Company & Sector Research

Europe

Arete Research

Ready for a reboot - while a new (preferably tech-experienced) CEO will have much to do, Arete sees an opportunity in the roll-out of ASC’s recently announced partner programme initiative. The online retailer must also step up capex materially to enhance its proposition in international markets, potentially cutting ties with RoW/ANZ. Alternatively, it may retreat to its core UK stronghold, ultimately leading to a merger with a larger rival. The stock is cheap on a 0.5x 2022E EV/GMV multiple (50%+ discount to peers) hence risk reward looks favourable here. Upgrades to Buy. TP £32.40 (45% upside).

Forensic Alpha

Surplus to requirements - growing risks identified within the current vaccine portfolio. Inventory levels are near all-time highs, while provisions against that inventory have fallen significantly. The combination of the Omicron variant and seasonally weaker fourth quarter sales means the conditions exist for a sizeable write-off. Forensic Alpha’s Dragonfly (MI) system has given BAVA a risk score of 9 out of 10, with multiple red flags identified in both the governance and accounting sections.

Seen as an EV-smart charging play, additional value can be found in its smart grid solutions and battery storage with sustainable growth in the low 20s at higher margins for a longer time-horizon than modelled by the Street. In the medium term, analysts at Sustainable Investing see margins increasingly accruing to smart grid suppliers and integrators at the expense of turbine and solar OEMs (which are at risk of becoming commoditised amid higher competition from Asian competitors). Alfen's charging / grid expertise (and 100%) free float make it an attractive target for both green utilities and oil companies that are investing in renewables generation.

TT Equity Research

Teun Teeuwisse’s short thesis remains intact post H1 results - SMDS has failed to benefit from the exploding demand for boxes as it has been unable to improve profitability. As such, the revenue and box volume growth are irrelevant, even though this is exactly what management focuses on to display its "outstanding" performance. Debt remains high and hidden debt (inflated payables / reverse factoring, factoring, the outstanding liability on the interstate put option and deferred capex liability) is at least double the reported debt level. When demand eases things will quickly turn ugly.

North America

MYST Advisors

Short Ideas: MYST’s clients generate impressive alpha

MYST hosted 23 Formal Events in 2021 which yielded 73 short ideas - 83% of these calls yielded positive alpha with ~21% average alpha over a 3-month period (12-month figs: 77% generated positive alpha with 21% avg. alpha). Ideas that remain compelling include:

United Parcel Service (UPS) - Multi-yr headwinds from increased competition, wage inflation and airfreight rate normalisation.

Elanco Animal Health (ELAN) - Questionable M&A strategy, bloated balance sheet and SEC probe to pressure results.

IPG Photonics (IPGP) - Anticipate precipitous ASP declines due to low-cost Chinese competitors.

Huber Research Partners

Bids around $22-23/share are way too low, but why sell at all? Would represent only 7.5-7.8x 2021/22 average estimated EBITDA (pre-synergies) vs. takeout range of 9-9.5x for most other TV station transactions this past decade. In fact, Craig Huber believes that TGNA would be better off remaining as a standalone public company and upping its share buyback programme from the current $300m to $1bn over next three years (he estimates it can generate $1.85bn in FCF after dividends 2022-24). 12-month TP $27 (45% upside).

New Constructs

Healthy product but unhealthy IPO - the stock is likely worth $0 given the company’s limited differentiation and the intense competition from other new entrants and established restaurants. Local sourcing model is expensive / risky; sees no path to profitability. Despite this, SG is priced to grow faster than Chipotle achieved in its first 10 years after going public.

In 2021, 36 out of New Constructs’ 41 Danger Zone stock picks outperformed as shorts with the top 5 outperforming the S&P 500 by an impressive 63% on average.

Quo Vadis Capital

How can a bankrupt Chinese fraud be a great long? John Zolidis argues that Luckin is conducting what is probably the most remarkable turnaround he has ever seen. Six quarters ago, store-level margins were negative 25%. In the Sept quarter they were positive 28%. In 2020, the company's EBITDA margin was negative 39%. In 2021, John is forecasting a 5% EBITDA margin, hitting 15% by 2023. Despite reporting stellar 3Q results the stock sold-off into year-end, but with no analyst coverage the potential for this equity to be mispriced is very high.

The Retail Tracker

IPO'd last year, this Swiss shoe company is on a winning path as it enters the US market - boasting a beautiful design and appealing logo, ON is targeting the fashion x function customer which has proved so successful for the likes of Nike, Lululemon and Moncler. This approach allows for a range of distribution points helping to broaden brand awareness. Retailers like Bandier and Dover Street Market will also help to bring the brand to the younger fashion crowd. This is important, while this shopper can be fickle, this space, unlike denim or beauty, is not seeing new brand launches every year.

Veritas Investment Research

Veritas have identified several headwinds that will weigh heavily on RUN’s share price including declining third-party ownership market share, key input costs of solar and battery systems, subsiding subsidies (both federal and state) and aggressive non-GAAP metrics. Jacob Liu estimates that RUN’s normalised 2021 recurring cash flow is $159m, implying a lofty 46x FCF multiple. Using a sum of the parts approach, he values RUN’s existing assets and development prospects at $20/share (40% downside).

Kailash Capital Research

Growth vs Income Investing: Why choose?

As the investment world obsesses over “DeFi” and “FinTech”, old-fashioned Financials are cranking out record profits on historically conservative leverage ratios amidst one of the most hostile Net Interest Margins on record. These cheap bank stocks have become high-quality growth stocks. The weight of Financials in the S&P 500 is barely above the levels seen at the trough of the GFC; despite generating ~25% of overall index profits they only represent an 11% weight in the index. KCR's top ranked stocks in the sector include Fidelity National Financial, American Financial Group and US Bancorp.

Costigan Reports

Having successfully identified the transformation at NOVT (turned bullish June 2017 at $36; current share price $176), Bob Costigan believes the company is poised to enter a rapid growth phase as it takes advantage of the global shift to mobile robotics. He projects revenue CAGR of 15%+ (10% organic), OCF CAGR of 30%+ and EPS CAGR of 30%+ (2022-24). NOVT has a history of innovation and Bob expects investment in R&D to increase to 9% of sales in each of the next three years. 1-yr TP $220; 3-yr TP $320 (90% upside).

Copley Fund Research

ESG-shaped recovery - DE is now owned by 15.8% of Global Managers (from a low of 5.4% in 2019). Steven Holden’s analysis highlights the extent to which the ownership base in DE has evolved over the last decade. Historically, DE had been bought and sold quickly (only ever held by 20-40 funds at any one time). However, 2021 was a breakout year, with 59 funds currently holding the stock, it has certainly changed the ownership dynamic, and with ESG a strong part of the investment case (8 of the top 25 holdings are held by ESG focused strategies), perhaps more funds will take note.

Alembic Global Advisors

Chemicals: Macro stars aligned

Global economic stimulus, a weakening USD, rising vaccination rates and lean inventories are perfectly aligned for continued commodity chemical strength, with higher oil prices providing an additional tailwind. Multiple compression at Olin, Chemours, Huntsman and Tronox seems excessive, particularly when compared to earnings growth prospects. FCF yields at Venator, Braskem and Trinseo are very attractive. For 2022, Hassan Ahmed prefers companies that may benefit from activism/M&A-like catalysts (Braskem, Huntsman and Tronox), secular changes within their markets (Olin), or have underappreciated proforma earnings power (Trinseo and Westlake).

AlphaSituations

The tale of two Fintech companies - ML is several steps ahead in becoming a fintech super app. Robert Sassoon argues that the substantial value premium at which AFRM is currently trading makes no sense given the potential headwinds from heavier regulation and increased competition likely to confront pure-play BNPL companies. A grossly undervalued ML (400% upside) and pricey AFRM (30% downside) offers a highly lucrative pair trade idea with potential to yield an outsized return in 2022.

Japan

Asymmetric Advisors

Now is a good time re-enter the name if you believe in the global automation story - trades at 15x PER & PBR, back near long term lows. More industrial robots = more Nabtesco gears. Dominant position (60% global share) which it has successfully maintained for the last decade+. Sales and operating profit can advance further this year driven by the all-important speed reduction gears (25% of sales but c.50% of profits) and a recovery from 5-year lows in its Transport business.

LightStream Research

An Epic partner - Mio Kato has been arguing that significant collaboration between Sony and Epic Games is likely in forming the key infrastructure for the metaverse. The recent Matrix Awakens demo starts to reveal some of the possibilities. In addition, it demonstrates why Mio believes popular metaverse theme names like Meta and Roblox have no realistic chance of competing. Mio also discusses the (increasingly high) likelihood that Tencent decides to sell its stake in Epic with Sony expected to be one of several interested parties.

Emerging Markets

New Street Research

Korean Telcos: Lessons from Japan

Something is changing in the Korean Telco landscape - buybacks from SK Telecom and KT Corp, increased stock ownership by employees and management, an increased focus on profitability / returns, and more progressive dividend policies all point to a better environment for shareholders going forward. At the same time, post the spin out of SK Square, SKT, which has not historically been a rapid growth company, is now guiding to 50% revenue growth over the next 5 years! Taken together Korean Telcos which have historically traded at a substantial discount to the rest of the EM telecom sector look set to re-rate materially.

Galliano's Financials Research

FinTech & Financials: 2022 investment themes

1. A shift into value in EM banks; cautious on digital banks - top picks are Sberbank, Banco do Brasil and HDFC Bank. Nubank likely to be one of the EM FinTech big negative surprises of 2022.

2. Southern Europe banks, position for the prospect of higher interest rates - highlights BBVA and Banco BPM.

3. Exchanges, competitive pressures are real, but are they priced in - B3 and Singapore Exchange standout.

4. Growth and value in digital payments - highlights Mastercard and, for its deep value, PagSeguro.

5. Digital wealth managers, picking a potential winner - BTG Pactual.

Hemindra Hazari

Toxic workplace - new employees take one look and run. Hemindra Hazari reveals that new hire attrition at the bank exceeds 25%! This appears to be a symptom of a toxic work culture at the bank, where employees are evidently under intense pressure to meet targets or are incompatible for their roles. Most analysts covering the financial sector tend to ignore non-financial data, but since labour is a key competitive strength in the banking and service industry, high levels of attrition can have a bearing on performance. Indeed, Axis Bank’s financial performance in 2QFY22 has already thrown up red flags.

RedTech Advisors

China’s Online Healthcare Market: Prescriptions for success

With both the government and China’s largest internet companies driving change, there is enormous potential for disruption and opportunity in the country’s RMB8.3 trillion consumer healthcare sector. The two leading players in the online market, JD Health and Alibaba Health, are down ~60-75% from their peak, but with opportunities still 18-24 months out it is now a question of whether to get in before the regulatory catalysts, or to try to catch the momentum after the fact.

Macro Research

Developed Markets

Greenmantle

Not Quite Out of the Woods: Predictions for 2022

Growth will be solid - not spectacular, inflation will overshoot, and Democrats will get shellacked in the midterms. Cold War II remains in force and tensions with Iran in the Persian Gulf could boil over into conflict toward mid-year. Russia's armies are poised to invade, though in the Kremlin no decision has yet been made. Niall Ferguson hopes it will be a Happy New Year, but we're not quite out of the woods.

CrossBorder Capital

Developed markets volatility ahead will provoke central bank reversals

Central bank liquidity is set to slow markedly in 2022. US Fed and ECB balance sheet sizes will see absolute falls from mid-year. Meanwhile, China is maintaining a stable course, albeit at a low ebb. Michael Howell suspects that rising market volatility will cause some policymakers to reverse their planned QE tapers, with the Fed folding first.

Belkin Report

Where to find alpha in 2022

85% of active managers underperformed the S&P500 in 2021. However, there were (Belkin recommended) alpha opportunities that most portfolio managers seem to have missed in Energy (+48% with 21% alpha) and REITs (+42% with 15% alpha). Moving into 2022 Michael Belkin sees the best sector prospects in utilities, consumer staples, REITs and healthcare, while stock indexes remain a sell & short recommendation in what looks like an epic long-term stock market top.

Eurointelligence

What to do with Covid debt?

The Draghi / Macron agenda for Euro area fiscal reform potentially includes ambitious proposals for a European debt agency that would buy Covid-related debt from the ECB. The German government is open to some stability pact reforms, but Eurointelligence can't see it accepting the idea of a permanent debt transfer for political and legal reasons. They argue that the EU can pursue a fiscal union, or inter-government debt alleviation, but not both.

Policy Sonar

Silvio and Rome's highest hill

Italy's upcoming presidential election is shaping up to be nothing short of a powerful Machiavellian plot of power and intrigue, with a ritual equivalent to a papal conclave. It is completely unclear how the turnout will be affected by Covid potentially reducing it by as much as 10%. While the other key factor is the return of Berlusconi waging an all-out charm offensive to convince voters to support his last hurrah bid.

Sour sentiment and surprisingly normal valuations set the stage for another strong year

Gloomy sentiment sets the stage for another boom year. The Omicron case-wave has crested. Equity valuations point to an above-average year for stocks. Fed lift-off in May won’t be tightening, only an appropriate adjustment. Inflation will cool, so they might wait as an insurance policy. Long-term yields will drift higher. Build Back Better can’t survive. The GOP will take back Congress. The cessation of child tax credits is not a fiscal cliff, but rather the end of an economic distortion.

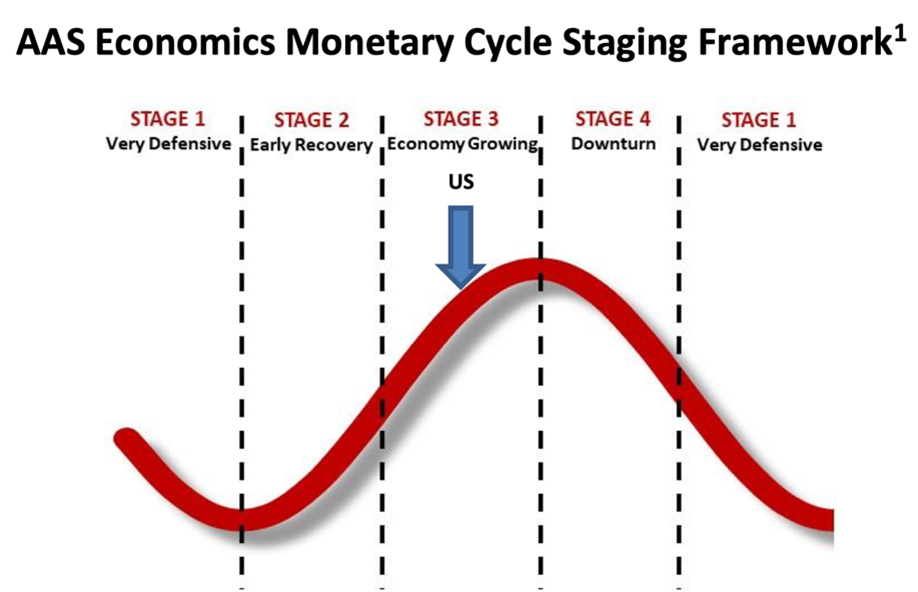

AAS Economics

US moving through the business cycle

As we move into Q1/2022, the US business cycle is rotating into stage 3 of the AAS cycle characterised by strengthening equities, property and commodities. Frank Shostak maintains his maximum overweight view of US equities and US listed property, and underweight US govt bonds. In contrast, the country composite for global govt bonds (ex-US) will move into stage 1 with stronger returns, and AAS suggests moving overweight.

Musha Research

The Gods of Fate are smiling on Japan

With the world’s largest waiting list for potential equity investment, Japanese equities will become significantly more attractive in 2022 as investors realise the superiority of the country’s business models, improved economic expansion and favourable geopolitical winds. Ryoji Musha also mentions GAFAM is running out of steam; expect Japanese equivalents to take over.

Emerging Markets

Macrolens

Poor EM performance

EMs are effectively short dollars, directly via USD borrowings and/or indirectly via a reliance on commodities. Given the commodity rally, EM performance has been remarkably poor. Brian McCarthy doesn’t see much improvement ahead and recommends long S&P vs EEM - the trade has moved a lot recently but still has plenty more room to run!

Independent Strategy

US Dollar to hold its attractiveness amidst EM instability

David Roche believes China turning inwards leaves emerging economies without international trade as a growth engine. Most lack the critical mass of China to drive growth domestically. Latin America politically is also designing itself into another lost decade. Russia is a kleptocracy bent on war and is economically set to lose by it. While Turkey is ruled by a madman. Global growth is set to plummet and with it being impossible for Europe or Japan to fill the growth vacuum, David maintains that investors should still be long the US dollar, but it will become highly volatile.

Greenmantle

Turkey’s deposit guarantee program unlikely to provide respite to monetary and fiscal systems

Niall Ferguson sees Turkey’s deposit guarantee program as a further step toward the nationalisation of bank risk and doubt it will provide much respite to the country’s monetary and financial system or its beleaguered and increasingly unpopular president. On the back of consumer price inflation hitting 36% at the end of 2021 and the government imposing capital controls on exporters - Niall states that Turkey’s slide toward insolvency has entered a dangerous new phase.

Totem Macro

Turkey: Ignore the worries

The finance minister’s solution to the plummeting Lira may be bank-friendly, but that doesn’t mean it won’t work. By increasing the forward return of holding Lira for those who were selling it in the first place, Whitney Baker is confident this is all that is needed. Ignore the overblown press panic over how risky this all is, the risk/reward is great and the cost to government will be fine. Buy Turkey.

PRC Macro

China’s monetary policy effectiveness dependent on expanding balance sheets

William Hess purports that for China’s upcoming stimulus to be effective, we will need to see corporate (developer and LGFV) and household balance sheets expanding. If they do not, it will signal inadequate stimulus and failed policy transmission. But before credit transmission improves in China, William sees growing downside risks for steel prices.

Forefront Advisers

Russia & NATO: State of play

Upcoming meetings between Russia and the US will be key pointers for the possibility of de-escalation. While Russian demands on NATO remain a non-starter, there is agreement among many US policymakers (shared by some EU members) that NATO enlargement can’t continue on autopilot. Instead, a new security arrangement is needed with Russia. This could provide an opportunity for Russia to climb down, if the US is also able to lean on Ukraine to play ball on Minsk implementation. But, if these fail, we can expect the West to increase the pressure by highlighting the cost of a conflict. This would indicate a diplomatic deadlock and so a high risk of conflict.

Alberdi Partners

LatAm faces slower growth prospects

Marcos Buscaglia expects Latin American countries in 2022 to face slower growth and a retracement of inflation. While most governments will be hard pressed to pull the plug on high government spending, Brazil and Colombia will especially find it politically unfeasible to cut decisively the fiscal deficits ahead of elections in 2022. As inflation rates in the region start to peak, respective central banks are expected to hike rates.

Oxford Analytica

Egypt: Gas and politics

By facilitating emergency gas deliveries to Lebanon, Egypt is seeking to leverage its strategic location, infrastructure and natural gas reserves for political and financial gain amid global shortages, providing windfall gains to stakeholders. We could see Egypt as an energy hub becoming a small but significant role in helping Europe reduce its chronic dependence on Russian gas.

Krutham (formerly known as Intellidex)

Electoral campaigning set to dominate South Africa’s 2022 political calendar

The African National Congress’ 8th January ANC anniversary celebrations will mark the informal kick off point for campaigning to start into the December 2022 elective conference where Ramaphosa will be seeking a second term. Peter Montalto believes that Ramaphosa has failed to unite the party and will win re-election only as a "least worst" option. Peter further expects much of the election drama to play out below the apex across the other top 6 positions.

Commodities

Cornerstone Analytics

Oil: MIKER Model points to triple digits for Brent crude price

Back in Oct 2020 Cornerstone Analytics suggested that 2021 would see the largest oil inventory draw in history while their proprietary MIKER Model asserted enormous upside for oil prices. Yet, while oil prices have indeed moved higher with global oil inventories tumbling by a record amount, some of the extremely non-consensus arguments behind Mike Rothman’s forecast at the time - largely centred around oil supply/demand dynamics, OPEC’s positioning, and key geopolitical relations - are still critical considerations as we head into 2022, while the team’s MIKER Model now suggests crude prices could very likely break the $100 mark.

ERA Research

Forest Products: Industry outlook for 2022

From commodity price forecasts to global supply and demand models through equity and debt coverage of nearly 30 leading forest products producers, ERA offers insight into recent catalysts and long-term market trends.

North American lumber prices are set for another spectacular year, although prices will have to fall from current elevated levels. BC’s high-cost position well ensure solid profits for others. Pulp prices have bottomed and will rise as we progress through 2022 although the unwinding of supply chain inventories will limit the recovery and add volatility. Paper prices will top out in H1/22 after reaching record (or near record) levels. High prices will accelerate the secular decline, with impacts felt more acutely in 2023.

Queen Anne's Gate Capital

Agricultural Markets: Focus shifts to supply in 2022

While acres planted this year will be large, Kathleen Kelley expects to see a detrimental impact on agricultural crops from a lack of fertiliser. High costs and lack of availability will lead to less fertiliser being applied. Fertiliser costs normally make up 15% of total costs for US farmers and since Sept 2020 costs are up 100-300%. Corn and wheat are the largest users of fertiliser, accounting for about 15% each of global demand. Soybean usage is closer to 5%, so one of the results may be a switching away from corn towards more soybean planting. So continued strong gasoline demand will lead to more ethanol demand and at the same time corn planting may fall off.