Company & Sector Research

Europe

Forensic Alpha

Papering over the cracks - longer-term earnings power is being overestimated creating a compelling short opportunity. Forensic Alpha’s 15-page report focuses on the wind turbine manufacturer's lack of development spend vs. competitors and how the growth of Chinese manufacturers puts it at a competitive disadvantage. Furthermore, following the release of Nordex's annual report, Forensic Alpha’s MI system flags several accounting issues / assigns the company the maximum risk score.

the IDEA!

In the box seat - one of the best positioned companies when it comes to a switch towards OOH delivery. Previously critical of INPST’s overpriced IPO, the IDEA revisits the investment case in this 71-page deep-dive with a focus on cost inflation for the last mile which is particularly affecting the to-door segment. With the shares trading at less than one-third of their all-time high the current valuation looks very attractive. Investors should not rule out a takeover which would offer further upside to the IDEA's TP of €8.91 (40% upside).

Insight Investment Research

Strong, high visibility FCF with rising tenancy ratio - Robert Crimes increases his TP to €56 (90% upside). Revenues +7% CAGR (2022-26E), driven by inflation escalators, new organic POP growth on existing sites and BTS sites. While Robert expects some near term margin pressure this year, he forecasts a swift recovery in FY24. Dividend yield to increase from 2.9% to 7.8% (FY26E). There is also plenty of firepower for acquisitions with Inwit seen as an attractive target given its FCF growth, strong market position and undervaluation.

Drewry Maritime Financial Research

Shipping: Dry Bulk remains the best bet heading into 2H22

DMFR are bullish on dry bulk shipping stocks as demand for dry bulk vessel is expected to expand by 3.8% in 2022 and a further 4% in 2023 amid strong construction and infrastructure activities in emerging economies. Whereas the fleet will increase at a modest pace of 2.2% over next two years. Additionally, the disruption in exports from the Black Sea will add tonne-mile demand as importers will source grain from farther countries, boosting rates after 2Q22. Vessel earnings are expected to remain well above break even across vessel class.

Entext

The metal recycling market size is expected to reach $370bn by 2030 (from $220bn in 2020) - NDA looks well placed to benefit. €3.8bn M/Cap, sub 5x PER and near 2% yield, Sean Maher believes the closed loop potential isn’t remotely discounted and you’re being paid to wait for ESG funds to discover it. NDA recently upgraded its full year outlook having exceeded expectations last quarter. It has also started the test operation of a new pilot plant for lithium ion battery recycling in Hamburg.

Messels

FTSEurofirst 80 Index: Bullish & Bearish Themes

Recycling and Renewable Energy stocks such as Umicore, Vestas Wind and Siemens Gamesa are rallying from medium term support. Selective Seafood and Tobacco stocks remain defensive including SalMar, Mowi and Scandinavian Tobacco. Banks are generally rallying in ranges; favours CaixaBank and Sabadell which have already broken out and extend relative bases.

Industrials have broken uptrends and are now losing relative momentum such as Schneider, Atlas Copco and Alfa Laval. Luxury Goods renew their 4-month price and relative tops including Pandora, LVMH, Dior and Hermes. IT Hardware and Semiconductors renew their 5-month price and relative tops; SeSa, BE Semiconductor, Infineon and Nordic Semiconductor are highlighted.

North America

AlphaSituations

High conviction mis-valuation opportunity only emphasised by Warren Buffet's increased investment in Paramount Global - Robert Sassoon argues Netflix’s woes are company specific (reliance on streaming subscriptions has simply laid bare its vulnerabilities). By contrast, WBD, PARA and Disney have diversified revenue models, backed up with high quality content libraries. WBD’s debt burden is also less onerous than it appears (very attractive fixed rate terms and interest payments will be dwarfed by FCF generation prior to the first repayment dates in 2024). Attributing a PARA-like value multiple to WBD's consensus 2023 EBITDA offers 80%+ upside.

Valens Research

The combination of Ford’s cash flows and cash on hand should be sufficient to meet all obligations including debt maturities through 2028. Furthermore, the firm’s large M/Cap and moderate recovery rate should allow it to access credit markets to refinance, if necessary. Despite this strong credit profile, credit markets are grossly overstating Ford’s credit risk with a 5-year CDS of 377 bps and a YTW on its 2025 bonds near 5.5%, relative to an Intrinsic CDS and YTW of 71 bps and 3.5%, respectively. As a result, credit investors are being over-compensated for the risk they are accepting and Ford’s bonds could make for a good addition in a corporate bond portfolio.

Customer Growth Partners

After two years of stellar Covid era growth, BBY has seen a sharp and (so far) enduring drop in its traffic momentum - as the category leader, BBY would normally pick up the mantle of expanding or innovating the entire consumer electronics market. However, discretionary consumer spending is rotating to outdoor-focused spending ranging from sports and camping to travel and dining out. BBY must take bold steps to break out of its funk. New initiatives in health, fitness and finances may help, but it must keep bringing innovation to bear.

JJK Research Associates

Following a strong 4Q22 report and despite global macro headwinds / FX pressure, the company is poised to deliver +HSD F23CC revenue and $8.25 to $8.50 F22 EPS - JJK's bullish view is driven by positive new customer acquisition and tailwinds in the recovery categories of classic wear to work and special occasion apparel / accessories. Forecasts +HSD revenue in North America and Europe while APAC is tracking at +LDD, with F23 EBIT margins poised to reach the F24 mid-teens goal. Investors should also expect an acceleration in share repurchases / dividends with RL's $2.5bn cash hoard set to increase further, driving total shareholder returns higher.

R5 Capital

Opportunities such as this do not present themselves very often - the combination of a failed merger and fears around the economy have pushed the equity much lower over the last year (down ~50%) leaving the stock priced at a ridiculously low 7x PE and 3.5x EV/EBITDA for FY22. This is something that might suggest a distressed operator, yet the company has virtually no funded debt. Moreover, there are good prospects for SPWH to grow sales and earnings above what was seen pre-pandemic (Scott Mushkin highlights new store pipeline, improved productivity, increasing omnichannel penetration, growing loyalty program). TP $24 (160% upside).

Veritas Investment Research

Current share price implies a ~6.0x multiple to Nigel D’Souza’s medium-term core earnings forecast (~30% discount to peers) - Nigel views this discount as unwarranted given MFC's strong capital position, positive cumulative policyholder experience during the pandemic, stable insurance earnings, and lower sensitivity to market declines. Nigel’s report includes details on the effects of IFRS 17, as well as an analysis of MFC's assets under management, Asian and Covid pressures and LICAT ratio.

Paragon Intel

Concerns surrounding the appointment of Jorge Gomez prove justified as the new CEO lasts one day on the job after probe at former company. Last month, Paragon Intel described Gomez as a "Career underperformer" - his career alpha destruction is nearly (-103%) compared to outgoing CFO David Meline who created positive alpha totalling +181% at all three C-Suite positions during his career. Gomez also has a history of concerning audit, financial, and governance red flags, enduring material impairments each year he held a CFO role dating back to 2018. His ManagementTrack rating is very low at just 2.5 vs. Meline's 7.6 and the platform average of 4.9.

Summer of disconnect as energy transition stumbles

Renewables are the future but the transition is being fumbled - due to the nature of its products Northcoast sees Generac (TP $292; 20% upside) as having the most near-term opportunity and Chart Industries (TP $209; 20% upside) winning as it benefits from the growth in small-scale LNG projects that are often used for utility load management solutions. Looking over the horizon, Bloom Energy (TP $23; 40% upside) and Capstone Green Energy (TP $7; 160% upside) will find success thanks to their unique power generation solutions.

ERA Research

LPX’s OSB earnings for 1H22 will be spectacular and 2H22 results should remain well above trend levels - OSB prices remain at historically high levels (but will move lower through quarter-end) and should housing demand pull back in late 2022 or 2023, downside for commodity OSB prices will be more limited than for lumber given the dearth of new supply coming to market in the next 12 months. In LPX’s siding business the biggest opportunity comes from displacing alternatives such as stucco and vinyl. TP $90 (30% upside) is based on a 5x multiple applied to a 50/50 blend of 2022E/2023E EBITDA of $1.5bn.

New Constructs

Data centres are dinosaurs - bulls have long argued that data centre operators, given their ties to data usage and the internet, deserve premium valuations. New Constructs disagree. They see poor / risk reward in both these stocks due to 1) Years of declining profitability. 2) Low pricing power in a commoditised industry. 3) Deep-pocketed customers becoming competitors. 4) Declining utilisation (overbuilding in good times). 5) Rising cost of commercial real estate makes improving ROIC unlikely. 6) Stock prices that imply immediate reversal in declining margins and years of above consensus growth. 60-80% downside.

Sales Pulse Research

Security channels continue to see strong growth for most vendors

While channels see security budgets as strong for the rest of the year there is concern that the time required to implement some projects has become extended because of a lack of skilled resources. This may result in delays of add-on orders in 2H. US Fed spending which had seen some delays due to operation under CR (Continuing Resolution) is now back on track. Sales Pulse has also found no evidence that Okta lost accounts following its recent breach, however they did hear of some new deals being delayed. Other stocks featured include CrowdStrike, Palo Alto, SentinelOne and Zscaler.

Australia

Global Mining Research

In GMR's view DRR remains well over-priced, although it is easy to see some positive features that have made it a “darling” of the Australian investment community (linkage to production growth is good and as a pure royalty play it has lower risk than regular miners). However, LIF trades 30-50% cheaper (depending on the metric used), has a much higher FCF and dividend yield, and sells a higher quality product. Even looking forward to 2026, when DRR has achieved its growth potential, leaves LIF a better investment proposition.

Japan

Tabbush Report

JPB is unlike any other bank in Japan. It is highly geared to rising US interest rates from its sizable investments there, including in CLOs. A structural decline in TEIGAKU deposits (which are longer term and higher cost than ordinary deposits) allows for better funding costs. This combination should lead to much improved NII, as interest income expands while funding costs decline. Daniel Tabbush also sees limited impairment risk and with improvements in core profit, JPB’s ROA delta can be significant given its 0.16% low ROA base. Meanwhile, the exceptionally weak JPY can further provide an impetus for increased JPY asset buying from USD holders.

Emerging Markets

RedTech Advisors

Worst is over on the China regulatory front: 4 high conviction long ideas...

Haidilao (6862 HK) - This hot pot chain is ideally placed to benefit from the 'Great reopening of China'. RedTech’s latest consumer survey’s indicate strong demand and long-term growth opportunities.

BOSS Zhipin / Kanzhun (BZ US) - Continues to be sold off as a targeted victim of the government’s crackdown, but as a market leader in job recruitment its interests should be very well aligned with the government.

JD.com (9618 HK) - Low regulatory risk and as incomes rise and tastes move up market, JD is well positioned to capture those upwardly mobile consumers.

JD Health (6618 HK) - Key regulatory obstacles will be swept away in the coming 1-2 years and the combination of JD’s userbase and JD Health’s one-stop digital offering should position it well to ride the wave.

Silk Road Research

China: Elevator channel checks & dealer feedback on Auto stimulus

Elevators - Order activity much better than SRR was expecting. 2Q22 industry orders tracking in the negative 10-20% range through April. Infrastructure outperformed residential, but even residential was reported within the down <20% range. First clear evidence since the recent lockdowns of government policies to support the economy having their intended impact.

Autos - Purchase tax reduction policy news is significant. First national-level auto stimulus announced since 2015-2017 and its “time-limited” nature will be key to stimulating near-term demand. Consensus expectations among industry participants are for a purchase tax cut of 50% (i.e. from 10% to 5%) for ICE vehicles <1.6L engines for 2H22.

Copley Fund Research

The China Rotation: Allocations hit 4-year lows

Allocations in China & HK equities among active EM investors have plummeted 10%+ in the space of 18-months (India, Taiwan and Mexico have been the biggest beneficiaries) - on a sector level, China Industrials and Consumer Staples are the overweights, with managers rotating into Financials and away from Consumer Discretionary. On a stock level, Alibaba remains a core holding; out-of-benchmark AIA Group and Midea Group are popular, and for Value managers, China Mobile and CNOOC are key overweights. Active managers have stayed away from both NIO and Xiaomi, so pressure to invest on the grounds of benchmark tolerance should be disregarded.

Macro Research

Developed Markets

AAS Economics

Forecasting PPI

According to Frank Shostak, there is a strong predictive relationship between movements in Adjusted Money Supply (AMS) growth and subsequent changes in Producer Price Index (PPI) inflation. In light of a decline in lagged AMS rates over this period, he forecasts for much of the steam in PPIs to begin to release in H2/2022 and especially into 2023. Chinese lockdowns and the Ukraine invasion may bring about some overshoots, but the underlying forces are for a significant moderation in PPI inflation ahead (see charts).

Andrew Hunt Economics

UK: Slowdown evident

The UK monetary environment is weakening. The rising funding burden on the non-bank sector and high inflation suggests upward pressure on Gilt yields, but the weakening economy indicates a move in the opposite direction. In practice, Andrew Hunt believes Gilts won’t be able to disconnect from US Treasuries, but the monetary environment suggests that the peak in Gilt yields should be towards year end and perhaps sooner than that in T-bonds. Sterling does not appear particularly cheap or expensive, but it could prove vulnerable if the latter scenario plays out.

Economic Perspectives

UK: Fiscal tightening has pre-empted monetary tightening

As recently as March, the OBR endorsed a forecast of economic expansion in 2022-23 that would have allowed the UK’s budget deficit to fall to around £50bn per annum in 2023-24. However, the abrupt loss of economic momentum and the rapidly mounting debt interest bill together imply fiscal tightening on an eye-watering scale this year. Unless the UK fiscal stance is relaxed materially and quickly, Peter Warburton claims there is minimal scope for the Bank of England to raise interest rates without sending the economy into a deep recession.

Blonde Money

UK: Goodbye, Boris

Helen Thomas’s analysis of Conservative MPs identified a number of relatively quiet and moderate backbenchers loyal to the party, but not necessarily the leadership, who have been waiting for Sue Gray’s report before taking action. We won’t see the required 54 letters of no confidence in Boris Johnson this week, but the drip-drip of bad news and unenforced errors, exacerbated by an even more hubristic Johnson, will ensure he does not lead the Conservatives into the next election.

Eurointelligence

Another shock heading towards Germany

Leaked photos of Chinese torture of Uyghur prisoners have had a profound effect on Germany, prompting politicians to call for a change in their China policy. Wolfgang Münchau comments that the sheer degree of rupture in German politics is breathtaking; the previous coalition’s policies on energy and bilateral relations with Russia have turned into another dark chapter for the country, and its pro-China policy is heading the same way. Wolfgang sees a slow-moving train wreck ahead with massive consequences for German industry and for Olaf Scholz.

Minack Advisors

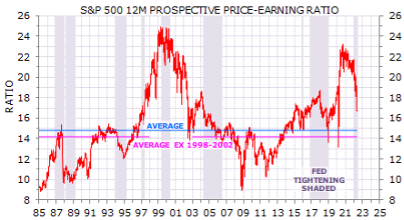

US earnings forecasts are too bullish

Equities are falling largely because tighter policy is compressing valuations, but US markets look vulnerable to a second leg lower if earnings forecasts are cut. Gerard Minack believes current forecasts are so optimistic that earnings estimates could fall even in a muddle-through scenario with no recession. This would be more of a problem for US equities than non-US markets. Equities typically de-rate when central banks tighten. The chart below shows the prospective PE on the S&P 500, with periods of Fed tightening shaded.

Longview Economics

US: Playing the SPX on weakness

Weakness in US equity markets was again centred on tech and growth stocks this week. Chris Watling believes there are signs of seller exhaustion appearing, especially as some stocks are seeing their 10-day MAs inch higher, and his risk appetite models are moving rapidly towards BUY levels. His 1–2 week short-term equity trading recommendation is to move LONG June S&P500 futures on weakness, 1/8th long at 3,855, with a further 1/8th position at 3,805. Place stop loss 4% below combined entry.

JST Advisors

AUDNZD trade has a lot of optionality

For a decade AUDNZD has traded between parity and ~1.10, but Jonathan Turek believes the catalysts for a range break higher are in place. Jonathan refers to the stubbornness of the 1.10 level even in light of recent global events and the level of divergence in the relative current account (see chart), the central bank convergence between the two and how this affects future rate movements, and also the potential for significant AUDNZD upside if global growth survives. The trade provides optionality to a cyclical theme, a structural theme (commodities) and for Chinese reopening with stimulus. He is LONG AUDNZD.

Emerging Markets

Totem Macro

Latin America anti-populism

Latin America is home to several reformed debtor commodity-driven EMs and a number of Whitney Baker’s most bullish inflation-hedge positions. Whitney has held most of these positions through last year, anticipating a huge commodity surge. But as the nations received their huge windfalls, their stocks and currencies barely moved. Whitney blames the flare-up of leftist populism in the region. As the politics shift back to the right, we’re starting to see accelerating inflows, which should close the wide asset disconnects via meaningful outperformance. Whitney remains LONG Chilean linkers, Brazilian two-years and Colombian tens.

Greenmantle

The EM debt divide

Niall Ferguson comments that rising rates in DMs and a strong USD usually spell trouble for EM debt. However, Russia’s invasion of Ukraine has shielded some EM commodity exporters from fiscal problems. Major energy and food exporters with stable fiscal foundations will perform best in this environment. Niall sees opportunities in Brazilian USD-denominated sovereign debt through year end despite election risks. He is bearish Turkey, Argentina, Hungary and Poland.

PRC Macro

China: Piecemeal stimulus a bull trap for commodities

William Hess claims that most of Prime Minister Li’s recently announced measures are just piecemeal fixes with limited funding. Although he expects Li and others to push for bolder stimulus, he believes the pro-growth camp has not achieved a decisive majority in Beijing. Ultimately, this sets up a bull trap for commodities. The longer the delays on easing Covid policies and on stronger measures to support fiscal spending and the property sector, the bigger the macro hole that will need to be filled.

Alberdi Partners

Colombia: Petro’s radical agenda would spook markets

Marcos Buscaglia compares the economic proposals of the three main contenders in the upcoming Presidential election: Petro, Gutierrez and Hernandez. The left-leaning Petro, currently leading polls, has the more radical proposals which include a considerable increase in tax pressure and full transition to clean energies. The other two represent a much more moderate and market friendly agenda. Even if he would have problems in implementing reforms, Petro’s relatively radical agenda is enough to spook markets in the event of a victory.

Alef Advisory

Egypt: Risks remain in the medium- and long-term

GCC aid is crucial for Egypt, but Hani Sabra claims not all is rosy; the GCC will not be as generous as in the past, and what the member states really want are valuable Egyptian assets on the cheap. Hani also remains unconfident in the authorities newly stated commitment to privatisation. The country will remain stable over the short-term, bolstered by an eventual agreement with the IMF, but political dynamics threaten this in the long-term - especially once the currency value drops in a few months and inflation intensifies.

Burumcekci Research & Consulting

Turkey: Higher and higher

In the week of May 20, Haluk Burumcekci estimates that the total reserves of the CBRT decreased to $100.3bn and its net reserves to $9.6bn in the week of May 20. In the May Market Participants' Survey, the year-end inflation expectation for 2022 rose to 57.92%, for the next 12 months to 33.28% and for the next 24 months to 19.54%. Haluk also comments on the rate of increase in housing prices reaching new records, with the NRPPI reaching 116.5% annually, but investors can expect it to climb even further.

ESG

Beacon Policy Advisors

US: The SEC takes on ESG

The SEC is moving to its next frontier in the climate regulatory space with new rules on ESG investing, which has been expected given SEC Chair Gary Gensler’s vocal and open intentions to require funds to back up their ESG claims. We could see increased transparency in sustainability metrics and standardised disclosures of ESG information. This comes as Gensler announced a $1.5m fine for BNY Mellon for misstating and omitting ESG information in mutual funds. Expect tougher enforcement with some inevitable pushback from conservative groups.

Krutham (formerly known as Intellidex)

Event: Driving ESG investments into emerging markets

Recent research overseen by Intellidex and MOBILIST has highlighted a growing tension between ESG investment strategies and flows to emerging and frontier markets. While ESG is often assumed to be supportive of development-oriented investment, this is not always true, and the extensive report written by Intellidex highlights how these stumbling blocks can be overcome. An upcoming webinar event on June 14th will introduce the findings of the report will host a panel discussion featuring leading institutions and experts. Please contact us to find out more.

Commodities

Greenmantle

Oil: Sanctions and Shut-Ins

Niall Ferguson’s base case remains that the EU imposes an oil embargo on Russia in the next month, most likely phasing out Russian oil imports by 1Q 2023, with potential exceptions for Hungary and other countries in Central Europe. The embargo increases the probability of US secondary sanctions on Russian oil - a greater threat to exports than the current diplomatic pressure being levied on Russia’s trading partners. In this piece, Niall considers the history of exports from Iran and Venezuela under different sanctions regimes to develop future scenarios for Russian oil exports.

Metals Focus

ESG in gold mining

Metals Focus’ new annual report, The Gold ESG Focus, is due for release in July. The extensive report compares a wide range of senior gold producers, including the likes of Barrick Gold, Endeavour, IAMGOLD and others. Looking at topics such as emissions, water, waste, biodiversity and health & safety, the report features “apple versus apple” ESG comparisons for the included companies. Please contact us to find out more.