Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

Accounting red flags surface in latest filings

At Nexans, supplier financing increased, with payables under third-party bank arrangements rising from €341m at FY24 to €449m at FY25. Receivables securitisation and factoring programmes also grew, from €181m to €201m over the same period. Nordex saw contract assets rise from 37 to 48 days equivalent, offset by a matching surge in trade payables that neutralised cash flow impact. Accor disclosed a notable jump in long-term loans to Orient-Express entities following deconsolidation, while Airbus recorded an increase in receivables past due (from 25% of total receivables to 31%) and a release of provisions amounting to a total of €634m, a large amount of which was via “other risks and charges”.

Moncler (MONC IM) Italy

The shift from puffer-only to broader fashion outerwear (wool, shearling, fur) has expanded consumers’ wardrobes, with MONC well positioned at the intersection of function and luxury. Its core styles are not overly trend-led, supporting their status as long-term investment pieces with resale value. Pricing sits above Canada Goose and Herno, but below Prada and Loro Piana, sustaining an attractive premium tier. Beyond outerwear, The Retail Tracker sees opportunity in functional yet fashionable handbags (e.g., a travel line between Rimowa and Away). Footwear remains strong but still lacks a viral breakout moment. Meanwhile, early signs of a streetwear revival could lift visibility for Stone Island and help the brand extend beyond its core. Under new leadership, renewed energy in the stock could support a move back towards the 52-week high.

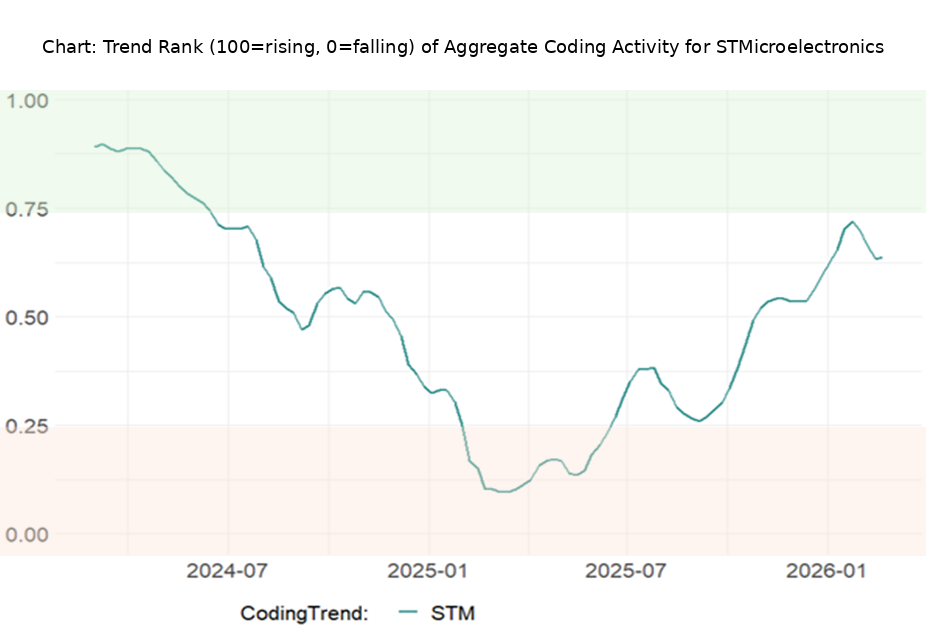

STM ranks in the upper tier of AnteData’s Coding Trend Ranking. Coding activity is trending on GitHub, showing rising developer interest in the company’s microcontroller platform. These projects typically focus on motor control, sensor reading and basic communication as used in robots, drones, cars and industrial machines. Besides, StackOverflow discussions and Google search trends are also positive, suggesting sustained ecosystem relevance and technical inquiry. In a bullish scenario (10% revenue CAGR over 5 years), operating leverage could materially expand margins, implying meaningful upside vs. today’s ~$30bn market cap.

Temenos (TEMN SW) Switzerland

US expansion is the key swing factor for TEMN over the next 12 months. With a well-resourced US sales team, a localised product suite and a pipeline growing faster than any other region, GR20 sees favourable conditions for deal conversion in 2026. They also believe the recent “Claude Cowork effect” that weighed on software valuations is fading, with sector multiples appearing to have bottomed. In GR20’s view, current valuations imply limited terminal value in DCF models - an anomaly given TEMN’s positioning and growth prospects. The stock trades at an undemanding 4.2x/3.9x 2026/27 EV/sales and 11.9x/10.9x EV/adjusted EBIT.

North America

Gross margins are rolling over, but net margin expectations remain high

Median gross margins for the Top 500 peaked at 46.4% in Feb 25 and have since fallen to 44.9% in Jan 26, yet bottom-up forecasts imply continued strong net income growth - likely reflecting embedded AI-driven productivity assumptions. Historically, Trivariate finds valuation multiples correlate more closely with gross profit growth than net income growth, implying further multiple expansion will require renewed gross margin strength or a structural shift in how markets reward earnings. Their quantitatively derived longs (e.g. Merck, T-Mobile, McDonald’s) have had recent multiple expansion and are forecasted to have margin expansion, but not more net margin than gross margin expansion. While shorts (e.g. Amphenol, Salesforce, Arista Networks, Las Vegas Sands) screen for gross margin contraction but net margin expansion, reducing estimate achievability.

AI driven 10Q / 10K text analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) AvalonBay Communities - bylaws last amended in Oct 23; is the added wording to its 2025 10K, prompted by takeover interest? 2) Diamondback Energy - loss of customers; Endeavor equityholders planning on selling shares? 3) GoDaddy - Microsoft partnership in trouble? 4) Align - more benign competitive environment. Caution on OSOs, DSOs and other large group practices. 5) Armstrong World Industries - better demand expectations. 6) Cigna - clients terminating / modifying contract terms?

Online travel & AI

Robert Mollins examines how OTAs are adapting to a rapidly changing environment driven by rising AI adoption. He focuses on 4 key themes: 1) AI as an emerging traffic channel; 2) structural advantages limiting disintermediation risk; 3) consumer-facing AI development across travel platforms; and 4) internal AI initiatives driving monetisation and cost-saving opportunities. AI companies have rapidly integrated tools into their assistants, raising concern over the technology’s ability to replicate functionality and reduce dependency on established platforms. Investor concern has extended beyond software into sectors with significant digital exposure, including online travel. While Robert acknowledges these risks, he believes AI assistants are more likely to evolve into a paid traffic channel rather than a vertically integrated travel marketplace capable of displacing Booking, Expedia and Airbnb.

Hedgeye provides updates on 3 of their top Retail shorts. For GIII, they expect the next guide for the year to be an absolute disaster; forecasting a 20%+ cash flow hit from the the loss of major Calvin Klein and Tommy Hilfiger licenses back to PVH, while prior channel stuffing and tougher retail conditions could force the company to increase markdown support to key partners. Meanwhile, VFC is caught between a heavy debt burden and weakening brand momentum; Hedgeye believes a massively dilutive equity raise will ultimately be required. And finally, DDS remains a mispriced security, trading at ~12x EBITDA despite a sharply decelerating model and the company overearning by 800-1,000bp. That suggests that the real earnings power is between $10-20 per share. 5x earnings, is an appropriate department store multiple, suggesting 80-90% downside.

Scott Mushkin remains cautious on TGT despite management acknowledging some operational challenges flagged in his field research. Recent store visits continue to reveal poor endcap execution, high levels of discarded items, long checkout lines, out-of-stocks and even extreme messiness. These nagging store operating challenges are likely to take more effort to overcome than management currently believes. He also sees several structural pressures ahead. TGT may need to sacrifice gross margin to improve price competitiveness, while everyday essentials could face deflation in 2026 amid heightened competition. Meanwhile, Walmart and Amazon are unlikely to cede share and TGT’s core demographic offers limited growth. Scott believes the recent swing to positive sales reflects easy comps and short-term consumer spending variability rather than a structural improvement in demand.

A large-cap trading at just ~11x earnings, with a ~12% FCF yield and will pay owners a 10% yield in the very near future. The Coterra deal markedly increases DVN’s stature and shale production in the Delaware Basin without incremental acquisition debt, adding ~4,600 high-return drilling locations, nearly half with sub-$40/bbl breakevens. The combined company expects $1bn+ in annual synergies and plans a $5bn buyback, materially lifting FCF/share and NAV/share. Nevertheless, investors have yet to adequately reflect DVN’s improved fundamentals in its share price, with it continuing to trade at a sharp discount to other E&P players in terms of both P/OCF and at a high required FCF yield. For each 0.5x improvement in its P/OCF multiple or a 1pp decrease in its FCF yield, DVN’s share price will rise by ~$5.

IgA nephropathy: Optical leadership or structural advantage?

Vertex's IgA nephropathy is being valued on perceived differentiation rather than durable commercial advantage. Foveal's report dissects how alignment, baseline architecture and segment economics reshape probability of success and peak sales assumptions across the class. They identify where consensus expectations appear stretched (VRTX, Vera) and where valuation leverage remains underappreciated (Otsuka, Novartis) ahead of key 2026 catalysts.

Sidoti reiterates their constructive stance on LMAT, arguing the company’s increasingly dominant niche positioning supports durable pricing power, margin expansion and visible multi-year growth. With price increases contributing meaningfully to organic growth and ~8% additional pricing expected in 2026, Sidoti sees LMAT as insulated from reimbursement and tariff pressures given its focus on critical, non-deferrable vascular procedures and predominantly single-use devices. The company will continue to benefit from the continued sales force expansion and additional European product approvals over the next several years. Backed by a strong balance sheet and capacity for accretive M&A, Sidoti increases their 2026 revenue estimate to $275.5m (from $264m) and EPS estimate to $2.86 (from $2.39). For 2027, they raise their revenue estimate to $291m (from $278m) and EPS estimate to $3.09 (from $2.67).

ESI exited a record 2025 with DD organic growth in Electronics and Fermium expects this momentum to continue, which was the key underpinning behind their positive initiation last Sep. Against this favourable backdrop, ESI has accelerated its efforts with two acquisitions, Micromax and EFC Gases, completed in early 2026. The company has exposure to datacentre infrastructure and high-performance computing, yet trades without the “nosebleed” valuations seen elsewhere in the AI supply chain. EBITDA grew MSD in 2H25, with implied 2026 guidance pointing to nearly double that pace - before acquisition contributions, which should lift growth into the mid-teens. Buy reiterated.

CEO Andrew Florance’s destructive leadership style makes him unfit to lead CSGP’s costly residential pivot. His rigid, totalitarian micromanaging is incompatible with the disciplined, multi-front execution now required, making his past strengths his current greatest liabilities. CSGP would be better served with Florance receding into an Executive Chairman role, where his visionary strategic brilliance could be offset by a disciplined operational CEO more focused on ROI than empire building. Paragon’s research includes interviews with former senior executives at CSGP who worked with Florance for more than 36 years combined.

Rosenblatt reiterates their Buy rating and Top Pick status on AAOI. The company invested $209m in capex in 2026 with a focus on increasing laser and transceiver capacity in Texas. This ongoing investment is poised to drive a tripling of Data Centre revenues in 2026 and even faster growth in 2027. Amazon and Oracle 800G demand are the primary revenue drivers in 2026 along with Microsoft's solid 100G and recently renewed 400G demand. By 2027, all these customers should also be buying 1.6T. Rosenblatt’s 2026 revenues/EPS estimates increase to $1.02bn/$1.18. For 2027 their respective figures are $3.3bn/$6.25. Their new TP of $125 is based on 20x CY27 EPS forecast - a conservative multiple to account for execution risk.

Nvidia's "Flammable Items"

Following NVDA's Q4 earnings release, Veritas believes several “Flammable Items” (these are items found in a company’s financial statements or within its operations that are waiting for a spark to ignite) it has previously identified are burning brighter and warrant continued investor attention. Their report examines whether supplier-funded demand is accelerating through channels including equity investments, a step-up in purchase commitments and expanded facility lease guarantees. The scale of these funding channels has increased materially, to the point where NVDA can effectively self-fund most of its reported revenue growth in the quarter. Veritas also isolates the contribution of “other income” in Q4 and presents an adjusted EPS intended to better reflect underlying operating performance. On this basis, they suggest that nearly the entirety of the Q4 EPS beat was attributable to “other income”.

Japan

Nichias (5393 JP) Japan

With a market cap of $3.6bn, Nichias is an industrial insulation company that Asymmetric has followed for over 20 years. While the shares have outperformed the TOPIX over the long term, the performance gap has widened materially in recent periods, a trend Asymmetric believes can continue, highlighting the group’s: 1) cash-rich balance sheet and strong FCF, supporting rising shareholder returns; 2) ability to raise margins across its business segments; 3) exposure to maintenance work related to nuclear restarts in Japan; and 4) earnings gearing to the slower than initially expected SPE cyclical pick up.

Emerging Markets

China Internet: Opportunity after KWEB’s ~30% drop from its Oct peak

Sector valuation, as measured by 86Research’s proxy basket, now stands at a distressed 15.4x. Over the past 3 years, there has been 5 KWEB drawdowns >20% and each peak-to-trough episode lasting 3-6 months, suggesting the current correction could be nearing its end. Several catalysts may also help stabilise sentiment including Trump’s visit to China, the upcoming Two Sessions (additional stimulus) and improving economics from China’s AI leaders. In this issue of 86TradeIdeas, the team highlights several quality names that could command significantly higher multiples in a normalised market, including Trip.com, Atour and DiDi, alongside Beike, which could benefit from further housing policy support. Kuaishou and Baidu offer differentiated exposure to key AI verticals. Despite near-term geopolitical uncertainty, they see compelling re-rating potential across these names in the coming months.

Why (some) EM Telcos’ multiples could double

The resumption of pricing power is one of the key drivers of the rally in EM Telcos and perhaps the area where consensus is most sceptical. In this note New Street analyses which markets have the greatest potential for sustained pricing power, looking at key issues: affordability and regulatory and competitive structure. Where these come together they see the potential for a multi-year period of above-inflation revenue growth from the core telco business. They also show that where pricing power is sustained, EM Telco multiples have doubled. As this plays out across the industry the scope for above market returns are high, and New Street remains (very) bullish on EM Telcos.

China: Channel checks on leading coffee & tea brands

The competitive environment across the country's leading beverage chains appears to be shifting from aggressive subsidy-led share grabs towards more rational pricing and product-led differentiation. For global investors, this suggests: 1) margin recovery potential after a prolonged discount cycle; 2) strengthened positioning for category leaders with innovation capabilities; and 3) continued consolidation towards scaled operators with diversified product offerings. Luckin’s near-term fundamentals look resilient with Jan SSSG likely >10% and pricing/ASP recovering sequentially. Mixue was modestly softer due to the CNY timing shift, while Guming was a clear relative winner among tea chains with SSSG/GMV +10-15% (still HSD even ex delivery fees) and momentum likely improved further in Feb on holiday & platform campaign effects.

Macro Research

Developed Markets

The West’s plague of idiots

From David Murrin’s five stages of Empire perspective, the West is suffering from a “Plague of Idiots”. David says it is increasingly evident that the leadership and Western society are experiencing a profound crisis of competence, judgment, and cortisol with which to drive our sense of collective danger and motivation to see and react to the oncoming threats. This crisis extends well beyond individual policy failures; it reflects a civilisation in the late stages of institutional decay and declining effectiveness. The Western order now appears weakened by a loss of strategic understanding and professional competence, and is increasingly marked by complacency, self-absorption, and managerial mediocrity. In an era defined by great-power competition, missile warfare, and systemic instability, such leadership deficits materially increase strategic risk. If left unaddressed, the imbalance may prove the most serious long-term threat of all, and the “Plague of Idiots” will inevitably sabotage the existence of our Western democratic civilisation.

Approaching peak AI hysteria

People are gregarious and instinctively follow the impulses of the herd, remarks James Aitken. The past two weeks have been a reminder of the mob mentality, and with dystopian projections on AI hysteria reaching millions of views, James believes we are approaching peak AI hysteria. Just remember when scouring the news: why am I reading this now and who benefits? XAI, Anthropic and OpenAI are all in windows to raise absurd amounts of money at lofty valuations, so it’s no surprise everyone is getting almost daily updates on LLMs about their improvements. DRAM, NAND and H100 rental prices suggest the AI juggernaut and associated memory shortage continues, yet so violent has been the recent shakedown that companies that would seem to have little risk of being disrupted by AI have been smashed, too. Just look at the current P/E of Microsoft (green) vs the current P/E of Colgate (red).

Making sense of the Citrini AI debate

Cam Hui reviews the controversial report recently published by Citrini Research that rhetorically asked, “What if our AI bullishness continues to be right...and what if that’s actually bearish?” The Citrini report postulates a scenario where AI wipes out millions of jobs, while AI boosters assume widespread productivity gains without disruption. Cam notes that the history of the adoption of disruptive technology indicates that outcomes are never utopian nor apocalyptic. He therefore prefers to adopt a middle ground. Artificial intelligence is a very real technology and its adoption will dramatically change society. There will be some degree of disruption in capital markets and return expectations. Cam points out that the AI bubble never reached the excessive levels of the dot-com bubble, and the degree of price adjustment will be lower. In all likelihood, its collapse will not cause a recession.

US manufacturing PMI does not set a new trend

Carl Weinberg points out that the US manufacturing PMI for February printed above its break-even level for a second month in a row, signalling an expansion in the sector. This is a surprise, and a positive one at that. However, Carl notes that the uncomfortable truth is that the correlation between headline ISM manufacturing and current-quarter GDP growth over the last decade is below 0.30. The economy has demonstrated it can grow without industrial growth, which has declined as a share of overall economic activity. The manufacturing sector is sick, barely growing at all. It has been contracting for a long time, and a print or two above 50 does not set a new trend. In short, manufacturing does not appear to be responding well to Trump’s economic policies. Tariffs do not seem to be increasing the business of existing firms, as this survey suggests, or creating new jobs in new firms as the payroll employment data suggest.

Japan: The balance of payments and the yen’s outlook

Andrew Hunt says that is difficult to gain a clear picture of Japan’s true Balance of Payments trends; some of the relevant data seems contradictory. Rising JGB yields have slowed capital outflows from Japan (predictable) but not reversed them. Elsewhere, foreign investors have been moving back into JGBs (intriguing) and Japanese equities (interesting). The foreign interest in Japanese equities and the importance of these flows within the BoP data arguably makes the JPY more of a “risk on” currency than safe haven. In the near term, Andrew expects the JPY to remain “choppy” with a bias towards being positively correlated with risk appetite, but any sharp falls would likely be resisted in the near term by foreign central banks. Longer term, Andrew says that the fate of the JPY is inexorably linked with that of the BoJ’s credibility, something that he expects to be undermined over time by fiscal primacy.

Emerging Markets

Emerging Markets: Stay the course

Callum Thomas points out that EM equities are pushing higher in local currency and US$ terms following the previous breakouts (+strong breadth), and the EM vs DM relative performance line is also pushing higher after chalking up a clear inflection point. EM consensus forward earnings are surging, breaking out (basically a fundamental breakout to back the technical breakout). Investor sentiment is starting to get extreme/overheated, as would be expected during a big inflection point and trend change – but it does make it liable to pullbacks as things have moved quickly and far. Valuations still have room to run vs history and vs global peers, but it is clear that EM equities are now no longer cheap. The EM stock/bond ratio is pushing higher after previous breakouts but relative sentiment and relative value are getting elevated. Callum remains bullish EM equities.

A new Gulf war begins

For months, Jawad Mian has been writing about the situation in the Middle East and about the likelihood that Iran would eventually face an attack. He says this is not another short episode, but the beginning of a far longer cycle of instability. For the US, rising oil prices or market disruption could become a political liability ahead of the November mid-term congressional elections. With the joint US and Israeli strikes on Iran intensifying and the killing of Iran’s Ayatollah Ali Khamenei, the entire strategic landscape of the Middle East has tilted. Jawad sees three objectives driving this conflict: regime change, neutralising Iran’s nuclear threat and controlling Iran’s oil exports. However, regime change requires troops being on the ground; instead Jawad observes that what we have is a heavy intelligence footprint, targeted strikes, leadership decapitation efforts and infrastructure degradation. This can destabilise a system, but it does not automatically produce a new one.

Iran: The War in English

The “War in English”, as jokingly referred to by Israeli officials, has settled into an intense but steady pace. Niall Ferguson believes that US and Israeli objectives remain on track despite a geopolitical expansion of the war. Should Iran prove unable to muster larger missile or drone salvos by the end of the week, it would seem likely that it has no remaining capacity to do so. This should give shipping firms and insurers more confidence to begin transiting the Strait of Hormuz next week. If disruptions to the Strait continue into next week, Niall expects a major and coordinated SPR release from net importers to take place to reduce the stress in global crude markets. However, the potential costs of a protracted conflict and closure of the Strait is being underestimated by markets. It is imperative not only for the Trump administration’s political self-interest but also for global economic stability that the duration of this war be measured in weeks, not months.

Brazil: Stagnation ahead

In the fourth quarter of 2025 Brazil’s GDP rose 0.1% QoQ s.a., broadly in line with the market median (0.1%) and BuySideBrazil’s projection (0.0%). Compared to 4Q/2024, GDP increased 1.8%. In Q4/2025 Brazil’s economic growth relative to 3Q/2025 was mainly driven by stronger exports and services. Services, slightly above expectations, posted a positive performance in the quarter, supported by higher consumer income amid a still-robust labour market. However, Andrea Damico says this momentum already shows signs of exhaustion, with a potential turning point in H1/2026. The key highlight is the sharp slowdown in domestic demand, with the weakest marginal performance in domestic absorption and private consumption since the end of the pandemic in 2021. The clearest sign of this fragility was the sharp decline in imports. Overall, this data reinforces Andrea’s view of cooling economic activity and stagnation in the first half of 2026. BSB’s projection for 1Q/2026 is 1.1% QoQ s.a.

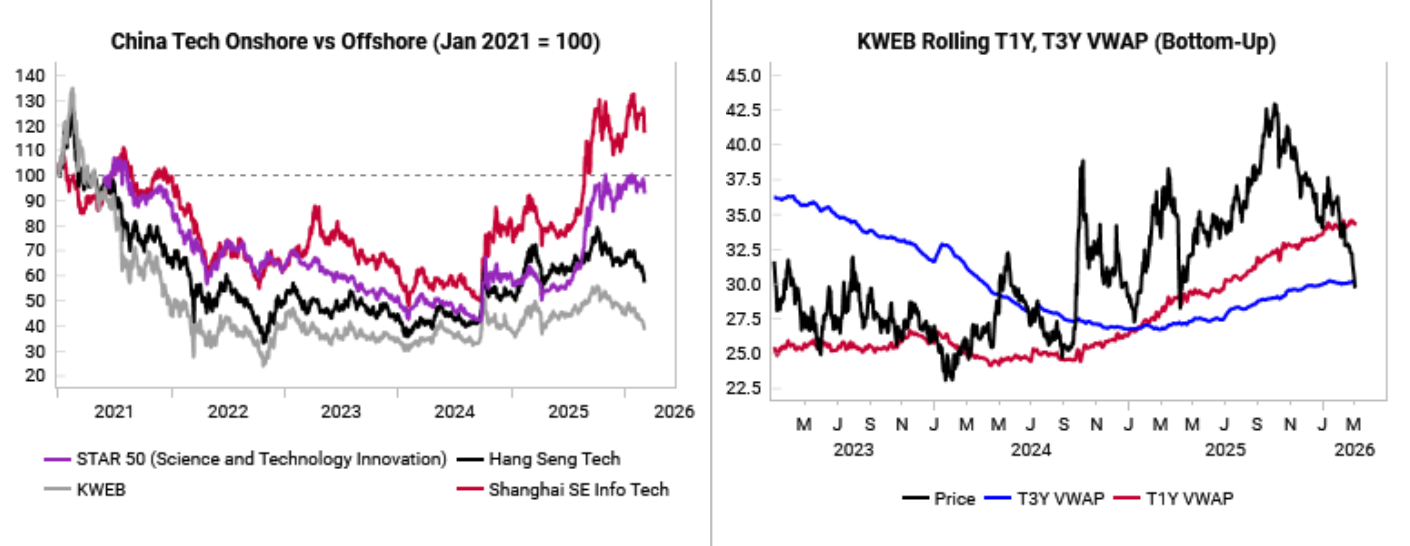

Buy the dip on China tech

Offshore Chinese tech equities have materially lagged onshore equities over the past 6 months, suffering big drawdowns even as onshore equities make new highs. The KWEB China Tech ETF has now fallen down major support levels at the T3Y VWAP (see charts). The Variant Perception team are starting to see more LPPL crash exhaustions signals for Chinese tech stocks, while their fast money speculative flow proxy shows that they are approaching contrarian buy levels for KWEB. MSCI China is now underperforming the MSCI EM index by a wide margin, with the trailing 1-year relative performance below -2 standard deviations. Despite this, Chinese small caps have been outperforming large caps, a positive divergence that bodes well for future Chinese equity returns. There is a chance the Iran situation will worsen, and Chinese assets will be further caught up in the energy shock, but there is already a decent amount of dislocation priced into Chinese tech equities. Ultimately, this is an attractive entry point for investors.

South Africa’s macro big bang is underway

According to Peter Attard Montalto, the macro big bang is underway in South Africa and has entered a new phase of focus on risk premia compression. The yield curve has extended its repricing lower as the fiscal credibility reset at the 2025 budget statement has held - and was reinforced by Budget 2026 last month. The 10-year yield is around 8.2% as of March 2nd, its lowest level in 5+ years. Sovereign risk premia have continued to compress, as the fiscal golden threads remain intact despite not-too-exciting growth, while the de jure shift to a 3% inflation target has helped anchor longer-run inflation expectations and real rates. With the SARB delivering back-to-back 25bps cuts in May and July, followed by a further cut in November, the front end has repriced lower, and the curve has flattened, with the belly and long end doing most of the work as fiscal uncertainty turned into fiscal positivity and inflation risk premia compressed.

South Korea: Words of warning

Jonathan Anderson observes that Korean equities shot up another 50% in the first two months, making Korea the best-performing market on the planet in 2026 so far. He notes that this is heavily due to the AI boom and Samsung, but "domestic Korea" has continued to rally this year as well. However, there's still no support from domestic macro. As before, Korea's economy is flatlining or contracting almost everywhere he looks: durables, construction, retail, credit, earnings. And while exports are rebounding, memory prices still haven't been able to bring Korea back to the EM-wide average trend. Jonathan says it will be hard to motivate further gains in local names. Equity multiples have already eliminated the famed "Korea discount" and continue to rise at the margin, i.e., corporate reforms have already been priced in well in advance of actual results - and there's no sign that the rally is boosting earnings and growth potential as of yet.

Commodities

Wheat joins the bull market

Spot wheat stands at USD5.91. Chris Roberts points out how the USD4.50-5.50 area is viewed as a floor, based on price action since 2007 (floors and ceilings can be penetrated but sustained moves are needed to change them). The 64% decline in 2022-25 is in line with other major falls since 1996, that range from -63% to -73%. The 9-Quarter RSI bottomed just below Low Neutral 40, similar to the 2016 low. Chris’s base case is that commodity bull market has resumed and he has a number of commodity-related longs. In the Grains and Oilseed complex, he has longs in soybean and soymeal and is now looking to add wheat.

Oil: Into triple digits

Vandana Hari sees a risk of the conflict sliding into a war of attrition in the Gulf, with both sides expending missiles, drones and air-defence interceptors while testing each other’s stockpiles and endurance. The US may have already missed the window for a “strike hard and fast” outcome. Tehran is willing to stake everything and has mistakenly expected Gulf states to pressure Trump’s administration into standing down. For oil prices, the worst may still lie ahead; the market is still pricing in a least-bad outcome, one where the Strait of Hormuz reopens before long. One reason Washington may have refrained from unveiling sweeping measures to cool prices is that it is keeping its powder dry for a potential — perhaps expected — surge towards triple digits. Crude, products and refining cracks risk being bid into a vacuum if physical flows remain paralysed. Stay tuned.

Start slowly closing oil positions on any further rise in price

William (Buff) Brown observes that the US/Israeli-Iranian conflict has spread throughout the region with major interruptions in oil transit in the Arabian Gulf, with Iranian missile strikes in neutral Gulf countries, i.e. Oman, Bahrain, UAE, etc. While most were strikes directed against US assets, there were also strikes against civilian areas. With regard to oil transit, Iran has claimed that the Strait of Hormuz is effectively “closed”. However, it is not closed in the sense that Iran is, as of yet, targeting vessels en masse and/or has mined the 2-mile-wide outbound channel. The situation remains highly dynamic, however, and could change one way or another at any time. In any event, with the prompt NYMEX crude oil contract trading above $70.00 per barrel, he suggests maintaining the status quo for the time being, but on any further material price strength slowly begin closing out long positions. He does not recommend going short as prices rise.

Helium: A commodity on the rise

Ben Finegold points out how the global helium market is a structural oligopoly, Qatar accounting for ~30% of the world’s helium supply. A prolonged conflict in the Middle East that disrupts production or shipments through the Strait of Hormuz could put a third of the world’s supply at risk. More importantly, the availability of helium iso-containers – critical to maintaining a global supply/demand balance – could be disrupted for at least 6 months. Demand for the commodity is accelerating, particularly in the aerospace industry where it is irreplaceable as a propellant of fuel. It is also used in semiconductor manufacturing and healthcare, where substitutes have yet to be found. How should investors play it? The Renergen Helium project, owned by ASP Isotopes Inc, produces both LNG and high-purity liquid helium from the same gas field, and is one of the world’s most significant helium developments and aims to become a major supplier.

Gold stocks chasing copper

The proposed acquisition of Foran Mining Corp by Eldorado Gold Corp, following Harmony Gold Mining Co Ltd acquiring MAC Copper, highlights the appeal of base metal mines for some gold miners. A few companies are forecast to increase base metal exposure, namely Torex Gold Resources Inc with Media Luna, Eldorado Gold Corp with the start-up of Skouries and the acquisition of Foran Mining Corp for the new McIlvanne Bay copper-zinc mine. Two primary reasons for gold stock to chase base metals are operations with minor gold can be reported as “low-cost gold mines” and the EV thematic remains appealing. Copper remains the preferred base metal for GMR, but gold is the preferred commodity for 2026. Recommended gold stocks are Barrick Gold Corp, Agnico Eagle Mines Ltd (upgraded to BUY) and Kinross Gold Corp in the seniors and Equinox Gold Corp, Genesis Minerals Ltd, IAMGOLD Corp and OceanaGold Corp for near-term growth-oriented stocks.