Company & Sector Research

Europe

Holland Advisors

Stepping into the light - share price jumps following the company’s FY update. Long-term bull Andrew Hollingworth thinks the rerating has only just begun. This is a company that has been through an extensive period of re-invention and investment. Its accounting has been uber prudent especially with reference to inventory and its store portfolio. Almost all investors have been referencing potential profitability vs. that recorded in this investment period. This has been an error. It has always been likely that post investment period margins would be better than its past peaks, due to discounting then and elevation now. TP £13.00+ (45%+ upside).

Blueshift Research

Is FEVR’s goal to be the #1 mixer brand in the US realistic? How is it performing in the “off-trade” retail segment? Is it making headway with major accounts in the “on-trade” restaurant and hospitality market? Is its new US leadership paying off? How is FEVR’s biggest national distribution agreement performing? Is its lower price initiative working? Is demand for upscale spirits and mixers on the wane? Will consumers trade down from high-end mixers due to the fear of recession? To answer these and other questions, Blueshift interviews beverage distributors, grocery chains, liquor stores, restaurants, bars, hotels, and other industry specialists.

Forensic Alpha

Inventory levels should be closely monitored - sheer scale of increase in DSI is a cause for concern. As at 30 June, inventories stood at €4.2bn, equivalent to over 5 months of sales. This has increased from €3.5bn at the end of last year and contributed to a CFFO outflow of over €500m in H1. While the Q2 analyst presentation calls it a "risk mitigation" exercise; the Q2 report appears to present a different nuance, describing it as "work in progress" that cannot be translated into finished goods. This suggests a higher level of risk associated with the supply chain.

ERA Research

Refreshed management team has taken bold action to enter North America (via Verso acquisition) and to exit underperforming assets - a leader in several niche markets, this packaging company has limited exposure to skyrocketing European energy prices, while its export options are enhanced with its low energy cost-base as well as the weaker euro. Q2 results were very strong, with sales growth across segments and a consolidated EBITDA margin of 20%. The outlook for Q3 is for price / mix to entirely offset input cost inflation. TP 190 SEK (45% upside).

MYST Advisors

Former one-trick pony now an exciting play on three high-growth opportunities within semiconductor fabrication - 1) MicroLED is “the future of display”; 2) Silicon Carbide, a leading material for EVs; and 3) Gallium Nitride, which is becoming the material of choice for all low-power charging devices (smartphones / PCs) and expanding towards higher-power markets (solar / data centres). Forecasts 20%+ / 30%+ upside to consensus FY23 / FY24 estimates. TP €41.00 (60% upside).

EquiVal Research

The future is on our plate

Against the background of a growing world population, our food system is considered unfit for purpose as it entails unsustainable or socially unacceptable environmental, animal and health costs. Agriculture and the food industry are responsible for about a quarter of global greenhouse gas emissions, largely because of animal farming. What is more, diets are biased towards animal fats, which have potentially detrimental health effects. Piers Nestler looks at the possible implications for the industry as he tries to identify beneficiaries from a transition to alternative proteins. Companies discussed BASF, Bayer, Biotalys, Danone, GEA, Kerry Group, KWS Saat and Vilmorin.

Copley Fund Research

France: Europe's high conviction holding

Global equity managers are positioned at their highest ever overweight in French equities - average holding weights have moved towards the top end of the 8-year range at 4.16%, pushing net overweights to a record +1.48% above the iShares ACWI ETF benchmark. Out of the 365 global funds in Copley’s analysis, 64.4% are overweight France compared to the ACWI index. Aggressive Growth and Yield managers have led the charge. On a stock level, LVMH is the most widely held name, while Sanofi and Capgemini have benefited from fund rotation this year.

North America

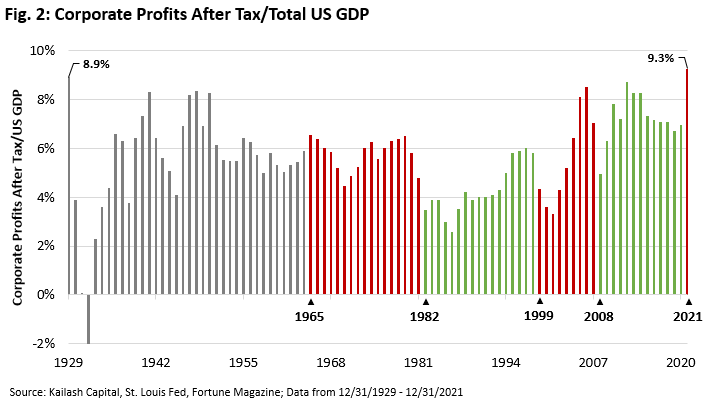

Kailash Capital Research

The Might of Margins & Mean Reversion: Are today’s profits sustainable?

The high-water mark for margins maybe in...

KCR's latest piece is designed to put today’s market valuations and margins in historical context. They believe forecasting the future is futile, but tremendous insights can be drawn by studying the past. In the spirit of that belief, their review of Warren Buffett’s Fortune Magazine article (Mr. Buffett on the Stock Market, 1999) highlights one of the most significant structural risks to investors today. At the end of the paper, KCR explains a tool they offer to subscribers. You can input your own assumptions around margins, growth, valuations, and interest rates to see what 10-year returns various assumptions generate using Mr. Buffett’s arithmetic.

Daniel Insights

Corporate Access: Hosting calls with industry thought-leaders

Peter Daniel hosts Zoom based calls with interesting industry (public & private companies) thought leaders for institutional equity investors. Here are some recent events. Stay tuned for future meetings...

Steve Saxon - Partner, McKinsey & Co., lives in Shanghai - Update on China Covid lockdown implications and supply chain issues.

Ward Nye - CEO - Martin Marietta Materials - Company update.

Dave Jackson - CEO - Knight-Swift Transportation - Company update.

Ryan Green - CEO - Gridwise - A mobile app that gig economy drivers use to track important job-related operating metrics.

Curtis Garrett - Former Chief Strategy Officer - Reconex - Update on the LTL Industry.

Bob Martin - CEO - Thor Industries - Company update and RVing industry review.

Spencer Patton - CEO - Route Consultant - Update on FDX ISP operators.

Valens Research

How to outperform in a bear market

Valens conducts deep fundamental work to identify investment themes that could underperform the broader market, and leverages proprietary tools including an adjusted accounting database, Embedded Expectations Analysis, and Earnings Call Forensics, among others, to identify which names are at risk for material downside. Over the past year, their Thematic Short Idea List has declined by 18%, while the broader market has only declined by c.6%, showcasing how owning these names in a long portfolio could lead to significantly poorer results. Recent shorts include Snap (-81% since inception), Six Flags (-42%), and Cognex (-41%).

Obex Capital Research

Delivering an inflection point - after two quarters of slogging through tough comps, incremental costs, and the rest...it is clear that AMZN is strengthening while other companies are weakening. Noteworthy highlights from 2Q22 include revenues accelerating and cost growth decelerating. No sign of discounting (stark contrast to others) and the competitive advantage of the fulfilment network is starting to shine through again. Advertising strength stood out (had the strongest quarter of all the large digital advertisers). AWS’ backlog is $100bn! It grew 65% this quarter (second highest rate in 3 years). AWS and Advertising are the entire valuation of AMZN right now.

Quo Vadis Capital

While there was a lot to like about 2Q22 results, John Zolidis argues CMG has taken too much price, too quickly, in an environment of increasing consumer price sensitivity - he believes the company is making a strategic error, by focusing on delivering arbitrary pre-Covid margin targets, and is imperilling its consumer offer in the process. In fact, John claims the negative impact of aggressive pricing is already evident in CMG customer metrics, and another 4% price hike this month will be met with further resistance. Analysts are raising estimates, but with transactions likely to turn negative by 4Q22, earnings downgrades are coming.

R5 Capital

R5's research reveals BBY’s business model is suffering from potential systemic challenges around its go-to-market strategy. Specifically, its high-touch showrooming model is under siege, in large part, due to an unprecedented crime wave impacting its stores. Management’s reaction has been to remove product from the floor or lock it up, transforming many stores to go from a showcase to a rather empty, uninspiring experience. This, in combination with flagging demand, deteriorating store conditions and supply chain challenges, leads Scott Mushkin to downgrade the stock to Sell.

Veritas Investment Research

Canadian Banks: Credit risk playbook for a recession

The coming credit storm - Nigel D'Souza expects provisions for credit losses in the upcoming cycle to match or potentially exceed PCLs during the GFC. Highlights from Nigel’s report include: 1) Household debt service ratio to set a record high. 2) International exposure to skew PCLs higher during a recession. 3) Real estate secured lending portfolios unlikely to drive material credit losses. 4) Wholesale portfolio credit risk likely to be more idiosyncratic than systemic. 5) Of the Big Six banks, Bank of Montreal would experience the highest peak PCL ratio during a recession (1.20% or 6.0x BMO's pre-pandemic level); National Bank the lowest (0.29%).

Paragon Intel

Possible M&A? Paragon’s JetTrack has been flagging some interesting flights between the two banks in recent months - this would be an acquisition that makes sense for USB and their acquisitive C-Suite. While more recent acquisitions have been focused in the Western US, CEO Cecere has stated that he would like to expand into the Southeast (where FITB has a large presence). Adding to the intrigue is the fact that USB flights have also been been tracked to Boston where multiple sizeable holders of both banks' stock are based.

Costigan Reports

Hidden gem ignored by the street - financial results posted over the past 18 months are too good for MLI to stay under the radar. The company is capitalising on increasing demand for investment in air conditioning / air quality and is reaping the benefits from a decade of significant Capex investments. MLI has been around for 100+ years and has a track record of making money in good times and bad. It currently trades at 7.3x Bob Costigan’s 2022 EPS estimate. The share price has more than doubled since he turned bullish, yet still offers 65% upside to his 1-Yr TP of $110 and over 150% upside to his 3-Yr TP.

Radio Free Mobile

Poor results and weak guidance - this is more about execution than the economy. Instead of 2023 EPS being c.$3.75 (PER 9.6x), EPS is now likely to be $2.00 to $2.25. This (again) brings down the “shut your eyes and buy it” moment from $36 per share to $20. INTC is no longer a value stock as its earnings have evaporated and one must now look through to the recovery. Although this is far from certain as Richard Windsor still has concerns re. the longevity of the x86 processor design and INTC’s financial strength is weakening fast. Qualcomm, MediaTek, and TSMC remain far better places to be in the semiconductor sector at the moment.

Emerging Markets

LightStream Research

Once one of the fastest growing segments within Chinese e-commerce, community group buying is starting to face multiple headwinds from funding shortages to excessive price competition. Oshadhi Kumarasiri points to PDD's competitors who have been announcing job cuts and rapidly scaling back operations over the last few months, and argues that the operating environment shouldn’t be much different for PDD. With QoQ revenue growth pretty much at a standstill and sales and marketing cost cutting almost fully exhausted, current consensus expectations are too optimistic and bound for a significant correction.

Hedgeye

In recent months this EdTech firm has staged an eyewatering rally as investors debate whether the sector’s surge is sustainable - Felix Wang doesn't consider Koolearn's new livestreaming platform to be the next big thing and says the market is already pricing in >70% revenue growth for blended FY23/FY24 which is far too aggressive. Furthermore, based on his channel checks, staff and operations costs are likely to rise substantially. As the company looks to spend capital building out supply chain, fulfilment centres and logistics infrastructure, it will struggle to post a profit. If you are looking for exposure to the sector, New Oriental is the better choice.

Galliano's Financials Research

On the back of 2Q22 results, Victor Galliano reviews six Thai banks’ core profitability, and their credit quality and coverage, to identify banks that are attractive value, have good earnings growth prospects and have the potential to deliver sustainably higher returns going forward. Krung Thai stands out with its low cost of risk, healthy post provision profitability vs. peers and its undemanding valuation multiples along with its low PEG ratio. Elsewhere, TMBThanachart is one to watch in the deep value category, especially given its attractive cost of risk trends over the last three quarters.

Alembic Global Advisors

Shares have underperformed a basket of their closest Western peers by 36% since March 2019 - there is a continuing, erroneous perception that Braskem is a Brazil-based, naphtha-biased polyethylene story, while ignoring the company's equal capacity of PE and PP, Brazil composing ~50% of EBITDA, and 40% feedstock exposure to NGLs. Braskem has meaningfully improved its operating rates, which, combined with cost management, has resulted in a significant (sustainable) boost in EBITDA margins. The shares trade at 0.40x replacement value and Hassan Ahmed continues to expect the company to be acquired. 12-month TP BRL50.00 (45% upside).

Niko Partners

The industry’s most comprehensive reports on esports in China and Asia

Asia is the world’s largest and most important region for esports, accounting for more than 57% of the USD $1.1bn global market, and is important to understand in its own right as well as a predictor of where the global esports industry is headed. Niko Partners is the leader in Asian games market intelligence and their latest reports cover market size and revenue, growth drivers and trends, game genres, top game titles, teams, tournaments and events, the esports ecosystem and organisation structures, women in esports, livestreaming, and mobile esports. For further details click here.

Macro Research

Developed Markets

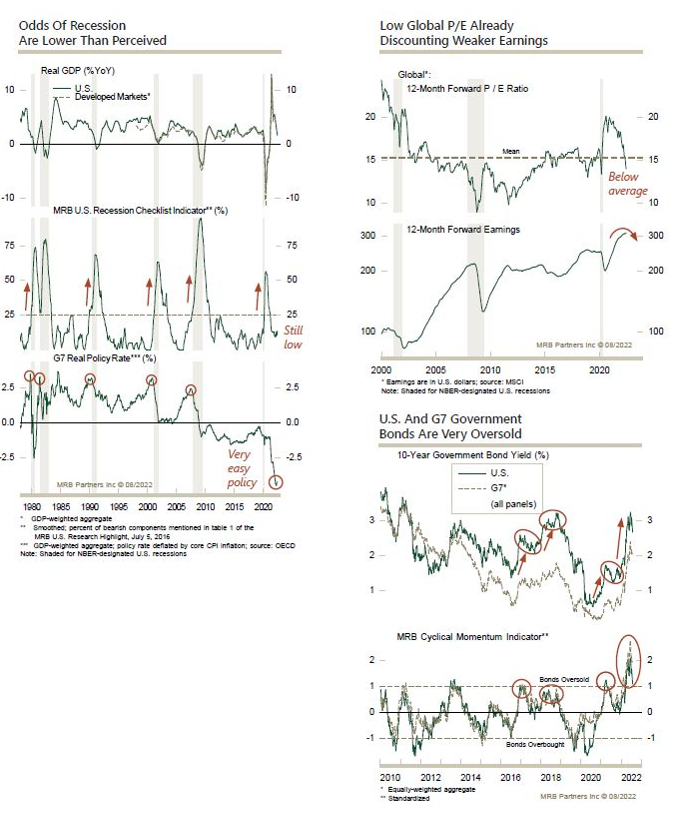

MRB Partners

Economic sentiment has become too bearish

The consensus shifted this year to embrace the call for a pending recession in the US and the global economy. Phillip Colmar challenges the validity of several core macro assumptions made by central banks and many investors, reinforcing his non-consensus call for a pronounced mid/late-cycle slowdown rather than a typical recessionary outcome (see graph 1). He sees room for global equities to bounce further. The bear market in government bonds is not over, but a further digestion phase should be expected while oversold conditions unwind and CPI moderates (see bottom-right graph, above).

Belkin Report

Government bonds have started a long-term bull market

It takes nerves to stay long bonds in the midst of Fed and ECB rate hikes, but that’s what Michael Belkin’s model forecast says to do. Michael’s equal-weighted index of global bonds has declined all the way to its 200-month average and has an upward forecast. In other words, govt bonds have already had the long-term bear market stocks have only just started. To put equity market downside risk in perspective, the 200-month average for the Nasdaq 100 is down -61% and for the S&P500 is down -50%. SELL stocks and BUY govt bonds.

Eurointelligence

Germany: The world of yesterday

Germans are slowly waking up to the idea that the supply chain deglobalisation constitutes an irrecoverable economic disaster, after long remaining in denial. Wolfgang Münchau believes that Germany’s structural savings surpluses are keeping the economy trapped in a bad equilibrium. There is no future for the current economic model; over the last two decades GDP kept growing because of immigration and wage moderation. Germany has never recovered from the pandemic and is now paying for the extraordinary complacency of the Schröder and Merkel years.

Variant Perception

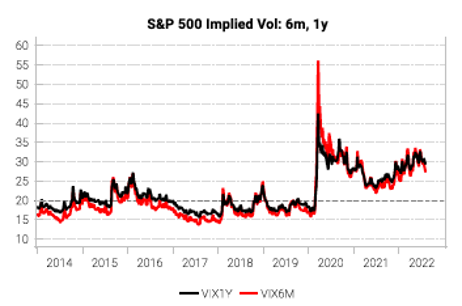

US: Short squeeze hits target, add back hedges

In their June 28th report, Variant Perception flagged the rare and powerful autocorrelation buy signal, with a short squeeze target of 4,150 on the S&P 500. It is now in range, so investors should look to re-establish hedges / downside trades. Longer-term volatility remains elevated post-covid (see chart) and index skew remains expensive relative to single names. Put-spreads collars expiring in Dec 2022 look attractive. Buying a 95-90% OTM put-spread, funded by selling a 110% OTM call would be a great portfolio overlay for a small credit upfront.

Andrew Hunt Economics

US: Liquidity cools down

Andrew Hunt senses we are witnessing a turning point in liquidity data and that liquidity growth is cooling once again, particularly in real terms. Quantitative tightening is gaining momentum just as Treasury issuance is accelerating, which will test the bond markets over the next few weeks. Yet again, this week’s data confirmed that the US banking system is rapidly withdrawing from global credit markets, indicating the deflation that is occurring within the global dollar credit system. If this continues, Andrew expects the dollar to overshoot upwards over the coming months.

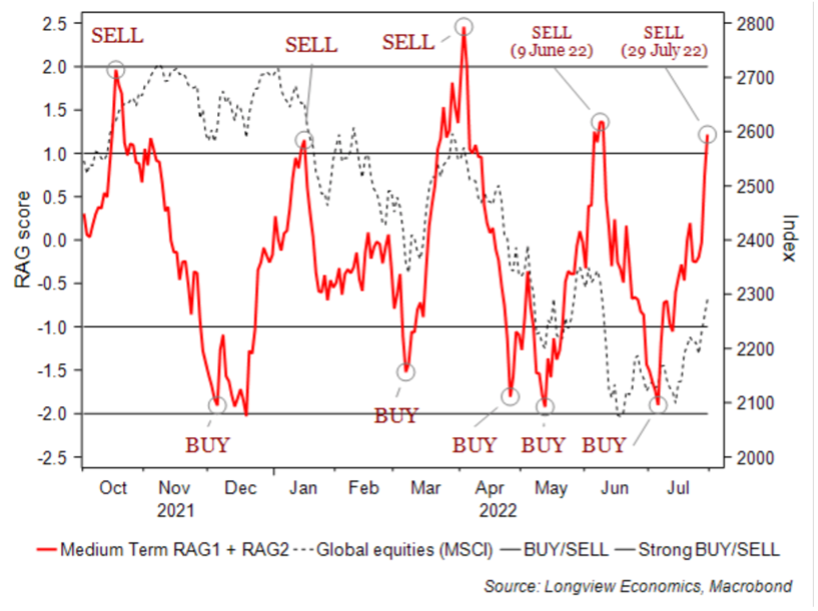

Longview Economics

US S&P 500 Index: Sell on strength

With further strength in US equities on Friday, most of Harry Colvin’s short-term market timing models are now on SELL. Harry claims the US equity market is overbought at an index, sector and single stock level. Increasingly, medium-term models are starting to mirror the message of the short-term models. Harry’s 1–2 week equity index trading recommendation is to SELL on strength: move ¼ SHORT at 4,190. Implement stop loss at 4,250.

Portales Partners

US: Fed attains optionality, what’s next for banks?

With the widely anticipated Fed rate hike of 75 basis points last week, interest rates are near ‘neutral’ at 2.25%-2.50%. The Fed seemed satisfied that it was fighting inflation and markets seemed to think that a ‘pivot’ was in place, but Charles Peabody prefers to describe the current status as one of ‘optionality’. The Fed will likely continue to hike rates, but at a slower pace. And this optionality has removed some ‘fear of the Fed’ which helped July turn into a great month for all stocks. They see a choppy month for August as banks enjoy positive PPNR and markets gnash about recession.

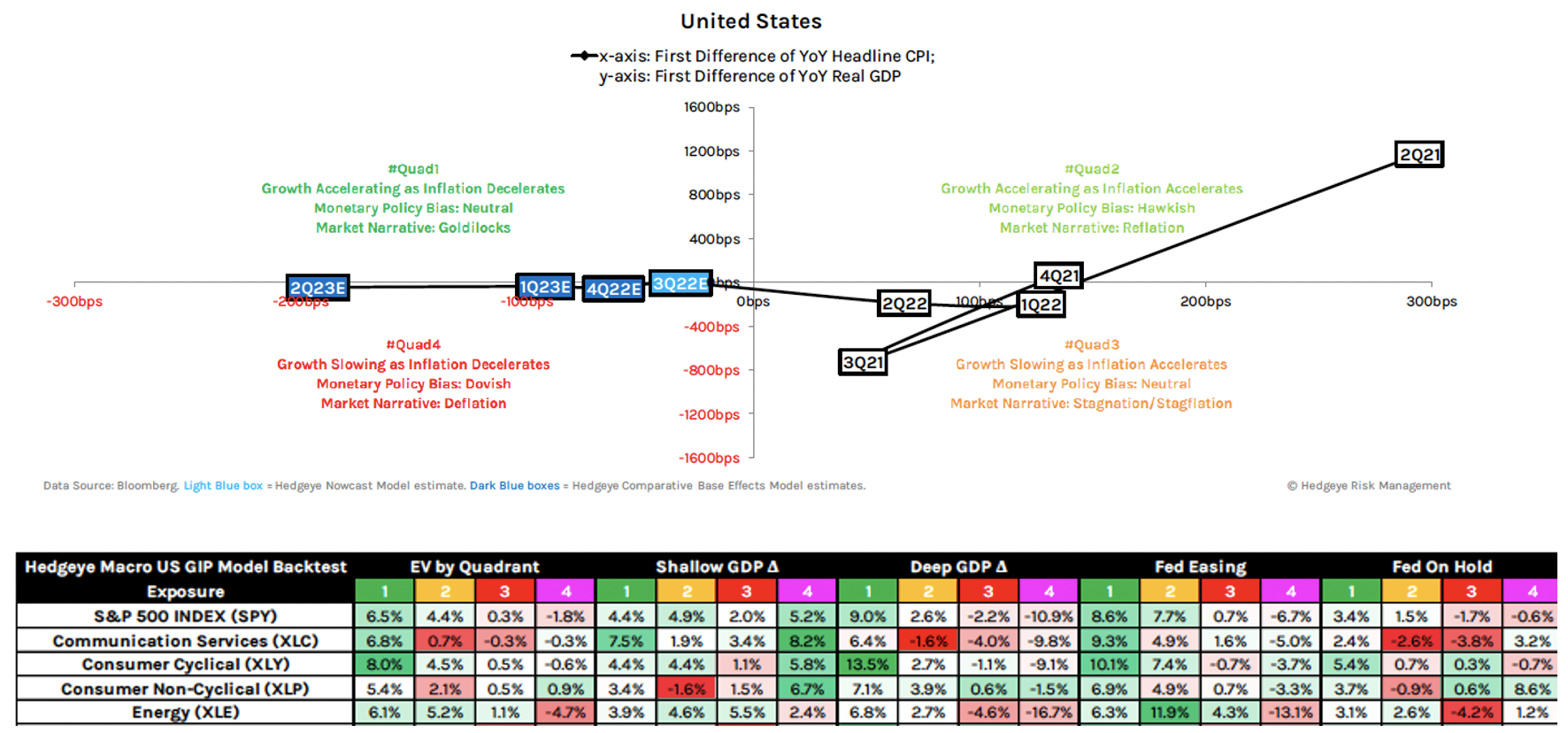

Hedgeye

Helping investors prepare with the Macro Quad Model

Hedgeye’s GIP model is a quantitatively oriented, regime-based framework that helps investors proactively prepare for volatility phase transitions within and across asset classes by triangulating the three factors that matter most to macro risk management: growth, inflation and policy. The model currently forecasts four quad 4’s in a row from Q3/2022 through to Q2/2023 (see graph). A snapshot of Hedgeye’s detailed quarterly expected values by GIP Model Quad Regime has been provided (see table above).

Minack Advisors

Australia: Further RBA tightening would increase recession risk

Australia has an inflation problem that requires some policy response, hence the RBA quickly lifting its cash rate target to 1.85%. However, Gerard Minack warns that further tightening would soon create real recession risks. The RBA is overestimating how high the neutral rate is, and (again) overestimating likely growth in wages. Rate markets are right to be lowering the expected peak for RBA policy. However, if the wider market is correct in forecasting a cash rate increase to 3.25%, then expect further cuts in 2023.

Emerging Markets

Totem Macro

Shorting the bubble

Whitney Baker believes that the immaculate disinflation priced into markets is wrong, and she sees a seismic realignment of market pricing in fairly short order, with a shift to high inflation and negative real rates at its epicentre. For now, Whitney remains hedged to outright equity downside since the bubble has much more unwinding to do. Shorts that are more precisely targeted for their liquidity-dependency will continue to fall outright, while oversold (inflation-beneficiary, cyclical value) longs rise. Whitney is kicking the tires on the best country-sector shorts within EM bubble epicentres, which she will be publishing in the coming weeks.

China Beige Book

China: Beware the July rebound narrative

China Beige Book’s latest data shows further deterioration this month, coincident with continued Covid outbreaks and lockdowns. Manufacturing and retail revenues decelerated while services saw no improvement. Factory output and new orders have slowed to a pace not seen since the height of the pandemic. Worse, hiring continues to evaporate and corporate credit has waned, with few exceptions. It’s another month on the wrong side of the ledger for Beijing. Hype aside, time is running out for a meaningful 2022 rebound.

Greenmantle

Chile’s catch-22 constitution

On September 4, Chileans will vote on a new constitution. Shoddily drafted and unabashedly progressive, it faces a long road to ratification and implementation. The new constitution is unlikely to transform Chile into Argentina or Venezuela, but the country’s politics will remain polarized—and markets will remain uneasy—regardless of the vote’s outcome. Meanwhile, Chile’s economic and fiscal challenges are increasingly dire. Chile is not positioned to thrive in a world of rising U.S. rates and flagging Chinese demand.

Teneo

Mexico: President Lopez Obrador’s stance on trade dispute signals turbulence ahead

President Lopez Obrador (AMLO) seems intent on exploiting a trade dispute between the US and Canada to stir up nationalist sentiment. With empty threats to leave the US-Mexico-Canada agreement, it is clear AMLO is looking to reap political dividends among an electorate that is always susceptible to nationalist rhetoric. The problem is that AMLO’s strategy is solidifying a toxic combination of policy radicalisation, regulatory uncertainty, domestic legal challenges – and now international trade litigation and the threat of trade tariffs – which will further stifle growth and keep investor wariness elevated.

Burumcekci Research & Consulting

Turkey: Slowing further

Exports data compiled by exporters’ unions suggests that in July, exports (excl. precious metals) reached $14.7bn with total exports possibly around $16.3bn at month’s end. This suggests that exports will drop significantly in July and will decline to the lowest rate of increased observed for a long time. In short, the first signals of the month suggest that the slowdown in economic activity may turn into a contraction in the third quarter.

Commodities

Global Mining Research

Iron ore: Falling prices pausing, or the cycle restarting?

Iron ore prices recently bounced off US$100/t, raising the question whether this represents a pause in the correction, or perhaps early signals that the price cycle is restarting. Sentiment continues to focus on broad demand risks especially in China, nevertheless Chinese crude steel production continues to annualise at +1Bt/yr, with the rest of the world’s demand recovering. David Radclyffe believes investors are getting close to an opportunity to start accumulating iron ore stocks; iron ore producers trade on a prospective 2023 FCF and dividend yield of 9% and 8% respectively. David’s preferred exposures are Vale, Fortescue Metals Group and Labrador Iron Ore.

Llewellyn Consulting

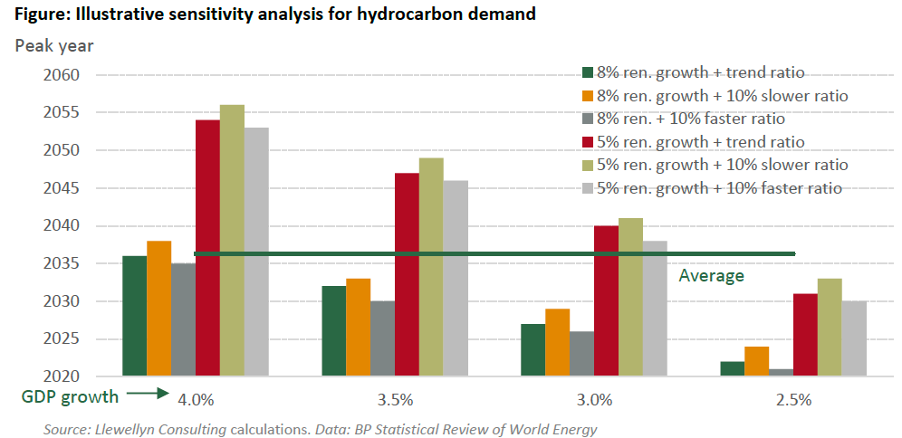

When will hydrocarbon demand peak?

John Llewellyn’s recent paper investigates the likely peak year for hydrocarbon demand, utilising a framework that takes into account GDP growth, the falling rate of energy intensity of GDP, the growth of renewables (at 5-8% a year) and other factors. Under current growth trends, hydrocarbon use will not turn down before 2032, and John fears it may in fact not be until 2047 before this happens. For us to see a peak sooner than later, policymakers need to get serious and abolish fuel subsidies, agree on a tough carbon price, and establish a fair revenue-sharing scheme with EMs.

CPM Group

The outlook for platinum

CPM Group’s industry-leading Platinum Group Metals Yearbook is now available, containing definitive and detailed statistics and analysis on the international PGM markets. These include the organisation of retail investors, the impact of Russia’s invasion of Ukraine, a reduction in liquidity and major market making capacity, and elevated investor demand for bullion and derivatives. Jeffrey Christian touches on these topics in his latest video.

Watch here.