Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

FDJ United (FDJU FP) France

Trading at the cheapest valuation since listing (9x FY25 P/E) and offering a 10% dividend yield, FDJU has more than discounted temporary headwinds. While regulatory tightening and higher taxes in France, the UK and the Netherlands will cut FY25 EBITDA by ~€55m (145bps margin drag), it is a small dent vs. the €3.3bn in lost market value since 2021. Beyond this, FDJU’s technology-focused, online-diversified model post-Kindred integration is more attractive than ever, underpinned by stable lottery cashflows. AlphaValue expects sentiment and the share price to recover sharply, calling it an exceptional risk/reward setup. Their TP offers more than 100% upside.

Spin-Off Research maintains a Buy rating on Unilever PLC (Consolidated), with a target price of $68.0 per share, based on their SOTP valuation. Their fair value for TMICC is $5.90 per Unilever share or $29.50 per Magnum share. TMICC leads the €75bn global ice cream market with a 21% share, driven by scale, strong brands and proprietary infrastructure. Its spin-off enables focused growth, especially in emerging markets with high potential and resilient demand. Spin-Off’s fair value for Unilever Stub stands at $62.10 per share. Unilever, a global consumer goods leader, is driving premiumisation and innovation across key categories. Post-TMICC spin-off, focus shifts to top brands (~75% of revenue), enabling margin expansion and sustainable MSD growth despite macroeconomic pressures.

GEK Terna (GEKTERNA GA) Greece

Still the best infrastructure play in Greece - ResearchGreece raises their TP to €30.6 (from €26.9) following model updates reflecting recent milestones, including commencing operations at Attiki Odos, progress at Kasteli Airport and securing the North Crete motorway concession, with Egnatia Odos still pending. Following its energy JV with Motor Oil, GEK’s results will now focus on construction and concessions, with the power and supply business equity-accounted. ResearchGreece sees Attiki and Egnatia driving a doubling of Group EBITDA by 2028, valuing operating concessions, Egnatia and Kasteli Airport at €21/share, equivalent to ~90% of GEK’s current m/cap. Updated forecasts factor stronger motorway traffic and higher financing costs, with valuation led by concessions (69% of total) in their SOTP model.

Prysmian (PRY IM) Italy

Forensic Alpha increases their PRY risk score from 5 to 8 (out of 10) following release of the company’s 9M25 results. Flags identified point towards issues re. cash flow presentation, notably a sharp increase in receivables factoring (€351m vs. €126m in 3Q24), which boosted OCF by ~€225m but was not discussed in management’s presentation or call. A closer look at “Trade and other payables” raises further questions, with a balance of €426m classified as “Other” - representing ~10% of net debt - has more than doubled Y/Y. Combined, factoring and payables effects account for >50% of reported FCF. Investors should be cautious in extrapolating the positive trends highlighted by management, particularly considering the company’s growing appetite to deploy its balance sheet for M&A under its new CEO.

North America

How to beat the S&P500 - the Q&A that matter

Trivariate examines six core issues for long-only managers benchmarked to the S&P500: 1) Beta: despite long-term data favouring sub-1.0 beta portfolios, this is currently nearly impossible given the high-beta “Great 8”. 2) Alpha vs. Risk: ~75% of holdings should be for risk management. 3) Diversification: run both a broad risk book and a concentrated alpha book - essentially two portfolios in one; holding a higher number of stocks vs. history. 4) Position Sizing: take large, conviction-weighted bets in names with high company-specific risk / hard to replicate (e.g. Healthcare). 5) Blow-up Avoidance: avoid large exposures to bottom-decile FCF converters, large increases in inventory-to-sales, large intangible accruals and extreme valuations. 6) Macro: portfolio managers must consider what set of macro conditions are best for their portfolio performance.

MAER Best Ideas

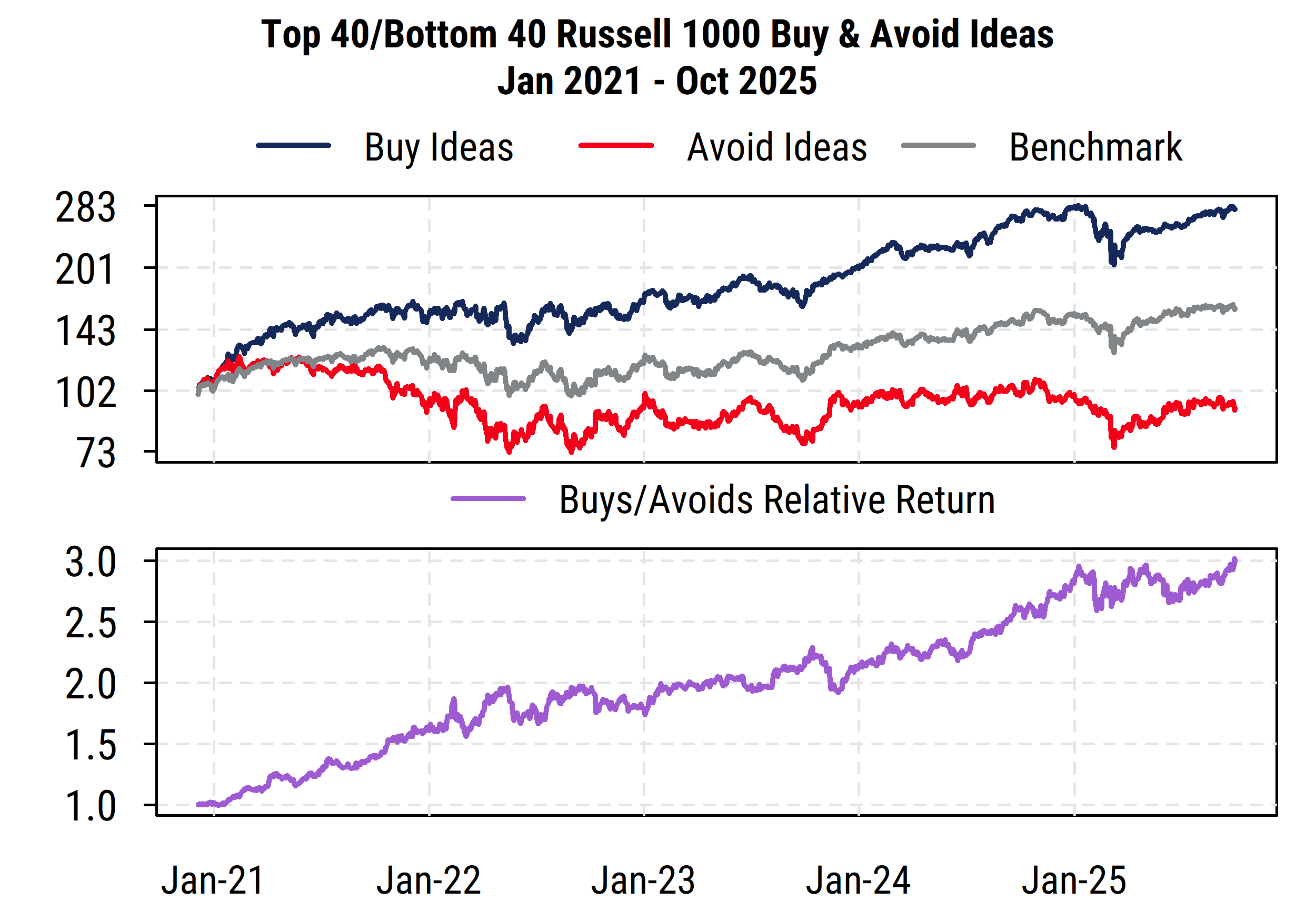

MAER (The Monitor of Analyst Earnings Revisions) is Mill Street’s long-standing multi-factor quantitative stock selection model and graphical tool. It uses proprietary indicators for earnings estimate revisions, price action and valuation to forecast intermediate-term relative returns for ~6500 stocks globally. With Q3 earnings reports in full swing, the latest monthly MAER updates for the Russell 1000 universe show ~60% of the universe is maintaining positive revisions trends, a relatively high proportion though off its recent peak. While Tech estimates remain quite strong, the sector has had a big move recently and the sector that stands out as a potential contrarian play is Financials, where estimates are still rising but relative returns have lagged lately, improving relative valuations. The list of highest-ranked stocks includes many Financials from multiple industries, including Morgan Stanley, BlackRock, US Bancorp and Chubb.

AI driven 10Q / 10K text analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) Akamai - ongoing competition, pricing pressure, DIY, alternative sourcing strategies. 2) Align - increased competition? Customs investigations? 3) Arista Networks - more benign competitive and market conditions. 4) Bruker - covenant concerns. 5) Celanese - greater than usual year-end destocking in Q4. 6) Jazz Pharmaceuticals - caution on ability to maintain or increase sales.

GHRA reiterates their Buy-rating following EXPE’s 20%+ post-earnings rally, as they believe management's efforts to improve the business will continue to pay dividends over coming quarters in the form of upward revision and in turn value creation. Q3 saw upside across key metrics (nights, GBV, EBITDA, EPS) while EXPE also issued Q4 guidance well ahead of consensus (GHRA increased their Q4 EBITDA and EPS estimates to $754m and $3.29, respectively). With EXPE trading well below Airbnb and Booking, they see a low-risk, high-reward setup, supported by a CEO that understands the task at hand (improving traffic & conversion), a growing B2B business, improving marketing efficiencies and sizeable buybacks. TP $320 (10x 2027E EBITDA).

Financials / Business Services Idea Forum

Many of the ideas presented at MYST’s buyside event featured a rate sensitivity or credit angle, while a few focused on competitive dynamics and incorporated unique proprietary data to track. It was noteworthy that several of the stocks discussed are either trading near 52-week lows or near recent highs. The most compelling ideas included:

Chime (CHYM) - Trading at substantial discount to peers despite strong member growth potential. TP $31 (65% upside).

Nu Holdings (NU) - Earnings set to inflect as Mexico losses abate while Brazil lending re-accelerates. TP $25 (55% upside).

Kinsale (KNSL) - Combined ratio unsustainable as competition intensifies in softening market. TP $270 (30% downside).

Blue Owl (OWL) - Dividend cut likely amid elevated leverage + margin compression. TP $11 (25% downside).

While PEN’s 3Q25 beat was driven by a surprise surge in Embolization & Access sales (+22% Y/Y), growth in the key US Thrombectomy business continued to decelerate (+19% Y/Y vs. +23% in Q2, +25% in Q1 and +27% in 4Q24). Despite management suggesting the slowdown was primarily attributable to weakness in the stroke thrombectomy market, US VTE growth also decelerated substantially (+32% Y/Y from +42% in Q2), likely because Stryker/Inari is getting back on its feet and new competitors are entering the market. With FY25 guidance implying PEN’s overall revenue growth will decelerate meaningfully from +18% Y/Y in Q3 to just +14% Y/Y in Q4, OWS sees the post-earnings rally as an attractive shorting opportunity.

Reno Bianchi argues that AAL’s core operating problem is management’s inability to control costs as effectively as competitors. Q3 was poor with a significantly deteriorating cash conversion rate and a substantial increase in the group's leverage metrics. He continues to recommend staying away from the risker parts of the group’s capital structure (equity and unsecureds) and also from the longer dated secured securities. He does not believe the fixed income market fully appreciates how speculative this credit really is.

Value in the volatility - concerns around AI disruption and Mark Leonard's departure, which have driven CSU shares down >30% since the start of Jul, are more sentiment-driven than reflective of any fundamental deterioration. On AI disruption risk, CSU is well positioned to serve as the distribution layer for AI solutions, given 1) its existing customer relationships, 2) proprietary industry knowledge and 3) in some cases, the ability to leverage data. In addition, CSU can continue to thrive despite Mark Leonard being less involved because of its decentralised structure, which pushes agency to the edges and fosters an entrepreneurial culture in both capital allocation and operations. Veritas maintains their Buy rating and intrinsic value of $5,500/share (70% upside).

JNK's research shows GOOG's direct TSM capacity reservations signal a shift away from expensive third-party AVGO design partnerships. The company is now booking advanced packaging without immediate orders, positioning for late 2026 TPU production deployments. TPU 7e progresses with MTK handling I/O integration on roughly 2M unit volumes, while TPU 8p selection between AVGO and AIchip reflects growing design house pricing pressure. This mirrors AWS's trajectory - from external partnerships towards full internal design control. Near-term, Alchip and MTK benefit from current programmes. Longer-term, AVGO faces structural headwinds as hyperscalers internalise capabilities. Click here to access the full note.

Richard Windsor argues that data centre revenue is the “elephant in the room” the market is ignoring, with substantial contributions now expected in FY27 rather than FY28. He estimates QCOM’s A200/A250 products could add ~$2bn in incremental data centre revenue, with potential upside if a hyperscaler deal closes soon. Combined with stronger PC growth (he views current forecasts as far too low) and upside optionality from its BMW-linked ADAS stack, QCOM’s diversification beyond smartphones is ahead of schedule. Q4 results beat across all metrics, but the real story is the growth visibility emerging in new segments. With Street EPS forecasts for FY26-27 still overly conservative and the stock trading at ~14x 2026 P/E, it’s easy to see how both multiple expansion and upward estimate revisions could drive a strong rally in the shares.

PATH has repositioned itself as an “agentic automation” platform riding the AI narrative, but the fundamentals point to slowing growth. Expansion within existing customers is under pressure and the company’s ARR metric - built on future invoice value rather than reported revenue - overstates momentum relative to true performance. Guidance has improved modestly, but it is based almost entirely on FX tailwinds and timing shifts, rather than underlying demand. Deferred revenue and billing trends point towards a normalised growth rate several hundred basis points slower than reported results and management’s increasingly promotional tone around partnerships leaves much to be desired. With federal spending already pressured in the first half and a government shutdown threatening further disruptions to its US federal pipeline, Corto believes that near-term risk is clearly to the downside.

Varonis: Impact of growing competition

The company’s latest stumble stems from a weakening Federal pipeline and sluggish on-prem renewals, but channel feedback points to deeper challenges from nimble DSPM rivals like Cyera and Concentric.ai to mounting pushback on costly cloud migrations that offer less functionality. With competitive share shifts and customer dissatisfaction surfacing in SPR’s 10/12 panel, it’s clear the DSPM market is heating up fast, fuelled by AI-driven data priorities and VRNS may be losing its footing. SPR’s full note unpacks which vendors are gaining ground, why end users are rethinking their data protection stack and where this market is headed next.

Australia

GMR upgrades GMD to Buy, viewing it as a compelling gold play in Western Australia’s Leonora–Laverton region, which accounts for ~20% of national production. The business has continued to advance organic opportunities and strategically bolt-on stranded resources, and now has the resource base to justify mill expansions, with an updated strategy release due in 1H26. GMR assumes a 2Mt/yr expansion at Gwalia, fed by Tower Hill and Laverton, supporting production growth towards 350-400koz/yr. Trading at 0.6x spot NPV5, GMD screens attractively vs. peers, offering appealing growth and rising NPV potential. Regional consolidation remains a key theme, with the company positioned as both a predator and potential target within a competitive Northern Goldfields landscape.

Japan

Katitas has mastered a business model that many find difficult to replicate: buying, renovating and reselling pre-owned homes with consistent success. With 36% foreign ownership, investors clearly recognise the company’s ability to address Japan’s vacant housing problem and the stock trades at a premium P/E of 18x vs. single-digit averages for residential construction peers. Following strong H2 results and raised guidance on Nov 7th, the stock jumped 10%. Yuka Marosek’s latest piece explains why Katitas’ unique business model deserves that premium.

Emerging Markets

New Street turns more positive on Bharti, arguing that focus is likely to shift back to the company itself after Airtel Africa and Singtel materially outperformed over the past year. Bharti has historically rallied ahead of tariff hikes and with price increases expected in H1 next year, momentum should build. Growth is accelerating across Home and Enterprise, AAF continues to perform strongly and capital intensity is now falling, supporting margin expansion and rising ROIC. With fixed wireless access (FWA) adoption gaining traction and scope for meaningful EBITDA beats through FY26-27, New Street raises their TP to INR 2,750 and sees a strong case for re-rating as earnings expectations climb.

Alibaba (9988 HK) Hong Kong

Breaking the value trap - 86Research’s report presents a focused analysis of GenAI-powered commerce, a strategic frontier they believe investors have overlooked. Market attention has remained concentrated on AliCloud’s reacceleration, while continuing to dismiss core commerce as a “value asset” trapped in macro drag. By spotlighting conversational interfaces and AI-enhanced ad tech as emerging structural advantages, 86Research sees a window of opportunity opening. A wave of initiatives has already unfolded in 2H25 and they expect Alibaba to further escalate its efforts in 2026, catalysing a period of positive news flow and re-rating potential.

Pemex: Debt strategy extends support, spreads tighten vs. Mexico

Mexico’s comprehensive debt strategy highlights extraordinary sovereign support for Pemex, easing refinancing pressures and compressing spreads relative to the sovereign. Still, EM Spreads thinks further tightening will hinge on Pemex’s fundamentals, as investors are likely to increasingly focus on its operational profile. At current spread levels and with a steeper curve, they continue to recommend the PEMEX 6.700% 2032s (6.7% YTM, 4.3-yr duration) as offering best value in the belly. For higher duration appetite, they see the PEMEX 7.690% 2050s (8.6% YTM, 10.1-yr duration, $82 price) as most attractive on the long end, with compelling carry and upside potential.

Macro Research

Developed Markets

Blonde Money

UK: Uncertainty in Number 10

It has begun. Last Tuesday No 10 briefed lobby journalists that the PM would fight any leadership challenge in the wake of the Budget, warning that to bring a fight could destabilise financial markets. Specifically, the finger was pointed at longtime young pretender, Health Secretary Wes Streeting, who according to the Guardian, has "50 frontbenchers willing to stand down if the budget landed badly and the prime minister did not go". Helen Thomas has stated for some time that Starmer's enemies had means, motive and, with the Budget, opportunity. Now, the PM definitely knows. Briefing such specific information smacks of desperation, rather than strength. It reveals the inevitability of a challenge. It forced Streeting's official spokesman to issue a rebuttal that any plotting was "categorically untrue". By pinning his survival on the financial markets, it also leaves the PM vulnerable to those self-same markets. Meanwhile markets must price in more political volatility ahead, including risks of a more left-wing government.

US: Manhattan 2.0

James Aitken definitely understands why so many believe Xi is winning, or that he has it all over Trump, and so forth. Yet, James is becoming increasingly confident that the full industrial, financial and entrepreneurial might of the US has embarked on a Manhattan project 2.0. We are not in a trade war, or a rare earths war, but rather a supply-chain war that the Trump administration has determined it must fight. The accelerated de-risking from China now underway is not always noticed by markets, but it is not going to reverse. Through time, de-risking done right gives one the option of a full de-coupling, should the latter be deemed necessary. Unbelievable amounts of money will now be thrown at the attempt to reduce China’s leverage over the West. Whether that attempt succeeds or not is perhaps less important for investors than the fact the money and deal flow is just getting started.

Short-Term Rates-1 Model

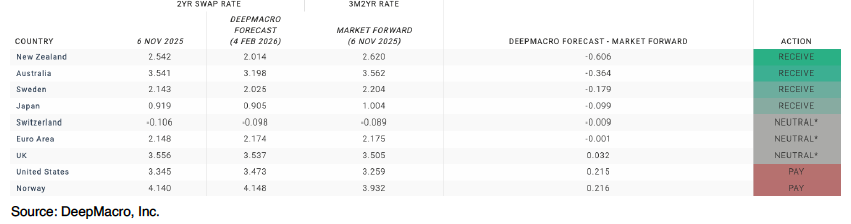

DeepMacro’s STR-1 is a short-term rates model, providing forecasts of 2yr swap rates for the G10 countries over the next three months. The team choose 2yr swap rates because they are an estimate of the market's expectation for monetary policy over the medium term, which they recognise as a function of economic growth and inflation. STR-1 generates receive/pay recommendations based on the difference between model forecasts, and market forward interest rates. The inputs to the model are the DeepMacro growth and inflation factors, including "Big Data", and DeepMacro's automated, machine-driven analysis of central banks. Currently, the model expects rates to rise in the US, but the market forwards expect rates to decline. In Europe the model forecasts rates to rise but by less than market forwards, and in UK it expects rates to decline but by less than market forwards, but both gaps are not large enough to recommend a trade. Please get in touch to find out more.

US: Portfolio adjustments after shutdown

To the surprise of David Woo and many others, eight Democrats decided to walk across the aisle on 9th November and the US government shutdown now looks set to end sometime this week. Meanwhile Trump is promising to send a $2000 stimulus check to every American, presumably to stem his sliding approval rating. In response to these developments, David Woo decided to close his short consumer discretionary position (but not his long staples position). Filled at 238.28. David is also adding a short position in 30y bonds to his long position in 5y notes to play for potential renewed curve steepening. The end of the data blackout could put more pressure on the Fed to cut rates. Filled in the December bond future at 117.03. David also initiates a long AUD/USD position that should also benefit from the calming of the US-China relations.

USD short squeeze thesis playing out

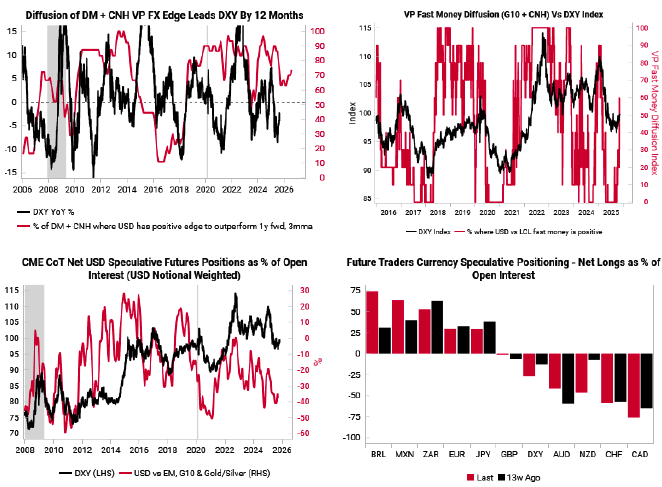

The Variant Perception team’s cyclical and tactical indicators still point to a rebound in the USD through year-end as markets are now pricing in less easing from the Fed and net positioning remains short USD. On a cyclical basis, their fundamentals-based FX edge model still shows the USD has a positive expected 1-year total return against most G10 currencies (top left chart). Meanwhile, most tactical indicators we monitor suggest the dollar is bottoming out. Their Fast Money diffusion index – a measure of speculative activity – has risen from 0% to over 50%, which has marked the start of dollar rebounds over the past decade (top right chart). To add to this, short positioning against the dollar remains stretched (bottom two charts): aggregate positioning is near multi-year lows, much of which is concentrated in longs for EUR, JPY and high-carry EM currencies. Their preferred expressions for a tactical dollar bounce remain long USD/KRW and short EUR/USD.

Hong Kong: Stepping in

Andrew Hunt believes that the HK authorities have contrived to boost domestic liquidity over recent months by repatriating government assets held offshore, and further expanding the domestic counterparts to base liquidity growth. The latter is in direct contravention of the rules of the HKD Link. Initially, the proactive policy did lead to an improvement in asset prices, domestic loan growth, and even economic trends. However – and just as theory would have predicted – the stimulus has caused the external accounts to weaken again. Unless the authorities repatriate more funds, investors can expect liquidity trends to soften again and the equity market to return to its underperforming status. At present, there are no signs of any further repatriations, but they are of course possible. Over the long term, Andrew Hunt maintains his bearish view of the HKD.

If AI blows up, Japan is holding the baby

When the dotcom bubble burst, the US paid the bill. Neil Newman says that this time, it’s different. The $550bn investment package proposed by Japan during tariff negotiations is now being channelled into specific projects, with $30bn already earmarked for the AI and chips sector. AI has yet to be monetised to any large degree; if Japan is paying for the development of AI infrastructure in the US, and AI fails to deliver the revenues needed to justify the data centre adjustments, Japanese companies and ultimately the Japanese taxpayer will be footing the bill this time around. While the drivers of speculation and FOMO remain the same, valuation is concentrated in a handful of mega companies. A significant correction is possible, but a total collapse like 2000-2001 is unlikely.

South Korea: Trend exhaustion

At last week’s new ATH of 599, the Kospi 200 index had just about doubled from April’s 303 low. But at the end of the week, the index had closed below the low of the prior week’s range. Chris Roberts comments that this is a key reversal, a signal of trend exhaustion. If the uptrend is exhausted, where will it find a place to re-group? There is a broad area of support at 400–444. If that’s too deep, then the area of the rising 40-week WMA (last at 444) may come into play. Indicators have started to retreat from extremes, the 14-week RSI was close to extremely overbought 90 before last week, signalling that sentiment was a bit OTT (over the top). If long, take some partial profits.

Emerging Markets

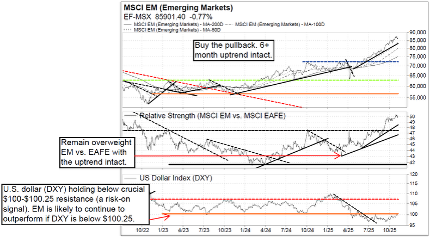

MSCI EM: Buy the pullback

The 6-month uptrends on MSCI Emerging Markets index (local currency) and EEM-US (USD) remain intact, and the Vermilion team remain bullish. They have discussed for months how they expect support at the uptrend, which also coincides with the 50-day MA on EEM-US. They are getting that test now -- buy. View any pullback to $48 support on EEM-US as a buying opportunity. For EM countries overweight recommendations include Taiwan, China, and South Korea. Taiwan and South Korea have pulled back some with the general pullback in global technology names, and the team are buyers. For EM sectors, defensive sectors (Staples and Utilities) continue to underperform and are near YTD RS lows; the team expected this underperformance to continue, and it has -- avoid. Meanwhile, attractive sectors include MSCI EM Technology, Materials, Industrials, and Communications. Look out for an RS bottom in EM Energy, where the team highlight several actionable names.

The rise of China’s intelligent economy

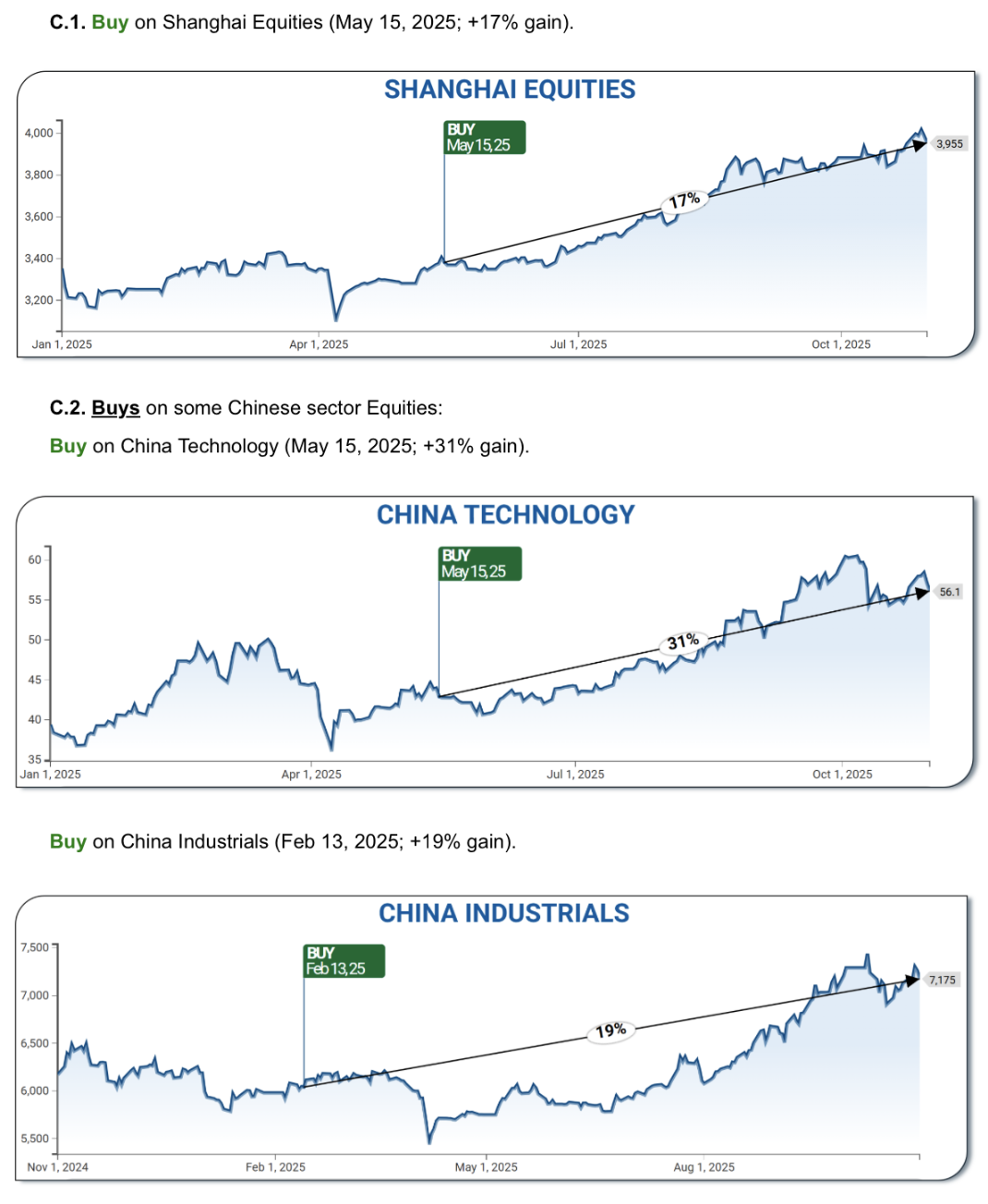

Konstantin Fominykh comments on the breathtaking structural rise of China’s intelligent economy, powered by technology and automation, which is advanced at a scale and speed that far surpasses global peers. It is overtaking the US in key next-gen industries, and over the next few years its main strengths will be EVs, green tech, 5G, high-speed rail, and defence. Currently, we might be witnessing a cyclical recovery, with manufacturing production up 7.3% YoY, service activity expanding again, exports up 3.3% YoY, and consumer confidence finally stabilising. Konstantin’s predictive tools predict further inflows into Chinese stocks, and he recommends a buy on Chinese sector equities, financials, tech, industrials and healthcare.

Two underrated EMs

According to James Burdass both Egypt and Saudi Arabia (excluding Aramco) are being underrated by emerging market investors, not least because they offer exposure to substantial natural resources and long-term growth potential. Egypt’s appeal lies in its demographics and strategic positioning. Recent economic reforms are improving macro stability, and Egypt’s energy resources, particularly the Zohr gas field, estimated at 30 trillion cubic feet with roughly 60% controlled by Eni, further enhance its investment case. In Saudi Arabia, Ma’aden represents a compelling opportunity. With a market capitalisation exceeding USD 60 billion and a free float of 37%, the stock trades in institutionally relevant volumes. The company is well known for its mine-to-market phosphate and fertiliser complexes, such as Waʾad al Shamal, and its integrated aluminium value chain from bauxite to smelting at Ras Al Khair.

Ecuador: At fair value?

Sovereign bonds have rallied sharply together with other EM high-yield dollar credits. Jonathan Anderson asks, is there still value here? On the one hand, absolutely. Ecuador is a successful exporter by commodity EM standards; the country is running sizeable external surpluses; the fiscal balance has improved greatly, and the current IMF program runs through 2028. On the other, Ecuador is also unique in two negative senses. It is a straitjacketed dollarised economy without the comforting buffers of a local-currency funding market or a flexible exchange rate, facing a rising debt service profile over the coming few years. It is also one of very few EM countries that have already defaulted twice on its external obligations in the past two decades alone, with the anti-debt and anti-IMF political left still a significant force at home. On balance Jonathan is maintaining his position, but comments that significant further price gains would present a good reason to take profits.

The Poland market boom continues

The big story in Poland today is the ongoing rally in stock prices. Of course, this isn’t just in Poland but the rest of CEE as well ... and not just in CEE but in most of EM ... led by the dramatic gains in US stocks. So, this is not "really" about Poland at all, remarks Jonathan Anderson. Having said that, he likes Poland macro. Exports continue to outperform abroad, and spending, credit and earnings continue to gain traction at home. What could get in the way? In the near term, the answer is "not much". Inflation is well-behaved, the NBP is easing, the local economy is not meaningfully leveraged and the external balance is still broadly supportive. The main "wild card" is the sharp fiscal deterioration, which will be something to watch in the medium term ahead.

Macro-Advisory

Russia: Close to recession

Christopher Weafer notes that the Russian economy is close to recession. Economic growth has accelerated on the back of big fiscal stimulus and an upswing in the domestic demand – but GDP growth could fall into a negative territory in 4Q25. Industrial output is expected to be near zero, while other segments, such as retail sales and agriculture, could help the economy escape a contraction. However, the growth dynamic will become far less certain in early 2026 with the introduction of higher VAT and inflationary pressures. In 9M25, GDP increased by just 1% YoY (0.9% YoY in September), which puts Christopher’s 2025 growth forecast of 1.2% more on the optimistic side. Over the next 2-3 quarters, the economy will balance at close to zero. Christopher expects that it will be no earlier than mid-2026 when credit conditions could start to improve, thus offering support to a gradual rise in consumer demand and corporate investments.

ESG

Feeling electric

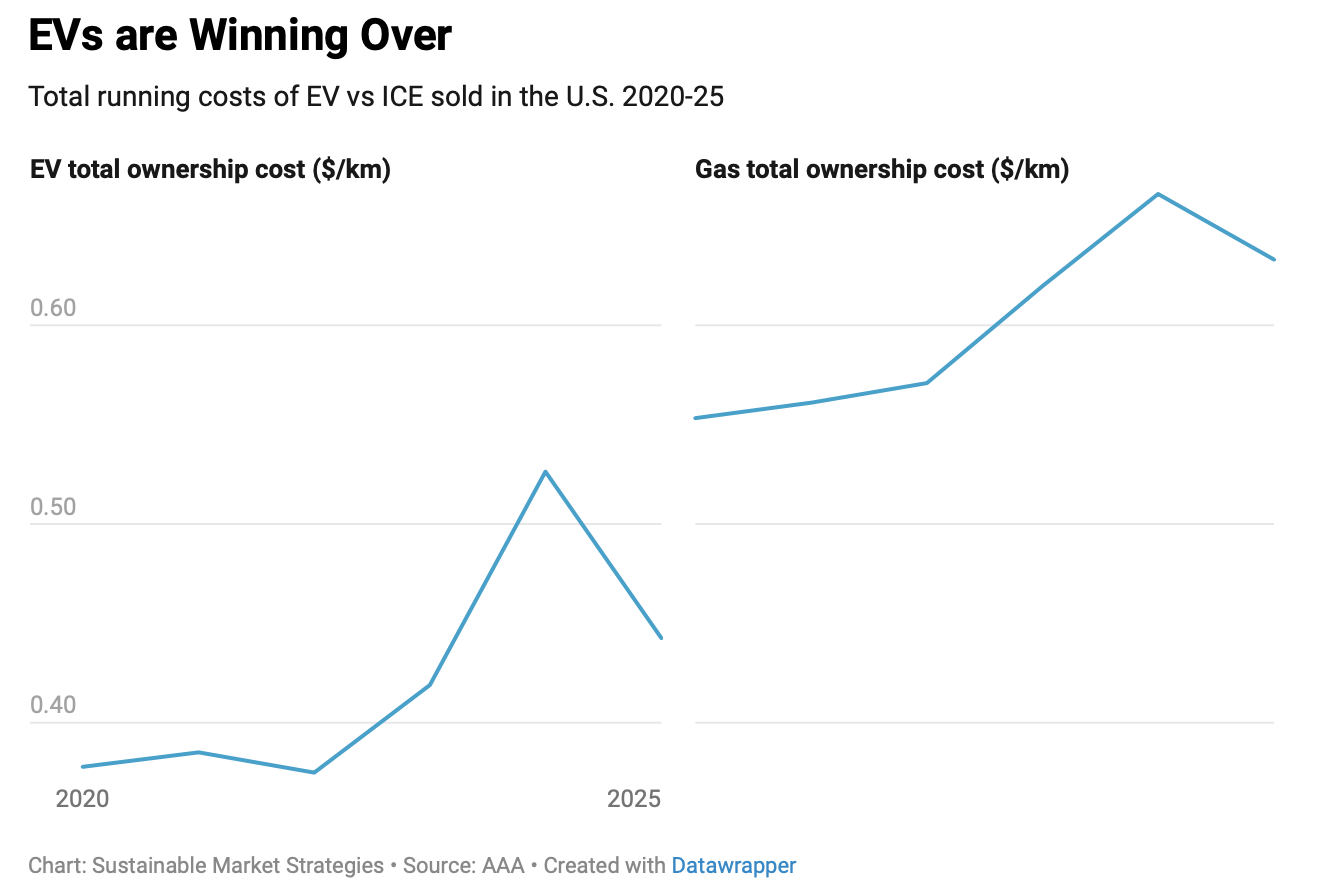

Rumours of the death of the EV have been greatly exaggerated. While Trump applied the brakes on the whole EV industry, setting back the overall energy transition a few years, change is still happening fast. What has gone unnoticed by many is that EVs are now cheaper to buy, own and operate than their equivalent ICE cars. EVs are even becoming the default mode of transportation in EMs, where electrification and grid infrastructure lag behind developed countries. While China steps on the “gas” and boosts their EV production and capabilities, US makers are slowing down their EV rollout, and in some cases even considering bringing production to a stop altogether. For those looking for exposure to up-and-coming EV names with some exposure to ICE tech, Korean automakers are interesting and cheap. Go short on US legacy automakers and long on Chinese and Korean auto and battery makers.

Investors not seeing the forest for the trees

With COP30 taking place in Brazil, deforestation is being thrust back into the limelight. Verisk Maplecroft’s new Deforestation Rates Index (DRI) shows that some of the major commodity exporters viewed positively by ratings agencies are failing to address deforestation. Such risks being priced in are becoming more important than ever as the EU Deforestation Regulation (EUDR) comes into play, mandating deforestation free key commodities. High risk countries include Nicaragua, which was upgraded by S&P from B to B+ in 2024, yet ranks third highest in the DRI; the country has seen significant loss of forest in areas with significant ties to its export industry. Bolivia ranks at the top of the Index, its deforestation rates tripling due to soy and cattle production. Indonesia and Malaysia have seen rates fall but still sit in the extreme risk zone of the Index. Ignoring the price of felled trees may come at investors’ peril.

Commodities

The gold-Bitcoin axis

Michael Howell notes that global money is bifurcating into two rival spheres, led by the US and China. America is digitising its debt to maintain dollar dominance, a technological upgrade aimed at boosting efficiency and creating new demand for US debt, yet does not solve the underlying problem of fiscal indiscipline. China is building a rival monetary system anchored by strategic gold accumulation. By offering trade partners the potential to exchange Yuan for gold, China creates ‘notional backing’ for its currency, building trust through a tangible asset. Michael identifies a systematic statistical relationship between Bitcoin and gold, with an "attractor point" around a ratio of 28 times. This implies their prices are linked in the long run, trending together despite short-term cyclical divergences. Both Gold and Bitcoin are hedges against monetary inflation, and the geopolitical battle for monetary dominance will make owning both digital and physical inflation hedges a prudent future strategy.

Gold and silver update

Andrew Egan Baptiste notes that both gold and silver have rallied up to his listed attraction zones. With the attainment of the new rebound highs, he has closed his tactical long positions into strength as recently discussed. Moving forward, given the overall shallow depth of the correction off the 3901.30 selloff low, Andrew expects a corrective pullback in a wave ‘x’ position, that can then lead higher towards the 50% retracement at 4142.00, and potentially up the highs of the prior triangle wave ‘b’ consolidation at 4156.00, 4171.50, and 4175.00. Above that is 61.8% Fibo. retracement at 4201, although he doesn’t believe we can get there without a pullback. If we see evidence of a corrective pullback, Andrew will consider another tactical long. He is now looking for the next opportunity, which he says will likely be on the short side in silver.

Why investors keep buying silver

In his latest video, Jeffrey Christian of CPM Group discusses recent developments in gold, silver, platinum, and palladium prices, and their consolidation following October’s sharp rise. He also looks at the factors that could determine the next breakout for the metals, and whether the next price move might be higher or lower. Jeff takes an in-depth look at the physical silver market and addresses several misconceptions about physical supply, fabrication demand, investment demand, and inventories. He looks at mine production, secondary recovery, fabrication demand, inventory levels, and investor activity, explaining how the market remains well supplied even as investment demand has risen sharply in recent months. Jeff also discusses ETF flows, coin sales, premiums for 1,000-ounce bars, and why talk of a “silver shortage” is misleading.

Click here to watch.