Company & Sector Research

Europe

Forensic Alpha

Contract Assets have been increasing much faster than sales - it seems strange that there should be such a sharp increase in the balance (from SEK 177m last year to SEK 790m) in the absence of a fundamental change in the business model. There is also an additional amount of SEK 1.2bn Accrued Income for which there is no description. The other interesting piece of disclosure in the accounts is around intangible assets, which highlights the sheer amount of internally generated development costs being capitalised in 2023 (SEK 12bn vs. SEK 3.7bn in 2022). For a company with an adjusted EBIT of SEK 6.4bn, this adjustment would turn the company from profit-making to heavily loss-making.

Insight Investment Research

Robert Crimes expects CLNX's sharper focus on organic revenue growth, efficiency gains from a rising tenancy ratio and lease reductions to lead to a S&P IG credit rating in late 2024, then high DPS growth from 2025. The dividend yield reaches 3.5% in 2027 and 12.2% in 2028, the latter when capex is half that of 2023 and Robert assumes all equity FCF is distributed. In addition to his detailed long-term model forecasts, Robert's report also includes suggested key action points for the new CEO including improving divisional disclosure and selling the Broadcasting division. TP €85 (135% upside).

the IDEA!

INPST announced that it has acquired a 30% stake in Menzies (with an option to acquire the remaining 70%) - the IDEA! believes the deal offers several advantages, the most important of which is that it will help INPST to accelerate its growth in the UK, both geographically (i.e., outside of the three metropolitan areas in which it is currently active) and in new market segments (predominantly B2B and B2C). While they do have some concerns re. Menzies’ high exposure to low-growth markets and its lower margins as well as its higher cyclicality, the call option will give management up to three years’ time to see how that will develop.

ResearchGreece

ResearchGreece addresses the following dividend-yield-buffer questions: a) How likely is it that the RAE will approve a higher WACC for IPTO? b) If so, what about RAB evolution? c) What is the impact on the fair value of ADMIE? d) What should investors do with the stock? A +100bps higher WACC means IPTO is worth €1.97-2.46bn based on peer multiples applied on 2024-2025 EBITDA. Therefore, ADMIE's 51% stake is worth €920m-1.06bn in NPV 2023 terms against a M/Cap of €555m. ResearchGreece estimates ADMIE's dividend yield at 5.3%-6.6% in 2023-2025 and upgrades their stock rating to OI (OWN IT) with a TP of €4.0 (70% upside).

Willis Welby

Screening UK Stocks: Combining quality, momentum and expectations indicators

Methodology - the initial universe are stocks with $2bn+ M/Cap. After that Willis Welby starts with a quality cut off based on their measure of Intrinsic Return on Capital Employed. They then narrow down using a combination of share price momentum and EBIT revisions before incorporating their expectations analysis via their measure of the implied to Y3 EBITM ratio. This has been another month of low turnover for the UK screen and it is notable that stocks coming in are exclusively in Consumer Services with the return of three retailers (B&M, Pets at Home, WH Smith) and Flutter. The four stocks leaving are Burberry, IAG, Hikma and Serco.

North America

Behind the Numbers

Hot pricing down south

BTN has come across several companies whose organic revenue growth and profits have been receiving material boosts from increasing prices in their Latin American operations at a far faster pace than foreign currency depreciation would seem to justify. When they look at the amount of pricing net of FX that many companies are getting of late, it’s greater than 10 percentage points. The problem BTN sees is the longer historical spread is closer to 2-3 percentage points. Many companies could soon see a sizeable part of their growth vanish.

Two Rivers Analytics

Declining Businesses: Best short candidates

Atlantica Sustainable Infrastructure (AY) - Faces competition from new renewable energy companies and weaker than expected demand for electricity. Sales growth averages just above zero since 2017. EBITDA and FCF have declined since 2021. Trades at 34x 2024 earnings.

Olin (OLN) - Weakened demand in its core chlor-alkali business, increasing competition and higher raw materials prices. Sales declined for four quarters (incl. -35% drop last Qtr). While current year growth forecasts have been cut, out-year growth forecasts have been increased.

Seagate (STX) - The demand for hard drives has been declining as storage shifts onto the cloud. Sales have declined dramatically for five quarters. Margins have plummeted and leverage has shot up (when measured against collapsing EBITDA).

Arete Research

It’s early days for CHTR’s rural investments, but first results look encouraging - Arete’s cohort modelling suggests that rural expansion can contribute 112k Internet net adds in 2023, 195k in 2024 and 241k in 2025 (ignoring further subsidy awards). Spectrum One can also be a further source of broadband (as well as mobile) net adds. Arete sees Internet net adds 22-33% higher than consensus over 2024-26 and expects CHTR to grow EBITDA at a +4.4% 5-year CAGR with FCF growing at +10%. TP $600 (45% upside).

The Retail Tracker

There are two lanes in retail winning right now - momentum and improvement

Brands with good momentum include Lululemon, Abercrombie, Chico’s, Steve Madden, LVMH, Prada, Ralph Lauren and Macy’s. According to The Retail Tracker, these retailers are entering the back half of the year with the consumer on their side and good assortments. In the improvement lane, they highlight Gap, Target, American Eagle, Bath & Body Works and Nike. They also like the risk:reward in two currently out of favour names - Williams-Sonoma (a high-quality company, with exceptional brands / leadership) and Victoria's Secret (left for dead / trades at a steep discount).

Quo Vadis Capital

TSCO has responded to its latest earnings miss by adding structural leverage to the balance sheet and by planning to ramp unit opening. These actions, by themselves, don't add an enormous amount of incremental risk, but they do signal that management is not acknowledging the change in the environment. John Zolidis thinks consensus comp assumptions for 4% growth in 2024 and 2025 are out of reach. He also sees risk to EBIT margin forecasts. TSCO is in the midst of a multi-quarter downward revision trend, which should make it an excellent hedge for long positions.

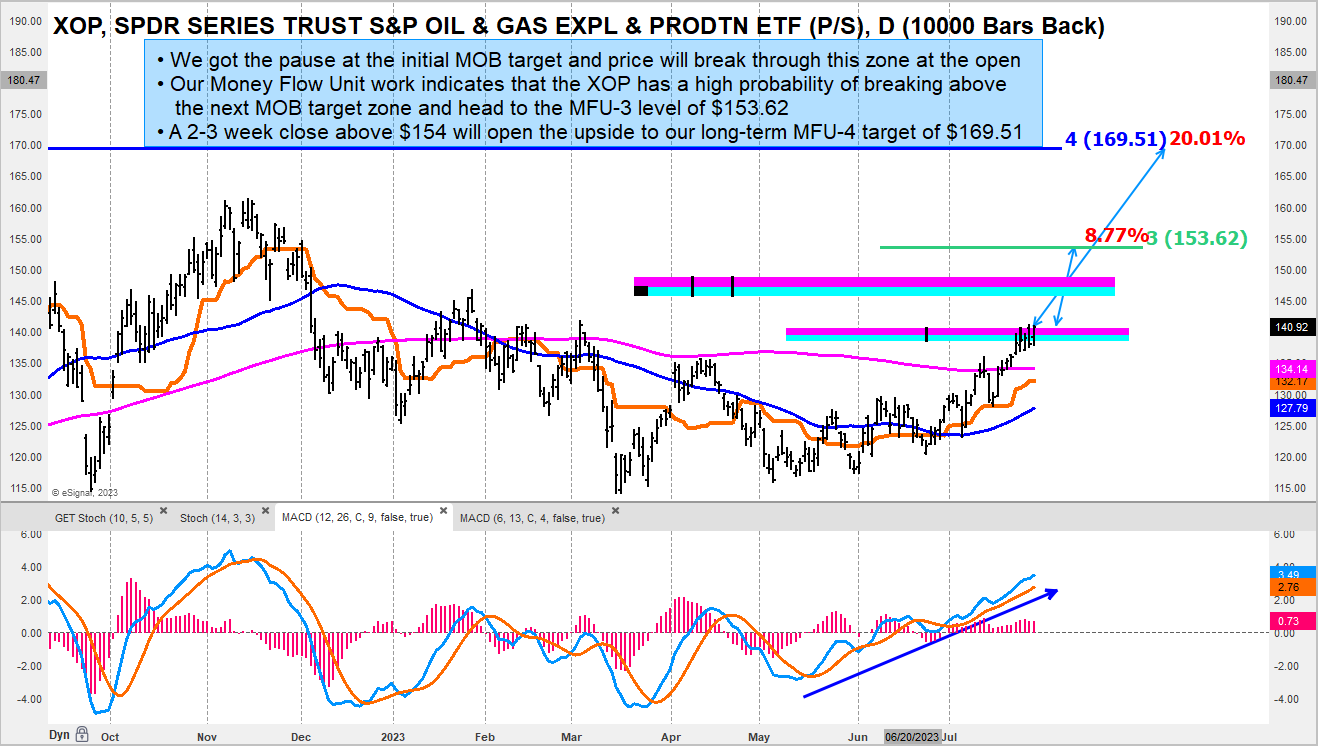

Cerundolo Investment Research

XOP: The pause is over and the next leg is about to begin

Guy Cerundolo's proprietary Money Flow Unit analysis indicates strong accumulation in the energy equities. While his initial target for the XOP is $153.62, Guy believes the sector is only in the early innings of the advance off its Jun low. The last time he was this bullish was in Nov 2020 and resulted in a +180% move up in the XOP.

280First

SLB was one of the stocks highlighted in a roundup of recent real time alerts that were extracted and published by FirstAlert (280First's 10Q/10K analysis module) after it flagged that the oil services firm had removed the following wording from its 2Q23 10Q "...as SLB continues to support the strong revenue growth that is expected to continue in 2023..." - this wording was first added to the 3Q22 10Q and continued in both the 2022 10K and 1Q23 10Q. The company noted on its earnings call that it continued to expect YoY growth of >15%. However, as there are always reasons why companies elect to remove wording, is management becoming less confident on SLB's growth rates this year?

Thompson Research Group

TRG initiates coverage on ROAD, a company benefitting from a structural US population shift to “smile states” and the passage of significant US and state funding initiatives supporting a 5+ year runway for infrastructure and private construction projects. They expect ROAD to generate significantly more cash annually through 2025 as EBITDA margins improve back to 12%+ and revenue continues to grow at historical rates (~18-20% p.a. - balanced mix of organic / inorganic growth). Importantly, management has also taken proactive steps (ahead of peers) to focus on recycled materials and additional ways to reduce the firm's carbon footprint. 12-month TP $39.

Veritas Investment Research

Seeking a wealthy partner - the Josemaria project in Argentina carries significant risk, with returns likely below a reasonable cost of capital for LUN. Absent a contribution from a partner, Martin Pradier fears value dilution on an equity issuance to fund the project. Development and associated funding risk, combined with unimpressive ROE, a weaker outlook for copper prices and recession risk, all contribute to his initiation on the stock with a Sell rating and $9.5 per share value estimate. His valuation implies 3.5x and 8.5x 1-yr forward EBITDA and EPS, respectively.

ETR

ETR’s latest survey reveals that spend within Networking has further deteriorated with 12% of respondents planning to decrease spend on the company in 2H23, up from 10% (Apr 23) and only 3% in the year-ago period. Expected spend on Linode (AKAM’s cloud computing acquisition) has fallen even further to a 0% Net Score, which places it in the lowly 23rd percentile of the Cloud Computing sector. Replacements of Linode have nearly tripled to 11%, up from 4% at the beginning of the year - putting it in the 91st percentile within the sector. While spending intent within Information Security was a bright spot in this survey, the large decline in ETR’s previous survey has likely yet to play out completely.

Gradient Analytics

Gradient’s main short-term concern is potential top-line disappointments driven by a host of demand-related factors, including elevated inventory levels at major customer, Ciena (among others), lower levels of data-centre Capex spend, lower demand for smartphone 3D sensing products and softer sales of Commercial Lasers products. A relative spike in AR exacerbates their concern and unusual growth in prepayments and other current assets adds another margin headwind in coming quarters. Additionally, disproportionate inventory growth appears to predate the NeoPhotonics merger and current inventory levels appear disconnected from near-term demand.

Huber Research Partners

Post 2Q results, Craig Huber increases his 12-month TP to $389 based on averaging 20.5x 2025E EBITDA (or 26.0x adjusted EPS) and his 10-year DCF analysis (9.0% WACC, 4.5% long-term FCF growth rate and 22.3x terminal FCF multiple). He thinks debt issuance trends are going to improve significantly over the next 2-3 years and MCO should benefit materially and at a time when it is currently tightening its costs to become even more efficient. Street adjusted EPS estimates for 2024-25 look significantly too low; Craig's 2023-25 estimates are $10.25/$12.40/$15.10 vs. consensus forecasts of $10.07/$11.47/$13.20.

Emerging Markets

New Street Research

XL reported a strong set of results with revenue and EBITDA ahead of consensus. As expected, mobile ARPU rose 7.7% Y/Y on the price increase in Q1, driven by prepaid. More positively, XL has upgraded top line guidance to high-single digit growth. ISAT also performed well during the quarter and upgraded its EBITDA guidance (as New Street had predicted it would). XL and ISAT’s mobile performance are indicative of a rational mobile market as operators look towards better monetisation opportunities. New Street's TP of IDR 5,000 for XL offers 100%+ upside and implies a valuation multiple of 6.2x FY24 EV/EBITDA, while their TP of IDR 11,000 for ISAT implies a valuation multiple of 5.5x FY24 EV/EBITDA.

ChartWizard

JUBI declined from 640 to lows near 420-425, then consolidated and defended this low for three months. The stock price eventually rose, crossing the 50-DMA and facing resistance at the 200-DMA. The MACD's positive crossover and RSI's new 14-period high and breaking out from a pattern ahead of the price signal a bullish trend. The stock broke out from a falling trend line resistance and positioned itself in the leading quadrant in the RRG quadrant, implying potential outperformance against NIFTY 500. If the breakout continues, the stock may reach 530 soon. Traders should use a stop-loss at Rs. 468 for this trade.

Hedgeye

Revenue growth has been the driver for both stocks, but they are facing tough top line growth comps in 2H23. For PDD, the slowing growth may not be temporary, as F&B delivery is likely to become a smaller part of the business with people out of quarantine, user saturation may be reaching its limit and merchants / consumers may be switching to JD.com’s offer. Felix Wang is also flipping DADA from long to short, as near-term catalysts are shifting. A critical part of his long pitch stemmed from support from short video disruptor, Douyin. However, Douyin surprisingly encountered major obstacles in local life services, including food delivery, in Q2. Competition for DADA is also heating up.

Galliano's Financials Research

Mexican banks, along with other Mexican assets, have benefitted from the nearshoring theme and more recently, the investor sentiment change in favour of EM assets which also supported bank shares. Yet bank sector headwinds are emerging in the data, with rising funding costs eroding credit spreads and worsening credit quality trends implying a worsening in the credit cycle. Victor Galliano believes that Banorte’s 2Q23 results vindicate his caution on the shares, with evidence of spread pressure and rising credit costs; he prefers to gain Mexican bank exposure through BBVA (BBVA Mexico consistently extracts premium returns on equity well in excess of 20% p.a., with its healthy core capital levels not acting as a major hurdle to its high ROE).

Creative Portfolios

Conservatively managed TTB produced a strong set of numbers in 2Q23 and the bank's elevated PH Score™ (9.4 out of 10) is indicative of superior relative returns going forward. Paul Hollingworth notes that there were improvements across almost all key variables - in Profitability, Capitalisation, Margin/Spread, Provisioning and in Liquidity. Management's strategy is focused on raising profitability via revenue synergies from the merger, adding a product for each customer (cross-selling of home and auto products plus other consumer offerings), widening digitalisation and continuing to get the CIR lower (40% target). The stock is up +46% since Paul turned bullish (vs. MSCI EM Index -24%).

Macro Research

Developed Markets

The Macro Compass

The liquidity illusion

One of the most popular but misleading charts in macro. Many believe the Fed “pumping money” into the system leads to equity markets going up, but that’s not how it works. Bank reserves operate in a closed system that never reaches the private sector. Some people point to the portfolio rebalancing effect to explain the relationship, but even then, we only see second-order effects, reliant on underlying economic fundamentals. A simple linear regression analysis shows that in the last 15 years, US liquidity only explained 3-4% of the variation of SPX returns!

Talking Heads Macro

The myth of enduring 2% inflation

Manoj Pradhan claims central banks are providing too much reassurance about the medium-term outlook for inflation than is warranted by the underlying fundamental risks. In doing so, they are almost ensuring that inflation won’t stay at 2% after it troughs, and we will see the next cycle of inflation be even more dangerous than the one we’re coming out of. Expect breakevens, equities, credit spreads, EM and r* to all behave very differently in the next cycle.

Stray Reflections

Where's the recession?

Many investors still believe the US economy will deteriorate in H2, but Jawad Mian believes the recession is already over. This shift in view from a delayed recession to one that’s finished is pretty crucial for investors but is overlooked. If Jawad is correct and yields move higher, expect investors to be forced out of their recessionary trades and EM carry positions. He questions the pervasive bearishness on the prospects for UK and Europe, wondering if investors should soon be diversifying away from US and dollar based investments – the idea that “America is winning” may no longer be true.

Eurointelligence

UK Politics: Sunak is moving to the right

A green line is increasingly splitting the centre of European politics. In the UK, Rishi Sunak is moving away from the net zero target, a political bet to help him secure rural and suburban constituencies most affected by the climate transition. Wolfgang Munchau sees net zero as the next Brexit-style political theme in the UK with deep divisions running through the middle of the Conservative Party. He notes that there are similar shifts on the way elsewhere in Europe too, but for now it is far-right parties like the AfD that benefit the most from disaffection with climate-change legislation. Another factor that is driving the Conservatives' lurch to the right in the UK is the return of Nigel Farage.

Independent Strategy

Three dark towers

There are three dark towers in financial markets of whose monetary rule we are the subjects: the BoJ, Fed and ECB. Darkness characterises their state of knowledge. The BoJ has just made the most momentous change to widen the YCC band to 0.5% on ten-year bond yields, described as neither a target nor a limit, it’s the end of YCC and the beginning of monetary tightening. Meanwhile, The Fed and ECB have moved to being ‘data dependent’ for future moves meaning they don’t know what is coming and have no conviction about it. Independent Strategy expects another two 25bp hikes from both central banks and that there will be no global recession.

CrossBorder Capital

Could changes to Japan’s YCC cause US treasuries to crack?

After months of speculation and 2-3% high street inflation now seemingly embedded, the Bank of Japan finally adjusted its controversial YCC policy. YCC alters the interest rate term structure, beyond what private markets decide, by manipulating the supply and/or demand for bonds. According to Michael Howell, Japan’s long-awaited YCC policy change threatens to roil international bond markets. He estimates that JGB yields could break 1% and US Treasuries could test 4½%, reinforcing their downbeat view of global bonds. Avoid duration.

Minack Advisors

Disappointment ahead

Gerard Minack says that markets, on a tactical time horizon, are all about outcomes versus expectations. Growth in most developed economies slowed in the first half of the year but was stronger than expected. Inflation was unacceptably high through the first half but lower than expected. Growth surprising to the upside and inflation surprising to the downside is always good for equity valuations. What’s unusual is when in the cycle this combination occurred. With expectations now bullishly resetting, the risk of disappointment – particularly about growth – will start to rise.

ChartAnalytics

Bullish setup in the EURAUD

A potentially favourable short-term trading opportunity is evident in the EURAUD pair - the price action has resulted in the formation of a bullish ascending triangle, indicating the possibility of an upward breakout upon surpassing 1.6530. Additionally, the 20-DMA has recently crossed above the 50-DMA, while the Histogram is narrowing sharply, suggesting a potential positive crossover in the MACD in the near future. If the anticipated breakout occurs, the price target at 1.7180 can be expected in the coming weeks. However, should the price drop below 1.6240, this bullish setup would be invalidated.

Emerging Markets

Trivium China

China: Zigzagging to prosperity

Anyone hoping China’s leaders were planning significant economic stimulus will be sorely disappointed by the readout of the econ-focused July Politburo meeting. The meeting promised to “strengthen countercyclical adjustments,” but offered nothing that’s up to the task of turning the economy’s fortunes in a hurry. The Politburo diagnosed the economy’s problems by saying it is “facing new difficulties and challenges” due to: “Insufficient domestic demand”, “Operating difficulties at some firms”, “Many hidden risks in key areas” and “A complex and serious external environment”. What’s to be done? Fiscal policy must be proactive and monetary policy prudent, fees and taxes must continue to be reduced and the PBoC must continue to deploy structural monetary tools.

Greenmantle

Brazil turns the corner

Falling inflation, interest rate cuts starting in August, and the emergence of a more solid government alliance in Congress makes Niall Ferguson more optimistic about Brazil in 2H23. Finance Minister Fernando Haddad won market approval and strengthened the position of governing moderates after securing significant—albeit limited—fiscal reforms. High debt and low confidence levels among domestic investors continues to weigh on the economy, but expect the buoyant agricultural sector to largely dodge the impact of the extreme weather associated with the incipient El Niño. The macro context will benefit Brazil and its main industries as the rate cutting cycle accelerates.

Horizon Insights

China: Opportunities in large-cap, mid-stream and export stocks

Better than expected, China's manufacturing PMI readings came in with a surprise on the upside, 0.2 up from last month's 48.8%. Improvements in domestic demand are the main reason, while the PMI's new export orders slightly edged down in July. Despite having no policy stimulus, Horizon Insights sees more signs that the Chinese economy is bottoming out on its own. They point out that the mid-stream manufacturing sector will benefit under the current setting. Large-cap stocks may also outperform during the market rebound. In addition, there will be opportunities with export-orientated Chinese companies going overseas.

Intelligence Research

Argentina: Free market dollar soars again amid economic scepticism

On July 24th the free market or ‘parallel’ dollar soared to a record Ar$550. Government plans to build confidence by announcing new economic measures and finalising a staff-level agreement with the IMF, failed to generate the hoped-for enthusiasm among investors. Economy minister Sergio Massa had already anticipated a new ‘agro dollar’ preferential exchange rate for regional farm exports excluding soya. An additional 25% higher exchange rate applied to imports of services and an extra 7.5% increase in the rate used for imports of goods. The ‘solidarity dollar’ rate also increased for those who seek to buy foreign currency for savings. The government claims tweaking these multiple exchange rates will generate US$2bn in extra foreign currency revenue for the country and US$1.3bn in extra government revenues.

Signal Risk

Niger: Will ECOWAS launch a military intervention?

The Economic Community of West African States (ECOWAS) regional bloc imposed multiple sanctions on Niger on 30th July. Sanctions have also been placed against the putschist National Council for the Safeguard of the Homeland (CNSP) soldiers, who overthrew the administration of president Mohamed Bazoum on 26th July. In addition to the sanctions, ECOWAS is demanding that Niger return to constitutional rule within the week, failing which the regional bloc will consider military action against the Sahelian state. Is ECOWAS's threat of military intervention in Niger credible? If so, how will the CNSP junta respond to a possible invasion?

Emerging Advisors Group

Taiwan's equity market is rallying once again

The Taiwan index outperformed massively in 2020-21 before collapsing back down in 2022... and is now again soaring well ahead of the rest of Emerging Markets. Just as in the last round of boom/bust, this rally has nothing to do with macro conditions in Taiwan, or for that matter with external trade or China exposures. Rather, the Taiex is rising as part of the global tech surge.

ESG

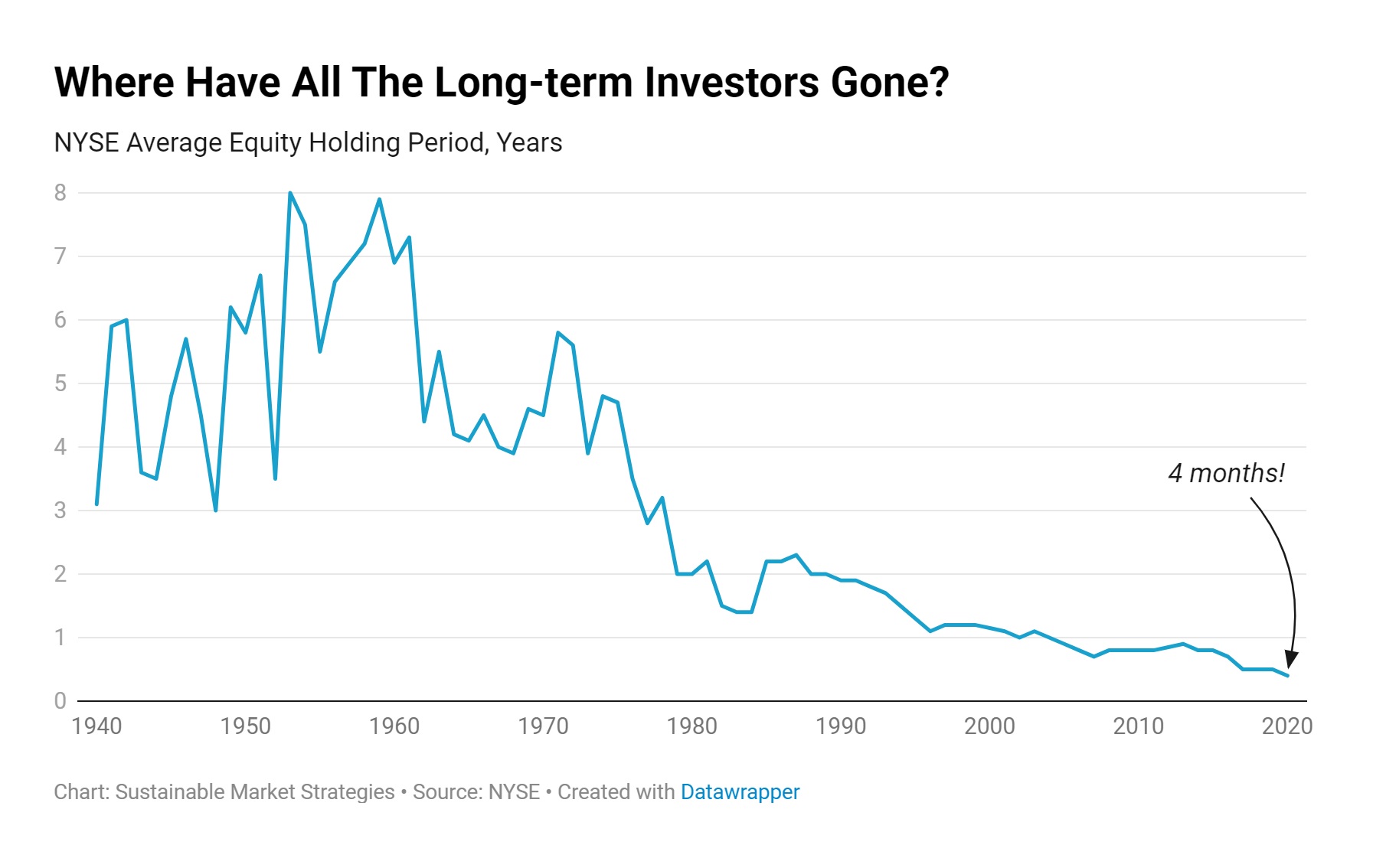

Sustainable Market Strategies

Where have all the long-term investors gone?

In their latest note, the Sustainable Market Strategies team examine the current issues of capitalism and the calls to rethink the contemporary economy. They analyse the implications of this growing awareness and the anticipated developments for the financial system to support the goals of stakeholder capitalism. Their analytical framework considers four critical economic drivers: demography, international relations, regulations and technology. These interconnected factors are charting the path towards a more responsible and inclusive economic system.

Commodities

Queen Anne's Gate Capital

Weekly Oil Market Update: Strong demand for US oil

Strong global demand for US oil exports will be the story all year. Oil production fell again to 12.2mmbpd. Refining runs fell again despite very low product inventories. Total US oil product demand rose to 21.3mmbpd led by good jet fuel demand. Cushing fell 2.6mmbpd to 35.7mmb, supporting WTI spreads. Imports from Canada, Brazil, Saudi Arabia and Mexico fell while imports from Nigeria rose. Total US inventories, including products, crude and the SPR are still low and are now heading lower. The macro picture for oil has improved and technically and fundamentally oil is recovering with the physical market tightening.

Global Mining Research

Falling nickel prices hitting higher cost producers

After a good 2022, nickel prices are now feeling the pressure of rising Indonesian production and generally soft economic conditions. Although nickel equities don’t appear expensive for the long-term, shares are now fighting a headwind of lower prices and margins are compressed enough that several would be in difficultly should prices weaken another 10-20%. David Radclyffe’s views are mostly negative to neutral, his preferred nickel equities are IGO and Sherritt, while he has SELL ratings on Vale Indonesia, Norilsk Nickel and Nickel Industries.

Meridian Macro Research

Gold: Record highs coming soon?

Meridian Macro Research suspects another test of $2000 is coming soon, especially should a gold-backed BRICS currency be announced at the BRICS summit in Johannesburg (August 22-24th). Whether such a currency is announced or not, South Africa's senior BRICS diplomat Anil Sooklal said on July 17th that the BRICS coalition will continue to switch away from the US dollar. As de-dollarisation of international trade efforts continues to heat up and mounting debt issues go unresolved, we should see gold reach record highs before long.