Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company & Sector Research

General

Insight’s Global Infrastructure Stocks Offer Massive Upside

Strong recovery from Covid, high lifetime FCF & IRR.s intact - companies covered by Robert Crimes offer an average upside of 73%. Europe (+98%) leads the way, followed by Asia Pacific (+51%) and South America (+43%). Highest average upside for Towers (+98%); prefers Inwit (+130%) to Vantage Towers and Cellnex. Airports (+81%); top pick is Aena (+131%). Stock selection in Toll roads is crucial - favours PINFRA & Aleatica in Mexico, offset by no upside for CCR in Brazil. In Contractors, Robert's top pick (and his No.1 ranked stock) is Ferrovial (+143%).

Europe

Stuck on shuffle - losing market share, estimates declining and needs fresh management. SPOT keeps reducing user guidance and is losing share to YouTube, which is winning Gen Z users. Despite spending €1bn on podcast ad tech/content, consensus estimates for both 2022 and 2023 sales and adj. EBITDA are lower than two years ago. ARPU has declined consistently despite price hikes. Ad sales compete with Internet players with better targeting and wider use cases. SPOT is struggling to realise “leverage” as prospects for a better deal from labels fade. TP $172 (30% downside).

Holland Advisors

Chewy still to come calling?! Andrew Hollingworth’s recent bull thesis (highlighted in The Cut here) has proved to be extremely well-timed as the pet food retailer becomes embroiled in a takeover battle. However, Andrew believes Chewy could still gate crash the party. If it wants to hit the ground running in pan-European expansion Zooplus is only one asset that will enable it to do that and the price it can likely get it for is hardly outrageous.

When too much success leads to suspicion - concerns remain despite the firm’s strong rebuttals of the accusations made by short-sellers. In particular, the non-certification of its accounts by EY has seriously undermined its credibility. French small caps specialist Julien Onillon forecasts a 30% drop in EPS in 2022 (vs. consensus forecasts for a 40% increase). He values the stock at 5.5 euros (35% downside). A short video outlining Julien's thesis can be found here.

Current supply bottlenecks are only masking a more fundamental problem - UBXN's obsession with developing its own chips has led to an inflated cost base that does not sufficiently focus on areas where it can gain a competitive advantage. Research Partners see no signs that the company can defend its market share (highlights Chinese rival Quectel’s rapid growth and Qualcomm’s intentions to enter the automotive market), control operating costs, make its services business a success or is willing to revise its strategy. Downgrades to Sell.

North America

$2000 anyone?! The TAIL earnings power is so much higher than the Street thinks - it’s almost ridiculous. The ecosystem RH is building is coming together quicker and stronger than expected. Global expansion will ensure ~20% top line growth for the foreseeable future, and unlike traditional retailers, RH has real pricing power. By year 5 of Brian McGough's financial model, he forecasts ~$8bn in revenue at a 25% EBIT margin - $50 per share in earnings (vs. $32 for the Street). Brian has been covering the stock since it IPO'd in 2012 and has never been more bullish. 200% upside.

The market misunderstands Nike's relationship with FL and is failing to grasp the impact that changes in the entire athletic footwear ecosystem will have on FL’s sales and margins. John Zolidis forecasts >$8 in EPS & FCF/ Share by FY23. Multiple expansion to ONLY 10x P/E - shares could rise to >$80 (+50% upside). Should Nike consider buying FL in order to accelerate its Consumer Direct offence?

Housebuilders: Look beyond 3Q results…

Alex Barron believes 3Q21 orders are likely to be the “low point” for negative order growth and investors should start building long positions / close shorts as focus turns to FY22 earnings (will benefit from higher prices and margins) and low valuations in the sector. Alex has recently upgraded the following stocks to Buy: D.R. Horton (TP $104), KB Home (TP $50) and Pulte (TP $64).

Canadian Energy Stocks: Gushing Cash Flows

Canada's 'Final Four' large-cap integrated oil sands producers are set to generate significant cash flow - Canadian Natural Resources (Veritas' top pick), Suncor, Cenovus and Imperial Oil trade at a 20% 2022 FCF yield (assuming US$65 WTI). Even if management teams spend half of free cash on debt reduction, it will still leave plenty of room for some eye-popping shareholder yields (dividends + buybacks) ranging from 8.7% to 13.5%. Veritas’ report also outlines potential M&A that could result from recent climate policy initiatives.

Brett Hart (President) sells $3.4m of stock at $45.14 reducing his holding by a massive 69% - this is clearly a concerning trade from an executive that was only promoted to President in 2020. Not only has he materially reduced his stake in the company, but it comes after long-term under-performance. It is his first non-option related sale since 2014. He currently only has 7,000 exercisable options. Stock Rank -1 (lowest rating).

Investors are underestimating further price increases - packaging markets remain exceptionally tight and global demand continues to strengthen. The US market has just seen a third containerboard price hike (August), but ERA expects another one in the coming months. WRK remains their preferred route to packaging exposure as it recovers from a cyberattack earlier this year, ramps up the gigantic new Florence linerboard machine, gains traction on boxboard increases and benefits from strong demand in Brazil. TP $62 (based on a conservative 6.5x on a 50/50 blended 2021/22 EBITDA of $3.6bn).

Atlantic Equity Research

ADSK lowered FCF and billings guidance for its recent earnings report (end of August) - management blamed not collecting all years of multi-year sales contracts upfront for one of its products as the reason why. Joe Gagan argues this is the canary in the coal mine. His channel checks consistently show that the company has been vastly outperforming its own resellers. This will correct.

US SaaS company issued USD 300m 0.25% 2026 senior convertible bond with 37.5% premium. Despite the low bond floor, delta is 54 with positive yield, and top line sales have grown by 31% CAGR. This growth company has little operating history but the demand for their services is robust as many small retailers are shifting their business online. BIGC can provide a suite of services. Mean stock target price is USD 74.64 or +31% upside.

Earnings Quality Matters

Increasingly aggressive accounting practices means it is only a matter of time before these companies face a day of reckoning:

Keurig Dr Pepper (KDP) - touts its debt reduction efforts, but a closer look reveals the company is simply moving debt to unorthodox short-term financing instruments.

Iron Mountain (IRM) - many integral cash costs are ignored by the company’s REIT metrics and are set to rise when the impact of Covid wanes. If these costs are subtracted from AFFO, IRM is not covering the dividend.

IBM (IBM) - large, never-ending charges and non-operational benefits have significantly eroded the quality of reported profit growth.

Market Cap of Companies Over 10x Sales is Out of Control

The market’s greed for speculative tech stocks is creating fantastic opportunities for long-term investors - Kailash Concepts believe now is the time to be focusing on the cheapest stocks in the market - these companies generate FCF of 5%; trade at 1x sales; P/E ratio of 22x; ~10% operating margins and 3% dividend yield. In fact, they have far more sustainable business models and having grown revenues by 24% over the last three years offer growth at a reasonable price! Some of the top ranked S&P500 firms highlighted include Molina Healthcare, Albertsons, Allstate and Ford.

Japan

Storm Research - Japan Small Cap Conference: 28th Sept - 1st Oct

A small selection of high growth, high return, uncovered companies that Storm Research believes can make the journey from small to mid to large cap. It is a unique list, encompassing a broad spectrum of models, from regenerative medicine to waste disposal & energy cost management to DX facilitation.

Companies presenting: CareNet (2150); WILLs (4482); CellSource (4880); Midac (6564); LTS (6560); Sun* (4053); gremz (3150); & MSOL (7033).

Click here to register.

Emerging Markets

Alibaba is now in a much better position than Tencent when it comes to regulatory matters - Alibaba's activities have very little bearing on societal issues that the Chinese government is so keen to address and Jack Ma has already been severely punished for his indiscretions. In contrast, the problems that Tencent faces are only just beginning. Richard Windsor believes it is only a matter of time before its financial services business is decimated by the state in the same way that Ant Group has been. Buy Alibaba, Sell Tencent.

The Rapid Growth of Cloud Gaming in Asia

The addressable market for cloud gaming in Asia is expected to grow from 150m in 2021 to over 500m by 2025. The next revolution in gaming will remove existing cost and platform barriers and as the viability of cloud gaming increases, it will allow for growth in various game related sectors such as native cloud games, live streaming, Esports, Playable Ads, User Generated Content and more. Niko Partners’ in-depth report includes the following markets: China, Japan, South Korea, India, Philippines, Thailand and Vietnam.

How to Pinpoint China A-Share Industry Cycle? Datayes Shows You the Way

By leveraging the wisdom in the Kelly criterion, Datayes' Industry Prosperity Forecast monitors prosperity trends and reflects real-time changes of industry fundamentals, supported by high frequency macro and industry data. With a daily forecast that presents high data granularity, Datayes provides early signals during your investment research process which helps to spot turning points and unveil investment opportunities. Click here for more details.

No comment from ABC despite a flurry of senior level exits at its NBFC subsidiary Aditya Birla Finance Ltd. - since May 2021, at least five senior officials in-charge of business verticals and control functions including the CFO have quit. The fact that these departures coincide with the Securities and Exchange Board of India (SEBI) investigating dodgy deals at ABFL should send alarm bells ringing for stakeholders.

Indian Banks: Screening for Investment Ideas

Victor Galliano identifies 3 banks that can weather the expected worsening of credit quality in the coming quarters - he highlights Axis Bank as a restructuring and earnings recovery story and HDFC Bank for its high quality balance sheet and premium returns, which are not yet fully reflected in valuations. Victor also considers State Bank of India as an attractive value play, despite its lighter core capital ratio. Banks to avoid - Canara Bank (value trap) and Bandhan Bank (large micro-finance and SME credit risk exposure).

Macro Research

Developed Markets

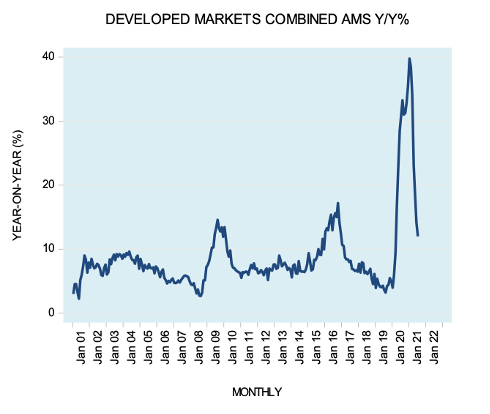

Chart of the fortnight: Negative monetary trends for the world’s major economies

Money supply trends are crucial to follow since they highlight the monetary forces that, due to the time lags involved, drive economic growth. AAS Economics' latest World Monetary Review is therefore concerning: Adjusted Money Supply (AMS) trends across the biggest nations are falling everywhere other than in China, and some AMS growth trends have even turned negative. Unfortunately, the world economy is not seeing the light at the end of the tunnel.

UK: Life, death and taxes

Boris Johnson’s social care reform is being presented as a reward to his new supporters in the North East of England, breaking a manifesto pledge not to hike national insurance. Combined with a labour shortage, Niall Ferguson sees the increased tax burden dampening an already soft recovery. Niall’s sources also suggest that Sunak is keen to raise capital gains tax rates alongside the already-planned corporate rate tax hike in 2023. Niall is underweight UK equities.

Sweden: Keep fighting the Riksbank

The Swedish Riksbank is foolish to believe that it can keep rates on hold for 3 years more than Norway’s Norges Bank, according to Manoj Pradhan. The truth is that the fundamentals in Sweden, including much higher-than-expected inflation, point to much greater similarities between the two nations. Expect at least two rate hikes over 2022-23, if not more. Paying 2y Sweden still remains the most asymmetric rates trade in the central bank peloton.

Global capex booms as companies prepare for post-Covid

Pandemic blockages, calls for green investment, the semiconductor crunch and pent-up consumer demand has spurred on investment like never before. Capex could jump as much as 13% this year. Mark Latham is hopeful that this surge offers a ray of hope into 2022 and beyond, especially when compared to the weak investment in the aftermath of 2008. This time, things are different.

Forefront Advisers

EU: Populists capitalise on energy price jump

The sharp increase in energy prices in many European countries is giving the EU’s populist right-wing parties the perfect opportunity to push back against the climate agenda, focussing their arguments on energy poverty and damaged EU competitiveness. Both EU and national governments will come under pressure to ensure that vulnerable groups are not hit by the climate policies, or the backlash will continue to grow.

Inflation and supply effects to hit the bond market

Michael Belkin argues that we are only halfway through the 2021 inflation impulse, and higher product and wage prices are now starting to develop (the Fed’s worst nightmare). We can also expect a deluge of Treasury debt issuance if Biden’s stimulus package is passed. On top of this, a flood of corporate debt is also looming. Stagflation is around the corner. SHORT US government bonds, junk bonds and EM bonds.

US: Flashbacks to 1990s Japan

Liquidity growth may have revived last week along with a surprise improvement in the country’s balance of payments, but Andrew Hunt is nevertheless concerned that the private sector credit system still looks broken. Once the Fed moves to taper later this month, liquidity stimulus will begin to dry up, and over the medium term we can expect stagflation. With the only positive counterpart to monetary growth being the public sector, we are in an unprecedented and very unhealthy situation, just as Japan experienced in the 1990s and 2000s.

US: Moderate Dems will benefit from debt ceiling concerns

A busy fall is underway in Washington as Congress tries to pass both the infrastructure ($1.2 trillion) and budget reconciliation ($3.5 trillion) packages. Driving the action, per James Lucier, will be a battle over the debt ceiling, set to start around September 30. The likely incorporation of a debt ceiling increase into the reconciliation bill will give moderate Dems huge leverage to scale back both taxes and spending.

Emerging Markets

Positive technicals underpin EM ex-Asia

Callum Thomas remains bullish EM ex-Asia, despite performance recently stalling vs EM Asia. There remains a significant valuation gap between the two and ETF market share has moved further lower, so there is a solid strategic contrarian case (value & positioning) for EM ex-Asia. FX also remains cheap and trades at a steep discount. Stay bullish EM ex-Asia on positive technical, intermarkets, valuations, positioning and FX. In particular, favour Latin America on valuations.

MRB Partners

Once again, investors are misreading China

Pessimism against China always waxes and wanes, but it has increased significantly as of late. MRB Partner’s recent report argues that, with localised lockdowns now being relaxed, the nation will remain a solid source of global demand as reaffirmed by strong import data. It is true that new policies of income redistribution will hit the monopolies, but the pessimism is nevertheless excessive, creating room for positive surprises down the road.

China: Taxing digitalisation and data

Data is the new oil for Beijing, according to William Hess. It is not only a means of social control but also a valuable source of fiscal revenue essential to China’s future. William estimates that Beijing needs to come up with an additional RMB6-8trn in new revenues per year by 2025 (~5% of GDP) if the regime is intent on limiting on-budget deficits to ~3.5%. To achieve this, we will see a combination of taxes being placed on private assets, increased dividends on state-owned assets, and taxes & fees on data and digital transactions.

What China’s economic slowdown really means?

In sharp contrast to the 2007/08 GFC, China is lagging policy actions and has been deliberately inactive since the Lunar New Year. Michael Howell believes this marks a new phase in Chinese economic development, away from growth and towards stability, evidenced by the more stable Yuan exchange rate. This is bullish for Chinese financial assets long-term, but comes at an obvious cost to the rest of the world through slower growth.

Argentina’s palace coup

Recent events in Argentina have broken the coalition into three this week and the intermediate future looks bleak. However, Marcos Muscaglia has been constructive on Argentina’s hard currency assets (and real assets such as stocks) since March on the basis of elections pushing Argentina away from a Venezuela-style path, a position which has been strengthened by the recent events. If you look past the near-term, things are looking up.

Russia and China will not rush to fill Afghan void

Moscow and Beijing have more to worry about than to rejoice at in the new Afghanistan. Both states benefit from the recent takeover as it averts further regional instability, prevents jihadist expansion and, in Russia’s case, blocks refugee flows. However, such objectives are mainly defensive; the two nations’ priorities lie in containment, and diplomatic recognition will not be followed by economic or military engagement. Concerns over a China/Russia takeover are overstated.

Intertemporal Economics

Ethiopia: Boiling Nile

Egypt is the hydro-hegemon of the Nile, a title Ethiopia is very keen to have. Brian Pellegrini comments that the ultimate reason for their building of the Grand Ethiopian Renaissance Dam is to create a new-unequal order, rather than equitable distribution, and the nation is keen to finish it regardless of feasibility. With Egypt determined to stop them gaining control over the Nile, deterioration in Ethiopia’s security will threaten the Middle East as a whole.

ESG

Pharma ESG: A sector specialist’s view

Intron Health Research’s latest report shows clear evidence that typical Pharma ESG ratings bear little resemblance to mid-term share price performance. They have therefore designed an ESG framework unique to the industry; governance is at the forefront of the model whilst social factors have a lower weighting. They show that AstraZeneca and Novo Nordisk fare the best, and GlaxoSmithKline and Roche fare worst.

Commodities

China’s production hits polyester chain margins

China’s PTA imports fell by ~1Mt whilst output nearly trebled from 17Mt in 2011 to 45Mt in 2020, a reflection of China’s drive to become self-sufficient. Margins are falling considerably, exacerbated by outside producers often cutting prices when losing out on Chinese exports, and PX, PT & PET margins have been crippled. Paul Hodges warns that we can expect other major petrochemicals to follow the same pattern as China becomes increasingly self-sufficient.

A deep insight into hydrogen

With hydrogen becoming a key component in the quest for global decarbonisation and a focal point of the automotive industry, it is more important than ever for investors to watch it closely. Metals Focus recently launched their new PGM Hydrogen Economy Quarterly, which assesses the trends, policies and technology driving the market and their implications for platinum and palladium metals demand.

Gold price to revisit 2020 high

Precious metals are inversely following USD movements but are also trading around the more sensitive drivers of inflationary pressures, interest rate movements and the discussion surrounding the Federal Reserve’s tapering plans. Looking ahead, WaveTrack International’s analysis shows gold on a broader path for a revisit back towards last year’s high of 2072.12 to 2081.00+/-.

China’s coal production sees improvement

Coal production in August is up 7% m/m and 3% y/y up to 516.7bn KwH, although it still remains relatively subdued considering how low stockpiles are. With winter fact approaching, Jeffrey Landsberg is near-term bullish on coal imports. Jeffrey’s report also features an extensive breakdown on electricity generation by type with implications for investors.