Company & Sector Research

Europe

the IDEA!

What’s New(s) in Amsterdam

InPost (INPST) - Impressive 1H22 but best is yet to come. OOH solutions are consumer centric, environmentally friendly and above all cheap. In view of the Green Deal and ESG reporting which has become mandatory for a lot of InPost’s clients, minimising carbon footprint is becoming an increasingly important driver re. transformation of last mile delivery.

Just Eat Takeaway (TKWY) - Further job cuts announced (this time in Canada) as management continues to target improvements in the profitability of JET's various units. Positive stance maintained.

Philips (PHIA) - VEB demands €16bn in damages re. the apnoea affair. More claims to follow. Shares to remain under pressure.

Hedgeye

PAH3 / POAHY is the best way to own Volkswagen according to Jay Van Sciver - Porsche SE principally owns VW common shares. VW trades at a discount to a SOTP valuation, with just the Porsche franchise likely worth more than the entire VW current Mkt/Cap. Then, Porsche SE trades at roughly 30% discount to the market value of those VW common shares. A Porsche IPO should make all this obvious and begin to unlock the value. Being on the same terms as the Porsche family is the most reasonable path to taking advantage of this disconnect as they go through the IPO. Porsche SE is the only long auto OEM Hedgeye currently has on their Best Ideas list.

Forensic Alpha

This wind turbine manufacturer has previously been on Forensic Alpha’s radar due to a litany of flags, including rising contract assets, use of supply chain financing and weak cash flow. The publication of H1 financial statements only adds to their concerns. At best it appears Vestas is a business that requires much more working capital investment than it did in the past, resulting in the poor cash generation investors have become used to. At worst the company may be booking revenue to accrual accounts (some of it through JVs and associates) that may never materialise as cash.

Smart Insider

Soren Skou (CEO since 2012) purchases €563k of shares at DKK16,746. He has an excellent record as a buyer, making a series of purchases into rising prices, most recently buying stock at DKK12,558 in Feb’21. What is intriguing about this purchase is that just one month ago he made his largest sale ever, an option exercise and sale that netted him €5.4m. That sale at DKK22,210 was perfectly timed, as was his option sale in Dec’21 at DKK23,303. Nevertheless, this is still an unusually large buy from him and as a result Smart Insider increases the company's Stock Rank to +N (positive rating).

Stockcube

FTSE Top 200 Weekly Technical Strategy

Stockcube’s Model Portfolio currently has 29 Longs (avg. gain +5%) and 18 Shorts (avg. gain +10.5%) - net position increases from 9% to 23%. Within sectors, F&B, Banks and Tobacco remain at the top of the price and relative range; Leisure reasserts downtrends; and Real Estate makes new relative lows, but becomes overextended. They recently opened longs in Beazley Group (tests medium term highs), Just Eat Takeaway (develops short term base) and TP ICAP (confirms short term price and relative base) along with a short in United Utilities (forms short term tops).

North America

MYST Advisors

Bear’s Den Idea Forum

Interesting shift in sentiment at MYST's latest buy-side event as the vast majority of participants felt the market did in fact bottom in June (vs. only a handful 5 weeks ago). The most compelling short ideas presented included:

Pfizer (PFE) - Adverse impact of Inflation Reduction Act not fully appreciated by the Street. TP $33 (30% downside).

Olaplex (OLPX) - Extraordinarily high margins to contract as competition intensifies and growth slows. TP $8 (35% downside).

Rogers Corp (ROG) - Expensive acquisition by DuPont in doubt as China regulatory approval delays persist. TP $170 (35% downside).

Sprout Social (SPT) - Low quality Software Co. trades at absurd valuation despite declining net adds / higher churn. TP $43 (35% downside).

EETCs look attractive

The recent appreciable trading weakness endured by most EETCs has made this space quite attractive for investors with a medium to long term view. AA tranches - buy most of the issues yielding over 5.5% and leverage these positions to the maximum extent. Individual security selection is not of the utmost importance given the structural soundness of these securities. A tranches - the current sweet spot. In Asterisk’s monthly update they highlight nine securities all yielding well over 8.0% that are their key long recommendations. B tranches - should be considered by investors seeking to invest cash in very high yielding short-dated securities.

MAPsignals

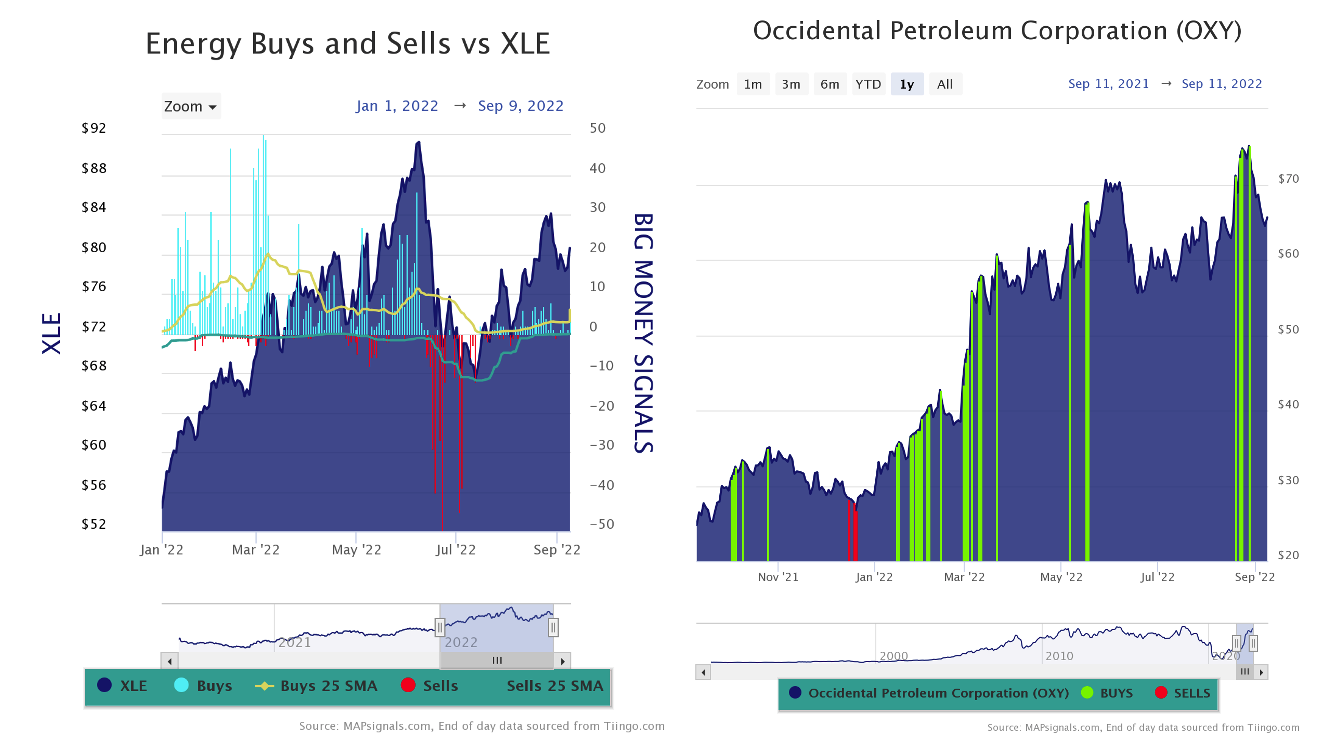

Energy stocks are set to continue thriving...

MAPsignals allows broad and granular self-directed research through a proprietary approach looking for unusual institutional buying of stocks that no one else offers, and the buying data, along with the strong fundamental backdrop indicates energy stocks are set to continue to thrive. Chart 1 clearly shows that big professional traders have been buying energy stocks for most of the year. Digging deeper, MAPsignals research portal software also allows users to see the stocks getting bought on a given day. Chart 2 shows how Occidental Petroleum has regularly featured in their Top20 report - the best ranked stocks getting unusually bought each week.

Off Wall Street

A large percentage of SSTK's business faces a massive threat that is only likely to accelerate over the next 24 months - generative AI image models, which can create detailed, accurate, and high quality images based on written prompts, represent an existential threat to the stock image industry. One of the leading models, OpenAI's DALL-E 2, recently began an open beta with pricing on a per image basis much cheaper than SSTK. Margins will resume their long term decline. TP $30 (45% downside) represents an EV of 1x OWS’ 2023 and 2024 revenue estimates and 5x their 2023 and 2024 EBITDA estimates.

The Retail Tracker

Around the Stores: Providing weekly insights into merchandising, promotions and sales trends…

Bed Bath & Beyond (BBBY) - Lacked inventory, energy, and sales help. Heard story after story about disappointed college shoppers.

Torrid Holdings (CURV) - Very under the radar. Website looks amazing with denim balanced with wear to work, dates and dresses.

Ralph Lauren (RL) - Very strong all around. Polo store looks outstanding and the Polo men’s assortments at Macy’s and Bloomingdale’s fantastic. Also found the Lauren sets in apparel and handbags in Macy's significantly improved.

Capri Holdings (CPRI) - Kors has some good new styles that break out of the logo story. Stores are cleaner promotionally than they have been. Versace was still very busy and is trending.

Compass Restaurant Consulting & Research

Stands out for the wrong reasons in Steve Crichlow’s monthly Restaurant Industry Pulse Report - August sales were negative and momentum decreased due to a failure to offer promotional items that would resonate with consumers (2 for $6.99 promotion is very good but the ads are confusing. The new Oven Baked Pastas, while good in theory, according to customers the taste and presentation made them unappealing). For September, SSS expectations are in the negative 4-2% range based on current momentum and failure of the relaunched Detroit Pizza promotion. Additionally, Pizza Hut gave up its sponsorship to the NFL and will suffer from this all season.

Paragon Intel

Decision to hire Laxman Narasimhan as the new CEO could be a mistake - Paragon’s previous diligence report includes interviews with 18 former colleagues, all of whom found him to be arrogant, self-centred, insecure, and abrasive. As a result, he destroys company culture and is not well-liked. Furthermore, he lacks the ability to execute on a long-term strategy. At Reckitt he underperformed as CEO (destroyed 17% alpha for shareholders), performance they believe stems from a "lack of deep understanding of the business”. Paragon will be supplementing their previous work on Narasimhan with interviews with former colleagues at Reckitt.

Radio Free Mobile

Form over substance - unimpressed with AAPL’s latest launch event, Richard Windsor believes the tech giant is now going to feel the full sting of the weak macro environment. Against this backdrop, the shares are not particularly cheap and there are plenty of other options to look at that offer far higher growth at a lower multiple. In a separate note, Richard also discusses the difficulties AAPL faces to keep both the CCP and the US Congress happy and is likely to be forced to drop its budding relationship with YMTC, meaning the Chinese memory chip maker will disappear once again into industry obscurity.

Inflection Point Research, LLC

Provides leading edge solutions to datacentres that increases performance, saves power and money - what is most notable is the breadth of the applications for the company's technology solutions. CRDO's IP licensing contributes at the chip level; gearboxes and retimers at the board level; AECs to short (<12m) intra rack connection; PAM4 DSPs to 2km-40km optical links; and its MACsec solutions contribute to coherent transmission over 1000’s of km. But the best thing is that it’s all being driven by CRDO’s hyperscale customers. Many small semi companies have been acquired for exorbitant amounts of money and with tech much less valuable.

BWS Financial

Share price is up c.150% since Hamed Khorsand turned bullish (Oct 2019), but he still sees further upside following Q4 results where revenue smashed his expectations (up nearly 24% Q/Q). Enterprise Technology was only $2m away from its highest ever revenue performance, while Service Provider revenue grew by 56% sequentially. Demand remains healthy enough to put UI back on pace for potentially exceeding $500m in revenue in a single quarter. Hamed increases his FY23 revenue estimate to $1.9bn and forecasts net income of $446m. UI should manage to grow EPS by 20%+ (to $7.38) and potentially by as much as 27% in fiscal 2024.

Australia

Aequitas Research

Aims to raise ~US$2bn to fund the purchase of its majority interest in Chicago Skyway - ALX’s largest shareholder, IFM (who recently increased their stake to 19.99%) has already publicly stated its opposition for the deal, nonetheless the company has chosen to go ahead with the acquisition. The performance of the shares are likely to be driven more by what IFM does next rather than the company’s fundamentals. The deal scores a negative score on Aequitas’ ECM framework owing to its large size and not being accretive to earnings in the near term - this is one to avoid for new shareholders even at the entitlement offer price.

Global Mining Research

GMR weighs up the investment case for these two project developers with assets based in northern Brazil - each control large scale nickel deposits that leave them potentially attractive as corporate targets. Both have types of projects that a +US$9/lb nickel spot price should incentivise. However, CTM is GMR's preferred choice on near term news flow. It trades on 0.7x NPV and has the advantage of pursuing a lower cost nickel sulphide mine with attractive economic returns. HZM (rated Hold) has better leverage / scale, but technical risks dominate.

Japan

Storm Research

Small cap growth opportunities...

Having peaked in Oct 2020, Japanese small cap growth stocks proved themselves a lead indicator on the downside. They remain 45% below peak, but are starting to inflect. With the Yen/USD trading at 24 year lows, Storm Research believes investors would be well served to re-examine this largely ignored asset class. Recent ideas include Dexerials (4980, Positive), WealthNavi (7342, Positive) and BuySell Technologies (7685, Positive).

Emerging Markets

New Street Research

It is rare for a single company to be able to change the direction of an industry globally, but New Street thinks that is what happened at Reliance Industries AGM where Mukesh Ambani, the Chairman of RIL and founder of Reliance Jio announced a target of 100m 5G FWA subscribers in India in coming years. For context, New Street estimates there are currently around 2-3m FWA subscribers globally. Jio’s announcement on its own therefore turbocharges the entire FWA industry. FWA in EM today is analogous to 2G mobile in 2000, with outsized returns likely given modest market expectations and strong underlying demand.

Horizon Insights

Going global - Horizon Insights expects SANY, a leading excavator manufacturer in China, to benefit from the export boom taking place in the sector. It has already captured 30% of the domestic market and is quickly improving its global market share. SANY is currently the market leader in many Southeast Asia countries and continues to develop localised products to meet the unique needs of the European market, while expanding its sales network in the US. Given that the next round of excavator growth is to be fuelled by electrification, SANY has also been dipping its toes in battery & electric control technology.

Silk Road Research

China Elevators: 3Q22 orders tracking below expectations

SRR's channel checks point to orders growth in the negative 15-25% Y/Y range through August - worse than the negative 5-15% range that occurred in 1H22, despite an easier comp. Although their early September read is slightly better, it may not be enough to lift the quarter especially since there have also been less-than-encouraging reports of industry layoffs at Elevator OEM factories in the Shanghai region. OTIS and Hitachi appear to have held / gained market share 3QTD and YTD, while Schindler and Thyssen have lagged. After a strong 1H22 KONE appears to be struggling.

Macro Research

Developed Markets

Greenmantle

Woes of the UK

As the United Kingdom and the world mourns the death of Queen Elizabeth II, attention has been temporarily deflected from the country’s economic, social and political woes. Truss announced an enormous fiscal package to aid households in the cost-of-living crisis, which Niall Ferguson predicts will cost £100-150bn. Combined with tax cuts, the fiscal expansion will be inflationary over the medium- and long-term, hence why Niall is more hawkish than the market, expecting a 75bp raise at the next MPC meeting and a ~4.5% policy by March 2023. He remains bearish UK assets and medium-term bearish on sterling.

Andrew Hunt Economics

UK: Trussnomics

Liz Truss’s policies are being equated with Reagonomics, but Andrew Hunt disagrees. Whilst Volcker set out to create a negative output gap in the US, Truss is aiming not to reduce aggregate demand but instead to foster a supply side recovery, which Andrew Hunt believes will be insufficient. Inflation in non-energy goods and services will accelerate next year. Continued underlying inflation and funding stresses in the Gilt market should place further significant pressure on Gilt yields over Q4, and in 2023 Gilt yields should remain elevated by global standards; Andrew’s near-term target for Gilt 10Y yields is 4%.

Harlyn Research

Euro and Sterling FX markets could become disorderly

Simon Goodfellow sees the prospect of a currency crisis getting more likely by the day. He has long thought the hiking cycle in the US would cause at least one major asset class to come unstuck, and the price action suggests it’s European currencies. Both EUR and GBP have broken out of previous trading ranges and could test historic lows of the FX markets. European investors need to own as many natural hedges as they can – US issuers in credit and dollar earners in equities.

Ineichen Research and Management

European economic sentiment continues its decline

The ZEW survey for the Eurozone fell by 2.2 standard deviation (sd) in September with the one for Germany falling 1.5 sd which was worse than expected. Many Eurozone business sentiment indices have been in decline prior the Ukraine war. Furthermore, outliers, i.e., sharp falls in these indicators, remain on the negative side. IR&M’s regime tests nowcast continuous below-average returns for risky assets in Europe.

Click here to read the report.

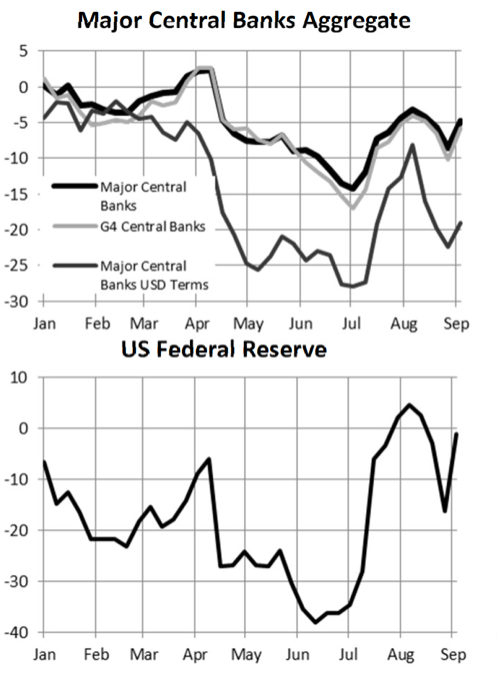

CrossBorder Capital

Fed data evidences rollercoaster re-normalisation

Fed QT stepped up a gear in the week following the Jackson Hole Symposium, when Fed Chair Powell struck a hawkish note. Yet, Fed QT has since tempered. Michael Howell is not reading too much into this. As the graph shows, short-term variations in the pace of QT are par for the course. Michael’s take is reinforced by the continued strength of the USD against the euro, sterling and yen. Against this background, BoJ liquidity conditions are fast deteriorating, the ECB is undertaking an orderly renormalisation of its balance sheet, and the PBoC is not intervening as much as might be expected.

Belkin Report

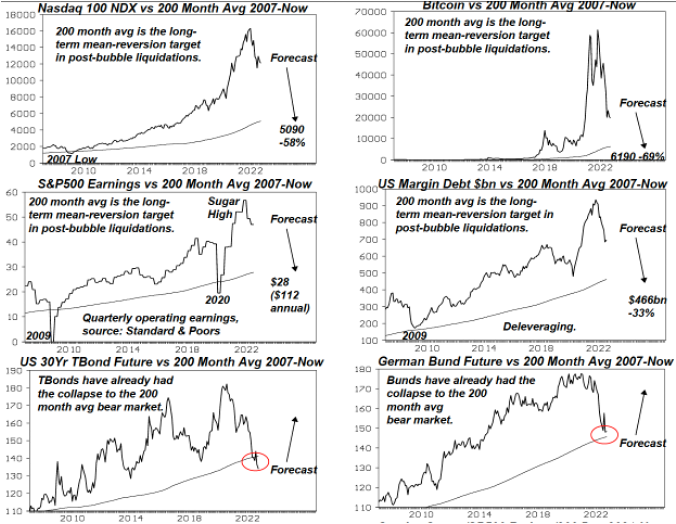

A classic deleveraging of a stimulus-induced speculative bubble is underway

Stimulus wasn’t necessary in the first place, claims Michael Belkin. The huge flood of money precipitated a huge speculative bubble in financial markets and investors are now taking for granted an unsustainable sugar high. Wall Street consensus earnings expectations are disgustingly wrong, and Michael argues that the previous big increase of S&P500 earnings was completely artificial! He recommends selling and shorting equities inro brief market bounces, shifting into utilities and consumer staples for long exposure and shifting out of equities into government bonds asset allocators.

Macrolens

Two trades in a tricky environment

Against the backdrop of a Fed dealing with so much at stake, we’re in an environment that’s extremely tricky for tactical trading. Brian Mccarthy advises investors to look for RV-type trades with a positive risk-reward skew that might serve to mitigate the directional risk embedded in a portfolio. He suggests an EDH3 ratio covered put, which sells the tails and captures most likely reasonable outcomes for the Fed terminal rate, and a CNH long funding trade (sell USD/CNH 1m at ~25pips and buy USD/CNH 12m at ~800pips) which is closer to a free hedge.

Ollari Consulting

Japan: A trapped BoJ

Christophe Ollari discusses the yen’s inexorable slide contributing to a terms of trade shock which is already becoming self-fulfilling. We’re seeing a BoJ threatening to intervene AND doing everything to keep the current unprecedented monetary policy divergence. A sole FX intervention will not work, argues Christophe, and the BoJ is trapped; a strong JPY appreciation will only unfold if either chief Kuroda abandons the YCC or we witness a massive treasuries rally, consequence of a US recession.

Emerging Markets

Greenmantle

China: Debt by a thousand cuts

China’s real estate is in crisis, says Niall Ferguson. Beijing will try to muddle through the next few months with an incremental bailout, but its actions will be insufficient; home sales will keep sliding and more developers will default. Should Beijing continue its zero-covid trajectory, property sales will decline by 30% by H2/2023 and the risks will spread to the local government and banking sector. A full-blown financial crisis will be averted, but markets will sharply downgrade their long-term growth expectations for China. The Japanification of China has begun.

Talking Heads Macro

Getting constructive on China

Despite the risk, Manoj Pradhan feels optimistic about China asset prices. Beijing is being forced to provide a breadth of policy support that only occurs when panic truly sets in; it won’t be the size of 2020’s fiscal package, but if China’s left-tail risk is cut out through injection of liquidity and guarantees based on solvency, then asset prices have upside. He advises building small positions in equities, betting on a steeper curve, and assuming that a substantial China rebound is needed for the CNH to fight the USD.

Horizon Insights

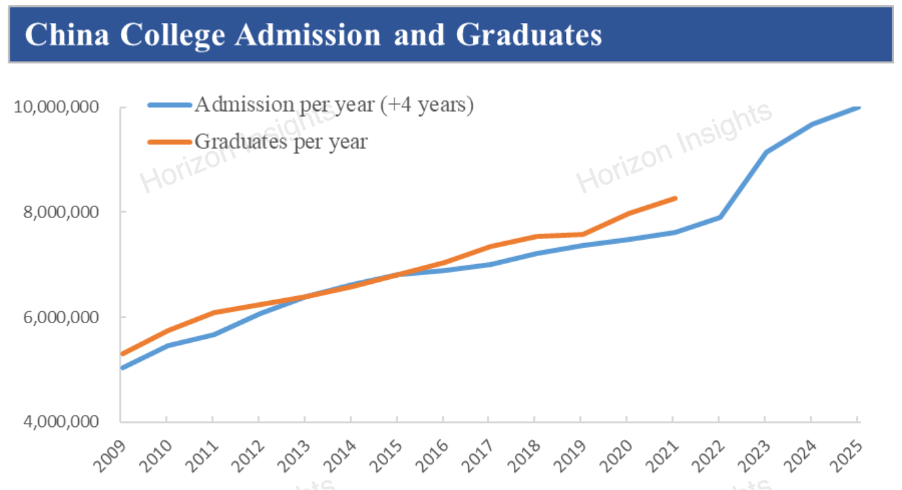

Markets are too pessimistic about China

The typical bearish consensus view forecasts a near-future plunge to 3-4% growth in GDP per year. Horizon Insights disagrees. Continuous increases in the country’s high-quality work force, in the form of 10 million new college graduates each year (see graph), will be the main reason growth will not ail as much as expected. With M2 growing at a pace of ~12%, expect growth rates to remain at 4-5% per year. Expect a reversal moment in the property sector soon as the fundamentals stop deteriorating further.

PRC Macro

China: National security economics will dominate resource allocation

William Hess believes the increased investment in military-oriented sectors during Xi’s third term will create new sources of growth uncorrelated with structural negatives, with capex likely to increase significantly in coming years. As part of national security economics, we will see more state-owned enterprise mega mergers in strategic sectors, including the semiconductor industry’s shift away from the VC/PE model to one relying on large-cap SOEs. This, along with accommodative monetary policy, should be equity market positive despite the lingering impacts of Covid and the property recession.

Creative Portfolios

Which markets do you buy?

Paul Hollingworth’s model identifies markets which have delivered a strong 12-month relative return but a relatively subpar or below-average 36 month return, which Paul deems a strong behavioural system. September’s model suggestions include being overweight Latin America (except Argentina) and a mix of selective markets such as Turkey. In Asia, Indonesia is favoured followed by Thailand. Underweight or arbitrage shorting opportunities are present, including Argentina, Taiwan, copper and sugar.

Eurointelligence

Russia: Has Putin’s gas weapon misfired?

A spooked Kremlin shut off Nord Stream 1 sooner than expected but European gas prices have still tumbled. It will no doubt be a difficult winter ahead for Europe who must replace 155bn cubic metres of gas if Russian gas were to disappear entirely. Yet, Wolfgang Münchau isn’t entirely pessimistic. Through careful planning and incentives, and possibly a restart of France’s offline nuclear reactors, there is even more scope for demand reduction in a way that spares major economies a hit. With spot gas prices potentially falling to a manageable €100/MwH, has Putin made another severe miscalculation?

Commodities

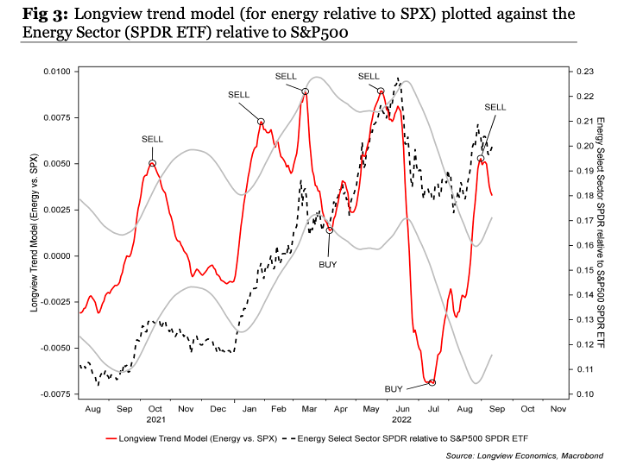

Longview Economics

Energy: A contrarian sell signal

Oil market fundamentals are poor, with the recent energy sector outperformance likely to reverse in the near term. Harry Colvin’s medium-term models are on, or close to, SELL levels, with energy overbought relative to the index (see chart). Nevertheless, positioning and sentiment towards energy remains bullish, with the net long futures position amongst asset managers/institutions accelerating in recent weeks and investors still overweight energy relative to equities. Harry advises to move SHORT S&P Energy sector ETF against a long position in the S&P500 SPDR ETF, with ½ the position at current prices and ½ on strength (at a ratio of 0.210). Place stop at 0.220 and risk 100bps on this trade.

Vanda Insights

Crude’s brief dive below $90 suggests OPEC+ resolve could soon be tested

Unless unforeseen supply shocks emerge, Vandana Hari expects crude to continue cascading lower into the end of the year. Russian supplies may have dropped, hurtling Europe further into its energy crisis, but the oil complex is shrugging it off with any incremental oil consumption in the continent dwarfed by concerns over global demand erosion. For now, OPEC+ can afford a wait-and-watch stance without risking the credibility of its pledge to cut output to avert further downward spirals; there is psychological support around $90, explains Vandana, albeit one that could be tested and breached unless the alliance is prepared to walk its talk.

Metals Focus

Annual Platinum Group Metals forecast

Metals Focus has recently announced the launch of a new annual PGM 10-year forecast, containing industry-leading insights into price trends, projections for key supply and demand components and the factors that will drive these sectors for platinum, palladium and rhodium over the next ten years. Key topics include autocatalyst demand, mine supply, jewellery, industrial data, and scrap market developments. Please contact us to find out more.