Company & Sector Research

Europe

Smart Insider

“Insider” sentiment is very bullish

May saw more directors and senior employees buying shares than in any month since Mar 20 - activity was very similar to Feb and Mar 22, where in each month there were >1,000 insider purchases vs. a very low level of selling (<300; Jan-May selling is -20% below 2020 levels), with a Sell/Buy ratio of 0.25 (<0.4 is bullish). Sweden, UK and Germany saw the most buying. Out of the 26 stocks that Smart Insider upgraded last month, the majority were in Industrials, Financials and Consumer Discretionary. Large May purchases (>€1m) in positive ranked stocks include Bank of Georgia Group, Corporacion Financiera Alba, Hemnet Group, Ratos, S&T, Skanska and Valmet.

TT Equity Research

A crying shame of managers' greed leaves zero equity value - the 2022 annual report again underlines that BOO is managed for the wealth creation of its founders and executives. Accounting is a mess, lacks disclosure and increasingly adjusted to support management remuneration targets. During fiscal 2022, growth slowed down significantly, real profitability crashed and cash evaporated. Even if capex normalises, Teun Teeuwisse does not see how the online fashion retailer can sustainably generate cash. Without cash generation and with debt rapidly mounting BOO shares are worthless paper.

Woozle Research

Primary research reveals a strong start to Q2 driven by bullish consumer trends in Europe with Asia recovery on track - Gucci: customers undeterred by price hikes are showing greater interest in higher priced and limited-edition items (especially women's handbags and "Gucci Link to Love" jewellery). Store managers are guiding for +11% LFL sales growth y/y. Bottega Veneta: first collection under new creative director is outperforming expectations; attracting younger customers and also seeing fewer delivery delays / faster lead times. Balenciaga: tourist recovery boost; store managers are optimistic amid growing interest in their upcoming collection.

Insight Investment Research

Prolonged traffic recovery at 407-ETR has been weighing on the share price, but Robert Crimes expects an acceleration as Covid restrictions were fully lifted at the end of Q1 - TomTom congestion data for Toronto is almost back to 2019 levels and Insight’s Google Maps survey shows 407-ETR average peak time savings of 26 mins and LV Cost of Time Saved per hour of US$30. Robert increases his valuation of FER's 43.2% stake in 407-ETR by +€0.6bn to €17.5bn (only slightly less than the group’s entire Managed Lanes portfolio at €18bn); it is the most valuable toll road in Insight’s Global Infrastructure universe. TP €62 (150% upside).

Arete Research

Upgrades to Buy - stock has over-corrected; extremely well positioned with its hybrid bonding technology. In this note Arete looks at 1) The impact of structural changes to compute architecture and how it benefits advanced packaging and BESI. 2) The likely progress of hybrid bonding driven by customer roadmaps in the high-performance compute space. 3) Why the cyclical risk into 2023 is lower than it was in the 2018/19 downturn. 4) Updated estimates and valuations. TP €74.2 (30% upside).

North America

MYST Advisors

Bear’s Den Idea Forum: 80% hit rate; 28% avg. alpha

Following stellar returns at MYST’s previous event, participants deliver another round of compelling ideas with significant downside potential. Interestingly, several stocks have relatively low short interest despite uncertain medium-to-long-term business prospects.

Coinbase (COIN) - Pressure from volume declines, increased regulation and continued share loss. TP $35 (50% downside).

SVB Financial (SIVB) - Shrinking Fed B/S to cause “VC / PE Winter” and stifle earnings growth. TP $240 (50% downside).

TuSimple (TSP) - Cash-burning autonomous driving software co. with inferior product years away from market. TP $1 (90% downside).

Yeti (YETI) - Material risk to outlook amid high inventories, slowing sales and raw material headwinds. TP $32 (30% downside).

Gordon Haskett Research Advisors

Broadlines & Hardlines Retail: Inventory review

Across GHRA’s coverage inventory grew ~35% y/y on average in 1Q (or ~$40bn in aggregate) vs. average sales growth of just 3.5%, with the inventory/sales spread widening to ~31.5% (from 4.5% in 4Q). Another disappointing update from Target will further raise fears that retailers are over inventoried and gross margins will face increasing downside risk. This inventory overhang will take time to work through, but off-price retailers TJX and Burlington are well placed to benefit as it will create attractive closeout opportunities that could drive upside to 2H22 estimates.

Compass Restaurant Consulting & Research

CMG - Can sustain current SSS trends (June est. +8-10%); growing positive traffic trends (one of the only concepts doing so) coupled with little to no resistance to price increases. The new Pollo Asado is one of the most successful promotions in a long time.

MCD - Dominating the price / value messaging and taking market share from peers. June SSS expectations are +2-4%. Top sales drivers: 2 for $6, Nugget Bundles, Off Premise sales. On the negative side, most franchisees unhappy with the new PACE Store Visitation Program.

DPZ - Declining momentum. June SSS expectations are in the negative 3-1% range. Driver shortages not only impacting sales and market share, but also brand credibility; not easily fixed.

AlphaSituations

The merger spread has widened significantly since Apollo Global Management’s all-cash offer for TEN was first disclosed (currently stands at 18% having hit 37% in May). So, is the TEN situation simply a victim of the current market disruption or is there something more to this spread? Robert Sassoon assesses the regulatory risk (low) as well as the risk of APO reconsidering the transaction (unlikely). Assuming the transaction closes by the end of the year, there remains considerable IRR to game in the 30-55% range, but even if the deal closes in 1Q23 you are still looking at an IRR in excess of 20%.

Kailash Capital Research

Is it too late to buy Oil stocks?

Energy stocks are still dirt cheap and are painfully under-owned by investors crowding into index and ESG funds - offers healthy yields, investment grade balance sheets and the stocks have highly asymmetric payoff structures based on history. KCR show that when Nat Gas prices rise 100% more than Energy stocks over the trailing 3 years, Energy typically goes on to trounce the S&P 500 Index. In the unlikely event that prices do collapse, it would be due to a macro shock that would level the economy and do far worse damage to other sectors. KCR’s top ranked Energy companies include Marathon Oil, ConocoPhillips and Occidental Petroleum.

Portales Partners

Likely to take several years before EPS starts to grow y/y as revenue potholes emerge in private equity and 10% growth in asset and wealth management proves challenging. While valuations are not dear, as liquidity is withdrawn and casualties litter the headlines such as Tiger Global, GS will suffer as well. Simply put, Charles Peabody sees $6-7bn of PE type revenues declining over the next few years and does not see more than $2.4bn in growth from asset management to replace it.

Renaissance Macro Research

The competitive and credit risk to BNPL margins

Bank competitors will drive merchant BNPL fees down by ~50% and put pressure on fintechs to offer longer loans so that BNPL evolves for credit-access as well as payments. This will increase credit costs and risks particularly for BNPL pioneers whose data window happens to fall in an unusually benign credit period; and it will play to the core strength of banks in underwriting credit. Further, large banks will act aggressively to narrow any broader deficit in data capabilities that can support BNPL in delivering advantaged customer experience and merchant lift.

Behind the Numbers

Security software earnings quality comparison

BTN’s earnings quality comparison on six of the major security software players (Cloudflare, Palo Alto Networks, Okta, Fortinet, Zscaler and CrowdStrike) examines factors such as relative dependence on stock options and policies regarding capitalised software, sales commissions, network depreciation, and aggressiveness of non-GAAP adjustments. The report ranks the company from most to least aggressive.

Radio Free Mobile

The strangest profit warning - Richard Windsor questions the validity of MSFT’s claim that USD strength is to blame and sees a difficult quarter ahead. Looking at the wider Technology sector, he notes that while many stocks have already fallen by 70%+ they could easily halve again. Stick with the value end of the sector and semis in particular. He favours Qualcomm, TSMC and MediaTek as companies with reasonable growth ahead, strong positions in their markets as well as valuations that are less than 15x 2022 PER.

Two Rivers Analytics

Sales have fallen for three quarters, from a growth rate of 51% last June to -23% in the quarter just ended. Margins have collapsed (gross margins down from 48% to 42% and EBITDA margins from 39% to 31%) and the company has added $1bn of debt since 2017. The share price is only down 13% YTD and is still 10% higher than a year ago. Eric Fernandez believes UI warrants a closer look as a potential short candidate with the stock trading at high multiples of both sales and earnings (46x Jun 22 and 35x 2023 earnings). Other companies flagged in Eric's ‘Breaking Estimates’ model are Nutanix, Upstart and Corsair Gaming.

Australia

Global Mining Research

Sub-A$9.00 this gold producer offers great value for a lower risk / higher growth senior - NST trades at 1.6x P/NPV (1.1x spot - close to an 18-month low), and FY23 FCF and dividend yield of 8.4% and 3.1% respectively. There is a clear pathway to ~2Moz/yr and GMR sees a potential cash surplus of ~A$0.8bn over FY23-FY25 which could be used to fund organic growth such as the KCGM mill expansion and / or increase returns to shareholders (dividend could be raised closer to A$0.5bn/yr). TP A$12.00 (40% upside).

Japan

Churchill Research

This homebuilder must be one of the cheapest stocks in Japan - Michael Churchill says, “You could buy all the shares, shut down the business tomorrow and walk away with $150m in cash, plus another $100m as you sold off the inventory". P/B is at an 8-yr low; management has provided strong guidance for fiscal 2023; operating margins have been running at c.14% for several years and cash has been piling up on the balance sheet. Guidance is for a 22 yen/share dividend (3% yield) but they could comfortably pay 100 yen/share (13% yield). 12-month TP ¥1306 (75% upside).

LightStream Research

PSVR2 is increasingly looking like a key differentiating factor for PlayStation - Mio Kato believes Sony is in the best position to dominate the VR space and continued VR title announcements into the launch of the PSVR2 could act as a catalyst for the stock which he still considers too cheap. The balance of AAA and indie titles looks good as do prospects for building momentum for the new PlayStation Plus plans. Continued revenue expansion from title launches on PC will also support revenue growth.

Emerging Markets

Horizon Insights

China: e-commerce grassroots surveys

Community group buying e-commerce competition landscape further optimised - JD.com shrinks, while Meituan Select, DuoDuo Grocery and Tao CaiCai’s market shares improve. Meituan Select and DuoDuo Grocery are clearly better positioned in terms of order volume, with a combined market share of c.80%. More details on traditional e-commerce business, live streaming e-commerce competition between Kuaishou and Douyin, and express industry dynamics are available in Horizon Insight's quarterly survey report.

Entext

Chinese clean energy space looks attractive after the recent selloff - BYD is one of Sean Maher’s long-time preferred electrification plays and he is increasingly confident that by mid-late decade it will be worth significantly more than Tesla. BYD set another record month for sales in May and its all-new Seal model offers another revolutionary innovation - a CTB (cell-to-body) structural battery system. The share price is up 80% since Sean added BYD back into his Energy Transition basket (+240% since initiation); constituents added in the last 6 months include Air Liquide, Linde, LG Chem and SK Innovation.

Galliano's Financials Research

Victor Galliano’s top pick following a review of several Indonesian commercial banks - Mandiri is well geared (with its exposure to MSME credit) to continued GDP recovery; it ranks well re. pre-provision profitability, and post-provision profitability should improve going forward; its return prospects are helped by healthy NPL coverage for its delinquency ratio which implies further potential for lower prospective cost of risk. Victor also likes Bank Rakyat and sees Bank Permata as a potential “turn around” stock, especially if management can improve credit quality and keep lowering its cost of risk to boost returns.

Aequitas Research

Share price slumps as Alipay cuts stake - in this note, Aequitas discuss the placement dynamics and run the deal through their ECM framework. It represents 20 days’ worth of ADV and hence, won’t be the easiest one to digest; KP is now likely to face a large overhang for several months. The timing of the share sale also seems odd since Ant could have reduced their stake when the share price was significantly higher. Despite the sell-off, KP is still trading at 21x FY22 and 15x FY23 EV/Revenue, which isn’t exactly cheap.

Macro Research

Developed Markets

Andrew Hunt Economics

The age of uncertainty: The UK and Hong Kong

Contrary to media reports, Andrew Hunt does not foresee an existential crisis for Sterling. Instead, we will see a societal / institutional crisis that will give rise to years of political instability, which will be problematic for GBP in the near-term. On the other hand, Andrew sees the Hong Kong Dollar as a candidate of currency existential crisis. The highly indebted, overvalued currency with a weaker balance of payments is not immediately at risk, but investors should be careful when it comes to long-term HKD-denominated contracts.

Eurointelligence

ECB: The case against another purchase programme

With the expiry of the ECB’s asset purchases this month, there is debate about a replacement programme. Wolfgang Münchau remains sceptical of the ECB’s willingness and ability to bail out governments in a time of high inflation, as asset purchases will result in central banks blunting their main policy instrument of the short-term interest rate, a disastrous decision that could give reason for member states to leave the eurozone. Instead, they will opt for a restrained emergency programme to protect monetary transmission channels in a time of crisis.

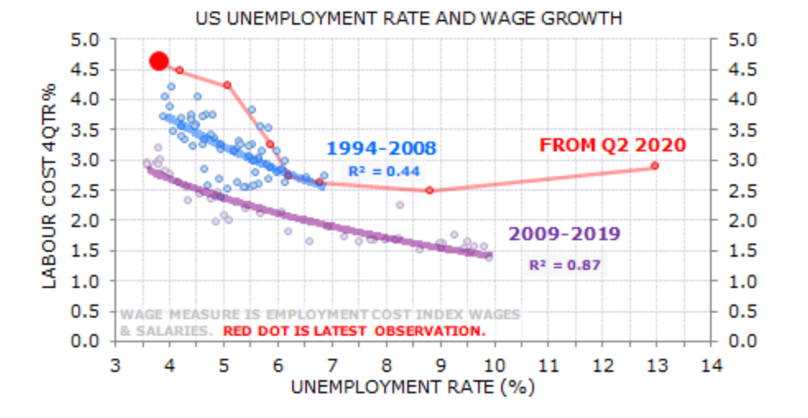

Minack Advisors

US past peak tightness, but is a long way from sustainable

US labour markets are starting to ease, but wage growth remains at a level incompatible with the Fed’s inflation target, which Gerard Minack explains will force them to engineer an increase in unemployment. The question remains how much the Fed will have to loosen labour conditions. Pre-GFC it would have been straightforward, but now the relationship between unemployment and wage growth has shifted to a new behaviour that makes controlling wages more difficult (see chart). A material lift in unemployment is needed, but there’s never been a >0.5% rise without a recession.

Greenmantle

Canada: The housing bubble deflates

Canada’s economy remains robust, aided by elevated oil and food prices and receding pandemic restrictions. For Canadians the picture is less bright, warns Niall Ferguson. Inflation is at a 30-year high, households are highly leveraged with variable-rate mortgages, and the housing market is losing ground. The Bank of Canada is signalling four more hikes this year; if they, like the Fed, have underestimated the inflation challenge, Canada not only faces a 2023 recession but also a sharp correction in the housing market.

AAS Economics

Australia: Down, down, down under

The Reserve Bank of Australia (RBA) has increased its benchmark policy rate by 50bps to 0.85%, with the 2022 sum of increases now at 75bps. Frank Shostak warns that the lagged momentum of the inverted policy rate does not bode well for economic activity in the months ahead (see chart 1). His AMS indices also indicate a subdued annual growth of job ads and a poor PMI services index ahead (see charts 2 & 3), further adding to the worsening outlook.

Musha Research

Japan: Land of the rising sum

Ryoji Musha claims investment opportunities for Japanese stocks have arrived, with potential for a summer rally. Once it becomes clear US stocks have bottomed out, Japanese stocks will step into the limelight. The country’s market has withstood the pandemic, the Ukraine war, inflation and US rate hikes, and the pandemic has accumulated desire and savings to a level that will result in an explosion of pent-up demand in the coming months.

Economic Perspectives

Lenders are running scared!

Governments and central banks that expected ultra-loose monetary policy to support a strong private sector recovery are dumbfounded. Yet, Peter Warburton explains that banks’ caution makes perfect sense in the face of uncertainty. When the state assumed responsibility for credit creation – and money supply growth – at the start of the pandemic, little thought was given to a graceful exit. From the pandemic to the cost-of-living crisis, the banks are being invited to resume responsibility. This is adverse selection bias writ large. Lending growth has turned negative in real terms, meaning that credit conditions are tightening well ahead of rate hikes.

Emerging Markets

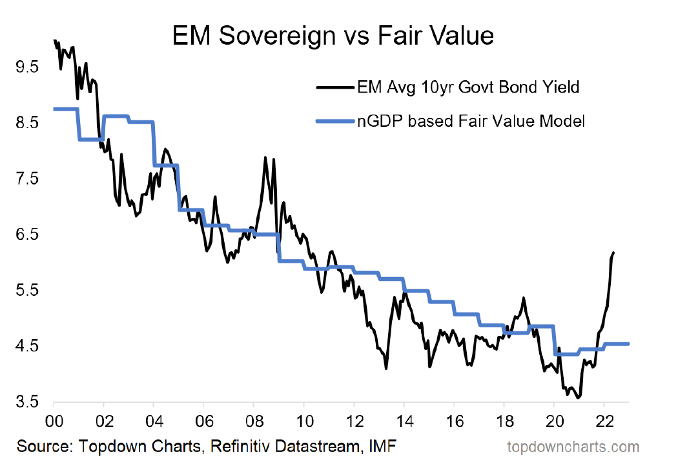

Topdown Charts

EM sovereign bonds

The spread between EM govt bond yields and the fair value model is the widest on record, claims Callum Thomas (see chart). His sentiment indicator points to a contrarian bullish signal for EM bonds. Although Callum prefers hard dollar EM sovereign, the valuation indicator for EMFX is still on the cheap side, but the decade-long bear market in EMFX needs to be shaken off first. Prefer USD EM sovereign bonds until EMFX looks tactically more sound.

Suttle Economics

EM: Going for a hike

Emerging rate hikes continue, with India, Poland and Chile recently increasing rates 50bp, 75bp and 75bp respectively. It is just a matter of time before Thailand and Indonesia join the fold as EM central banks revise up near-term inflation forecasts. The outlier remains Turkey, which Phil Suttle says is the best near-term prospect for those looking for an EM credit crisis to spark a broader credit problem. Surprisingly, the relative lack of growth damage from the aggressive monetary tightening across EMs remains limited.

Talking Heads Macro

China: A new dawn?

China’s rebound will not represent a new dawn, but rather a sunny spell in the early evening of its economic cycle. It will, however, remain the only major economy with expansionary policy and surging growth, with an inflationary impact worldwide. With markets yet to pick up on the divergence, Manoj recommends SHORT USDCNH with noticeable downside expected later on. The upcoming rebound may not be a new dawn, but it will still be significant, so investors should stay LONG China equities.

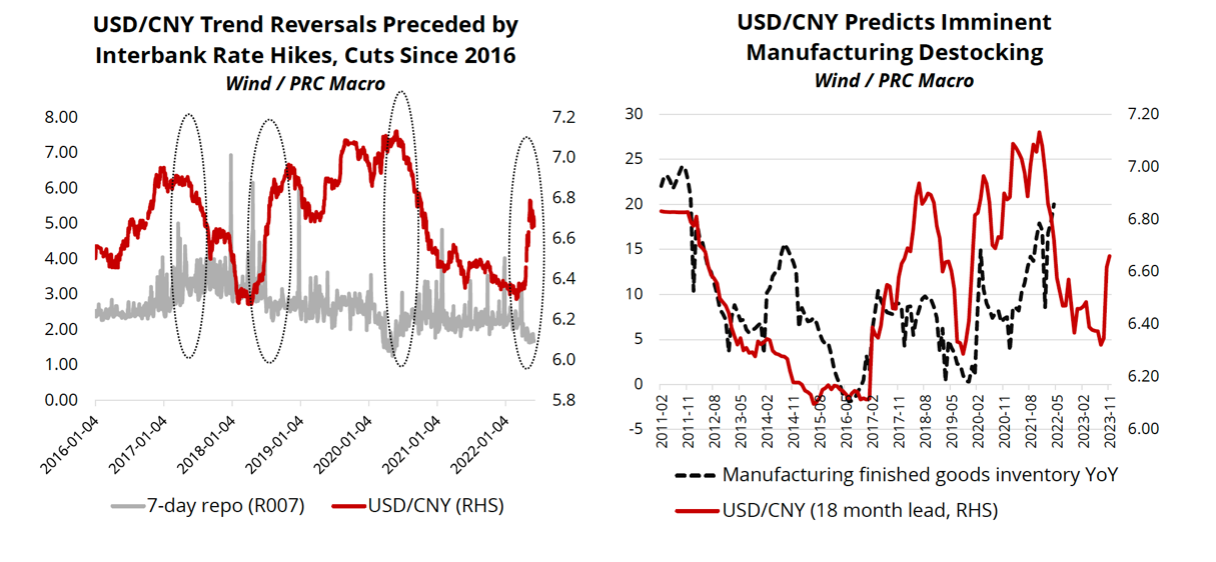

PRC Macro

China: RMB depreciation is not over yet

Since 2015 the RMB exchange rate has been primarily driven by PBoC interest rate policies (see chart 1). William Hess sees no intention for the PBoC to exit from its current pursuit of growth/asset price reflation. With greater correlation between USD/CNY and domestic asset prices & the inventory cycle since 2015, the current direction of USD/CNY causes William to be vigilant towards the sustainability of the equity market rebound and imminent risks to base metals prices from manufacturing restocking (chart 2). Expect USD/CNY to test the 6.9-7 threshold.

Oxford Analytica

The Middle East and Africa’s looming food crisis

Rising food prices were already an issue before Russia’s invasion of Ukraine, with the recent geopolitical shock raising the spectre of physical shortages in the MENA states. The shock could destabilise governments and tear at the fabric of societies, as was the case in the run-up to the Arab spring. An upcoming webinar hosted by Oxford Analytica will see a discussion on the drivers of rising insecurity and how the crisis will manifest across the region, and which countries are most exposed to instability. To find out more, please get in touch.

Teneo

Nigeria: Tinubu’s victory poses a risk to the governing party

Tinubu’s victory as the presidential nominee will come at a cost to the imploding APC party. Division is strong within the APC as many members will be inevitably aggrieved by the decision to elect Tinubu, who faces a difficult decision of who to select as vice-president elect, which may force him to trade influence for popularity or vice versa. As tensions grow, there is an increasingly serious – but not inevitable – risk that the APC will fall in the 2023 presidential elections.

Burumcekci Research & Consulting

Turkey records highest consumer inflation in 24 years

In May CPI increased by 2.98%, below the median expectation of 4.55%. The significant acceleration in price increases were sourced by the increases in both food and non-food groups, with the reflection of the depreciation of TRY and the increase in energy prices. Thus, Turkey’s annual inflation increased to 73.50% in May from 69.97% in April 2022. While this was the new historical peak of the 2003-based index, it was the highest value since October 1998 (76.6%) in the 1994-based index.

Commodities

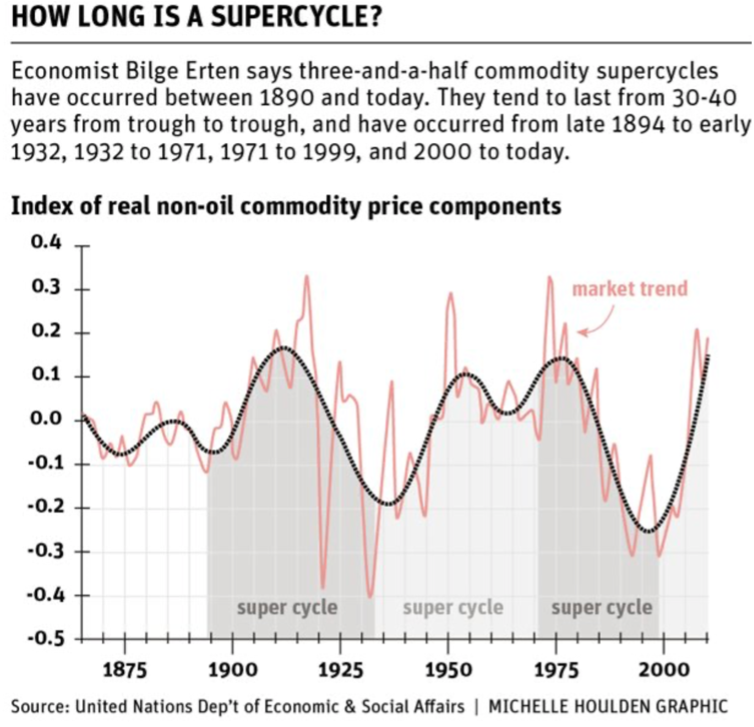

Commodity Intelligence

Where is the commodity supply?

We are in the best bull market of Mark Latham’s career, he claims. There is no supply and the focus on transition, net zero and green inhibit the normal capex response. Exploration activity for oil rigs is pathetic and small. Mark wonders if Brent could even go to $300 and ponders the existence of a long-drawn out commodity supercycle (see chart). He recommends as much coal, oil and natural gas exposure as possible in investor portfolios, and advises on Alberta, Texas and Australia as ideal locations to make excess return.

Rosenberg Research

Lucrative lithium?

David Rosenberg’s latest report examines the opportunities & challenges in the market for “white gold”. David mentions growing projects in the US and future opportunities in countries with large untapped reserves including Australia and Brazil. Over the near-term, opportunities can be found in the lithium battery spaces as government support and increasing demand provides a tailwind. Alternatively, one of the best ways to gain exposure to the sector is through lithium-targeted ETFs, such as the Global X Lithium & Battery Tech ETF. There are short-term trading opportunities, but David warns there will not be a long-term secular uptrend in prices.

Global Macro Investor

Things are ugly in the crypto world, but that’s to be expected

Recent events in the crypto world haven’t dissuaded Raoul Pal, who explains that his crypto investments are a long-term secular trend that will play out over the rest of the decade. Right now, we’re experiencing inevitable volatility. He compares Bitcoin to Amazon, with the former providing a superior risk-reward for investors who suffered through the volatility. The same goes for Ethereum with a higher Sharpe Ratio of 1.6 to Bitcoin’s 1.31 since 2015. Don’t let the short-term pain dissuade you and stay LONG.