Company & Sector Research

Europe

Creative Portfolios

UK Risk Rankings

Paul Hollingworth sifts through ~300 UK companies to ascertain their financial risk. He incorporates seven different Risk Models and scores companies by each model to come up with an aggregate Score. Investors should not be chasing high risk or "a dash for trash" (as we saw in Jan) but should combine classical valuation assessment with low risk opportunities. Companies featured in the top quartile of low risk include Renishaw, Rightmove, Sylvania Platinum, AG Barr, Rotork and Wilmington. Investors should eschew companies such as Wizz Air, Aston Martin, Mitchells & Butlers, Rolls Royce and Ocado. Let alone small caps such as Kromek, Plant Health or Pressure Technologies.

Smart Insider

David Hutchison (Chairman) purchases 14,075 shares at £16.35, spending £230k and increasing his holdings by 16%. Hutchison has a very good record of purchasing the shares since 2014, with a +15% six-month average return. This is his second largest purchase and the highest price he has paid. Jasi Halai (COO) has also been buying shares - her first reported open market purchases in III. It is interesting to see these purchases taking place with the stock at all-time highs, up from £11.00 just three months ago. Stock Rank +1 (highest rating).

ResearchGreece

2023 has started off strongly in ADV terms - average daily trading values of transactions in the Greek stock market reached €92m in Jan while Feb-to-date is at €120m. These are the strongest first two months since 2015. ResearchGreece guestimates ADV by using the following equation: (M/Cap of Greek equities × velocity rate) ÷ No. of trading days. Their modelling work implies M/Cap will hover at €75bn-80bn, but velocity rises to 40-45% (from 30% in 2022), pushing ADV to €125m this year (vs. €74m in 2022) and to €147m by 2025. TP increased to €5.90 (40% upside). They use DCF @ 9.5% hurdle rate (= 4.5%+5%); on their TP shares would trade 9.5x EBITDA and 20x EPS 2023E (15x ex-cash).

MDC Financial Research

GSK and other makers of Zantac are still facing potential liability in the United States. While a Federal Court Judge in West Palm Beach, Florida, issued a ruling on December 6, 2022, finding no "General Causation" between Zantac and Plaintiffs' cancer, that issue has now gone up on Appeal to the Eleventh Circuit in Appellate Case #22-12528. There also appears to be over 1,000 Plaintiffs remaining in consolidated Case #JCCP005150 at the Superior Court of California - County of Alameda. MDC will continue to follow these cases for its investor clients in all US venues.

Iron Blue Financials

An Iron Blue score of 30/60 is top quartile (fertile ground for shorting). Red flags include elevated stripped out restructuring costs and acquisition (GIL) fair value adjustments. There is also an expanded gap between headline net debt and Iron Blue’s preferred calculation method (factoring +DKK0.6bn y/y, restricted cash +DKK0.9bn y/y). Trade receivables days outstanding have fallen to a decade low (50 vs. decade range of 56-73 days), leaving risk of mean reversion. Governance red flags include a non-independent board & committees as well as an unusual CEO variable pay approach (share options based and pay-out on EBIT/TSR/ESG rather than EPS, cashflow or ROI).

Vision Research

A new $3bn+ M/Cap European industrial short

Trades >$10m/day and has <1% short interest - will be lapping price increases at a time when volumes have turned negative and there are substitution threats and declining per capita usage of products at some of its largest customers. It trades >10x EV/EBITDA on 2023 estimates that call for 40% growth in EBITDA.

In the last 24 months, Vision has closed several shorts including: Allegro, Boohoo, Colruyt, H&M, Inditex, New Relic, Nokian Tyres, Peloton, Similarweb, Thule, Trex, TSMC and UiPath.

Shephard Media

Support for the Armed Forces of Ukraine leading to increased defence budgets in 2023

The war in Ukraine and subsequent changing threat perception in continental Europe and beyond, as well as accelerating support to replace Ukraine’s military capabilities with modern platforms has resulted in a substantial increase in defence budgets. The past ten months have seen a wave of announcements of military assistance for Ukraine, from the drawdown of equipment from MoD inventories to fast-track procurement for donations. The defence industry has been trying to ramp up their manufacturing capabilities to meet the increased demand and rise in defence budget expenditure.

Click here to access Shephard's top 20 defence programmes for 2023.

North America

AlphaBox Advisors

A counter cyclical bet in a weakening macroeconomic backdrop - UBER’s uniqueness stems from its multi-product platform which ensures higher utilisation and earnings potential for drivers. A strong supply-side leads to lower wait times and cost for customers which are the two most important variables for customer stickiness. The barrier to entry is increasing for competition as UBER’s moat continues to widen driven by its scale and network. The company reported a blowout Q4 whereas competitor Lyft struggled. The stock could compound at ~17% over 5-7 years with a 30% upside over 12-18 months as UBER achieves GAAP profitability in 2023.

Games Investor Consulting

NFLX now describes video games as one of its three core media offerings alongside movies and TV series and has ambitions to be a games market leader. That is a pretty bold statement from the streaming giant that has changed film and TV forever but is still only a minnow in games. Does it have the potential to succeed, or will it follow so many other major media / tech companies whose hubris and strategic misjudgements led them into expensive video game car crashes? GIC analysts, veterans of advising big media companies about games strategy over 27 years, take a deep dive into NFLX’s approach, challenges and prospects.

Antya Investments

All leading indicators, including customer aggregation, buying habits, and sales/customer, have already turned negative and Neeraj Monga does not believe that ETSY has additional headroom to increase prices, which will result in the e-commerce firm disappointing investors in its sales forecast for 2023. Companies delivering 8% EBITDA growth and declining sales do not justify 30x EV/EBITDA multiples. Neeraj also details management's clueless approach to capital allocation - within one year of splurging $1.5bn in cash to buy UK-based Depop, the company was forced to write down its investment.

Off Wall Street

Many of the catalysts for the recent golf boom have begun to reverse. Meanwhile, the drivers of the long-term decline in participation remain intact. As golf-related brands seek to continue growing revenues in the face of declining industrywide demand, competition is likely to intensify. GOLF’s large-but-eroding market share position and lack of off-course diversification leaves the company particularly exposed. OWS forecasts EPS falling to $1.78 in 2023 (-34% y/y), significantly less than consensus of $2.78 (+2% y/y). TP $28 (40% downside).

Foveal Research

PFE are attempting to move from their successful, but now outdated Prevnar 13 pneumococcal vaccine to Prevnar 20. However, paediatric data suggests it may be slow to achieving noninferiority to old Prevnar 13, and a lack of superiority on the extra seven varieties that Prevnar 20 is meant to prevent in children. Thus, Dr Amit Roy is concerned that it may struggle to position itself as better than already approved alternative MRK’s, Vaxneuvance. He expects most of the $4bn dollar paediatric pneumococcal vaccine market will go to MRK with only $1bn for PFE. Combined with better data in the $1bn adult market, Amit sees $1.6bn for Prevnar 20 overall.

Inflection Point Research, LLC

Following its share price collapse, Michael Fox remarks that it is difficult to watch a big customer like Microsoft treat a small vendor with leading edge technology in such a terrible way. However, he believes MSFT’s development of new tech has been broken for some time (internal ineptitude / no cohesive strategy) and it may well turn out that they realise that they need CRDO as a strategic vendor and will give them additional business going forward. Meanwhile, the other business activities remain intact, and the overall trends in the industry benefiting AECs, and CRDO as the first supplier, have not changed.

Abacus Research

A high-quality, defensive, EPS compounder that will out-grow semiconductor volume growth due to trends of increasing purity and material intensity in semis. Furthermore, the benefits from the CMC acquisition could surprise on the upside and are not fully appreciated by the market (the deal represents a step change in establishing a scale advantage over ENTG's competitors). EPS growth will accelerate meaningfully in late 2023 (can compound at ~15% CAGR for the next three years), driven by revenue growth, high incremental margins and cost savings. $5.68 EPS (FY25E) x 20 PE = $114 share price.

Huber Research Partners

Craig Huber thinks the firm's Ratings revenue guidance is far too conservative - for the five years though 2027, Craig’s average Ratings revenue growth estimate is +9.5% vs. management's new guidance of only +2-5%. At this stage the trough for global debt issuance appears to have been 4Q22, 1Q/2Q23 should look sequentially better (but still down y/y), and 2H23 should be up significantly once the Fed is likely done raising interest rates. Craig increases his 12-month TP to $360, based on averaging 21.0x 2024E EBITDA (or 27.2x adjusted EPS) and his 10-year DCF analysis (9.0% WACC, 4.5% long-term FCF growth rate, and 22.1x terminal FCF multiple).

Radio Free Mobile

Artificial Intelligence: Look for the picks and shovels of this latest bubble

The popularity of ChatGPT and the technology press’ willingness to ignore the reality of what it is, has kickstarted an arms race where a series of huge but very dumb machines will be created to meet demand. Richard Windsor predicts crashing valuations, huge write-offs and another period of navel-gazing while the AI industry ponders what went wrong. This will be the 4th AI Winter. This does not mean that there is not money to be made but it will not be in the companies that are building these behemoths but in the companies that supply them (e.g. Nvidia and Advanced Micro Devices) who may well see a sudden surge in demand as this bubble gets underway.

280First

Rapidly detecting meaningful language changes in 10Qs / 10Ks

HII: Takeover interest? The following wording has been removed from its 2022 10K vs. last year, "These provisions may discourage acquisition proposals or delay or prevent a change in control, which could reduce our stock price". General Motors: China rethink? “Pursuing opportunities in the Chinese market is an important component of our global growth strategy”, has now been removed from its 10K. ServiceNow: Brighter growth rate outlook; dividends set to resume; strategic transactions? US Steel: Covenant concerns; customer payment delays? Brinker International: Missing performance targets.

Japan

Asymmetric Advisors

Announces a massive buyback, crowning what has a been a great 2 years of performance since Asymmetric Advisors, as the only broker in the market recommending the stock, turned bullish in Feb 2021. Their buy thesis was based around this long overlooked name having a very cash rich balance sheet, emerging from 3 years of intense restructuring and asset write downs and re-orientation of its watch business towards higher priced, premium models. This delivered a major earnings recovery, and having announced a 6% buyback in May 2022, management has surprised the market again by detailing plans to repurchase up to 25.6% of its outstanding shares.

LightStream Research

Activism on easy street - shares soar after response to Elliott’s demands. While there is some operational / fundamental / earnings risk in the near future, Mio Kato would not be surprised to see the market mostly ignore this and instead choose to focus on what the “new” DNP will look like. He describes it as a less sexy play than Toshiba and Softbank, but thinks the returns on offer are greater, while the risks feel noticeably lower. Mio also believes this could prove to be a key acceleration point for Japanese governance improvement and provides a simple and obvious playbook for activism in the country.

Emerging Markets

Westlake International

Based on Westlake’s proprietary analysis and survey of 19 large agencies and advertisers, IQ has outperformed its peers in recent quarters with strong content and can meet 4Q street revenue expectations. Bilibili can at least deliver in-line 4Q revenue growth propelled by solid VAS and better-than-expected ad and game biz. Kuaishou can deliver 4Q ad revenue in-line with street expectation propelled by solid streaming eCommerce growth and growing advertisers; and saw robust ad spending from gaming in Jan. They are positive on all three names, given recent sharp ad spending rebound from several verticals and further consumer / ad spending recovery in 2023.

Hemindra Hazari

How liquid is the group? That is the critical question raised by the firm’s decision to rescind its Rs 200bn FPO - Hemindra Hazari’s analysis suggests that raising additional short-term borrowing will be extremely difficult. He thinks it unlikely that the government banks will take a decision on their own to extend further short term funds and any decision on this issue will be a political call taken by the government. The situation will require deft financial management, injections in long term debt from founder entities, cuts in capital expenditure, and divestments to raise resources for the company in the immediate future.

Aequitas Research

Shocks the market with a US$2.4bn rights issue (30% discount to the undisturbed price of HK$62.80 as of 9th Feb & 45% discount to NAV Sep 22) and comes shortly after the group announced a S$2.2bn acquisition of two Singapore assets in late Dec 2022, where management explicitly mentioned that they didn’t need to raise any new capital. The issue is complicated even further by the fact that management has spent HK$400m+ over the past year buying back its units at prices above where the stock is trading now. In this note, Sumeet Singh talks about the rights issue, its previous acquisition and the overall implications.

AceCamp International

Management's gross margin guidance is overly optimistic - Qualcomm's aggressive pricing strategy has left MediaTek in a difficult position between protecting margins and not losing market share. Post 4Q22 results, AceCamp lowers their 2023/24 EPS estimates to NT$50.6/NT$44.3 (-32%/-13% y/y), to reflect weaker than expected 1Q23 revenue guidance and higher than expected OPEX guidance. The stock currently trades at 14.4x/16.5x 2023/24 PE, following a 40% rebound from the 3Q22 low. However, given the significant EPS declines forecast and an environment of lukewarm smartphone recovery, a 12-13x PE would be more appropriate.

Macro Research

Developed Markets

Aitken Advisors

Don’t evacuate all your fairly-new European overweights

James Aitken wonders whether the thinking on February 2nd’s price action (essentially what we saw was capitulation/liquidation, so fade everything) was too simplistic. Why? In Europe, the economic outcome is less bad then feared, and recent months represent one of the few times since the GFC that European equity markets have outperformed the US in euro and dollar terms (see chart). Many of the sectors in the European value space remain inexpensive compared to the market and their own history. It may take a while for this churn in equities to settle down, but that doesn’t mean to evacuate all new European overweights. If you are looking to reload European equities, look first to basic resources, energy, autos and banks.

Eurointelligence

Germany: Berlin elections have an important lesson for federal politics

Berlin city state elections were interesting in what they tell us about how difficult it will be to dislodge Olaf Scholz as chancellor, remarks Wolfgang Münchau. The CDU scored a landslide victory, but it is far from clear whether the CDU can form a government. Together, the current Berlin coalition of SPD, Greens, and the Left Party has retained an arithmetic majority. It would be a coalition of the losers, but viable nevertheless. It's now up to the Greens to decide what they want to do. The traffic light coalition at the federal level is clearly not working for the party. The main policy lesson from the recent results is that the CDU's only power option, at state and national level, is with the Greens.

Greenmantle

Italy: Internal risks loom for PM Meloni

The results of recent regional elections will help Prime Minister Giorgia Meloni’s right-wing government and strengthens Niall Ferguson’s view that the internally divided opposition is weak. In the next months, her biggest problems are going to come from her erratic allies within the administration, Lega and Forza Italia, as well as from within her own party, Fratelli d’Italia. Niall does not expect a collapse of the governing coalition in 2023. Meloni will continue to pursue the reformist path needed in order to tap NGEU funds. Niall no longer see significant upside in Italian risk assets and moves to NEUTRAL.

Minack Advisors

US: Leading indicators may mislead

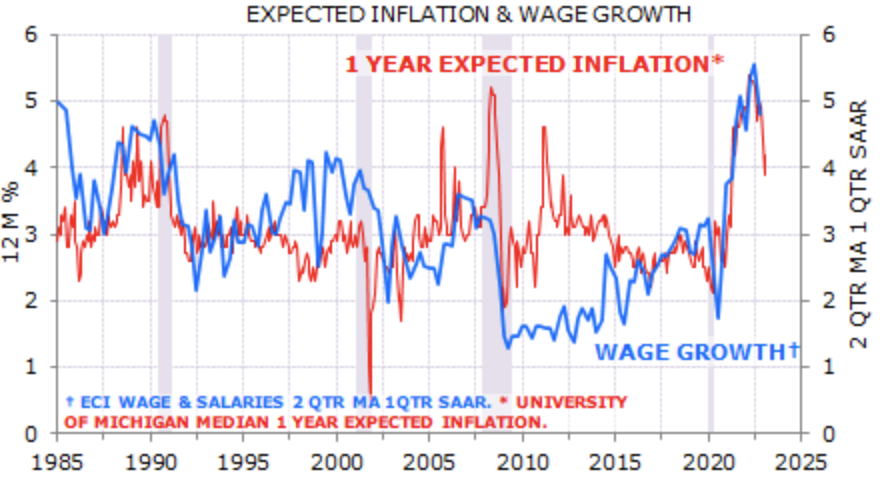

Numerous long-standing leading indicators suggest an imminent US recession, but Gerard Minack believes a recession is more likely to be delayed until H2/2023. The swing back to labour-intensive service sectors is underpinning labour demand, supporting labour income and consumer spending. The decline in inflation before the recession is providing an unusual pre-recession boost to real labour income growth. With concerns that a tight labour market will maintain service sector inflation at unacceptable levels, expect the Fed to keep rates higher for longer as wage growth continues to grow at unsustainably high levels.

Belkin Report

FANG fans

Michael Belkin’s model forecast shows an economic cycle peak developing, but large speculators don’t agree – they keep adding to TBond short positions that are losing this year. In fact, Michael is still LONG FAANGMT. It may go against conventional wisdom to buy stocks because the economy will weaken, but the stock market responds to Fed policy, the economy, earnings and market psychology. Having lost money in the 2022 bear market, investors were mentally programmed to sell and short the 2023 stock market. The results speak for themselves: +19% FAANGMT alpha and -19% alpha for long defensive/short FANG ytd. Don’t worry, it’s probably not too late to join the rally.

Independent Strategy

Japan: Appointments point to reform of the BoJ

The yen is David Roche’s biggest currency long. JGBs are his biggest sovereign bond short. Japanese banks are one of the few equity sectors (along with global energy) that David thinks have fundamental value, and recent news of likely appointments at the BoJ confirm these portfolio positions. If anything, investors should add to them. We will see the end of Yield Curve Control (YCC) and Kuroda’s hyper-lax monetary policy in an economy with cash wages rising faster than in decades and core inflation that has doubled since April. Of course, the policy plateshifts will happen in stages, as all things in a well-orchestrated tea party do, but they will happen, nevertheless.

Messels

UK: FTSE 250

The FTSE 250 index has yet to break out of the recent base formation, and there is also still work to be done for many constituents to complete bases. The index is below resistance at the top of the 8-month range, and performance is not improving relative to the FTSE 100 index. The most constructive looking areas remain Building Services, Retail and Financials.

Emerging Markets

CrossBorder Capital

Asian central banks lead the upturn

Latest weekly data show major Central Banks’ aggregate liquidity edging higher (+0.4%) in local currency terms. The numbers confirm the trends noted in recent weeks; Asian Central Banks are leading the liquidity upturn and with some vigour. Next in line is the US Federal Reserve where liquidity conditions have stabilised. The ECB and Bank of England are lagging. Liquidity expansion in US dollar terms has decelerated to 13% (3m annualised rates). The sharp slowdown from the previous week’s +27% rate reflects a pause in the US dollar’s downwards trajectory.

Teneo

Africa/China: Sovereign debt crises are the latest geopolitical irritant

The role of Chinese state lenders in blocking debt restructuring and IMF bailouts in low-income countries has emerged as another point of tension between China and Western countries. Chinese creditors are largely unwilling to accept write-downs, and Beijing wants the World Bank to share the losses from debt restructuring. China’s role in restructuring distressed sovereign debt is significant for two reasons. First, China is the largest official creditor to around half of the 38 countries that the World Bank classifies as in or approaching default. Second, the Common Framework mandates that official bilateral claims are restructured first, followed by private creditors, who are expected to restructure on “comparable terms”.

RW Advisory

2023: The year of China's reawakening

China’s reawakening is tactically bullish, albeit an uneven growth story. This strikes a metaphoric juxtaposition of fire and ice, fuelled by pro-growth expectations in China (fire) and signs of a slowdown in US growth and inflation, hoping for an early cooling in Fed rate hikes (ice). RWA’s global cross-asset model© signals China outperformance, based on CSI300, which integrates a diversified stock mix of China onshore shares. However, China’s offshore investable growth stocks and the rest of the market (non-TMT) have already broken under major technical supports, implying a structural breakdown. This reflects the new cycle phase of a growth/value rotation, coupled with the ongoing geopolitical risks, notably of de-listing from US exchanges, whereas onshore stocks will likely enjoy policy support.

PRC Macro

China: Business as usual, or business unusual?

William Hess questions whether Beijing can steer the economy towards Xi's "new development pattern" without structural adjustment funds. The previous round of equity market strength was driven by inflows, but these effects have been waning. William expects the effects of resource front-loading to wear off soon, and there may be room for a pullback as market breadth tops out. The perception is that local governments are still struggling with financial stability management, constrained leverage growth, and lingering ZCP shocks. As a result, significant resources are still being diverted to paying for the past, not Xi's "new development pattern". Beijing's "business as usual" approach to structural shifts in the operation of the economy is the right step in the wrong direction, and market sentiment may get squeezed in the middle.

Horizon Insights

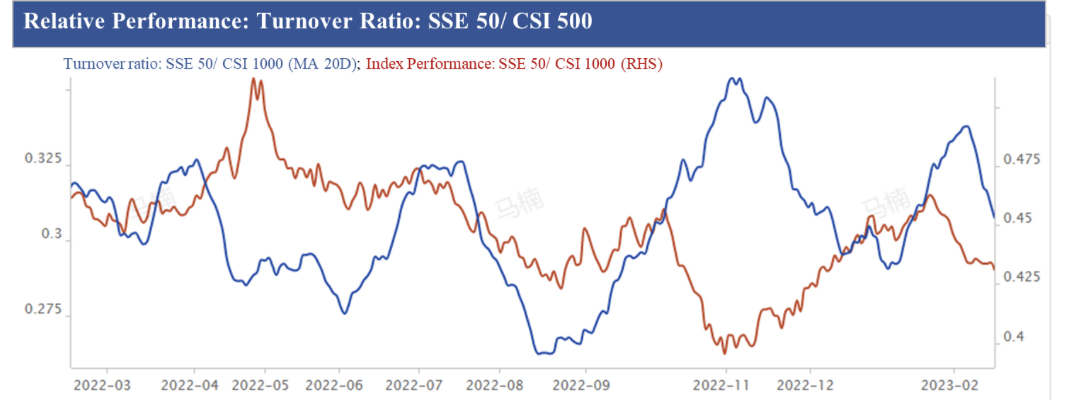

China: Outperforming small cap stocks

Thanks to concepts fuelled by ChatGPT, small-cap stocks have led the A-share market – overall, the smaller the share’s market cap is, the better it gets in stock price (see chart). The strong performance of small and medium cap stocks does not trigger any extreme behaviour in turnover ratios, with changes in line with that of stock prices, which are still far from historical highs. Worries about the resilience in the US economy weighing on Chinese market performance will be unfounded; the two economies are growing at different paces, and the direction of monetary policy may not stop yield spreads between Chinese and US 10-year bonds to expand in the future.

Emerging Advisors Group

Stress testing Brazil for 2023

All asset classes seem to be “working”, claims Jonathan Anderson, with a stable BRL, long end yields that are not yet falling, and an equity market that has outperformed broad EM. The fundamentals are mostly supportive going into 2023: the external position is in balance, export earnings have held up well, the budget is in much better shape and inflation is falling, and Copom is keeping nominal and real rates stable. All of this is good for the currency and for carry. What worries Jonathan is the equity side of things, with a weakening private credit cycle that may need more aggressive easing to get things moving again. Jonathan isn’t exiting his trade yet, but will be keeping a close eye on momentum.

Greenmantle

Mexico looks good to go

Throughout early 2023, Mexico’s economic fortunes have been rosy. Yet the country’s politics remains less than stable. With President Andrés Manuel López Obrador (AMLO) increasingly combative ahead of the 2024 presidential election (in which he cannot run), the likelihood of political turmoil is rising. Yet the MXN has seen its most prolonged period of strength in the AMLO era. Niall Ferguson expects AMLO’s government to continue to stabilise Mexico’s finances and the central bank to continue its tightening in 1H23. The market’s newfound love affair with Mexico and its “súper peso” is likely to persist over coming months. Niall remains LONG.

Commodities

Independent Strategy

Gas and LNG: The cawing of crows

Last year, investors who went short on EU gas and global LNG made a wise decision. However, with the crows once again cawing, David Roche reckons it may be time to go long on both. Global oil supply is predicted to fall, with the price of Brent crude oil reaching USD140/bbl in 2024. Russia is being forced to cut production, Europe’s natural gas inventories are falling and LNG storage is down to 45%. The crows would see the fall in EU gas prices as food for optimistic cawing and prognostications, but David remains doubtful that a zero-productivity growth economy with big government, big deficits and swathes of social protection can sustain low inflation for more than the flickering of an historical eye.

Longview Economics

Gold: Where next?

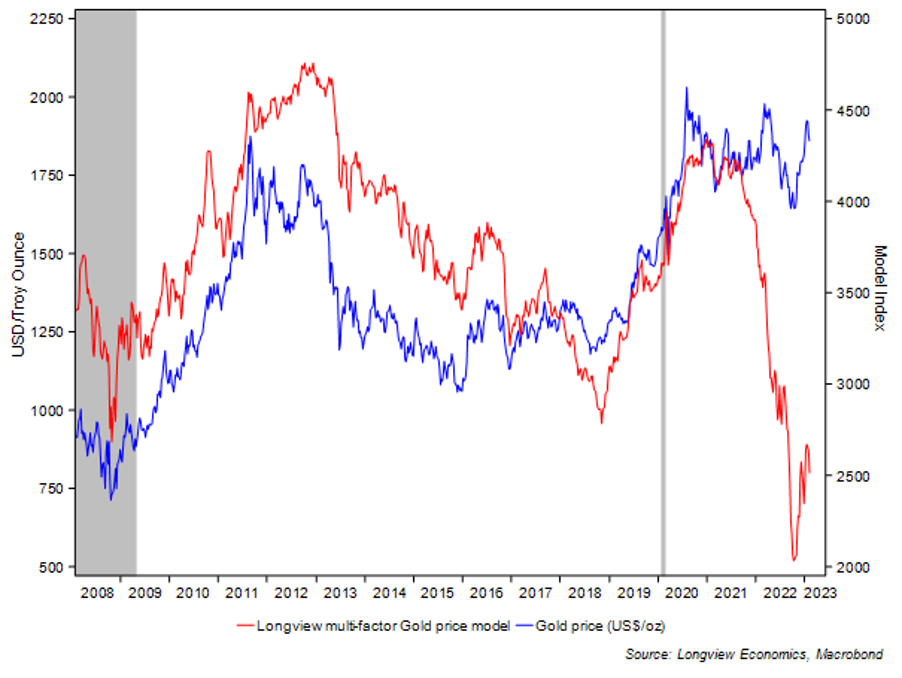

In the near term, the direction of the US dollar is critical, with a phase of dollar strength likely in the coming months. This is consistent with the current gold price action, sentiment, and technical models outlined by Harry Colvin, which highlight the potential for further near-term downside in gold. In the medium/longer term, gold price direction principally depends on changes in Fed liquidity, which is driven by changes in the outlook for US inflation and the economy. If the US economy enters a recession and inflation continues to fall, then a Fed pivot towards policy easing is likely, and the Longview gold multi-factor model should move sharply higher over the next 12-18 months, with gold therefore likely to deliver strong gains over that longer timeframe.

Global Mining Research

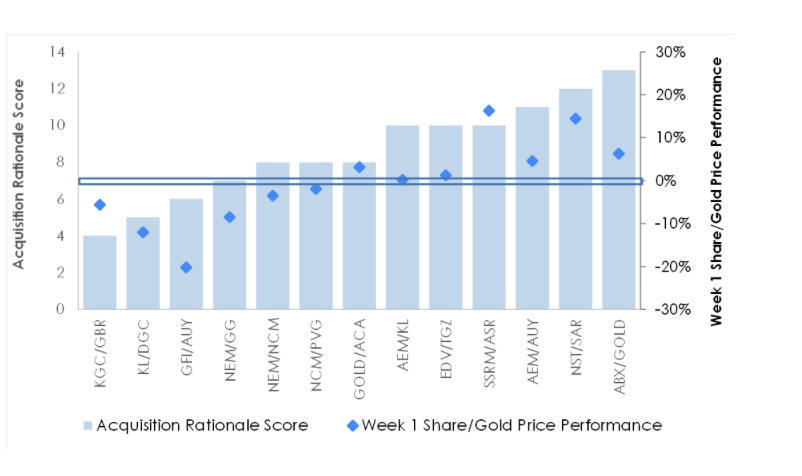

Does gold M&A create value? A rational screen offers clues

The recent proposed offer by Newmont to acquire Newcrest demonstrates that corporate M&A is alive and well in the gold sector, but it also raises the question as to whether it creates value. David Radclyffe’s latest report analyses major mergers over the past five years in the gold sector, concluding that most deals do not create lasting value – less than one-third show positive returns a year after the deal. Global Mining Research have developed a screen to explain why some deals generate a positive initial market reaction and others do not, providing investors with a ready tool.