Company & Sector Research

Europe

Arete Research

Squeezing the juice - consensus is not pricing in peak capex. Market scepticism over weak dividend cover should dissipate as FCF doubles by ’24E, with further potential upside from Masmovil JV. The possibility of Totem merging with Vantage Towers is ORA’s €9bn hidden gem, which further fuels the positive train. Meanwhile, the French outlook remains bullish and should the possibility of consolidation become a reality, this will also play in ORA’s favour. TP increased to €16 with a 57% TSR by YE23E (excluding potential for special dividends).

Propitious Research

The long-term open-ended share repurchase programme, funded by PRX’s on-market sale of its Tencent shares, is a massive positive catalyst for reducing the discount to NAV from its trough of ~60%. However, given the estimated short- to medium-term drag on cash flow from consolidated operations, Wium Malan concludes that it is difficult to argue for much less than a 30% discount. He also thinks it is likely that PRX’s management will significantly scale back its buyback programme should the discount approach the 20% level.

Woozle Research

Store managers report +10.5% LFL sales growth in May and June - 81% of those interviewed have a bullish outlook for the next 6 months. Demand has remained strong despite inflationary pressures, bolstered by the introduction of new menu items such as the ‘Summer Salads’ and new sandwich ranges. Several managers noted the increasing popularity of the Greggs Rewards app, which they expect to drive footfall higher y/y. On the negative side, 48% of those interviewed noted that they are experiencing some supply chain issues - something Woozle will continue to monitor over the coming months.

Smart Insider

Paul Bulcke (Vice Chair since 2017) purchases €606k of stock at €303. He is on the board as a representative of Nestle (where he is Chair). It's interesting to note that Nestle reduced their ownership in L'Oreal from 23.3% to 20.1% in Dec 21 (at €400) and to see Bulke now make his first ever direct purchase in the stock. Béatrice Guillaume-Grabisch (Non Exec since 2016) also recently purchased €133k of stock. This is only her second purchase and it's notable to see her now buying at nearly twice the price after a 5 year gap.

the IDEA!

Amazon’s insourcing of (part of) the last mile delivery is already having a negative impact on bpost’s parcels volume (-17% in 1Q22). However, the main threat of a local AMZN website will come from AMZN targeting small and mid-sized web shops to use its platform and its FBA services. By doing so, it would directly compete against bpost which is trying to compensate for the loss of its AMZN volume share by chasing new clients in this segment. Now is not the time for investors to go bottom fishing.

TobaccoIntelligence

EU Commission confirms flavour ban for HnB products

A flavour ban for heated tobacco products, which have developed sufficiently in the EU to now play an impactful role, was confirmed following the EU Commission’s publishing of a delegated directive amending the Tobacco Products Directive 2014/40/EU (TPD). Publication in the Official Journal of the European Union is likely to occur within two months of the adoption date (29th June 2022) unless the Council and the European Parliament decide to end the scrutiny period.

North America

Two Rivers Analytics

Companies with dangerous inventory levels

"FISH" - First In, Still Here. Two Rivers deconstruct their Earnings Quality model to focus solely on one aspect of poor earnings quality: significant inventory slowdowns. This looks at 1) The materiality of inventory levels to the business. 2) The trend in turnover. 3) The magnitude of the slowdown. As the odds of recession rise, companies caught with excess inventory will find themselves forced to offer price concessions, leading to sales and margin declines, and to earnings disappointments. Highlighted names include Alcoa, Amazon, Arista Networks, Beacon Roofing, Beyond Meat, First Solar, LGI Homes and Walmart.

Thompson Research Group

2Q22 Heavy Materials survey

TRG’s survey focuses on aggregate, concrete, asphalt and cement volume and pricing trends throughout the quarter. During this survey season, they have been particularly focused on the relative changes in momentum, especially for the residential end market. Pricing is going through while volumes and margins are a mixed bag. TRG’s 25-page report also includes earnings previews and estimate changes for Arcosa, Atlas Technical Consultants, Eagle Materials, Martin Marietta Materials, Summit Materials and Vulcan Materials.

Badger Consultants

Another profitless prosperity stock - Tom Chanos sees no way to scale the business. FRPT has been unprofitable for 10 straight years, 2022 will make it 11. Margins are collapsing even with price hikes; burns cash like crazy (latest offering only buys them c.9 months); and much bigger competitors, no barriers to entry. Selling expensive pet food in a recession is a bad place to be. TP $25 (50% downside). Other short ideas initiated by Tom over the last year include Peloton, Carvana and Coinbase.

Renaissance Macro Research

With rising NII and continued expense discipline, Howard Mason expects BAC to reach its target for a 60% efficiency ratio by the end of 2023 - this will support a return (on tangible common equity) of 16-17% consistent with a valuation multiple of 1.8x that, applied to Howard’s estimate for tangible book value of $23/share by end-2023, supports a TP of $42 (30% upside). In the meantime, even as BAC raises its dividend and looks to delever (increasing the CET1 ratio to 10.75%), there remains significant capacity for buybacks (expects $8bn over the next twelve months representing ~3% of current M/Cap).

Alembic Global Advisors

Pete Skibitski upgrades the stock to Buy post 4Q22 - a big part of his improved outlook for AVAV relates to expectations for higher defence spending in Europe, along with the need to replace TMS-related stock in the US (much of which has been supplied to Ukraine). The firm has now garnered US export approval of its Switchblade 300, and the larger 600, to more than 20 countries, from just 1 recently. Supply chain and labour challenges remain, but Pete expects these to alleviate as we get deeper into FY23.

Veritas Investment Research

Defence wins championships - gold's precedent of outperforming amidst real GDP loss and high inflation offers a defensive diversification opportunity for Veritas’ V-list model portfolio (1-yr +8.95% vs. S&P/TSX Composite -3.87%). The new ABX combines low-cost assets with a proven CEO that will not destroy value in expensive acquisitions. ABX is trading at low P/E and EV/EBITDA multiples compared to Newmont and Agnico Eagle despite higher profitability per ounce of gold produced, a higher dividend pay-out and an attractive buyback programme in place. TP C$32 (40% upside).

BWS Financial

Recurring income stream - investors associate HHC to residential real estate since it has relied upon selling land to home builders to grow its master planned communities (MPCs). However, Hamed Khorsand believes the MPCs are now at a stage where not much, if at all, any new homes are required to support recurring cash flow. Investors should take advantage of the recent dislocation in the stock price from the fundamentals in the business. TP $150 (100%+ upside).

Abacus Research

This defensive compounder offers compelling risk reward - trades at 11x EPS yet has grown EPS at a 25% CAGR for the last decade. With highly predictable earnings, SSNC is relatively well positioned into an economic downturn. Investors shouldn't focus on organic growth, earnings is driven by acquisitions and now is an opportune time with more targets available and at better prices than they have been for ages. TP $85, offers 50% upside, while Abacus Research's bearish scenario sees downside risk of only 12%.

Japan

New Street Research

It is now clear that NTT and KDDI have entered a phase of faster growth, which New Street calls "The Golden Age". They expect SoftBank to enter it in 1-2 years. Stocks are not priced for this, nor for the likelihood that Rakuten scales back or exits its MNO business. New Street increases their TP to ¥5,250 for NTT (35% upside) and to ¥6,000 for KDDI (40% upside). For Rakuten, they remain bearish and cut their TP to ¥520 (20% downside).

Asymmetric Advisors

Contrarian Buy opportunity - currently has ZERO analyst BUYs. This air conditioner company will benefit from the recent drop in copper (its most important input cost) which hammered earnings last year. While Fujitsu General and the popular Daikin will both benefit from rising global temperatures, an extremely hot Japanese summer benefits Fujitsu General to a greater extent given its higher domestic exposure. It is also likely to see a surge in heat pump sales in Europe ahead of winter given fears for Russia gas supply. Lastly, 42% holder Fujitsu will sell its stake, potentially sparking a bidding war.

Emerging Markets

LightStream Research

Short attack by Grizzly Research - accuses NIO of likely using an unconsolidated related party to exaggerate revenue and profitability. Claims Wuhan Weineng helped NIO inflate revenue and net income by approx. 10% and 95% respectively in 9M2021, and FY2021 earnings beat by at least 60%. In this insight, LightStream's Shifara Samsudeen assesses the merits of the claims by Grizzly and finds most of the allegations difficult to refute. It appears that the main purpose of establishing a separate entity to carry out the BaaS operation was to keep the company’s large battery inventory off balance sheet as well as to inflate its earnings.

Silk Road Research

China: The SRR Auto Discount Sequential Change Index rose by +22 bps m/m in June

This marked the seventh consecutive month of sequentially higher discounts and the second highest in 13 months. Domestic brand discounts increased for the first time in nine months, likely due to increased dealer efforts to boost sales for 1H22 as Covid restrictions eased. This is also consistent with SRR’s latest dealer checks that indicated OEMs were offering discounts alongside the auto purchase tax cuts announced in May. WM Motor, BMW and Nissan discounts rose most; Chery, Great Wall and BYD discounts moderated most.

Periscope Analytics

Double index inclusion and huge passive inflows - after being deleted from major global indices last year due to prolonged suspension, Brian Freitas expects GCL will be added to the MSCI China Index and the FTSE All-World Index over the next few months. This will require passive trackers to buy over US$1.1bn of GCL stock. Even after the recent rally, GCL trades cheaper than its peers on EV/EBITDA, forward PE and price to book.

Tabbush Report

Taiwan Banks

Daniel Tabbush is concerned there could be a negative surprise from unseasoned loans turning bad - the rate of credit growth in the most recent period through April 2022 is higher than the peak pace of growth in 2011 and 2005. To give some perspective, this is not the case for US banks or Australian banks, and it is very unusual for a country that tends to see pedestrian growth. The CBC will be acutely aware of banks’ lending binge in recent years and its hesitation on raising rates more aggressively may have been coloured by its concerns for rising delinquencies / credit costs.

Macro Research

Developed Markets

High Frequency Economics

Global economic downturn

Carl Weinberg is predicting economic recessions starting right now in the Euroland, Britain, Japan and across the globe. These will push prices down, reversing current inflation expectations by the end of the year. As expectations for central banks wilt, yield curves will flatten and possibly even invert if the central banks are inertial in changing their footings away from tightening. For all the talk about tightening monetary conditions, this incipient economic contract will halt any tightening long before interest rates predicted by financial markets today are achieved.

Aitken Advisors

A rough period ahead for financial markets

James Aitken ponders over the recent rapid repricing in rates markets (OIS). As much as growth concerns abound, James wonders whether the rapid repricing is less a reflection on growth risks than it is about growing risks to the market structure itself. At long last, people are starting to notice things like DPSI1CE LX Equity, that AAA-CLO tranches are more difficult to place, new issuance is declining, credit index bid-offer spreads are widening, and secondary market liquidity is as bad as it has been in a long time. He also comments on CET1 requirements in light of the Fed’s latest bank stress tests and advises clients looking to ensure that their CET1 requirements are floored at a suitably high level to shed RWA.

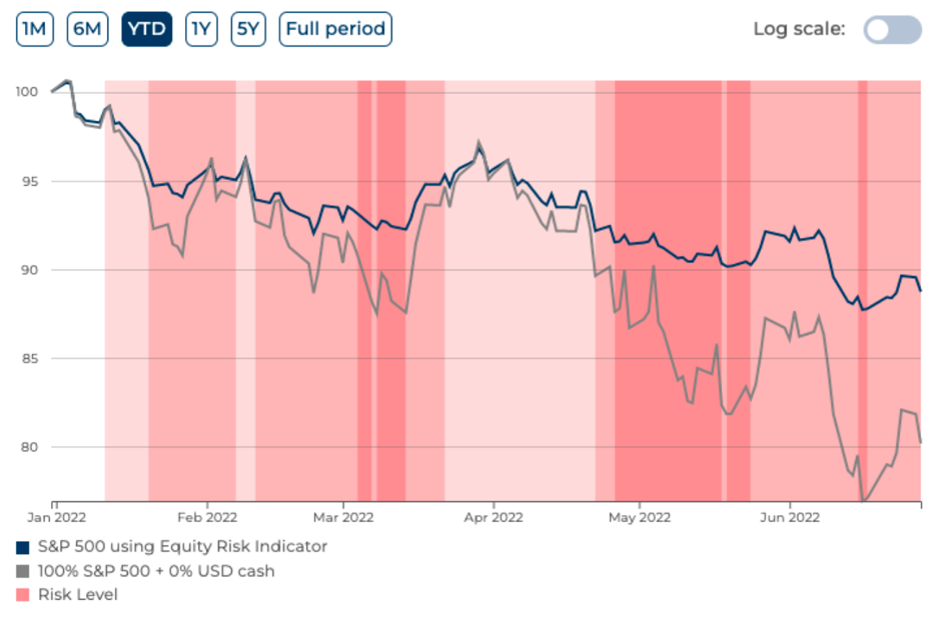

Alquant

How to outperform the S&P 500 by almost 10%

Prisma, a new platform developed by Alquant, provides a way to adjust equity exposure based on data-driven risk indicators rather than emotion. Year-to-date, the Equity Risk Indicator (ERIC), which combines all of Alquant’s indicators, would have outperformed the S&P500 by almost 10% (see graph) ERIC is accessible with a free account which can later be upgraded, please contact us to find out more.

Ollari Consulting

European chaos

EURUSD is printing 20 years low this week (see graph 1). Christophe Ollari comments on the broad-based weakness (see graph 2), brought on by a staggering number of variables ranging from the energy crisis and the Ukraine conflict to Germany’s trade deficit and the central bank’s actions. In the front of the current macro outlook, is the acceleration of the weakening of the common currency really that surprising? Although some remain positive, Christophe remains puzzled by anyone who would buy the Euro or be long European stocks.

Andrew Hunt Economics

Hong Kong: A perfect storm

Andrew Hunt foresees the HKD’s currency link to the USD facing a perfect storm more serious than that which afflicted the SAR during 1997. He explains how the SAR’s capital account has moved into a very significant deficit as international and domestic factors have collided. Markets have yet to discount the fact that the current bout of deflationary pressure within Hong Kong’s assets markets could quickly spread to the HKD itself. Expect the PBoC to intervene after concerted pressure on the HKD.

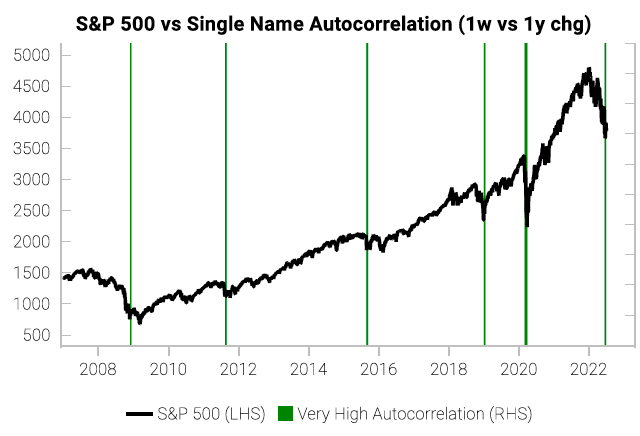

Variant Perception

US: Bear market squeeze vs medium-term cyclical caution

Consensus S&P 500 earnings imply an 18% YoY EPS growth rate for the next 12 months and a 9% YoY EPS growth rate in 2023. In contrast, Variant Perception’s Business Cycle Indicator is pointing to negative EPS growth. Their autocorrelation signals (see chart) have triggered for US and European equities, a powerful indicator of a short squeeze and a good contrarian tactical buy signal historically. Interestingly, in their market bottom checklist, only market and sentiment conditions show capitulation whilst economic indicators resemble market tops.

DeSaque Macro Research

US: Summer tug of war between inflation and growth fears

The Fed will remain steadfast in requiring evidence of a return to price stability before any reduction in the federal funds rate is contemplated. Yet, markets are incorrectly believing that the Fed will pivot towards rate cuts once there is unambiguous evidence of significant economic deceleration. It will take at least three months for the Fed to feel confident that price stability has been successfully reached, so don’t expect a shift from hawkish behaviour any soon. With a hawkish bias being retained, expect the 30-year fixed US mortgage rate to breach 6% and a cooling of the housing sector.

Emerging Markets

Horizon Insights

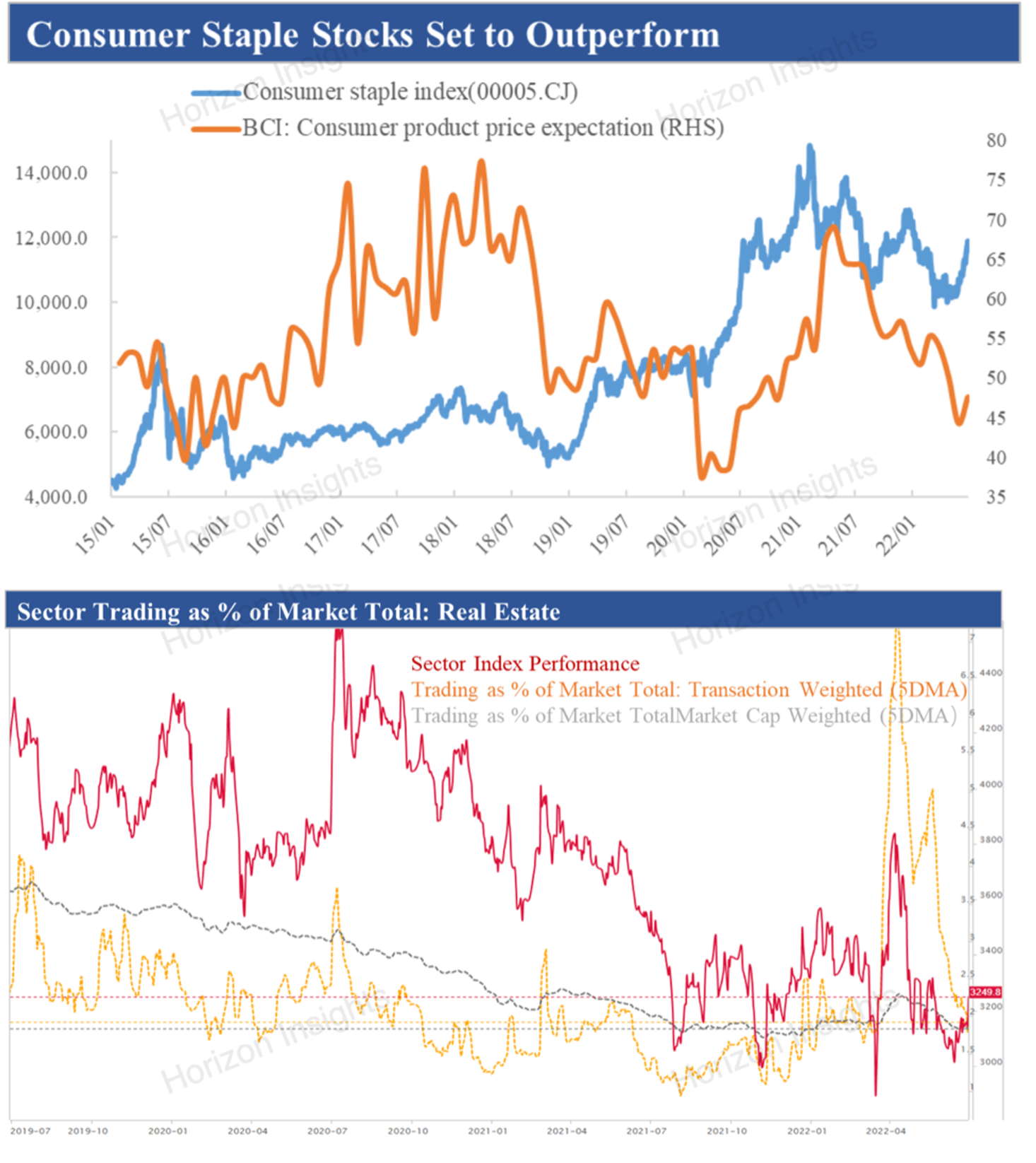

Playing China’s bounce back

China’s economic activity continues to improve as the impact of Covid-19 wanes. Whilst the manufacturing PMI missed markets expectations coming in at 50.2 in June, the non-manufacturing PMI handsomely beat expectations with a 4.2 rise to 54.7. As more companies think to increase consumer good prices in light of improving trends, Horizon Insights reiterates their BUY recommendation for consumer staple stocks in H2 (see graph 1). Real estate stocks will also see opportunities arise (see graph 2). Given the reshuffling of the industry, try to shift portfolios towards central-government-owned SOEs.

Crystal Shore Alpha

China: Big red dragon goes green

Crystal Shore’s systems have been flashing red on China since February 2021 but now the indicators are turning green, signalling that the risk of further capital loss is now low. This is to be expected: the market that crashed the earliest and the deepest is the first one to recover. The same cannot be said for other EMs in which risk remains high, with the exception of India and Indonesia which are recommended BUYs.

Greenmantle

India inflates

Inflation continues to rise in India, with little sign of abating. It will likely exceed 7% by year-end, even as real GDP growth dips and the Reserve Bank of India (RBI) hikes rates. With less than two years until the 2024 general election, the Bharatiya Janata Party (BJP) government does not see cutting the budget deficit as a priority. Niall Ferguson expects higher deficits as the government reduces excise duties and raises subsidies. As the economy runs hot and inflation expectations become de-anchored, Niall expects upward pressure on long-end yields.

Teneo

China: Stimulus ramping up in all-out push

Recent comments by President Xi stated that China will “strive to meet” it’s original GDP growth target of around 5.5% despite recent growth lost to Covid-19 lockdowns. There is some implication that 4.5-5% would be acceptable but achieving even this would require highly aggressive stimulus in the coming months. Given that consumer sentiment remains week, expect infrastructure to be the primary stimulus tool, with additional quotas for local-government infrastructure bonds issued in coming weeks followed by escalation of stimulus to the maximum level by late July.

Alberdi Partners

Assessing Latin America’s external vulnerability

With rising interest rates in DMs, Marcos Buscaglia's latest report analyses how vulnerable Latin American countries are if there is a sudden stop in capital flows to EMs. He finds the main short-term risk present in Chile and Colombia, especially in their private sectors. Most of Latin America’s currencies have the bad outlook priced in, although Marcos comments that the Argentine peso and Peruvian sol are undervalued in real effective terms. Expect Brazil’s central bank to lead the ending of the tightening cycle in the region, with even a rate cut by 2022’s end.

Greenmantle

Roast Türkiye

Turkey may have changed its name to Türkiye, but Niall Ferguson explains that the country remains on its downward economic trajectory. High energy prices and currency depreciation continue to burden the current account and the budget deficit respectively. President Erdogan hopes to prop up Turkey’s rickety financial system with creeping capital controls while distracting the populace with manufactured foreign policy crises. This strategy will remain in use until next year’s presidential elections. In the meantime, Niall expects more inflation, lira depreciation, and stealth capital controls.

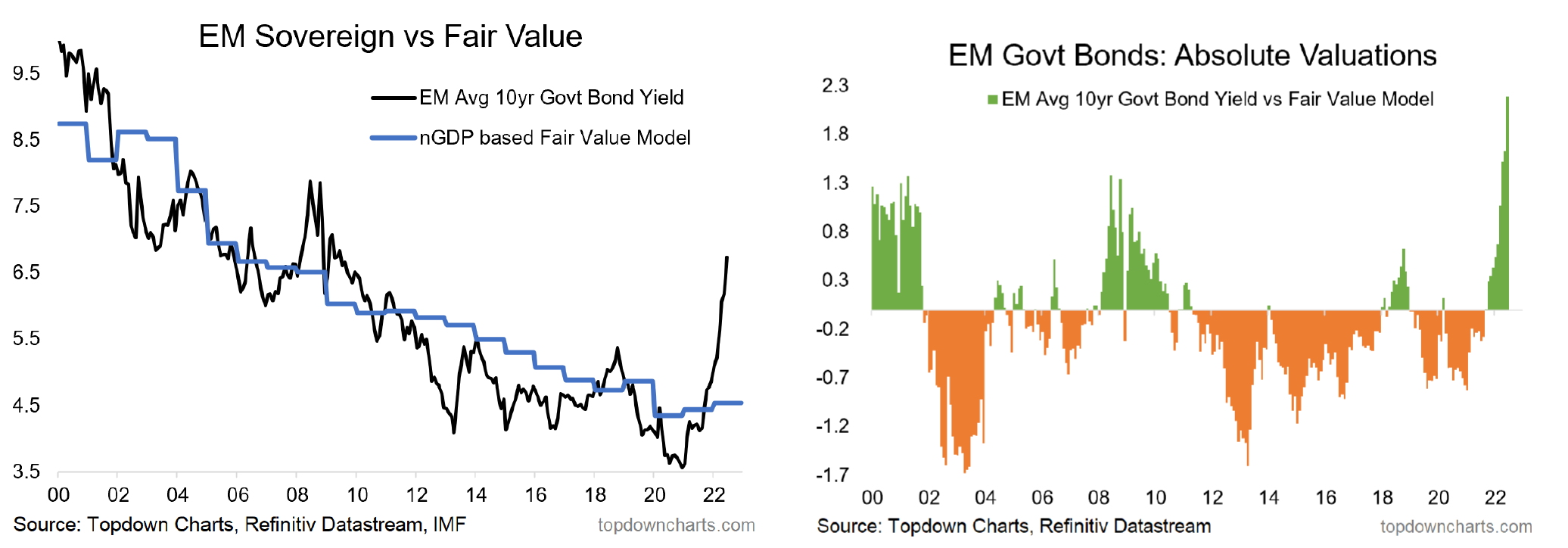

Topdown Charts

Value in EM fixed income

While EM equities look mixed, it’s an entirely different story for EM sovereign bonds according to Callum Thomas: EM 10-year govt bonds are looking very cheap in absolute terms and relative terms (see chart). He also comments on the fairly cheap looking EMFX, although he adds caution that for now, we are still in an entrenched long-term bear market for EMFX overall vs USD, so while there is the extra value in EMFX and hence local EM govt bonds, hard dollar might be the safer bet.

ESG

Rosenberg Research

Opportunities from the European forced energy transition

David Rosenberg’s latest report covers the energy transition and its significant implications for investors looking for the right sector asset allocations within the broader European energy sector. David sees significant opportunities in several sectors: energy (incl. nuclear, green hydrogen, biogas), transport (charging stations, hydrogen trucks) and housing (heat pumps, green construction). Outside of traditional partners such as the UK and US, David also finds some winners in Africa. There are also implications for world bond markets as the current plans will trigger the use of untapped common EU debt instruments.

Forefront Advisers

UK climate targets increasingly implausible

The UK’s Climate Change Committee recently published its annual report. Unsurprisingly, the UK government continues to set very ambitious climate targets with no plans in place to credibly deliver them. Progress remains uneven, with lots of renewable electricity generation and the take up of EVs on one hand, and very little in buildings, agriculture or many areas requiring behavioural change on the other. The cost of hitting net zero will rise and the UK is increasing its exposure to climate litigation as it fails to take necessary action.

Commodities

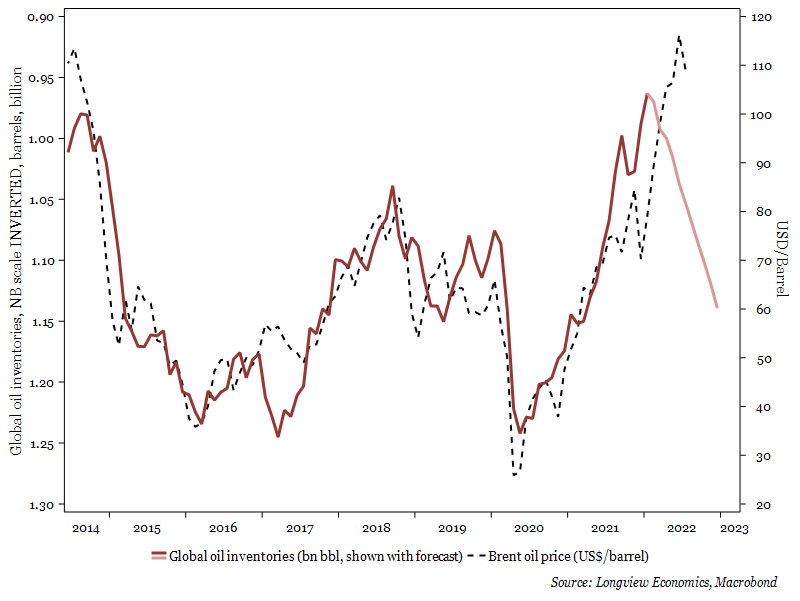

Longview Economics

Building oil positions

Harry Colvin sees large oil supply surpluses emerging over coming quarters (see chart), reflecting a mix of factors including a gradual recovery in Russian supply, continued uptrend in OPEC output and a slowdown in global demand growth. The long oil trade is already crowded and Harry’s models are flashing SELL ratings. Average into SHORT Brent oil futures trade with a ½ short position at current prices and ½ SHORT on strength at $112.00, with a stop loss at $115.80. Implement a bearish Brent futures calendar spread, moving SHORT second month Brent futures and LONG 8-month Brent futures at current prices.

CPM Group

Tantalum: An extensive, industry-leading report

CPM Group’s new Quarterly Review and Outlook is now available. These reports enable clients to stay on top of tantalum market developments with the provision of more granular, detailed, and up-to-date research, information, data, and analysis than has been and is currently available elsewhere. Included in the research are 10-year projects of tantalum supply, demand and price and an analysis of developments for individual producers, processors and users. Please contact us to find out more.