Company & Sector Research

Europe

ResearchGreece

Acquisition of ~30% stake in Ellaktor makes MOH the top RES / wind player in Greece and diversifies its investment case further away from the cyclicality of the refining business. However, it is MOH’s refining business that is currently thriving. Adjusted EBITDA in Q1 grew >2x y/y with refining EBITDA nearly tripling. This strong performance looks set to continue, resulting in ResearchGreece’s increased conviction re. leverage (net debt to max out at 3.0x group EBITDA in 2023) and dividend payments (6% yield) following the RES deal. Their EBITDA estimates are increased by 15%/53%/36% (2022-2024).

Vision Research

Transportation / Logistics short idea

$10bn+ M/Cap, trades more than $50m/day and has short interest of less than 1% - this business over-earned as a result of Covid and tight supply chains that should reverse given loosening supply chains, a shift from goods to services, excess inventory at many retailers, slowing global GDP, and competition from digital first firms. 2023 estimates seem very optimistic. This is Vision Research's fourth new European short idea in the past few months; having also issued nine US shorts since the start of the year.

Forensic Alpha

Walking on broken glass - while GXI has concentrated on convincing the market that the currently high level of capital expenditure will lead to sustained growth Forensic Alpha’s analysis suggests something more untoward might be developing. An unsustainably high payables balance suggests management are delaying payments to suppliers to inflate cashflow and decrease net debt. Together with factored receivables and the pension deficit, leverage is much larger than the figures management have been highlighting.

MYST Advisors

Misunderstood cross-border payment provider with structural cost advantage - WISE has built a “Moat” as the low-cost provider in the space by establishing direct connections with local payment networks and regulatory bodies while obtaining the necessary licenses to operate in its various geographies. Concerns over declining take rates are unwarranted; management lowered rates strategically (which has actually helped to expand gross margins). Despite sustainable 25-30% revenue growth, high 60%s gross margins, >20% EBITDA margins, WISE’s current 4-5% FCF yield more closely resembles a value stock. 2-yr TP £7.00 (100% upside).

Willis Welby

UK: The Manufacturing fan club still looks expensive

Despite Croda, Halma and Spirax having seen 40%+ share price falls YTD, Willis Welby, who specialise in expectations analysis, still struggle to make sense of the share prices. Their caution is compounded when they consider what is available elsewhere. The UK market is not renowned for its growth names, but that does not mean there are none. They see Rightmove, Auto Trader, Softcat and Experian as looking particularly attractive.

Messels

FTSEurofirst 80 Index: Bullish & bearish themes

Bullish charts featured in Messels' weekly 'European Technical Highlights' report include: Ferrari - finds 7-year price and relative uptrend support; NEL - finds 4-year price and relative uptrend support; ABN AMRO - finds 2-year uptrend support and is bottom of the relative range, although they still prefer Banco de Sabadell and CaixaBank. Bearish charts include: Akzo Nobel - breaks support and loses relative momentum; Legrand - breaks support from prior highs and loses relative momentum; Schneider Electric - breaks the uptrend and develops price and relative top formations.

North America

Radio Free Mobile

Carmageddon

Apple declares war on OEMs - expansion of CarPlay into the instrument cluster pushes OEMs further away from the Digital Life of the vehicle and brings them closer to being handsets on wheels. RFM’s research has found that electrification and autonomy could reduce vehicle transport spending by up to 65% which no OEM is likely to survive in its current form. Hence, it is crucial that OEMs have a seat at the table when it comes to delivering digital services in the vehicle. So far OEMs have kept Google out of the heart of their vehicles, they now need to treat AAPL in the same way.

Hedgeye

Subscriber losses to persist - sees the stock below $100/share over the next 6-12 months. Andrew Freedman has long argued that NFLX’s addressable market for subscribers was smaller than management and most investors were modelling, and that pricing power was challenged by competition. This would trigger a reverse flywheel effect that would expose the inefficiency of its content strategy and the fragility of the business. With the stock down ~70%, Andrew goes back to the drawing board to determine what comes next for the streaming giant (incl. strategic options and what a push into advertising could look like).

Quo Vadis Capital

The market is ascribing zero value to the company’s store opening plans - ASO is currently at a growth inflection making it especially susceptible to being misvalued in the current market. John Zolidis considers a range of outcomes for earnings and cash flow from the existing business in addition to the impact of adding 80-100 new stores from FY22-FY26. Shares are <$38, just 5x FY22E EPS, if ASO can trade at 10x, it suggests a $110 price by early 2026 (190% upside). Alternatively, a 10%-12% FCF on the current business plus $25 for the discounted value of future stores suggests a $75 value today (~100% upside).

The Retail Tracker

Shares down 40% YTD and 20% since the split - trades at <6x 2022 EPS, a very depressed multiple for a company with real potential to grow. Since Martin Waters took the helm, the brand has made significant changes to the stores, marketing, product assortments, partnerships and even the structure of the international business. Changes are resonating with the consumer. She is re-engaging at high rates, and they are bringing in new customers. Expects to see more collaborations / partnerships as well as investments as the company begins to think about the VS brand more as a platform for their customer rather than just a simple intimates brand.

Alembic Global Advisors

Recent underperformance and valuation multiple compression vs. peers is overdone - APD has underperformed Air Liquide and Linde by 23% and 81% since hitting March 2020 lows. However, Hassan Ahmed’s analysis shows APD’s margins are turning a corner; it has the most attractive geographic exposure in the current global macro environment amongst the industrial gas majors (US & Asia > Europe); and its higher exposure to the hydrogen economy is not fully appreciated. Last, but not least, the company has a slew of growth projects coming online over the next five years which should add $36+ per share to valuation. 12-month TP $305 (30% upside).

Thompson Research Group

Separating wheat from chaff - FERG outperforms even in tough times. Q322 results saw continued growth above market (organic sales +23% on a tough +20% comp) and FY operating guidance was ahead of expectations. TRG expects another meaningful ($1bn+) buyback plan to be announced with next quarter’s results as FERG continues to generate loads of cash. They initiated coverage with a Buy rating in July 2019 highlighting FERG’s dominant US market share, DD revenue growth, clean B/S, strong FCF and deep discount vs. US peers. 12-month TP $216 (100% upside).

Lynx Equity Strategies

As companies adjust to a down economic cycle, topping the list of corporate priorities should be to contain costs / expenses and maintain a healthy FCF. INTC should be no exception. While cutbacks in opex are to be expected, KC Rajkumar believes there is low-hanging fruit in the cost domain for the CFO to rationalise. The option is not without risk, but hard times call for bold measures. KC thinks a viable case can be made for INTC to pull out of TSMC’s 3nm foundry service slated to start in 2023/24.

Antya Investments

A cloudy outlook - Neeraj Monga presented his short thesis on this cloud service provider at our recent Equity Shorting Conference

(click here for audio and slides). Neeraj posits that CDAY’s aggressive and creative accounting, nosebleed valuation and uncertain prospects in Asia Pacific portend a steep decline in its stock price. He estimates downside of more than 50% to below $20 per share.

BWS Financial

Headlines surrounding the Videotron case occurring during a broad market sell-off has created a deep discount in XPER's valuation - however, the patent lawsuits in Canada are just one of several catalysts that could develop in 2022 and were not included in Hamed Khorsand’s earnings model. Investors should instead focus on XPER’s expanding end markets and the company’s ability to generate revenue from new automobile models incorporating AutoSense in Europe. Hamed estimates FCF of $200m in 2022 (FCF yield of ~14%) and even more in 2023. TP $26 (85% upside).

280First

Decoding the Financial World: 10Q/10K text analysis

Utilising AI, NLP, data analytics and qualitative analyst oversight, 280First can rapidly glean material / actionable insights on companies.

Qorvo (QRVO) - Concerns about large customers. The following wording was added to its risk factor in 10K 2022 “The loss of one or more of these customers could have a material adverse effect on our business, financial condition and results of operations”.

HP Inc (HPQ) - Pricing issues. Changed wording in 2Q 10Q vs. prior quarter; “We expect the pricing environment to get more competitive”.

Cavco Industries (CVCO) - Seeing early signs of increasing cancellations?

Ralph Lauren (RL) - Worried about increasing prices and its impact on demand.

Japan

Asymmetric Advisors

PER now <20x (next year's forecast) for a company that has grown profits >4x in 4-yrs - this DX consultant is a great example of a strong growth name where fundamentals haven't changed at all, but the share price has retraced ~50% since last Sept as foreigners (52% shareholder ratio) look for profit-taking targets. Other fallen angels in the small-mid cap growth names that the analysts at Asymmetric Advisors are keen to highlight include Descente, Sato Holdings, Shibaura Machine and TRE Holdings.

Emerging Markets

Bondcritic

Asia HY Credit Market: More rating downgrades to come

Slowing growth and uncontained inflation are spread-negative for Asian bonds as rising rates will increase refinancing risk. In addition, cost-push inflation and slowing demand will hurt bottom-line earnings and deteriorate credit fundamentals in general. Bondcritic prefers USD bonds over local currency bonds and expects deteriorating credit fundamentals to force bond investors to resort to high-quality high yield bonds in India, Indonesia, and Vietnam where there should be more bond supply. Conversely, they expect bond supplies to continue drying up in China. While there is value to be had in the Chinese property sector, bottom-up homework must be done.

Propitious Research

Better-than-expected revenue growth from its non-marketing core business as well as strong cost control provided a positive surprise to 1Q22 results. However, evidence remains that Baidu continues to lose digital advertising revenue market share and that its new growth driver engines (AI Cloud and Intelligent Driving) negatively contribute toward operating margins and are unlikely to drive positive earnings surprises over the medium-term. In this insight, Wium Malan looks at the Chinese digital ad market, Baidu’s market share loss, and assesses whether AI Cloud and Intelligent Driving could compensate to deliver earnings growth surprise.

New Street Research

Why 5G FWA is a game changer in EM

~1bn homes lack broadband globally - the vast majority of which are in Emerging Markets. Broadband today reminds New Street of mobile in 2000 ahead of the 2G EM bonanza, with penetration high in DM and low in EM and most analysts predicting this to remain the case for many years. However, 5G FWA dramatically improves cost to serve and will likely therefore significantly upscale demand for broadband in EM. Investors should start to think about implications as it is potentially transformational for EM Telco revenue growth.

Hemindra Hazari

While the market and the media’s attention are focused on the purging of toxic assets, a very different and critical asset continues to silently exit via the back door - Hemindra Hazari reveals that since April last year, 21 senior executives have quit Yes Bank (18 in FY22 and 3 so far in FY23) and this follows 19 departures in FY21. The high attrition would have been acceptable in FY21 (the first year of the reconstruction) the fact that it continues is indicative of major inter-personnel issues involving executives in the highest echelons. A lack of transparency to stakeholders re. these managerial exits is also a concern.

Aequitas Research

Investment blacklist will further pressurise the upcoming US$18bn lock-up release - a limited free float likely explains why shares in this AI software provider have performed so strongly since listing despite sentiment surrounding its IPO being so weak. However, this will change drastically when the lock-up expires later this month. Even if one assumes that SoftBank, Alibaba and Cornerstone's won’t sell, there is still 45% of the company, worth US$11bn coming free. Furthermore, due to it being on the US investment blacklist, which bars US companies from investing in it, some shareholders will have to sell.

Macro Research

Developed Markets

MRB Partners

Upside surprises expected from some central banks

Most central banks will be welcoming of currency appreciation to dampen inflationary pressures. In the short-term, there is greater room for upside surprises from other central banks, particularly the ECB, providing support for select pro-growth currencies. However, central banks in economies with greater household debt imbalances will be unable to lift policy rates the same degree cyclically without causing significant disruption. Netting out these crosscurrents, Phillip Colmar recommends mild overweight exposure to the euro on a 6-12 month horizon, but barbell this with the more defensive Swiss franc. Avoid commodity-based currencies and the pound.

Alternative Macro Signals

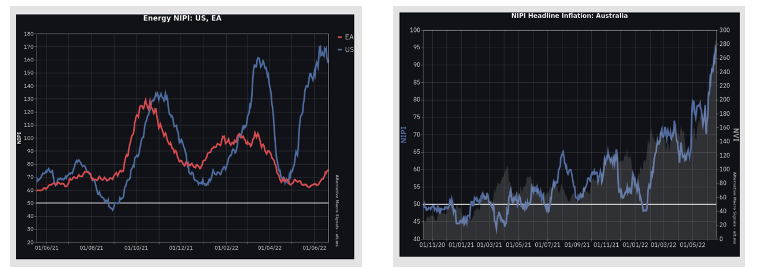

Inflation pressures show no signs of easing

The News Inflation Pressure Indices (NIPI), developed by Alternative Macro Signals, scans an extensive range of new sources to track and forecast inflation across the globe. In their latest report, they find that US energy price pressures remain very strong and that consumers should expect sharp rises in utility bills this summer, a potential source of upside risk relative to consensus (see graph 1). Meanwhile the euro area shows no signs of easing and Australia stands out among DMs as inflation momentum strengthens considerably as the country’s NIPIs reach fresh all-time highs (see graph 2).

CrossBorder Capital

Euro set to fall below parity

Large imbalances, no embedded fiscal transfer mechanisms and a lack of safe assets are all some of the Euro’s underlying structural flaws that are now again being exposed by the latest global monetary tensions. Could a political fix solve the issue? Michael Howell doesn’t think so, especially with the anti-inflationary instincts embedded in Northern Europe. The only practical path for policymakers is to ‘do a Japan’ and crash the Euro. Michael is staying SHORT EUR.

Greenmantle

As safe as houses

Historically, housing has proven a good hedge against inflation, but this does not mean that frothy housing markets are exempt from sharp declines, especially during a steep hiking cycle. As central banks tighten in response to the recent surge of inflation, warning signs are flashing across global housing markets. New Zealand, Canada, and Australia are now experiencing the start of a housing market correction. The housing markets in the UK and Ireland are also starting to cool. Niall Ferguson expects US residential real estate prices to flatline and then moderately decline over the next year.

Belkin Report

US: Blowing up the bubble

Michael Belkin believes excessive US stimulus pumped up an enormous speculative bubble in US risk assets and turned investors into bubble people. Sure, dominoes are already falling but sentiment has yet to grasp what happens in a severe recession, which is now developing: ‘good news’ on inflation becomes bad news for earnings, stocks and the economy. A rude awakening awaits. Michael recommends selling and shorting into brief market stock market bounces, shifting LONG exposure into defensive consumer staples, utilities and health care and SHORTING tech, consumer discretionary, materials and energy.

Deep Macro

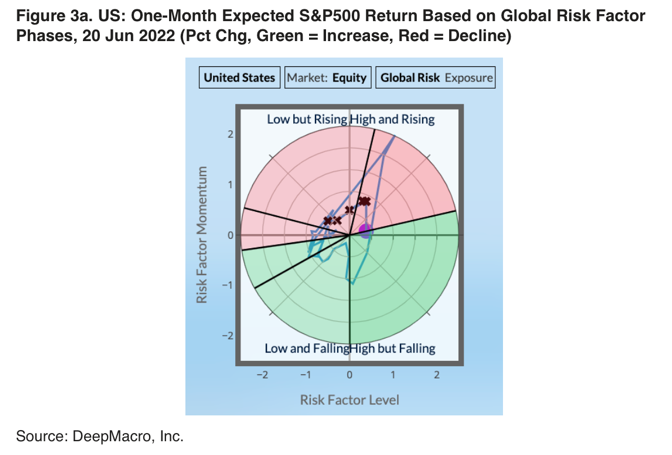

Questions on US equities

The growth outlook isn’t necessarily the problem facing equities, claims Jeffrey Young. Data has been slowing for many months and the equity market has been declining. Surprisingly, the risk outlook isn’t the problem either with risk levels today the same as over the last few months (see marked graph). The real issue is inflation; in order for it to be less of a threat to the market, it needs to develop significantly more negative momentum. Expect this to take a quarter or two before the short-term outlook for equities improves.

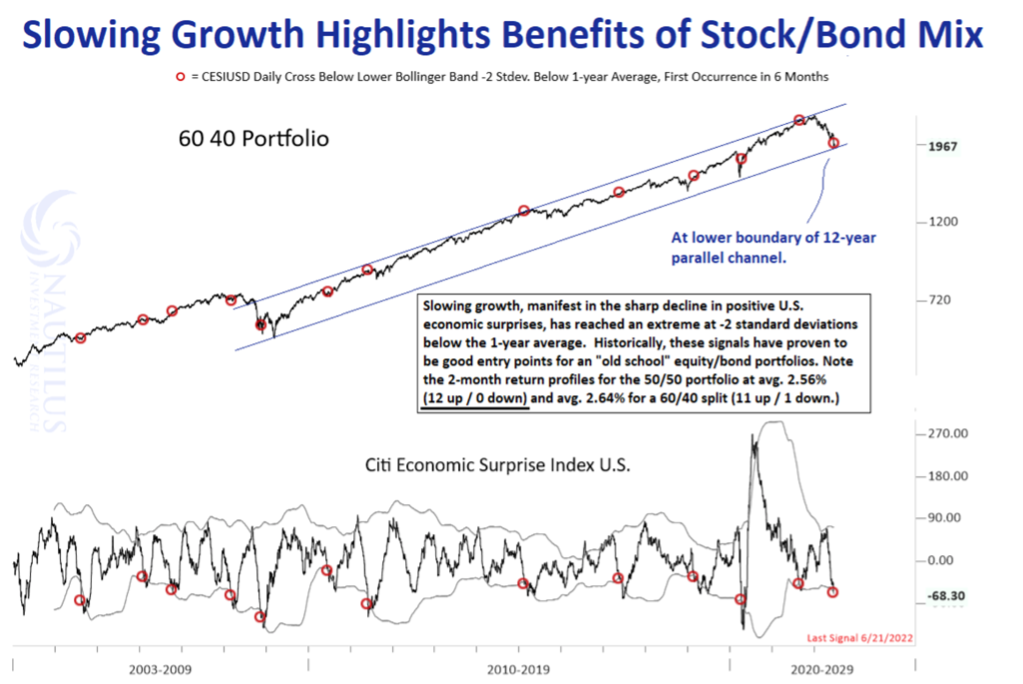

US: Bonds typically add value when economic data slows

Bonds have become more attractive as the Fed hikes rates to combat inflation and recession becomes increasingly likely. In historical observations when US economic data was much worse than expected for an extended period, a classic 60/40 portfolio including the S&P500 and the S&P Aggregate Bond Index returned 2.64% two months out, while a 50/50 mix produces a 2.56% return; a mix of stocks and bonds typically produces a positive outcome over the short-term more often than a portfolio entirely consisting of one or the other.

Minack Advisors

Australia unlikely to tighten aggressively as Fed

After a surprise 50bp hike in the RBA’s last meeting, futures pricing indicate they will tighten more aggressively than the Fed (see graph). Gerard Minack disagrees; Australia doesn’t have the same underlying inflation than the US, and the economy is more sensitive to changes in short rates. The RBA is right to tighten policy but were it to do so as much as the market expects, it would threaten to explode the housing market.

Emerging Markets

HED Capital Management

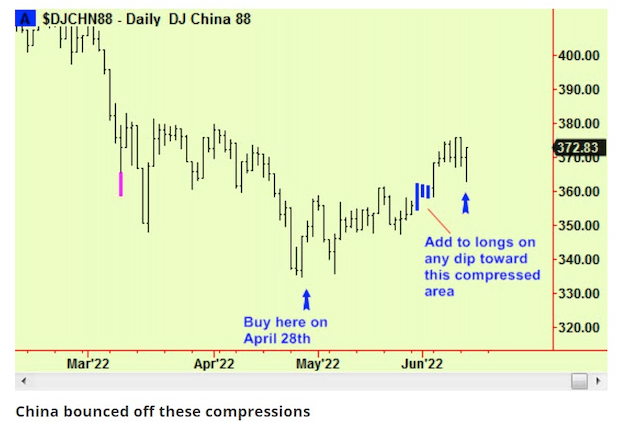

China: Not bearish

Richard Edwards comments that China continues its trend, largely unaffected by weakness in the US and Europe, although he did see a forecast dip back to the recent compressions in today’s session [published June 14th] followed by a rally into the close. That was another buying opportunity, as Richard pointed out in the last edition, and prices are now likely to rise more steeply for a while.

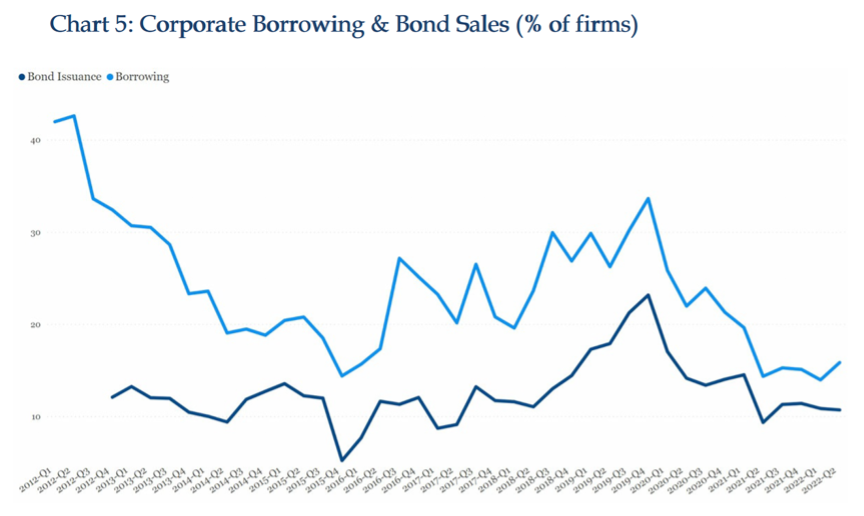

China Beige Book

China: Monetary stimulus is fiction

Nominal increases in the government’s Total Social Finance (TSF) data from Jan-May were the second-highest on record, leading some to believe a stimulus wave had begun. Leland Miller points out that TSF can be deceptive. He instead directly tracks credit uptake at firms, and comments that through this lens the trend is as tight as ever; for the fifth straight quarter, national borrowing checked in between 14-16% of firms, skirting the record lows since 2012 (see graph). Worryingly, credit seems to be no cheaper than a year ago for most firms, and for SMEs it appears that borrowing is out of the question altogether.

Teneo

China: Rural bank runs don’t signal systemic financial risk

Bank runs in rural areas have captured significant media attention, but their wider risks are overstated. The problem stems from the country’s village and town banks (VTBs) that benefit from relatively limited regulatory oversight, including the freedom to offer high deposit rates and operate outside their home regions. Of the 333 banks the PBoC deems high risk, VTBs comprised 103. Losses at VTBs are too small to ignite systemic risk and their problems are not a harbinger of the country’s financial demise.

Alberdi Partners

Argentina: Central bank decisions

The Central Bank of Argentina (BCRA) has barely bought reserves this year in spite of record high grain exports, and Marcos Buscaglia sees its loss of reserves from Aug 2021 onwards as a bad omen for what lies ahead. We will see the government introduce more controls to avoid a devaluation of the peso, but it will not be enough. Faster money printing, pressures on reserves and more FX controls leads Marcos to expect the FX gap to widen in H2/2022, at least to 100%.

Intelligence Research

Colombia: Petro elected as country’s first left-wing president

Petro’s victory marks a historic shift for Colombia. Whilst he has repeatedly insisted that he is not as radical as his critics make out, his pledges to redistribute wealth, end fossil fuel extraction and implement a wide-ranging land reform mark a significant departure from the incumbent president. Petro also faces the challenges of reassuring better-off Colombians that he is not seeking to expropriate their wealth. However, lacking a majority in congress may force him to tone down some of his more radical proposals once he takes office.

Oxford Analytica

India: Modi’s challenges

Prime Minister Modi is secure in power but faces several political and economic challenges, particularly around curbing inflation and its major downside risk to India’s near-term GDP growth prospects. Expect a sustained monetary tightening cycle ahead. Meanwhile, Delhi will step up its various trade negotiations and may soon announce a free-trade agreement with the UK. The ruling BJP party will win the Gujarat and Himachal Pradesh polls, boosting the party’s confidence of winning a third successive governing term nationally in 2024.

Commodities

Independent Strategy

Agro commodities provide a hedge against tightening liquidity

Commodities remain a good hedge in the current macro environment, claims David Roche. Food security remains an increasing problem and, although consumer demand may suffer from falling average disposable incomes, food demand remains relatively inelastic. The risk to prices is if supply blockages in grain suddenly loosen, but grain storage and logistics remain pressured and the increased restrictions on the export of agro commodities by many countries are strangling supply. David maintains his LONGs in grains and cotton.

Queen Anne's Gate Capital

Individual commodity fundamentals could provide good opportunities

In the face of a higher USD, unclear Chinese lockdowns, stock market declines, commodity-specific issues and a rush to cut VaR during outrageous volatility, Kathleen Kelley discusses how commodities have clearly faced a powerful witches brew. Just a week after the Invesco Commodity ETF drew attention for its record holdings, Bank of America’s monthly fund manager survey reported that Long Oil/Commodities remain the most crowded trade for the 2nd consecutive month. Commodities could be entering a period where individual fundamentals matter, providing excellent relative value opportunities.

Global Mining Research

Copper: Risk vs Reward

The post-Covid economic hangover has arrived. For copper this means equities have corrected, yet the metal is close to $4/lb. Markets have repriced risk, especially in small caps, but this is a short-term view. There is a case for investing while there is blood on the street, explains David Radclyffe, as he advises investors to position for a traditionally strong Q4. His preferred exposure is through more attractive and better value larger caps such as First Quantum Minerals and Lundin Mining Corp. He also upgrades 29Metals to a BUY given its better overall metrics to peers.

PRC Macro

China: Shallow economic recovery bearish for commodity cycle

Although local governments may retreat from the most restrictive measures of previous Covid outbreaks, gentler measures will still create enough uncertainty to dent a recovery to demand. The recovery to upstream supply continues to be much stronger, and William Hess expects this imbalance to ultimately drive a destocking cycle. This is at the heart of William’s bearish cyclical outlook for commodities and nearer term call for a correction to metals prices.