Company & Sector Research

Europe

Iron Blue Financials

A score of 25/60 is top quartile for Iron Blue, which suggests fertile ground for shorting - accounting red flags include a high degree of discretion around revenue recognition, stripped out asset impairments (reducing future D&A expense), regular stripped out redundancies & other costs, new capitalisations of development expense exceeding amortisation by a material amount each year, reduced provisioning in 2021 for bad debtors, inventories and book returns and an unusually high gross cash balance. Regarding governance, Iron Blue notes that PSON is set to change auditor in 2022 after 25 years with PwC.

Paragon Intel

Former colleagues interviewed by Paragon unanimously believe new CEO Amedeo Felisa is a good fit for AML who can lay the foundation for a rebound in its profits and reputation - Felisa was “one of the most important men” in creating Ferrari’s success, developing high-performance cars while generating industry leading margins. He is described as a “tough, honest and demanding leader”, who is “fanatical” about quality. Felisa cares little for corporate hierarchy but readily defers to others on issues outside of his expertise. He “always achieves” financial targets.

Holland Advisors

Thriving in the chaos - many analysts appear anchored to a profit recovery potential of c.€10 net profit per passenger. However, Andrew Hollingworth thinks €15 NPPP is a very achievable target. He also expects c.25% EBIT margins. At 225m passengers (RYA’s 2026 target), €15 NPPP gives net income of €3.4bn. For a little perspective RYA’s almost debt free M/Cap is only €13bn. Some will argue that c.20% ROE’s is impossible - it is. The magic comes from negative working op that is c.30% of sales. Customers and suppliers fund much of RYA’s growth so shareholders don’t have to!

Green Street Advisors

Residential Sector: Trouble brewing or storm in a teacup?

The sector’s cash flow stability is highly regarded by investors. However, listed companies have stretched their balance sheets as interest rates have fallen. TAG Immobilien, a ~€6bn German landlord, is the first victim of changing macro paradigm. A €200m equity rights issue (~20% share count expansion) is >10% dilutive to spot NAV. Other companies on Green Street’s watch list include Vonovia and Nordic PropCos. Tough decisions lie ahead. Cost of capital signal warrants disposing assets, paying down debt and taking other cash preservation measures otherwise equity raises could be required.

Willis Welby

Screening UK & Europe: Combining quality, momentum and expectations indicators

Methodology - the initial universes are stocks with $2bn+ M/Cap in the UK and $5.5bn+ across Europe. After that Willis Welby starts with a quality cut off based on their measure of Intrinsic Return on Capital Employed. They then narrow down using a combination of share price momentum and EBIT revisions before incorporating their expectations analysis via their measure of the implied to Y3 EBITM ratio. This month sees 6 stocks enter the UK screen (including Rio Tinto, Flutter, Renishaw) and 17 names added to the European version (including Nestle, Hapag-Lloyd, Roche, Vestas, Aker).

North America

Kailash Capital Research

Mean reversion, market prices & common sense

Simple arithmetic tells us 25% annual returns are not sustainable and highly susceptible to mean reversion - the long-run annual return to the US stock market from 1871-2022 is 9.1%. From 2009-2021, the market returned 16.0% p.a. and for the five years from 2017-2021, the market averaged 18.4% p.a. For today’s market to simply fall in line with history’s expected rate of return would require another 40% sell-off in equities. Over the long term, the data is clear: value investing is one of the most effective reversion strategies available and KCR’s top ranked stocks offer significant advantages when compared to the fundamentals of both the Russell 1000 Value and Growth Indices.

New Constructs

Short model portfolio outperforms by 31%

26 out of New Constructs’ 32 ideas outperformed in 1H22 with an average return of -50% compared to a 19% decline for the S&P 500. Underscoring just how important reliable fundamental research is in turbulent markets, their model portfolio has beaten the S&P by an even wider margin (48%) since the start of 2021. Top performers have been Coinbase, Carvana, Peloton, Snap, Beyond Meat and Lyft. As we enter 2H22 high conviction shorts include Netflix, Uber, Shopify and Robinhood.

MDC Financial Research

MDC's “Event-Driven Legal℠" service is following Twitter litigation against Elon Musk in the Delaware Court of Chancery - on July 19th, the Chancellor Granted Twitter's Motion to Expedite. A five-day Trial will be scheduled for October 2022. The Chancellor mentioned that she does not think that Damages would be an appropriate remedy in this case. So, it seems that either there will be "Specific Performance" or not. MDC currently believes that a deal will eventually be done at a higher price than current, but likely from a Settlement. MDC speculates that Twitter has misrepresented its "mDAU" metric.

JJK Research Associates

AE brand continues to see higher promotional activity with full price and clearance assortments now offered at 25% off - while slowing consumer spending patterns are likely the primary reason fuelling deeper discounts, JJK are also disappointed in the BTS assortment’s innovation level across both men’s and women's ranges. At Aerie, a key concern is that inventory levels are tracking well above last year, while demand levels moderate. JJK expects discounts to deepen as 3Q unfolds, putting further pressure on the P&L. They cut their FY22 EPS forecast to $1.10 and see no improvement to top line / margin gains until 2H23.

Entext

Growing China autonomous exposure - specialises in lidar technology used in self-driving vehicles and is one fallen SPAC that Sean Maher believes has a good chance of retesting prior highs over the next couple of years given its strong niche position in a secular growth market. Alongside LAZR, Sean has been keen to add auto exposed semi / sensor names like NXP and On Semiconductor into current weakness because the consensus is underestimating just how much incremental hardware will be embedded in the average vehicle by 2025 onwards.

Portales Partners

2Q22 results mask $1bn in additional earnings power as fortress balance sheet is strengthened - JPM reported $2.76 EPS but core earnings power was closer to Charles Peabody’s $3.00 estimate after backing out marks and other adjustments. While the market was disappointed by the suspension of stock buybacks, Charles’ analysis suggests JPM can raise the dividend and resume buybacks very soon while still building CET1 to 13% levels by 1Q23. The stock is very attractive at current levels.

Costigan Reports

Adapting to raw materials inflation, supply chain constraints and Covid disruptions - Bob Costigan explains why these global headwinds are, in fact, a net gain for KAI and why the company will continue to surpass street estimates. Improving fundamentals should lead to significant returns for shareholders over the next one to three years through a combination of earnings growth and price multiple expansions. Bob estimates adjusted EPS of $9.25 in 2022, $11.00 in 2023 and $12.65 in 2024. 1-Yr TP $250 (30% upside) and 3-Yr TP $350 (80% upside).

Gradient Analytics

The can-maker’s equity is expected to come under further pressure - the main concerns cited in Gradient’s 13-page report include: 1) Volume and profitability headwinds. 2) Inventory growth higher than targeted and has outpaced forward sales estimates. 3) Growth in receivables suggests a pull-forward of revenue. 4) Accrued compensation fell to a five-year low relative to adjusted operating expenses. 5) Despite the recent share-price correction, BALL still appears expensive. Other active shorts Gradient have initiated coverage on this year include ADT, Cerence, Lamb Weston, Owen’s & Minor and RingCentral.

Singular Research

Updated PFS for SA’s 100% owned KSM project (British Columbia, Canada) shows a considerably more sustainable and profitable mining operation than its 2016 predecessor - SA currently trades at an EV/ounce of only around 20x. However, recent developments in both operations and the potential for higher gold prices warrant it trading up at and EV/ounce of 30x in the intermediate term, which represents a share price of $30.00 (140% upside), and a higher valuation once a JV partner is signed.

Inflection Point Research, LLC

In-house modem development is tougher than it looks

The blogosphere continues to buzz that Apple's in-house modem will not ship in 2023 and the iPhone 15 will ship with 100% Qualcomm silicon - while Michael Fox does not believe AAPL has “failed”, it is proving to be more difficult than Johny Srouji and his team anticipated. AAPL highly unlikely to risk all-important iPhone franchise on first-generation internal silicon; will begin the switch with iPads / Macbooks which have simpler use models. As with AAPL, Samsung continues to struggle with its LSI modem. Despite years of experience with developing / shipping in-house modems, design flaws could push the company to ship all 2023 Galaxy S models with QCOM modems.

Blueshift Research

Giant layoffs loom as Tech firms face customer budget freezes

Blueshift’s IT sector sources are pointing at Oracle’s plan to cut c.30k jobs as the crack in the dam that is going to trigger a resizing of workforces across all of tech - as one recruitment executive said, “They have literally been making up jobs for the past several years to beat each other to talent. It had nothing to do with rightsizing. It was a competition to impress investors.” Sources were unanimous that earnings forecasts for the rest of the year across most vendors in all verticals of DIY enterprise networking are going to be poor. Companies covered include Arista Networks, Cisco, CrowdStrike, Dell, Fortinet, IBM, Palo Alto and Zscaler.

Emerging Markets

RedTech Advisors

Douyin eCommerce: From strength to strength

Against a background of widespread pessimism about the macro-environment for 2022/23, merchants in RedTech’s 2Q22 eCommerce survey highlighted Douyin, and to a lesser extent Pinduoduo and JD.com as winners, while Alibaba underperformed. Merchants liked Douyin’s eye-catching content, which delivers excellent performance on ad KPIs, resulting in rising sales and an even greater chunk of merchants’ ad spending. They also noted Douyin’s strong potential for sales in lower tier cities. Alibaba on the other hand has hit its peak, user growth is stalling, costs for merchants on the platform are high, and competitors in both the high and low end loom large.

Galliano's Financials Research

Another blow for SoftBank as its fintech holding eToro has its IPO plans de-railed and now its latest funding efforts point to a "down round" - the now defunct SPAC deal had implied eToro was worth in excess of USD10bn. However, its latest funding round suggests a valuation range of only USD5-6bn, and Victor Galliano argues that even at this lower valuation eToro is too expensive, pointing to the fact that its valuation to assets under administration is at a massive premium to all listed peers.

Aequitas Research

Korean IPO aiming to raise ~US$690m - WCP is a leading maker of separators which are key materials used in EV batteries. While sales growth has been spectacular, its top three customers accounted for 89% of revenue in 1Q22, and only one of them has shown consistent growth. Prices have also been on a downward trend and this is expected to continue despite the market moving into a supply deficit by 2024. OCF has mostly been negative and debt has been increasing. Additional concerns relate to WCP’s parent company (Japan listed W-Scope) who has faced going concern issues and is currently involved in a patent litigation for some of its products.

Off Wall Street

Long-term peril? The foundation of its semiconductor advantage appears to be crumbling. TSMC’s current position was enabled by three key factors: globalisation, China’s participation in the US-led international order and Taiwan’s innovation edge. TSMC’s technological edge could preserve its position for the next couple of years, but bullish expectations of annual long-term revenue growth in excess of 15% appear foolhardy. While nationalism may be more pronounced in the case of semiconductors, OWS sees this concept of deglobalisation leading to higher inventories and concomitant margin pressures in other industries as well.

Copley Fund Research

Positioning insights among active EM managers

Key takeaways from Steven Holden’s latest report: 1) Tech to Financials rotation - Financials becomes largest sector allocation for 1st time since early 2020. 2) Longer-term drop in Discretionary allocations offset by renewed sentiment in Consumer Staples. 3) Communication Services weights at their lowest ever levels. 4) Active EM managers warming to the Real Estate sector (led by China & HK, UAE). 5) Consumer Staples and Information Technology remain key overweights. 6) Materials, Energy and Utilities among key underweights.

Macro Research

Developed Markets

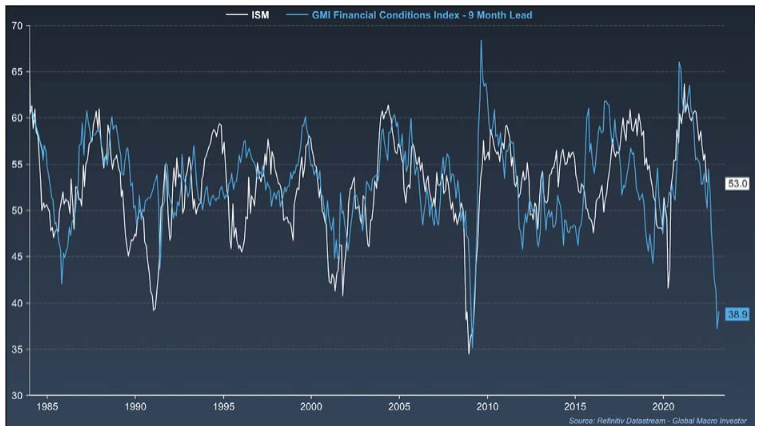

Global Macro Investor

Playing the oncoming recession

The chances of not seeing a recession are off the table, and Raoul Pal remarks that we are experiencing the worst sentiment he has ever seen in financial markets. All of the charts are bleak, and his combined rates, USD, and commodities chart (see below) indicates GDP growth at -4.5% QoQ annualised in nine-months’ time! The markets haven’t yet priced all of this in, with bonds being the most mispriced asset of all. Raoul predicts rates at 1% or less by March 2023, and is max LONG fixed income. BUY March 2023 Eurodollar 99/99.25 Call Spread for 1 tick, US 5yr bond futures and June 2023 Eurodollar futures.

AAS Economics

UK: A very toxic combination

Frank Shostak comments that the UK experienced dramatic policy-induced fluctuations in money supply (AMS) growth as a response to lockdowns. The impacts of these fluctuations are always felt with a lag, and we are currently seeing the contractionary effects of the recent decline in AMS growth coincide with the inflationary effects of the earlier increase in AMS growth. Towards the end of this year, these output and inflation growth trends should move back into alignment, but in a downwards direction. Expect the property market to come under pressure. Frank’s asset allocation remains quite defensive.

Eurointelligence

We need to talk about Italian debt

Wolfgang Münchau stresses that it is not hyperbole to state that the Eurozone would simply not survive an Italian debt default. With Draghi having now resigned and Meloni the likely next Prime Minister, the conversations around restructuring Italy’s debt must continue. Wolfgang's latest article compares the available options, including the ideal Depla/Weizsäcker blue bond/rend bond proposal that would involve creating a Eurobond out of the portion of debt up until 60% of GDP, as well as other less effective ways. The fiscal union isn’t some idealist, first-best construction; it is necessary for stability.

CrossBorder Capital

ECB and Bank of Japan add to QT

Michael Howell reveals that major Central Banks’ balance sheet data shows aggregate liquidity shrinking at an increasing pace (-13.7% 3m ann. in local currency terms). ECB liquidity is shrinking at the fastest rate in three years (-9.9% 3m ann.) and reflects the end of net asset purchases from the start of July. The sharp downturn in the BoJ data (-1.8% vs. previous +21.7%) is puzzling, given the BoJ’s repeated commitment to a loose policy stance. Whether it turns out to be a temporary blip to iron out the previous spike, or the start of liquidity tightening, remains to be seen.

Ironsides Macroeconomics

US: FOMC stress test

Barry Knapp’s latest podcast focuses on rebalancing, second order dollar effects, curve inversion, monetary policy and banks. He discusses his belief that equities are bottoming and, while the term premium on longer term Treasuries is too low, the worst of the rate shock and liquidity tightening is behind us. Barry also remarks on a possible systemic crisis with exchange rates likely to be where a crisis originates; and the S&P500 Bank Index trading far lower than return on sector equity would suggest (1.6x book value compared to current level of 1.07).

Listen here.

Intertemporal Economics

US labour market: Neutral is negative

The seeming contradiction between a strong labour market, high inflation, and weak sentiment is easily explained by a potential growth rate below zero and continuing stimulative monetary policy. Since actual output > potential output, any growth will be highly inflationary. Only a reduction of demand below potential will cool output, but the current situation differs from so-called “soft landings” where the growth rate has exceeded the potential rate and the economy can rebalance without shrinking just by slowing down. A neutral stance to monetary policy would result in recession. Given the FOMC’s move towards a restrictive stance in the immediate future, the economy is in for a bumpy ride as the Fed triggers a worse recession than it expects.

Andrew Hunt Economics

New Zealand: A gloomy future

With a model reliant on rising house prices and elevated debt ratios in both the household and company sector, Andrew Hunt fears that an unfortunate combination of changing global credit conditions, domestic quantitative tightening, and a weak external balance will combine to create a significant damaging credit crunch in New Zealand over the next 18 months. In the face of the crunch, expect the central bank to halt its rate hike programme – potentially at only a 3%-3.25% cash rate. Andrew is structurally bearish of the New Zealand Dollar.

WallStreetCourier

The CBOE put-call ratio: A useful greed & fear contrarian indicator?

WallStreetCourier’s latest white paper analyses the effectiveness of the put-call ratio as a contrarian indicator to exploit extreme levels of greed and fear within the option market. The paper derives precise thresholds to identify appropriate entry- and exit points and analyses them based on their average forward-looking returns on the S&P 500. The paper also discusses a new way on how to improve trading results by applying the z-score statistics to the put-call ratios. They find that the put-call ratio can indeed be very useful in identifying attractive trade opportunities.

Creative Portfolios

Strategies for equity markets in times of inflation and stagflation

Creative Portfolios’ latest think piece discusses decision-making in markets burdened by stagflation. Equities aren’t a suitable choice as an inflation hedge in time of stagflation. Rather, the best strategy to limit pain is to use more momentum rather than value, low-risk, or quality. This means taking active long/short bets rather than buy and hold. Diversifying factor premiums can help too as part of a momentum strategy.

Emerging Markets

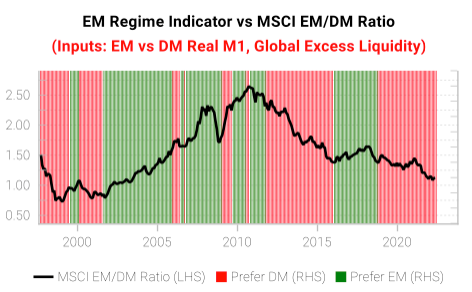

Variant Perception

Don’t bet on EM outperformance yet

Jonathan Tepper acknowledges the structural bullish case for EM equities based on extreme investor outflows and low valuations, but he claims the cyclical 6-month environment is still too weak to warrant EM overweights (see chart). It is true that EM liquidity conditions are improving and China will drive EM real M1 growth higher in coming months, but it’s not enough to go bullish. However, EM debt will present opportunities as the market narrative moves away from the inflation scare towards the growth scare.

HCWE & Co.

Emerging Market Selector

HCWE’s Emerging Market Selector summarises the outlook for emerging markets on a country specific basis, using “market signals” of world economic growth, inflation, relative valuation, and currency “surprise”. It incorporates the results of new research on the combined forecasting power of corporate quality spreads and gold prices. The emerging markets that are most strongly in favour this month are Chile, Hungary, Pakistan, Sri Lanka and Turkey. Those most out of favour include China, Peru and Thailand.

PRC Macro

China: Potential outcomes of the Politburo meeting

Don’t expect a big stimulus push in the short-term. William Hess believes a message will be sent out that stimulus will come if and when necessary, wholly contingent upon downside outcomes for growth in Q3. Energy security will also be a pressing topic, with Beijing potentially diving back into global thermal coal and energy markets to help offset a winter energy shortage. Investors should also listen out for the Politburo hinting at the importance of maintaining a stable RMB exchange rate, which he explains could create a great arbitrage opportunity to be LONG the RMB against a basket and SHORT the RMB against the USD.

Alberdi Partners

Chile: Peso’s weakness is here to stay

The Central Bank of Chile (BCCh) announced its sixth FX intervention program since the CLP started floating in 1999, the decision matching the bank’s pre-determined intervention criteria. Although the FX intervention was successful initially, Marcos Buscaglia thinks the peso’s weakness is here to stay. Weaker commodities, high political uncertainty and too much external leverage for such low reserves all point to CLP weakening in real terms this year, coming in at under 900 per USD.

Andrew Hunt Economics

Indonesia: Lacklustre growth

Andrew Hunt doubts that Indonesia’s economy is growing as rapidly as the official data suggests. It possesses a high level of foreign debt which Andrew suspects it is finding difficult to rollover as the global supply of dollars dries up. With its legacy problems, expect to see further downward pressure on the foreign reserves and the IDR. Given the softness in the domestic economy, the central bank will likely match the Fed instead of enacting aggressive rate hikes, providing that the decline in the rupiah does not become disorderly.

Greenmantle

Mexico muddles through

President López Obrador is constitutionally barred from seeking re-election, and internal jockeying to succeed him risks widening fissures within his amorphous Morena coalition. With presidential attention increasingly monopolized by party business, shoring up the voter base with public events, and micromanaging his pet infrastructure projects, Niall Ferguson does not expect any more market-rattling attempts at structural reform this year. Given Mexico’s relatively robust fiscal situation, and Banxico’s current place in the hiking cycle, Niall considers it well positioned to outperform EM peers against a backdrop of rising U.S. rates.

Commodities

Totem Macro

Liquidation: Oil & Pemex

Don’t confuse risk liquidation on the back of tighter financial conditions with economic deflation, warns Whitney Baker. In her latest report, Whitney shows that the oil move is financial in nature, while spot markets and cracks remain tight. The de-risking of assets and the dollar move has hit oil-related dollar credits globally, but none more so than Pemex. The fixed income blowout, particularly in a quasi-EM dollar credit where support is all but assured, has once again opened up an asymmetric trade opportunity. Whitney goes LONG Pemex 2027s.

Global Mining Research

Diversified miners becoming less diversified

The three leading diversifieds have worked hard in un-diversifying themselves in recent years, becoming more and more iron ore focused, with fewer points of differentiation. David Radclyffe finds that nearly all investment ratios favour Vale (FCF yield 15%, EV/EBITDA 2.6x), then Rio Tinto and finally BHP Billiton. For as long as iron ore can hold around US$100/t, expect average cash return yields of 8-12% in 2022E. BUY Vale with a target price of $15.40.

HED Capital Management

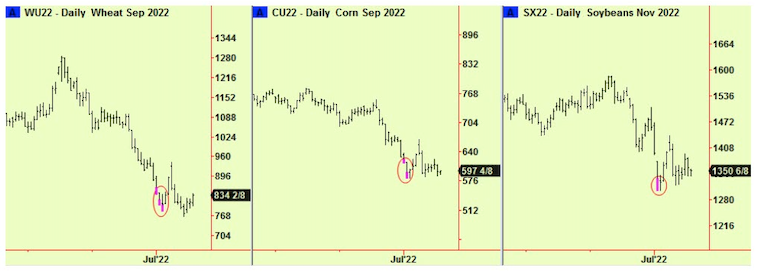

Grains and gains

Richard Edwards recently reported that there had been bottom extensions across the board, which had led to rallies. Richard advised buying dips, and comments that these signals are still in date. BUY the dips, you shouldn’t have to risk much.