Company & Sector Research

Europe

the IDEA!

Having received a growing number of questions from investors about the dynamics in the Dutch FttH/O market, the IDEA! takes a deep dive into the market with this 67-page report and stumbles on some surprising findings. They discover that there will be overbuild on a massive scale (by almost 50%), which will hamper profitability and capital allocation for the telecom sector, have negative effects for consumers / society at large and will slow down the rollout in areas without fibre.

ALEZOR Research

Alejandro Acosta initiates coverage with a TP of €13 (60% downside) - he argues that the hotel operator's credit risk is closer to a rating of B or below, which is significantly lower than both S&P (BB+) and Fitch's (BBB-) ratings. Key points of interest include: 1) Perpetual subordinated debt is reported as equity when it is debt-like. 2) The “Booster project” led AC to deconsolidate its real-estate related debt and operating lease commitments therefore bypassing the application of IFRS 16. 3) The lead Senior Independent Director doesn’t have skin in the game and doesn’t seem focused on the company. 4) Employee turnover is alarmingly high and increasing.

ChartWizard

IHG exemplifies a classic quadrant crossover on the Relative Rotation Graph (RRG), indicating potential relative outperformance vs. the broader markets. Currently, IHG's stock is forming a neutral symmetrical triangle pattern, which usually acts as a continuation pattern. Providing further support, the price is holding steady at the 50-Week Moving Average of 5122. Notably, the stock has entered the leading quadrant on the RRG, reinforcing its potential to outperform. If the expected technical scenario unfolds as anticipated, IHG may reach 5800 levels in the upcoming weeks. However, it is essential to monitor any drop below 5150, as it would invalidate the current technical setup.

Green Street Advisors

Green Street initiates coverage with a Buy rating. This €13bn-GAV Industrial PropCo listed in 2021 and has weathered the rise in real rates unscathed. They highlight CTP’s 1) strong internal growth (5-yr LFL NRI CAGR of 4.6%, ~100 bps above Continental peers), 2) voracious appetite for development-led growth (targets doubling GLA by 2030), 3) development profit margins have stabilised at ~30%; >9% yield-on-cost is achievable, 4) vanilla corporate structure, palatable balance sheet metrics and sufficient liquidity, 5) CEO’s c.75% holding warrants GAV discount, but skin-in-the-game placates fears, 6) offers the highest risk-adjusted five-year REIT returns across Europe at >11% p.a.

Willis Welby

Seriously cheap UK mid caps

The median implied to Y3 EBITM ratio for Willis Welby’s UK coverage is now 68 for which you get median consensus Y3 revenue growth of 5.4%. And over the last three months the median move in Y2 EBIT is still an UPGRADE of 0.8%. The Q2 reporting season could be a rude wake up call, but so far, they cannot see the huge economic downturn that is priced into this part of their coverage. And if it does not materialise, then UK mid cap shares are seriously cheap. Industrials (Manufacturing & Support Services) look particularly interesting - highlights Coats, Morgan Advanced, Qinetiq, Hays and Serco. They also see decent revisions and a compelling balance of growth and expectations across Technology names such as Team17, Moneysupermarket, Auction Technology and Kainos.

North America

Trivariate Research

US corporate earnings will erode not implode

The current bottom-up consensus earnings expectations embed a $219 (or 0.2% growth) forecast in 2023 S&P 500 earnings. However, Adam Parker still sees estimates as too optimistic. He forecasts $215 in earnings this year and $225 in 2024 (vs. consensus at $245). While there is a narrative that earnings could be as low as $180 this year, Adam sees this as highly unlikely. He also believes a great signal for investing at this point in the cycle is the incremental gross margin expectations vs. the business model average - companies with high incremental margin expectations are more likely to have below average estimate achievability. Quantitatively derived long and short ideas are available.

MYST Advisors

Special Situations Idea Forum

Presenters at MYST’s latest buy-side event offered a diverse set of ideas with significant (50%+) upside spanning almost every major sector. Highlights include:

Alight (ALIT) - Imminent removal of Blackstone supply overhang to cause shares to re-rate towards peers. TP $20 (100% upside).

Bayer (BAYN GR) - Forgotten stock with activist involvement to push for potential Monsanto spin. TP €82 (60% upside).

Equitrans Midstream (ETRN) - Completion of long-delayed pipeline to drive EBITDA inflection + takeover target. TP $16.50 (80% upside).

Golar LNG (GLNG) - Simplified LNG play with several enormous contracts finally nearing fruition. TP $40 (65% upside).

Secure Energy Services (SES CN) - Waste co. disguised as an oil services co. poised for material re-rating. TP C$13 (100% upside).

Arete Research

DTC subscriber growth has stalled in the face of price increases, marketing cuts and future content reductions, while the company’s cost allocation accounting means streaming losses in FY22 ($3.4bn) were understated relative to the accounting policies of Warner Bros Discovery / Comcast to the tune of $2.5bn, giving an indication of the challenges. Despite assuming a DIS / Hulu merger, Arete expects DTC to generate one-third less EBITDA long-term than they previously modelled and have lowered their TP from $94 to $65 (25% downside).

Huber Research Partners

Post Q2 results, the stock trades at 20.9x/16.2x Craig Huber's 2024/25(E) EBITDA and 26.6x/19.8x EPS, which appears attractive given his expectation that revenue growth should accelerate in Q3 (estimates +6.8% y/y) and Q4 (+10.0%) and remain at 10%+ in 2025/26. Ad-supported tier and password sharing initiatives should start to materially contribute to higher overall average revenue per member in 2024 and long-term secular trends favour NFLX. He estimates that 35-40% of its content is developed outside the US which is a huge competitive advantage vs. peers on several fronts, especially with the ongoing Hollywood strikes. Craig increases his 12-month TP to $500.

Paragon Intel

Fish-out-of-water CEO will struggle to build long-term value - Paragon’s sources provide negative feedback on Chris Cocks who describe a leader with disdain for the core fanbase and contempt for subject matter expertise. He follows his gut rather than data or the advice of those in specialist roles and builds a deeply negative company culture rife with burnout and attrition. Cocks will focus on streamlining the company’s operations and “doing fewer things better,” but he has neither the finger on the pulse of the fanbase nor the maverick vision to turn around a company that has struggled to expand its market share.

The Edge

This recent Spinoff from BorgWarner provides an enticing opportunity. PHIN, a supplier of automotive engineering and technology solutions, has witnessed heavy index selling pressure and is mispriced at current levels, trading at a 32% discount to its peers even though it has a lower leverage to its peers (1x vs. 2.2x), strong FCF generation & conversion (15% of FCF yield on a market cap) and has a pending dividend (in the 2% to 3% range). The Edge sees more than 50% upside from here.

Housing Research Center

Despite forecasting a small miss (on the top line and bottom line) for 2Q23, Alex Barron remains bullish. There is underlying demand that should increase each year for another five years based purely on demographics. If i/r remain near current levels, supply is likely to remain restricted. If i/r were to come down, Alex thinks demand will increase substantially. TMHC has the highest upside among the top 10 builders, which remain attractively valued relative to historical valuation metrics and given they are stronger companies today with lower risk profile they should be trading at much higher multiples. TP $79 (60% upside).

Gordon Haskett Research Advisors

TXRH is due to report Q2 earnings on July 27th and Jeff Farmer is looking for SSS / EPS upside - he models Q2 EPS of $1.24 with SSS +9% which reflects 1) the already reported +8.6% Apr SSS, 2) HSD% average SSS in May and Jun with GHRA’s traffic data showing that Y/Y average traffic growth was similar to Apr and 3) 5.6% menu pricing, down from the 5.9% menu pricing in Q1. He forecasts +6.6% Q3 SSS and EPS of $1.08. TXRH remains Jeff’s top casual dining pick. He sees it as the lone casual dining concept delivering MSD SSS, positive traffic, MSD% unit growth and mid-teens% EBITDA growth across 2023 and 2024.

Cmind

Cmind expects LUV is very likely to miss its Q2 earnings, scheduled for release on 27th July - their latest prediction shows that the probability of beating the consensus is 0.25. Comparing LUV against its peers (Delta Air lines, United Airlines and American Airlines) they find that the ratio Cash/Operating Profit of LUV exceeds 75 percentile and Receivables - Estimated Doubtful is below 25 percentile of the same metrics of its peers. In addition, linguistic signals indicate excessive CEO evasiveness, and CFO and analysts bullishness from earnings transcripts. Finally, LUV has missed its targets in the past two quarters.

Inflection Point Research, LLC

JNPR is seeing slowing service provider sales, increasing competition and has a dismal technology roadmap - IPR’s industry checks reveal a bleak picture for the company in the short, medium and long term. It is not benefiting in any way from the significant shift in cloud capex from “normal” networking spend to AI deployments. It is the only networking OEM that hasn’t bought 800G test equipment yet. Currently, the 800G tester market is taking a breather but will burst wide open by 4Q23. Unfortunately, IPR does not see how JNPR will be participating in the beginning of the largest networking upgrade cycle in decades.

Sales Pulse Research

SPR’s latest channel checks reveal surprising weakness - although PANW still has time left until the close of its fiscal year, SPR notes that it has been quite a while since they picked up weak checks, even mid quarter. Interestingly, their checks on Fortinet have been more positive. So what is happening at PANW? Possible factors include 1) pushback by customers against multiple significant price hikes, 2) in this macro environment, big deals are easy targets for delay, 3) SPR has picked up numerous examples of complaints about the firm's Tech Support.

Japan

LightStream Research

Having suffered an 80% loss in value over the last 8 years, Oshadhi Kumarasiri believes Rakuten has emerged as an enticing prospect for value investors. His analysis shows that the combined fair value of Rakuten's Cards, Bank and Mobile businesses now surpasses 100% of the company's M/Cap. Furthermore, Rakuten Ichiba (Japan's leading e-commerce business) also appears significantly undervalued. Oshadhi sees upside potential of up to 130% for the stock in the short to medium term.

Emerging Markets

RedTech Advisors

Every time Douyin enters a new sector, the incumbents suffer - RedTech’s 2Q23 local services survey is more evidence of that trend but with a slight twist. After more than a year of making inroads in local services, Douyin is winning share but so is the top player, Meituan. The biggest loser is Alibaba. RedTech’s survey includes responses from 1,000 online consumers in tier 1-6 cities. The sample city tier weightings are 20%/20%/30%/30% for tiers 1/2/3/4-6.

Smart Insider

Krishnasai Tanneeru (Senior Officer), Renuka Ganesh (Divisional GM) and Veena Vasanth (Senior Officer) made large % sales in Jun, reducing their holdings by -65%, -100%, and -39%, respectively. These are also the largest disposals of shares that any of them have made and at lower price points than prior sales. Smart Insider ranked this stock -1 (lowest rating) on Jan 4th based primarily on sizeable sales from five operating officers at prices ranging from INR 262-282. The stock has moved lower since then and it is concerning to see this new cluster of officers significantly reducing their holdings.

Silk Road Research

China 2Q23 elevator survey

The % of dealers expecting positive orders growth in 2023 exceeded those expecting the opposite by a net +20%, the highest in four quarters. Industry sentiment improved to a six-quarter high, although remained below 2020/21 levels. SRR’s survey readings also indicated a stable pricing environment. While customer receivables have improved from a year ago, SRR’s June reading was the lowest in 13 months. That said, this metric remained above levels seen prior to recent government measures aimed at improving the liquidity conditions for developers, with the recent extension of those initiatives through 2024 seen as a positive. Relevant stocks: OTIS, KONE, Schindler, Yungtay and Canny.

Horizon Insights

While China's recovery may not have met investor expectations, Horizon Insights believes this is merely a temporary setback and are confident that the country's economy is transitioning towards innovation. Anker is a shining example of a Chinese brand that has successfully leveraged innovation to carve out a significant global presence. Its strategic foray into the rapidly growing portable power storage market and the burgeoning home security market underscores its ability to identify and capitalise on emerging trends. Its user-friendly products, competitive pricing and strong brand reputation have positioned it as a formidable player in the smart device sector.

Macro Research

Developed Markets

Antipodean Capital Management

A new inflationary decade

Craig Ferguson points out that a new inflationary decade of macro variable volatility, policymaker mistakes & activism, demographic change, deglobalisation and geopolitical tension is underway. This suggests that decade long bubbles in growth assets - stocks, property, corporate bonds – that were leveraged to & dependent on low discount rates, yields & excess liquidity should unwind. This unwind started in 2022 and should continue into mid 2024. The correction of the bull cycle should last 24-36 months, end in recession and will see growth assets correct to “cheap” levels by mid 2024.

Steno Research

Why Norway and the UK are the odd ones out on inflation

Although the two economies look worlds apart given their characteristics, they both stand out as extreme inflation cases. Andreas Steno dives into the reasons, including the two countries’ constraints on services workers, Norway’s weak Norges Bank that is way behind the inflation curve, and the UK’s everything-inflation cycle. Andreas is looking to implement a high conviction bet in SHORT Norwegian bonds and/or in NOK swaps soon. He’s also considering adding a bond bullish bet in EURs as a spread against short rates exposure in Norway, seeing a high probability of a landslide in Eurozone inflation over the next three months.

Longview Economics

Germany: A short view

Signs of complacency and froth have continued to build in the US, with a robust case for near-term giveback/weakness. Chris Watling comments that the picture is similar in Europe, but the key difference is that price action in European equities is notably poor. The DAX, in particular, has traded sideways in recent months, and the poor price action has been confirmed by a widening of BTP-Bund spreads (see chart). With it lacking momentum and appearing to be rolling over, the DAX is an attractive short opportunity in global equities. Move ¼ SHORT September DAX futures at current prices 16,135. Place stop 2.5% above entry.

Greenmantle

Europe: Talk like a hawk

The euro area entered a technical recession in 1Q23. Looking ahead, Niall Ferguson expects GDP to decline again in 2Q23, as consumers cut back on spending and private investment falls further. At the same time, he believes the ECB will deliver a 25bps hike at the monetary policy meeting on July 27. He also expects euro area policymakers to continue striking a hawkish tone in the coming weeks as they seek to keep the ECB’s future policy options as open as possible. This leaves Niall tactically SHORT Bunds over a one-month horizon.

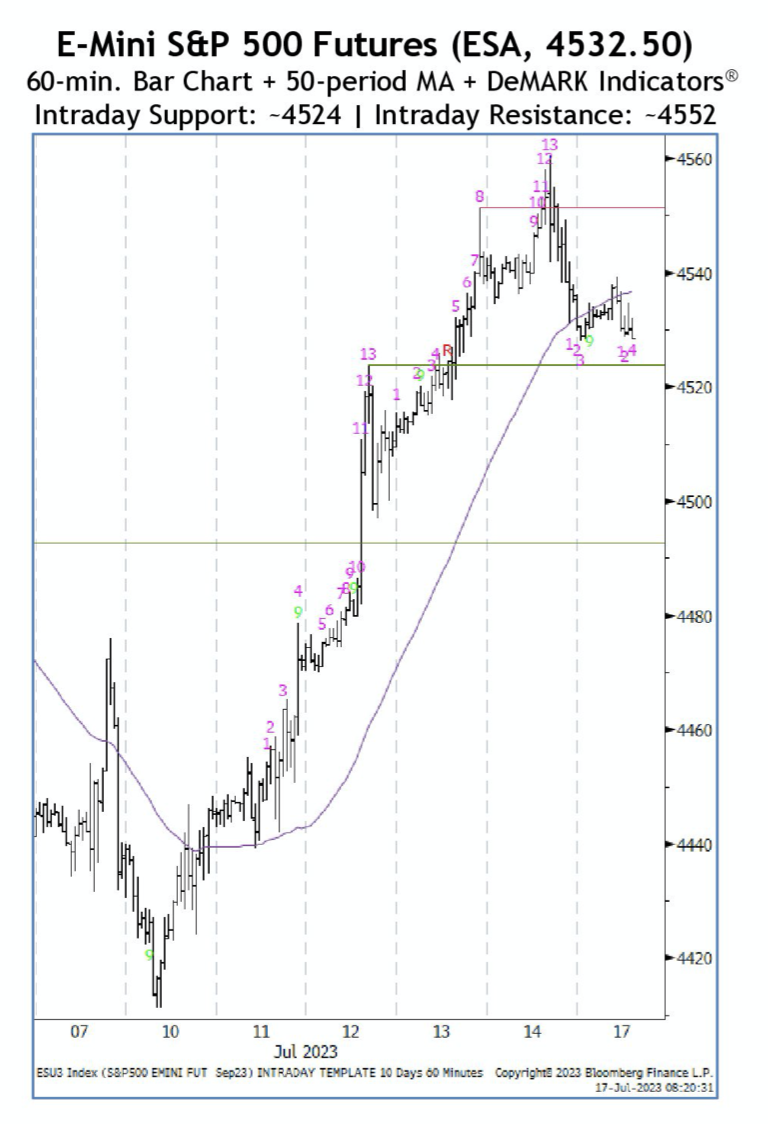

Fairlead Strategies

SPX objective reached

The major indices pushed higher ahead of the earnings season, allowing the SPX to reach the measured move projection of -4,510 last week from May’s breakout. Momentum gauges still point higher, suggesting the SPX may make progress towards minor resistance from early 2022 near 4,600. However, be wary of any downturns, with the Fairlead Strategies team noting that signs of upside exhaustion have arisen for the SPX and NDX.

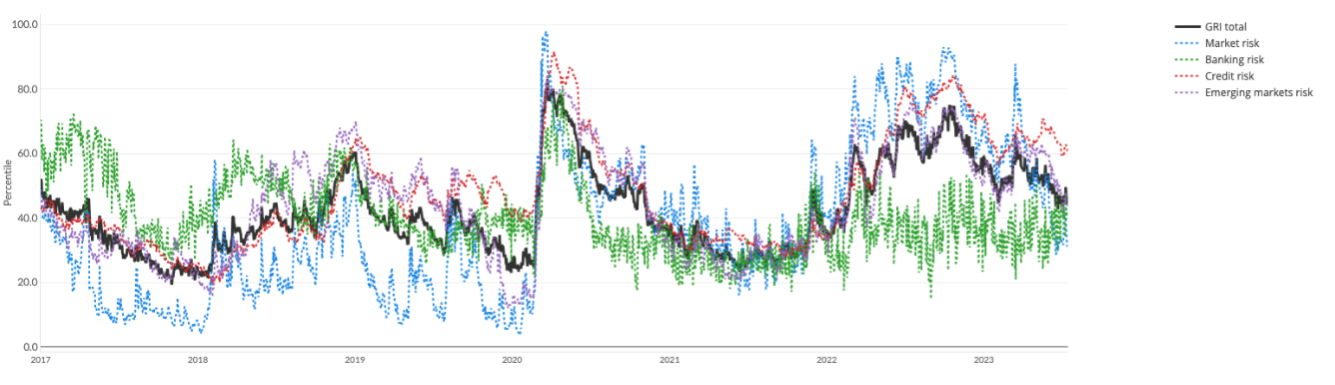

Deep Macro

What is global risk appetite like now?

Global risk is somewhat below trend, and falling. The chart shows the Deep Macro Global Risk Index, a composite of risk indicators from four different categories: market risk, banking risk, credit risk, and emerging market risk. Currently it is in a "low and falling" state. Jeffrey Young points out that there was a moderate increase in banking risk in March, but the increase was minimal. Inflation was the driver of the increase in risk aversion from mid-2021 until autumn 2022; but after inflation peaked, risk sentiment improved, even though central banks around the world were at peak hawkishness. The lesson is simple: inflation is the big threat to risk appetite, not interest rates per se. If interest rates rise to take care of inflation, markets are capable of dealing with it.

Emerging Markets

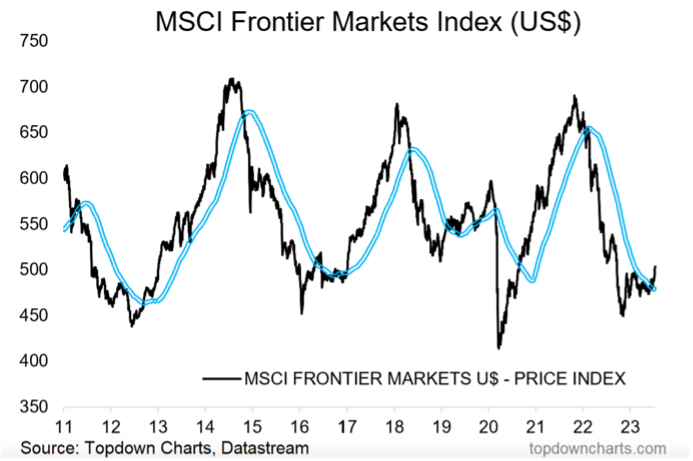

Topdown Charts

Bullish signs in frontier markets

Frontier market equity technicals are looking up as the MSCI FM index notches up a new high and pushed above its 200-day MA (see chart). Callum Thomas believes the strategic case for frontier markets is intriguing and mostly overlooked. FM equities sit at the top of the expected return table, have historically traded on lower correlations vs other major chunks of global equities and lower historical volatility than EM equities. The FX situation is also consistent with the bullish technicals and strategic outlook, with FM FX trading at record cheap valuations and FM FX breadth trending up.

The Macro Compass

Finally emerging?

Selected emerging markets are having a great year, with equity markets like Poland and Mexico already up 25-30% YTD. EM currencies have been broadly appreciating against the USD. The macro context generally required for a sustained EM rally includes disinflationary, below-trend growth in the US with a weak USD benefitting the EM space, and strong global demand and trade growth. We have a lot of the first scenario and a little bit of the second. The team are currently LONG Poland and Latin America, mainly Brazil with its promising growth story.

PRC Macro

China: Energy is the new property

Despite challenges from property developer and local government austerity, China experienced an acceleration in infrastructure investment and energy-related industrial production in June. William Hess sees this as indicating a shift away from the property cycle and towards energy-related investments, driving restocking and downstream durable goods demand. As manufacturing destocking is expected to transition to restocking by Q3, William expects domestic producer prices, RMB exchange rate, A-shares, and copper prices to rebound. Beijing only needs modest H2 growth to meet the 2023 target, reducing the likelihood of significant fiscal stimulus.

Trivium China

China: Stimulus needed

The June monthly economic data is bleak: retail sales rose only 3.1% y/y, while fixed asset investment (FAI) rose only 3.1% y/y. Growth is increasingly reliant on the state sector, as SOEs increased investment 7.4% y/y in June, but private firms cut investment 0.6% y/y, with real estate investment dropping 10.3% y/y. The dire performance of the economy in Q2 means that without effective stimulus measures, there is a genuine risk China won’t hit this year’s GDP growth target of 5%. To avoid this outcome, the need to support the private sector – particularly households – should be an open-and-shut case at this month’s Politburo meeting.

Alberdi Partners

Who will blink first, Argentina or the IMF?

Argentina is on the brink of a financial catastrophe, with the stability of USD-denominated deposits preventing a complete collapse. Even with the scheduled IMF disbursement, the outlook for reserves is dire, making negotiations all the more important. Both parties face difficult choices: the IMF wants to avoid sending Argentina to default but has zero confidence in the administration, and the government is stuck between a rock and a hard place between devaluation and going into arrears with the IMF. Marcos Buscaglia believes the government will have to blink first and expects the FX gap (and bond spreads) to rise substantially as negotiations head until the end of the month.

Teneo

Kenya: Trigger moment

Kenya is on the brink of a major showdown as the opposition plans three days of protests, defying President William Ruto’s warning. The demonstrations, fuelled by public anger over Ruto’s controversial tax plans, have gained momentum and pose a significant challenge to his administration. The recent protests, marred by violence and arrests, have caught the attention of the international community. With the potential for escalation and echoes of past ethnic violence, the situation remains precarious. There are whispers of a possible political compromise, with Ruto seeking a ‘handshake’ agreement with opposition leader Odinga, but such a move is fraught with challenges and risks further weakening the opposition.

Emerging Advisors Group

Pakistan’s rebound

Sure enough, Pakistan markets have rebounded in light of the new IMF program announcement. It’s easy to make the case for near-term stabilisation: the current account is essentially closed, interest rates have shot up, Saudi and China have committed new financing, and the rupee may trade stronger soon. However, Jonathan Anderson explains that, as before, there’s no structural fix; the country still has no export base, hasn’t resolved its fiscal or monetary imbalances, and now suffers from a permanent debt overhang. Jonathan does hold dollar debt and has no problem with tactical FX or equity exposure, but he stresses they are speculative positions – it’s quite difficult to make the case for Pakistan as a fundamental buy.

ESG

Saltmarsh Economics

Europe’s carbon footprint

Recently, the Saltmarsh Economics team examined emissions intensity and environmental productivity of 70+ sectors in each euro area economy. They also take a broader look at emissions, analysing the carbon footprint of each European economy: how it is calculated and how it is evolving. The results provide a macro perspective on Scope 1, 2 & 3 corporate emissions, and offer an alternative take on the direction of overall carbon intensity of industries. Please contact us to find out more.

Commodities

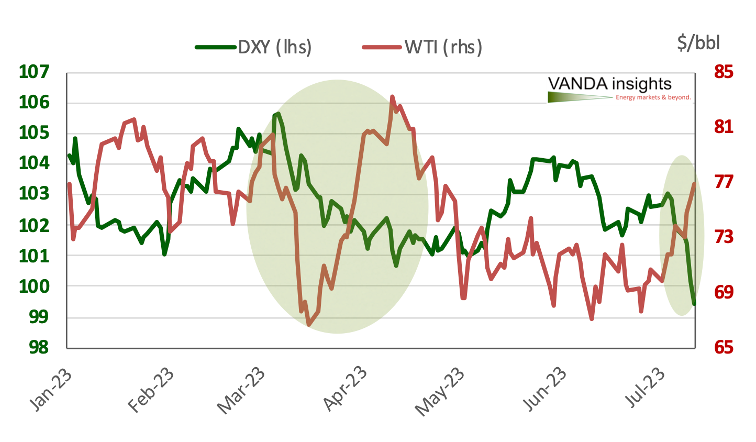

Vanda Insights

A crude correction

The cooling signs of US inflation have boosted investor confidence and conjured up the prospect of a feasible soft landing. However, many economists have warned that the Fed may continue its hawkish approach, continuing the rhetoric tug-of-war that has played out at the centre of financial markets since last year. There are even more dots to connect for oil market participants, but Vandana Hari believes there is a good chance of the rosy economic narrative getting a reality check, pulling crude prices lower. The recent lift from the falling dollar may help crude prices (see graph), but investors should be wary that the inverse relationship may only continue for as long as the dollar remains under pressure.

Global Macro Investor

Don’t miss out on Crypto

The chart of Crypto Total Market Cap Exclude BTH and ETH is one of the most bullish charts Raoul Pal has ever seen, which may well give us a repeat of 2015-17; this has been Raoul’s base case for a while. This would ignite Solana, which will break the inverse head-and-shoulders. There’s also some big news brewing in the crypto space, with the Bitcoin spot ETF about to get passed. Interestingly, when the SEC asked all of the ETF providers to say which exchange they will use, they all said Coinbase, which Raoul sees as a repeat of Amazon in the early 2000s. BUY Coinbase, Ethereum, Solana and double KR1 LONG position.

Inferential Focus

LNG has moved into a sweet spot

The Liquified Natural Gas (LNG) market is growing at speed, with interregional LNG trade growing more than four times as fast as pipeline trade from 2011-21. Long-term deals for LNG are multiplying, which will help finance the construction of new export facilities and create jobs and economic growth in the US. It may also provide a formidable barrier to more renewable installations, including solar and wind, whilst decreasing the leverage of major pipeline gas producers. Expect Korean LNG shipbuilders, companies building terminals and export facilities, and the UAE to all benefit.