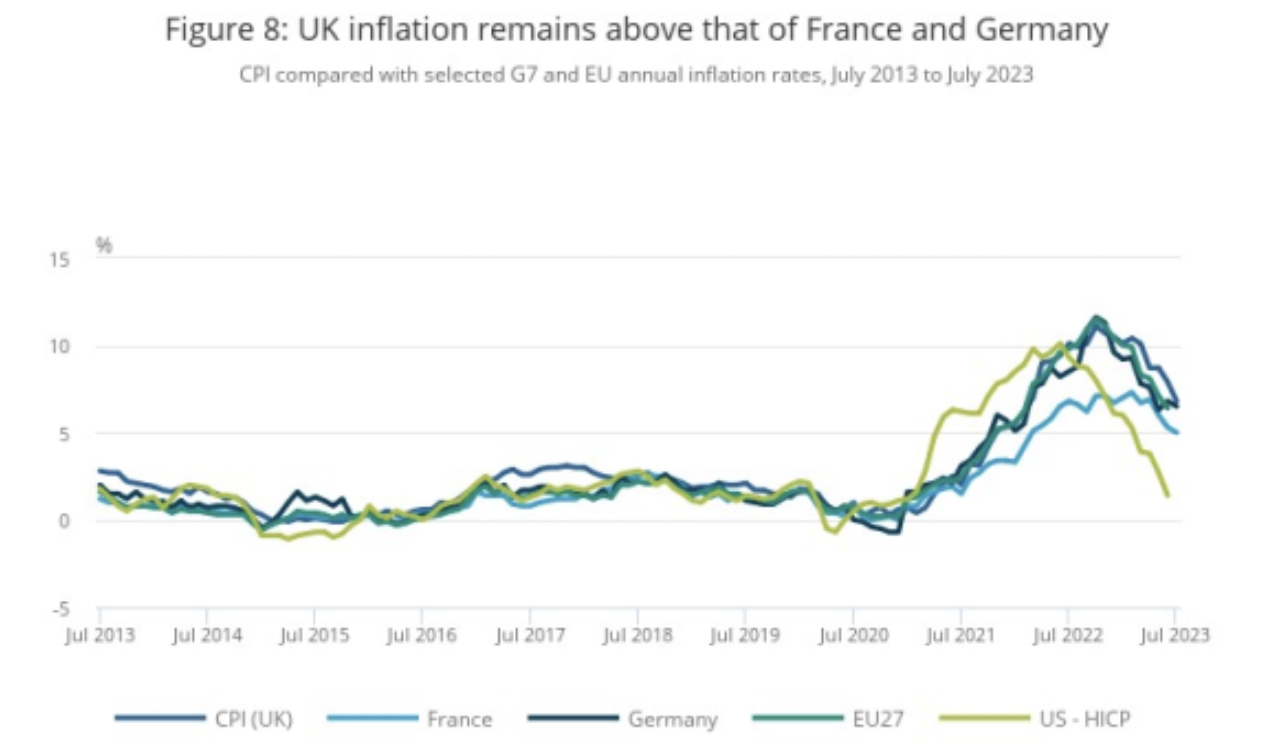

UK: Inflation dynamics unbroken

July’s inflation figures are quite awful, remarks Wolfgang Münchau. CPIH figures are nearly identical to where they were a year ago, with no change in the level of inflation and underlying dynamics. There is some optimism that the UK is following the same path as the US and various European countries with disinflation coming soon (see chart), helped by deflationary trends in the global economy. This will help policy makers bring down headline inflation rates, but they will struggle to keep them there once the economy recovers: the labour market dynamics that is behind inflation stickiness remains unchanged and will get much worse once the economy recovers.

UK: Open the doors

The jobless rate remained roughly steady in July, and the 12-month change in average weekly earnings in the private sector rose once again at 8.2%. The three-month moving average of wage increases accelerated to its highest level since the data began 23 years ago, yet wage increases in June barely kept up with CPI increases, although Carl Weinberg says this will change. If the BoE believes that the solution to rising prices is monetary tightening, and that a tight labour market generates risks to wage stability that threaten price stability, the recent data will encourage the MPC to continue hiking rates. Carl believes that opening the doors to immigrant workers would accomplish the task of stabilising prices faster and more humanely than wildly hiking interest rates to kill demand.

EUR/AUD trade opportunity

TECCS Research provides comprehensive coverage of global financial markets, shaped by more than 30 years’ experience providing technical strategy research to institutional clients. Their views are aggregated in reports that cover Treasuries, Equities, Commodities and Currencies, including easy-to-read-charts. Find above an example of a EUR/AUD trade opportunity recently flagged by the team.

Positioning for a narrow range of outcomes

For Paul Krake, the macro backdrop remains cloudy but within a relatively limited range of outcomes. The recession debate is somewhat nuanced between a mild recession and a soft landing. While a correction in the US stock market in September appears inevitable, it is questionable as to how bad it can get in the face of a rock-solid labour market, credit spreads that reflect a robust economic environment, a macro narrative where a hard landing is taken off the table, and a fundamental outlook for major technology firms that remains entrenched despite recent corrections. It makes sense to be LONG bonds and slightly SHORT stocks going into the most seasonally weak period of the year, but to expect a repeat of 2015 or 2011 is at odds with the apparent narrow range of economic outcomes.

Emerging Markets

Asia FX: Gloom in the news

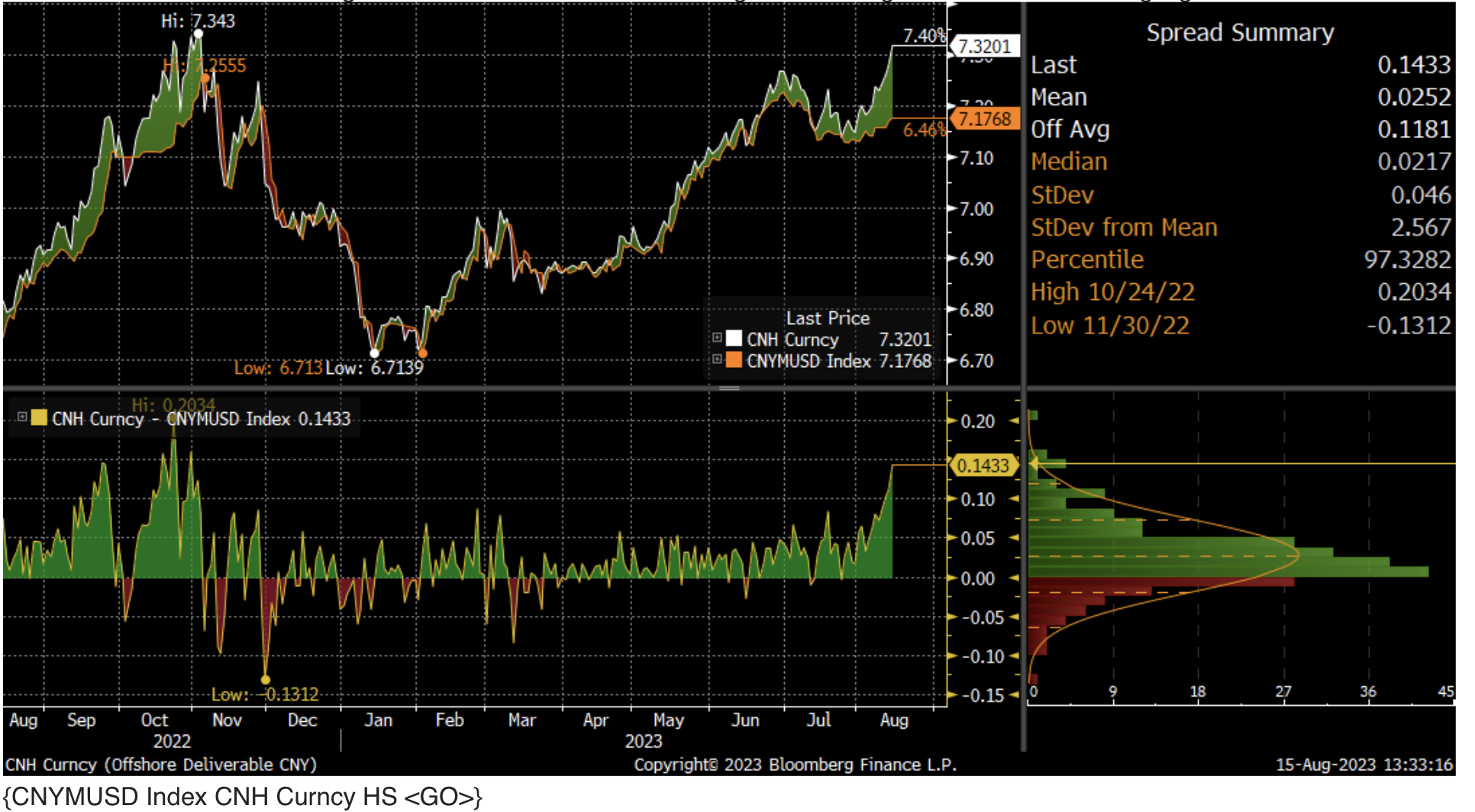

Last Monday, Patrick Perret-Green highlighted the upside risks to the yuan/CNH, Asia FX as a whole and particularly the won, which had strongly outperformed. Since then, there’s been a heap of dismal data and lots more turmoil in the real estate sector. At the time USD/CNH was 7.20 and USDKRW 1-month NDF at 1,305, now they’re flirting with 7.32 and 1,335. The former is almost 14 sen higher than the official fixing, with such divergence often a warning sign for dollar bulls. The yuan and forwards are at an attractive level for exporters to hedge. Further out, the view remains one of weakness, but Patrick would look to lock in profits or place some tight stops on CNY/CNH and AsiaFX.

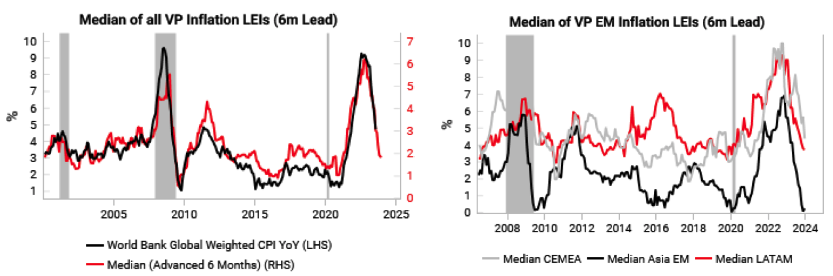

EM disinflation not fully priced in

Variant Perception LEIs continue to fall around the world, led by EM (see charts). EM inflation LEIs have returned back to pre-Covid levels, and the team note that their Brazil inflation LEI is at a multi-decade low. The team remain bullish on select EM debt as market pricing for cutting cycles is very tentative. Brazil remains their favourite pick, and they like buying the dip in Mexico and India debt.

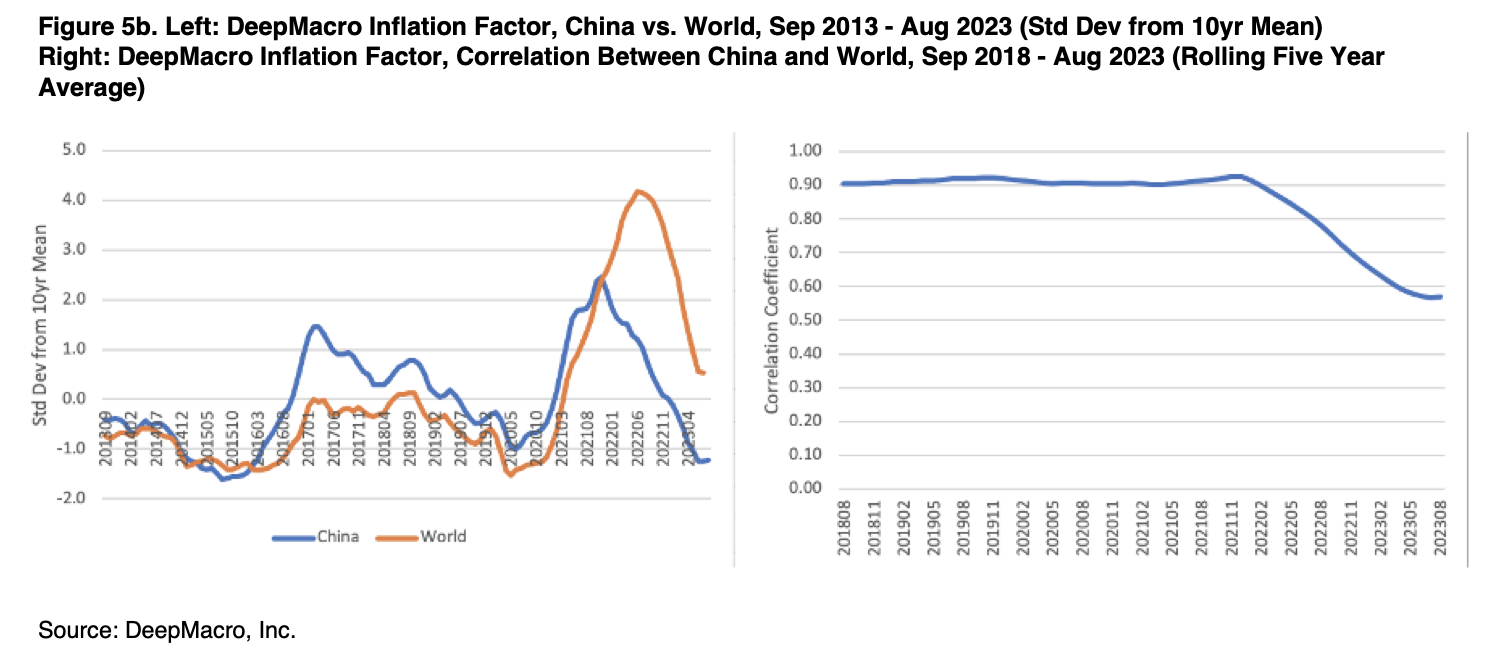

China’s impact on global economy will be mute

Jeffrey Young’s data on China indicates that it is in weak states of both its economic growth and inflation cycles but goes against the consensus with a relatively optimistic view on industrial production. This aside, it’s clear that China’s long-term potential growth rate has fallen, and the country faces major structural problems. However, its impact on the global economy will be muted. Jeffrey draws parallels to Japan’s lost decade, which represented a loss to the world but was primarily a loss for Japan itself. The potential for contagion from China is greater, but nonetheless limited. It’s much the same for inflation too, with the relationship between Chinese and global inflation seeing a large break after the pandemic (see chart).

China: Prices not as weak

Property price deflation accelerated in July, which is unsurprising given the weakness in transactions and mortgage lending last month. The prospects for August don’t look any better. The weakness is happening despite all the rate cuts and loosening of the macro-prudential measures that have restrained the property market. For real estate to stabilise the government needs a new approach, but there’s no signs of one yet. However, the overall rate of inflation ticked up from June, and the East Asia Econ team are cautiously optimistic that can continue even if the overall property sector doesn’t revive.

J Capital Research

China is making AI the enemy

Beijing is rapidly bringing in new rules to restrain AI, having implemented ten significant regulations, three of them formative. It’s not necessarily a bad idea, but the guiding spirit is Communist Party information control; that does not bode well for innovation. Recent developments, including the panicked booking of $5bn worth of Nvidia chips by Chinese internet giants, suggest that the country is not leading in AI development. Tech companies across China are all investing in AI but have yet to show a revenue boost. As AI gets integrated into everything from travel to law, Chinese companies will be on the import, not the export, side of the equation.

Argentina’s three thirds

Niall Ferguson discusses the Argentine primaries which surprised everyone this week. Libertarian economist Javier Milei achieved ~30% of the vote, followed by middle-of-the-road Juntos por el Cambio with ~28.3%. The ruling Peronists came in third, with around ~27%. Within JxC, center-right Patricia Bullrich resoundingly defeated moderate BA Mayor Horacio Rodríguez Larreta. Not a single pollster predicted such an upset. It was the worst election for Peronism since the return of democracy in 1983, with around ~60% of the electorate wanting an anti-Peronist, pro-market change. These results are likely to lead to Peronism losing control of Congress for the first time in decades. Yet Milei’s outperformance and JxC’s relative underperformance increase uncertainty on the road to the October elections, which should lead to increased volatility in the short run.

Chile: BCCh is in no need to rush

Little seems to be working out for Boric’s Presidency in recent months, comments Marcos Buscaglia, with a stalled legislative agenda, stunted economy and growing discontent. He expects the economy to have continued contracting in July, but we should not assume from the data the economy is that weak: the drop in sales is just a return to normal levels, and the output gap is being closed. After the surprising 100bp cut in July, Marcos believes the market and consensus got ahead of themselves; he expects BCCh to cut rates by 100bp in its next meeting at most, a risky strategy in an economy that isn’t too weak, which may result in upside inflation surprises.

A cautious eye on Indonesia

The underlying mantra of Jonathan Anderson’s Indonesia position is simple: a flat economy at home, no import pressures and attractive bond yields. This doesn’t do much to recommend Indonesia as an equity story, but it has helped maintain a stable rupiah and kept him in IDR fixed income. As with most of Jonathan’s EM FX and local fixed income positions, the trend most likely to force an exit is a widening external deficit, so he’s keeping a cautious eye on the recent worsening in the country. The latest trade numbers aren’t enough to take him out today, but if deficit momentum continues, he’ll have to rethink.

Commodities

Longview Economics

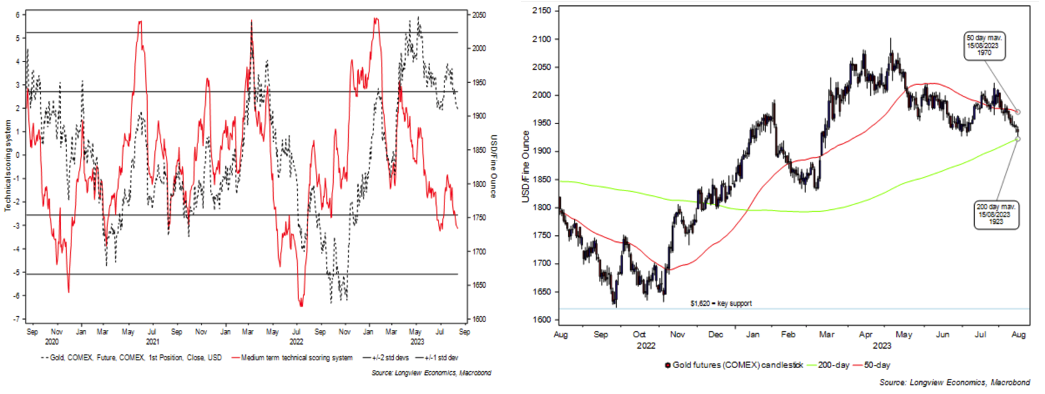

The case for buying gold

Chris Watling’s latest report examines in detail the reasons for buying gold. He touches on a wide range of topics, from the macro landscape to the emergence of Cold War II. It’s become quite clear that gold has become oversold and is back at its 200DMA (see chart) and, given Chris’s expectations about the shift in rate expectations and TIPS yields, gold is once again an attractive long proposition. Move LONG gold futures. Implement ½ position at current levels, approx. 1,930 (GCZ3 Comdty) and the second half on weakness (if forthcoming) – i.e. at 1,880. Risk 120bps on this trade. Place stop loss at 1,825.

Wake up and smell the coffee

The coffee market continues to hover around $1.60 in New York, which is to some degree based on the direction of the dollar relative to the Brazilian real. Nevertheless, Judith Ganes remains negative and does not see this level being establish to even trade sideways from for any extended time frame. She isn’t convinced that the crop production was disappointing in volume, but rather that producers aren’t willing to part with their stock at current prices. Judith reckons this will catch the market by surprise, with evidence already present in export volumes. She remains bearish coffee.

Platinum: Testing support

Spot Platinum has been rangebound for 7.5 years, between ~USD770-825 and USD1,125-1,200. Chris Roberts is anticipating another test of the support area, where he would like to buy – if platinum gets closer to the USD770-825 area, he will look for a buy set up (see chart 1). Platinum is volatile, and another test of support may see 9-month RSI trade down to 30-35. Chris would also likely scale-down buy an initial position into support and add when a weekly close above the 40-week MA occurs (see chart 2).