Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

Ferrari (RACE IM) Italy

AlphaValue sees the recent share price correction as a compelling entry point, arguing that RACE’s equity story is unchanged: a scarcity-driven model, limited volume to protect residual values and earnings growth driven by mix, personalisation and pricing. The market’s disappointment with the 2030 targets is misplaced - management has a long track record of beating guidance and the new goals look intentionally conservative. Demand remains exceptionally resilient, supported by a growing collector base, rising UHNW populations and consistently oversubscribed limited series. The stock trades at a discount relative to its historical performance and direct peers, providing a safe haven in the automotive and luxury space, insulated from macroeconomic headwinds, trade disputes and China-related risks. TP offers >40% upside.

FLSmidth (FLS DC) Denmark

Iron Blue initiates coverage on FLS with a score of 29/60, which is top decile and fertile grounds for shorting. They highlight 1) reliance on percentage of completion revenue recognition with an associated rise in FY24 balance sheet contract assets; 2) elevated stripped out restructuring and software/R&D amortisation costs; 3) evidence of deteriorated client payment behaviour; 4) FY24 headline margins supported by Y/Y reductions in inventory and bad debtor impairment expense; 5) DKK1bn headline net debt adjustments from reverse factoring and restricted cash; and 6) many disclosure gaps.

Wolters Kluwer (WKL NA) Netherlands

Concerns that AI threatens WKL are significantly overstated; in reality, AI is reinforcing its competitive position. WKL’s AI-focused analyst teach-in underscored how rapidly the company is evolving into an AI-first, cloud-native software and content provider. Recurring, AI-enabled digital revenues continue to grow strongly, supported by deeply entrenched platforms in tax, legal and healthcare that deliver high customer stickiness and expanding scale efficiencies. Management also highlighted the rising financial burden of US clinical errors (USD 38.5bn in payouts from 2009-18), emphasising the value of WKL’s proprietary evidence-based, longitudinal data in reducing risk and liability. With solutions that deliver far more savings than they cost, the IDEA! maintains a positive stance on the stock.

Payment Companies: 1H26 high conviction ideas

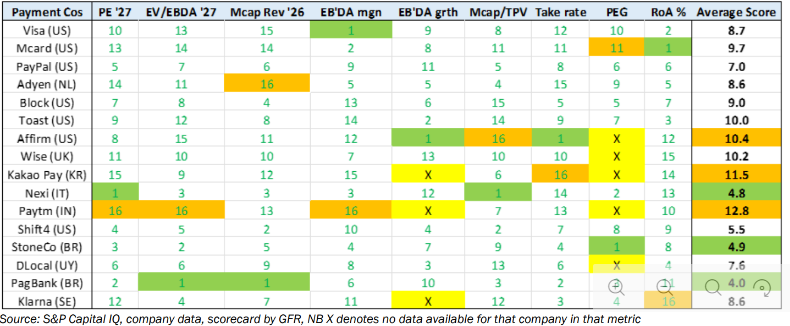

Nexi is Victor Galliano’s top pick - it screens as one of the cheapest global payments names on market cap to revenue and market cap to TPV, with expanding EBITDA margins, rising take rate and improving cash opex discipline, all supported by increasing digital-payments penetration in Italy. PagSeguro remains his core LatAm Buy, despite strong YTD performance, valuations are still compelling and it ranks highly on Victor’s proprietary scorecard (see above), with a high net take rate relative to market cap to TPV. Affirm is the key Sell: Klarna’s IPO erodes scarcity value; valuation looks stretched on market cap to TPV and credit quality in its interest-bearing receivables is worsening. Klarna is one to watch - cheaper post-IPO, but BNPL competition and credit risks keep Victor on the sidelines pending a clear catalyst.

North America

Shorts continue to deliver impressive alpha

Vision has closed 4 short ideas so far in Q4. Wingstop, initiated in 3Q25 on the view that its rich valuation was unsustainable amid intense competition, category saturation and a disappearing customer cohort benefit, delivered 40%+ alpha. Duolingo, also a 3Q25 initiation, faced a massive influx of AI produced competition at lower cost and some slowing in KPIs, generated 30%+ alpha. Kadant, shorted in 2Q24 as a late-cycle capital goods name with deteriorating fundamentals but a “priced-for-perfection” multiple, added 30%+ alpha. Patrick Industries, initiated in 1Q25 given its peak multiple on overly optimistic estimates and exposure to excess inventory, weak demand and tariff/regulatory risks, generated 5%+ alpha. YTD, Vision has launched 13 new US shorts, 7 European shorts and 5 APAC shorts, with 2-3 more initiations expected before year-end.

Earnings manipulation, anyone?

Two Rivers has recreated the Beneish model showing the highest potential manipulators and highlighting stocks such as QXO (due to M&A-driven sales spikes for AI supply chain plans), Joby Aviation (high growth amid declining margins), Rivian (rising accruals suggesting expense capitalisation), Alpha Metallurgical Resources (falling gross margins) and Pinterest (rising balance sheet accruals and sales growth). The model's inputs are similar to some that Two Rivers use in their own Stock at Risk's Earnings Quality model - albeit with some additional proprietary “secret sauce”.

Craig Huber downgrades NFLX to Underweight following its $82.7bn agreement to acquire Warner Bros Discovery’s studios, HBO and HBO Max streaming assets - a major strategic shift he views as unnecessarily risky. He argues the deal brings significant regulatory hurdles, adds heavy leverage and could slow NFLX’s organic revenue growth while pressuring margins. Large US media acquisitions rarely succeed and NFLX had excelled for 15+ years without pursuing major M&A. With the deal likely taking 12-18 months to close, Craig expects a prolonged stock overhang. Re. Paramount’s hostile bid, he believes PSKY would need to raise its offer to $32/share to fully entice shareholders away from NFLX’s attractive proposal.

Hesham Shaaban argues the Street is underestimating the durability of RBLX’s monetisation surge. Historically sceptical of its Robux-driven model, he now sees clear evidence that incremental traffic is highly monetisable: mid-2025 saw a material surge in traffic (DAUs and Hours) with limited slippage in bookings efficiency, which isn’t typical of a freemium model. Engagement is also “snowballing”: the fact that average hours are even up Y/Y - especially double digits - on a 70% surge in DAU growth suggests engagement is now viral. Hesham sees 4Q25 earnings as the key catalyst - he expects RBLX to produce booking growth more comparable to Q3 results than management's muted guidance triggering a short squeeze.

John Zolidis sees DG’s Q3 results as strengthening both the near- and long-term bull case, with traffic growth and gross margin expansion reinforcing that estimates remain too low. The long-term opportunity is margin recovery: FY24 EBIT margins were 4.7% vs. a 10-yr average of 8.9%, yet DG is targeting 6-7%, far above what the Street has modelled for FY26/27. Near term, analysts were expecting a H2 slowdown, but Q3 comps and margins instead accelerated, suggesting upside - especially as consensus Q4 GM (30%) looks far too conservative vs. 31.2% in H1 and a long history of Q4 outperformance. With execution improving under returning CEO Todd Vasos and profitability still well below historical levels, John sees room for further re-rating.

Kroger indicates more price reductions are ahead

Scott Mushkin has been highlighting for several months that price discounting would become more aggressive by the end of 2025. His latest findings show Walmart has become increasingly willing to drive down prices and Kroger is gearing up for battle, using a part of its ecommerce rationalisation to lower prices to become more competitive. The increase in competition, unfortunately, will come with further erosion in end demand. This is related to GPL-1 coverage in Medicare and Medicaid, GLP-1 oral compounds coming to market and some additional curtailment in SNAP benefits. At the same time, the continuation of the MAHA trend will remain a headwind. This marks the beginning of what will be a tougher period for the industry, especially those such as Kroger, that have significant overlap with Walmart.

BTN views AAON as exhibiting some of the most aggressive revenue-recognition practices in its peer group. The degree to which revenue is pulled forward makes it difficult for the company to sustain momentum from quarter to quarter, resulting in pronounced volatility in reported results and limited visibility into the underlying run rate. Unbilled contract assets remain elevated at 50 days of sales (vs. 27 days a year ago), reflecting AAON’s practice of booking revenue upfront when parts are ordered. Receivables increased $96m sequentially, reaching a new high of 64 days of sales and was the primary driver of the revenue beat. Falling inventory days suggest Q3 was backloaded, consistent with the jump in accounts receivable. OCF remains negative, with BTN sceptical of management’s claims of a swing to positive cashflow in 2025. The company is borrowing and stretching payables to plug the gap.

Results will not live up to the enormous expectations surrounding this story, as the company shows almost no customer traction beyond Walmart. While SYM is rolling out systems across 42 WMT distribution centres through 2029, new wins have been minimal, leaving a massive revenue gap ahead. In contrast, competitors Knapp and Witron have announced dozens of new customers since 2022 including new business with WMT. Half of the company’s touted $22bn backlog sits in a stalled SoftBank JV (GreenBox), with little evidence of progress. With heavy insider selling, a recent revenue restatement, TAM overstated and the stock trading at ~10x 2027 sales, the bear case sees estimates beginning to be revised down next year and SYM’s valuation potentially halving.

Ivanhoe Mines (IVN CN) Canada

A 2026 copper turnaround story - IVN is now producing from all 3 of its core and globally significant mining assets. However, this has not been reflected in the share price following the seismicity event at Kakula in May 25. The market is focused on short term risks, but Kakula’s recovery is being managed and 3Q25 volumes (annualised at 285kt/yr) likely marks the bottom. With the 3 operating assets contributing in 2026 and a new smelter set to lower costs, GMR sees next year as the inflection point. IVN also offers major exploration upside - its 100%-owned Makoko district alone has 9.2Mt of copper identified, with additional drilling across Angola, Zambia and Kazakhstan providing further optionality not priced in. Trading at 1.4x P/NPV10, IVN’s growth, scalability and asset quality make the risk/reward compelling.

Cisco's 800G just hit the same wall GPUs did

JNK Research indicates CSCO's Silicon One networking roadmap faces the same thermal management bottleneck that constrained Nvidia and AMD GPU production. CSCO is ramping wafer starts 8x - from 1k to 8k annually - at TSMC in 1H26. However, heat spreader suppliers already operate at 85%+ utilisation with capacity concentrated among few Taiwan suppliers. The company is proactively qualifying secondary thermal suppliers and paying for tooling upfront to secure allocation. This mirrors the CoWoS packaging constraints that limited GPU shipments in 2024. Networking ASIC thermal requirements are approaching GPU-level complexity as data centre switches migrate from 400G to 1.6T.

2Xideas argues OS is tapping into a large, visible market opportunity as enterprises replace outdated software applications and tools. The company continues to gain market share, strengthening its position relative to peers and is on a "winner‑take‑most" path. Furthermore, OS is well‑positioned to integrate emerging AI technologies, benefitting from its role as a trusted governance and compliance layer, which largely insulates it from disruption. 2Xideas forecasts 19% revenue CAGR, driven by new customer wins, strong cross-/up-sell opportunities and international expansion. Over the next 5 years, they expect a total shareholder return of 20.8% p.a., based on an exit NTM EV/Sales multiple of 8.0x.

Memory pricing dynamics & new monthly tracker

The rally in memory prices shows no signs of abating - a burden for buyers but a windfall for suppliers, especially late entrants and firms focused on legacy products. Yet the upside may carry unintended outcomes: elevated prices could slow AI innovation, trigger cyclical downturns despite structural demand growth and most critically, accelerate China’s push for semiconductor self-sufficiency. DRAM prices are expected to jump 40-60% in 4Q25 and another 15-20% in 1Q26, forcing buyers to either secure expensive inventory early or cut memory content. Counterpoint is launching a Monthly Memory Pricing Tracker with monthly contract-price updates and market commentary. Meanwhile, supply is ramping fast, with their 2026 bit supply growth forecasts raised from 16% to 25% for DRAM and from 14% to 16% for NAND. China remains a key variable in pricing and Counterpoint is formalising its tracking of Chinese supply.

Japan

MCAP is emerging with the strongest momentum in Japan’s once-tainted M&A consulting sector. Unlike scandal-hit peers, MCAP avoided reputational damage and is now growing faster than Nihon M&A, generating higher margins and trading on just ~15x FY9/26 earnings despite forecasting >30% Y/Y profit growth (which may well prove conservative). Deal sizes are rising, consultant numbers are compounding 20-25% annually and MCAP’s high-incentive pay model draws top sales talent, keeping churn low. The company’s Recof subsidiary remains a drag, but restructuring should push it towards profitability. With improving industry governance, fears of a “kabarai-style” crackdown fading and cash piling up from strong FCF, the shares are attracting renewed investor interest.

Yuka Marosek examines whether ISK can narrow its sizable profitability gap with Nissan Chemical, whose operating margins are more than triple ISK’s. She attributes the gap to ISK’s heavier reliance on lower-margin TiO₂ and inorganic chemicals, while Nissan benefits from higher-value agrochemicals and semiconductor materials. ISK’s mid-term plan aims to shift its portfolio towards higher-value TiO₂, consolidate production under the chloride process, upgrade its functional materials mix and continue disciplined R&D investment. Early signs are constructive: ISK’s Q2 FY3/26 margins have already begun to recover, helped by improving TiO₂ pricing and mix. With further optimisation, new capacity through the MF Material JV and a strengthening agrochemical/vet-pharma pipeline, Yuka sees credible scope for margin expansion and valuation catch-up.

Emerging Markets

Meesho (MEESHO IN) India

Meesho enters its IPO with strong user and order growth, but Iii flags mounting financial-quality concerns. Despite improving KPIs, the company remains loss-making and faces significant litigation risk, including large tax-related disputes. More troubling, impairments and write-offs are rising sharply: the company has written off INR 223m in bad debts over the past 18 months, its impairment provision has jumped from INR 110m in FY24 to INR 588m in 1H26 and total impairments plus write-offs reached INR 720m in 1H26 alone. Heavy churn in key management roles, new regulations around employee worker costs and recurring audit-trail weaknesses further underscore the risks for investors considering this IPO.

Jun Lei (Co-Founder) purchased ~ $12.9m worth of stock at HKD 38.58. While modest relative to his 1.9 billion-share stake, the purchase is noteworthy. It is his first open-market acquisition in this stock and also represents the first meaningful insider purchase since the IPO in July 2018 at HKD 17. Despite the recent share price decline, it is interesting to see him making a sizeable purchase shortly after the company released its Q3 earnings. Smart Insider ranks the stock +1 (highest rating).

Macro Research

Developed Markets

The next financial crisis

That we live in a hyper-financialised world is not in dispute, but James Aitken cannot see the net benefits to society from changes like Kalshi, which monetise differences in opinion. He argues that over the long run, monetising any difference in opinion will create negative utility due to the externalities of normalising the idea of betting on everything. And one would think that these betting markets are enormously susceptible to manipulation by state actors; yet such is the path we are on. So what? James says he isn’t tilting against the windmill of the ongoing, hyper-financialisation of everything. Instead, he suggests that the path to the next financial crisis won’t run through (e.g.) private credit, geopolitics or whatever, but instead it will run directly through market structure, period. What happens when, for any period of time from minutes to hours to days, all the machines that intermediate 1x, 2x, or 3x levered ETFs, prediction markets, 0DTE, bonds, stocks etc. decide ‘computer says no’?

The US-China AI war

The White House will allow Nvidia to sell its H200 chips to China, but the 25% tariff presents a disincentive to sell at a time where demand is so high money can be made elsewhere instead. Xi remains the biggest hurdle, who maintains that technological independence takes priority over economics. China’s chips are much less capable, with Richard Windsor calculating that Huawei’s SuperPod system is 32x less efficient than Nvidia’s equivalent. Although Chinese AI models are performing well, the country simply cannot compete when it comes to the tech. It’ll be a long while before Nvidia and AMD truly re-enter the Chinese market, and the country will continue to stay behind with little scope for it to catch up due to its lack of cutting-edge hardware. For now, the West has the advantage.

2026 risks being overstimulated

Developed economies enter 2026 with inflation above target, labour markets tight, wage growth solid and governments running gargantuan budget deficits. Yet Gerard Minack points out how markets expect most central banks to ease or keep policy rates steady, Japan (and Canada & Australia) excepted. There are many hard-to-calibrate risks – such as the war in Europe, US trade policy, Fed independence – but the base-case macro-outlook is for at-or-above trend growth that threatens higher inflation and undermines the case for easier monetary policy. Gerard will discuss the implications of this for markets next week. Spoiler alert: two of the biggest issues for investors – the AI equity trade and risks around developed economy sovereign bonds – don’t hinge on the near-term cycle forecast.

Ukraine: The litmus test of European determination

Zelensky rejected the latest US peace plan this week, but this does not change David Woo’s view that the war will be winding down in Q1. He remains of the view that, with dwindling US financial and military support, Ukraine has no way of sustaining its war effort much beyond this winter. The recent proposed plan is as good as Ukraine is ever going to get. The biggest risk to David’s view is if Europe decides to step up, with the debacle of convincing Belgium to turn over frozen Russian assets to Ukraine a litmus test of European determination. David has established a short position in the Dec26 Brent future on the view that a peace deal will be accompanied by a lifting of sanctions on Russia. He will double it should the US invade Venezuela, given the likelihood that the conflict will be short and sanctions will be lifted post-Maduro. If Europeans turn over the frozen assets to Ukraine, sell the euro.

Italy: Industrial Devolution

Italy’s industrial production undershot expectations in October, with production falling 1.0% month-on-month, a sharper contraction than the expected 0.3% decline. The pullback was broad-based across key categories: consumer goods output dropped 1.8%, capital goods declined 1.0% and intermediate goods slipped 0.3%. Energy production provided only a modest offset, rising 0.7%. On an annual basis, industrial output fell 0.3%. John Fagan points out that the year-on-year breakdown highlighted persistent structural weaknesses, with significant declines in chemical manufacturing (-6.6%), textiles and apparel (-5.0%), and refined petroleum products (-4.6%). The data reinforce the fragile momentum across Italy’s industrial base, which continues to face a combination of soft external demand, elevated input costs, and sector-specific pressures in chemicals and textiles. The sharp monthly swing also signals that September’s strength was not sustained, raising concerns about the durability of Italy’s manufacturing recovery.

US: Rumble in the market jungle

The bull may have danced like a butterfly, but the bear has once again shown its ability to sting like a bee. US equities recently triggered a 5% drawdown alert from their 52-week highs, with S&P500 key support at 6500. Only a weekly close above psych level at 7000 would neutralise the mean-reversion signal. Ron Williams points out that late-cycle signals are flashing: broad market weakness, crowded mega-caps under pressure despite strong earnings, shifts in investor psychology towards balance-sheet strength, and macro uncertainty. As risk appetites fade, gold remains a resilience diversification play while it’s LT trend holds above $3,930. Multiple timing models suggest a potential high-risk cyclical inflection heading into Q1 2026, with tightening conditions, slowing growth, margin pressures and crowded trades converging. Ron advises investors to stay flexible, patient and diversified, to emphasise balance-sheet quality over speculative growth, and to follow RWA tactical strategies to enhance trade setups and market timing.

US monetary policy: QE by another name?

Andrew Hunt says the FRB has U-turned on QT and that other central banks will surely follow as their governments’ fiscal / debt issuance arithmetic bites in a world in which the PBoC now seems less inclined to fund “everyone else’s” deficits. As expected, the Fed has gone down the path of YCC. This is QE-by-another-name, but the “certainty” provided by the Fed’s shift towards guaranteeing stable yields out to three months may have been slightly undermined by the divisions shown in the dot plots and a degree of risk aversion within the banking system. Andrew expects some positive quantity reaction vis-à-vis monetary conditions but perhaps not a large one. The Fed’s move does however confirm that there is little stomach for hard budget constraints in Washington despite the economy’s positive output gap. As such, this will undermine the USD’s internal and external values over the medium term, likely starting with the FX rate.

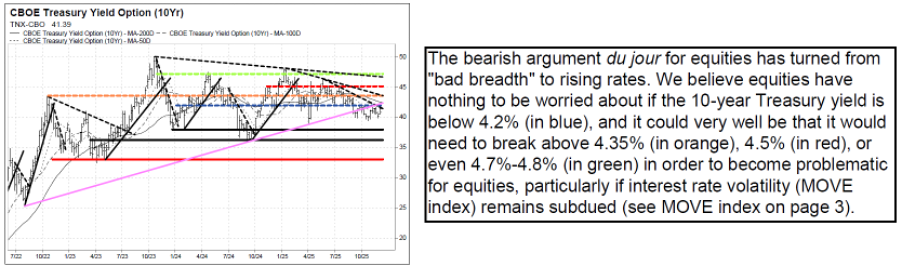

US: Rising yields a problem?

The Vermillion team maintain their near-term bullish outlook on the SPX and QQQ, and will maintain this view as long as crucial support levels of 6480-6520 on SPX and $580-$583 on QQQ continue to hold. Bears that were complaining about "bad breadth" -- which the team argued was not a big concern -- have moved on to a new worry: rising interest rates. As long as the 10-year Treasury yield is below 4.20% resistance, the team believes the equity market has nothing to worry about. And it could very well be that the 10-year yield would need to move above 4.35%, 4.50%, and even 4.70-4.80% in order to become problematic for equities, particularly if bond market volatility (MOVE index) remains subdued. Additionally, the Russell 2000 (IWM) is back above its major 4+ year base, and is extremely bullish as long as base support holds at $245.

The Fed’s upcoming productivity bet

According to Cam Hui, a Trump-dominated Fed is on the verge of a rate cutting cycle based on a probable Greenspan-style bet on AI-driven productivity. If AI does significantly boost productivity, the economy could be in for a period of non-inflationary growth and prosperity. The risk is a policy error, rising inflation and a falling USD. Much depends on the usefulness of AI across different applications and industries. From the market’s perspective, the preliminary verdict is that the Fed will undertake an inflationary outcome. Yield curve spreads are undergoing mild steepening reactions, which is discounting higher inflationary expectations in the future. Regardless of the outcome of the productivity debate, Cam believes strength in the gold price is consistent with his long-term observation of a relative breakout in gold against both the S&P 500 and 60/40 portfolio, which is a signal that the market is undergoing a shift from paper to hard asset leadership.

Australia: The RBA isn’t as dovish as you thought

Following remarks by RBA Governor Michael Bullock, Craig Ferguson says it is clear that the RBA is not as dovish as many had thought and consensus will shift towards pricing in more rate hikes in 2026. Over the last 2 months the AU 10yr yield has risen by 75bps from 4% to 4.75% and the AU 3yr yield now stands at 4.15%, a full 55bps above the official RBA cash rate. When short and long yields are far higher than the current cash rate, that tells you that bond investors think growth and inflation are both returning such that it is unlikely for the RBA to cut rates. Indeed, 3yr and 10yr yields are now so far above official cash rates that the 3yr is suggesting in 3 years’ time the RBA cash rate needs to be 4.15% or above and the 10yr yield is saying the cash rate needs to be more than 100bps higher than it is today to stamp out persistent inflation risk.

Emerging Markets

EM: Heading up

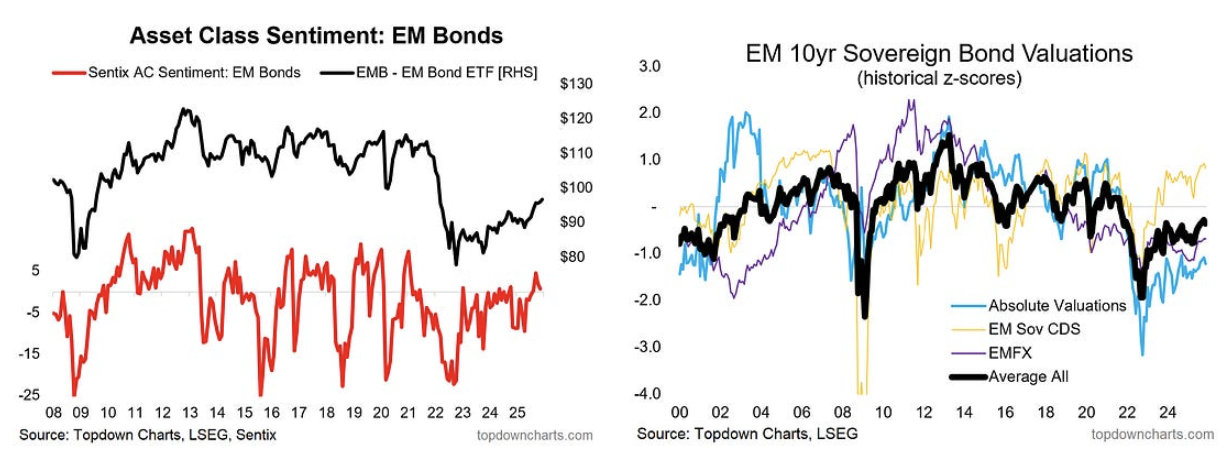

EM sovereign bonds are establishing an uptrend from cheap valuations, with sentiment trending in the right direction and boasting solid real yields and monetary policy tailwinds. EM policy rates continue to drift lower as inflation remains contained for now across emerging markets (and surprising to the downside); anticipate further policy rate normalization. EMFX is also improving, with the equal-weighted EMFX index turning up from lows, and attempting a long-awaited trend change off cheap valuations. Callum Thomas points out that one mixed aspect is EM credit spreads and risk pricing, which are tracking near record lows, which could indicate complacency (and little risk cushion). On the other hand, it also reflects benign/positive risk sentiment and supportive financial conditions. Remain bullish EM sovereign given cheap valuations, improving sentiment, strong technical, policy support, and a favourable financial conditions backdrop.

China: Back to 1994

Andrew Hunt examines China’s deteriorating economy. Households, companies and the public sector are spending less. Liquidity trends are weakening. The country’s external trade surplus is being pushed higher. The practical mechanism for this is a fall in PRC export prices and a reduction in imports. China is therefore exporting (intense) deflation in global goods markets. Previously, capital outflows were providing an inflationary counterbalance to global capital markets, and even (implicitly) non-traded goods sectors. Over recent weeks there are signs that not only have China’s private sector capital outflows decelerated, but so too have public sector flows. The slowdown on private sector outflows is the result of declining domestic liquidity but the reduction in PBoC-sourced outflows may have a political dimension. If the PBoC continues to hold back vis-à-vis its intervention, and instead allows the CNY to appreciate, Andrew Hunt warns that global bond markets will come under more pressure in what could amount to a repeat of 1994.

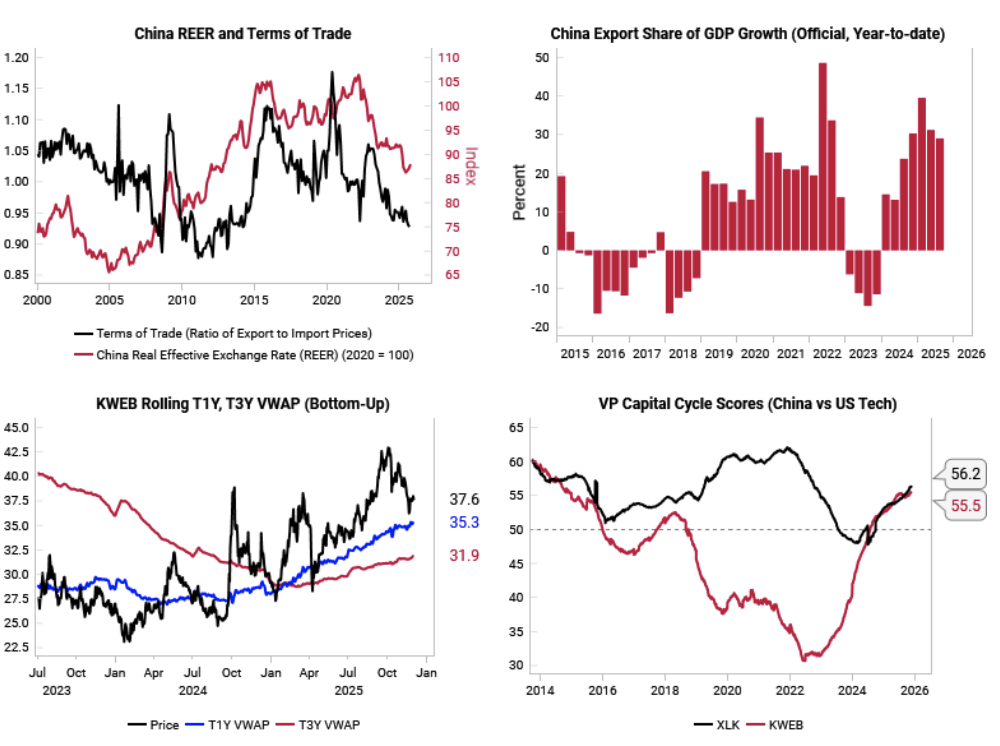

China: Not yet time to look for CNH strength

The Variant Perception team point out that the renminbi (RMB) is undervalued by traditional metrics (see top left) and its exceptionally large current account surplus. But the increasing importance of net exports amid weak domestic growth suggests policymakers will continue to prefer a weaker or steady CNH (top right). A key risk factor for the RMB is an increase in tariffs or other trade barriers from non-US countries targeting Chinese imports (effectively devaluing these currencies vis-à-vis CNH). This could prompt Chinese policymakers to weaken the currency to maintain export dominance, but this will likely only occur until the government feels confident in its leverage with the US. This probably won’t happen while China lags Western semiconductor equipment and EUV capabilities. Chinese tech stocks should continue to benefit from Chinese policymakers’ easing bias throughout 2026, and are nearing key support levels and have improved rapidly in key VP bottom-up indicators (bottom two charts).

China: Shifting the focus

China’s leaders discussed their economic priorities for 2026 at the recent Politburo meeting. According to Andrew Polk, the short readout largely signals policy continuity, calling for:“Continued implementation of a more proactive fiscal policy and a moderately accommodative monetary policy”. This mirrors the Politburo’s prescription for 2025 macro policy one year ago. However, there was a nod to “cross-cyclical policy” (which was absent from last year’s readout), which indicates that macro policy will not be as supportive in 2026. Specifically, the readout calls to: “Strengthen counter-cyclical and cross-cyclical policy adjustments”. For reference: Cross-cyclical policies are more long-term in nature, targeting structural challenges – such as demographics and innovation – to raise potential growth. Andrew says senior policymakers appear less worried about short-term growth in 2026 than they were a year ago, and are once again shifting focus toward longer-term structural issues.

Hungary: Another good year for the forint?

2025 was a good year for the forint, in light of weak demand, lower inflation and a supportive external balance. Jonathan Anderson remarks that 2026 will likely be the same. The MNB is in no hurry to resume easing, real interest rates are solidly in positive territory and there's no sign of credit or demand pressures going into the new year. Jonathan was on the sidelines with HUF in 2025, but is now taking up the carry trade for a while. There’s still no end to the equity rally. CEE stock indices continue to "blow the doors off" the rest of EM, in Hungary's case led by main listed name OTP Bank. As before, however, this is not a reflection of Hungarian macro trends at home.

South Africa: One notch down, guard up

The SARB delivered the unanimous 25bp cut that Peter Montalto expected, but this was no dovish pivot: the CPI path was only nudged slightly lower and the language stayed cautious. The MPC is now comfortable moving into “less restrictive territory”. It means that the country now sits a little above the new neutral range around 6.50%. Looking ahead, Peter remains more conservative than the QPM on both inflation and the policy path. He still sees a stickier non-core wedge and slower expectations pass-through than the model assumes, given the fixed public-sector wage agreement, Nersa’s tariff pipeline and unusual food CPI seasonality, even though the de jure shift to a 3% target pulls the expectations profile down. That keeps Peter above the SARB’s inflation and repo projections: his baseline is no further change for roughly six months, and a clearer next leg down only in H2 2026 to 6.00% end 2026.

Taiwan: Lai’s big bet

Whilst the country rides the AI boom, political risk is mounting. The opposition KMT party is divided, with a controversial new pro-Beijing leader, and President Lai is looking to split the opposition in the legislature by simultaneously pushing a bold defence spending plan and closing a trade deal with Washington. The potential market and geopolitical upside are significant if Lai’s gamble pays off, with the Taiwan dollar strengthening and a likely announcement of big new TSMC investments in the US. However, Lai still needs opposition votes from a party spoiling for a fight, and should he fail to secure suitable support, the Trump administration may sour on Taipei just as it steps up détente with China in Q1/2026. Niall Ferguson expects Lai to get the support for both a defence spending hike and trade deal, but he will lack support for every line item, and his plan could easily go off the rails.

ESG

The end of Net Zero at any price

As the global energy sector digests the outcome of the 2025 Duke of Edinburgh Future Energy Conference, mainstream financial press like Forbes is reporting a “reluctant consensus” regarding the transition: costs are high, timelines are slipping, and fossil fuels remain dominant. But while the headlines are catching up to the mood, Commodity Intelligence has already defined the mechanism. James Burdass produced a detailed write up on December 2nd, which can be accessed below. While others were observing a general sentiment shift, James was the first to codify this new era as the “Age of Industrial Realism.” By looking beyond the public speeches and tapping into the critical private intelligence exchanges at Mansion House, James helped shape the debate by moving it from vague “macroeconomic concerns” to hard-nosed structural realities.

Click here to read the report.

Commodities

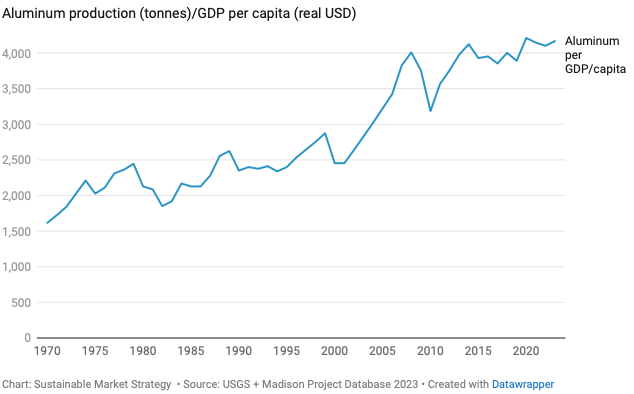

Aluminium in transition: The neglected materials play?

Fossil fuel demand may be falling in the future, but aluminium certainly won’t, driven by demand for EV and solar adoption, the great grid buildout and more aggressive lightweighting. There are no physical constraints to aluminium supply, with bauxite a plentiful resource that can be found near the earth’s surface, yet supply is expected to tighten relative to demand beyond the next three years. China is the main reason, having imposed a national ceiling of 45m tons per year on primary aluminium production. The next big reason lies in electricity constraints; given the amount of electricity required to produce aluminium, the economics of the metal are essentially the economics of power. Competitive advantages are available for producers with sizeable recycling operations, which the team expects to outperform over the next few years. Expect the likes of Constellium, UACJ Corp and Norsk Hydro ASA to be the biggest relative winners.

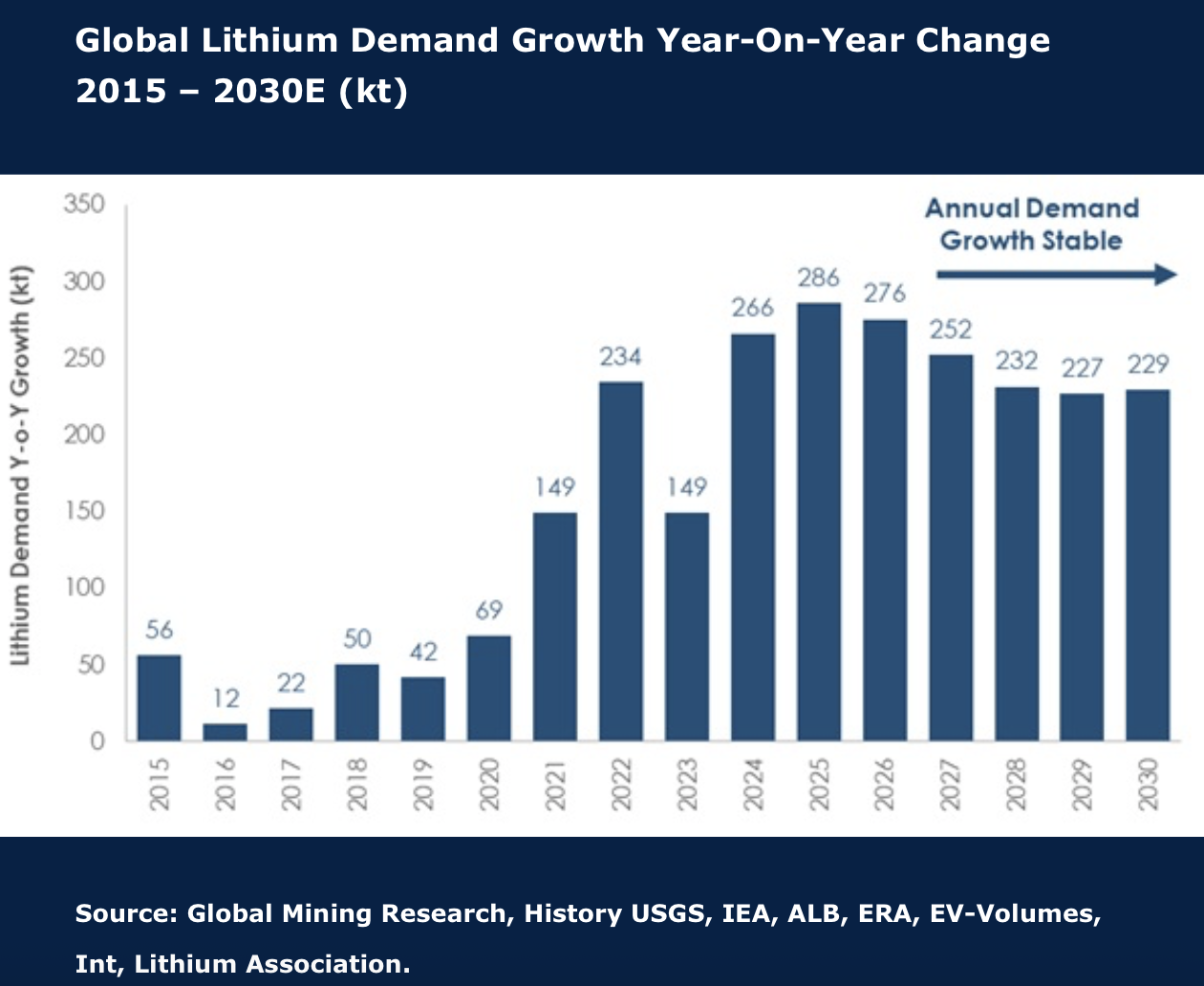

Lithium production to exceed demand to 2030

Lithium, like other minor commodities, is marked by volatile short- to medium-term cycles, with an extraordinary bull market of 2021–2022 followed by a relatively prolonged bear market. This is despite very strong demand growth, due to an equally strong (or greater) advance in production, plus inventory de-stocking. David Radclyffe finds evidence for a continued market surplus out to 2030. Although prices have recently started to turn up, an excess of idled capacity along with significant new projects coming online suggests prices will hover around the top of the cost curve for some time. Of late share prices have moved up ahead of the commodity prices, with equity markets getting more optimistic. Investors should be cautious and favour those already in production or juniors with fully financed projects. David has no Buy-rated stocks dealing in lithium. Pilbara Minerals Ltd has outperformed and, now looking expensive, is downgraded to HOLD. Rio Tinto Plc and Sociedad Química y Minera de Chile SA are rated HOLD, while Albemarle Corp, Energy Resources of Australia Ltd, IGO Ltd and Mineral Resources Ltd are rated SELL.

Don’t fall asleep at the wheel, this is a secular bull market

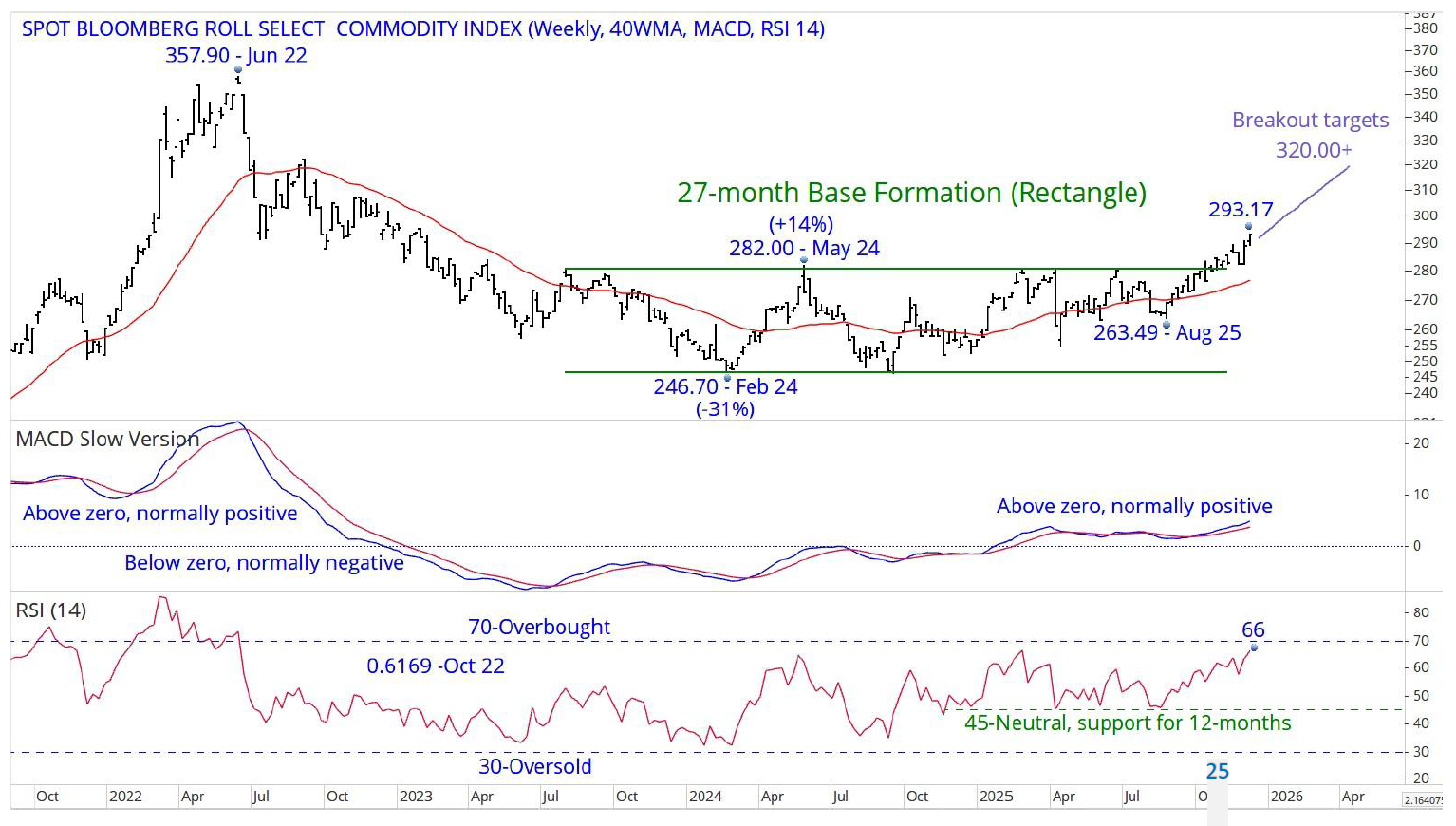

The Spot Bloomberg Roll Select Commodity Index (293.17) is the instrument that Chris Roberts’ newest data provider has, that is just about identical in shape to the Bloomberg Commodity Index that he used to feature. The breakout from the 27-month base formation targets a move to 320.00+, but Chris’s target is a new high above 2022’s 357.90. A secular bear market ended in April 2020 (see next page). The 1st leg of a secular bull market ended in 2022, and following a 30%+ decline and a distracting, time consuming sideways movement, the 2nd leg up is now underway. Indicators have room for further gains.

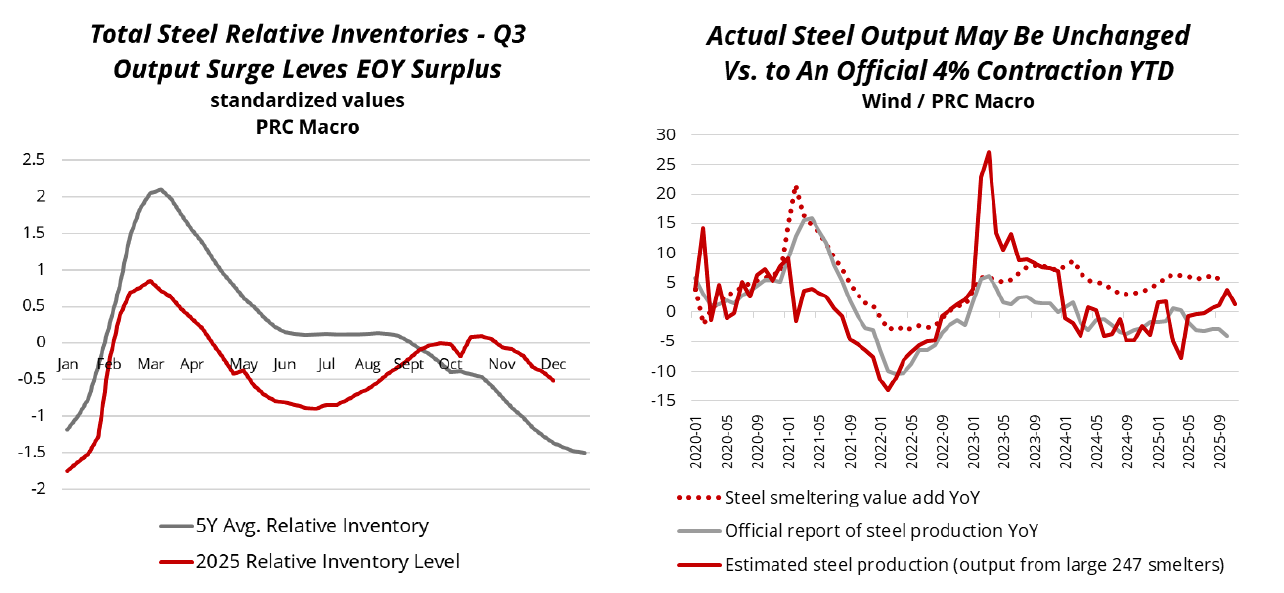

Markets are misreading the China steel story

Beijing’s latest Five-Year Plan signals a shift from volume growth to productivity, profitability and price stability. William Hess notes that headline production cuts are likely smaller than consensus; actual 2025 output appears underreported, and Beijing is taking care not to deindustrialise too quickly. Contrary to what some investors think, capacity adjustments will focus on improving operating rates and margins, not aggressive output suppression, which should be supportive of better than consensus iron ore demand – the current institutional outlook of average prices drifting to low $90s by Q2/2026 is too bearish. On the demand side, expect a better year in 2026 supported by multiple factors including a moderate recovery to infrastructure investment, manufacturing capex and machinery upgrades, as well as a tailwind from ODI. William also notes that capacity reductions could stem from carbon costs, which could wipe out 10-15% of inefficient producers if set at RMB 150-200/ton.

Oil: Waiting for a downward spiral?

Vandana Hari doesn’t see a plausible path to an equitable compromise in the Ukraine-Russia peace talks, at least not within the timeframe President Trump has in mind. The market seems to agree, moving no more than 2% on any given day over the past four weeks, with Brent stuck in the low $60s. Glut-watchers are still waiting for a downside spiral that, judging by the more bearish oversupply forecasts, could have materialised at any time since the start of this quarter. However, Vandana says that the idea a Ukraine deal will unleash a flood from floating storage in a step change may be overstated. Before the market can price post-sanctions flows, it must contend with escalating Ukrainian strikes on energy infrastructure; unless Washington leans on Kyiv to halt these, further attacks on refineries/ports and potential sea-drone strikes on “shadow fleet” tankers could keep risk premium embedded.