Company & Sector Research

Europe

Forensic Alpha

H1 results disappointed the market (down 15% on the day & 30% in the last two weeks) and Forensic Alpha's machine intelligence system, Dragonfly, has identified an additional risk on the balance sheet: a sharp rise in DSI, from 83 to 105 days - more than 3 months of inventory now on the books. Inventories have gone from £168m in August 2020 to £255m in August 2021, representing ~150% of FY21 adjusted EBITDA. Any write-offs or write-downs of inventory could be substantial.

the IDEA!

New subsidiary, NN Insurance Belgium, to sell closed book life portfolio - worth €3.3bn of assets and liabilities. This further simplifies their IT structure and enables full focus on further growing the protection and pension business, building on its strong distribution network in the Belgian market. This chimes with NN’s long-term strategy and ambitions. The IDEA reiterate their bullish stance.

Engineering group with a large non-strategic stake for sale. Assystem is benefiting from an ongoing €50bn program to extend the life of French nuclear power plants. With French electricity prices on the rise, and an expected 20% increase in capital expenditure on nuclear power over the next three years, LPE forecast a 40% increase in Assystem’s EPS in 2023, compared to 2021. TP €45 (~45% upside)

Vision Research

At the IRF Short Ideas conference in June, Vision explained its thesis, including increased competition (Amazon and others), high household penetration, and rising cost pressures. Amazon recently announced the rollout of Prime in Poland and Shopee has announced its entrance. Since the conference shares are down ~14% while the Stoxx600 is up ~1%.

TT Equity Research

Solutions 30 continues where it left-off: manipulating results and hiding debt. Teun Teeuwisse still sees zero equity value. HY21 results have been reviewed but not audited. Management claim strong revenue growth and stable profitability in H1 2021, but do not be fooled by their attempts to deceive the market. Cash generation is non-existent and the 'net cash' position is nonsense. S30 has a serious debt problem.

North America

Radio Free Mobile

The American ByteDance? - In a bad week for FB, Mr. Zuckerberg shot down allegations effectively, claiming that the US government wants to utilise events to stifle his company's ability to distribute news and information. The media is not a neutral observer and a draconian crackdown seems on the cards, which would hurt the US as a tech superpower long term.

Huber Research Partners

IAC announced the purchase of MDP’s legacy magazine unit and National Media properties for $42.18 per share. They are throwing in the towel, better late than never with long-term secular issues in magazines too hard to overcome. Having bought Time Inc. in 2018, they struggled with the properties from day one. The rating remains a long-held Underweight at this stage. TP $59

Blueshift Research

Celsius’ growth is sustainable. An established leader in functional-energy drinks, with popular flavours, it is not a fad and is growing in strength amongst customers interested in healthier options. CELH can grow even faster with a stronger distribution network and increased marketing. It is navigating supply chain problems well and has not raised prices yet.

Off Wall Street

A "perfect storm" in the housing market since mid-2020 has allowed MTH to generate abnormally high margins in its homebuilding business. Street expectations imply this will continue into 2023 but it is unlikely that MTH can continue to raise home prices and volumes, while keeping its costs flat. Field work in MTH communities indicates demand and pricing growth have slowed significantly. TP $70 (~30% downside)

Badger Consultants

Peloton is Peddling into an all-familiar Headwind. It is yet another fad exercise equipment maker given ridiculous multi-year valuations by Wall Street. COVID-19 pulled forward years of consumer demand. Subscriber & workout numbers are in decline, inventories are building up and equipment prices are being slashed. Even at all-time sales levels PTON never made an annual profit. For historic examples see NordicTrack and BowFlex. TP $50 (~40% downside)

R5 Capital

Something to Snack On: Three that Should Thrive

Walmart, Target, and Albertsons, roughed up by last month’s choppy market, are now building momentum and recent pullbacks present buying opportunities. WMT-Home Depot partnership shows a positive business trajectory. TGT is creating an unrivalled total experience allying with Levi's, Apple and Disney. ACI's company specific initiatives, including streamlining purchasing and growing its private brands, show the business is strong.

Actively integrating its business into the rapidly growing RNG supply chain. Recent deal with Amazon provides significant business model validation. CLNE is set to benefit from a more robust sales network, added scale, and a larger balance sheet. Expect RNG production, distribution, and consumption to continue growing significantly. TP $13 (~45% upside)

Two Rivers Analytics

The pandemic brought unsustainable sales in Danaher’s Life Sciences and Diagnostics segments. With weak organic growth, masked by a string of acquisitions, analysts’ estimates are too high. The stock is trading at rarely seen premia over an expensive comp group. Expect Danaher to show slower growth and lower margins leading to a rerating and a cut in multiples.

Alembic Global Advisors

US Chemicals: Expect a Strong Q3 21 and 2021

Current consensus expectations for the sector in Q3 still seem tepid, keeping in mind product margin gains and pricing strength. It is highly possible that companies under coverage will experience positive earnings revisions throughout 2021. Covestro AG, TP $73 (~25% upside); Chemours Company, TP $46 (~50% upside); Celanese Corp., TP $200 (~25% upside); Dow Inc, TP $85 (~45% upside)

Veritas Investment Research

Despite alleged accounting irregularities, the company can provide more high-quality disclosures and still exceed short term guidance. In the long term, however, increased competition in e-commerce and payments may be obstacles to the company’s burgeoning valuation. Intrinsic Value C$96 (~20% downside)

Summit Insights Group

RNG has one of the best product portfolios in the UCaaS market as well as relationships with legacy vendors and service providers which will drive growth. Termination of the Zoom/Five9 merger will benefit RNG in the enterprise segment of the market. Expect the company to continue to beat estimates when it reports in November. TP $300 (~25% upside)

Japan

JapanConsuming

Muji (7453): a ¥3 trillion brand by 2030?

Ryohin Keikaku fired a broadside at Uniqlo last month. He confirmed that not only was their new president a former lieutenant of Tadashi Yanai, but that it plans to reduce prices to compete with Uniqlo in apparel and Nitori in homeware. Muji has big plans to become a ¥3 trillion behemoth in just 10 years with more stores in Japan than even discount apparel chain, Shimamura.

Emerging Markets

New Street Research

Singtel has announced the disposal of a 70% stake in its Australian tower asset for A$1.9bn – a 38x EBITDA multiple based on company commentary - and A$500mn more than anticipated. The majority of proceeds will be paid directly to Singtel, facilitating additional deleveraging and increased balance sheet flexibility. Market reaction was underwhelming and it remains a good opportunity. TP S$4.10 (~65% upside)

Westlake International

Given antitrust rules, BABA has offered more free traffic resources to younger & medium sized brands and encouraged merchants to participate in Taobao Live streaming by giving more weights to promotional streaming / short video content for this year’s 11.11. Weaker consumption in China lowered sell-side consensus estimates, but expect BABA to likely deliver inline with Q3 China retail revenue, driven by strong appliance, home food and healthy FMCG.

Copley Fund Research

Both stocks already have an investor base among both EM Aggressive Growth and Growth funds, whilst also appealing to Value investors. As such, Copley would expect both to be on the shortlist of the many underweights and non-investors looking to ramp up allocations in the Energy sector.

Galliano's Financials Research

Exchanges - More than just trading places

Galliano believes SGX is one exchange to watch. Management has more to do to diversify the revenue base, yet its valuations are relatively undemanding and the market’s competition concerns, as in the case of B3, may be overdone.

Lynx Equity Strategies

Unless there is fall-off in end demand, shortages of IC from lagging nodes can be expected to be with us for up to 3-4 quarters, which seems quite disconcerting. End demand may in fact be already falling off in TVs, PCs and perhaps even smartphones in some geos. If so, IC shortages could ease up even before the addition of wafer capacity. The bad news – falling end demand drives down TSM’s Cy22 revenue. PT NT$600 (5% upside)

Macro Research

Developed Markets

New Normal Consulting

UK: Critical Brexit decisions lie ahead

Chief UK negotiator Lord Frost has signalled that he is prepared to suspend parts of the Northern Ireland protocol, but Paul Hodges believes he may be overplaying his hand. Should the UK suspend parts of the protocol, it will risk an escalation that could result in the suspension of zero tariff/quote clauses in the Brexit agreement, a trade war with France, and a break with the US due to its bi-partisan support for Ireland.

Suttle Economics

Don’t worry, global growth is just delayed

Q3 growth news is generally on the weaker side, but Phil Suttle believes this to be a case of growth delayed (e.g. Germany and Japan) rather than the start of a cumulative downturn. Higher inflation has also raised the reality of (and expectations for) more outside-in monetary tightening, with the EM process well advanced and the spread to DM (which will dominate 2022) now underway.

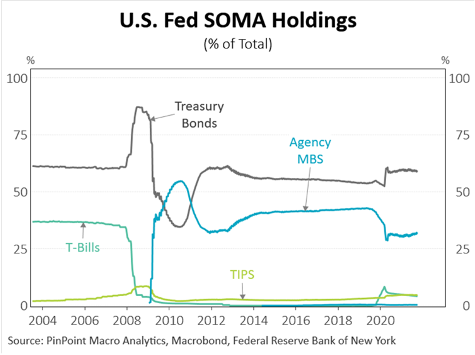

PinPoint Macro Analytics

Chart of the fortnight: US Fed SOMA holdings

Consensus estimates predict that the Fed purchase program will be scaled back by $15bn from December. It all looks simple enough, but what happens when the taper is complete? Fed discussions indicate a preference to run down Agencies and MBS, but Richard Grace and Michael Blythe point out that this will be difficult against a desire to maintain the overall size of the balance sheet and, somewhat paradoxically for a post-QE world, the Fed may end up continuing to buy Treasury Bonds.

Minack Advisors

US: Lower returns, higher volatility as equities leave Goldilocks zone

US equities are exiting a goldilocks zone of strong gains with minimal drawdowns. Gerard Minack sees the most important factor behind this being the emergence of persistent inflation pressures through 2022, increasing the prospect of Fed tightening. It won’t end the bull market, but we can expect lower returns and higher volatility. We will also see a change in equity leadership as sensitive FAAANM stocks react to rate changes.

Intertemporal Economics

US: The Fed’s Dilemma

The supply chain crisis is worsening. Problems are bubbling that only an increase in interest rates can solve. The Fed’s dilemma of long-term weakness and short-term strength is starting to play out in the bond market; in the near-term, supply constraints are driving inflation; in the long-term, deflationary pressures are emerging as low-return capital is liquidated amid higher interest rates. If the yield curve steepens too fast, Brian Pellegrini sees a dollar crisis on two fronts.

Krainer Analytics

Rapid changes in the geopolitical environment

Alongside the dizzying pace of economic development changes, Alex Krainer believes interesting changes are forming in the geopolitical arena that have gone unnoticed. In particular, Alex mentions the EU-AUS trade breakdown; significant escalation of tension in the Balkans (with potential future catastrophic results); a redrawing of Middle East alliances; and a pivot of Turkey towards a Russia-China alliance.

Antipodean Capital Management

Australia: A Great Reopening?

Craig Ferguson doesn’t believe that Australia will be undergoing a powerhouse re-opening. Nevertheless, Craig comments that re-opening plays or trades are present in recreation, travel and hospitality, which could soar to overvalued levels. AU 10yr bonds could regain 2% or more, but are a big buy up there as 3yr yields are set to rise sharply. If PMI/commodity factors become stable and the USD turns lower, it may be time to become super bullish the AUD.

High Frequency Economics

Japan: Deflation forever

BoJ Governor Kuroda reiterated his optimism last week for a recovery of Japan’s economy next year. However, recent data confirmed a severe economic contraction in August, the latest notch down in a 3.5 decade secular decline. Don’t take comfort in the latest headline CPI YoY monthly data, warns Carl Weinberg, it appears higher only due to the September 2020 plunge. The reality is, as Japan’s population shrinks, chronic excess supply and deflation remain ahead.

Emerging Markets

Totem Macro

Intra-EM country divergences to close

Whitney Baker breaks EM into two groups: the classic debtor economies that came into the 2010’s highly overvalued and that have spent the last decade adjusting the imbalances, and the growthier markets in Asia that benefitted from the outsized role of China and tech in the last weak cycle. Whitney favours the first group; she sees them as early cycle, with the best balance sheet of their lives, no external imbalances and cheap valuations. Their policy-makers are also hawkish, and they offer solid inflation protection via commodities and value-sector gearing.

Topdown Charts

Frontier markets: A compelling strategic case

Frontier markets (FM) have performed remarkably well through this selloff, outperforming both DM & EM. FMs still look good technicals-wise with solid breadth. Despite a tick-up in valuations, the strategic case remains compelling with expected equity returns on par with EM and favourable demographics. FM FX also appears oversold with valuations moving further cheaper. Callum Thomas remains bullish.

Greenmantle

China: Exporting inflation

Despite Beijing signalling a desire to avoid floodgate stimulus, it will need more short-term liquidity injections and a targeted RRR cut to keep markets afloat. Niall Ferguson expects weaker growth than expected this year (6-6.5%) and next (5%). Restrictions on industrial energy use will exacerbate global supply chain disruptions and export inflation to the rest of the world. Expect CNY to fall slowly into 2022.

PRC Macro

China: Supply constraints v. softening demand

Forget about the power shortages and production cuts in major coastal provinces, the combination of slowing land sales, new starts and local government investment has been a major catalyst for previous growth scares. The energy crunch may be softened as coal plants fire up, but William Hess sees this as an indication of Beijing undertaking a higher-carbon path than many are expecting. Even if supply-side constraints appear less binding than assumed, William still expects demand-side weakness to dominate market balances and prices.

Alberdi Partners

Argentina: Stagflation ahead

President Fernandez has indicated that the IMF agreement will be signed in Q1/2022, the first official recognition of a delay. The December $1.9bn amortization payment should be made with international reserves, which will reach 2015 lows. Despite the loan, things aren’t looking good. Marcos Buscaglia claims that consensus calls are too optimistic; he forecasts 0% growth (2.3% consensus), inflation at 66.3% (46% consensus) and FX eop at 198.8 (consensus at 155.86).

Greenmantle

India scarred

New Delhi still claims a V-shaped recovery is imminent, but Niall Ferguson is sceptical. Persistently high unemployment, lower household incomes, a rapid rise in poverty, and consumer pessimism together will force a slow recovery. Inflation will remain contained in the short-term and allow the large-cap equity rally to continue, but when the central bank hikes rates in 2022 the ebullient equity market will see a correction.

Eurointelligence

Russia: Playing the EU

Russia is putting pressure on Germany and the EU to accelerate the Nord Stream 2 approval process. It is filling the pipeline with gas, allegedly for technical reasons, aiming to create facts before the Greens enter the German government. It is too late to stop the project, but there is still a chance of its commercial viability being reduced through regulation and legal action, or even eliminated completely.

Burumcekci Research & Consulting

Turkey: A brightening outlook

Industrial production hit a new historical peak in August with a monthly increase of 5.4%, and Haluk Bürümcekçi expects a Q3 production increase in the range of 8-9%. Domestic demand maintains its strength, increasing 15% YoY, and the rate of increase in unemployment benefits is declining rapidly. As the global economy slows, the IMF has raised its growth forecast for Turkey to 9%.

Commodities

Renaissance Macro Research

The impact of rising oil prices

Jeff deGraaf’s oil impact model indicates an inverse relationship between oil prices and equities since 1986. When the model is in the 90th decile, which it currently is as oil prices break through $80/barrel, we can expect equity performance to start suffering soon. Historical sector performance for the current decile indicates that investors should look to benefit from Healthcare, Utes and Energy sectors, and avoid Discretionary, Tech and Comm. Services.

Vanda Insights

Crude’s raging bulls are missing key factors

Market voices are calling again for $90/barrel, but it won’t happen according to Vandana Hari. Such calls ignore both the fact that oil isn’t always a substitute for coal and gas, and that oil demand will be dampened by supply chain issues. Don’t expect the price to go lower either: OPEC+’s ability to influence prices and maintain stability will remain greatly diminished through the winter of discontent.

Global Mining Research

Nickel: Recycled projects adding to production growth

High prices with a favourable outlook have driven interest in nickel. Old projects are being recycled and presented with fresh economics. David Radclyffe reviews the sector, introducing the ranking system for nickel producers. Key takeaways include idled projects in Australia and Zambia predicted to restart in the near term with good economics (50-75kt/yr by 2023). David’s preferred Nickel exposure is through Nickel Mines Ltd (leverage), IGO (quality) and MMC Norilsk (Value) now upgraded to BUY.

Forefront Advisers

Blue Hydrogen: UK to push ahead despite detractors

Produced using natural gas, blue hydrogen has an important transitional role to play in the EU’s hydrogen strategy. Yet, scepticism remains, primarily around the lack of abatement. Still, Forefront Advisors believe that hydrogen is here to stay; there will be little political opposition in the UK, and despite ESG concerns there is substantial investment underway, emboldening its position in the nation’s energy roadmap.