Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

A compelling growth story

AIR highlights Spain as the Eurozone’s standout growth opportunity, further supported by US immigration tightening redirecting talent and labour. The country is benefitting from its strong position in the EU’s €750bn Next Generation EU program, minimal exposure to US tariffs and insulation from Chinese industrial competition. A rapid transition to renewables has driven a 40% decline in wholesale electricity prices over five years, while lower structural taxes and spending continue to support competitiveness. Preferred sector calls include Infrastructure (Acciona, Ferrovial, Sacyr) with robust project pipelines supported by public and private investment; Banking & Insurance (CaixaBank) benefitting from SME exposure and high household savings rates; Real Estate (Merlin, Metrovacesa) poised for catch-up gains vs. other European countries amid supply constraints; and Defence, where Indra Sistemas is well positioned for M&A.

DCC (DCC LN) UK

Following publication of the company's FY25 annual report, Iron Blue increases their DCC rating +3 pts to 27/60 (newly top quartile / fertile grounds for shorting). Key changes vs. FY24: 1) Higher one-off costs: FY25 stripped out restructuring expense increased to 7% of PBT adj, highest in 7 years. DCC also stripped out from headline earnings £74m goodwill impairment. 2) Took £17m profits on disposal of PPE inside underlying profits in FY25, the highest figure in the past decade. 3) P&L expense for inventories write-downs dropped to a decade-low of £5m. 4) DCC continued its strategy of promoting top management from within, with internal promotions to the CFO and newly created COO roles. 5) In its principal risks assessment, DCC highlighted Y/Y risk increases concerning the DCC Technology strategic review and also the impact on its operations from higher tariffs.

Siemens Energy (ENR GR) Germany

A “backdoor” AI infrastructure play amid growing power bottlenecks from new data centre construction. As data centres cannot rely on intermittent renewables, natural gas turbines are seen as the only viable near-term solution. The market is extremely tight, with projected demand of 80-100GW vs. supply of only ~70GW and consensus likely underestimating both pricing and volume potential. ENR’s Gas business is positioned to deliver 20%+ long-term margins, while its Grid Technologies division should benefit from global electrification and grid modernisation, with revenue expected to exceed €20bn by 2030. Shares could double over the next 3 years, driven by earnings beats and a profit inflection in the Wind segment. The upcoming November Analyst Day is viewed as a major catalyst.

Tenaris (TEN IM) Italy

Alejandro Acosta highlights a structural shift in global energy markets, noting that oil and gas exploration has not kept up with production since the 2014-2016 crisis, but is now rebounding as major producers resume investment. Slower-than-expected EV adoption and renewed automaker focus on internal combustion engines support sustained demand, while rising US natural gas consumption - driven by data centre power needs - adds further tailwinds. Alejandro argues these dynamics are not yet priced into TEN, whose improving financials and active share buybacks underscore management confidence. Although potential tariffs pose risks, TEN’s extensive US manufacturing base provides a competitive edge over other foreign suppliers.

Nexperia dispute highlights Europe’s semiconductor dilemma

The escalating dispute between the Dutch government, China and chipmaker Nexperia has become a flashpoint in the global semiconductor power struggle. With parent company Wingtech already on a US trade blacklist and facing tighter restrictions, Nexperia’s plan to separate its Chinese and European operations is now in jeopardy. The export ban poses an immediate risk to Europe’s industrial supply chain, especially in the automotive sector. Finding and certifying alternative suppliers could take months, echoing the chip shortages of 2021/22. Strategically, it spotlights the West’s push for technological sovereignty and the Netherlands’ pivotal role in the China–West tech decoupling. Several (Dutch) companies could be affected including ASML, NXP, Philips and ASM International.

North America

What’s really driving alpha

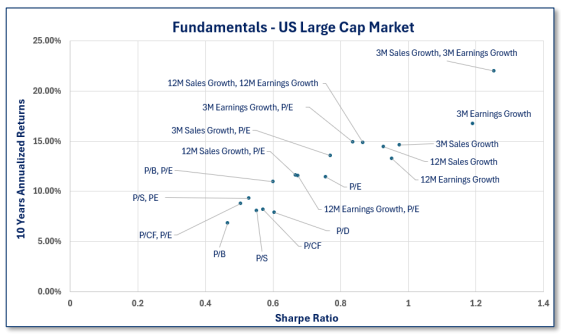

Trendrating’s latest analysis provides data-driven insights into the fundamental parameters that have historically generated the most alpha across US sectors. Their report identifies and ranks the combinations of metrics most rewarded by the market, offering investors a factual framework for factor-based decision-making. In US Large Caps, the combination of Highest 3-Month Sales Growth and Highest 3-Month Earnings Growth has delivered the strongest returns over both 3- and 10-year periods, while Lowest Price/Book and Lowest Price/Dividend generated the weakest returns. Their report also includes results for specific sectors including Consumer Discretionary, Financials, Industrials and Technology - click here to access.

Access to proprietary short-availability data

As many quantitative researchers know, reliable historical short-availability data, especially intra-day, is notoriously difficult to obtain. Recognising this gap and leveraging the accessibility of real-time market feeds, Capital Systems began recording real-time short-availability data for all US equities in Aug 23 and for all USDC-denominated cryptocurrencies on the Binance exchange in Jun 24. The data is of particular use in two areas: 1) Reducing assumption bias in short-selling strategies, especially for hard-to-borrow securities. 2) Alpha capture. Why would Capital Systems share such an edge? The firm trades only a small fraction of the markets it monitors, allowing them to offer this unique dataset on a limited basis to select clients.

Hesham Shaaban initiates a new tactical long in RBLX, arguing that the recent sell-off following the M Science report has created a “coiled spring” setup ahead of 3Q25 results. His analysis indicates that Concurrent Users have accelerated each month through Q3 and into Oct, contradicting perceptions of a slowdown. He believes the M Science data may not fully capture RBLX’s expanding user base, underestimating bookings growth. If platform activity trends hold, even modest monetisation could yield a double-digit bookings beat for Q3 and stronger Q4 guidance. With the shares up >100% YTD, Hesham expects short exposure to increase into the print, meaning any upside surprise could trigger a sharp rebound if results confirm his thesis.

Antedata’s coding activity data points to rising freelance projects related to ETSY, highlighting its strong positioning as an AI beneficiary. Freelancers typically help sellers set up storefronts, optimise search visibility, automate listings and create professional branding. ETSY’s vast, unstructured dataset and its dual role as marketplace and discovery hub make it a prime use case for AI. The company already employs AI in search, personalisation and ad targeting, driving better conversion and marketing efficiency. With operating leverage and discretionary R&D / marketing spend, even modest efficiency gains could meaningfully boost profitability - supporting AnteData’s view that ETSY’s current valuation can be justified by earnings growth potential.

Brian McGough reiterates his bearish view on FND despite the stock’s ~50% drop since his Apr 24 short call (vs. the S&P +33%). Brian is updating his analysis using his M.A.P.S. (Market Area Performance Study) framework, which tracks store performance by opening cohort. His latest findings suggest that stores opened in 2024 & 2025 are performing even worse than earlier cohorts, reinforcing that FND’s weak comps are structural, not cyclical. New units also show rising market overlap with the likes of Home Depot and Lowe's. While FND is often seen as a housing-recovery play, Brian expects another ~30% downside as earnings, growth guidance and unit expansion continue to disappoint.

Capital Markets at Risk: Jefferies echoing Bear Stearns

Charles Peabody believes we are in the mature phase of the capital markets cycle, with revenues likely topping out in 2026, while stocks are expected to turn lower well before then. He recommends selling Morgan Stanley and Goldman Sachs on near-term strength. Credit and liquidity stresses are emerging following the automotive credit, Tricolor and First Brands developments, while syndicated loan offerings are being pulled. He sees echoes of Bear Stearns at JEF, noting that MS and BlackRock have ended relations with Bonita Point, the JEF subsidiary housing First Brands receivables, just as this rapidly growing broker reached top-tier status. Sell Capital Markets, Buy NII - he favours Citi, M&T, Citizens Financial and UBS.

Drug pricing demos as Pharma scrambles

President Trump's drug pricing plans are progressing from the conceptual to a more serious phase. As CMS prepares to issue its most favored nation (MFN) demonstrations and pharma companies attempt to cut pricing and manufacturing deals with the administration, Capital Alpha Partners' Rob Smith and Kim Monk caught up with a former director of the Center for Medicare and Medicaid Innovation (CMMI) on the administration’s advancing Medicare drug pricing agenda. The team sees at least one demo being proposed by the end of the year and implemented by late 2026, though legal challenges remain significant. Physician-administered Part B drugs are the most likely target for a drug model.

Could the stock soar over 100%? KCR argues that CSCO isn’t just cheap vs. AI peers - it is cheap relative to the broader market, trading at roughly the same multiple as Kimberly-Clark despite far stronger growth. Networking product orders have risen 10% Y/Y for 4 consecutive quarters, suggesting investor concerns about a slowdown are unwarranted. Meanwhile, the company’s rapidly growing exposure to AI infrastructure products and shift towards subscription-based revenue both support multiple expansion. CSCO trades at one-third of Arista Networks’ P/E multiple and one-quarter of its EV-to-revenue ratio - even a modest narrowing of the valuation gap would translate into substantial gains for CSCO shares. Finally, a ~5% FCF yield is far too high for a company of CSCO’s quality.

Craig Huber raises his 12-month price target to $2,300 (from $2,100), citing stronger long-term earnings visibility under the company’s new 2026 US mortgage pricing models. The existing Per-Score Model will double to $10 per score, while the new Performance Model combines a $4.95 per score fee with a $33 funding fee on closed loans - boosting mortgage origination revenue by ~130%. Craig lifts his FY26/27 revenue forecasts to $2.54bn / $3.12bn (up 27.5% / 22.7% vs. prior) and expects EBITDA margins of 62.2% and 66.6%, respectively. His adjusted EPS estimates for FY26/27 increase to $43.85 / $60.00 (vs. previous estimates of $36.25 / $45.35). Craig sees limited competitive threat from VantageScore, arguing that FICO’s market dominance and pricing power remains intact.

BTN continues to see several areas where OSIS's results may be unsustainable. The company has reduced its bad debt reserve to just 2% of receivables (vs. a 5-7% historical range), adding ~11 cents to Q4 EPS (OSIS only beat Street estimates by 5 cents). The current reserve for bad debts is at least 200 bps too low; if OSIS had to raise it by 100 bps, it would be a 39-cent headwind for EPS. DSOs have surged to 151 days (historically ~90), making Q4's revenue increase more suspect and the $372m forecast for 1Q26 tougher to reach. Warranty expense was cut again (added 3.7 cents to EPS), while OSIS continues to let its PP&E age and is using fully depreciated equipment - saving 29 cents in EPS last year. Finally, FCF remains weak (negative in 5 of the last 8 quarters).

Japan

Japanese Banks: Taking profits, staying selective

Victor Galliano has lightened positions in Japanese banks, retaining those with larger cross-holdings relative to market cap, which he expects to benefit under an easier-for-longer monetary policy. He argues that managements’ commitment to realise cross-holding value through disposals should be a key near-term driver of share performance. Despite potential delays to further rate hikes, lending rates and net interest margins have continued to rise since the end of NIRP, supported by low delinquency levels. Combined with attractive valuations, these trends should underpin higher medium-term multiples. Among large caps, he keeps Resona and Shizuoka as Buys (downgrading Mizuho to Neutral) and among mid-caps, maintains Buys on Iyogin, Hokuhoku and Hachijuni, while downgrading Hirogin to Neutral.

Asymmetric Advisors has turned bearish on Fujikura, having recently closed their long position after what they call a “crazy rerating”. They were “beating the drum” when the stock traded around 15x earnings, but it now sits near 30x FY27, a level they see as unjustified for what remains a largely commodity cable supplier. While earnings surged in recent years on strong demand for its Spider Web Ribbon fibre cables used in AI data centres, capacity constraints and intensifying competition from Corning to Ciena to Furukawa and Sumitomo Electric are likely to cap further upside. Asymmetric now views Fujikura as a suitable short hedge against more attractive technology names in their portfolio.

TD trades at levels implying investors value its operating business at near zero, reflecting deep scepticism about growth and profitability amid dependence on Samsung and exposure to memory price volatility. While these risks are real, Yuka Marosek argues they are already priced in and TD’s close ties to Samsung Japan and Toyota Tsusho provide stability and long-term relevance. Expansion into automotive and server / storage markets, supported by rising AI-driven demand for memory, offers potential for improved margins and diversification. Toyota Tsusho owns 50.1% of TD and Yuka wonders if Tsusho might eventually absorb the entire company - if Samsung allows it.

Emerging Markets

Unpacking China’s growing pet market

Marie Boyé examines China’s rapidly expanding pet industry, projected to reach $114bn in 2025, or 10% of global market share - tripling in size since 2020. Growth is led by pet food, followed by veterinary services and accessories, with emerging segments in pet tech, premium nutrition and luxury care. Cats now outnumber dogs, driven by urban lifestyles and regulatory shifts. Despite inflationary pressures, spending on pet essentials remains resilient, underscoring the sector’s defensive nature. Competition is fierce between multinationals and digital-savvy domestic brands leveraging influencer marketing and e-commerce dominance. Changing attitudes towards family and younger consumers’ growing attachment to pets are expected to drive continued spending, innovation and investment across China’s pet sector.

AI insights from China’s Tech giants

Westlake’s latest reports draw on discussions with AI experts from Tencent, ByteDance and Alibaba, offering fresh perspectives on China’s evolving GPU and ASIC landscape. Tencent’s AI Product Manager detailed the rationale behind increased domestic GPU procurement this year and outlined potential market shifts if B30A and H20 export policies are relaxed. ByteDance’s AI Solution Architect described surging AI compute and token usage and the rapid expansion of AI investments and custom chip development. Alibaba’s AI Project Manager discussed GPU procurement trends, progress in its T-Head ASIC programme and ongoing Qwen model development, including on-device use-cases.

Macro Research

Developed Markets

Global bulls

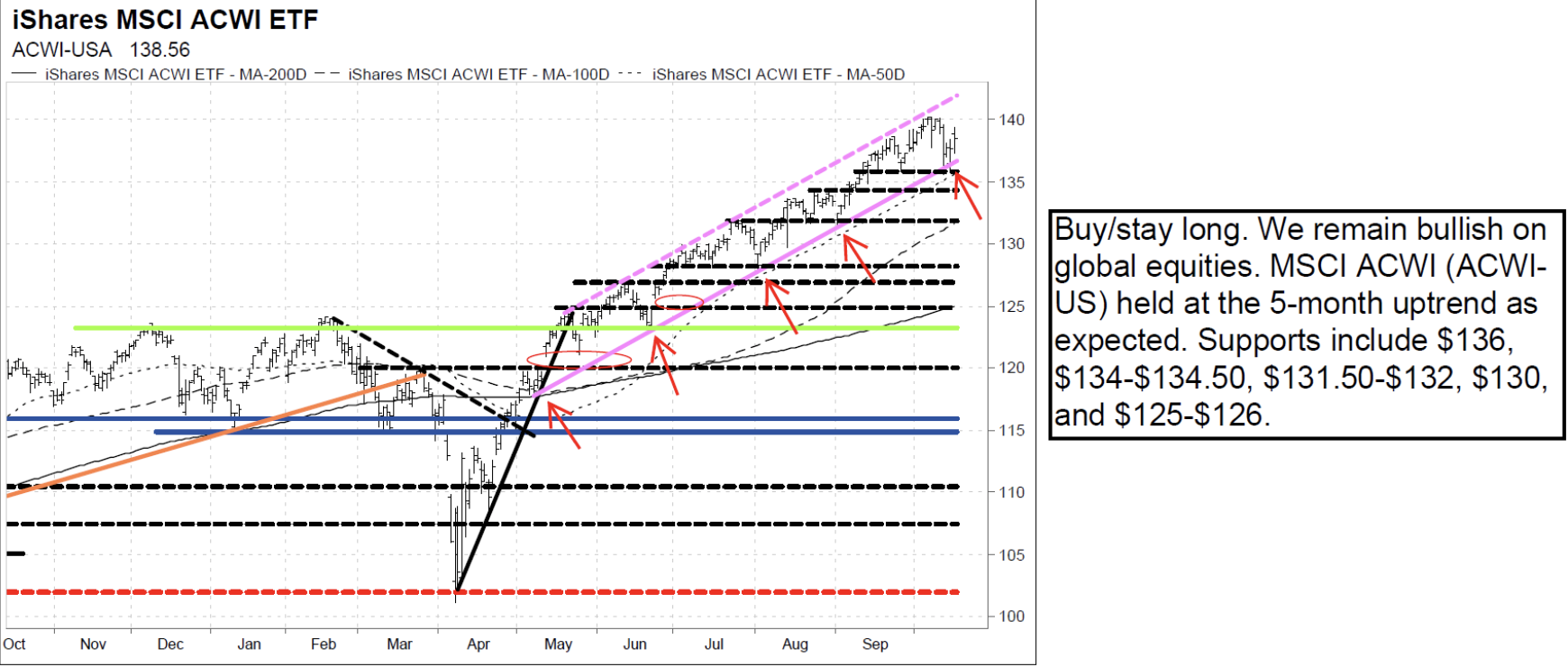

The Vermilion team remain near-term bullish since their April report, with their intermediate-term outlook also remaining bullish. They will maintain this view for as long as market dynamics remain healthy and the SPX and ACWI-US are above 6028-6059 and $125-$126. Their bullish near-term outlook will remain in place as long as the 5+ month uptrend continues on ACWI-US. So far, the latest pullback is testing the uptrend -- buy/stay long. Short-term supports to watch on ACWI-US include the 5+ month uptrend (currently at $136), $134-$134.50, $131.50-$132, $130, $128, and $125-$126. Expect more upside into year-end and early 2026. Remain overweight Taiwan, China, Korea and the US, and bullish on EM particularly MSCI EM Tech and Materials.

France: Survival

French Prime Minister Sébastien Lecornu survived two motions of censure on Thursday in the French National Assembly. The oppositional far-right Rassemblement National (RN) and the far-left France Insoumise (FI) were 18 votes short of toppling Lecornu. Parliament will now negotiate the 2026 budget, which it will vote on in December, and Macron can sigh a breath of relief. These negotiations could still fall apart, with the centre-left Parti Socialiste (PS) likely to threaten that it will walk away from a budget deal. That said, Niall Ferguson’s base case is that the various centrist parties that backed Lecornu today will reach a budgetary compromise resulting in a deficit of around 5% of GDP. The rise of French sovereign bond yields is over… for now.

Eurozone: Consensus too optimistic on disinflation

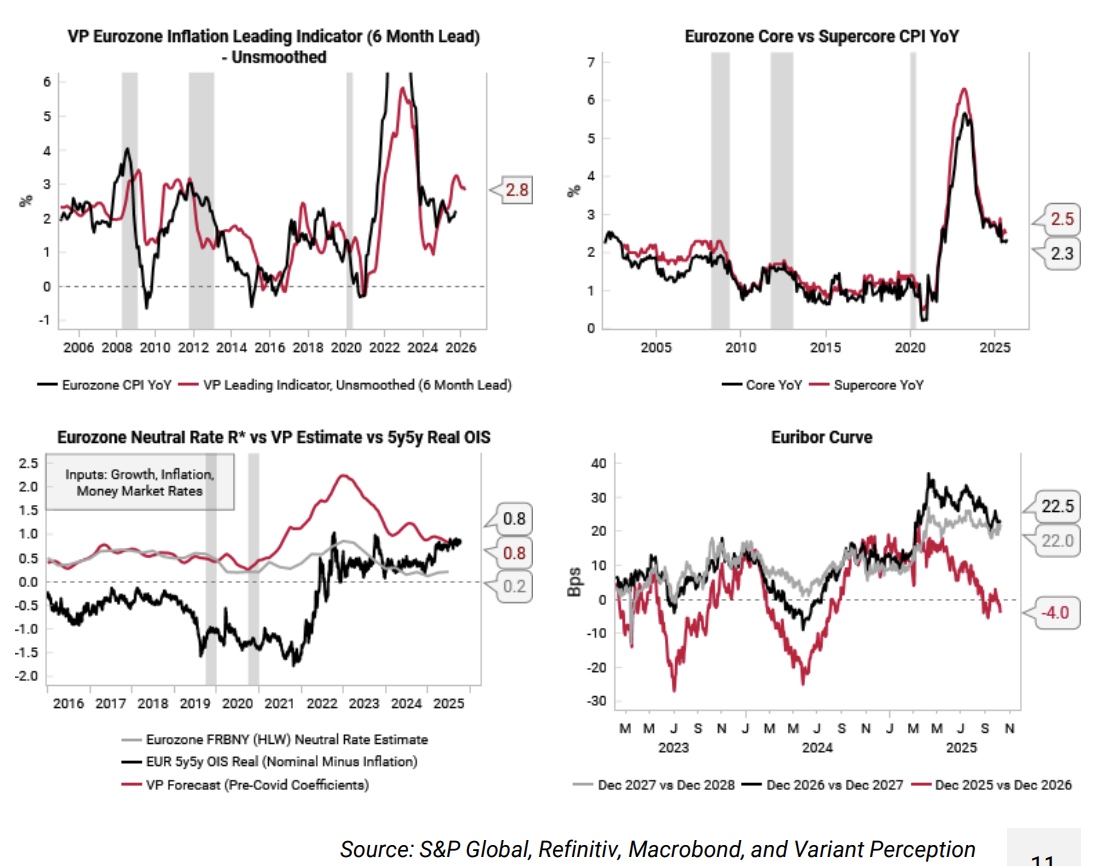

Consensus expectations see 2026 eurozone headline CPI at 1.8% and core CPI at 2%. The Variant Perception team suspects that inflation risks are tilted to the upside from here given the recovery in their eurozone growth leading indicators and the ECB rate cuts so far this year. Their main inflation leading indicator is rolling over from a high level, but the point estimate remains elevated at 2.8% (top left chart). Core and supercore CPI have also been slower to fall, still at 2.3 to 2.5% YoY (top right). The team put the real neutral rate (R*) for the eurozone at 0.8%, which is also where the 5y5y EUR real OIS is trading (bottom left). With headline CPI at 2%, there is good chance that ECB policy is already stimulatory, potentially creating inflation upside in 2026. The team take profits on their SOFR vs Euribor Dec 25/26 convergence trade established last month.

Make European Equities Great Again

Earlier in the year, Callum Thomas told investors that he saw several factors lining up for MEEGA (Make European Equities Great Again); still cheap valuations, lingering excess pessimism, monetary tailwinds, political drift to the business-friendly governments, fiscal stimulus, and the prospect of global growth reacceleration into 2026. Callum’s chart this week shows a breakout to new all-time highs, which he remarks only took 25 years! Callum has recently documented several other big breakouts currently underway, including DM ex-US equities, EM equal-weighted index and China tech stocks, and he says the European one has good company. When there’s a clean, clear breakout like this after such a prolonged period of base-building, you better pay attention.

US: It’s not time to be bearish

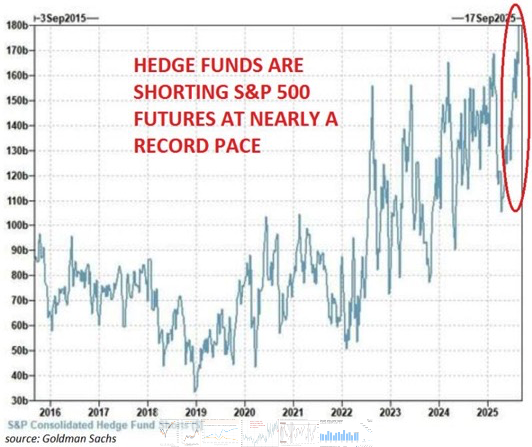

Forget the argument that this is a new dot.com bubble, argues Gaius King. The top 10 countries in the S&P500 are the ones delivering real growth whilst the remaining 490 and the broader economy are remarkably weak. Ironically, fund managers shorting this market is actually a contrarian indicator. There is little or no seasonality this year, and recall that asset and fund managers remain seriously under invested since the Tariff Tantrum. Actively shorting this market (see chart) in such a low volatility environment is hopium that they will match the index if the market falls. Gaius expects an additional year of market craziness ahead of us, peaking in Q3/2026, and draws remarkable parallels to the 1970s. Investors should buy momentum stocks. If you want a market canary, look at AI’s forward order book.

US: A bubble in bubble fears

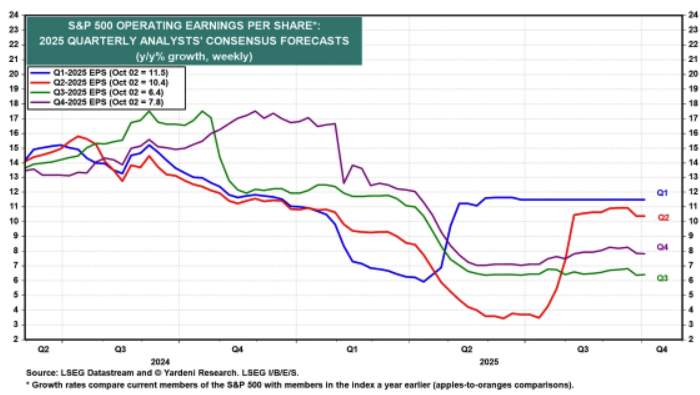

Ed Yardeni is raising his S&P500 year-end back to 7,000. He reckons that the V-shaped stock market rebound since April is discounting the economy’s resilience, which reduces the odds of a recession. Right now, we’re experiencing a slow-motion melt up, a result of the Fed rate cut in September and expectations of an additional one or two cuts before 2026 arrives. Ed sees the odds for a melt up at 30% and reduces the base-case for a sustainable bull market (without correction) at 50%. When the tech bubble emerged in the 90s there wasn’t as much chatter about the bubble, unlike this time; from a contrarian perspective, Ed sees this as comforting. He is counting on another better-than-expected quarter earnings season for Q3 to support the stock market’s rally to record highs. He expects a 10.7% increase compared to the 6.4% consensus (see chart).

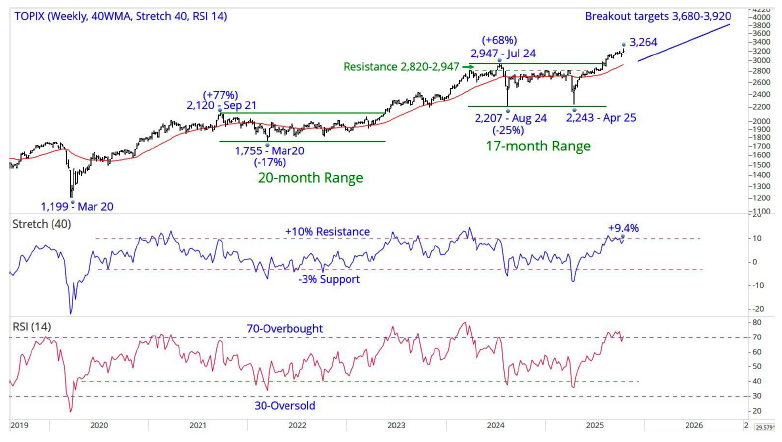

Japan: Hot Topix

The Topix’s (3,198) breakout from the 2,207–2,947, 17-month range targets an advance to 3,680–3,920. The break above the 1,700–1,825, 28-year ceiling in 2021 targets a minimum of 3,400–3,650+. Weekly indicators are either overbought, or close to overbought, but have been higher during this bull market. Chris Roberts remains 50% long from 2,857, with the stop for all longs moving up to a daily close below 2,780 from 2,475. His preferred target is now 3,680+, and he is looking to add to longs. He will add 5% long at 3,178, 5% at 3,168 and 5% at 3,158. If fully executed, he will move to 65% long.

Emerging Markets

Chile: Policy rate should stabilise at ~4.5%

Igal Magendzo points out that the market — which in recent weeks had been converging toward a scenario with a policy rate somewhat higher than the Central Bank’s baseline projection — has slightly adjusted the timing of the final cuts expected in this cycle. Specifically, the highest probability of a rate cut shifted from next January to this December, in line with the medians of both the Economic Expectations Survey and the Financial Operators Survey, and consistent with Igal’s baseline scenario. Regarding the final cut, although the probability of a 25-basis-point move remains only around 50%, the market brought its expectation forward from October to June (compared with last week). Igal continues to maintain his view that the policy rate is close to neutral and should stabilise around 4.5%.

China: Xi-Trump summit still possible despite tariff threats

William Hess comments that the tumultuous week for US-China highlights the latter’s position: China is happy to drag out negotiations for as long as possible. The backdrop to successive negotiations is a situation of fundamental distrust and geopolitical realignment that Beijing is in no hurry to slow down. These developments set the stage for markets to blow off some steam after recent rallies appear overextended. In terms of activity levels, William’s proprietary indicator for China is showing activity that is moderating but in line with cyclical expectations and far from collapsing. This is consistent with his expectations for Q3 GDP growth that is a tick above the consensus of 4.7%. More important for market expectations will be the Fourth Plenum next week, which should be Beijing’s attempt to improve the macro narrative with structural reform plans.

China: From trade war to tech war

Don Ma has distilled the latest US-China escalations into actionable insights. The shift from trade to tech war amplifies trends like self-reliance and friend-shoring, reinforcing long-term investment themes rather than disrupting them. In the short term, rising risks in market sentiment, supply chains, countermeasures, and geopolitics could trigger a 10%+ adjustment, eroding momentum strategies. Rare earth disruptions pose real threats to global tech production. Over the medium-term, expect supply chain redundancy builds, accelerated Chinese outbound manufacturing, and stronger domestic substitution. Trump's negotiation leverage may weaken due to legislative roots, prolonging tensions. Over a longer horizon, systemic distrust will entrench friend-shore/near-shore economies, benefiting ASEAN hubs and amplifying US’s structural inflation vs China’s deflation. Hedge with long gold/short crude. Compared to prior rounds, the recent conflicts are more strategic and entrenched, with lower compromise odds mid-term but enhanced supply chain rebuilding long-term.

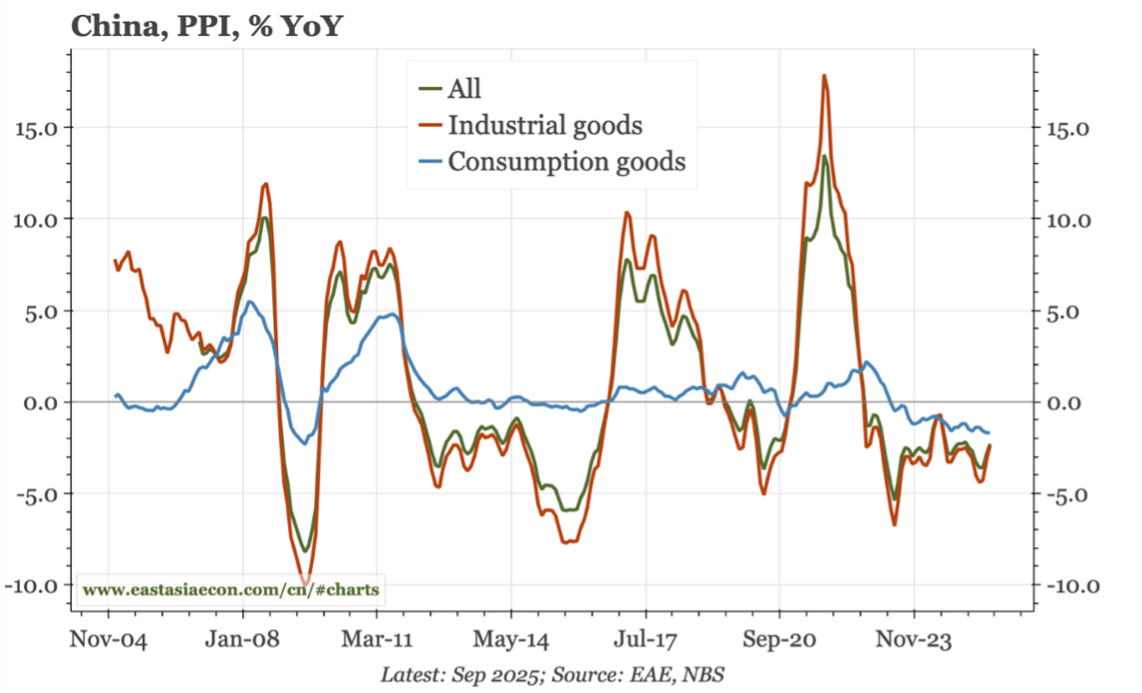

China: A fragile improvement in PPI

For the first time in more than a year, in level terms, the producer price index (PPI) has stopped falling; however, in year-on-year terms it was down 2.3%y-o-y (versus -2.9% y-o-y in August). That is an improvement, but one that looks fragile. Prices in auto manufacturing – one of the sectors targeted by the anti-involution drive – are falling more quickly than ever, and the "consumption" sector of the PPI in general shows no turnaround. Building material prices continue to be dragged down by the problems in the property market. The stabilisation in PPI is being driven by prices for "industrial" products, namely mining and energy. The short-term leads don't suggest much change in PPI in the next couple of months. But there is some upside risk coming from the YoY rise in global commodity prices (in CNY terms). Paul Cavey remarks that this would be more powerful for China if the construction cycle really finds a floor, allowing building materials prices to do the same.

Gaza: Ceasefire, for now, but tensions remain elsewhere

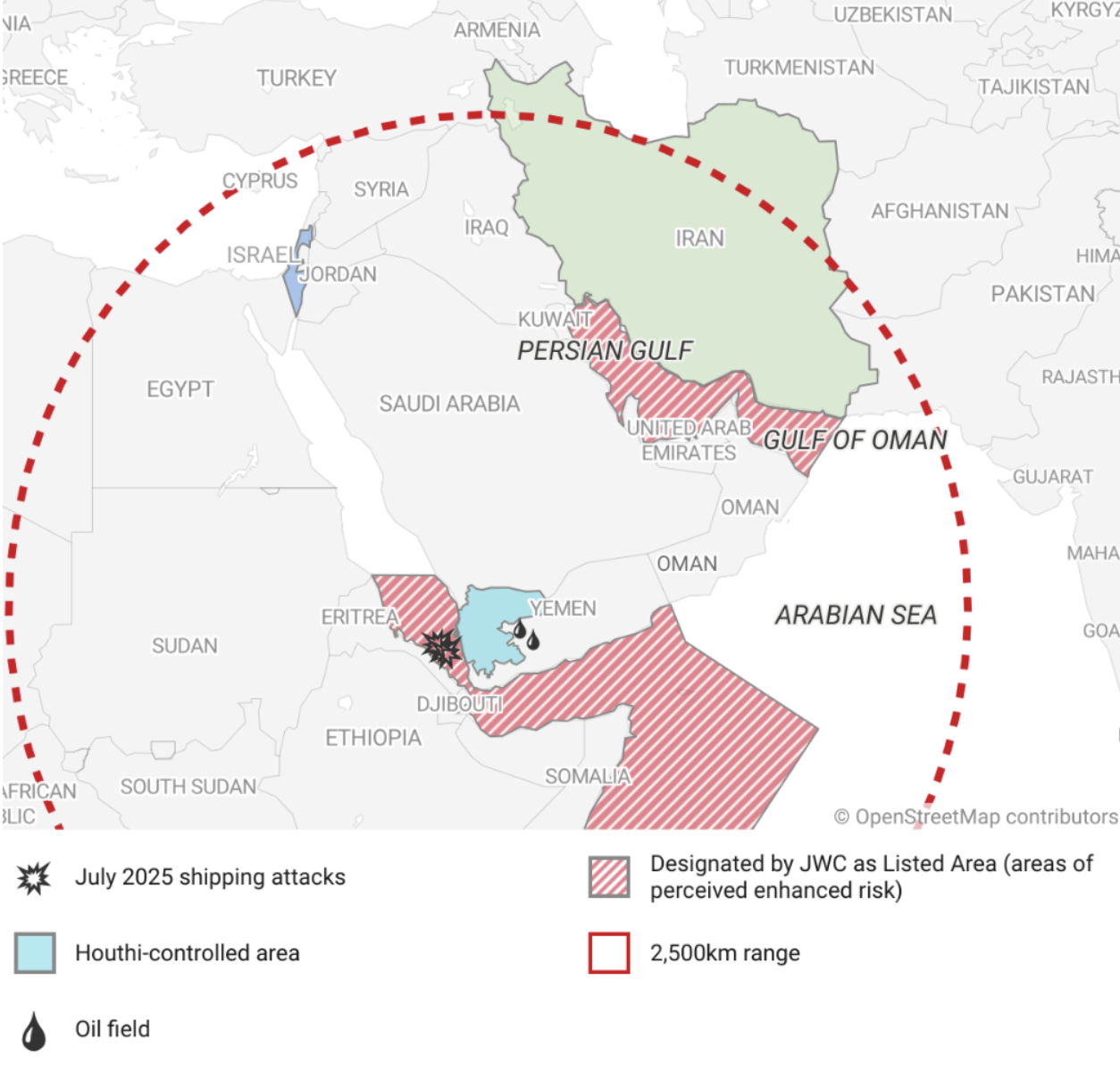

Maplecroft’s latest report from their MENA team dives into the Gaza ceasefire, which they say faces challenges but will succeed in preventing a return to full scale fighting. Why? Trump’s pressure on Israel, Netanyahu’s political pivot to achieve success in 2026 elections, and a weakened Hamas’ lack of options. Cairo and Amman will be breathing a sigh of relief and will face reduced popular pressure from related protests, a driver for their high-risk performance on Maplecroft’s Civil unrest Index. However, major fault lines still remain, with Israel occupying portions of Lebanon and Syria. The Houthis in Lebanon also pose a major risk in the area, and could pivot to attacks on commercial shipping in the Persian Gulf or Gulf of Oman, which the Maplecroft team assign a 66% probability of happening (see chart of Houthi drone range). Risk of a US-Iran conflict also remains high, reaching over 95%.

How the Gulf is saving Pakistan

Foreign remittances from the Gulf are still exploding upwards, as Saudi, UAE and other GCC states continue to borrow and spend at a rapid pace, employing overseas workers in the process. Jonathan Anderson points out that remittances now overwhelm exports and official financing as the single biggest source of dollar income in Pakistan. The inflow has kept the current account in balance and the rupee stable, leading to equity gains too. It’s also pushing dollar sovereign spreads lower still. Jonathan had already exited his dollar bond position last year and had been cautious on further equity upside, but he has to admit that markets look more attractive today. Without remittances, Pakistan has a moribund export economy, much wider fiscal imbalances, an unworkably rising debt load and no exit strategy, but as long as Gulf earnings are flooding in it's difficult to be short this story.

Peru: Under Pressure

Mario Marconini and Nicholas Watson point out that the new President Jose Jeri is under mounting pressure to name his cabinet as soon as possible. The delay in unveiling the new 19-strong ministerial line-up suggests that Jeri is struggling to recruit fresh faces; Jeri has already ruled out re-appointing ministers who served under his predecessor Dina Boluarte, who was impeached on October 10th. The final poll carried out in the days before Boluarte was ousted put her approval rating at just 3%. A cabinet needs to be in place as soon as possible. Even though Boluarte has gone, the protests by Gen Z protestors and transport unions have continued, having been reframed as an act of repudiation against the “mafia pact” of corrupt parties in Congress that are widely perceived as pulling the strings of power. If protests turn violent, Jeri’s could see his position come under threat.

Commodities

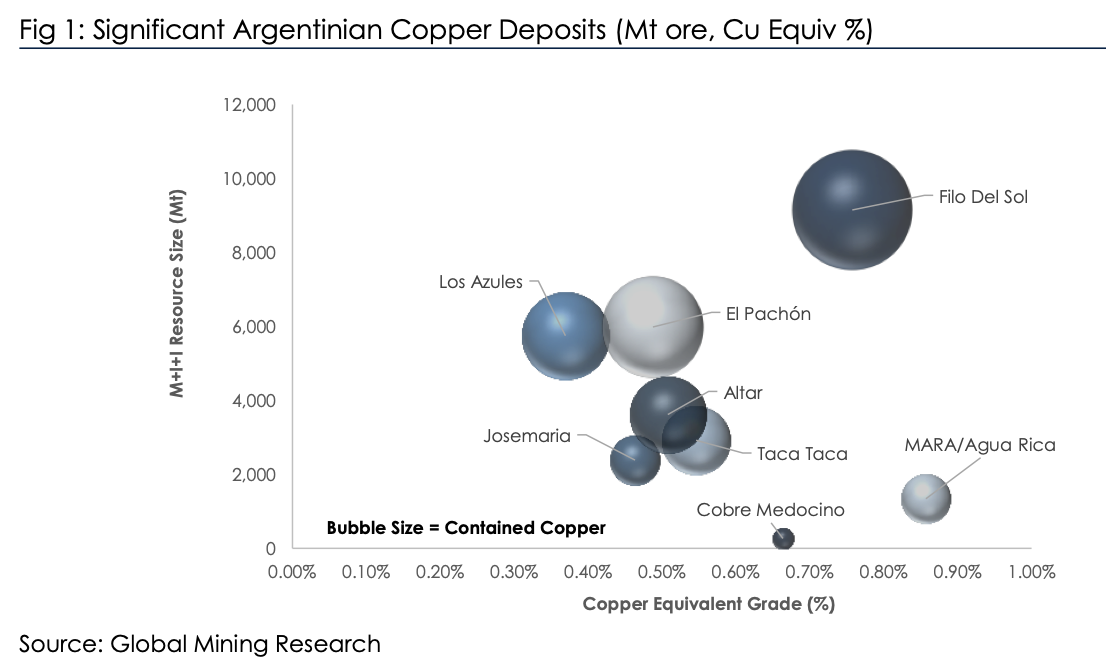

Is Argentina the next big thing?

Argentina has significant copper reserves yet produces no material copper (see chart). The new investment climate (RIGI) in Argentina, spearheaded by libertarian President Milei, is hoping to reverse this. Other volatile countries including DRC have achieved significant growth, so it’s possible. In his latest report, David Radclyffe examines the potential of Argentina copper. He sees potential for the nation to become a 1.0–1.5 Mt per year copper producer (top 10 globally), but comments on the aspirational timelines, with first copper unlikely on this side of 2029. Issues also cannot be discounted, with ESG concerns bubbling alongside a lack of infrastructure and skilled workers. David estimates the total capex at USD $40–50 billion. Lundin Mining has the most leveraged exposure to Argentina in partnership with BHP and is the preferred exposure. There are a few exploration plays, of which NGEx Minerals (non-rated) and its Lunahuasi discovery is the largest.

Is the Gold rally being driven by the US current account?

Gold breaching $4000 last week triggered a plethora of simplistic explanations, many of which undoubtedly contain a grain of truth; debasement, unsustainable developed world debt, inflation, and more. While these issues may be motivating some buyers, Barry Knapp is sceptical. None of his Treasury market indicators of expected supply, 30-year swap spreads, 30-year real rates, the 5s30s nominal curve or 10-year term premium are suggesting market participants expect greater supply. Additionally, market implied inflation expectations aren’t increasing. The US is not losing its allure as a destination for global capital. Barry points out that currency, inflation and debt themes resonate with the press, but in his view the primary catalyst for the rally in gold has more to do with the breakdown of mercantilist export dependent economic models. He explains why he suspects the most important driver of the rally in gold is an end to the ever-widening US current account deficit.

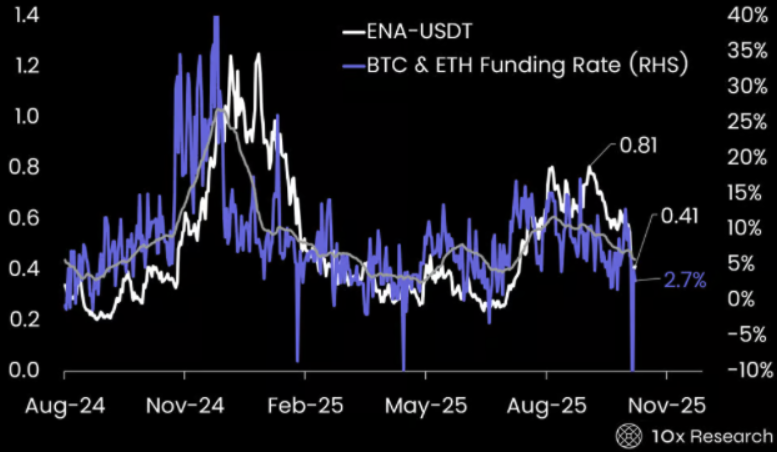

The Altcoin that might have 100% upside soon

Markets rarely break this violently twice in a cycle, yet this time the catalyst came from Washington, with a single tweet on tariff triggering one of crypto’s largest liquidations on record. Once market structures normalise, one altcoin in particular stands out as a potential winner. The recent volatility caused Ethena’s USDe stablecoin, along with Binance’s liquid staking tokens, to lose their intended pegs. USDe liquidity on Binance was exceptionally thin, yet it was being widely used as margin collateral for large leveraged positions — despite lacking the strict peg protections and risk parameters found on platforms like Aave. ENA-USDT now trades at $0.41, which the 10x team say is fair relative to BTC and ETH funding levels. If funding rates continue to normalise, the upside potential could see ENA-USDT rebound toward its previous $0.81 level, presenting an asymmetric upside of 100%.

Oil: WTI to fall below $50/bbl?

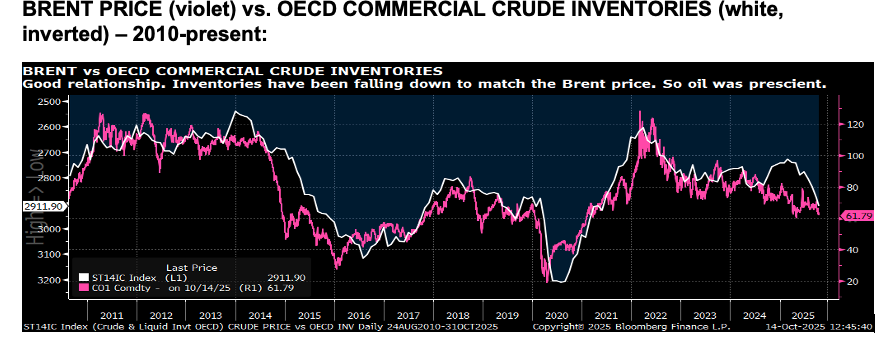

Michael Churchill says if we are in an oil glut, one has to be open to the risk of oil falling below $50/bbl for WTI. Moreover, if Trump has made a deal with Arab leaders to keep that glut going, then there is no floor until some of the North American players lay down rigs or shut in production. Gas is less at risk for this kind of event since it is already so cheap relative to oil. Michael points out that if the new race for global power is focused around AI domination, it stands to reason that the old E&P elites will be gradually losing their power in geopolitics – particularly geopolitical moves meant to keep oil prices firm. Oil prices began falling in January, in anticipation of an increase in OECD crude inventories. Brent peaked at $82/bbl in January. Shortly thereafter (in February) OECD commercial crude inventories hit a low of 2.73b barrels. Since then, Brent has fallen to $62/bbl and OECD inventories have risen 5% to 2.91b barrels.