Company & Sector Research

Europe

Willis Welby

Expectations analysis for European Apparel & Branded Goods

Luxury Goods have had a reputation for being one of Europe’s growth areas for a long time and last month they performed well ahead of wider indices. Although the median implied to Y3 EBITM ratio of Willis Welby’s large cap universe is now 96, that still feels tenable given the generally high levels of financial productivity and the almost universal high levels of current and projected revenue growth. In this note, they focus on Cucinelli. While the company is currently on a roll, Willis Welby finds expectations ratios far too high and financial productivity too low. The likes of Kering, Inditex, Richemont and Moncler look far more appealing.

Galliano's Financials Research

Victor Galliano sticks with his core theme for global exchanges of growing post-trading revenues, as well as capitalising on “big data” in financial transactions and data services, as we move into 2023. He identifies four relative value opportunities. In addition to the two mentioned above, HKEx and MexBolsa feature positively multiple times in Victor’s value screens and they are all diversifying revenue streams. He sticks with Coinbase as the exchange to avoid. Its revenue streams are heavily exposed to low volumes of crypto transactions and recent events highlight counterparty risk.

Copley Fund Research

UK Healthcare: Value funds drive underweight

Healthcare now stands as the third largest underweight risk to UK investors (behind Consumer Staples and Energy) driven by two key factors: 1) AstraZeneca positioning. The net underweight of -2.62% accounts for more than the net underweight of -2.36% for the entire sector. Overweights in Smith & Nephew, ConvaTec and out-of-benchmark Sanofi provide the partial offset. 2) Value Fund positioning. Active UK Value managers are seemingly happy to let underweights increase, with a huge gap of -6.27% vs. the FTSE All Share weight. Value managers are banking on some serious underperformance.

ResearchGreece

While ResearchGreece is still struggling to comprehend the premium on Terna Energy’s speculated €22-23/share M&A price, it does not change the fact that GEK is reportedly close to selling its 37% stake in the company. If GEK pockets ~€1.0bn from the sale, what does that mean for the implied valuation of the remaining major assets / investments in its portfolio? It means they are seriously undervalued! GEK is a great stock pick for long-term investors favouring infrastructure plays. TP €15.00 (40% upside).

Woozle Research

Double downgrade to Short / Sell - 50% of respondents interviewed* reported softening demand with pessimistic trading outlooks. Spend levels increased by 6% YoY, trailing consensus estimates of 10.1% YoY in organic revenue growth for 4Q22. Some CAP clients decided to shift more work to Accenture and a few were impacted by budget cuts and IT spending reductions this quarter. Reduced spending was particularly prominent among big enterprise retailers.

*Woozle conducted interviews with 22 CTOs and IT service procurement specialists. Regional split: 56% from Europe, 11% North America and 33% Asia.

ALEZOR Research

Alejandro Acosta initiates coverage with a Buy rating despite decreasing Covid support activity and issues with the moderation team in Colombia. Remediation efforts for the unfavourable working conditions will also impact operating margin. Alejandro always places a strong emphasis on earnings quality. While he finds no major red flags at TEP, he implements meaningful adjustments to reported debt and the cash flow statement. He believes €595m is a good estimate for the Group’s FCFF. WACC stands at 7% (+8% short-term growth moving towards a LT growth rate of +3%). This results in an equity value of €274.

Smart Insider

Markus Krebber (CEO since 2021; joined 2016) acquires 7,000 shares at €41.43, spending €290,000 - this is his fifth purchase after he began buying shares in March 2020 at €23 and his activity has proven to be timely. His last purchase was in June 2022 at €35. Furthermore, Hauke Stars (Supervisory Director since 2021) has also recently topped up his holding. The stock is near a multi-year high and it is interesting to see these insiders add to their holdings at a higher price level. Stock Rank +1 (highest rating).

North America

Abacus Research

All about the margins - companies that have started on the path to margin expansion will be a leading theme in the market over the next few years. So, why would investors be interested in PINS now? 1) There has been a stabilising of MAUs over last two quarters and ARPU is growing again. 2) The company is under-monetised and as the current investment period rolls off, the operating leverage in the model will become apparent. Long term, EBITDA margins can move above the previous high of 31%. 3) Comps get easy soon and the structural tailwind remains. 70% upside.

Battle Road Research

Poised for recovery - now that the dust has settled on TSLA's Q4 numbers, Ben Z. Rose of Battle Road Research sees good things on the horizon for the company and reaffirms his Buy rating. He considers the most important catalysts to be the impact of the $7,500 federal EV tax credit in the US, expansion of its Austin and Berlin factories, production ramp of the Tesla Semi with an intriguing autonomous driving twist, the launch of the long-awaited Cybertruck, and the potential for a share repurchase. Ben reaffirms his one-year price target of $316, based on a 40x multiple assigned to his 2024 EPS estimate of $7.90.

JJK Research Associates

Major blow as Amy Hauk (CEO of the VS and Pink brands) resigns - Janet Kloppenburg had been optimistic that Hauk’s well-regarded brand-positioning and merchandising / sourcing expertise would be effective in executing the company’s plan to increase domestic market share through elevation of the VS brand and through a successful repositioning of the Pink brand. However, Janet is now concerned that the execution of this program and the outlook for sales gains and margin improvement to reaccelerate in 2H23 may be at risk. She lowers her (below consensus) 4Q22 and F23 EPS estimates to $2.15 and $4.75, respectively.

Two Rivers Analytics

New short idea generated from Eric Fernandez’s ‘Declining Business Model’ - key takeaways from his 25-page report include: 1) Sales have fallen for four quarters. 2) Gross and EBITDA margins have contracted to pre-pandemic levels and Eric expects margin problems to intensify. 3) Remote optometry and automated vision checking are devaluing EYE’s optometry services. 4) The company is plagued by customer complaints. 5) Management’s acquisition and expansion strategies are constrained by debt levels. 6) Multiples are historically high and ignore deteriorating fundamentals.

BWS Financial

Hamed Khorsand raises his sales and EBITDA estimates citing continued improvement in the automobile industry - a stronger Euro should reduce the headwind GTX has experienced in prior quarters. In addition, management’s forecast of a sequential decline in average price per unit should reverse by the time GTX reports 4Q results. The stock has been trading around $7.50 after the company said it was evaluating options, but Hamed doesn't expect GTX to sell right now and expects the shares to rerate higher as investors realise there is more to the group’s product line than just turbochargers for internal combustion engines. 100% upside.

ERA Research

Forest Products: Tough year ahead

The outlook for lumber / panel producers (Canfor, West Fraser, Boise Cascade, Louisiana-Pacific) is difficult, with no obvious upside catalyst before a recovery in US housing (unlikely before late 2023). ERA expects pulp prices to move lower through 1H23. Anticipated price declines are now almost fully priced into pulp names (Mercer, International Paper). In packaging, more pain lies in store for containerboard (Westrock) and a raft downtime will be needed to combat weaker demand and offset new capacity. Boxboard will outperform (Graphic Packaging, Clearwater Paper), with both demand and prices expected to remain robust.

Alembic Global Advisors

Chemicals: Recent declines are overdone

Chemical equities' performance is worse than anything we have seen in recessionary periods over the last 60 years, suggesting limited downside and significant upside for some. Sector balance sheets and cash flows are far better positioned today than in 2008/09. For 2023, Hassan Ahmed prefers companies that may benefit from catalysts (Tronox and Braskem), secular changes within their markets (Olin), or have high China / Europe exposure (Covestro and Tronox). He sees PureCycle as a high-risk / high-return play - TP $30 (300%+ upside).

MYST Advisors

Transitioning from “great to good" - the stock is far too expensive trading at ~15x CY23 gross profit. BILL’s growth algorithm will decelerate from 50-100% down to 25-30% over the next few years. The company faces 3 primary issues: 1) Macro headwinds. 2) Competition - Intuit, the “Big Gorilla” in the space, is launching a competitive solution. 3) Negative mix shift - many investors are not taking the time to model out BILL’s business by channel, so they don’t understand the dilution to unit economics caused by adding more customers from the Financial Institutions channel. TP $62 (40% downside).

Sales Pulse Research

IT Spending & Cyber Security

As always, SPR will be tracking the trajectory of IT spending, changing priorities and competitive dynamics for the segments and vendors they follow. Key questions / themes for 2023 include: IT Spending: 1) Which vendors are seeing more than anticipated pressure from reduction in seats and end user efforts to contain costs? 2) Vendors benefitting from the rapid growth in DevOps / DevSecOps. Cyber Security: 3) Which vendors are executing well with XDR solutions, capturing share and potentially disrupting existing vendors? 4) Maturing of the End Point Protection market. 5) Growth for Zero Trust Network Architectures. Additional Themes: 6) Vendors successfully leveraging AI / ML. 7) M&A speculation.

Positive views include: Palo Alto, Cyberark, Five9, Snowflake, Ciena, Datadog. Cautious: ServiceNow, Salesforce, Tenable.

Japan

Churchill Research

Beating the Nikkei

Since inception, Mike Churchill’s Japan II portfolio has outperformed the Nikkei by 23.6 percentage points - the portfolio was started in Nov 2020 with the idea of screening the entire Japanese equity universe once a year. Mike picks 100-or-so names for the first cut, then narrows that down to the 30 most attractive. Every year the portfolio is completely sold off and re-stocked with those 30 best ideas. Top performers last year included Nippon Steel Trading, Nakayama Steel and Torishima Pump Mfg. One stock he is particularly keen on is Shinnihon Corp, describing the homebuilder as “so insanely cheap it's ridiculous”. TP ¥1,235 (70% upside).

Asymmetric Advisors

Analysts worry that Fujitsu will fall short of its FY3/23 CoE of OP at ¥400bn +83% YoY and their consensus is already much lower at ¥370bn. However, this is +41% YoY, and the impression Asymmetric Advisors gets is that the actual result may be better than that. This leaves the stock trading on an attractive PER of 13x. The other attraction here is buybacks (>¥550bn over the next few years to FY3/25) with FCF of >¥1trn from operating FCF + the gains from divesting stakes in Fujitsu General (shares are +25% since Asymmetric became the only Buy rating on this unloved name) and Shinko, worth c.¥380bn.

Emerging Markets

Horizon Insights

Covid restrictions have resulted in the rise of millions of Chinese using online services to work from home. China’s online job recruiting platforms & apps are at the forefront of transforming the country’s job market. In this report, Horizon Insights looks at BZ, the widely talked about company that has used automation, big data, and AI technology to emerge as China’s No.1 online job recruiting platform & app in terms of MAU (grown from 11.5m in 2019 to 27.1m in 2021) despite being a relatively late comer.

LightStream Research

Price performance following the 2Q23 beat remains unwarranted - the shares are up over 60% from near-all-time lows, but Oshadhi Kumarasiri argues that management's cost-cutting is turning BABA into a slow-growth business. Almost all of the company's operating profit is generated from its two cash cows, Taobao and Tmall, however, they are both losing market share. Furthermore, rapidly rising Covid infections create new headwinds that could affect business performance for at least two more quarters. Oshadhi is short the stock as he expects earnings to miss consensus estimates.

New Street Research

The cheapest PayCo globally? The market remains hyper nervous on the Brazil Payment companies, but looking ahead to 2023 New Street thinks the ~8x 2023E PE multiple (with 2023-25E CAGR of ~40%) is too hard to ignore. Having sat on the side lines for most of last year they move to Buy with a TP of $17.00 (100% upside), taking a view that we are near enough at the end of the earnings downgrade cycle and assuming no significant change in the SELIC outlook. Their preferred LT pick exposed to this space remains MercadoLibre.

Propitious Research

Although the overall channel and customer inventories reduced aggressively by the end of 3Q22, we are only in the middle of the inventory adjustment cycle. We’ve seen early signs of global inflation peaking, and an initial normalisation in US dollar strength, which supports a recovery in end consumer demand and channel inventory restocking by mid-2023. In Wium Malan's latest piece, he argues that MediaTek's dividend yield (>10%) and PE ratio (11.4x NTM) indicates a meaningful margin of safety in valuation levels, with probabilities skewed towards a positive surprise.

Macro Research

Developed Markets

Global Forecaster

2023: The year to take cover

WW3: The challenge to America's hegemony and the bifurcation of the world. David Murrin points out that the end of globalisation and the bifurcation of the world has been unfolding since the onset of Covid at the start of 2020. That process has seen Russia evicted from the Western trading sphere and will see China similarly evicted by year end as a consequence of its military actions. He believes that the best outcome by 2024 would be a clearly delineated democratic trading sphere and a separate autocratic trading sphere. The worst, and almost certain, outcome is that we will be locked into a global conflict.

Andrew Hunt Economics

UK Gilts: The challenge is still in front

If anything, the UK monetary environment has eased over recent weeks. But Andrew Hunt remarks that, in nominal and real terms, money and credit growth remains lacklustre. Crucially, the BoE / public sector has yet to begin QT or other liquidity sapping actions – the move from an under- to over-funded budget deficit has not yet started. Over the coming months, Andrew expects less of a price-centred tightening but a more de facto quantity-based tightening as the funding arithmetic in the Gilt market changes. This suggests a steeper yield curve even as the economy weakens, and a potential further relapse in the GBP.

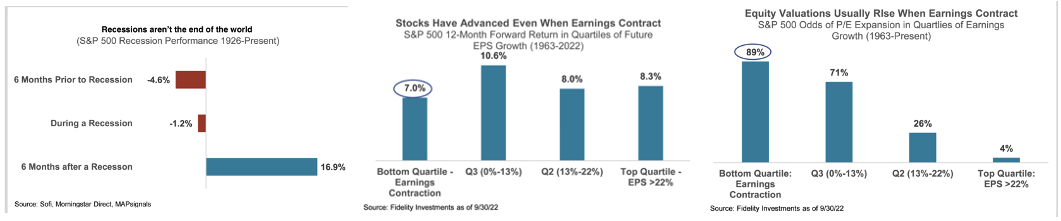

MAPsignals

Why stocks can be a good bet in 2023

Alec Young is quite upbeat about stocks in the year ahead. Sure, there may be a recession, but stocks historically gain a lot more coming out of a recession than they lose in the 6 months prior and during the recession itself (see chart 1). Alec also mentions how inflation is often seen as a reason to sell stocks, but stocks average 14% gains in the 12 months after it peaks. He also plays down fears of the earning apocalypse – don’t forget, stocks are a leading indicator that price in bad news ahead of time (chart 2). Don’t get scared out of stocks, buy quality on sale and stay the course. Alec’s top pick for the year are financials, with its cyclical nature and plenty of upside on offer when the fed stops tightening (chart 3).

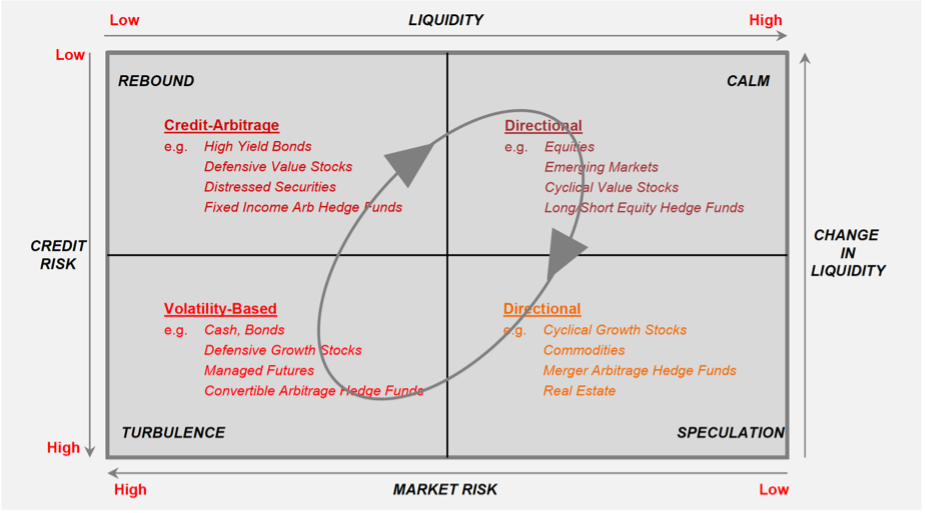

CrossBorder Capital

Global liquidity should rise, but investors are positioned badly

Expect stronger global liquidity in 2023. Risk assets have two moving parts – liquidity and risk exposure. Michael Howell is most concerned that risk exposure looks too high, particularly compared to the weakening state of the world economy. This makes equities more risky than normal at this stage of the cycle. The upcoming rebound investment phase, where liquidity rises but risk exposure continues to fall, is often tricky for stocks (see graph). Michael suggests that better opportunities lie in precious metals and corporate debt.

AAS Economics

The FX market from an excess money supply perspective

Frank Shostak postulates that the fundamental drivers of the exchange rate are a function of the growth dynamics of excess money supply between two countries. In his latest report, he outlines 12 major currency pairs. Frank’s recommendations include LONG EUR/USD, SHORT GBP/USD (with some technicals supporting a long signal, but net position remaining short), LONG USD/CHF, LONG USD/BRL (with fundamentals supporting the USD) and LONG USD/ZAR

Belkin Report

Investing in 2023

After a very successful 2022, Michael Belkin illustrates his 2023 long-term forecasts. He mentions his view on US interest rates, expecting a Fed cut later this year and steepening of the yield curve. He closes his 10yr minus 3-month inversion trade and adds a 10-2yr steepen trade. The TLT TBond ETF remains a strong BUY recommendation. Michael expects the USD to fall and inflation to head down on all measures, with the price level potentially declining by year’s end. He expects the S&P500 energy sector to fare worse than any other sector, but gold, silver and precious metals mining stocks should do well.

Quill Intelligence

US: Job losses

At 30.9%, the 7-month increase in Americans collecting unemployment benefits is on par with prior recessions back to 1967. While headlines point out that initial claims are still historically low, the economy has never seen continuing claims rise this much and not be in recession. We are at the recognition stage, which will propel more companies to push forward with cost cuts to weather the downturn. Spreads and volatility enter 2023 with the highest risk of repricing to reality as Fed policy continues to deplete liquidity from an increasingly fragile financial system.

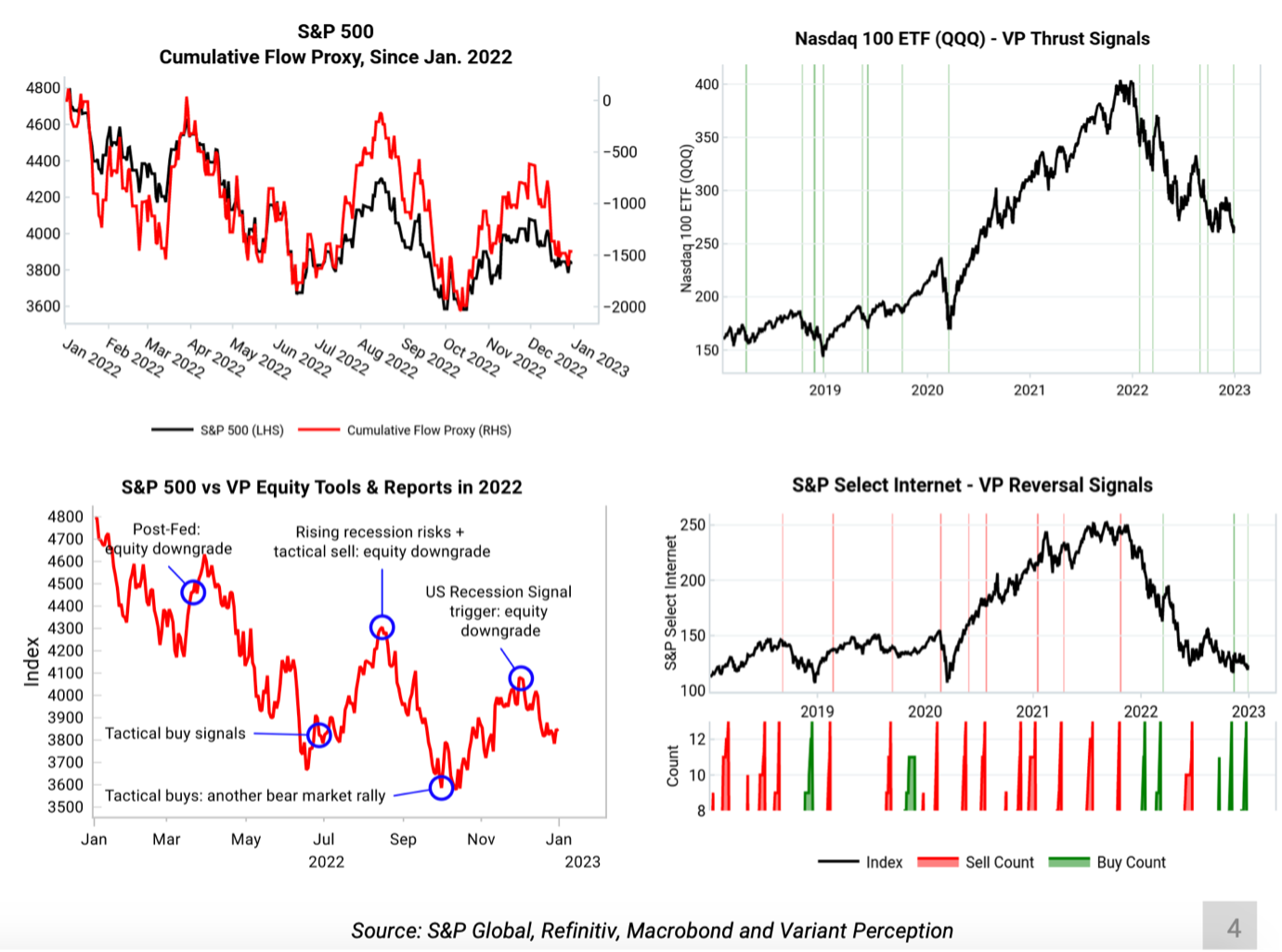

Variant Perception

US: Tech buy signals, room for more inflows

On a shorter-term tactical view (1-3 months), Variant Perception’s models indicate room for an equity rally to start the year. Their US equity flows proxy has dropped back towards the lows again in December (top-left chart), indicating that we are getting closer to another short squeeze. Tactical buy signals have triggered for tech (right-hand charts), but not for other sectors. For tactical investors, even while maintaining a “core” risk-off allocation, it may be attractive to buy upside in tech as a right-tail hedge.

Kailash Capital Research

How the crypto-FTX fraud could be masking epic capital misallocation

Crime in crypto is distracting investors from bigger issues, remarks Jim Rocchio. As the FTX saga unfolds, there are a swath of stocks that investors appear to have an almost Pavlovian desire to buy because they are “down”. A lower price for a low-quality asset with poor growth prospects does not a good investment, make. Jim fears the next shoe may be dropping in equity markets. The market value of the “biggest burners” - firms that have failed to generate positive free cash flow and are burning through cash - has grown from $2trn to a staggering $6.9trn in 10 years. If these companies couldn’t generate cash profits in a period of rock-bottom rates and epic government largess, when will they?

Musha Research

Japan: The BoJ will win

The Nikkei painted the picture that the BoJ has lost, but that is not the case at all. Ryoji Musha believes that the change in YCC is positive in that it signals a long-term trend of rising interest rates and encourages risk-taking. The YCC was originally introduced to prevent the yen from appreciating, and now that concerns about the yen’s depreciation have dissipated and there is no fear of the yen plummeting, the time is ripe for a normalisation process.

Emerging Markets

Greenmantle

China: A rocky road ahead

January will be met with lower mobility and worse economic data, foresees Niall Ferguson, who cautions that the country is still a few months away from fully reopening. The exit from a zero-Covid strategy will be reflected from 2Q/23 onwards, primarily through a modest recovery in consumption and business investment. Niall expects Beijing to target GDP growth of ~5% throughout the year. Whilst the end of zero-Covid will make it a relatively good year for Chinese assets, markets are overstating Chinese pent-up demand and understating the withdrawal of fiscal stimulus in 2023.

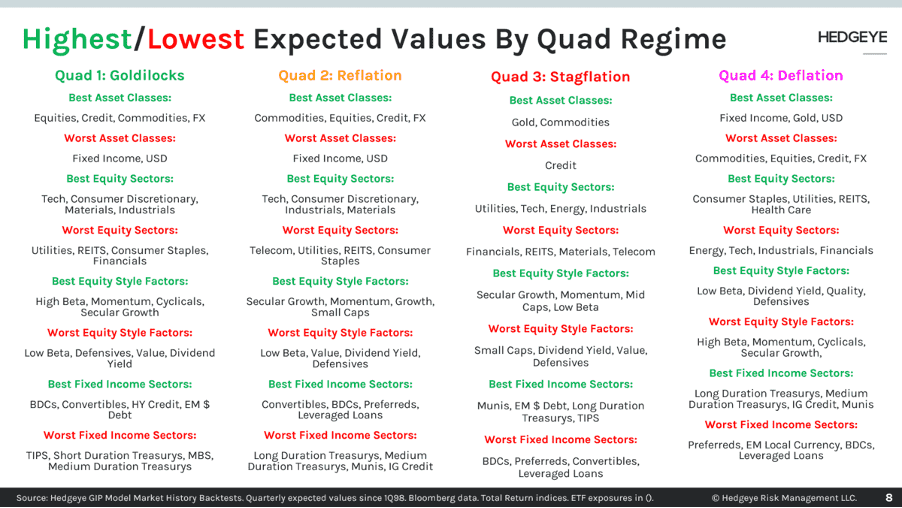

Hedgeye

Buy China?

Having been broadly bearish most of the past two years on China, Hedgeye is currently neutral, but adding select, single stock longs. Since the onset of the pandemic, in Quad terms (see diagram), China has tended to run a quarter ahead of the broader G20. That remains the case still; looking ahead to the first 9 months of 2023, of all of the G20 countries only China has a quad 1 setup for Q1/2023. By contrast, every developed economy is looking at a Quad 4. The unleashing of Covid is likely to amplify this condition set as it will increase the probability of stimulus.

Emerging Advisors Group

China’s reopening

Jonathan Anderson is pretty confident that the epidemic will be broadly over by February, with true recovery beginning in March. Mobility-related services will rebound dramatically though the year, but the manufacturing sector will head into recession as the export boom reverses. Expansionary credit and fiscal policies will underpin Beijing’s focus. However, as always, stimulus efforts won’t stick without a sharp property recovery. This brings us to the question: how big will China’s property rebound be? Jonathan reckons things will pick up at the margin, but it’s still fully up to consumers to start borrowing and buying property assets again.

Emerging Advisors Group

Bolivia heads back into troubled territory

The last two years saw Bolivia in external surplus, which has in turn helped keep the fixed boliviano currency regime going through the present. Now that export prices are falling, however, the economy is rapidly heading back into wide twin deficits, and Jonathan Anderson see a high risk of messy devaluation, forced fiscal adjustment and domestic recession. Until this happens - and until the dust settles - avoid exposure to Bolivian assets.

Teneo

Pyongyang consolidates relations with Moscow against the West

A lesser-reported secondary effect of the invasion of Ukraine has been the impact on ties between North Korea (DPRK) and Russia, with Moscow and Pyongyang becoming more closely aligned against the United States and the West more broadly. Strategically, North Korea sees an opportunity to tighten a Russia-China-DPRK axis that reduces fears of isolation against the US-Japan-Republic of Korea trilateral. For Moscow, which has been a key sponsor of the Kim regime in the past, Pyongyang offers a rare source of diplomatic and practical support on the international stage.

Commodities

Global Mining Research

Increasing overweight position in copper

David Radclyffe recently published on the positive supply outlook for copper, setting out the scene for near- and medium-term market deficits and noted the lack of new projects to fill demand. In addition to the near-term price forecast, the long-term copper price forecast has been lifted to $4.00/lb in 2023 dollar terms. As a result, the sector trades on a prospective 2024 EV/EBITDA of 8.2x, and P/NPV10 of 1.3x. For equities, copper exposure remains in demand and is likely to drive more M&A. Investors may move along the equity risk curve to small caps. Capstone and Sandfire Resources are preferred in the small cap copper stocks, and Antofagasta and Grupo México in the mid/large ones.

HCWE & Co.

Crude oil, forward gold and inflation: A triangular relationship

David Ranson addresses the paradox whereby the prices of crude oil and derivatives, such as gasoline, have been in a downswing despite a context of sustained inflation. Copious evidence has long suggested that the cause of inflation is the depreciation of currencies. Internationally, the currencies that depreciate the most are associated with the highest inflation. Domestically, given sufficient time, inflation is proportionate to the extent that the dollar depreciates relative to gold. Over longer periods of time, the prices of oil and gold move in parallel. As the price ratio between oil and gold moves back toward normal, which is likely, the recent puzzle may evaporate.

Janus Analysis

Is energy the next decade thematic?

Are we on track to experience another 1970s? History may not repeat, but it certainly rhymes. Gaius King is of the firm belief that a major commodities super cycle is about to commence, particularly in energy and energy metals. To generate a single terawatt-hour of electricity from solar/wind requires 100-300% more metals, than from a gas-fired power plant. For many base metals, prices will have to be substantially higher than they are currently in order to justify future exploration and development. Supply constraints are here and now…

Queen Anne's Gate Capital

A changing commodity landscape

There was something for everyone across the commodity space in 2022, but that’s so last year, claims Kathleen Kelley. Looking ahead, Kathleen points out that one third of the global economy will be in recession in 2023. Manufacturing PMIs have stopped falling, but only India, Hungary, Switzerland, Norway and Mexico are in expansion territory. That said, inventories are low across metals and energies, and Latin America is dry. Any demand stabilisation/increase will have meaningful price implications for the lucky sector(s). Muddling through the first half of 2023 is largely priced in.