Company & Sector Research

Europe

Huber Research Partners

Teams up with Nvidia to use generative AI to produce advertising at scale - Doug Arthur continues to like the moves of the new management at WPP, who are quietly right sizing the company, vastly improving the balance sheet and feeding interesting growth initiatives. This new partnership, among other facets, should allow WPP to replace costly aspect of ad production with an AI approach potentially vastly reducing time to market as well as costs. At Doug’s TP of £12.50 (45% upside), the stock would be trading at 6.7x estimated 2024 EBITDA and 11.3x adjusted EPS as well as 9x FCF.

Woozle Research

Woozle upgrades the stock to Buy based on findings from their recent surveys - store managers report LFL sales growth of +3.5% in 2Q23 vs. the same period last year with sales rising sharply in recent weeks after a muted start to the quarter. 40% of respondents report sales are trending ahead of internal targets (with only 10% underperforming). This is a much stronger performance than other names under Woozle's coverage such as H&M and Superdry. Promotional activity is unchanged due to healthy inventory levels and strong sell-out trends. While summer ranges have been particularly strong, menswear has seen stagnant sales trends due to rising competition.

Smart Insider

Insider selling has picked up in a meaningful way in May, as six officers have sold a total of 1.6m shares at prices ranging from £2.65-£2.81. Adrian Morris has sold 634k shares, 591k of which are option related, but this is greater than his combined sales since joining. Christine Heffernan sold 175k shares, her largest sale and 5x her only other sale in Nov 22 at £2.77. Alessandra Bellini, Gerry Mallon, Jason Tarry and Ashwin Prasad are also making large sales. While SmartInsider would expect to see some insider selling given the strong share price performance over the last 9 months, some of these sales look particularly aggressive.

Starling Advisors

Focus on organic growth opens a new chapter in the equity story of CLNX - Alex Dwek believes the telecom giant is well positioned to benefit from its strong position within the European 5G ecosystem. Now that BTS and expansion capex are being reduced, organic growth will allow for CLNX’s tenancy ratio to increase (from 1.36x) and be more in line with peers such as Inwit (2.16x) and Vantage Towers (1.45x). Shorter-term catalysts such as the appointment of a new CEO (Marco Patuano), a significant deleveraging (from 6.5x net debt/EBITDA) and a strong cash flow generation, as well as reaching investment grade should also support the fundamentals. TP €56 (50% upside).

Click here to access the full report.

the IDEA!

Following the news that Czech investment group PPF has increased its stake in INPST to 16.75% (with an option to buy a further 15% stake from Advent), analysts at the IDEA! wonder if we could be seeing the creation of a new giant in transport and logistics. PPF is no stranger in e-commerce and last mile logistics and nor are its partners (includes the two Czech billionaires, Daniel Křetínský and Patric Tkáč). Consolidation within the sector looks set to continue and by combining the activities of INPST, Packeta (believed to be for sale) and those of EP Logistics, this would create a very dominant player in central and south-eastern Europe.

North America

Holland Advisors

Andrew Hollingworth has previously been keen to highlight the many aspects of NFLX's long term Sustainable Competitive Advantages while also being attracted to the short-term price discovery that was due to occur because of password-sharing changes. Following the recent news that each user not from the main household will now have to pay $7.99 in the US and £4.99 in the UK, Andrew’s prior calculations are revealing - he suggested that just a single add on charge of $4 p/m income for each of the 100m password sharing households would add $4.8bn in revenue; EBIT margin would jump from 20% to 30% and RoNTA from 14% to 25% - it's operational gearing on steroids!

Arete Research

The heavy lifting on restructuring is now largely complete (Paramount and Disney are just starting theirs) with expenses down $2.8bn and cash content spending running at ~$4bn/qtr. Studios look likely to recover from 2H23, advertising looks to have bottomed, and the new Max streaming platform has a good mix of content that should be attractive to all viewers meaning top and bottom line should show amelioration from here. Arete forecasts EBITDA of $11.2bn in 2023 and FCF of $4.4bn. For 2024, they expect a further improvement in EBITDA to $13.1bn and FCF to jump to $5.9bn (net debt declines to $36.1bn (2.8x) allowing a buyback to start late in the year). TP $31 (130% upside).

Gordon Haskett Research Advisors

Chuck Grom’s recent downgrade of the stock proves timely as the share price plummets on the back of dismal earnings - it is third time in the last four quarters that DG has missed Street estimates. Taking a step back, several company specific headwinds are playing out between: (a) higher wage investments, (b) elevated store maintenance costs, and (c) pricing gap headwinds…in addition to DG suspending share repurchases while reducing capital to new stores. Chuck also thinks the risk to the basket size giving back some of the gains over the last five years (avg. basket $12 to $17) remains elevated. He lowers his FY23 EPS estimate to $9.70 and FY24 estimate to $10.30.

Gradient Analytics

Earnings quality concerns remain elevated - lower quality unbilled receivables drove outsized growth in total accounts receivable, which grew significantly faster than sales again in Q3. Accrued expenses continued to decline rapidly. Thus, even though prepaid expenses and other current assets improved slightly during the quarter, Gradient remains concerned about the net effect of recent expense recognition trends. They maintain active coverage with a negative outlook. MRCY's share price has fallen c.30% since they initiated coverage (Jan 22).

Abacus Research

Has proven itself to be resilient and defensive with significant improvements over the last few years - OTIS shares can generate an IRR of 10-13% with less than market risk and limited downside. Its market share will continue to increase because of digitisation in the industry, which favours the OEM, a meaningful change vs. 5 years ago. The Services business (84% of profits) can continue to deliver ~6% growth while improving operating margins. Abacus sees EPS growth of 10-12% for the next few years, fading to ~9-10%. Plus a dividend yield of 1.7%. Stock should hold its multiple.

MAPsignals

Materials stocks are set to rally hard

Too much selling often signals a very bullish setup and that is exactly what happened to Materials stocks on May 31st - Lucas Downey remarked that it was the most red he had seen in the group since Sep last year. 30 discrete stocks were dumped. Going back to 2013, there has only been 33 instances where 30 Materials stocks or more were sold in a day. This showcases how rare this action was. Looking at the forward returns of the XLB post these selloffs: the fund gains 3.3% a month later; 6 months later it is up 19.6%, and a year later it is up 32.9%! This is the power of the MAPsignals process. They don’t follow the news, they follow the Big Money! Click here to access the full report.

BWS Financial

Hamed Khorsand thinks ADEA could be the most under the radar AI beneficiary through its patent portfolio related to hybrid bonding. Key points from his report include: 1) ADEA has secured nearly the entire DRAM and flash market through licenses and is expected to broaden to image and logic semiconductors. 2) Hybrid bonding is expected to help usher the next generation of semiconductors to handle the growing need for speed and bandwidth with lower power consumption. 3) ADEA’s stock has been mainly valued on the FCF the business is able to generate from its media patent portfolio with little value given to its semiconductor patent portfolio. 12-month TP $16 (50% upside).

MYST Advisors

The presenter (at MYST’s latest TMT Idea Forum) views TEAM as a timely opportunity due to its nascent SaaS transition that he describes as “the most terminal value-accretive” he has ever seen. He models post-transition FCF of $20-25/share (vs. consensus at ~$10/share), but says this could prove conservative, as he notes that Autodesk and Adobe both saw FCF generation increase by ~5x over the course of their transitions. He also highlights a key misperception among investors, with many expecting just ~16% of the installed base to see a material repricing of 3-4x vs. his belief that 80% will reprice to ~8x (or more) pre-transition ARR. TP $550 (~230% upside).

ChartWizard

SPGI reached a high of 477.41 in Dec but subsequently experienced a correction, losing over 42% from its peak. The stock has since formed a bullish ascending triangle, supported by technical indicators, suggesting a potential breakout to 440 in the coming weeks. SPGI's position in the improving quadrant of the RRG indicates a likely period of relative outperformance, with the RS line rising against the broader S&P500. A breakout in RSI and a close above 385 could lead to a 15.75% appreciation, while a close below 345 would invalidate this setup.

Valens Research

As the world relentlessly shifts towards cashless payments, giants in payment processing such as Visa are central to this revolution. Despite initial lagging behind its rival, Mastercard, in developing high-profitability partnerships aimed at digital and e-commerce solutions, Visa is now mirroring its competitor's strategy. It's concentrating on expansion into digital solutions and pouring significant investments into partnerships. These efforts are now positioned to start reaping benefits for the company.

Blueshift Research

Connectivity, speed & scale combine to blow up IT as we know it

In John Harrington’s latest Tech Trends report, he looks at several factors that have combined to change IT development and sales dynamics. These include how the accelerating deployment of speedier wired and wireless connectivity to the cloud, very fast computing platforms being built at scale within the clouds, the accelerating development of quantum computing as a viable commercial business, and the development of serious AI capabilities are affecting the global digital landscape. As IT increasingly transitions from in-house networking to the cloud, some new areas of IT will benefit, while others face an uncertain future.

Positive: Advanced Micro Devices, Alphabet, Apple, Amazon, Broadcom, Ciena, Dycom, Intel, IonQ, Microsoft, Nvidia, Rigetti.

Negative: C3.ai, Cisco, Dell, Qualcomm, Salesforce.

Japan

JapanConsuming

Key stories from Japan's retail & consumer markets

Consumer Discretionary / Staples

Highlights from this month’s issue of JapanConsuming include: 1) The great divide: Isetan & Hankyu break records as regional stores close. 2) Rakuten’s Seiyu sell off will boost netsuper business. 3) Authentic Brands to open office in Japan’s “¥3trn brand paradise”. 4) Yaoko: 34 years of record profits. 5) Ecbeing nears ¥1trn in GTVs. 6) Big apparel revival: Onward up again, Sanyo Shokai finally makes a profit. 7) Seven & I CEO survives - just about. 8) Their 'FOCUS' article examines whether today’s ‘normal’ is the same as it was back in 2019: record levels of income, full to bursting savings accounts, alongside subtle signs of a falling propensity to save mean people are out spending again.

Emerging Markets

Aequitas Research

In Sumeet Singh’s earlier note in 2022, ‘Tencent investee selldown - The US$120bn global overhang’, he had looked at the group's overall investment portfolio. With two of its heavyweight investments having now been spun-out, Sumeet re-looks at Tencent’s shareholdings in various companies to try and gauge which ones it could sell out of and how. In terms of regulatory scrutiny, Pinduoduo is probably very high up on the list, alongside Kuaishou, Futu and PolicyBazaar. Announcements re. the divestments of JD.com and Meituan occurred towards the end of 2021 and 2022, respectively. Thus, some of these names could start to come under pressure by the last quarter.

Propitious Research

Wium Malan examines the industry and macro-environment and analyses what he believes to be the three key controversies in JD’s investment case, namely: slowing revenue growth, margin progression, and its significant net cash balance sheet. He notes the stock now trades on only a 4.1x Dec-23 PE multiple (excl. net cash balance sheet and associates at book value) and on an extremely attractive 12.8% NTM FCF yield, which is a significant discount to its historic average trading range and its global peer group.

Tabbush Report

There are few banks like PNB which have seen NPL ratios decline from 10.9% to 6.8% over the past 12 months. Operationally, there are not many with such a robust delta in core NII, NFI, and given relatively pedestrian loan growth (+7% y/y to 1Q23 while NII was +23%). Despite all the positive developments the PNB story still appears hidden within Asian banking. Daniel Tabbush highlights m/cap to assets of several major banks in the region, where PNB is at 2.5% vs. others that are >10x higher. On more traditional metrics like PE and PB, PNB also appears overlooked (or more likely under covered), but with continued strong results Daniel is not convinced that it will remain hidden.

Alembic Global Advisors

The shares have underperformed peers by a whopping 77% since Mar 2019 - Hassan Ahmed believes this is unwarranted and argues that the company’s geographic and feedstock diversity, along with improving fundamentals, isn't appreciated by investors. He continues to believe that a takeover is the most likely outcome and sees the recent bid as a win:win for shareholders and acquirers: shareholders would be able to sell at almost double the current share price while the acquirers would obtain relatively new and world-class assets at a replacement value of 0.54x. He increases his 12-month TP to R$35.

Entext

Sean Maher takes a 110% profit on Japan's Advantest in his semi basket after the Nvidia inspired surge, but still thinks SK Hynix remains undervalued and the key high bandwidth memory play as AI inference explodes. Sean has added Taiwan’s server maker Wiwynn to his networking basket as a key play on booming demand through end decade for its lower power consumption / heat generation technologies in AI server clusters. Climate change and the energy transition also remain key themes, driving secular AC and heat pump demand; Carrier has been added to his transition basket on its M&A reinvention as a HVAC / heat pump pure play.

Macro Research

Developed Markets

Global Macro Investor

The Exponential Age has begun

Raoul Pal has long believed that The Exponential Age, a revolutionary transformation of the world into a new digital era, would come. It has now arrived. We’re at that really sweet spot in the cycle where no one believes what is happening in tech and everyone is underweight equities. A sharp correction in the short-term is likely, but any purchase of stock stocks will soon pay off very well. Any sell-off is an opportunity to buy more. BUY NDX, tech stocks such as Google and Microsoft, and crypto including Ethereum and Solana. Don’t miss out.

Belkin Report

Volatility and interest rates are headed higher

Michael Belkin comments that the stock industry group rotation suggests a cyclical slowdown that would warrant lower interest rates, but a structure is in place that could drive interest rates higher this year due to massive debt issuance. A weaker economy with higher interest rates is the worst of all possible worlds. This is potentially positive for the USD, but negative for corporate earnings and tech stocks, obviously contradicting the current infatuation with AI. But nothing continues forever, and market tops are legendary for luring investors in before major reversals. Bonds and stocks are recommended SHORTs on brief good-news bounces.

Ekins Guinness

Bonds: Shaken, not stirred

Bond markets are still in a downtrend, but nominal yields and some real yields are starting to look attractive. It’s quite hard to imagine that they are attractive long-term investments given such high and growing debt levels, but the fact is that inflation has peaked and is falling. The contraction in monetary aggregates especially in the US is, according to some monetarists, at a level not seen in post-war history which might propel bond yields down. Gilts triggered oversold flags in the last week of May, albeit not as extreme as the disastrous mini-budget last September. The bond downtrend is gradually being replaced by an improving shorter-term uptrend. The case for bonds is building.

Topdown Charts

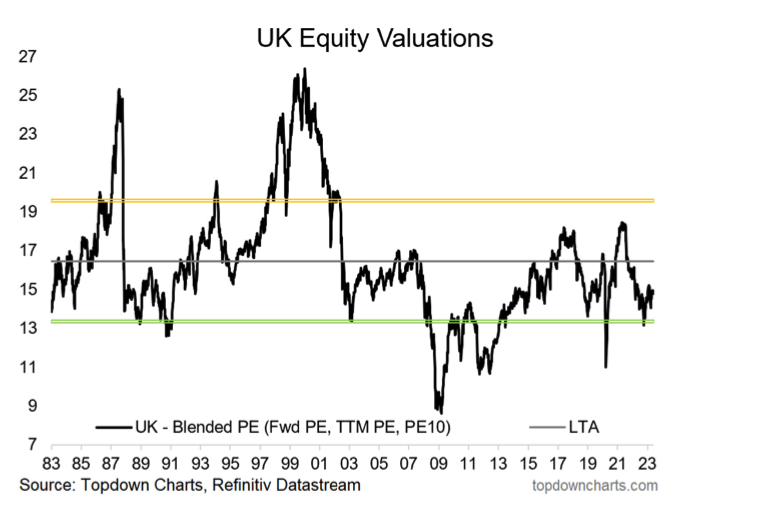

UK: Lagging behind

UK equities have had a decidedly less impressive run relative to Europe and are now trading at a minor discount vs their European peers, and at a decent discount vs global equities, claims Callum Thomas. Earnings sentiment is turning up from mild pessimism, US investor allocations remain near record lows, and valuations remain cheap, so there is a mild contrarian bullish setup. Callum Thomas is mildly bullish UK equities.

Eurointelligence

Germany: Fragmented coalition

Germany's ambitious traffic light coalition under Olaf Scholz aimed to modernise the country and lead in the energy transition, but after two years their agenda is faltering. The parties are divided, and Scholz's leadership style isn't helping. The biggest problem? The budget. With disagreements on spending cuts, the coalition is in turmoil, yet Wolfgang Münchau is confident no new elections are ahead since another coalition would simply not be possible. They will govern and squabble to the bitter end in late 2025. In the meantime, things are likely to get worse - a lot worse.

Grey Investment

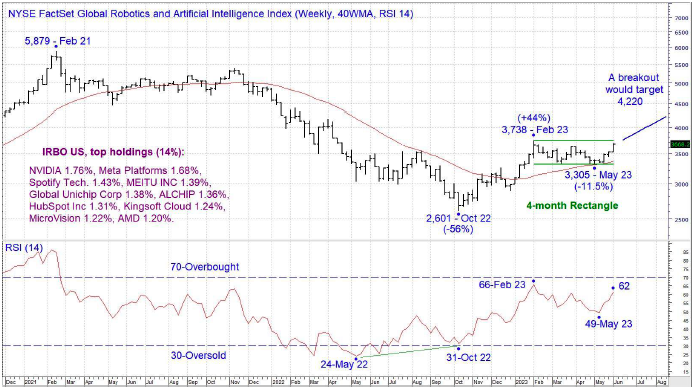

US: NYSE Global Robotics & AI Index

The index (NYFSRAI, 3,700) has been ranging for 4 months following an initial advance from last October’s low. A weekly close above 3,815 would be viewed as a breakout from the Rectangle targeting 4,220. If that target gets approached, the case can be made that a breakout from a larger Head & Shoulders base is underway targeting 5,000+. The Grey Investment team will go LONG the NYFSRAI if a weekly close above 3,815 occurs.

Greenmantle

Japan: Land of the rising dove

In April, more than half of Japanese CPI components were up over 2% y/o/y. However, the greatest price increases are concentrated in goods, and inflation in stickier sectors remain well below 2%. FX base effects will soon turn disinflationary. Meanwhile, negative real wages are crimping consumption while weakening global demand weighs on the export sector. Niall Ferguson is increasingly confident that BoJ Governor Kazuo Ueda shares his analysis and is prepared to tolerate a substantial overshoot of 2%. Believing that a break from the yield curve-control (YCC) policy would be highly contractionary, Ueda will retain dovish forward guidance until he is confident Japan has achieved 2% inflation. This is a long way away and Niall therefore remains SHORT yen and LONG Japanese equities.

HCWE & Co.

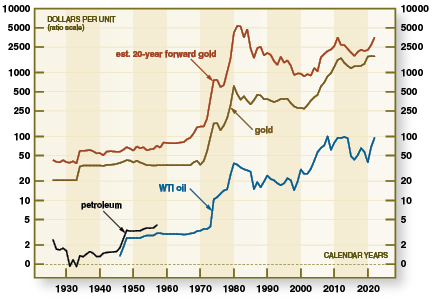

The three central prices that govern inflation

David Ranson states that the prices are central to the economy's price system: gold, long zero-coupon T-bonds, and crude oil. They orbit around one another. Prices for goods and services throughout the economy, together with their rate of inflation, are "tethered" to, and driven by, these three. To understand and anticipate overall inflation attention must be paid to these, the fastest moving and most influential prices in the entire system. The absolute centre of the price system is approximated by the price of forward gold far out in the future. All other prices, in the end, move proportionately.

Radio Free Mobile

Rise of the machines?

The big names in AI are now saying that mitigating the risk of the robots enslaving the human race is as important as dealing with pandemics or nuclear war which Richard Windsor claims is either peak hyperbole or a cynical attempt to keep the smaller players out of the nascent AI industry. The big question is whether these large language models (LLMs) have somehow obtained the ability to think. Richard points out there are indications that these machines are not thinking but simply regurgitating and reconstructing data. Indeed, the real threat of generative AI will be driven by humans who desire to commit bad deeds and use it to do so.

Musha Research

The era of low interest rates is not over

Views are becoming widespread that the era of disinflation and low interest rates is over, but Ryoji Musha disagrees. Over the past year we have seen it confirmed that inflation is transitory, with primary inflationary factors almost eliminated and inflation returning to 2%. There is large room for current interest rates to fall, which should occur once the Fed’s policy shift becomes clear; monetary tightening has become harmful, and the Fed will have no choice other than to change. Concerns of asset bubbles occurring due to extreme monetary easing are unfounded. As the world enters a new industrial revolution, expect fears of continuing high inflation to fade away.

Emerging Markets

Creative Portfolios

Which markets should you buy?

The Creative Portfolios team take a quantamantal and behavioural approach to asset allocation, searching for markets which have delivered a strong 12-month relative return but a relatively subpar 36-month return – a strong behavioural system. In their latest report, OVERWEIGHT recommendations include Egypt, Poland and Peru, followed by Thailand, the Philippines and Malaysia. Underweights include the Czech Republic and Saudi Arabia.

Trivium China

China: Grappling with AI

As the world wrestles with the implications of ChatGPT, China’s cyber watchdog rushed out a draft regulation on AI-generated content (AIGC). As it is currently written, it threatens to place big burdens on Chinese tech companies seeking to compete on AIGC, primarily through restrictions on the data used to train AI. However, Beijing isn’t new to implementing controls on new technologies whilst encouraging innovation enough to stay competitive: the internet, smartphones and crypto are all such examples. We will likely see the state accelerate data sharing and trading initiatives, move faster to bolster legal frameworks governing data access, and looking for new and novel ways to improve legal data access.

DeSaque Macro Research

China: The floor has gone

The outlook for a consumption-driven growth model in China looks lacklustre, claims Said DeSaque. Tough market conditions in lower tier cities will depress aggregate national home sales in 2023, despite the apparent return to normality in top tier locations. The removal of the national mortgage rate floor on a city-by-city basis has created an uneven funding environment across the country. It will lower household leverage as existing mortgagors engage in prepayments, which is bullish for financial stability, but it will ultimately be detrimental to consumption in the current state of consumer sentiment and labour market conditions.

Longview Economics

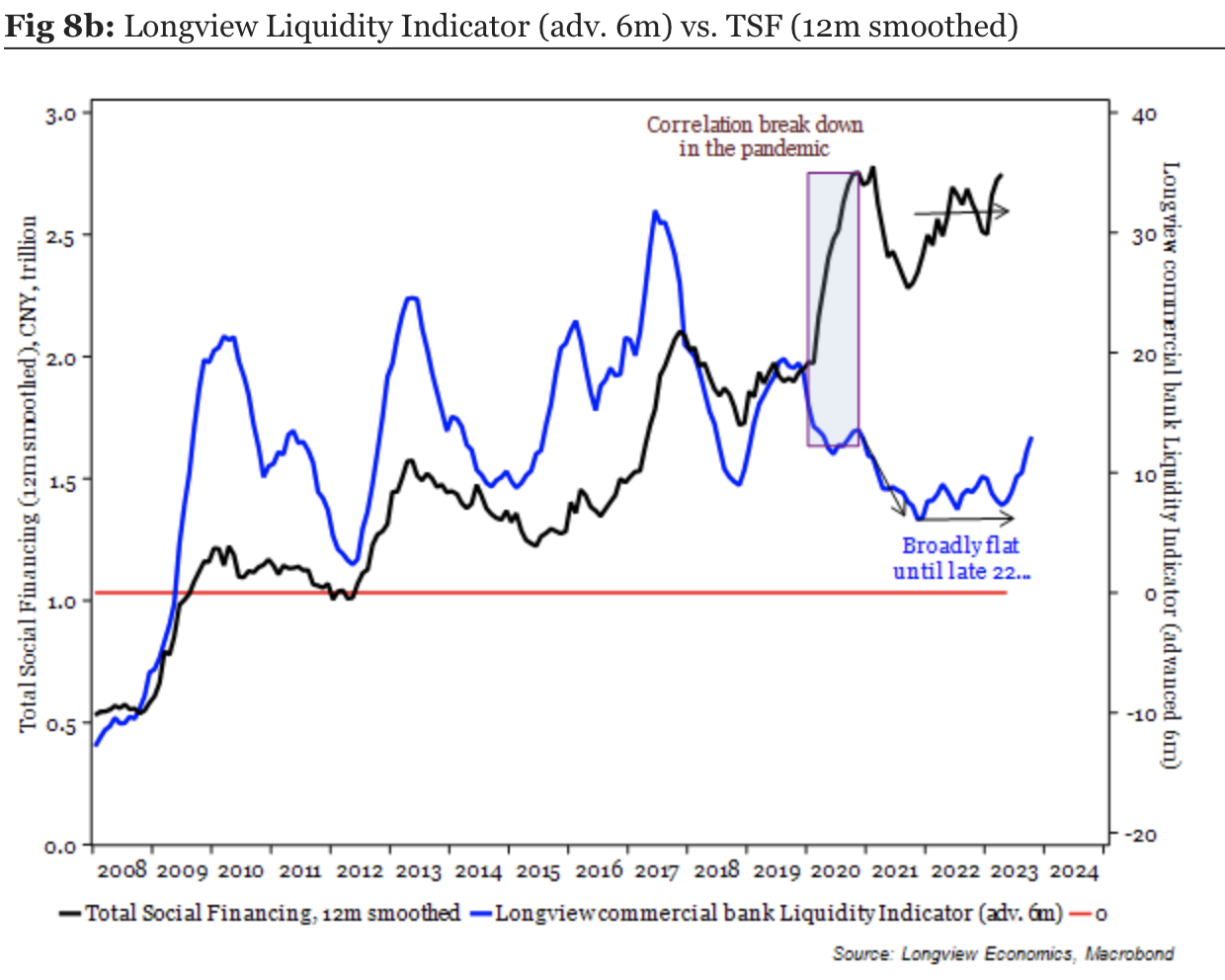

China: Rolling over? Or changing economic growth model?

China’s post lockdown recovery has been surprisingly poor, most notably in parts of the old economy. However, certain parts of China’s new economy have taken up leadership, and we should see policymakers continue to support the economy. In light of recently loosened policy and RRR cuts, Chris Watling revises his liquidity indicator (see chart). Although the country doesn’t remain immune to a US/global recession, expect the economy to move out of sync with the West and remain relatively robust, which Chris stresses is a key theme that investors should recognise.

Alberdi Partners

Argentina: Inflationary surge

Headline inflation surged by 8.4% m/o/m in April and is still running high in May. Marcos Buscaglia therefore expects headline inflation in May to increase to 9%, helped in part by a moderation in meat price increases. Due to benign weather, Marcos believes perishables goods prices have downside risks in the coming weeks. Tamed parallel FXs prices after April’s jump should lead to a deceleration in inflation of tradables goods such as home equipment and clothing. As we enter June, expect a deceleration in headline inflation, albeit a reading that will remain in the high single-digits.

Emerging Advisors Group

Is Kenya a buy?

Kenyan sovereign dollar yields have blown back out in recent months and the shilling has started to give way. Is this just short-term market jitters, or the beginning of the “end” for the Kenyan debt and FX trade? Not necessarily today, claims Jonathan Anderson, as we could see Kenyan spreads reining back in if the market calms down; after all, Kenya has a different liquidity picture than, say, the recent stress cases of Ghana and Sri Lanka. However, the country remains fundamentally insolvent, with no hope of repaying its debts over the medium-term and thus no escape from what Jonathan believes will be an inevitable default and restructuring.

Greenmantle

Mexico: AMLO’s closing year

Even though the international context is growing more complicated, Niall Ferguson remains bullish on Mexico. The central bank remains hawkish, Mexican President Andrés Manuel López Obrador (AMLO) is steadfast in controlling fiscal spending, and nearshoring has grown from a trickle to a reliable stream which Niall does not expect to subside, given Sino-American tensions. Turbulent domestic politics will not spoil the stable macro outlook. The greater risks come from outside Mexico, such as a recession in the United States. For the near term, though, Mexico is still a strong bet, including Pemex.

Commodities

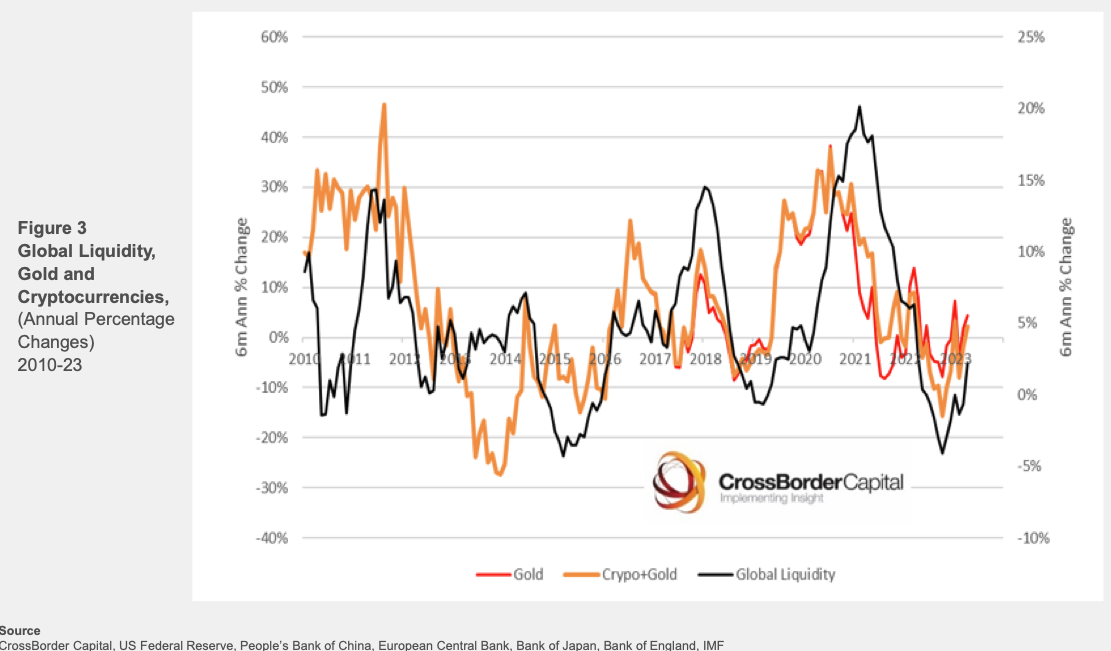

CrossBorder Capital

Gold and crypto are going up…. and by a lot

We are moving into a new era where central banks may have no choice but to create monetary inflations to fund future structural deficits. QE is unquestionably coming back. Gold and crypto look to be great monetary hedges against this risk, claims Michael Howell. A 75% increase in US monetary inflation would easily take gold bullion prices through $3,000/oz and Bitcoin should test US$40,000. However, Michael notes the extreme sensitivity of crypto currency prices to global liquidity (see chart). With a 7.5x multiplier, a 75% prospective rise in liquidity could see Bitcoin training through $US100,000. Get ready!

Metals Focus

PGM: What’s ahead?

The recent London Platinum Week highlighted the diverging perspectives on the current and future PGM market, in particular the viewpoints on key demand drivers and their implications for autocatalyst demand. There are differing views on the pace of vehicle electrification by various stakeholders. Furthermore, the uncertain growth trajectory of the hydrogen economy is also contributing to disparate opinions. Metals Focus expects a modest decline in South African PGM supply this year. Globally, platinum and rhodium mine supply is expected to remain flat at 5.5Moz and 0.7Moz respectively, while palladium is expected to decline 4% to 6.3Moz. However, demand uncertainty and price volatility is resulting in conservative approaches to expansion capex.

Marex

Oil: A strong floor ahead

The Marex team see prolonged overproduction as unlikely, with Russia likely to fall under Western sanctions similar to what occurred in Iran and Venezuela. If Russian production declines, the recent OPEC action and the potential for the US to refill its SPR will put a strong fundamental floor beneath oil prices barring a major recession. The Saudis appear willing to defend oil prices at all costs and could extend their July production cut indefinitely until prices rally back above $80 per barrel basis Brent.

Global Mining Research

Foreign ownership cycle of Australian gold production

David Radclyffe’s latest gold sector report examines the M&A cycle in Australia, with the country having witnessed a full cycle of foreign acquisitions. The trend started with the significant loss of Australian mines, peaking in 2003 at 60% foreign ownership. Over the years the trend reversed, but now the cycle has moved back to Australian gold companies and assets being attractively priced to international peers. With the proposed acquisition of Newcrest by Newmont, we could see foreign ownership levels lift back to ~40%. Northern Star and Evolution appear well poised to attract domestic investors looking to move on from Newcrest and to take advantage of the next phase of industry rationalisation in Australia.

ERA Research

Lumber: Chopped down

SYP lumber prices are falling, closing the gap with depressed S-P-F levels. Low prices should induce curtailments/closures, but many high-cost producers are resisting; painful quarters await. Panel prices have peaked. Oversupply will become an issue for OSB, requiring supply discipline. Share prices remain depressed (unsurprisingly); however, the ERA Forest Products Research team don’t expect much upside until late 2023. Interfor is their preferred way to play any short-term rally, as well as the long-term thesis.