Company & Sector Research

Europe

Agency Partners

European Defence: Paradigm shift

€180bn bare minimum required to re-equip European armies to a standard necessary to provide credible deterrence against Russia - Agency Partners’ 31-page report explores this ‘rearmament crisis’ and which companies are best placed to benefit. Despite recent share price rises throughout the sector they still see a lot of valuation upside in European large caps. Preferred stocks include BAE Systems, Leonardo, Lockheed Martin and Rheinmetall. While European mid caps have fuller valuations, they offer much faster gearing to increased defence spending from short cycle businesses. Top picks include Saab and Babcock.

Forensic Alpha

Often finds itself at the top of Forensic Alpha’s rankings for aggressive accounting and this year is no exception with several new flags appearing following the publication of its annual report - the first thing that looks immediately odd is the sharp rise in trade receivables. A 45% increase YoY in the DSO, leaves it well outside of its historical range. Furthermore, while the receivables have been rising, the provision against those receivables has been falling. There is also a pattern of creating reserves as a result of acquisitions, then releasing excess provisions into income statement in future years. This pattern has strong echoes with what WorldCom did in the early 2000s.

the IDEA!

Compounding growth - recovery in Europe, ongoing strong performance in Latin America and accelerating growth in North America, boosted by the acquisition of Letco Medical, will push FY22 revenue and REBITDA ahead of consensus expectations. The performance of Fagron Sterile Services will be a major driver; FSS aims to grow average revenue per SKU by over 40%. Based on 2023 estimates, FAGR trades at 8.1x EV/REBITDA and FCF yield of 6.5%. TP €20.40 (30% upside).

Holland Advisors

While not as foolishly cheap as it was in the summer of 2020 (9x PE), today’s multiple of 18x (Apr 23) and offering ~15% p.a. return, looks very attractive whether we are in a 0% interest rate world or a 3% one. AHT continues to grow strongly across all areas; while its execution and articulation of its capital allocation model is exceptional. For all the market’s changing moods towards interest rates, war, growth, etc., a very large proportion of AHT’s future growth is within its own control as it enlarges its market position using its scale powerfully to do so.

TT Equity Research

H1 results may appear strong but weak disclosure raises many questions - since there is no competitive reason for the reduced disclosure, one must assume that the company is attempting to hide reality. DARK’s business model is built on its aggressive sales approach and financed by client’s prepayments. Meanwhile, management has no incentive to control costs. A lack of product development also puts pressure on the sales model. However, if they do lift R&D spending to the industry average, then the company will become a serious cash burner and the growth model no longer finances itself.

North America

Abacus Research

Fallen Angels: Sorting through the rubble

Short term pain, long term gain - three ideas where negative short term fundamentals are obscuring long term attractive businesses...

CoStar (CSGP) - No competition, plus headroom to increase prices. 2022 EBITDA margins will be ~27% vs. the 40%+ that the business should do as growth matures.

Etsy (ETSY) - Scaled, capital light, low SBC, and management team with a good history of execution. Take rates will rise longer term, thus revenue can compound faster than GMS.

Pinterest (PINS) - Not all users are equal; core users will be sticky and engaged. Worst case scenario the stock is worth ~$25, but in this scenario Abacus are ~50% below the street for EBITDA.

Behind the Numbers

Six companies at risk of inventory-related 1Q'22 misses

The current macro environment is bringing to the forefront the importance of the different impacts that the various inventory accounting methods have on company results during times of inflation. BTN have noticed several companies whose inventory levels have declined which may have shielded them from the full impact of rising costs. Meanwhile, their revenues have benefitted from aggressive price hikes. They believe this may be setting the stage for earnings disappointments in 1Q and 2Q 2022. Companies highlighted General Mills, The Coca-Cola Co, The Hershey Co, Post Holdings, Ball Corp, and Mondelez International.

Paragon Intel

CEO diligence report - evidence suggests Parag Agrawal will struggle to enact needed changes to TWTR’s organisation. Paragon Intel have assessed Agrawal’s capabilities and personality in the context of his ability to reaccelerate user growth, increase the velocity of new product introductions and tap into larger digital advertising pools: 1) Agrawal is a product-focused technologist with limited leadership experience. 2) He is well respected within the company, but ill-prepared to be the public face. 3) He is more contributor than leader and is unlikely to be a change agent. 4) Considered largely hands-off, he has not managed large teams or set goals during his tenure.

AlphaSituations

Activist excitement to be short-lived this time around - Robert Sassoon deems it unlikely that a PE firm will pay a much better than MSD multiple price for BBBY which is where the shares are currently trading. Even assuming the BABY banner spin-off scenario valuing BABY at $1.5bn, Robert's SOTP comes out to no more than $27. Given the uncertainty over how impactful Ryan Cohen's intervention will be in the long-run as well as the continuing challenging environment affecting BBBY's core business, chasing the shares at these levels is fraught with risk and not justified by the potential upside.

BWS Financial

Is in the final stages of turning a crude oil refinery into a renewable fuel refinery utilising camelina as its primary feedstock - GCEH has a patented camelina seed for refining into renewable diesel approved by the California Air Resources Board, making GCEH vertically integrated. The company has also obtained a product offtake and purchase agreement with Exxon Mobil for nearly all the production from its under-construction refinery, scheduled for commercial production later this year. The Series C Preferred funding completed last month gives GCEH capital to finish construction. It also makes XOM financially invested in GCEH. TP $7.55 (55% upside).

Portales Partners

Quality on sale - Charles Peabody sees 25-30% return over the next 12 months. He expects Q4’22 to be the transition quarter that ushers in a shift from negative to positive operating leverage and growth YoY in PPNR. 2023 EPS could come in closer to $13.50 a share (~$1 a share above Street expectations). This earnings power should support a 17% RoTCE. Charles expects TBV to grow toward $77 a share by year-end and $82 by year-end 2023. In addition, JPM has been unique in how it has managed its liquidity, not willing to extend duration; this will prove to be a competitive advantage in the current stress periods.

Smart Insider

A cluster of aggressive buying surfaced recently which includes the CEO, President, Co-CEO and two directors, spending a total of $8.7m at an average price of $59 - Bryant Riley (Chairman & CEO) spent $5m, Randall Paulson (Director since 2020) $2.4m, Kenneth Young (President) $590k, Michael Sheldon (Director since 2017) $502k and Thomas Kelleher (Co-CEO) $252k. Paulson, Young and Sheldon are all making their largest purchases. Smart Insider have ranked this stock successfully several times over the past few years and this is one of the most aggressive clusters they have seen.

Summit Insights Group

Best short ideas in Software

Former software engineer, Srini Nandury, who was the original bear on Nutanix and JFrog, highlights three names that continue to offer material downside…

Gitlab (GTLB) - Reminds Srini of JFrog; market fragmentation and intense competition will limit growth.

HashiCorp (HCP) - Growth to slow more quickly than investors realise; VMware catching on faster as it did with Nutanix. Stock could easily fall to $22.

UiPath (PATH) - Turned bearish with the stock at $70 last June. Expensive solution in a commoditising market; Microsoft is quickly vaulting to the leadership position in RPA.

Inflection Point Research, LLC

A Cloudy future is a good one - ANET is in a great competitive position, with tailwinds across all its end markets and product lines. Michael Fox points to the ongoing and accelerating networking upgrade cycles at Microsoft and Meta Platforms, in addition to greenfield business ramping at Alphabet as reasons to be bullish. Add to that share gains in an increasing TAM for enterprise / campus and you get the best networking growth story for the next two years.

Japan

New Street Research

Entering a golden age - this under the radar $100bn telco still has 50% upside. NTT is the 4th largest owner of data centres in the world. Japan’s data centre market is immature with only 7% of the capacity of the UK or US, population-adjusted, with most Japanese data currently held in regional hubs such as Singapore. New Street expects the Japanese government to introduce data localisation laws which will drive demand. At the same time, cost cutting will lead to material EBITDA upgrades. On a single digit P/E two years out, and with profit growth accelerating to HSD and LDD EPS growth, a sharp re-rating is likely. TP ¥5,000 (18-24 months).

Asymmetric Advisors

Hugely undervalued at 0.87x BV - massive order backlog, long lead times and high number of order enquiries, especially for its LiB seperator extruder machines, means potential for strong earnings growth for at least the next few years while operating profit margin can more than double. PER as low as 7x 3/24. A lack of analyst coverage means this stock is not as well-known as it should be. Also, it is cash rich and while management has been resistant to pressure for better pay-outs, as earnings pick up that pressure will only increase.

JapanConsuming

Keep track of Japan's Retail & Consumer markets

JC’s monthly report offers subscribers an easy, fast way to keep up with key trends, deals, marketing ideas, competitor strategies, and all the latest store and consumer data. Top stories from this month's edition include: 1) Seven & I sells Oshman’s to ABC Mart - clear sign that it is beginning to tackle its legacy operations. 2) Aeon Mall looks to experiences to get people into its properties. 3) Workman to open in Ginza; paves way for next big expansion. 4) Omnichannel accelerates in fashion: 40% of eCommerce sales from staff blogging. 5) Subscription retailing goes mainstream.

Emerging Markets

RedTech Advisors

A reversal for China CGB

RedTech’s latest eCommerce survey finds consumers switching back to traditional eCommerce platforms - the underlying rise of groceries in eCommerce remains in place, though, and this may be a temporary reversal of the trend toward community group buying. The low prices that drew consumers to CGB and local service platforms are now rising, taking away some of the appeal, and smaller platforms without a deep-pocketed parent company are pulling back from underperforming markets, while larger platforms like Pinduoduo and Meituan have lost market share.

Creative Portfolios

Value pick underpinned by fundamental momentum and lower risk - while GEM investors tend to prefer expensive bank franchises within Indonesia’s innovative financial ecosystem, Paul Hollingworth thinks they should instead be looking at much improved BBTN - FV of 6%, PBV 0.88x and Earnings Yield of 13.5%; the bank commands a sky-high PH Score™ of 10. A well-managed state-controlled bank dedicated to mainly collateralised mortgages (77% of portfolio), BBTN continues to benefit from the government’s Housing Loan Liquidity Facility. FY21 results showed positive momentum in Profitability, Efficiency, Liquidity, Asset Quality, Provisioning, Capital Adequacy and NIM.

Horizon Insights

The development of OA software in China

Strong demand will persist on the back of a vast customer base, resulting in a massive market with huge growth potential - the core critical success factors of the Office Automation software industry include the capability to standardise products and the ability to rapidly expand sales channels. As one of the industry leaders Weaver Network looks set to thrive. Its current product matrix can meet the needs of enterprises of all sizes in terms of deployment methods, implementation delivery, customisation, etc. Horizon Insights estimates annual net earnings growth of 30% in 2022.

Aequitas Research

Indonesia's biggest tech firm set to raise $1.25bn in local IPO ahead of US listing later this year - GoTo was formed in May 2021 following a merger between two of Indonesia’s largest unicorns Gojek (ride hailing) and Tokopedia (e-commerce). In 2021, GoTo had 2m+ drivers, 11m MSME sellers, 100m+ MAU and accounted for 2% of the national economy. The combined entity has been registering decent growth, but profitability remains less than optimal, to put it mildly. GoTo will have to trade well ahead of local and international peers to justify its desired valuation, something that Sumeet Singh is not convinced that it will manage to do.

Macro Research

Developed Markets

Totem Macro

Forces are aligning for a violent yield move

We already have unsustainable low yields, unsustainable liquidity, and bubbles across deflation-beneficiary markets in the USA and elsewhere that have grown to gargantuan sizes. Those extreme disconnects were only viable as long as inflation and discount rates remained suppressed, explains Whitney Baker, but the economic conditions for this are long dead and the market is turning a blind eye to an imminent massive bubble deflation. There are problems on all fronts for bonds, which Whitney delves into in her latest report.

Longview Economics

Eurozone: How high is recession risk?

Bearishness of Eurozone macro outlook has risen sharply, but Harry Colvin believes there’s a robust case for ongoing strength over the next 1-2 years. The large cash buffer of Eurozone households will absorb higher energy costs; house price increases are resulting in a strong wealth effect; real household income growth should accelerate; companies are cashflow rich; and monetary policy currently remains loose with signs the credit cycle is turning up. The case for ongoing cyclical strength is strong.

Forefront Advisers

Eurozone: After Versailles - Roadmap to new EU borrowing

Despite a lack of Recovery Fund 2.0, the Versailles summit could still be the first step towards new EU borrowing with an agreement reached as soon as June. This will involve the repurposing of some €150bn of existing EU funds to finance the transition away from Russian gas. Expect a top up of the European Peace Facility when it comes to bolstering EU defence spending. Meanwhile, in the face of soaring energy prices, expect the Commission to suggest a state aid regime and support windfall taxes on energy companies.

US S&P500: A frightening first fifty days

The market rebound after some positive news over Ukraine has underscored the oversold conditions outlined by Nautilus, and the +10% six-month S&P500 returns dovetails with their analysis of near-term strength following bear market declines. Longer-term investors should take solace in improving risk appetites: the S&P500 was still down more than -10% in the first 50 trading days of the year. History tells us that that will mark a significant mean reversion soon, with three-month returns averaging +11.50%.

RDQ Economics

US: Fed projects much steeper funds rate path

New published Fed projections include a median fed funds rate projection in 2022 of 1.9%, 2.8% in 2023 and 2.8% in 2024. John Ryding explains that these massive forecast revisions show that FOMC participants have finally decided to present a more realistic, rather than hopeful, outlook for inflation. However, he believes the Fed will nevertheless have to push its target rate above 3% to get inflation back on track towards 2%. Expect the May meeting to indicate details on the plans to reduce the balance sheet as the Fed sets course for tight policy in 2023.

Quill Intelligence

US: Industrial recession retrenches

Record semiconductor inflation is underpinning a higher core CPI and provides convincing evidence for Fed lift off. However, there is surprising and abrupt weakness in the Empire Manufacturing survey; shipments-inventories spreads fell to -28.9 and new orders-inventories fell to -32.7, with both negative for a third straight month. There is growing evidence the US is in an industrial recession; a further reduction of industrial exposure should be in the offing.

Aitken Advisors

Why you may want to go LONG Australia

James Aitken comments on Australia’s resilience which suggests that the costs of a decoupling from China are far lower than many assumed. That fact will not go unnoticed by other countries or blocs (like the EU) that have differences with China. The ground is potentially fertile for Australia to become the world’s most trusted supplier of both commodities and renewable energy. Is the structural short in the AUD the largest, convex wrong-way risk in global currency markets?

Emerging Markets

Talking Heads Macro

For inflation and the Fed, China lockdowns are a bigger threat than Russia

Manoj Pradhan believes that if China lockdowns spread further the Fed would have to tighten by even more than with a sustained Russia shock. The latter is an outright supply shock that raises inflation but brings down growth. On the other hand, if China lockdowns extend and demand in DMs only have to deal with central banks that are woefully behind the curve, the supply-demand imbalance will go much further and lead to a painful cycle. The recession watch must continue, Manoj warns.

Horizon Insights

China: Panic Sell

We’ve seen the biggest sell-off of Chinese stocks since 2008 across all sectors, happening in liquidation style. It’s panic selling. The concerns of investors simply do not justify the scale and scope of the sell-off; worries over lockdowns, economic slowdown and the ADR delisting threat are overstated. So, who will lead the rally back to normalcy? Leave aside the tech giants and look instead at local, smaller businesses and companies aligned with policy goals, including healthcare, mass consumption and green energy.

Macrolens

China is all in on a Sino-Russian partnership for a new era

Russia’s invasion of Ukraine will have no significant ramifications for China, claims Brian McCarthy. The two nations share an elegant symbiosis: the commodity superstore coupled with the most finely-tuned manufacturing powerhouse the world has ever seen. Recent events have allowed the internationalisation of the Yuan to move from being a pet project to an existential task and will mark the emergence of a Sinocentric trading bloc. A new financial iron curtain is rising and we’re on the weaker side of it this time.

Alef Advisory

Egypt: There will be a currency devaluation this year

The dynamics in Cairo are even worse than expected. In the fallout of Russia’s invasion of Ukraine, business sentiment is ailing and many are feeling the squeeze. Egypt will apply to GCC for aid, but an insufficient amount will force it to turn to the IMF. Expect a currency devaluation soon after Ramadan. Although the authorities will escape a politically destabilising backlash for now the current political system is unsustainable in the long-run.

Inferential Focus

The fight for Latin America

China has ended the Monroe Doctrine, claims Charles Hess. We are seeing a geo-economic fight for influence in Latin America between the US and China, with the latter ramping up support to nations who have endured the IMF’s restrictions. New left-leaning leaders in the area will be able to play both parties against each other for their economic advantage. With this power in their hands, along with new and surprising approaches to policy, we will see considerable expansion in the region in the near future.

Krutham (formerly known as Intellidex)

South Africa: The economy is still not right

There are too many sectors contracting as others grow, reflecting an increase in the volatility of sectors moving in different directions. Peter Montalto retains his 2.1% 2022 GDP growth forecast, but risks are clearly tilted to the downside most especially from loadshedding - telecoms and renewables infrastructure support may also see delay risk. His estimate does include the global demand shock from Russia-Ukraine, but this will be offset by increased demand for SA coal and other minerals.

HCWE & Co.

Turkey on the menu

HCWE & Co. offer a frequently updated Emerging Market Selector, using market signals of economic growth, inflation, relative valuation and currency “surprise” to generate a rating of country forecasts and their favourability. In Turkey, recent currency movements, equity market performance and aversion to prevailing economic trends have placed it at the top of David Ranson’s latest ranking.

ESG

View from the Peak

China is risking an ESG embargo over Russian support and Xinjiang

Is China facing a selling pressure based on governance? Paul Krake argues we could see a longer-term move towards private sector covert sanctions and investment embargos as major firms divest from Chinese assets (US pensions in particular). Currently, global allocations to Chinese stocks and bonds fall short of its economic might (MSCI has a 6% allocation despite China accounting for 17% of global output). The structural bull scenario was that this gap would be closed, but Russia and Xinjiang make it highly unlikely in the years to come.

Commodity Intelligence

An ESG inversion in coal equity

Amidst the recent market freefall and chaos there is an anomaly… Coal India. The unloved, long-ignored stock has risen over 16% over a period when others have seen their value halved, leading Mark Latham to comment on an amusing ESG inversion in coal equity: Coal India is trading at 7x EPS, Adaro 6x EPS, Whitehaven 4x EPS and Peabody at 3x EPS. In other words, the more pronounced the ESG narrative, the lower the PE!

Commodities

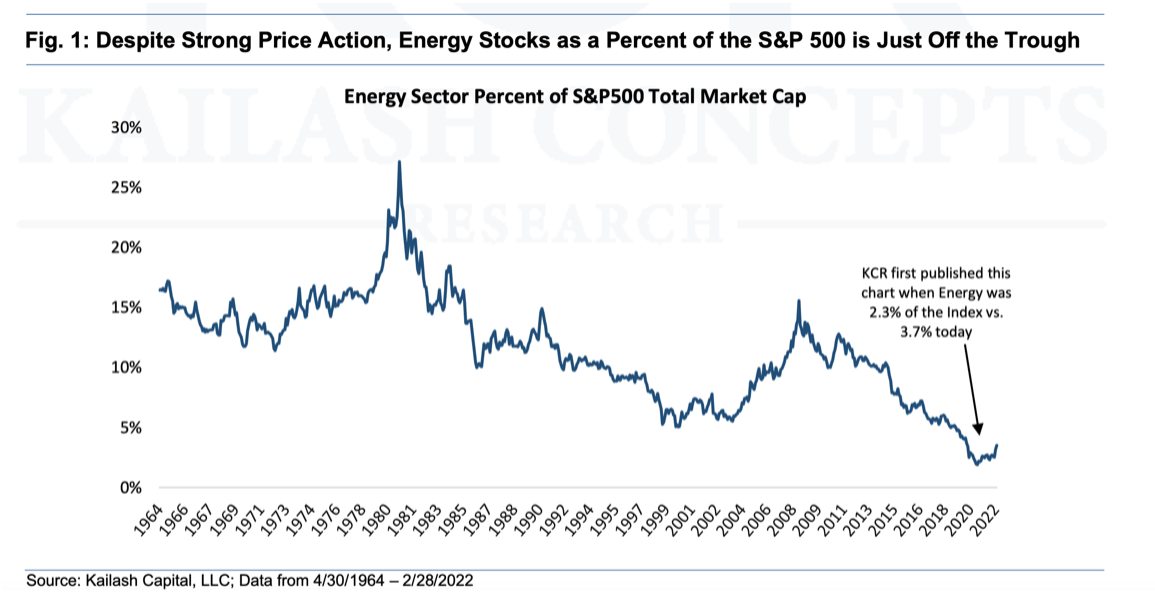

Kailash Capital Research

Undervalued energy stocks: The case for adding exposure

Energy stocks have even further to run. Incredibly, energy stocks continue to be the cheapest stocks in the market by a wide margin and have only been this relatively cheap once before in history. On top of this, oil & gas companies’ FCF yields are understating reality and investors are looking at the wrong companies! Recommendations include Devon Energy, Occidental Petroleum and APA Corp.

Global Mining Research

Nickel in turmoil after hitting $100,000 per ton

David Radclyffe’s team reviews the listed nickel equities in a world of increasing geopolitical and LME market tension, and volatile price swings that will continue throughout 2022. After a very large market deficit last year of ~130kt he estimates a balanced market in 2022 with price forecasts raised from US$7.45/lb to US$11.75/lb. There are very few investable nickel equities left, but GMR prefers IGO and Nickel Mines, and Vale among the diversified miners.

HED Capital Management

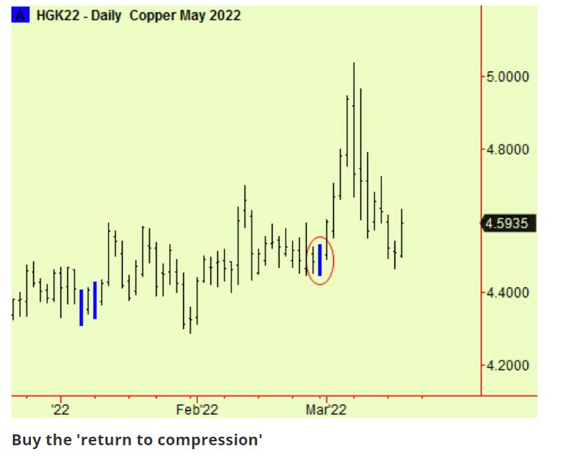

Copper starts a new upwards trend

Richard Edwards likes to remind readers from time-to-time about compressions; they act as attractors, the phenomenon known from mathematical complexity theory. When formed they signify a change in market dynamic is imminent. Recently, copper movements appear to be indicating a new trend having seen a rise, followed by a brief compression then a renewal of the increasing price. Copper becomes a BUY.