Europe

Consumer Discretionary

ITX faces a “perfect storm” of structural, regulatory and consumer headwinds. Consumers are showing trend fatigue, increasingly shifting towards second-hand and longer-lasting purchases, with resale markets now outgrowing fast fashion. EU regulation is tightening, while initiatives such as Zara Pre-Owned are viewed as largely cosmetic greenwashing. Operationally, store closures and a pivot to large city-centre flagships risks worsening accessibility and competitiveness vs. ultra-fast online rivals like Shein and Temu. With discretionary demand under pressure, FX and tariff risks looming and no meaningful innovation, AIR argues 28x 2026E earnings leaves ITX priced for perfection. Added to this, they flag succession risk, noting that Marta Ortega is not Amancio Ortega and the absence of a true visionary successor is a key strategic weakness.

Industrials

RAND offers an attractive risk-reward anchored by a “virtually guaranteed” dividend yield of 5.6%, providing support for the share price. The company’s FY25 FCF is more than sufficient to pay shareholders the conditional ordinary cash floor dividend of EUR 1.62 per share and is highly likely to be repeated thereafter. Beyond income, the IDEA! sees scope for a share price recovery as staffing markets across the company’s key geographies appears to have bottomed. The US market is improving, France may be nearing a trough and conditions in the Netherlands have stabilised. Trading on undemanding multiples (EV/EBITDA ~7.9x), RAND is preferred over Adecco and ManpowerGroup due to its superior FCF generation and sustainable capital returns.

Materials

AlphaValue reiterates their negative stance on WCH after weak FY25 prelims disappointed, even against already low expectations. While sales broadly matched consensus at ~€5.5bn, earnings told a harsher story: adjusted EBITDA missed by ~5%, hit by weak pricing, soft volumes and persistently low utilisation rates that continue to crush fixed-cost absorption. Adjusted EBIT collapsed to ~€20m vs. ~€50m expected, with a further unexplained shortfall at net profit level. The year was also weighed down by heavy one-offs, including ~€100m of restructuring costs, ~€310m of Siltronic valuation adjustments and significant tax and goodwill impairments. Lower capex and some inventory release may support near-term FCF, but with demand still weak and utilisation low, AlphaValue sees little to change the earnings outlook.

Technology

SAP’s shares fell 16% on a minor shortfall in current cloud backlog growth and slightly softer 2026 cloud revenue guidance, despite FY25 results broadly meeting or exceeding expectations and strong 2026 profitability and FCF guidance. The underlying drivers reflect timing and mix effects rather than weakened demand. There is no evidence that SAP’s plan to accelerate revenue and operating profit growth by 2027 has been compromised. Cloud growth >20% by 2028 and operating margins of 30-31% by 2027 remain achievable. While investor concerns around AI agents have weighed on sentiment, SAP’s deep integration of applications, data and AI, combined with its embedded, extensible agent strategy and AI-enabled ERP migration opportunity, positions it competitively. Current valuation levels appear reasonable considering expectations for a 14% adjusted EPS CAGR over 2025-2028.

North America

Two earnings trends the market is missing

YWR’s Global Factor Model (which screens 4,000+ global stocks across estimates, valuation and price momentum) flags two themes that remain underappreciated by the market. Earnings estimates for US regional banks are rising sharply, yet share prices have barely reacted. Loan growth is reaccelerating, deposit costs are moderating as rates fall and credit quality remains strong - signs that lending activity and “animal spirits” are returning. At the same time, the energy complex is showing a broad-based inflection in forward earnings across multiple sub-sectors, pointing to a cyclical turn. The pickup in estimate momentum across US banks and oil services has also strengthened the relative momentum of the US vs. other markets. Stock-specific ideas are available on request.

Communications

Josh D’Amaro’s mix of leadership and operational qualities make him a strong choice to succeed Bob Iger as CEO. A 27-year Disney veteran, D’Amaro is viewed as a high-EQ leader who balances creative ambition with financial discipline. He is currently tasked with overseeing a $60bn capital plan over the next 10 years to turbocharge growth in parks, cruise lines and resorts, generating the FCF required to support the company’s riskier media transformation. While he lacks direct media experience, he has a proven track record of turning around underperforming assets and successfully navigating crises, including rebuilding the Experiences’ division profitability post-Covid. Paragon’s report includes interviews with former senior executives who worked with D'Amaro for more than 75 years combined.

Communications

Craig Huber updates his forecasts following another strong quarter from the company. He now estimates 1Q26 revenue of $55.9bn (+32% Y/Y) and EPS of $6.99, well above Street consensus of ~$6.56. His FY26/FY27 EPS estimates are $28.65/$34.45, with EPS dipping in 2026 due to significantly higher depreciation assumptions tied to AI infrastructure spend. Craig forecasts FY26/FY27 revenue up 23.4%/15.4% to $248bn/$286.2bn, driven by Family of Apps growth of 23.4%/15.3%, including advertising up 23.2%/15.0%. Reality Labs revenue is seen rising ~20% in both years, helped by AI glasses and a Quest 4 launch this year. Despite higher costs, 2026 operating income is still expected to grow Y/Y to $85bn and to $102.9bn in 2027. Craig’s new 12-month TP increases to $880 (35% upside).

Consumer Discretionary

Brian McGough thinks the market is materially overestimating the company’s long-term earnings power. Investors are buying into BOOT’s ambition to expand from ~515 stores to 1,200, but Hedgeye’s M.A.P.S. (Market Area Performance Study) analysis suggests the company has already exhausted its most profitable “power alley” stores tied to mining, agriculture and construction - locations with a healthy 70/30 workwear-to-fashion mix. Incremental growth is now shifting to more expensive, fashion-heavy stores that rely on a Western Wear trend that Brian believes is in the late innings. In aggregate, he estimates BOOT needs ~7% comps just to leverage occupancy (the highest hurdle in retail), while many new stores carry rent escalators exceeding 10%. Brian sees sustainable EPS closer to ~$4 vs. consensus TAIL expectations >$8, implying up to ~75% downside.

Cautious optimism in discretionary retail with Home Improvement a winner

Consumer Discretionary

Scott Mushkin turns incrementally more constructive on the 2026 outlook for discretionary retail, arguing that a gradual moderation in inflation for “have-to-have” items, lower interest rates and steady wage growth could create a better backdrop than a year ago. He sees middle-income households as the key beneficiaries and highlights home improvement as a relative winner, helped by potential catch-up demand after years of underspending on household durables. Against this backdrop, he upgrades both Lowe’s and Home Depot to Hold from Sell, almost 3 years after he downgraded them. Scott also believes the difficulties facing the in-home consumables industry could get worse in 2026 and would avoid most, if not all, the equities, especially companies such as Kroger and Target that compete directly with Amazon and Walmart, who will continue to use aggressive pricing to drive market share.

Healthcare

RDNT’s AI narrative is materially overhyped relative to fundamentals. The AI business remains nascent, loss-making and largely unreimbursed, with equipment vendors increasingly bundling AI into imaging hardware, eroding RDNT’s perceived edge. Meanwhile, the core business remains highly capital intensive: imaging equipment is costly and capex has consumed ~50% of EBITDA for several years. Lately, that is 10% of sales in a mid-teens margin business, more than twice that of Two Rivers’ selected comp group. Operating leverage is limited as labour, equipment and supply costs continue to rise. While RDNT has reduced its leverage, it is still a concern at 4.4x forward EBITDA. The stock is priced to perfection, trading at all-time high EV/Sales, EV/EBITDA and earnings multiples. It has historically traded at a 40-50% EBITDA multiple discount to the comps - now it trades on par with them.

An early, data-driven read on MedTech trends

Healthcare

Medmine analyses purchase order data from 3,500+ US healthcare providers, providing investors with an early, differentiated read on demand and revenue drivers. Last year, they captured several trends including tariff impact & pricing resilience, supply chain disruptions, Pulsed Field Ablation (PFA) adoption in EP labs, TAVR market resurgence and a robotics supercycle. Crucially, Medmine’s models provide a more accurate read on company performance than comparable market estimates. They averaged a 1.5% error rate, compared to 4.1% for consensus through the first three quarters of 2025. Additionally, their models tracked within 1% of reported actuals in 68% of cases, while consensus estimates met that threshold in only 13% of instances. Their Q4 models, incorporating Dec data, are now available. Contact us below for further information.

Industrials

Hamed Khorsand initiates coverage with a Sell rating, arguing that reported growth is driven more by aggressive accounting and acquisitions than underlying cash generation. While demand from hypersonic missiles, tactical defence and space has lifted backlog, unbilled revenue now exceeds 43% of reported sales, driving earnings growth without translating into FCF. Gross margins contracted in Q3, organic backlog growth is slowing and the balance sheet remains levered, leaving little support for KRMN’s elevated valuation. Recent acquisitions introduce additional risk: retaining all employees could jeopardise small-business status, potentially leading to contract losses in 2026, while management’s 2026 revenue and EBITDA guidance appears aggressive as margins trend lower. Hamed also notes that PE owner Trive Capital fully exited at $49, reinforcing his cautious stance. 12-month TP $37 (60% downside).

Materials

Forensic Alpha raises their risk score sharply after Dow’s 10-K highlights balance-sheet concerns tied to the Sadara JV with Aramco. Their report highlights a $901m negative investment balance linked to sustained losses at Sadara, reflecting Dow’s exposure through guarantees on ~$1.3bn of debt and a $500m revolving credit facility. Despite these losses, Dow’s net debt has risen only modestly and no new loans to Sadara have been disclosed. Forensic Alpha suggests the company has instead supported Sadara via favourable working capital movements, helping explain weak OCF over the past two years. Notably, 10-K language now indicates performance under guarantees is “no longer remote” ahead of Sadara’s 2026 refinancing. With negative FCF, restructuring costs and rising minority cash leakage, investors should question dividend sustainability and the growing gap between EBITDA and true cash flow.

Low Units, Big Signal: Enterprise networking quietly catches up to AI

Technology

Enterprise networking is quietly ramping to catch up with AI infrastructure buildout, though early-stage volumes keep this trend under the radar. Cisco recently began its ramp and JNK's supply chain research shows system assemblers building dedicated capacity for both CSCO and Arista Networks switch programs alongside optical connectivity. The 800G transition provides a multi-year tailwind with cleaner margin profiles than AI system assembly, where OEM-directed procurement compresses economics. Modular data centres are also gaining traction as pre-built units integrating server racks, power and cooling reduce construction timelines by ~30% while expanding addressable value from 40% of DC CapEx to 60-70%. As hyperscalers work through power constraints gating AI deployments, networking and optical infrastructure scale in tandem, with unit growth still in early innings.

The Hidden Tailwind: Extending useful lives in AI infrastructure

Technology

Depreciation assumptions have become a meaningful, underappreciated driver of reported earnings as AI infrastructure capex accelerates. As spending shifts from CPUs towards high-cost GPUs and accelerators, the useful lives assigned to these assets directly influence margins, earnings growth and return metrics. Veritas’ analysis estimates that across Meta, Alphabet, Amazon and Microsoft, extensions to asset lives since 2020 boost 2025E net income by ~13% on average. They also assess what this widening gap between accounting lives and economic lives implies for earnings quality, sector capital intensity, financing structures and asset duration risk across the AI infrastructure ecosystem as accelerator upgrade cycles compress.

Technology

Arete upgrades SHOP to Buy, arguing fears that AI coding tools erode SHOP’s moat materially underestimates the platform’s merchant lock-in. Their checks find no evidence that tools like Claude Code are displacing SHOP’s front end or app ecosystem. Instead, Arete sees SHOP as a key beneficiary of agentic commerce: as selling channels fragment, merchant complexity rises, reinforcing SHOP’s role as the operating system for commerce. They believe SHOP can retain control over payments in GenAI shopping environments, with LLM providers unlikely to intermediate payments given liability and regulatory hurdles - supporting a higher share of GMV through Shopify Payments. While AI agents with embedded wallets pose a longer-term risk to Shop Pay’s convenience, Arete expects checkout value to shift towards managing merchant-agent interactions. Agentic tools should also support merchant acquisition and retention, with optional upside from the Shop App and Ads. TP $175 (60% upside).

Emerging Markets

Energy

Vista announced the acquisition of Equinor’s non-operating interests in Bandurria Sur and Bajo del Toro, reinforcing its scale in the core of Vaca Muerta with low-cost, oil-weighted, cash-generative production. EM Spreads views the transaction as credit supportive, adding immediate EBITDA at implied multiples well below Vista’s own trading levels, while limiting execution risk through producing assets and established infrastructure, despite YPF remaining operator. The earn-out structure further improves downside protection by linking additional payments to higher oil prices. At current levels, EM Spreads maintains their Overweight view on Vista, preferring the 2033s for their better risk-adjusted balance of carry, duration and Argentina exposure.

Financials

KTC has moved past its key technical headwinds, with the share overhang from index removal and fears of further stake sales now largely reflected in valuation. Following a sharp sell-off after its removal from the MSCI Global Standard Index in mid-2025, the share price has stabilised, with PBV trading in a tight range. Attention is shifting to fundamentals, where KTC is showing clear improvement: ROE remains attractive and profit after loan-loss provisions as a share of average assets reached a seven-year high in 4Q25. This reflects tighter opex discipline and strengthening credit quality, with a declining cost of risk and a very low NPL ratio vs. Thai peers. Earnings momentum is also improving, with positive EPS revisions accelerating over recent months. KTC is Victor Galliano’s sole Buy-rated Thai financials name.

Real Estate

Iii flags an emerging risk beneath strong NCR housing headlines, drawing on on-ground channel checks. They argue that deferred payment schemes (~10% upfront, no EMI for ~36 months) are inflating booking and collection optics by converting housing demand into option-like investor positioning rather than true end-user purchases. While developers such as Signature Global appear financially resilient today, Iii highlights a growing duration mismatch between reported collections and economic cash flows. The key risk is not near-term solvency, but lagged earnings pressure, ROE compression, and valuation adjustment as payment cliffs approach and investor exit liquidity is tested. Iii sees NCR as an early indicator for similar investor-heavy housing micro-markets across India.

Developed Markets

UK: Mandelson in disgrace

It was always a risk appointing Lord Mandelson to be Britain’s man in Washington DC, With Niall Ferguson pointing out that he had to resign twice from Blair’s government. The recent news is the last straw for many furious Labour MPss angered by No. 10’s lack of grip and control, and Niall expects a leadership challenge in the coming months with Starmer forced to resign by June. Three candidates could succeed Starmer: Wes Streeting, Shabana Mahmood, and Angela Rayner – the latter is likely to win. This would be bearish for the UK as her tenure may only be temporary, lasting only until Burnham is in Parliament, and because she may end up handing over the keys to Downing Street to Nigel Farage’s Reform UK. If the best alternative Labour can produce is Andy Burnham, an identikit politician of no real stature, then Niall comments that the public’s swing to the political extremes is understandable.

Italy: Meloni’s links to Trump a liability

According to Francesco Galietti, PM Giorgia Meloni’s bridge to Trump appears to be burning - yet Rome has not fully recalibrated toward a more distinctly European sovereignty. It should consider doing so to address the security exposures created by years of lax procurement and open-armed capital inflows. The era when Italians viewed Donald Trump with indifference - or through Meloni’s calculated enthusiasm - is decisively over. A recent poll captures a populace in open rebellion against the American presidency: 73% of Italians now see Trump as a force for instability, with 59% demanding that Meloni distance herself from him. For Meloni, the implications are uncomfortable. Her self-styled positioning as a bridge between Washington and Brussels - a role she has cultivated with visible relish - is becoming a liability. The personal rapport with Trump, once a rhetorical advantage, now exposes her flank to the charge that she remains tethered to an agenda Italians increasingly reject.

US: Taking profit in RSPS

David Woo has been long RSPS on the view that Trump will pass stimulus to try to head off impeachment, running counter to the consensus of a K-shaped recovery. The trade has worked spectacularly well, although at this point stimulus is looking a long way off with discussions on the ACA reportedly dead, and the Supreme Court yet to rule on tariffs. The latest rally has been mostly a function of demand for defensive stocks as software stocks crash. This Thursday saw bonds rallying sharply, which indicates an inflection point where defensive stocks will start to underperform. Accordingly, David takes profit in his RSPS position. He bought RSPS at 28.93 and exited at 31.93 giving him a gain of about 160bps on the trade.

US: A tradeable dollar rally

Paul Krake says that recent USD weakness reflects a cyclical adjustment rather than a structural break in US exceptionalism or a threat to dollar hegemony. US dominance was built despite Washington, not because of it, and while policy volatility under President Trump temporarily undermined confidence, markets have once again asserted themselves as the binding constraint. Markets are now in the midst of the first value-at-risk (VaR) shock of the year, triggered by a sharp sell-off in precious metals. Silver’s collapse highlights the violent unwinding of crowded fear trades. Paul says dollar weakness since late 2024 has been driven by global asset rotation, a dovish Fed, and, lately, Japanese bond market stress, all of which are now losing momentum. A short-term dollar rebound is likely as leverage is flushed from the system, while the longer-term trend remains a gradual reallocation toward international assets benefiting from AI-driven margin expansion.

US: Anger, rage and wealth disparity

Inferential Focus’ latest piece examines the growing frustration, anger and rage of Americans becoming disillusioned with the possibility of achieving some version of the American Dream. Affordability and inflation are two causes of this evolving frustration, with large disparities in wealth stoking anger in the populace. Large corporate profits are being enjoyed at the expense of customer satisfaction, and people are growing tired of Big Tech making a grab for their attention, negatively affecting their interpersonal connections just to make more money. Citizens also no longer feel protected by institutions – whether government or corporations – to protect them from financial and physical risks. Americans face critical decisions about the survival of their democracy versus extending wealth disparity, fairness for all or for a few, and even traditional morality versus a transactional ethics. The country has entered America has entered an era in which its traditional identity is being challenged.

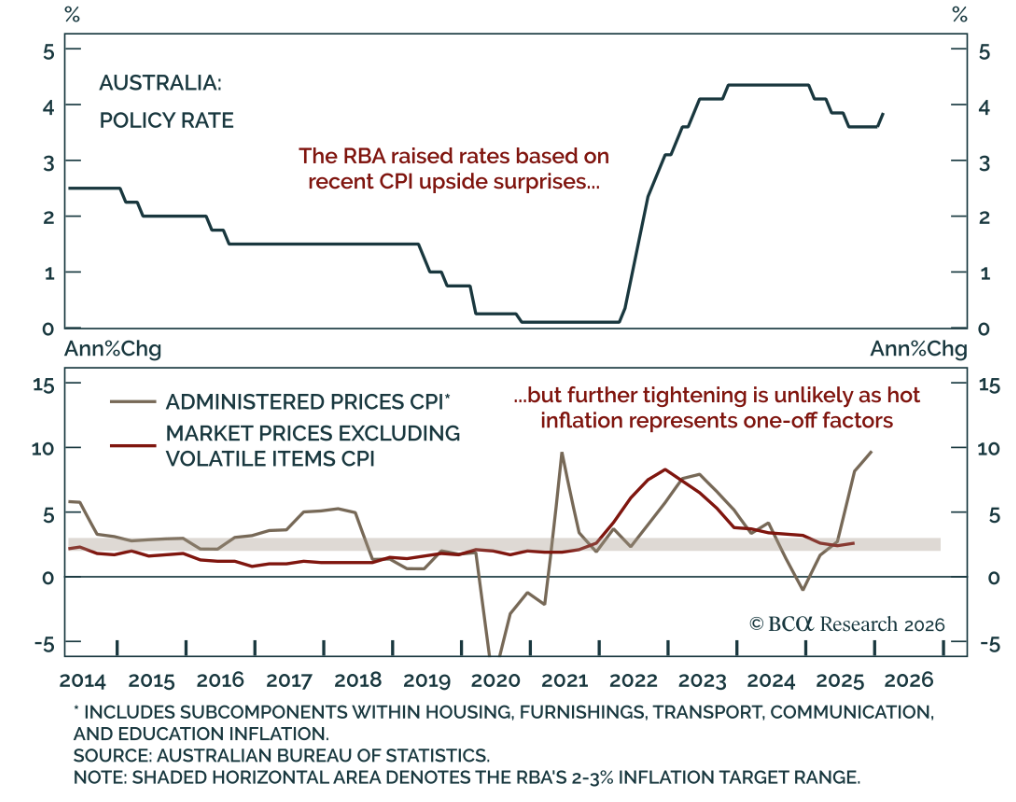

Australia: Inflation case for more hikes is weak

Report by

BCA Research

BC

The RBA raised its policy rate by 25bps to 3.85%, as expected. While inflation has moved back above the 2-3% target range, the recent acceleration reflects transitory factors including the expiry of energy rebates. The recent tightening should cool housing activity and inflation. It is true that the labour market remains strong relative to other DM peers, but there is little evidence pointing to renewed inflation pressures that would justify a sustained tightening cycle. Despite markets pricing nearly two additional rate hikes this year, the latest move is likely a one-and-done adjustment. BCA’s Global Fixed Income strategists therefore recommend staying long Australian 10-year government bond futures and maintaining an underweight in inflation-linked bonds, as hawkish market pricing looks overdone. Their FX strategists remain positive on the AUD over the long term, but are waiting for a pullback, as the currency remains overbought.

Finding the silver linings in the longevity economy

As the world gets older, there is a growing shift away from “wellness” to “longevity” as the dominant health theme. Think less fitness tracking and more clinical grade biomarkers and biological age, with a focus on healthspan just as much as lifespan – ensuring that vitality lasts just as long as the heartbeat. The shift is creating a massive, recession-resistant market for active prevention. Investors wanting to take advantage should not be chasing high-risk, unproven life-extension drugs, but instead should look to own the infrastructure of healthspan by investing in the companies that provide the “maintenance capex” for the aging human asset. Many will become consumer staples in the silver economy. Suggested names include DexCom Inc, Stryker Corp, Abbott Laboratories and Jamieson Wellness Inc.

Emerging Markets

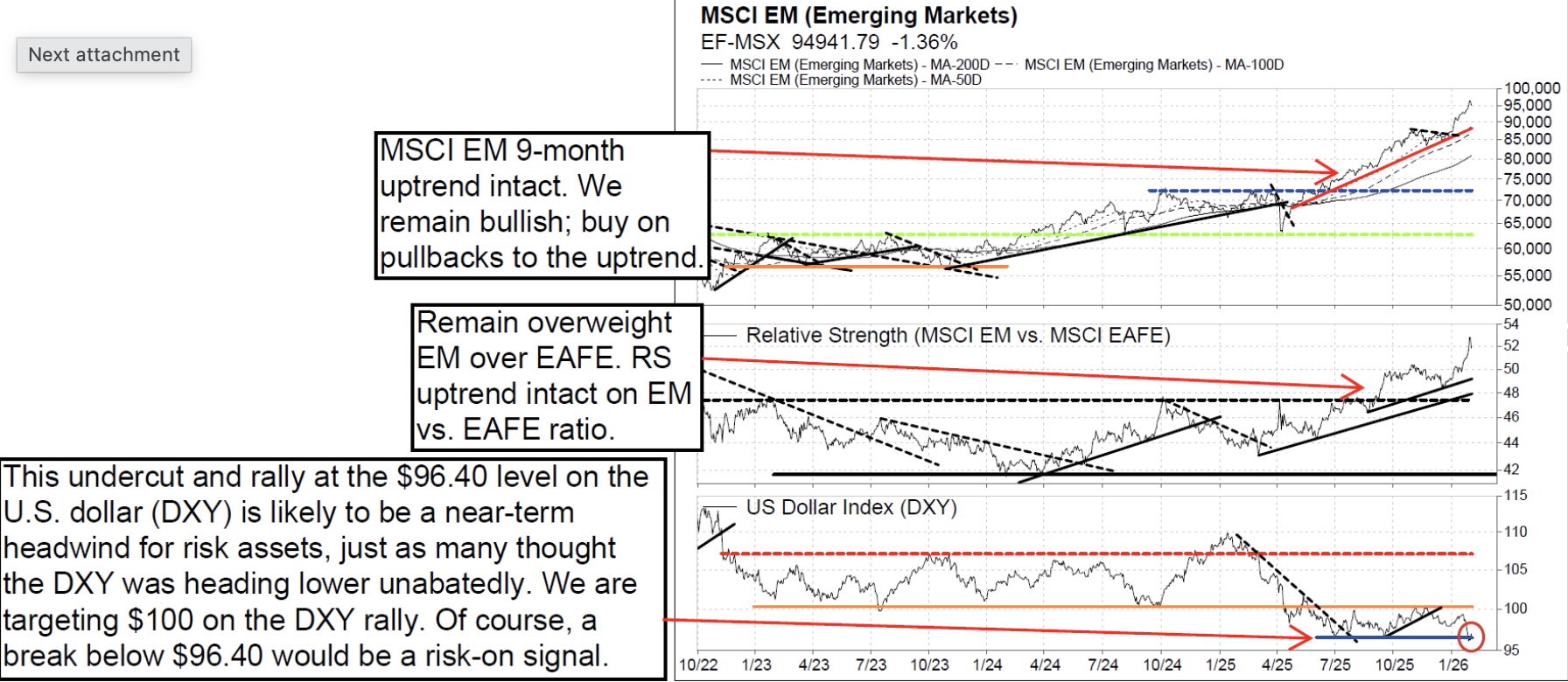

EM: Bullish outlook

The Vermilion team remain bullish on EM with the 9-month uptrends intact on the MSCI EM index (local currency) and EEM-US (USD). They continue to expect support at the uptrend, which is something the team have discussed for the past few months. A period of consolidation/pullback is increasingly likely, considering how extended MSCI EM is and the team’s views on the DXY. The weak USD has supported their bullish outlook on global and EM equities, though they see an undercut and rally at the $96.40 support level on the DXY, which is likely to be a near-term headwind for global equities. Supports to buy on EEM-US are at the uptrend (currently $56.50), $55, and $51-$51.70. The team also remain overweight on various EM countries including Taiwan and South Korea, but are taking their foot off the accelerator considering how extended they are. Brazil, Chile, Colombia, Turkey and Egypt are also looking attractive.

Ethiopia: Rising risk of full-scale conflict

According to Hugo Brennan, a resumption of full-scale armed conflict between government troops and Tigrayan forces is becoming increasingly plausible. The region is heavily militarised, tensions between federal and regional groups have been brewing for a while and now look at risk of boiling over. This matters to sovereign investors because a resumption of armed conflict in Tigray would pose both political and economic challenges for the government as well as potentially triggering another humanitarian crisis. Federal elections scheduled for June would be at risk of postponement, while ongoing efforts to restructure the country’s debt would likely be derailed. In addition, Ethiopia’s restructuring of its sole USD$1 billion Eurobond, one of the last outstanding under the G20 Common Framework, is at risk of tipping into litigation amid a disagreement over the terms between the bondholders and official bilateral creditors (led by France and China).

The Korea rally for 2026?

With the Korean index rallying through year-end, Jonathan Anderson examines the outlook. Part of the trend, of course, is the ongoing massive global IT boom. But, as before, the main story at home is the sharp rerating of the rest of the index; "domestic Korea" jumped dramatically over the past nine months on promises of corporate reforms. There's zero support from domestic macro. Korea's economy is flatlining or contracting almost everywhere Jonathan looks: durables, construction, retail, exports, credit, earnings. As a result, it's hard to motivate further gains. Korean multiples are already converging on EM-wide levels as the "Korea discount" narrows, i.e., reforms have already been priced in well in advance of actual results - and even in the strong success case this may not necessarily impact aggregate earnings and growth potential going forward. In short, at the macro level Jonathan doesn’t see significant upside potential from here.

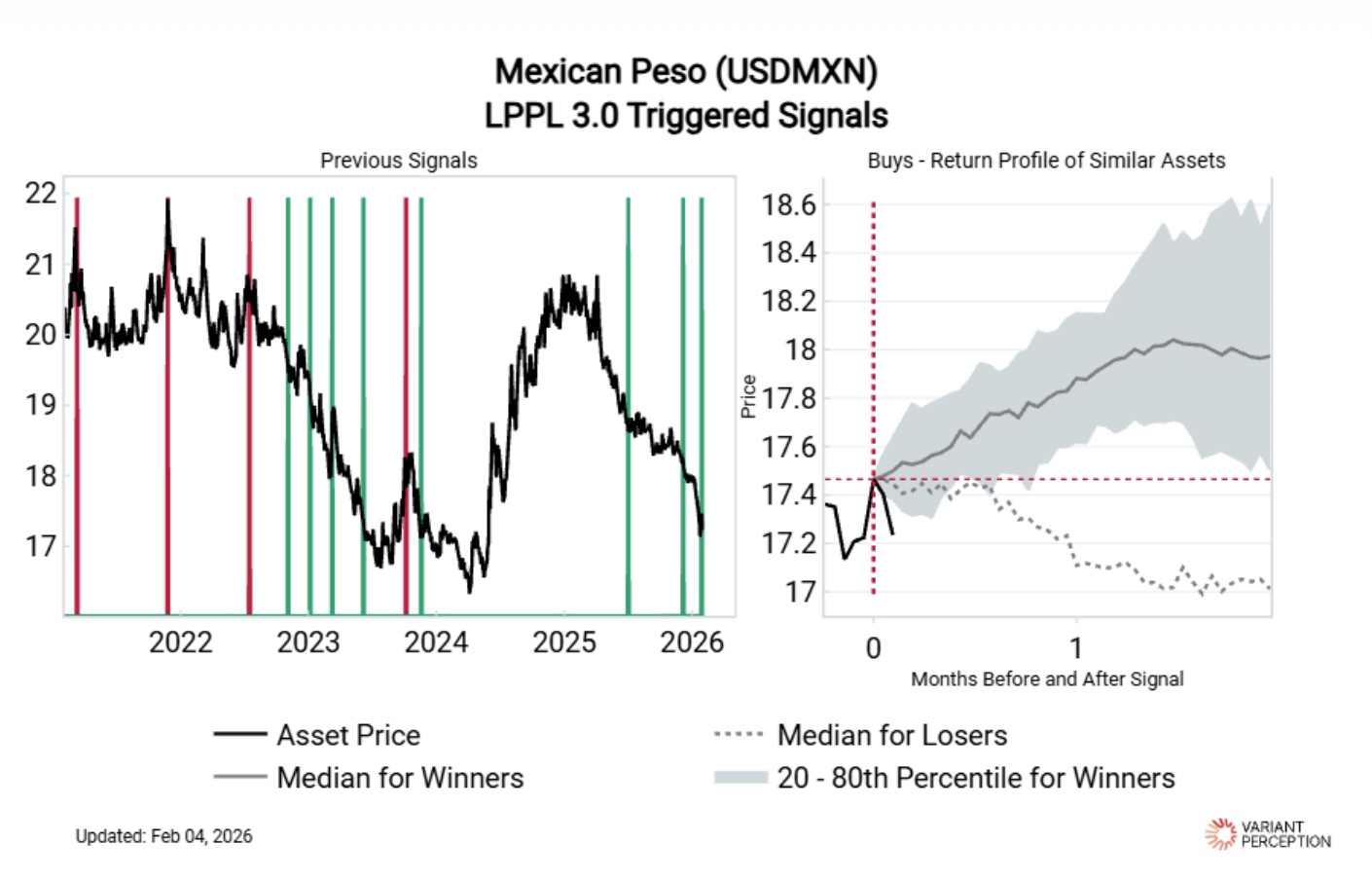

Mexico: Reversing course

The Mexican peso has been among the best performing currencies vs the USD since Liberation Day, but Variant Perception’s tactical indicators suggest that it has reached exhaustion. Their log-periodic power law (LPPL) indicator is their highest conviction trend exhaustion signal and triggered last week (see chart). Speculative positioning is heavily skewed long, in contrast to the short squeeze that fuelled the peso’s 2023 rally. Implied volatility has also fallen to bottom decile levels across all tenors from 1m to 1y, a rare but reliable signal that tends to precede major selloffs in the peso. Ahead of upcoming USMCA renegotiations, the exceptionally low volatility doesn’t seem to match the story.

Turkey: A new bull market?

The MSCI Turkey ETF (TUR US, USD41.25) lost 81% of its value in a 2010-2021 secular decline, basing around the area of the 2008 GFC bear market low. The 29-month advance in 2021-2024 is seen as an initial move in a larger advance, possibly part of a new secular bull market or, if not, a cyclical bull that will likely test the area of the USD79.00, 2010 peak. Recent strength increases the odds that the Jun 2025 low of USD29.64 is an important cyclical low (that level represented an exact 38% Fibonacci retracement of the 2021-24 advance). Chris Roberts will put on an initial 20% long position at USD38.86, using a daily close below USD31.40 as a stop loss.

Commodities

It’s all about timing

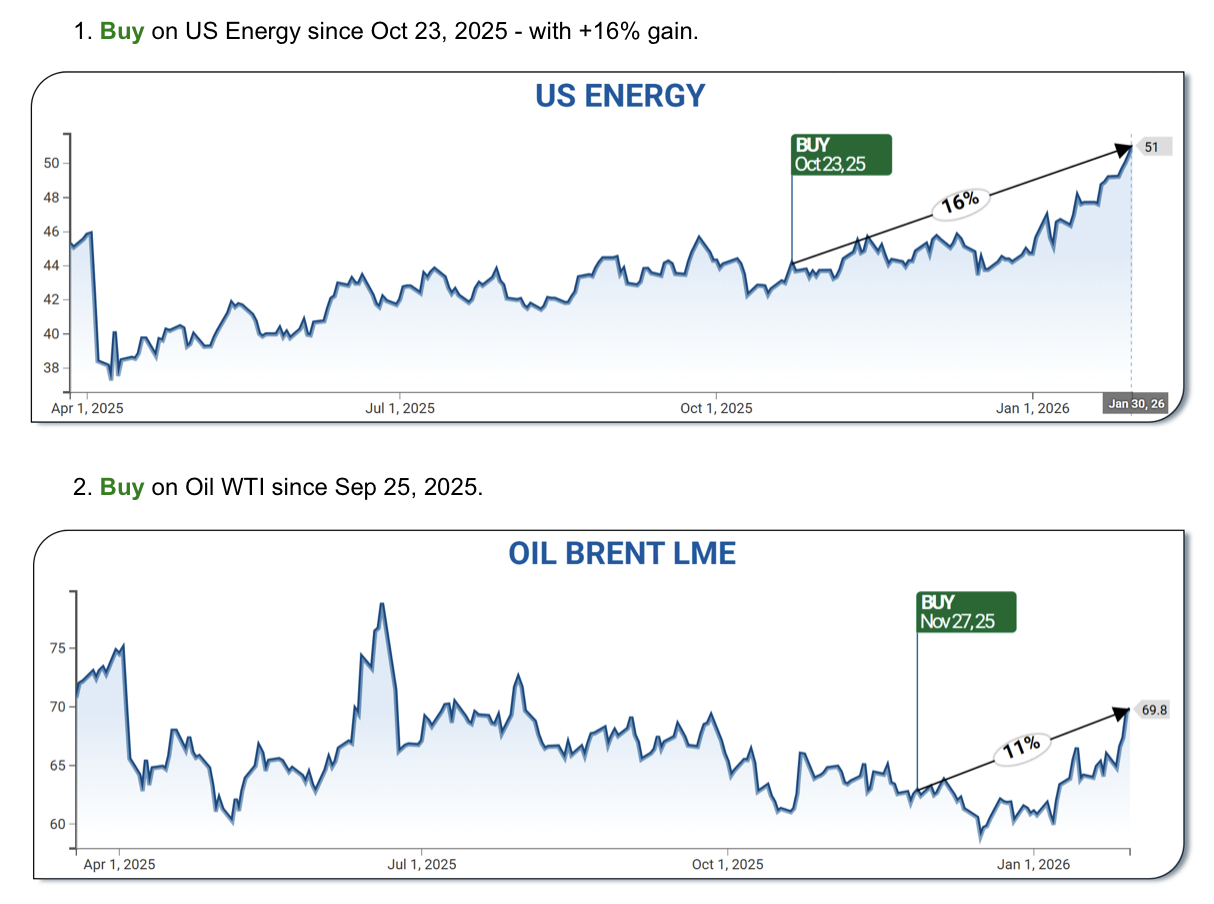

Konstantin Fominykh’s tools generated an amazingly well-timed sell on gold on Jan 26th, just one day before the peak. Commentators were inventing stories to justify the news, but it was just pure speculative excess. This wasn’t an isolated case, as Konstantin’s models produced sell signals on Bitcoin in Nov, platinum and the Mag 7 on Jan 19th, and the USD/DXY on Jan 21st. Going forward, he recommends energy and energy-related commodities (buy signal since Oct with +16% gain), and Oil WTI (buy signal since Sept).

Gold & Silver: There and back again

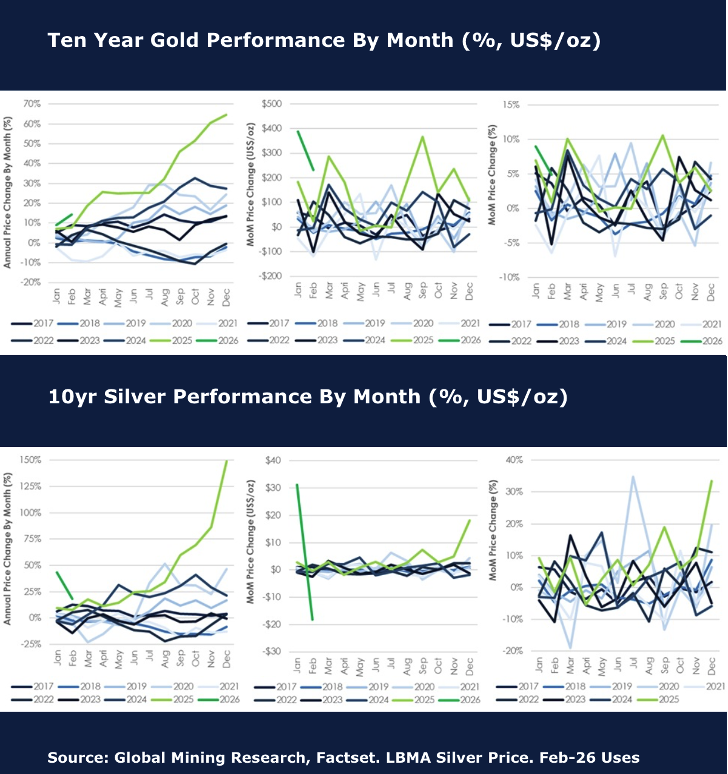

Recently, gold and silver prices hit a new record nominal high closing on Jan 29th at ~US$5,318/oz and US$118/oz respectively. The following day markets used news of the appointment of Kevin Warsh as Fed Chairman as a positive or moderate step and so took profits, resulting in the largest recent correction in precious metal markets. Volatility is high and the focus is on the near term, but the GMR team thought it worth focusing on gold and silver prices and discussing how recent moves relate to historical price moves during the last decade. Over the last decade the historical range was broadly +/- US$100/oz. However, in 2025 and into 2026 the monthly moves on a US$/oz basis exceeded this, making the moves seem larger. However, on a percentage basis the gold prices have broadly moved between up 10% and down 5% month to month. Significantly, the percentage change of those moves over recent months don’t seem totally out of historical context.

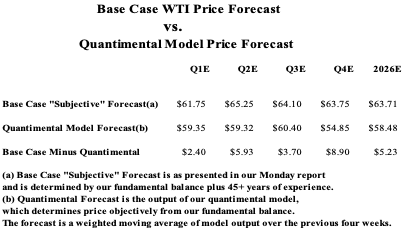

Oil: Iran hype subsides, for now

As William Brown anticipated, funds have begun to deflate the Iran hype balloon. The catalyst was President Trump’s statement that Iran was “seriously talking” to the US. Of course, talk means absolutely nothing. Nonetheless, Monday’s price reaction clearly supports his contention that funds became over hyped in terms of a potential military conflict and are more than willing to bail en masse in response to any less aggressive rhetoric from Washington. As far as William is concerned, Iran may be acting serious simply as a delaying tactic to preclude indefinitely any US military action. If so, clearly at some point Washington’s patience will run out, and the aggressive talk will begin again. No doubt if this occurs, funds will jump back in again, pulling the prompt NYMEX crude oil contract back toward and modestly exceeding $65.00 per barrel. On balance, William’s trading range remains intact.

Gold & Silver: Where prices move from here

In this presentation, Jeffrey Christian of CPM Group discusses what comes next for gold, silver, platinum, and palladium following last week’s sharp selloff, and explains why the pullback was not surprising after the rapid surge in prices. Jeff begins by looking at the US dollar, showing why claims of a “collapsing dollar” do not hold up. He emphasizes the importance of time horizons in market analysis, explaining how prices can be unsustainably high or low in the long run while remaining volatile for months or even years in the short run. Jeff then looks at the role of COMEX contract rolls and positioning, including how large open interest can affect price moves without implying any shortage of metal. He also reviews ETF activity across gold, silver, platinum, and palladium, explaining how gold ETF investors were net buyers through January, while silver ETF investors were net sellers, even as prices spiked.

Click here to watch.