Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

Europe

Harlyn Research

Bear Market Sector Strategy: What to focus on and what to ignore

In any bear market there are about 10 sector pairs (out of 45) which really drive the performance of a regional equity portfolio and the rest don’t matter very much. These pairs vary from one bear market to the next but are relatively easy to identify. There is also another set of pairs, which may be significant in market cap terms, whose relative performance cannot be easily integrated with the rest of the portfolio. There is nothing you can do about this, so don’t waste time trying to analyse the problem. European sectors which feature heavily in this list in this bear market are Materials, Utilities and Financials. Click here for the full report.

Announces its long-awaited Vantage Towers transaction - selling down 32-50% of its stake for cash at 24x EBITDA, or €32/share, a 33% premium to the 2021 IPO price. New Street analysts see this deal as transformational for VOD’s balance sheet with the potential to take leverage below 2.5x for the first time since 2019 and this should open the door to having excess capital for potential distribution. In this note, they run through the full balance sheet implications for VOD and the read across for other EU tower names. TP £1.75 (65% upside).

Finally lets Google off the leash - after four years of procrastination, the French car manufacturer has decided that its long-term future in EVs is not to do the software itself. It is the first major OEM to go in this direction and it is going to need to gain some market share to offset the impact of ceding the customer relationship to Google. Given the mess that the rest are in and how important the software user experience is becoming in the vehicle, this might just work for RNO. Qualcomm is also a winner here as RNO appears to be taking the whole QCOM digital chassis offering.

Philip Morris International will accept all SWMA shares that have been tendered to it despite failing to achieve its 90% minimum stake threshold. PMI must still secure further shares in a voluntary transaction during a new offer period to achieve its goal of utilising compulsory purchases to acquire all remaining stakes in the Swedish company. After PMI raised its public offer in October, the total bid now amounts to SEK176bn ($15.8bn).

Elliott has taken a stake in Fresenius SE, but the company’s top shareholder, the Else Kroner Foundation, is an obstacle to immediate value creation, a source told CTFN. As Elliott faces down the foundation, the activist could force a breakup of Fresenius Medical, a partially owned subsidiary of the company, or agitate for equity-dilutive M&A by subsidiary Kabi to improve its market share in the US. Bankers are already pitching the firm’s components to potential private-equity bidders, with subsidiary Vamed proving the toughest sell, the source said. Click here for the full story.

Beating expectations - 3Q22 performance in Poland was particularly impressive (vol. growth accelerated to 26%) given the economic environment but also because it shows that INPST is relatively immune from the increasing competition in APMs. Prospects in France also look upbeat (roll-out of APMs, plus the launch of the 24hr service, which can really give a boost to B2C volumes, a segment INPST is still only very modestly present). Once again, the IDEA! were keen to stress that the relative cost advantage of APMs vs. to-door delivery can become an even stronger growth driver going forward.

Green Street Advisors

Nordic Property Cos: In search of a miracle

Castellum and Samhallsbyggnadsbolaget are both Swedish property companies with complex ownership structures, impaired corporate governance and stretched balance sheets. The current challenging macroeconomic backdrop has now lifted the veil on the many risks embedded in their corporate structures. In this report Green Street explores the various implications of the recent announcements made by companies’ CEOs and provides insights on how to navigate the current market volatility.

Multiple new red flags picked up from SCT’s FY22 Annual Report - the 14% Y/Y increase in DSO is particularly concerning as it comes off an already elevated level. Investors should be concerned about the scale of receivables (~£500m) sitting on the balance sheet, representing ~6 months of sales. "Unbilled Receivables" have also been rising sharply (+150% Y/Y). Receivables "past due" >30 days now represent 16% of the total (11% of which are past due >2 months vs. 3% last year). Investors should closely monitor the receivable level in future quarters to corroborate management's narrative that this situation will unwind in FY23.

North America

Large Cap Growth Index Funds & the Path to Poverty

The top 30 names in Russell Large Cap Growth Index Funds make up ~65% of the index weight - despite recent declines, these stocks are at the same valuation that the 30 largest stocks were at the peak of the dot.com bubble when scaled by GDP. So, what does history tell us? Nearly 80% of the top 30 experienced losses on an absolute basis over the next six years. Fortunately, this flaw can be easily remedied...click here to continue reading.

Pricing power - this 38-page in-depth report highlights the industry’s favourable characteristics (capital light, low competition and consumer staple like nature) and WMG’s compounder qualities (highly predictable FCF, consistent margins and returns). After 10 years of streaming platforms & labels keeping subscription prices low to attract new subscribers, the time is now ripe for increasing prices. Abacus analysts believe an EV/EBITDA of 16x 2024 is appropriate for a one year forward fair value. They estimate 2024 EBITDA of $1.5bn, giving a M/Cap of $21bn or $42 share price (55% upside).

New high conviction short from Retail analyst Brian McGough - the bearish macro setup cannot be ignored. Brian thinks we could see the most rapid demand pressure ever in the space over 6-12 months. In the last housing recession, HD store comps were down 14 straight quarters and margins collapsed, yet the Street doesn’t have a single down quarter in its model. Brian’s base case EPS figure for FY23 is $14.78 but would not be surprised if the earnings number was closer to $12.00 (vs. consensus at $17.35)!! A 12-13x multiple would see the stock at $150 (50% downside).

Cheap for a reason - this slow grower is about to grow even slower. Tom Chanos correctly predicted SKX would miss the bottom line and lower guidance (EPS was cut by 34%) following the release of its third quarter results. Management blamed the miss on issues that they had already accounted for in previous guidance (incl. FX & Covid headwinds), suggesting they are not telling investors the whole story. With several shoe companies facing bloated inventories (SKX inventory was up 45% Y/Y), Tom expects SKX will be forced to cut prices in the fourth quarter. 1-Yr TP $25 (30% downside).

Holland Advisors

Andrew Hollingworth provides an update to his bull thesis having previously described the company as the “Amazon of finance” - it offers customers "no-trade-off" between good service and super low pricing. His early analysis revealed how SCHW would become extremely cash generative whilst continuing to grow. That day has now come - its arrival being delayed by its merger with TD Ameritrade. This piece focuses on what Andrew believes investors are missing and why Mr Market’s forecasts remain much lower than his own - 2023E EPS is $5.62 (vs. consensus at $4.80) and 2025E is $8.69 (vs. $6.30). TP $155 (100% upside).

Bank stocks roaring into leadership on micro & macro factors

Charles Peabody has been making the case that, if the financials outperformed the broader averages in the “down” market during Q3 (they did), they would emerge as a new leadership group in the next bull market. He continues to believe that such a transition is occurring. While the macro catalysts (Fed decelerating rate hikes (Jan 23); Treasury announcing a buyback (Feb); and end to China lockdowns (Mar)) are likely to bring in the generalist portfolio manager, the micro catalysts are already being recognised by financial specialists (+ive inflection in PPNR, share buybacks resuming, etc). Banks' outperformance to continue.

The Covid crisis allowed HUBG to produce record growth and profits - sales and margins surged on a 40%+ intermodal pricing increase. However, these effects are now reversing. Import volumes and port congestion are falling. Pricing is easing. Transportation could end up in a glut quickly. Multiples may appear low, but they are based on sustaining record margins. Margins closer to longer term averages (let alone recessionary levels) implies HUBG is an expensive stock. HUBG benefitted the most from the rise in pricing vs. peers. As such, Eric Fernandez expects them to be hurt the worst as prices turn down.

Inflection Point Research, LLC

Cybersecurity: Beat-and-raise being replaced by marginal-beat-and-cautious-outlook

Economic woes impacting cybersecurity vendors - security projects are being delayed / cancelled at a rate not seen for several years. Following recent earnings, IPR questions whether Tenable will be able to sustain its surprisingly impressive momentum over the next couple quarters. Varonis’ lowered guidance is consistent with IPR’s belief that their offering has shifted to being a like-to-have technology. Qualys and Rapid7’s reliance on vulnerability management must be considered a negative. Meanwhile, Check Point's results underscore IRP's hypothesis that vendor consolidation trends are strong and becoming stronger.

Rapidly detecting meaningful language changes in 10Qs / 10Ks. Recent alerts include...

Acuity Brands (AYI) - Working on a large acquisition(s) that could endanger dividends / share repurchases?

Amazon (AMZN) - No more reduced prices for AWS customers?

Kilroy Realty (KRC) - Under pressure to lower rents and increase expenditures for re-leasing?

Microsoft (MSFT) - Growing concerns that government contracts are at risk of being cancelled?

Corporate Access: 24 events hosted so far in 2022...

Peter Daniel hosts Zoom based calls with interesting industry (public & private companies) thought leaders for institutional equity investors. Highlights from this year include Tamara Lundgren (CEO, Schnitzer Steel); Lee Cooperman (Omega Family Office); Bill Rooney (VP- Strategic Development, Kuehne & Nagel); Ward Nye (CEO, Martin Marietta Materials); Scott Hamilton (President, Leeham Company); and Ken Langone (Co-Founder, Home Depot). Further details and a full list of all the events that Peter has hosted this year can be found here.

Japan

The tough market environment for publicly listed and unlisted tech companies remains, and yet SoftBank’s share price has held up since the end of Sept. In part, this is due to the share buybacks in place, and its reduced exposure to Alibaba through its derivative contracts. Nonetheless, Victor Galliano shows that SoftBank’s share price strength is unlikely to last, given the declining valuations of its listed holdings and the recent down rounds relating to its unlisted holdings which will be at least partially captured in 2Q22 results.

Emerging Markets

An in-depth look at China’s online grocery market through the prism of Meituan and the multiple online grocery business models it operates. Part 1 looked at the broad outlook and took a closer look at the CGB model that dominated Meituan’s growth in 2020-2021. Part 2 looked at 3P on-demand models such as Meituan Instashopping and took the view that the market will gravitate toward that model in the long run. Part 3 takes a last look at Meituan Grocery and competing 1P on-demand grocery services and considers the challenges they face.

Reno Bianchi has long opined that Turkish Airlines has withstood the pandemic pressures better than most other global airlines. Recent results unequivocally support this theory. This has not gone unnoticed in the equity market as its ADRs are up more than 200% YTD. However, the fixed income market has been seemingly indifferent to the airline’s substantial operating and financial progress. THYAO 4.2% due 2027 continues to trade at a deep discount to par. Reno maintains his Overweight recommendation on the airline’s only EETC tranche and would not hesitate to pay considerably more than Bloomberg’s current quote price.

Indonesia’s latest tech IPO sees the owners of eCommerce firm, Blibli, raise approx. US$515m - Sumeet Singh’s pre-IPO analysis revealed no clear signs of profitability improving. Not to mention the lack of synergies across its offerings. He believes the stock will have a similar fate as GoTo, which is trading well below its IPO price and is likely to go even lower when its lock-up expires later this month. Based on Sumeet’s estimates, Blibli should be trading at least 50% below its IPO price.

Propitious Research

Indian IT Services

Following the purple patch of growth experienced in the wake of accelerated digitisation following the global pandemic, revenue growth has continued to slow down. Operating margin deterioration has also continued, despite significant FX tailwinds, largely due to the inflationary impact of increased employee attrition rates (to record levels) across the industry. Given weakening near-term growth prospects and above-fair valuation levels, Wium Malan remains cautious on the sector. In this insight, he focuses on the four largest companies in the sector - Tata Consultancy Services, Infosys, HCL Technologies and Wipro.

Macro Research

Developed Markets

Central Banks still believe they can get away with the bare minimum to arrest inflation

On the one hand you have the ECB’s approach of ‘we will create a recession to bring inflation down’, which James Aitken has no doubt they will. On the other hand, you have the Fed: same idea, different language. Since Jackson Hole Powell has stopped using the words ‘soft landing’ which have been replaced by ‘narrow path’. Then you have the BoE. Despite thirty years of evidence to the contrary, the MPC seems to believe that during the current inflationary episode, peak Bank Rate will be well below peak Fed Funds. As James writes, peak RBNZ (OIS) is @ 521bp, peak Fed (OIS) @ 511bp, peak BoE (OIS) @ 465bp, peak Bank of Canada (OIS) @ 447bp, peak ECB (OID) @ 300bp and peak RBA (futures) @ 399bp. James thinks that all of them are still too low.

UK: The Credibility Doom Loop

Helen Thomas points out that the LDI Gilt yield debacle should serve as a salutary lesson for countries that pursued relentless monetary easing since March 2020. The pivot from “whatever it takes to prevent a market meltdown” to “whatever it takes to stop inflation” necessitates a withdrawal of liquidity that will expose the excessive yield-hunting risk-taking taking place. Central bank credibility will come under increasing scrutiny as they seek to balance the incompatible goals of tightening monetary conditions whilst preserving financial stability. In her latest article, Helen dives into the latest Treasury Select Committee hearing and what it means for the UK and central banks across the globe.

MRB Partners

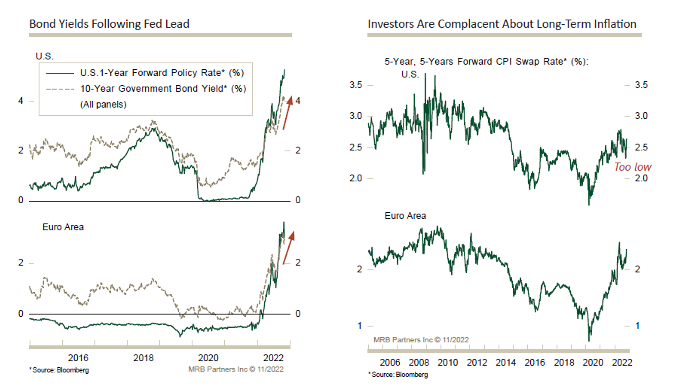

Complacency about long-term inflation

Major central banks will soon shift to a more moderate pace of hikes. In the near-term, bonds remain oversold and have moved in lockstep with expected policy rates, such that the risks to G7 government bond yields are to the upside. While bond yields are following the Fed’s lead, Phillip Colmar still expects a positive total return on bonds on a 6–12-month horizon. While both the Fed and ECB are likely to pause next year, it is premature to price in rate cuts thereafter because inflation will prove stickier than expected. Furthermore, markets remain overly sanguine about longer term inflation.

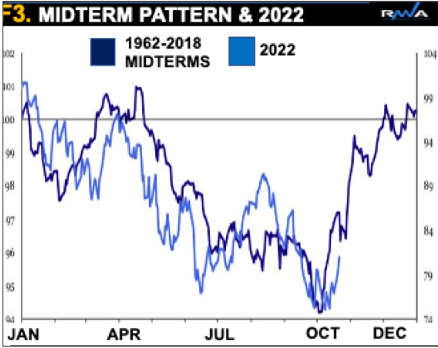

US: Politics & portfolios, how will midterms impact?

The 2022 midterm could trigger a relief-rally, in-line with an average return of 16.3%, in the 12-months periods afterwards. A typical reason is the “political put”, whereby investors expect leadership to take necessary measures to support the market and appease voters. This time it is likely due to gridlock! With polls showing the Democrats could suffer from the so-called “midterm curse” whereby incumbent parties are fated to lose seats. This stalls any major legislation and freeze the splurge in spending. Additionally, policy factors near a record low and may serve as a contrarian bullish setup. Perhaps a Fed pivot or China re-opening finally ahead, or an unknown scenario? Ron William’s cycle model signals a brief upsurge into the new year followed by a rollover, as macro headwinds weigh in!

Don’t believe anything the Fed Chairman says

Under the false pretence of strong labour markets and more rate hikes, Chairman Powell encouraged macro traders to expect more big interest rate hikes, so they bought USD, sold TBonds and shorted the stock market, which are all very crowded trades. You might think Michael Belkin is bearish because of the weakening economic picture, but he forecasts bounce potential in many depressed stocks and global stock indexes. Most investors believe that Fed interest policy is the primary determinate of stock prices, and once investors have a whiff of the forthcoming reversal in policy, we should see a bear market rally in stock indexes and many depressed groups. Go SHORT the USD, LONG TBonds, LONG stock indexes and higher-beta industry groups.

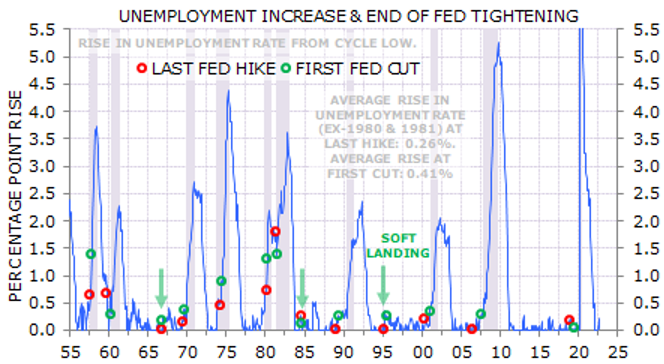

US: Unemployment, not inflation, normally drives Fed pivots

Historically, the Fed pivots when unemployment starts to rise, not when inflation starts to fall. It makes sense, explains Gerard Minack, given that inflation is a lagging indicator. He remarks that the usual time between the last hike in a Fed cycle and the first cut has been 3 months, but the last three cycles saw an exceptional average of 10 months. This was because the Fed had started to tighten well ahead of a potential inflation breakout, but now they’re playing catchup. The markets are right to expect the Fed easing policy by late 2023, but they’re underestimating the pace of cuts through 2024. All that matters for equities is whether the economic landing is soft or hard - expect it to be the latter.

US to witness weakest rates of real money growth since the Great Depression

The Fed allowed an increase in base liquidity last week, which has been reflected in a degree of stability in bond yields and a softer USD. Unfortunately, Andrew Hunt expects heavy levels of bond issuance to reverse these better trends over the coming weeks. Indeed, Andrew believes we could be on the cusp of the weakest rates of money growth in generations. He also notes that the US banking system seems to be withdrawing further from foreign credit markets. This, and the overall monetary environment, should be USD positive over the coming weeks.

Suttle Economics

Keep your eye on Japan

Tokyo approved a supplementary budget which sees extra spending amounting to ¥29.1 trillion (5.25% of GDP), funded by an extra ¥22 trillion of bond issuance. This one seems like a pretty sizeable stimulus to Phil Suttle. The justification behind the fiscal push is to provide households with a cost-of-living relief, yet Phil knows of no coherent economic framework in which fiscal stimulus and ultra-easy money at full employment delivers lower prices. He does, however, know that such a policy mix can often produce deep crises, generally led by capital flight. The country has maintained a high government debt ratio of 264% of GDP but their net interest burden on this debt in 2022 will amount to only 0.5% of GDP. Imagine them having to pay 3-5% on this debt, that’s a large snowball to avoid.

Ollari Consulting

USD/JPY following the script

As Christophe Ollari highlighted recently, after the first MoF FX intervention, the 140.20 previous breakout level remained support. After the second MoF FX intervention, the trigger for the first intervention (145.20/50) also remained support. While, Christophe also knew that the only one time in 2022 when the 50DMA got broken, it quickly tested the 100DMA. Thursday’s price action saw stop activated through 145 which was also coinciding with the 50DMA. This triggered a brutal sell-off down to the 100DMA that has been just reached now. Christophe expects some relief here. If the 100DMA breaks, he reckons we can quickly go down to 135.

Emerging Markets

China is the only 15%+ equity market in the world

Despite the cloudy outlook for zero-Covid China, Manoj Pradhan is optimistic on China on the basis of policy easing. We have the usual suspects that have been in action – rate cuts, infrastructure investment, special bond issuance – but Manoj is drawn by a range of policy measures designed specially to support housing. On the whole, the breadth of policy easing in China will deliver growth that no other economy can match for the next 6-9 months. Investors should stay in developer equities (as per Manoj’s Sept recommendations) and look to add the broader equity market.

China: Equities jump in response to signs of zero-Covid policy ending

Niall Ferguson retains his view that the government will relax restrictions incrementally in 2023, but this policy shift has a hard limit; cities and provinces will continue to lock down whenever community spread is detected as Beijing simply cannot afford further relaxation of rules. With no plans around booster vaccines or mandates in place and no clear timeline forward, the macroeconomic upside from the mooted easing measures has been exaggerated.

Argentina: The government’s financial program will be under stress in 2023

Even with a debt swap, financing the deficit until year-end will be a herculean task. Marcos Buscaglia runs two scenarios. In the optimistic one, the market rolls over 108% of the debt maturities, and the central bank would thus not need to issue pesos to finance the government. If the roll over ratio drops, the government will likely have to resort to substantial monetary financing. In the second scenario Marcos assumes the roll over ratio drops to 85% in the first nine months of the year, implying a monetary financing of ARS4.5tn. That Peso issuance would certainly be partially sterilised through Leliqs, raising the quasi-fiscal deficit above 6% of GDP in 2023 according to Marcos’ estimates, and sending inflation above 100%.

Brazil under Luna is little different than from under Bolsanaro

…at least from a macro and market perspective, explains Jonathan Anderson. Economic performance over the past 30 years has been driven by external growth and commodity conditions, as well as the related leverage cycle at home, and this is equally true today. He is LONG Brazilian assets given the combination of domestic deleveraging, supportive external conditions, falling inflation and high interest rates. However, he isn’t interested in buying Brazil “structurally” due to the global downturn and Brazil’s own fading industrial capacity, which makes Brazil the opposite of other EM countries he holds through current weakness in light of buoyant export prospects, such as Vietnam and the CEE periphery.

Burumcekci Research & Consulting

Turkey: Gold and FX reserves still on a negative course

Haluk Burumcekci’s latest report examines the ownership status of Turkey’s Central Bank’s (CBRT’s) gold and FX reserves at the end of October. Although a significant part of the foreign exchange flows in recent months have been directed to the CBRT, the Bank has been unable to achieve a consistent accumulation in total and net reserves, with factors indicating a clearly negative course. Haluk argues that the CBRT does not have its own (purchased) FX reserves and that FX reserves are at a negative level (- $65.2bn), even if the Treasury’s foreign currency deposit is not deducted. He calculates the CBT’s ownership status at - $32.4bn.

Commodities

Crude in for hyper-volatility

A slumping USD, impending December 5th EU bans against Russia, and heightened tensions between Iran and its neighbours in the Middle East are all current tailwinds for crude right now. But Vandana Hari notes the economic and oil demand concerns that are lurking in the shadows. We have the UK with its 75bp interest rate increase and warnings of its longest-ever recession, and Vandana also advises caution around rumours of Beijing readying a plan for a conditional easing of its zero-Covid policy. With myriad uncertainties stacked high on both the supply and demand fronts, it’s time to belt up for a period of hyper-volatility in crude.

Global Macro Investor

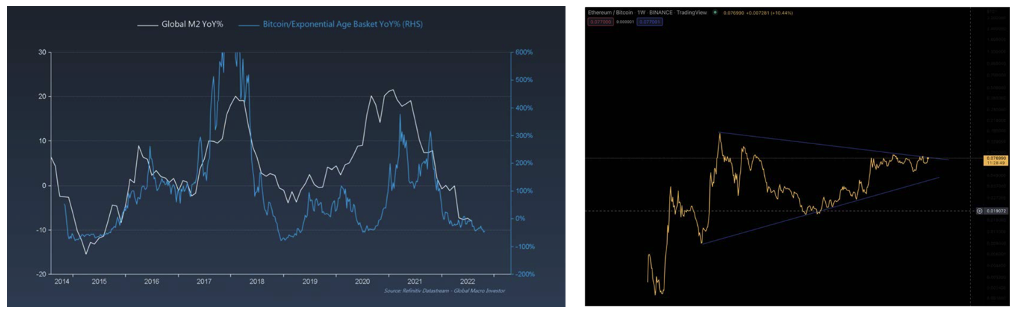

Crypto: The most bullish graph on Earth

M2 is about to turn, hard, claims Raoul Pal. When M2 goes up a lot, Bitcoin (BTC) goes exponential, so much that Raoul can’t scale the top of the chart (see chart 1). Bitcoin inverted is also exactly following the RRP, and when this starts reducing, we’re going to see Bitcoin explode. Yet Raoul isn’t buying Bitcoin since far superior crypto assets are available; indeed, he sees the Ethereum/BTC cross rate as the single most bullish chart on earth, suggesting that ETH may get 10x or more the performance of BTC (chart 2, log). Crypto is the fastest adoption of any technology in all human history, don’t miss out. BUY Ethereum and SOL.

Longview Economics

All that glitters is gold

Harry Colvin remarks that gold and silver are base building, which is technically bullish and typical at key turning points. Gold has tested and held above its recent intra-day lows of $1,618 on three occasions in the past month (see chart), and silver has been building a base since its June low ($18/oz.), as well as a reverse head and shoulders price pattern. Sentiment and positioning in precious metals are bearish, therefore generating a contrarian BUY signal. Move LONG Vanek gold miners ETF at current prices, place stop at $21.1 and risk 50bps on this trade. Stay LONG December ’22 gold futures position.

Independent Strategy

Oil to boil

Russia will disrupt the oil market rather than sell below caps, especially since Putin sees this as one of his key escalation weapons. The global tanker constraint will stop Russia shipping meaningfully more oil to Dark Markets and EMs. India and China don’t want more Russian oil dependence, so Russia will shut down capacity. We will see global supply shrink, but not demand. And do not expect help from OPEC. David Roche is adding LONG oil to his portfolio.