Company & Sector Research

Europe

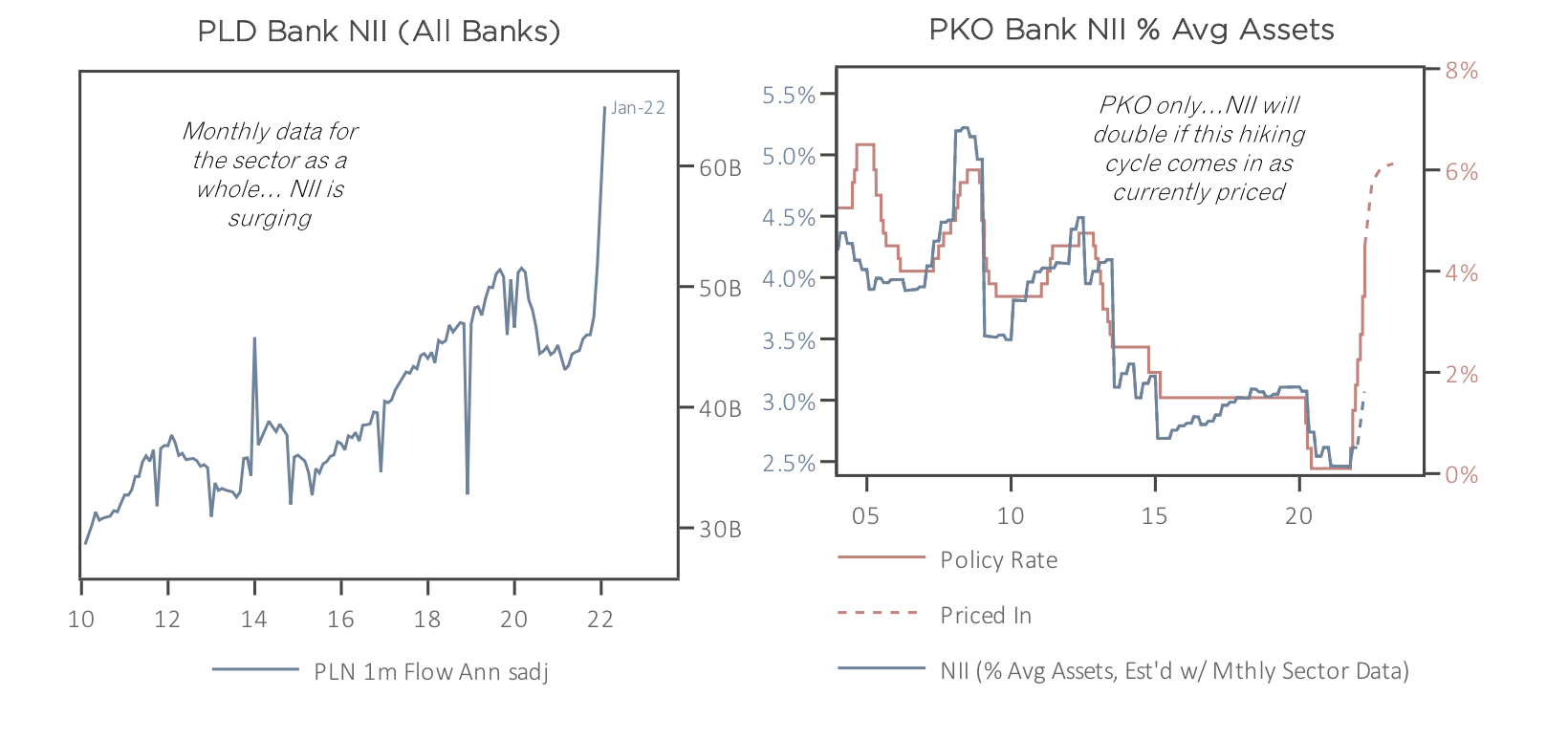

Signum Intel

Local mining rush

A global supply chain that sources components from different parts of the world, cobbling them together into products and then shipping them to end markets is unsustainable - this system looks increasingly risky and costly in a fraught, inward looking, slower growth and heavily bordered world. Signum Intel sees a move towards hyperlocal manufacturing as battery materials, metals, carbon and bacteria are reclaimed from the local environment: with four companies in the vanguard...

ResearchGreece

Spotting opportunities in Greek equities

Covering 22 names (80% of total M/Cap), ResearchGreece provides unbiased research, analysis and ideas on Greek (& Cypriot) equities. They offer a clear-cut, binary rating system: Own It (OI) or Do not Own It (DOI). Two stocks they are particularly keen on are…

National Bank of Greece (ETE) - Deserves to be trading at a higher P/TBV multiple than the current 0.50x; enjoys the highest FL CET1 among Greek banks; will benefit the most from a loan rate increase given its low L/D ratio; boasts the lowest combination of NPE ratio and NPE coverage.

OPAP (OPAP) - Q4/FY results comfortably beat expectations on stronger online contribution (Betting and Casino) and GGR/EBITDA guidance for 2022 points to ~40% growth Y/Y. In addition, the dividend was increased to €1.5/share (11% yield).

Galliano's Financials Research

Credit Agricole acquires a 9% stake in the Italian bank sparking bid speculation - Victor Galliano believes a takeover is highly likely and expects it to be at a similar valuation to the Credito Valtellinese deal, which implies 40% upside potential for BPM's share price. The Italian bank remains one of Victor’s 2022 High Conviction Ideas; not only a modestly valued potential M&A target, but its valuations are also underpinned by improving fundamentals.

MYST Advisors

Undiscovered “truly special asset” poised for meaningful growth acceleration - Qt is the go-to developer framework / toolkit for building software into embedded devices (car screens, medical devices, etc.). Transitioning from an open-source model to a subscription model; the subsequent ARPU uplift is anywhere between 45-80% depending on contract duration. Additionally, its Volume-based Business is beginning to accelerate as supply chain disruptions ease (grew ~40% in 2021). Qt’s impressive 30-40% 2025 CAGRs are likely to prove VERY conservative. TP €272 (120% upside).

Stockcube

Europe Weekly Technical Strategy

The Euro Stoxx 600 encounters medium term resistance at 440/450 with Stockcube anticipating a period of range trading - their Model Portfolio currently has 40 longs (avg. gain 9.3%) and 23 shorts (avg. gain 4%). Within sectors, they highlight Healthcare making new short term highs; Media testing short term resistance while breaking relative range resistance; Energy reasserting uptrends; Industrial reasserting short term downtrends and Technology reasserting downtrends. They recently opened a long in Air Liquide (makes new highs) and shorts in Saint Gobain (reasserts tops), Deutsche Bank (reasserts short term downtrends) and Vonovia (makes new lows).

North America

Busted Converts: Screening the HY universe for investment opportunities

Potential target list of $38bn+ of converts from over 70 issuers with an average YTM of ~15% when adjusted for the option value of each convert - with a recent back up in yields and credit given Covid / Ukraine war, there has been seen some price dislocation across the convert space which has created opportunities for investors looking for yield. Asterisk Advisors flags Beyond Meat which is a $3bn TEV plant-based meat company with $1.15bn of convertibles yielding 13% covered at market value by cash and covered over 5x by the equity value of the company, which they see as very interesting as these bonds are down 15 points in the last six weeks.

$5bn reasons why we’re watching Amazon's Project Kuiper

AMZN just made history with the largest commercial launch contract ever, cementing Project Kuiper as Starlink’s most formidable competitor - in their new 9-page brief, space sector analysts at Quilty Analytics break it down, focusing on implications to the sector at large, including the three big contract winners (Arianespace, Blue Origin, ULA), the GEO market (Inmarsat, Intelsat, SES, Eutelsat) and other heavy-lift launch operators (Firefly Aerospace, Relativity Space, Rocket Lab).

Abacus Research

Too cheap to ignore - this 35-page report focuses on why social media companies, especially Meta, look very attractive. Yes, there is a lot of noise around FB, but it is worth sifting through it as all the problems are short term in nature with plenty of free upside options. Abacus sees tailwinds for (sustainable) 10%+ revenue growth and margin expansion. Net income (GAAP) approximately doubles by 2025 from 2022 levels. The stock currently trades at close to intrinsic value; offers minimal downside with potential for 100% upside over 3-yrs.

Radio Free Mobile

Moving to subscription is going to hurt - slashing the price of its new Guide product, has ensured that PTON will lose money every time it sells a device. It has also reduced the subscription that goes along with Guide. While the digitisation of personal training is the right strategy, we are going to see a big correction in revenues and the reality is that the company is not really trading on a 2022 EV/Sales multiple of 2.2x but something closer to 6x or 7x. Richard Windsor continues to have no desire to go bottom fishing for PTON.

TobaccoIntelligence

Considers leaving the Russian market as it scales down operations - PMI cancels the launch of its heated tobacco device Iqos Iluma in Russia. It has also withdrawn plans to manufacture over 20bn Terea sticks for its device, losing $150m. Last month PMI, British American Tobacco and Japan Tobacco announced they would have limited investments in Russia, continuing their sales and domestic production. Imperial Brands was the only company halting domestic Russian production and sales & marketing activity across the country.

Veritas Investment Research

Canadian Banks: Tax grab

New bank and insurance company surtax unjustified - unfair to use pandemic earnings as a benchmark to support additional taxation. It is not a good look to attract foreign investment to the sector or for the sector's performance over the long term, given its importance to retirement portfolios and Canada's economy. Onerous taxation during 'good times' could hurt banks during 'bad times' and change the calculus on bank expectations for ROE through the full cycle. Bank of Montreal remains Nigel D'Souza's only Buy-rated bank of the Big Six.

Hedgeye

Speeds + Inventory + Covid → Peak Trucking. The easing of the Covid pandemic portends the easing of capacity constraints and crucially higher network speeds. Jay Van Sciver expects pricing momentum to reverse sharply through mid-year. He sees a repeat of the painful 2H18 inflection with falling rates, earnings and valuations. The trucking industry structure (highly fragmented, capital intensive, low barriers-to-entry that is characterised by low returns even in the best of times) makes it a great source of funds for short positions. Jay expects ~30% relative underperformance from KNX in 2022, and for truckers to underperform more generally.

Lynx Equity Strategies

Smartphone sector China demand risks are still not fully appreciated - consensus believes the premium end of smartphones will outperform the overall smartphone market, as they did in 2021. However, Lynx believes that this year, it will be the low-end of the price spectrum that outperforms. Ultra-low-priced 5G models will flood the developed markets (especially the US). A shift away from high ASP models is not good news for QCOM. The degree of weakness at China brands is also being underestimated (QCOM is heavily exposed). Even in the iOS domain, QCOM’s downside has not been fully priced in; expects Apple iPhone shipment in FY22 to underwhelm investors.

New Constructs

Poor risk/reward - priced for significant profit growth despite weak fundamentals. To justify its current price of $53/share, KBR must improve its NOPAT margin to 5% and grow revenue by 8% compounded annually for the next decade. In this scenario, KBR grows NOPAT by 17% compounded annually. Given that KBR’s NOPAT fell 8% compounded annually over the past decade, these expectations look overly optimistic. Even if KBR can achieve a NOPAT margin of 4% and a 5% revenue CAGR over the same timeframe, the stock is worth just $31/share today (40% downside).

Paragon Intel

New CEO Rick McConnell will profitably scale DT to a multi-billion dollar company - former colleagues describe McConnell as the perfect fit for the job because of his industry expertise and track record scaling businesses (Akamai and Cisco). Well versed in finance, product and go-to-market strategy, he will grow DT's business from $1bn to $5bn+. Unlike many of its high-valuation software peers, DT’s valuation reflects sustainable 30% revenue growth, 25% EBIT margins and strong >30% FCF margins. Forecasts EPS to increase 44%-65% from FY22-FY24, materially ahead of current estimates.

Gradient Analytics

Short thesis based on margin sustainability concerns and earnings quality issues - Gradient’s 12-page report focuses on 1) Smaller customers driving growth (increases risk of surprise sales declines from customer hardship). 2) Believes management may have pulled levers to optically improve operating margin. 3) Inventory has surged ahead of supply-chain threats. 4) Accrued expenses benefited TTM operating profit but could turn to a headwind. 5) Capitalised costs have surged. 6) Valuation metrics leave room for further downside.

Japan

LightStream Research

Transfer of Arm China shares does nothing but raise red flags - Arm moves its shares in China JV to a special purpose vehicle which it owns together with SoftBank. While this could technically eliminate the obstacles to an audit for an IPO, Mio Kato believes regulators would be remiss in allowing such a flimsy change to pass muster. In addition, the move reeks of desperation for cash and SoftBank’s typical disregard for prudence and the importance of due diligence to investors. Stay short.

Asymmetric Advisors

IPO'd in December but is quickly gaining analyst coverage because of its attractive growth prospects - KK is the global no.1 in undersea optical cable isolators. Ever expanding data demand is driving more cable laying and a rising number of bundles per line laid, meaning further strong growth prospects. Meanwhile, it also has close to 100% share in lead terminals for aluminium electrolytic capacitors for EVs. While its lead terminal business has traditionally been low margin, it can sell the lead terminals for EVs at 2-5x the price and as the ratio of its lead terminal sales that are used in EVs is rising rapidly, this will boost margins.

Emerging Markets

Arete Research

The time has come to simplify its confusing sprawl of assets with a series of spin-outs - Tencent Games could replace Activision as the largest global game content stock, worth $150bn, and this excludes its vast portfolio of studios, IP and private stakes. While Tencent will likely be obliged to put Fintech into a standalone Holdco., this creates an opportunity to spin out Cloud & Business Services; potential to be a $10bn business by FY26. Major stakes in Tesla, Meituan, Sea and Kuaishou are not required / should be unwound. Importantly, by taking decisive action, it would make it less threatening to the government and limit the impact of regulation across the group.

Niko Partners

Game licensing resumes in China

Positive sign for China’s video game market - Niko Partners forecast 500-700 games to be approved in 2022. Enforcement and compliance have become a major part of the NPPA’s role over the past couple of years and investors should continue to expect strengthening of policies and a crackdown on loopholes. Fortunately, ARPPU has been rising...this will be covered in Niko’s upcoming China PC Games Market and China Mobile Games Market reports, which will include a current market model and 5-year forecast, along with results of gamers surveys, interviews, trends analysis and M&A activity.

Tabbush Report

One of several high growth Asean banks that also offers a sustainably high dividend - TISCO was one of the banks that fared best during the Asian Financial Crisis of 1997 and its core income delta is exceptional. ROA is up from 2.37% to 2.94% over the past four quarters. This is not only credit costs. Margins moved from 4.92% to 5.33% over this time with strong growth in each of the past three quarters. An added delta for ROA expansion should be improved operating costs, which were uncharacteristically high during 4Q21 at 3.56% of assets. This can easily come in by 10bps+, suggesting dramatic ROA growth from multiple drivers, and it comes with a 7.1% dividend yield.

Macro Research

Developed Markets

CrossBorder Capital

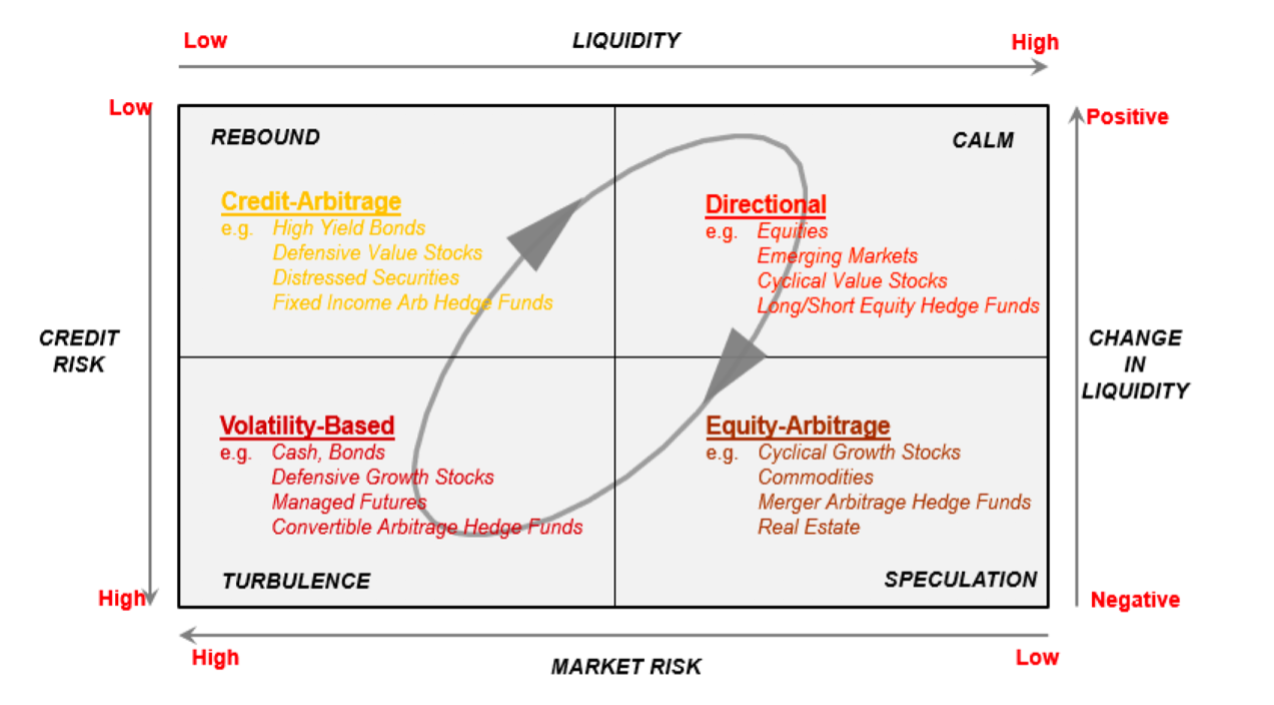

A turbulent investment phase is approaching fast

We are in a downswing that is fast approaching the investment phase Michael Howell dubs ‘Turbulence’, characterised by slowing and sub-par liquidity (see graph). In light of the backdrop, Michael claims investors are positioned too ‘risk on’ with extreme positioning seen across the Eurozone and Asian EMs. He favours defensive areas of investment markets, considers long-dated US Treasuries and reiterates the potential of ‘buying the dip’ in equity markets, although he fears it will be a large dip.

Andrew Hunt Economics

Germany: Growth fairy tales must be questioned

Economic growth is proving elusive in Germany. The rise in import prices has eroded household spending power and led to a marked deterioration in corporate cash flow. We’ve also seen corporates prefer financial surpluses over deficits in recent years, which will constrain CAPEX in the uncertain environment. Fiscal policy is neutral and monetary conditions have tightened. The outlook is weak, and Andrew Hunt wonders if we may see a repeat of the 1974 recession, also caused by a similar-sized commodity price shock.

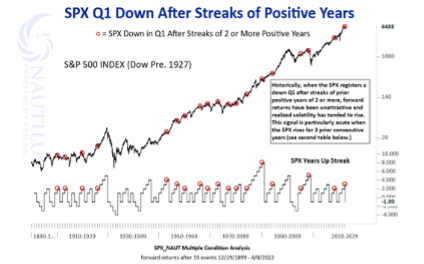

US S&P500 Index: Cautionary developments

Nautilus Research’s bearish outlook was especially heightened in recent weeks given the extreme backup in rates, the shock in energy and the hawkish Fed. They are also troubled by a first downward Q1 for the index following a streak of 2+ years, the weakness in transports, and concerning underlying trends. A major top has been registered and the recent strength represents a bear market rally; a break of the 12-month moving average (4475) could open a Pandora’s Box!

US: What you’re not hearing about who to blame for CPI

The White House blames high oil prices on the Russian invasion of Ukraine. Its anti-oil bias has to share culpability, but a geopolitical risk premium for the fragility of Russian supply is the main issue. Beyond oil, inflation's momentum has reversed, with key sectors like used cars contributing an offsetting element of deflation. The risk now is that the Fed will inadvertently cause a recession by fighting an inflation it didn't cause, just when it is proving to be transitory.

Click here

Quill Intelligence

Risks to Canada’s economy are rising

With inversions across Canada’s forward yield curve, Danielle DiMartino Booth senses that the reality of recession risk has been postponed, not allayed. The country’s Nanos Confidence Index was down 12% YoY in March with inflation concerns bubbling amongst households. Danielle also questions the popular narrative that Canada could replace Russian exports. With the 50bps rate hike on Wednesday, has the worst yet to come?

Longview Economics

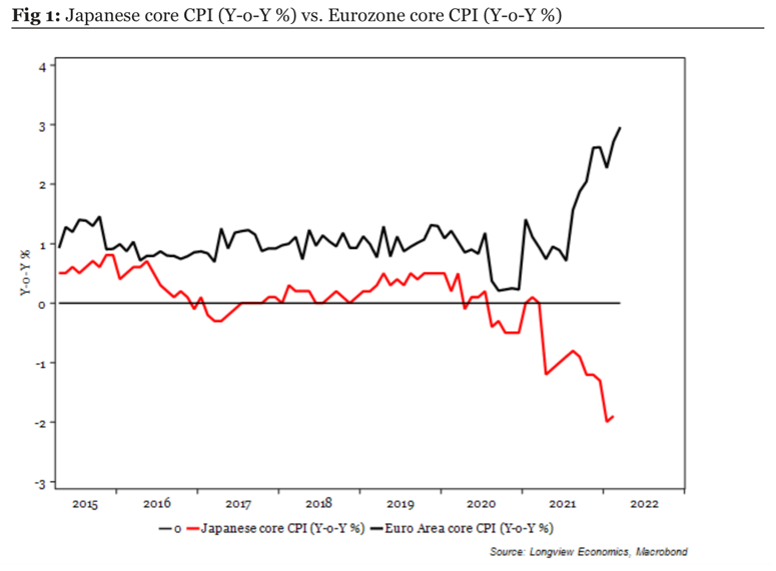

Japan, the odd one out

In contrast to the rest of the world, Japan continues to battle against a deflationary backdrop. Bond yields in Europe are moving rapidly higher whilst the BOJ reiterates its commitment to cap 10-year yields at 0.25%; of note, the 10-year JGB yield has tested, but not broken above, that level. Harry Colvin advises to move LONG EUR-JPY June futures with ½ the position at current prices and ½ on weakness. Place stop at 131.50 and risk 80bps on this trade.

Alternative Macro Signals

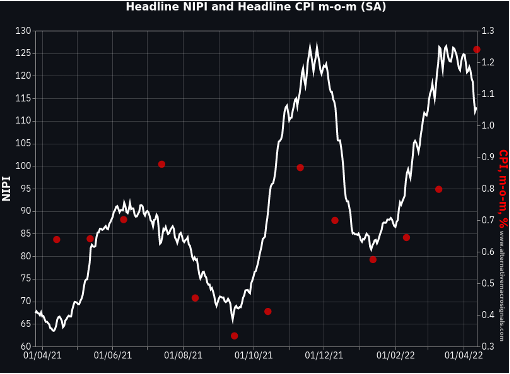

Predicting inflation

Alternative Macro Signal’s measures are used by central banks and hedge funds for inflation forecasts, inflation-linked assets trading and rates modelling/trading. Their News Inflation Pressure Index (NIPI), which analyses hundreds of thousands of news articles per day for positive and negative inflation news, has once again showcased its ability in forecasting inflation rates as it predicted recent strong US inflation (see graph).

Macrolens

Remaining bullish

Brian Mccarthy feels like his bullish call on equities is certainly being tested, but he remains confident that it’s far too early to be fretting about recession. He believes the yield curve will re-steepen a bit, that QT is of no concern, and points towards the positively sloped yield curve. The issue here is rampant inflation-phobia, whereby many investors are failing to consider scenarios of decelerating inflation rates, which Brian estimates could indeed be dramatic. The matter of fact is the market is using models of stock prices and yields that make no sense at all!

Emerging Markets

Greenmantle

China: Losing control of the Covid-19 outbreak

With the BA.2 variant spreading rapidly, Niall Ferguson believes that provinces accounting for most of China’s GDP will be locked down by May. Large-scale fiscal stimulus is coming to replace some of the lost economic activity, with restrictions on property developers and monetary policy eased further, but Chinese growth and mobility will nevertheless take a big short-term hit. Niall remains short oil and expects the China slowdown to be broadly deflationary for developed markets.

PRC Macro

China: The economic cost of the latest Omicron outbreaks

The latest outbreaks and subsequent lockdowns have had little impact on upstream industrial production, reaffirming William Hess’s bullish outlook for iron ore and coke. By contrast, domestic logistics and shipping has seen a big hit, with port shipping for domestic trade contracting by 24% YoY and cement shipping by 30% YoY. Expect the PBoC to ease more aggressively to prop up the property sector and initiate toxic asset purchases, including via a 50bps RRR cut in April, which will steepen the yield curve.

Entext

Stay long China tech

Back in March, the MSCI China Index saw its valuation halve in a year to about 9x 12mth forward earnings, vs the 5yr average of 12.6x. However, the sector is now a remarkably cheap leveraged play on a diplomatic resolution to the Russo-Ukrainian conflict, belated regulatory stability and a surge in buybacks and even PE deals among the smaller players. If China is perceived to be creating distance from Russia, and so avoiding sanctions risk, the rally in mainland tech names will accelerate in Q2.

Alberdi Partners

Chile: Stagflation intensifies

Uncertainty remains over whether Chileans will support the new constitution for Chile, but Marcos Buscaglia reaffirms his belief it will be approved. However, short-term issues remain at the forefront of Chileans’ minds as inflation rises and activity contracts. Marcos expects the nation to step into recession territory in H1/2022, with GDP inching down in Q1, Q2 and Q3. Expect the central bank to hike rates by 150bp again in May, leading rates to a peak of at least 9.25%, sending real ex ante yields to 5% by yearend - their highest on record.

Intelligence Research

Costa Rica heads into uncertainty as outsider Chaves wins run-off

The victory of anti-establishment Rodrigo Chaves has upended Costa Rica, one of the region’s most stable democracies. It reflects the electorate’s frustration with the ruling class, choosing to opt for the outsider over former President Figueres, a scion of the political elite. His victory could test the nation’s very institutions: his manifesto and behaviour has drawn parallels with authoritarian leaders, raising questions about Chaves’ commitment to playing by democratic rules.

Totem Macro

Polish banks are making money

Polish banks are turbo-levered plays on the rate cycle, trading at trough multiples, in a very cheap currency, which itself will benefit from surging rates and EU grant flows – hence why Whitney Baker sees them as the best incremental buy in the wake of Russia-related risk-off. Just look at the exploding bank earnings and Net interest Income (see graph). Whitney also postulates that the market is undershooting reality on the rates pricing, thus she remains SHORT Polish bonds.

Signal Risk

Cote d’Ivoire: Achi out

Prime Minister Achi tendered his resignation on April 13th to President Ouattara, a largely procedural decision so as to enact a long-touted cabinet reshuffle that will culminate in the PM’s re-appointment. The move could potentially improve government efficiency and address intra- and inter-party dynamics, although no shift in state policy orientation is anticipated in the near-to-medium term. As part of his aim to achieve middle-income status by 2030, President Ouattara is aiming for private-led, broad-based and inclusive growth and hopes for 7.25% annual GDP growth and US$100bn in general direct investment.

Commodities

Global Mining Research

Investment opportunities in iron ore despite uncertainty

Despite uncertain Chinese growth rates and hence iron ore demand, along with rising inflation and the Russo-Ukrainian war, David Radclyffe believes there may be more time to stay invested in the iron ore sector. With FCF yields remaining high for pure plays and diversifieds (~14%), investors should look for strong dividend yields (~9%) and cash returns this year. The big global diversifieds continue to offer better value than the pure plays, with Vale the preferred single entry, followed by Rio Tinto. For pure plays, David’s preferred exposure is Fortescue Metals Group, a non-consensus call.

Metals Focus

Gold to benefit from inflationary pressures and ongoing geopolitical uncertainties

Despite the unwinding of some geopolitical risk premium, gold continues to manage to trade at levels seen before the Russo-Ukrainian war. Not only does it reflect concerns over a protracted invasion, gold’s resilience also reflects growing fears about a Fed policy mistake. Expect gold prices to be supported in the following months, especially if rate hike bets are scaled back, although investors should be aware current levels will be unsustainable later in 2022.

Horizon Insights

Macro outlook supports copper prices

Commodities investments will be favoured by the prolonged US stagflation period, with robust clean energy sector outlook further bolstering copper prices. It is true that Chinese credit demand remains weak and that subdued consumption alongside a slow real estate sector recovery will drag on copper prices, but investors can be assured that low inventories and rising net long positions will limit copper price downside.