Company & Sector Research

Europe

AIR Capital

AIR’s portfolios outperform (again)

AIR’s Top 10 European Best Ideas portfolio has outperformed the Euro Stoxx 50 by a whopping +241% since launching a decade ago - the portfolio was +28% in 2021 (+23% in 2020 and +32% in 2019). Meanwhile, AIR’s Top 5 Swiss Best Ideas portfolio has also had a stellar start, having launched in Jan 2020, it has outperformed the SMI Index by +44%. One stock that Pierre Essig is particularly keen on at the moment is Spanish Auto Supplier CIE Automotive. At 10x 2022 Earnings, CIE appears massively undervalued when looking at its strong growth profile, profitability vs. peers, risk management and execution. Pierre recently increased his target price to €45.00 (75% upside).

Woozle Research

Food Delivery Apps to remain under pressure

Woozle's restaurant partners report slowing delivery fundamentals in 1Q22 with order volumes down -10% and order values -15% vs. 4Q21. Deliveroo is expected to suffer faster than market declines and reduced take-rates in 1H22 due to increased competition, poor service levels, rider shortages, and a focus on adding new restaurants and channels over servicing existing customers. Although Takeaway.com is expected to relatively outperform peers, more than half of Woozle’s sources said they would be prioritising in-person dining over e-commerce offerings in FY22 to boost margins and streamline operations.

Demand for salmon is not the issue; sustainability of production is. While the market appears focused on (over-hyped) land-based farming, ocean farming is the most credible new technology (less complexity, better economics, lower capex) according to Sustainable Investing. They highlight SALM as a long-term winner - it is the lowest cost producer (costs per kg have averaged 7% less than competitors resulting in an EBIT per kg between 35%-100% higher than peers) with the most attractive growth options.

Intron Health

Start of a multi-year EPS upgrade cycle - SAN is the most obvious Buy since AstraZeneca in its early transformation several years ago - Intron shows there is 11% CAGR EPS growth (2021-26), 6% CAGR sales growth, a burgeoning pipeline driven by a transformed R&D engine, commercial excellence and discipline in M&A. 10% of 2026 EBIT will come from new launches that Intron estimates will sell €2.7bn by 2026. Despite this, SAN trades on just 11.2x 2023 EPS, a 30% discount to peers. TP €135 (45% upside).

New Street Research

In recent weeks INW has sold off on news of 4-to-3 consolidation in Italy and fears over the ensuing tenancy losses. However, New Street believes the market may have underestimated the protections embedded within the company's MSAs. They now think that INW may be a beneficiary of consolidation in the Italian mobile market, with further potential upside from the issuance of new mobile spectrum bands in the future. TP €12.50 (40% upside).

Green Street Advisors

UK Industrial REITS: Urban winners

A flurry of inner London transactions in the past four months all points to increasing capital values - marking to where assets could trade today (rather than a valuer’s snail pace recognition of change) results in notable increases to spot NAVs. Buyers are pricing in significant, yet realistic, levels of rent growth (25%+) over the medium-term. As such, one eye should be kept on capital values per square foot, which remains at palatable levels when considering alternative uses such as residential, suburban office or even grocery-led retail. Key recommendation changes include upgrading Segro to Buy.

Betaville

Breaking M&A news

Betaville published two proprietary intelligence alerts in Dec 21 and Jan 22 highlighting how Audioboom, the Aim-listed, podcasting business was at the centre of takeover speculation, including the possibility of interest from a US-based technology giant. At the time of the first alert, BOOM’s shares were trading at £14.20. On Sunday, Sky News reported that both Amazon and Spotify are looking at purchasing the company. The shares are now trading above £20.00.

North America

Boyar Research

Value stocks for 2022: Uber (UBER), Bank of America (BAC), Scotts Miracle-Gro (SMG)

Jonathan Boyar recently spoke to Barron’s about Boyar's Forgotten Forty portfolio which has produced an average annual gain of 11.5% over the last decade - all the companies highlighted are businesses which they believe are most likely to outperform the leading indices in the year ahead due to a catalyst on the horizon. Stocks discussed include:

UBER - Profitability in Mobility business is underestimated. It also holds valuable equity stakes in other ride-hailing businesses worth ~$10bn. TP $79 (100%+ upside).

BAC - The most interest rate sensitive of the major US banks; lots of room for NII to rise. TP $61 (30% upside).

SMG - Cannabis business (which has grown 100% in the last 2 years) is in the price for free. TP $242 (~75% upside).

Gordon Haskett Research Advisors

Powering through Omicron - news of long-term development acceleration is unprecedented for a company of CMG’s size. Jeff Farmer upgrades the stock to Buy arguing that the risk / reward has shifted dramatically following a sell off driven by rotation out of growth stocks. CMG is in a league of its own when it comes to the combination of: unit growth at scale, SSS growth, cash-on-cash returns, digital penetration, loyalty program relevance, margins and menu pricing power.

Behind the Numbers

Raised prices to grow sales and margins amid cost inflation against easy comps. However, KO has NOT fully replaced inventory at higher costs as DSIs are down 10 days (with units likely down more than dollar terms). The repurchasing delays should pressure margins more quickly as KO will be buying at even higher costs than last fall. 1Q21 and 2Q21 bring tougher comps on pricing and volume and BTN expects margin pressure to build.

Blueshift Research

Faces an uphill battle to win back share as competition increases, trends move toward ‘better-for-you’ options and ongoing supply chain problems that have caused defections do not return. Blueshift's industry sources also stated that MNST's reduced promotions risks alienating a customer base that is trained to expect discounts. Red Bull remains the dominant competitor and gained share last year with its aggressive marketing as well as its success in bars and restaurants (an opportunity MNST missed). Celsius Holdings is also taking share and stands out as a primary healthier option along with Alani Nu.

Veritas Investment Research

Canadian Banks

Rising risks trump rising rates - Nigel D’Souza expects market sentiment to shift over the coming months as slowing economic growth and elevated credit risk outweighs the benefit of higher NII. Ahead of this inflection point, Nigel is lowering his sector forward P/E multiple for Canadian banks to 10.6x (NB assuming a pre-pandemic PCL ratio, it currently stands at 13.5x, the highest multiple since the GFC). He downgrades Scotiabank, CIBC, National Bank, RBC and TD Bank to Sell. If you are taking money off the table in banks, consider moving it to the insurers. Nigel continues to pound the table on Manulife Financial and recently upgraded Sun Life and Great-West Lifeco to Buy.

Gradient Analytics

The share price fell ~80% last time Gradient turned bearish back in 2017. Key concerns highlighted in their 12-page report this time round include: 1) No evidence of sustainable organic growth. 2) Inventory build looks far more ominous than management describes. 3) Other current liabilities may have provided a temporary boost to revenue and profit. 4) Risk of negative adjustments to previous tax returns. 5) Elevated executive sales. 6) Shares trade at a substantial premium relative to historical averages and vs. peers.

ERA Research

Prices for both lumber and OSB are surging - both businesses will generate spectacular FCF for WFG through at least 1H22. Concerns about rapid interest rate increases and sluggish housing demand are overstated, while limited supply growth should keep lumber (and panel) prices well above historical averages for several quarters to come. ERA’s target price of $155 is based on a very conservative 4.0x multiple applied to a 50/50 blend of 2022E/2023E EBITDA of $2.7bn.

Alembic Global Advisors

Highly attractive FCF yield and unjustifiably depressed multiple - share price is down ~20% from Nov 21 highs despite guiding to an above-consensus 2022 and experiencing a 177% uptick in consensus 2022 EBITDA estimates since the start of 2021. Hassan Ahmed explains why investor concerns surrounding spot Asian caustic prices, Epoxy segment earnings, supply / demand fundamentals, and an earnings “cliff” are overblown. OLN is expected to generate $8bn+ of levered FCF over the next five years (equivalent to its current M/cap). Trades at a FCF yield of 23%. 12-month TP $85.00 (65% upside).

Summit Insights Group

Another bullish quarter - demand continues to be exceptionally strong and subscription revenue is growing faster than guided driven by the company's SaaS offerings. The ongoing digital transformation, attacker innovation, elevated threat levels, an expanding attack surface, will ensure elevated security spending in 2022. Identity remains the central pillar around which enterprises are re-architecting their security strategy and Srini Nandury believes CYBR will be one of the main beneficiaries. Srini's target price of $225 (50% upside) translates to 13x EV/C2023 sales of ~$673m.

Japan

LightStream Research

The thesis here is simple - consensus projects a 3% OPM next FY and Mio Kato believes Mazda will double that. Profitability is surging. Q322 OP beat expectations by 26% even excluding a reclassification of some costs to extraordinary losses. Mazda has been revamping its US business, sales structure and model line-up (Mio compares its approach to Subaru’s when the stock went from ¥660 to ¥5,000). If Mazda can do all this in the face of significant headwinds, when those turn and become tailwinds next FY it will blow away consensus numbers (could see OP of ¥300bn!). Mazda could be a multi-bagger even if we end up going into a bear market.

Emerging Markets

Creative Portfolios

Good work on costs with a rock-solid balance sheet - Paul Hollingworth sees upside to management's very conservative guidance. He highlights positive changes in Profitability, Efficiency, Liquidity, Asset Quality, and in Provisioning. He notes that Earnings Quality could be better but believes the bank may be materially understating its bottom-line given that Comprehensive Income is well in excess of Net Profit. The shares currently trade at a FV of 9% and a P/B of 0.56x. BBL also has a PH Score™ of 8.3 - the highest Score in Thailand.

RedTech Advisors

No-Man’s Land - BILI delivered strong growth in users and revenue in 2021 but margins collapsed as the result of its growth-at-all-costs strategy. With the stock down ~75% from its peak, one might assume that most of the bad news is already baked in, but RedTech are concerned that BILI may face more headwinds. While margins should improve as the company focuses on higher-quality revenue sources, RedTech worries that growth was inflated by KOL’s recycling livestreaming revenue, which could lead to slower growth in the future. Separately, BILI faces more risk than many peers from competition and heavy-handed regulation.

Propitious Research

Indian IT Services: Unattractive outlook

Will increased dividends and buybacks be sufficient to support current elevated valuation levels? Following 2 years of exceptional performance driven by accelerated digitalisation in the wake of the Covid pandemic share prices have started to correct. While demand remains robust, revenue and earnings growth rates are decelerating. Wium Malan's report focuses on the prospects of the 4 largest companies in the sector - Tata Consultancy Services, Infosys, HCL Technologies and Wipro.

Copley Fund Research

Global Funds: Investor positioning insights

EM Unwind - Allocations among active Global managers have taken an aggressive move lower led by China & HK, South Korea and Brazil.

China & HK Style Switch - Value and Yield managers have aggressively reduced underweights, whilst Growth and Aggressive Growth managers have moved to new lows. AIA Group takes the crown as the most widely held stock and largest overweight.

Asia's Communication Services Fall - Ownership breaking new lows led by Tencent, Nintendo, NetEase and Nippon Telegraph.

Energy Conviction Underweight - TotalEnergies is the most widely held stock, but there is little conviction or consensus to suggest managers are concerned over long-term outperformance of Energy vs. sector peers.

Macro Research

Developed Markets

Aitken Advisors

Central banks and the markets

The unwind of highly levered, long-duration, embedded-short-volatility bets clearing at heroic valuations has defined most of the past nine months, and the past month in particular. In James Aitken’s latest report, he claims this unwind is far from over: if the FOMC wants to tighten financial conditions enough to nip a nascent price/wage spiral in the bud, then many financial assets remain far from the right price. James also discusses the ECB, BoE, current inflation and economic backdrop, and the UK’s disastrous climate transition strategy.

Andrew Hunt Economics

UK: A recession will occur sooner than many are expecting

The UK has an obvious conundrum: falling real wages despite a tight labour market and record vacancy levels. Andrew Hunt postulates that this situation has arisen due to inelastic labour supply and elastic labour demand brought on by a declining labour force and weak productivity growth. Unless the UK can engineer a supply side renaissance, Andrew’s hypothesis of the shape of the s&d curves indicates that a deep recession will be required to control inflation. Unfortunately, it’s the most likely outcome.

Greenmantle

US: Erring on the side of Dovishness

Having underestimated inflation throughout 2021, markets responded to Thursday’s inflation print by pricing 45bps in rate hikes in March, with ~90% probability of more than 150bps of rate hikes by year’s end. Niall Ferguson believes traders are overestimating the Fed’s hawkish turn and its resolve. He expects a total of 125bps in 2022, with no rate hikes before March as this will have no meaningful impact on near-term inflation.

Longview Economics

US: Don't buy the dip

Chris Watling advises to stay ½ SHORT S&P500 March futures (combined entry was at 4,504.12) and to widen modestly the stop loss to 4,590 given current volatility levels. His reasons are fourfold: the follow through on BUYing after recent positive news on Russian troops apparently returning to base was limited; volumes during the Tuesday rally were light; models are yet to reach a collective BUY message; and evidence of markets entering into wave 3 of this current pullback remains strong.

Quill Intelligence

US households signal recession

Consumer expectations hit a decade low in February, the third consecutive quarter of falling expectations. A quarter of consumers expect their finances to worsen over the next year, the highest since 1980. The bond markets and US households are in a footrace to see which can flag recession the quickest. For now, US households are “winning”, suggesting downside to longer-dated maturity Treasury yields.

What you’re not hearing about the awful CPI report

Just three categories explain most of January CPI. As they experience high inflation, their weighting in the index rises, making their impact increasingly damaging - even if consumers are buying less of them. The BLS introduced new weights today. Based on pandemic-era data, the weights in the most inflamed categories went up. As supply chains are repaired, and price of items in scarcity fall back, their disinflationary impact will be greater than their inflationary impact on the way up. To watch Donald Luskin’s latest video, click here.

Asymmetric Advisors

Japan: BOJ’s battle to keep rates low to bring huge shorting opportunity for JGBs

Japan’s central bank has plunged itself into a losing battle to keep rates low while yields spike elsewhere as nations abandon QE. The huge selling opportunity for JGB holders and macro investors will ultimately provide a big payday for macro funds and will further pressure the yen to weaken as rate differentials widen. Indeed, the hit to real incomes will unlikely go down well with the current government, who may end Kuroda’s tenure as BoJ chief sooner than expected.

Minack Advisors

Can Australia escape its horrendous decennium?

Gerard Minack claims the pandemic has given Australia’s ailing economy a circuit breaker: fiscal policy kick-started growth and border restrictions are tightening the labour market, which may be what is needed. With recent wage growth trends, investors should expect the RBA to start tightening later this year. However, a return to pre-pandemic policies would mark a return to low wages, low growth and low rates, and markets look wrong to be pricing aggressive further hikes through next year.

Periscope Analytics

S&P/ASX Indices: A busy March rebalance

Brian Freitas' report highlights potential changes to the S&P/ASX family of indices as a part of next month's rebalance. The M&A wave in Australia has resulted in changes to the indices in 2022 and there will be plenty more in March. Passive trackers will need to trade over 5 days of ADV on quite a few stocks, while there are others that will receive inflows from the FTSE All-World/All Cap passive trackers.

Emerging Markets

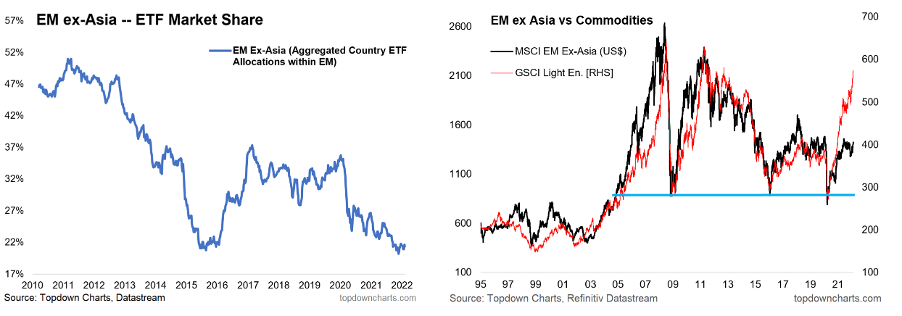

Topdown Charts

Chart of the fortnight: Bullish EM ex-Asia

Callum Thomas explains how the second wind in commodities will provide an impetus for further upside in EM ex-Asia equities, which have outperformed EM Asia since early 2021. Add this to very low relative allocations to EM ex-Asia, along with attractive valuations in both absolute and relative terms, and you have a strong bullish case for EM ex-Asia. With attractive equities and FX valuations investors should look most towards LatAm, especially with its central banks further along the path in normalising interest rates.

Totem Macro

EM portfolio positioning

Whitney Baker remains concerned about equities and is LONG certain EMFX and bonds in reformed debtor countries, which already price in historically high real rates. She’s paid in lower yielders with inflation problems and holds Chilean linkers. On global stocks, Whitney worries about prior overstimulation, stagflation, unwanted monetary policy trade-offs, and surging yields. Monetary largesse has inflated asset valuations across the globe, so Whitney prefers to lean into the rotation via Asian SHORTS against her preferred “reformed debtor” longs, without taking directional stock beta.

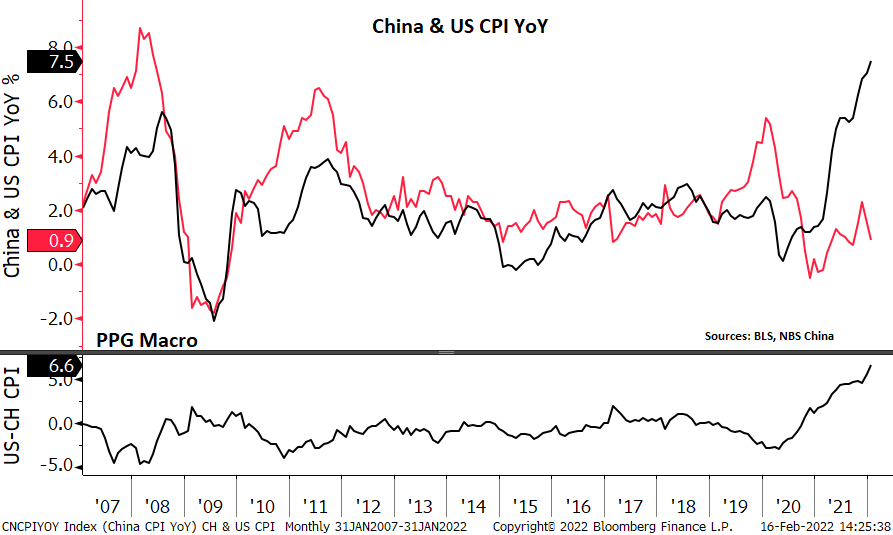

PPG Macro

China: The great divergence and the return of the great deflator

While the West obsesses about inflation, it’s a very different story in the Middle Kingdom; growth remains subdued and consumer prices undershot forecasts for the third month in a row. Never has US-China CPI diverged so much, and Patrick Perret-Green believes it to be unsustainable. Looking ahead, Chinese producer prices have the potential to fall very sharply – expect PPI to be close to zero on a YoY basis by mid-2022, and negative in Q3. Expect the effects to spill over into the global economy which could be teetering on the edge of recession by year’s end.

High Frequency Economics

China, Russia and the oncoming economic war

Carl Weinberg sees a dangerous alliance forming between Moscow and Beijing with the specific intention of toppling the US and NATO from control over the global diplomatic, military and commercial order. With China as an ally, sanctions against Russia will be powerless, and NATO’s military will fare no better – the two nations have the leverage to achieve any goal they want. An economic war is coming and nobody will be able to hide from the consequences.

Oxford Analytica

India will intensify push for trade deals

Investors can expect India to announce several bilateral trade deals in the medium-term, including preliminary agreements and full FTAs. Expect deals with the UK (which will be more focused on goods than services) and Australia to be within reach but expect an EU agreement to be noticeably more complex. The focus of pacts will be to bar entry to India of Chinese-made products, to facilitate digital trade and to reduce immigration barriers for Indian professionals.

ESG

View from the Peak

Are EVs really better for the environment?

Mobilit-e is Climate Transformed’s two-week virtual immersion into every facet of the EV supply chain. Douglas Johnson-Poengsen, CEO of Supply Chains Tracing/optimisation software firm Circulor, delivers the keynote by digging into whether EVs really are better for the environment. To manage the carbon in building an EV, you have to measure it – in this video Paul Krake and Douglas talk about supply chain optimisation, especially for batteries, and debunking myths. Click here.

Commodities

Queen Anne's Gate Capital

Stronger demand points to higher oil prices

Average global demand growth coming into the pandemic was much higher than originally calculated, so investors should expect higher demand growth in the next few years. Supply restraint by OPEC/US producers continues to push OECD inventories below their 5-year averages, and Kathleen Kelley sees more draws coming. Although she expects higher oil prices and a higher commodity price index, a commodity super-cycle is not underway; for many commodities demand is falling and production is on the rise.

Independent Strategy

Agro-commodities

The latest WASDE report by the US Department of Agriculture reaffirms David Roche’s LONG position in wheat and other grains, which he has held during the pandemic. He has also been LONG cotton as a key agro-commodity in short supply. David reckons there is further upside in food prices to come as demand rises, supply chains falter and global grain stocks fall. More immediately, grains also provide a hedge against a Russian invasion of Ukraine and the subsequent sanctions that will follow.

Global Mining Research

How to pick a gold stock in 2022

Global Mining Research’s BUY and SELL signals served investors well in 2021 despite some market disconnect between equity price and numerous variables, including dividends. This year, David Radclyffe sees the gold sector shifting more to a growth/scale focus over returns/balance sheets; so, more M&A, growth investment, inflation impacting margins, lower dividends and a focus on ESG. David’s latest report looks for stocks that match the investment themes within the sector. Key picks include Agnico Eagle (new BUY signal), Barrick Gold, Northern Star Resources and Endeavour Mining.