Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

General

Could disruptive technologies in container ports & terminals be a game changer?

We are seeing a rapid adoption of innovative technologies as competition intensifies among terminal operators - DMFR notes the marked difference in strategies with some companies building on their internal capabilities and others that are acquiring specialist firms in an attempt to quickly gain an advantage. DMFR also discuss the cost saving opportunities (e.g. how automation significantly boosts APM Terminals’ margins), in addition to exciting developments such as the revolutionary BOXBAY container stacking system (JV between DP World & SMS Group) that dramatically improves a port's efficiency.

Europe

Consensus estimates need to catch up with fundamentals - this Swedish home appliance manufacturer has benefitted from a Covid-driven pull forward in demand. However, with no replacement cycle for at least 5 years and management’s cost-cutting plan derailed by the fact that nearly all ELUXB’s input costs are at all-time highs, there is no chance that FY22 earnings end up being down only 5% (which follows estimates of an all-time high earnings level in FY21 of up ~40%).

New CEO Benedetto Vigna to successfully lead Ferrari into the BEV era - Vigna will leverage Ferrari's operating model to fund a BEV transition by increasing volumes, pricing and margins. Paragon’s research also includes interviews with several former colleagues and industry sources. Feedback was unanimous - an outstanding leader; his experience as a technological innovator and senior executive will compensate for the lack of a luxury or comprehensive automotive background.

Intron’s detailed obesity model shows that Wegovy can achieve $7bn in peak sales with a path to $10bn if Medicare reimbursement is achieved. This will drive 200bps of margin expansion by 2026 (despite management guiding to a flat margin and Intron including $2.6bn higher SG&A spend and $1.7bn higher R&D spend 2021-26). Intron forecast 9% CAGR sales growth over the next five years with the potential for material upgrades (currently assumes zero sales from Alzheimer’s, concizumab, Mim-8 and the oral PCSK-9).

French small caps expert Julien Onillon believes investors are massively underestimating SEFER’s earnings growth prospects. This materials manufacturer is in the midst of a spectacular turnaround (1H21 operating profit more than doubled vs. 2019) thanks to strong growth in the solar protection, marine and furniture markets. In addition, two important acquisitions (Verseidag in Germany and F.I.T in Taiwan) should enable SEFER to accelerate growth outside Europe. The stock is valued at barely 5x this year’s EBITDA and Julien forecasts EPS growth of 50% between 2021 and 2023. TP €15.00 (~65% upside).

Green Street Advisors

Infill vs. Big Box

As infill logistics emerges as a distinct asset class from ‘Out-of-Town’ Big Box, Green Street sheds light into what the relative reletting spreads have been for the two segments. They collected 1,530 leasing renewal data points from half-a-dozen owners of industrial properties across Europe (c. €40bn AuM). The renewal/regearing uplift for Infill was ~22% vs. ~5% for Big Box and London Infill spread (+28%) crushed it vs. any other European Infill location studied. Going forward, Infill's favourable fundamentals (vs. Big Box) suggest stronger releasing spreads should persist and London Infill's c. 75-100 bps sharper reversionary yield could justifiably be wider.

North America

Blueshift Research

Which fuel cell companies are best positioned to benefit from the Infrastructure Bill?

Plug Power and Ballard Power Systems to benefit the most from The Infrastructure Investment and Jobs Act commitment to hydrogen. PLUG was cited for its industry leadership, strong management, innovation and how its recent acquisitions have expanded its offering across the hydrogen economy. BLDP is well-funded and considered the “big dog” in transportation. Other companies highlighted in Blueshift’s 31-page report include Air Liquide, Anglo American, Caterpillar, Cummins, Hyundai, ITM and Linde. Traditional oil & gas companies will also have a role to play, while Hyzon Motors and Nikola could be M&A targets.

These retailers are primed for growth in 2022

Consumer stocks are climbing the wall of worry reflecting supply chain challenges, higher distribution expense, rising prices and tough comps. Hence, there is limited visibility on the consumer sector delivering yoy F22 earnings gains. JJK highlight a select few who are well positioned for growth, including the value focused off-price retailers (TJX, Burlington, Ross) and beauty leaders (Bath & Body Works, Estee Lauder, Ulta). Upgraded growth strategies and Europe’s emerging rebound should also drive strong upside at A&F, Capri Holdings, Lululemon, PVH, Ralph Lauren and Victoria’s Secret.

Blockchain and crypto to change the world as COIN becomes a Super App - the company boasts a highly advantaged business model with an LTV / CAC >10 even under trading volume normalisation. Abacus' 2022 EBITDA estimate of $3.5bn is +50% higher than consensus. Their compelling 70-page report also addresses investor concerns re. increased regulation (will be a long-term positive) and fee pressure. TP $364 (~60% upside).

Deeply discounted - trades at an unjustified and substantial discount to large cap peers. Excess capital is $23bn! To put that into context, MFC is currently trading at ~$46bn market cap. If MFC were a bank, that would be the equivalent of the bank trading as if it was insolvent. Solid underlying fundamentals will overcome negative investor sentiment. Dividend yield >4.5%. TP C$33 (30% upside).

Growing fast but strategy remains unclear - Hong Kong tycoon Richard Li's pan-Asian life insurer aims to raise up to US$3bn in its US IPO. FWD continues to derive the bulk of its premium from slower growth markets and appears to be divesting out of a high growth market as well. Sumeet Singh also fails to see how the company has disrupted the distribution channel or is doing anything different vs. other listed firms. In addition, there are several related party issues investors should consider.

Thesis turbocharged - credible case for this being a $300 stock (~75% upside) in the next 2+ years. TRG discuss the key takeaways from HRI's recent investor day. N.America’s third largest equipment rental company is shifting into a higher growth mode through investing organically (fleet, greenfield openings) and M&A, with ongoing margin expansion moving them towards peers in the high-40% range. This should be supplemented by capital returns to shareholders. Investors to be handsomely rewarded as the "big get bigger".

Priced for perfection despite signs of growth waning - overly bullish management forecasts to leave investors disappointed. CALX has benefitted from an increase in broadband service providers adopting its software solutions during a time when people were staying at home, but those trends are now changing. Comcast and Altice USA have both recently reported a decline in broadband subscribers and Hamed Khorsand believes CALX’s customer concentration towards smaller providers makes it prone to even greater volatility with orders. 12-month TP $13 (75% downside).

On track to win a higher percentage of the Rural Digital Opportunity Fund (RDOF) than many expect - CIEN is winning the largest of these deals because of their broad product portfolio and cutting-edge DSP technology. Feedback from Sales Pulse’s industry contacts suggest recent management comments re. supply chain concerns may be too conservative and that the company is not seeing extended lead times. The other drivers of CIEN’s business, including the ramp of investment in optical transport for 5G, data center interconnect, upgrade to 800G and the transition to next generation pluggables remain intact.

Focused strategy of shifting into high margin recurring revenue markets - in addition to revenue mix, gross margin will benefit from: 1) pricing discipline; 2) increased automation within operational services; 3) richer hardware configurations; 4) increased software content within storage. No additional large restructuring programmes are required and HPE is well capitalised ($4.5bn cash) to make accretive acquisitions while returning cash to shareholders and benefitting from its H3C JV investment. TP $20 (~45% upside).

Inflection Point Research, LLC

The party is just getting started - MRVL is the best semiconductor idea for 2022. While there are many great companies to choose from, MRVL stands out as the top semi supplier in terms of multi-year growth prospects. Since Matt Murphy took the reins the company has made several great acquisitions, pulled off the divesture of the decade (Wireless to NXP Semiconductors for $1.8bn), and is poised to take on Broadcom as the dominant communications semiconductor provider focused on the datacenter.

Sector rotation just hit a major inflection point

Energy, Financials and Value are IN, Tech and Growth are OUT - that's according to market timing and sector rotation specialist Michael Belkin. Having previously had an underperform forecast for both energy (S&P Energy -26% alpha from early Mar to end Aug) and financials (S&P Financials -10% alpha from its Jun peak to its recent relative low), his model forecast has just turned bullish for both these sectors on a 3-6 month view. This rotation also feeds into a reversal for value vs. growth - Michael has a fresh sell signal and underperform forecast for the likes of Alphabet, Amazon, Apple, Facebook and Microsoft.

Australia

In a bold and transformative step, SFR has announced it has beaten off peers to acquire the Minas De Aguas Tenidas (MATSA) operation in Spain - this is one of the largest copper transactions for some time and it is not cheap (GMR estimates SFR has paid the equivalent of US$3.90/lb LT). Investor interest in the stock is likely to increase significantly given the big jump in Mkt/Cap (it would notionally now have a larger capitalisation than both Hudbay Minerals and Ero Copper). Post deal the miner is trading at a prospective 1.0x P/NPV and 5.9x FY23 EV/EBITDA.

Emerging Markets

Blood in the water - Richard Windsor explains why he believes the Chinese state intends to drive the value of the company to $0. Richard does not expect to see any let-up to the regulatory pressure now that government entities have invested $591m in rival firm Cao Cao Mobility. There is now a clear incentive to ensure that Didi goes out of business (it has already lost 30% of its user base and 50% of its opportunity since the crackdown began). Jean Liu is hoping that making an exit is going to save her company, but all the evidence points towards a far bleaker outcome.

Deafening silence from media and sell-side on HDFC’s ‘processing fee’ scandal - the latest revelations by a whistle blower reveal the shocking fact that India’s most valuable bank allegedly extorted fees from prospective loan customers who submitted false documents. If this practice is found to have been widespread then the RBI must impose stringent penalties. Hemindra Hazari believes that shareholders should review their exposures to the bank in light of these disclosures.

The rise of Chinese surgical robots

Opportunity for domestic brands amid the expiration of several patents belonging to market leader Intuitive Surgical and its da Vinci robot. Only 0.13% of surgical procedures were performed by robots in China in 2020 (vs. 13% in US). First-mover advantage in branding and costs will be crucial given 30,000 parts the R&D involves and ongoing product iteration. Re. endoscopic surgical robots (the most widely used medical robot), MicroPort and Shandong Wego lead the way with their Toumai and Miaoshou robots which are expected to be approved in 2021-2022.

One of four high conviction plays on China's new industrial ambitions - as the country's largest chip foundry SMIC is totally aligned to Beijing policy priorities and is making faster than expected progress in moving towards 7nm process technology while being able to supply domestic companies with their needs at 14nm and above (which is where the majority of demand lies). It's on the entity list but can use older generation ASML technology, with ASML likely to breach US sanctions and supply it with its latest UV technology to enter what would be a bigger market than the US by 2030. ASML and Brussels are bridling against the trans-territoriality of US sanctions.

Macro Research

Developed Markets

MRB Partners

Chart of the fortnight: Policy, economic and investment cycles are out of sync

Are we early, midway or late in the cycle? Phillip Colmar suggests that the landscape has elements of all three! Phillip’s latest report examines the implications on investment strategy; recommendations include maintaining a mild pro-growth bias, with focused bets on assets that will benefit from inward revisions in longer-term growth/inflation expectations. With yields historically depressed, investors will need to find portfolio protection outside of G7 government bonds markets, including exposure to defensive currencies.

Forefront Advisers

UK: What happens if Article 16 is triggered?

There is little confidence in the EU’s ability to prevent the UK triggering Article 16 in the coming weeks, explains Catriona Benn. Should it be triggered, tariffs could appear within a month. Fines could ensue under the Withdrawal Agreement. It is possible the EU can retaliate in other areas of the relationship, with implications for data adequacy and financial services.

UK equities: Keep calm and carry long

The FTSE100 is holding onto its breakout thus far, with solid earnings revisions momentum and an improving dividend outlook underpinning the narrative. An elevated equity risk premium, light positioning by global investors and reset in absolute valuations all support the medium-term case according to Callum Thomas, along with the deep discount vs global equities. Remain bullish UK equities.

Independent Strategy

Germany: A vote for change

The next German government will be an SPD, Greens and Liberals (FDP) coalition, forming a greener, more pro-European and more investment focused government. The changes will be gradual with the FDP in control of the Finance Ministry, but markets will worry not; the changes are in the right direction. The outcome is neutral for Bunds and the Euro, and positive for European equities.

High gas prices are putting upward pressure on EU inflation

A flurry of factors has sparked an unprecedented rally in European spot gas prices. Niall Ferguson expects prices to stay elevated, with upward pressure on EZ inflation in coming months. The ECB will nevertheless decide not to accelerate its taper schedule in response, aiming to prevent another Trichet hike catastrophe. The biggest losers will be energy-intensive industries, left once again in the lurch and forced to curtail production, dragging on the EU’s Q1/2022 economic recovery.

US: Democrats must downsize tax and spending by October 18th

It is possible for the Democrats to meet McConnell’s demands and increase the debt ceiling on their own through budget reconciliation, but James Lucier believes the party will be forced to cut the oncoming bill from $3.5trn to $1.5trn. Clean energy tax credits will survive as will other consensus revenue raisers, but everything else will have to shrink or be removed.

Renaissance Macro Research

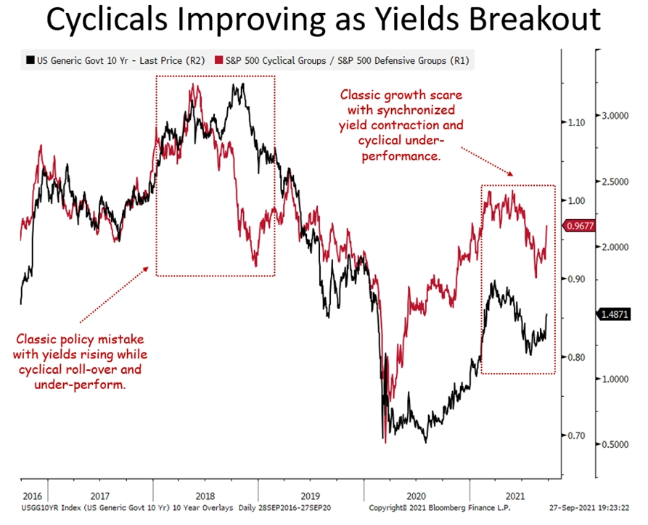

US: Cyclicals improving as yields breakout

The last few months have seen a classic growth scare with synchronised yield contraction and cyclical under-performance. Jeff DeGraaf claims that this will change as we head into Q4, with yields pushed higher and seasonality favouring the cyclicals. There comes a point where yields negatively impact the cyclical trade, but we’re not quite there yet. Investors should be wary of a potentially stronger dollar; hedge cyclical calls with the USD.

Shift from large caps into small caps

As John Karle envisaged, markets finally reacted to various factors (incl. higher rates and supply chain constraints) this week by aggressively reducing exposure to large cap growth stocks. This shift will continue as John recommends playing Russell vs S&P500 with potential outperformance for the next 3-6 months, with further exposure if the S&P500 can regain a foothold above 4500.

Australia: Monetary headwinds

The deceleration in recent months of the growth momentum of Australia’s money supply almost mirrors the rapid expansion experienced last year. Various data points remain at lofty levels on account of the 2020 stimulus, but Frank Shostak sees monetary headwinds prevailing as we move into 2022. Historical data indicates that global equities are preferred to domestic equities in similar events, and Frank moves his weighting from overweight to MAXIMUM UNDERWEIGHT.

Emerging Markets

Totem Macro

China: An unprecedented property sector bubble

China’s economic model is based on unsustainably leveraged asset appreciation, especially in the form of its unprecedented property bubble, according to Whitney Baker. There are worries of a fallout that will ripple across world markets, but Whitney claims this will be limited beyond a Japanification of China’s economy. Investors should watch property prices closely: if Beijing lets them fall in a meaningful way, the downward property cascade and social unrest scenario will become a reality.

China: A new and potentially dangerous phase of development

China is embarking on a new phase of development that emphasises stability over growth and signals the growing financialization of the economy. Evergrande marks the dawn of tighter Chinese policy control over credit, with big implications for the future hegemony of US finance. It may end up exposing cracks not only in China’s financial system but in Western finance too; Western policymakers should take heed not to dismiss the China threat!

Musha Research

China: Power and economics

Beijing is addressing China’s unsustainable growth path, claims Ryoji Musha. Their response will see a contraction in the real estate and construction sector with ensuing unemployment, difficulties in local government finances, a deterioration in consumer confidence if asset prices stop rising, and a marked slowdown in economic growth. To overcome the potential difficulties, strong social control and centralisation of power will be essential as Xi’s despotism will strengthen even further.

Latvia: A case study in population decline

Rapid population decline has already arrived in Latvia, with low fertility and a mass exodus of young people is resulting in an annual population shrinkage of -1.1%/yr, causing a host of economic problems. The country refusal to implement pro-immigration policies worsens things further. It is a warning to other nations: once the demographic tide is far enough out, it’s difficult to find your way back to shore.

Small Latins vulnerable to capital flows and commodity prices

Looking at a series of variables important to external vulnerability, including as external debt and current account deficits, Marcos Buscaglia sees Bolivia, Ecuador, Paraguay and Uruguay as the most vulnerable. Bolivia and Ecuador are the most fragile, with the former likely to struggle to keep the fixed exchange rate in an adverse external scenario.

South Africa: Take-off in sight but no signal of urgency

The SARB MPC kept rates unchanged as expected at 3.5%. There was no shift to May communication patter readying the market for take-off and no forward guidance, as Peter Montalto expected. Peter keeps his view of January lift off for a very slow and more limited cycle that fails to reach the heights on the QPM. The market is still far too fixated on QPM, especially its longer-term rates projections.

Malaysia unveils latest 5-year plan

Prime Minister Yaakob unveiled the country’s 2021-25 plan, allocating $96bn to initiatives designed to transform the nation into a high-income economy. Although the PM has yet to call a confidence vote, he appears to command a thin parliamentary majority and maintains a cooperative relationship with the opposition party. The 5-year plan will be key to restoring the economy, setting it on a robust growth trajectory and reducing income inequality.

Commodities

Crypto: The new outlaw in China

Beijing’s ban on cryptocurrencies will push all innovation in the groundbreaking sector overseas, according to Richard Windsor. Interestingly, the blockchain technology on which cryptos are built remains legal, allowing work on NFTs and decentralised finance to continue, but Richard sees them soon becoming outlawed too. The changes are among the many seeds being sowed that will see China losing the technological Cold War with the USA.

Suttle Economics

Semiconductors: Chips on the side, please

Recent chip shortages, which will not end anytime soon, have become a constraint on the global recovery. Phil Suttle sees sustained macro and sector-specific effects into the future. It is emblematic of the post-Covid world: one of strong demand and short-term inelastic supply leading to persistent price pressures; one where strong capital spending adds to global cyclicality later in the expansion; and one of growing geographic fragmentation, reversing decades of rapid globalisation.

The gold and silver bull market is not over!

CPM’s latest video suggests that weaker gold and silver prices since their Aug 2020 peaks do not represent the end of the bull market. Instead, the current sideways movements in prices are likely to be consolidation phases between a first leg upward and a second leg likely commencing in 2022. Watch here

NdPr demand to soar, providing investor opportunities

EV and wind turbine growth could see NdPr (neodymium and praseodymium) demand skyrocket from ~2,590t/pa to 220,000t/pa, according to Gaius King. Gaius forecasts NdPr shortages becoming acute far more quickly than anticipated. Only a fraction of planned rare earth element (REE) capacity will enter the market to meet the demand, with the first entrants building a monopolistic market that will block out other entrants. Opportunities are rife for investors as the Light REE sector morphs into the NdPr market, but you’ll have to be first through the door!

Higher production will rein in sugar prices

Sugar consumption is still likely to show moderated growth overall due to pandemic consumer trends. The commodity has gained support from Brazil weather and high gas prices, but production elsewhere will exceed expectations and cap market increases. Nevertheless, Judith Ganes believes it will take a downturn in other markets and easing in global supply constraints for the markets to turn sharply lower.