Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

Apollo: Data that changes the game

Libra’s flagship platform enables investors to observe, rank and act on fundamental market shifts across stocks, sectors and themes. Apollo highlights re-ratings, de-ratings and forecast changes - supporting timely, data-driven decision-making. Access to Apollo data allows investors to map changes in valuation, identify entry points and exit points, and the evolution of the (dynamic) investment cycle in real time. This ability to detect inflection points as they develop provided early evidence to build and maintain exposure to gold stocks while avoiding the subsequent de-rating in LVMH.

DSV (DSV DC) Denmark

Following publication of its FY25 annual report, Iron Blue increases their DSV score by 4 points to 33/60 (top decile and fertile grounds for shorting), reflecting 1) more cost strip outs; 2) increased use of provisions accounting; 3) Schenker acquisition accounting (principally around general and bad debtor provisions fair value adjustments and possible future PPE sale & leasebacks); 4) increased pension deficit (including when adjusting for a high liabilities discount rate); 5) another doubling of whistleblower cases and deteriorated health & safety performance & target; and 6) a rise in the rate of employee unionisation to 41% from 30%.

Vinci (DG FP) France

Robert Crimes updates its long-term forecasts for the stock and increases his TP to €192 (40% upside). The company boasts a high-quality mix of French autoroutes, international airport concessions, while Energies benefits from global megatrends driven by energy transition and digital transformation. In 2026-30E, Robert estimates DG will generate >€30bn of cumulative FCF pre-dividends. He assumes ~€20bn is returned to shareholders including €17bn of dividends, supporting a DPS CAGR of +10% over the period, plus €3bn of net share buybacks, while still leaving c.€8bn of additional capital available for debt reduction (yet Group ND/EBITDA is already low at 1.3x in 2026E), long-duration acquisitions (most likely airports) to increase the company's weighted average Concession duration or enhanced shareholder distributions.

Insider buying in beaten-down Tech stocks

Smart Insider flags a number of insider buys at Hexagon, Sage and ATOSS following recent share price weakness, ranking all 3 stocks +1 (highest rating). At HEXA, the new CEO, Chief Strategy Officer and Vice Chair made their first purchases, buying a combined €3.4m of stock, shortly after results and the announced spin-off of Octave Intelligence. At SGE, 2 long-serving non-execs bought stock, including one director tripling his holding in a rare purchase and at a higher price than his last buy 5 years ago. At AOF, the CEO invested €11.6m (adding 4% to his stake) and the long-tenured CFO made his first-ever purchase - a notable shift from a series of smaller sales.

North America

Selling the tollbooth: How markets misprice AI disruption

Paul Krake argues the software sell-off is a template for how markets will misprice AI disruption across sectors, with narrative overwhelming fundamentals. Investors are pricing the speed of AI code generation while ignoring what it takes to replace enterprise software embedded in payroll, compliance, procurement and financial reporting across years of data and regulatory architecture - these systems are upgraded, not replaced. AI agents may compress seat counts, but pricing can migrate towards usage and consumption models - the toll changes, the tollbooth remains. Hyperscalers are incentivised to monetise AI infrastructure by supplying incumbents, not competing with them at the application layer. In a post-cyclical framework where margins compound and friction removal benefits incumbents, he views the sell-off as an opportunity rather than a structural warning.

Accounting red flags emerge across multiple names

SMCI moves to Forensic Alpha's maximum ‘10’ risk rating after its 10Q revealed extreme working-capital swings: receivables surged from $2.5bn to $11bn in one quarter, heavily concentrated in a single customer, while payables ballooned to $13.8bn, masking weak cash conversion. Bloom Energy also remains a top concern, with a widening gap between adjusted and statutory earnings, rising contract assets and growing reliance on off-balance-sheet JVs. NiSource’s score rose on higher DSO and advances to unconsolidated VIEs, while Cummins saw a jump in sales to equity investees to $1.70bn, with receivables outstanding from these investees of $523m, suggesting extended credit terms. Other stocks flagged last week include Amentum, Atlassian, Becton Dickinson, Ford and Impinj.

Special Sits Idea Forum

MYST’s buyside events continue to draw impressive attendance while consistently delivering strong results. This Forum was notable for highlighting several foreign companies with imminent US listings (Ashtead, Guardian Metal Resources, SK Square) as well as Healthcare stocks (Cigna, Qiagen). Other ideas presented include:

Boise Cascade (BCC) - trough multiple at cycle bottom with potential business split under new CEO. TP $207 (145% upside).

Core Scientific (CORZ) - robust HPC pipeline not reflected despite buildout running ahead of schedule. TP $34 (95% upside).

Ralliant (RAL) - cyclical inflection masked by “one-time” cost headwinds. TP $60 (35% upside).

VSE (VSEC) - compelling entry point for “transformational” aerospace story. TP $300 (35% upside).

OWS reiterates their short on COCO following 4Q25 results, arguing the print reinforces their original thesis that the company’s perceived supply chain “moat” is overstated. Management disclosed ongoing US market share losses and flagged heavier promotions, distributor incentives and stepped-up SG&A to defend growth. Private label competition is intensifying, pricing benefits are set to fade through FY26 and inventory has surged to 106 days, increasing the risk of further discounting. Meanwhile, ~96% of revenue still comes from coconut water, underscoring limited platform diversification. With insiders adopting new 10b5-1 selling plans and shares still trading at ~3.9x FY26 sales, OWS sees meaningful downside with a TP of $31 (35% downside).

The investment thesis is straightforward: EG's market cap is $13.7bn, its book value is $15.5bn and it generates >$2bn per year from investment income alone. In other words, EG could make no money at all through its core reinsurance and insurance businesses every year, and still be undervalued. It is an incredibly low bar for positive returns. The core risks would be heavy insurance losses going forward or significant deterioration in the investment portfolio. The losses required would need to be much more serious than simply a ‘bad catastrophe’ year, it would require multiple years of dreadfully written business. Ben Jones thinks this is highly unlikely, especially as the group is moving in the correct direction by limiting casualty business and purchasing additional cover for previously written long-tail business.

Tom Chanos trimmed his short ahead of earnings, covering 25% and locking in a 40% gain in 7 weeks. In his original thesis he argued HOOD was trading at ~50x 2026E adjusted EPS and ~30x sales on what he saw as peak cyclical earnings. Transaction revenue fell 44% from 2021-23, remains skewed to options and crypto, and faces regulatory risk around payment for order flow, while newer initiatives like credit cards and gold contribute only ~5% of revenue. Post-earnings, he highlights weak customer performance: including Jan losses, clients have made virtually no money since the start of the Meme Stock Era despite the S&P 500 nearly doubling, with AUM growth largely driven by net deposits. Tom remains very bearish, viewing any strength as an opportunity to rebuild the short, with a materially lower price target.

Craig Huber believes fears that AI start-ups can replicate S&P's data and tools are misplaced, noting that 95%+ of revenue is tied to proprietary benchmarks, subscription data and workflow-embedded products that cannot simply be scraped or reproduced. In Ratings, access to confidential, non-public financial information under NDAs creates structural barriers that AI entrants cannot bypass. He highlights S&P’s entrenched market position, pricing power, high margins, recurring revenues and disciplined capital allocation as unchanged. Importantly, management is investing 3-4% of its expense base annually, including in AI, which Craig sees as margin-enhancing. Bottom line, there is zero evidence that AI is hurting S&P’s financials and market position, and he does not see that changing.

Delivering alpha in 2025; positioning for 2026

In 2025, Bios published 12 short ideas and 2 longs, delivering a 78% absolute hit rate, with 7 of 14 positions closed intra-year. Notable winners included Anavex Life Sciences (~77% absolute return to short sellers), Butterfly Network (~49%) and Arcellx (~30%), while 89bio returned ~115% on the long side. Looking ahead, top short ideas for 2026 include a ~$40bn medtech facing reimbursement pressure, new competition and GLP-1 headwinds; a ~$20bn biotech exposed to excessive hype, competitive threats and clinical trial failure; and a ~$10bn commercial pharma/biotech likely to see material y/y sales declines and poor regulatory environment. On the long side, Bios highlights a $1.5bn development biotech with strong data and potential for FDA approval in 2H26 and a ~$600m biotech with multiple assets in development and 3+ years of cash, where material licensing / M&A potential exists.

Following Bayer’s full Phase 3 FXIa stroke readout, the market appears to be positioning BMY/Johnson & Johnson's milvexian as a structurally disadvantaged, late entrant. The central debate is whether differentiation remains plausible or whether share is effectively locked. Foveal's work suggests the probability of clinically meaningful separation is not being fully reflected in positioning, creating asymmetric equity implications across both sponsors in a multi-billion-dollar stroke market, with additional optionality in AF that is currently treated as zero.

AXON is a play on increasing digitisation and AI adoption in police and public safety, with potential for 20%+ revenue growth for many years. Abacus argues AXON is not “just” SaaS but a physical and digital “walled garden”, combining dominant hardware (TASER, body cams) with high-margin, recurring software (96-97% subscription-based) that drives 124% net dollar retention and strong upsell. Multiple product cycles (TASER 10, robotics, Draft One AI, 911 suite) and expansion into enterprise and international markets underpins growth. While the market is focused on weaker incremental EBITDA margins and tariff headwinds, Abacus sees these as short-term risks within a structurally advantaged AI beneficiary.

Ero Copper (ERO CN) Canada

The company reported 2025 copper production of 64kt, below its latest 67-80kt guidance (previously 75-85kt). FY26/27 guidance has been cut, Tucumã costs increased and capex lifted materially vs. GMR’s previous expectations, extending a multi-year pattern of downgrades. Despite this, the shares fell only ~15% which was not much worse than other miners in the recent sell-off. On the positive side, Q4 production improved sequentially and GMR forecasts copper output to rise to 67kt in 2026 and 76kt in 2027, with Xavantina gold remaining highly profitable. However, on the back of the news, they have reduced NPV10 (copper US$4.75/lb real) by 33% to US$12.45/sh. The stock trades at ~2.5x valuation with FCF yields now much lower than previously estimated. To GMR the risk/reward is no longer attractive given the shares are near a five-year high. Downgrade to Sell.

Contrary to Street expectations, JNK supply chain research indicates AMBA's near-term strength masks structural headwinds. Book-to-bill remains above 1.0x, channel inventory is lean and pricing is stable. However, the underlying trajectory is weaker: FY27 revenue is tracking roughly flat Y/Y, reflecting rising customer and geographic concentration risk. Two customers account for more than one-third of China revenue, while Qualcomm design activity is increasing across AMBA accounts. In addition, Samsung remains AMBA's only foundry partner for leading-edge 3nm and 5nm nodes; whereas competitors source from multiple fabs. Limited consumer exposure further constrains diversification. Recent order strength does not mitigate the single-foundry dependency or competitive encroachment now visible in JNK's tracker data.

Emerging Markets

Iii conducted channel checks across the 3 companies to assess demand, competition and store economics. Footfall is flat to modestly down, growth is increasingly promotion- or online-led and store-level productivity appears constrained - pointing to normalisation rather than reacceleration in discretionary demand. On FirstCry, consensus expects multichannel growth to reaccelerate to mid-to-high teens via RocketBees and FC Quick, however, Iii believes execution delays and intense competition will keep growth in low single digits. For Bluestone, the Street assumes Q3’s operating leverage and ~12% pre-IndAS EBITDA margin are sustainable, but Iii expects margins to deteriorate within 1-3 quarters as seasonally weaker revenues expose a high fixed-cost base. At AVL, incremental store expansion appears supported by discounting and channel inventory build rather than productivity-led leverage.

TGCC (TGC MC) Morocco

AlphaMena sees TGCC as a prime beneficiary of Morocco’s structural investment cycle, demonstrating resilience and robust operational performance despite broader market volatility. The company’s strategic positioning on high-visibility infrastructure provides rare multi-year visibility and underpins a strong order book. Growth has been driven by the integration of STAM VIAS and expansion in civil engineering, lifting cumulative operating income +51% Y/Y, while net debt has significantly reduced. Flagship projects such as the Mohammed V Airport terminal and Grand Stade de Benslimane reinforce long-term revenue visibility ahead of the 2030 World Cup. A ~18% post-summer 2025 share price correction, presents an attractive entry point for investors, with AlphaMena targeting 30%+ upside.

Indika Energy: Moody's downgrades ratings to B1 from Baa3

Lucror broadly agrees with Moody’s downgrade, consistent with their “Negative” Credit Bias since Aug 24. Weak metrics are set to deteriorate further amid higher-than-budgeted capex at the Awak Mas gold project and subdued thermal coal prices. Leverage is projected to rise to c.7.0x Debt/EBITDA in FY26 (from c.6.0x in FY25) before easing toward c.4.0x in FY27 as gold operations stabilise. Liquidity is viewed as adequate over the next 12-18 months, but covenant headroom will tighten, particularly around the 3.75x Net Debt/EBITDA test. That said, the Newcastle coal benchmark has stabilised for almost a year now, so, Indika’s credit metrics may not worsen much more going forward and Lucror agrees with Moody’s outlook revision to stable. They maintain a "Buy" recommendation on the INDYIJ 8.75 '29s at 99.6/8.9%/2.7Y, as the high yield more than compensates for the weak and deteriorating credit profile.

TSMC (2330 TT) Taiwan

Arete describes TSMC’s 4Q25 call as one of the most significant tech updates in years. There were some seismic statements from the normally conservative management team: $52-56bn 2026 capex, “significantly higher” three-year spend, AI accelerator growth at a mid- to high-50% CAGR to ’29 and a 25% five-year overall revenue CAGR. Arete believes TSMC has unmatched visibility across the AI supply chain and is effectively fully booked at the leading edge through 2027, with hyperscaler capex underpinning multi-year demand. They model N2 capacity ramping to ~295k wpm by YE28 and see pricing power (including US wafer premiums) sustaining low-to-mid 60s gross margins. Despite execution and hiring risks, Arete lifts their TP to NT$2,770 (45% upside), viewing earnings growth - not multiple re-rating - as the key driver.

Macro Research

Developed Markets

The troubled AI trade

What goes up must come down, reminds David Woo. The AI trade is clearly stalling. Of the 6 Mag7 firms that have released earnings reports, the 4-quarter moving average of their EBIT has slowed to the lowest level since 2023. The question is how long before profit taking begins. For the last three years the AI trade has been driven by the capex spending of the hyperscalers, which investors saw as a proxy for expected return in AI investment. David has been sceptical of this for some time, which is why he went short Nasdaq in September. Over the past month the correlation between the AI trade and related spending not only broke down but went negative, a watershed moment for investors. Hyperscalers are driven by fear rather than greed, and overinvestment is almost certain. The bubble remains the biggest risk in 2026, and David is staying short Nasdaq, long Nifty50, short Bitcoin and long 5s-30s steeper positions.

Cycle convergence: Oil, geopolitics and crisis risk

Ron Williams explains how the correctly anticipated Q1 2026 shakeout signals a structural repricing rather than routine macro volatility. Cycle convergence; late-cycle economics, geopolitical tension, and behavioural reflexivity, is pushing markets to price credibility risk and supply fragility ahead of fundamentals. Oil has become central to this shift, increasingly trading as a geopolitical hedge amid rising volatility and renewed attention to chokepoint risk. A longer historical view of Iran shows recurring phases of strain, rupture, consolidation, and renewed pressure. Current developments suggest another inflection window, unfolding within a broader transition in the global order that favours hard assets and resilience over precision.

STOXX 600: Leaders coming up to resistance

Valerie Gastaldy points out that the STOXX 600 has outperformed US indices in 2025. The strongest contributors to this performance have been Basic Resources, Telecom, Utilities, and Oil and Gas. Valerie notes that these sectors may still have a few additional percentage points of upside before three of them retest their 2007 highs. Banks, meanwhile, approached resistance again a couple of weeks ago. In the past, reactions at comparable levels have been relatively benign. However, if several leading sectors were to encounter resistance simultaneously in the coming days or weeks, Valerie says it would make the achievement of new index highs more challenging.

The post-1945 international order no longer exists

Brunello Rosa notes that the 62nd Munich Security Conference took place at a moment of profound uncertainty for the international system. Under the stark theme “Under Destruction”, much of the conference can be understood through two lenses: the Trump administration’s National Security Strategy, and the contrasting keynote speeches delivered in Munich by German Chancellor Merz and US Secretary of State Rubio. Chancellor Merz said the post-1945 international order “no longer exists”. A widening rift has emerged between Europe and the United States. Rubio gave a conciliatory address, emphasising that the United States and Europe “belong together”, but he also echoed Merz’s conclusion that “the old world is gone”. The conference ultimately laid bare a central paradox. Transatlantic tensions are real, structural, and unlikely to dissipate. Yet disengagement is not an option. In a world defined by fragmentation, rivalry, and competing visions of order, continued engagement may be strained, but it remains indispensable.

US: Fall in short-dated Treasury yields needs to be quicker

Graham Turner points out that US core inflation is trending just above 2.0%. The ex-food, energy & shelter CPI was up 2.20% in the 6-months to January, annualised. Meanwhile unemployment is falling, despite a rise in the labour market participation rate to new highs. The rapid adoption of AI suggests that the growth-inflation trade-off for the economy should improve. Therefore, the noninflationary growth path of the US economy is notching higher. Graham comments that how the Treasury market views the jobs and inflation data has been interesting. The two-year Treasury yield fell to 3.40% on Friday, the lowest since October 27th, 2022. This is pulling longer-dated yields down: break-even inflation rates are falling across the curve. The Treasury market has rightly concluded that stronger labour market data does not preclude lower interest rates when AI shifts the NAIRU lower. However, to prevent stock markets falling, the decline in short-dated Treasury yields is going to need to be quicker.

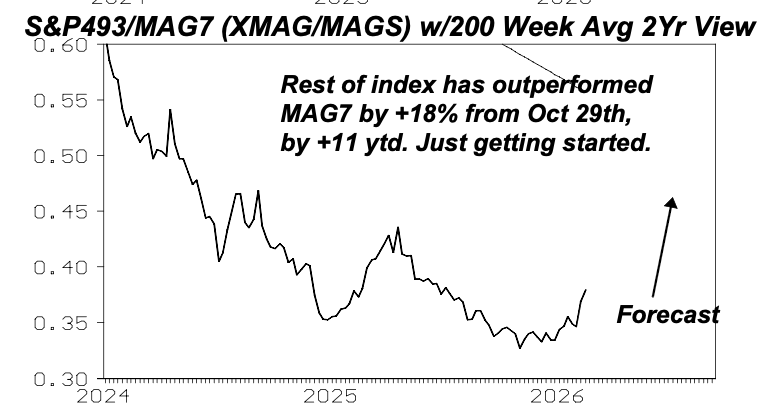

TBonds join the risk-off rotation

Michael Belkin’s model closed most short bond positions last week as he adds US and global sovereign bonds as new long positions, at what is now a major inflection point for US and global long-term interest rates. Michael’s hunch is that the recent risk-off move in sector rotation is now moving from equities into fixed income, with the MAG7 stocks in massive liquidation and the S&P500 unchanged on the year. Meanwhile, energy, consumer staples and utilities are all up, signalling a massive risk-off move in sector rotation. Of course, that’s the last thing Wall Street expects; the same sell-side strategists who said the software stock selloff was overdone never said to sell in the first place! Michael’s forecast for the Nasdaq points down big, both intermediate- and long-term. He maintains his bullish forecast for the value/growth and S&P493/MAG7 spreads, already up +13%ytd and +11%ytd (see chart).

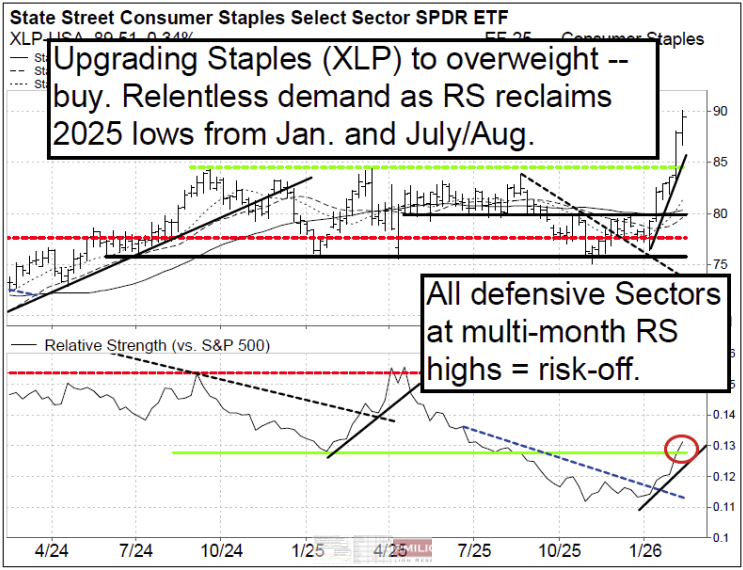

US: A staple diet

The Vermilion team will maintain their near-term bullish outlook on the S&P500 and Russell2000 as long as crucial support levels of 6780-6824 on SPX and $255-$257 on IWM continue to hold, although they do expect a period of consolidation/pullback. The team also maintain their bullish intermediate-term outlook, and recommend buying pullbacks, as long as market dynamics remain constructive and the SPX is above 6480-6520 and IWM is above $245. Staples (XLP) are at 7+month RS highs and the team are upgrading Staples to overweight (see chart).

The best FX trade for 2026

In Stephen Jen’s view, USDJPY may be the best (i.e., with the highest Sharpe ratio) FX trade for 2026. With the dominant election victory, Stephen points out that the LDP has enough popular support for PM Takaichi to go through with her 3%-GDP worth of fiscal stimulus. With inflation still above the BOJ’s target (headline CPI is down to 2.1%, but core-core is still hovering around 3.0%), this prospective fiscal stimulus will likely be met with accelerated or earlier rate hikes by the BOJ. Stephen says that the US Fed and the BOJ will continue to converge in 2026, with the former cutting while the latter is hiking. Stephen argues that the US dollar itself is in a structural descent, and the particular policy mix in Japan should lead to a stronger JPY. He still views 125 as a very reasonable target for USDJPY this year.

Emerging Markets

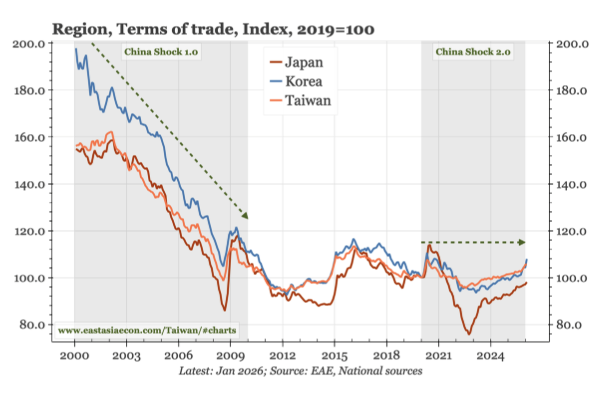

Asia and the China Shock 2.0

There’s a lot of talk about China Shock 2.0, where the flood of capital goods exports from China will be deflationary for the rest of the world. However, for the rest of Asia, Paul Cavey argues that the impact will be considerably less than that in the 2000s. That era saw a sharp deterioration in the terms of trade of nations across Asia, brought on by the huge demand for commodities from China which had offset the fall in electronics prices that occurred in the same period. By contrast, the last five years has seen export prices contributing positively to the terms of trade for the first time since at least the 1990s, helping offset the impact of the rise in import prices. The more stable terms of trade should provide support to Asian currencies. Asia is certainly exposed to China’s move up the value-added chain, with Korea looking particularly vulnerable, but the impact is likely to stop there.

Argentina: A positive outlook

Niall Ferguson has argued that Argentina needs to show more and say less on reserve accumulation if it hopes to roll over its dollar debt maturities. The new year began with the central bank accumulating reserves at an impressive pace and Argentina’s country risk compressing sharply to ~500 basis points. Niall believes Economy Minister Caputo could soon be in a position to issue a bond in international markets, as Ecuador recently did at a comparable spread. Moreover, Argentina and the United States have concluded a trade and investment agreement, underscoring President Javier Milei’s steadfast political alignment with President Donald Trump. Niall remains optimistic about the Milei administration’s political and macro durability, and reforms are passing in Congress. However, he expects the FX outlook to continue dampening growth potential, forecasting ~3% growth this year along with a consolidated fiscal surplus.

Bangladesh: Reform agenda focuses on deregulation and costs

Asif Khan observes that 49 individuals, primarily newly elected Members of Parliament from the Bangladesh Nationalist Party and its allied parties, were sworn in on February 17th as ministers and state ministers in the new cabinet led by BNP Chairman and Prime Minister Tarique Rahman. In policy-related remarks, newly appointed Finance and Planning Minister Amir Khosru Mahmud Chowdhury outlined a reform agenda focused on deregulation and reducing the cost of doing business. Meanwhile, the newly appointed Commerce Minister indicated that the government will seek a deferment of Bangladesh’s graduation from the Least Developed Country (LDC) category by at least three years.

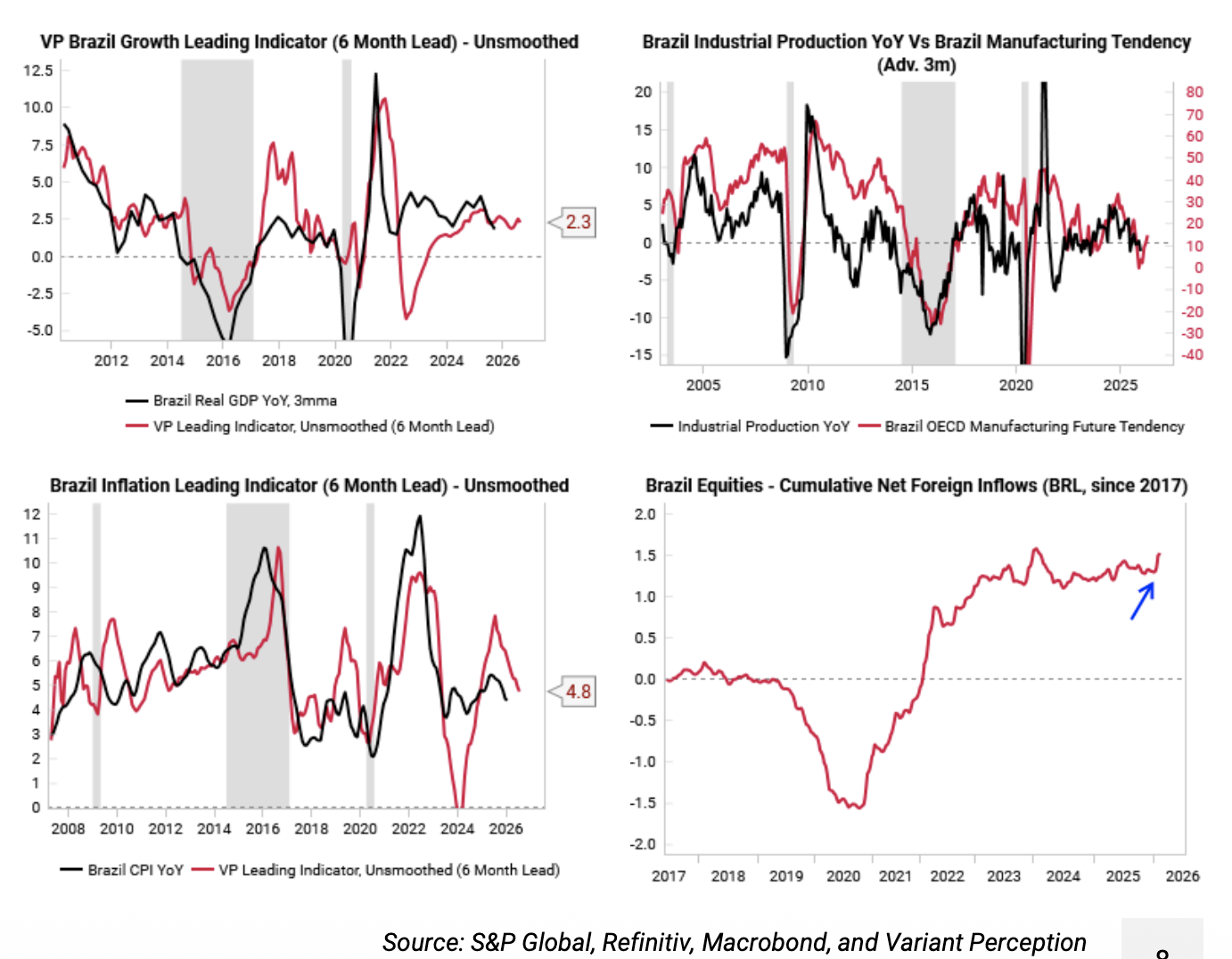

Brazil: Bullish case remains intact

Variant Perception’s leading indicator for Brazilian growth has stayed resilient despite the lagged effects of the recent tightening cycle (top left chart). Some indicators in rate-sensitive sectors like manufacturing are showing an upturn in expectations, which tends to lead growth in industrial production (top right chart). Inflation has continued to fall, in line with the team’s leading indicator (bottom left chart). This should give the central bank plenty of scope to ease the Selic rate from very high levels and shift monetary policy from a headwind to a tailwind. The macro setup still looks favourable for continued gains in bond and equity prices. There has been an uptick in net foreign inflows as Brazilian equities have rallied (bottom right chart). But this is minor compared to the major inflows seen from 2021 to 2022. And as interest rates fall, domestic investors will be encouraged to shift from cash/bonds to equities, another tailwind as the cycle progresses.

Not made in India

According to Jonathan Anderson, India has little chance of catapulting itself into middle-income levels without seriously raising its game on exports, in particular light manufacturing exports which would maximise employment, income and dollar earnings gains. Jonathan points out that there are no examples of sustained rapid services-led growth in any but the smallest emerging market economies – and certainly not in a case like India with a population of 1.4 billion. In practice, the only proven model that leverages on underlying comparative advantage for the populous low-income world is labour-intensive manufacturing. And until India jumps on the bandwagon, it will not be a breakout. This doesn't stop Jonathan from investing in India's domestic growth cycle on a cyclical basis, but it does very much inform how he sees the country's structural prospects.

India: Sounds nifty

The iShares MSCI India ETF (INDA US, USD52.89) has been ranging for 7.5 months following an initial 18% rally from the Mar 2025 low. Chris Roberts views the INDA’s Mar 2025 low as an important cyclical trough. At USD47.60, the ETF had retraced an exact 50% of the 2023-24 cyclical bull market. Note that RSI has been ranging between Low Neutral 40 and High Neutral 60, typical of a rangebound market. Chris remains 60% long the NSE Nifty (last 25,471) from 24,627.69 but will only add to Indian exposure if the INDA US breaks above the Jun high of 56.01.

Venezuela: The fiscal receivership trap

Over a month after Maduro was removed, Venezuela is operating under a modern form of US fiscal receivership. Niall Ferguson remarks that history doesn’t point to a positive outlook, with previous examples rarely increasing revenues or creating long-lasting institutional change. Iraq showed that going all out with military occupation and recovered oil production, deep bond haircuts can still materialise. Genuine democratic transitions, like those in Spain or Paraguay, can take decades to materialise. Niall sees the most likely outcome for Venezuela being a modified Chavismo with closer ties to Washington. This is not the “different Venezuela” Secretary Rubio envisions but rather a rebranded authoritarianism, at least in the short term. Despite the market rally, Niall sees Venezuelan and PDVSA bonds as high-risk.

Commodities

The disconnect between energy and metals

Kathleen Kelley notes that much of the recent to-ing and fro-ing in commodity and other markets has been driven by AI headlines and/or disruption signals, and by the implications each will have on global capex. AI needs reliable power supplies, robust power grids, data centres for computing, and the manpower and stuff to build it all. Metals have behaved as if a global manufacturing cycle were underway. Ruining that conclusion, energies have not. There is now a disconnect between stable manufacturing, surging copper (aka metals), and lacklustre energy. Which category is correct? Or will everything meet in the middle? Kathleen says that identifying which markets are likely to be in surplus or deficit is a good place to start the analysis. She expects surpluses in oil, gas, iron ore, zinc, and nickel. Grains, too. Aluminium, copper, and palladium should be close to balanced, barring any surprises. Silver and platinum will be in deficit.

Is the gold rally over, or is it the start of a new bull-phase?

Is the gold rally over, or is it the start of a new bull-phase? Metals Focus’ industry-leading Gold Five-Year Forecasting Quarterly report was released this week, evaluating the evolving dynamics influencing gold’s outlook. Then report examines what could happen to gold under a base case, bullish and bearish scenario, with detailed commentary and analysis. The 60-page report includes a forecast out to 2030; a dive into mine supply and hedging; a look into the current state of recycling; an analysis of jewellery consumption and industrial demand; and an investment and price outlook. Please contact us to find out more.

Silver volatility explained: Inventories, deliveries and price risk

In this presentation, Jeffrey Christian of CPM Group reviews current conditions in gold and silver markets, beginning with the latest US inflation data and what it implies for interest rate expectations. He explains the January CPI and PCE readings, why inflation has remained structurally higher than in the past, and discusses how this environment continues to influence investor behaviour toward gold and silver. Jeff then focuses on silver market realities, addressing widespread misinformation surrounding Comex inventories, deliveries, and so-called “shortages.” He explains how Comex silver actually functions, including good delivery standards, the difference between eligible and registered inventories, and why metal moves in and out of depositories. He also provides historical context, showing how large contract rolls and speculative positioning can drive sharp price moves without implying market failure or physical scarcity.

Click here to watch.

China’s commodities: Shock and awe

James Burdass observes that China’s 15th Five-Year Plan is moving the goalposts from raw GDP growth to high-quality development and security. Explicit targets aim for solar capacity to surpass coal capacity in 2026, cementing structural demand for silver and lithium. Furthermore, James expects Beijing to explicitly formalise national security reserves for critical minerals. In this new era, copper and lithium stockpiles are likely to be treated with the same strategic importance as oil reserves, potentially tightening market balances faster than fundamental supply and demand would suggest. James says this is why the bears were wrong. Heading into 2026, the consensus trade was likely "Short China Commodities" based on the property collapse. However, the RMB 4 trillion grid budget is not just a "replacement" for lost property demand; for specific metals like aluminium and copper, it acts as a growth accelerator. China's property bubble has burst, yet electrification is not dead. This is the critical takeaway for the year ahead.