Europe

Consumer Discretionary

ResearchGreece flags growing competitive risks as Dutch retailer, Action, reveals plans to open its first store in Romania later this year. This marks the first time a similar, yet more aggressive, retail chain is entering into one of Jumbo’s markets (Romania contributes 22% to group sales). Action offers 6,000 products across 14 categories that compete with Jumbo's, with about two-thirds of these items priced under €2.00. Furthermore, investors should not rule out the possibility that Action may choose to enter Greece, where Jumbo operates 53 out of its 89 stores, given Action has identified existing and potential markets with the capacity to add an additional 4,700 stores.

Consumer Staples

Woozle’s 1Q25 channel checks reveal organic revenue trends that are materially below consensus estimates. European organic growth of 1.3% lagged Bloomberg’s 2.4% forecast, reflecting subdued consumer demand entering Q2. While targeted promotions stabilised volumes in Skin Care and Hair Care, high-margin categories like Derma and Fragrance underperformed, creating margin headwinds, particularly amid increased discounting pressure in the UK and Italy. Despite widespread price hikes in the Americas, consumer shifts toward lower-priced alternatives indicate weakened elasticity, while flat-to-slightly-up pricing in Europe masks underlying trade-down risks. Inventory conditions were mixed, with optimal stock levels in Europe contrasted by excess inventory in struggling US categories. Additionally, new product launches failed to significantly drive growth.

Healthcare

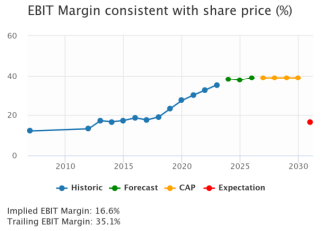

Following publication of its FY24 annual report, Iron Blue increases their CTEC score to 28/60 (top quartile / fertile grounds for shorting). Reductions in inventory & bad debtor impairment provisioning contributed 36% of FY24’s Y/Y rise in PBT adj while the trend of restructuring and asset impairment provisions strip outs continued. The gap between PPE/software capex and the P&L D&A charge narrowed Y/Y but remained elevated at 16% of PBT adj. Receivables factoring increased to $43m (FY23: $27m, FY22: nil) while working capital days outstanding compressed to a decade low 47 days (FY23: 57), implying risk of future mean reversion. CTEC lowered the discount rate used to impairment test its goodwill to a blended 10.3% from 13.3% in FY23. This is now below the 11.5% average for Iron Blue’s coverage universe.

Industrials

This business has a lot to like - high margins, good growth and plenty of opportunity for more accretive M&A. The Healthcare deal has also left a strong financial base from which to move forward. FY numbers last month were no surprise. Revenues were up 4% and adjusted margins were flat. Analysts had put through some upgrades with the trading statement in early Jan and though the share price has collapsed they put through another round in March. The implied to Y3 EBITM ratio is now back to 43. Willis Welby can see the share price doubling.

Industrials

The company has evolved from a traditional electrical component provider into a key enabler of structural megatrends such as electrification, digitisation and energy efficiency, while its diversified portfolio and focus on high-growth segments provide a buffer against economic downturns. Industry-leading margins, coupled with operational efficiencies from the “Legrand Way”, indicate significant economies of scale. Fragmentation in the LV industry supports continued consolidation with LR actively participating through its acquisition strategy. Over the next 5-7 years, 2Xideas expects the group to grow EPS by ~9% p.a. outpacing revenue CAGR of 7%, driven by margin expansion.

Technology

SGE’s AI strategy is taking shape, positioning the company competitively in the SMB software market. While not a first mover, what matters most for the business is having a clear GenAI roadmap and up-to-date AI functionalities. The integration of Sage Copilot with Sage Network enhances customer retention and cloud migration, reinforcing SGE’s ecosystem. However, the monetisation strategy for AI agents remains uncertain. The shares trade at an estimated 21.9x FY25 and 18.8x FY26 adjusted EV/EBIT multiples, which is relatively reasonable given SGE’s successful migration to a subscription model. The challenge for the company now is how AI agents will disrupt its business model and potentially evolve it into a consumption-based model.

North America

Belkin’s Q2 playbook following a stellar Q1 performance

Michael Belkin’s proprietary time series model produced another impressive performance (+37% in Q1), that saw him ranked No.1 out of 188 contributors on a leading alpha capture platform. So far, the stock market decline has been orderly, but he expects that to change as retail investors lose their nerve and start selling along with hedge funds. For Q2, Michael reiterates his call to shift away from tech, communication services and consumer discretionary stocks in favour of gold stocks and defensive sectors (stock specific recommendations are available on request). The next trend analysis downside targets are the 200-week averages. That is currently 4670 for the S&P500, 15700 for the Nasdaq 100 and 8030 for the NYFANG index.

Consumer Discretionary

An off-the-radar winner of the evolution of Amazon’s ambitions and role in the auto ecosystem - AMZN is not looking to own, prep and ultimately sell cars, but is instead looking to provide more content on its marketplace and to help dealers reach consumers. It was likely to have been a very competitive environment for a back-end auction platform to get status with AMZN and the fact that ACV has been chosen as its partner, signifies something special about the approach it is bringing to the market from a technology and go-to-market standpoint. Northcoast is increasingly confident in the company's growth trajectory and considers the pullback in the shares YTD as a buying opportunity. TP $28 (100% upside).

Consumer Discretionary

The world’s largest e-commerce company is considering spinning off its India business and listing it on the domestic stock market. Data localisation requirements and the ability to maintain direct inventory are among the key factors driving this consideration. In recent years, AMZN has also faced certain challenges in India, losing market share to Flipkart and encountering increasing competition from Meesho, which recently raised over $500m in new funding. The Indian e-commerce market is projected to grow from $123bn in 2024 to $292.3bn in 2028, reflecting a CAGR of 18.7%. This rapid growth presents a compelling opportunity. Click here to access Joe Cornell’s Forbes article.

Healthcare: Top short ideas for Q2

Healthcare

Bios sees several opportunities with low short interests and high ADVs that have potential for material downside. Highlighted ideas include: 1) ~$15bn commercial pharma/biotech co. will see material Y/Y declines in sales and poor regulatory environment. 2) ~$13bn facilities & services co. will be materially impacted by changes in reimbursement and impacted by the growth in GLP1. 3) ~$10bn diagnostics & research co. is negatively impacted by the overall biotech funding market for Phase 1 and Phase 2 companies. 4) ~$3bn healthcare services & development co. is grossly overhyped and is burning excessive amounts of cash. 5) ~$1bn development biotech co. is a classic "Fad, Fake, Fraud".

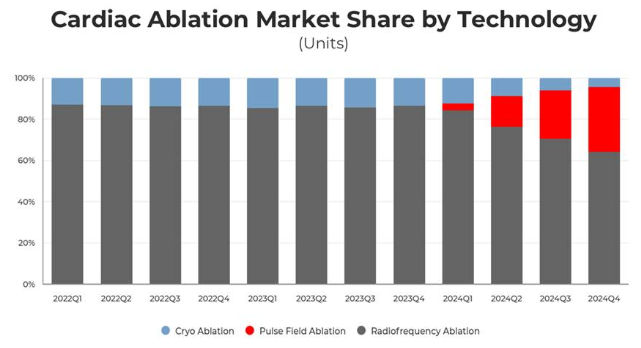

Pulse Field Ablation: Revolutionising atrial fibrillation treatment

Healthcare

The AF treatment landscape is evolving rapidly, driven by the rise of PFA, which is reshaping cardiac ablation and accelerating adoption - particularly benefitting Boston Scientific. Staying ahead in this shifting market requires data powered intelligence to track industry dynamics. MedMine's newly launched therapeutic model delivers comprehensive data on cardiac ablation and left atrial appendage closure across 5 major companies, 70+ product families and 5 key categories: 1) Mapping/Diagnostic Catheters; 2) RF Ablation Catheters; 3) Cryo Ablation Catheters; 4) PFA Catheters; and 5) LAA Occluders & Clips. From Farawave and PulseSelect to Watchman and Amulet, MedMine’s dataset delivers unparalleled visibility into the devices shaping this space.

Materials

SLVM's singular focus on the uncoated freesheet market positions it to gain from capacity rationalisation while strengthening its competitive edge through high-return capital projects. In the 3 years of operations since its spinoff from International Paper, SLVM has generated a total shareholder return of 150% and adjusted FCF of $920m, while debt has fallen $725m. The company has a top-tier management team driving its long-term strategy and despite the secular decline in UFS, Sidoti expects SLVM will continue to reinvest in its business to grow cash flow and earnings. TP $93 (45% upside).

Technology

Revelare recently hosted a call for their clients on APP’s e-commerce advertising expansion. Their guest speaker was Jonathan Snow, co-founder at Avenue Z, an advertising, performance marketing and PR agency managing $75m+ in digital media spend annually across APP, Facebook, Instagram, TikTok Shop, Snap, among other platforms. Mr. Snow provided an update on his agency’s use of APP’s advertising platform for ecommerce clients, growth of brands on the platform, APP’s performance relative to Meta, growth of advertising budgets for APP, how they test for incrementality, audience demographics, CPMs, improvements to the tech stack, and competition from Unity and Liftoff, among other topics.

Technology

CRWD moves from a ‘5’ to Forensic Alpha’s highest risk rating of ‘10’, following the publication of the company’s 10-K. One of the biggest concerns flagged is the sharp growth in ‘Capitalised Contract Costs’, which is now one of the largest items on the balance sheet at ~$850m. It has grown rapidly over the past 5 years, far exceeding growth in sales. CRWD capitalised expenses of $584m in 2025 (vs. $374m last year), far in excess of the amortisation charge of $318m. Remarkably, this represents nearly one third of the entire sales and marketing spend for the year. Also evident, is a rapid growth of ‘Other Asset’ accounts, with minimal disclosure of the makeup or reason for the change. Finally, there is a growing divergence between GAAP and non-GAAP earnings, due to the increasing use of stock-based compensation.

Technology

Cyber diamond in the rough - unloved and out-of-favour, VRNS has underperformed its peers by a wide margin over the last 12 months. However, Felix Wang thinks its fortunes may start to change this year. His bullish thesis revolves around overplayed concerns re. the company’s ongoing SaaS transition and with continued product leadership, alongside a better sales team, VRNS's 2025 ARR and earnings guidance are beatable. Investors are highly sceptical of the company’s ability to reach $1bn ARR by 2027. This is why it is trading at only 6.6x 2026 EV/ARR. With a multiple re-rating and M&A optionality (Google's historic acquisition of Wiz for $32bn could open the floodgates to more M&A in cybersecurity), Felix sees 30%+ upside.

Emerging Markets

Industrials

Multiple directors and senior officers bought in total $8.1m worth of stock at prices ranging from KRW 627,000 to 672,000. The largest purchase was made by Dong Kwan Kim (Co-CEO and a member of the founder's family), who bought over $2m in his first purchase. Jae Il Son (Co-CEO) purchased $619,000 in only his second purchase, despite a long tenure, and his largest buy. Additionally, Byeong Cheol Ahn (Exec. Dir.) bought $575k and Hyeong Lae Ye (Officer) $382k. The buying seems to be coordinated and could be in response to the Korean financial authorities blocking a proposed $2.4bn capital increase. While the stock has dipped just below its multi-year high, it is encouraging to see this huge cluster of insider purchases.

Technology

The Apple Killer - Xiaomi is eating up global market share in smart phones, tablets, home electronics and now cars. Erik@YWR feels like many investors are living in a bubble. They don’t spend time outside the US and Western Europe. They don’t go to Africa, the Middle East, or South Asia and see how brands like Xiaomi are gobbling up the world markets. Brands like AAPL and Western car companies are getting boxed into a smaller and smaller market. If the dam breaks and Xiaomi gets momentum in Europe it will do serious damage to AAPL. You can see the network effects it is creating. Make the phone, the tablet, the home appliances and the car, and have it all interconnected with its AI system.

Developed Markets

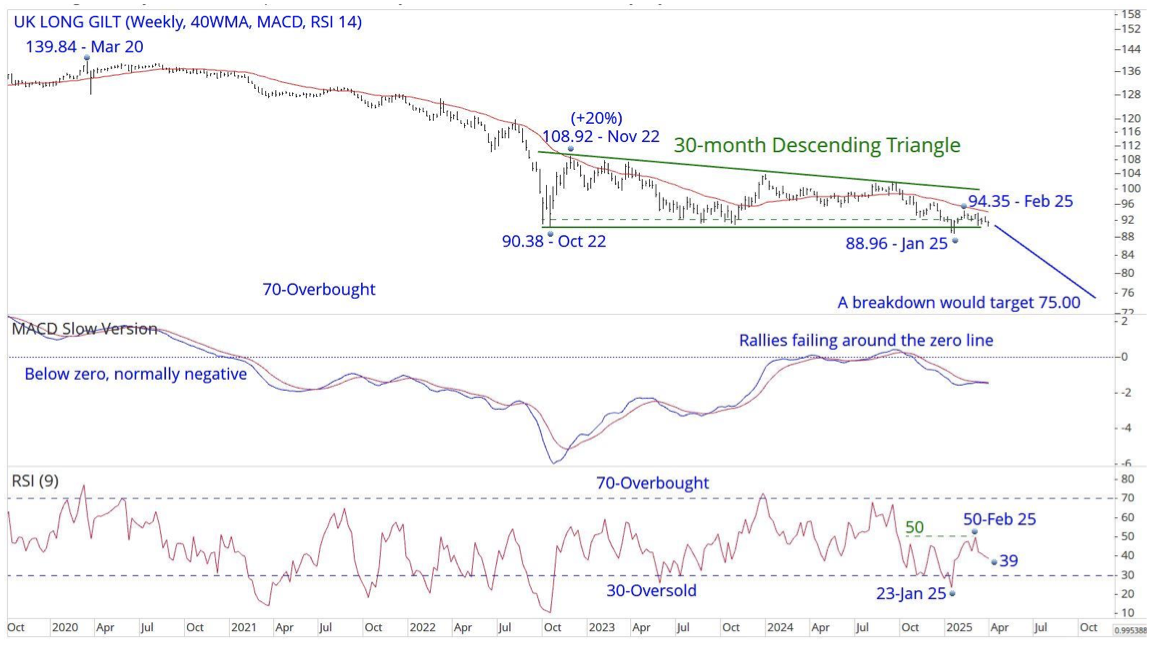

UK: Long gilt

In Jan, the UK long gilt (91.48) briefly broke the 28-month area of support that extends from 90.38 to 92.33. The market traded as low as 88.96, now considered an important support level. The chart shows a potential 30-month Descending Triangle. A weekly close below 88.10 would confirm the breakdown, targeting a fall to 75.00. The recovery rally from the Jan low has been stalling below the falling 40-week WMA. RSI rallies have been reversing from around Neutral 50. Chris Roberts will look to recommend a short if the Gilts complete the confirmed breakdown. Initial resistance is at Feb’s 94.35 high.

April 2nd hasn’t liberated the markets

Paul Krake sees the second quarter of 2025 being defined by immense economic and earnings uncertainty surrounding Trump’s tariff regime on April 2nd. The shift away from US exceptionalism has largely run its course without meaningful fundamental support. No investors today have dealt with a tariff regime of this breadth. The Fed will be forced to balance the act of fighting the stagflationary impact of tariffs and cushioning their impact on the economy. Q2 is a battle between optimism and falling bond yields, weakening the USD further. The S&P 500 could trade towards 5000 by the end of June, with the potential for a short squeeze at the start of Q2. Expect commodities to weaken, but gold to outperform. German fiscal stimulus will do little to offset the tariff-induced pain as it remains highly exposed alongside Japan.

The name’s Bond

A recession is Manoj Pradhan’s base case, and he expects bond yields to fall to the 2.5%-3% range over the next few months in the role of an automatic stabiliser and reflecting the ‘stag’ part of stagflation in the US. Markets have yet to price in a recession. That gives plenty of room for bonds everywhere else—other than Germany—to rally, particularly in EM. Central banks across the world have a much clearer path to lower policy rates compared to the Fed. If the Fed becomes cautious, other central banks may be hesitant to ease rapidly, meaning that bonds in those economies will rally even more. Bonds present the clearest risk-reward, and there’s no point in curve trades. USD weakness provides a second-best risk reward because retaliation by other economies or successful negotiations on a bilateral basis can shock FX pairs substantially.

US: Liberation Day

The swathe of tariffs was worse than expected, and Gerard Minack says that lower tariffs must be negotiated within the next few weeks to prevent a serious knock to growth. Whilst a recession is possible, it’s not yet Gerard’s base case, and markets are wrong to expect Fed intervention otherwise. He also expects double-digit percentage declines in both US and non-US equity markets. As is to be expected, treasuries will rally as equities fall, but the gains may not persist. If inflation concerns limit the Fed’s ability to ease, long-end rates will start to rise as short-rate markets take out the cuts that are now priced. Moreover, treasuries will have to cope with large ongoing deficits. Just as equity investors are now realising that the strike on the Trump put is lower than they expected, treasury market investors may also recognise that any Bessent put is almost as worthless.

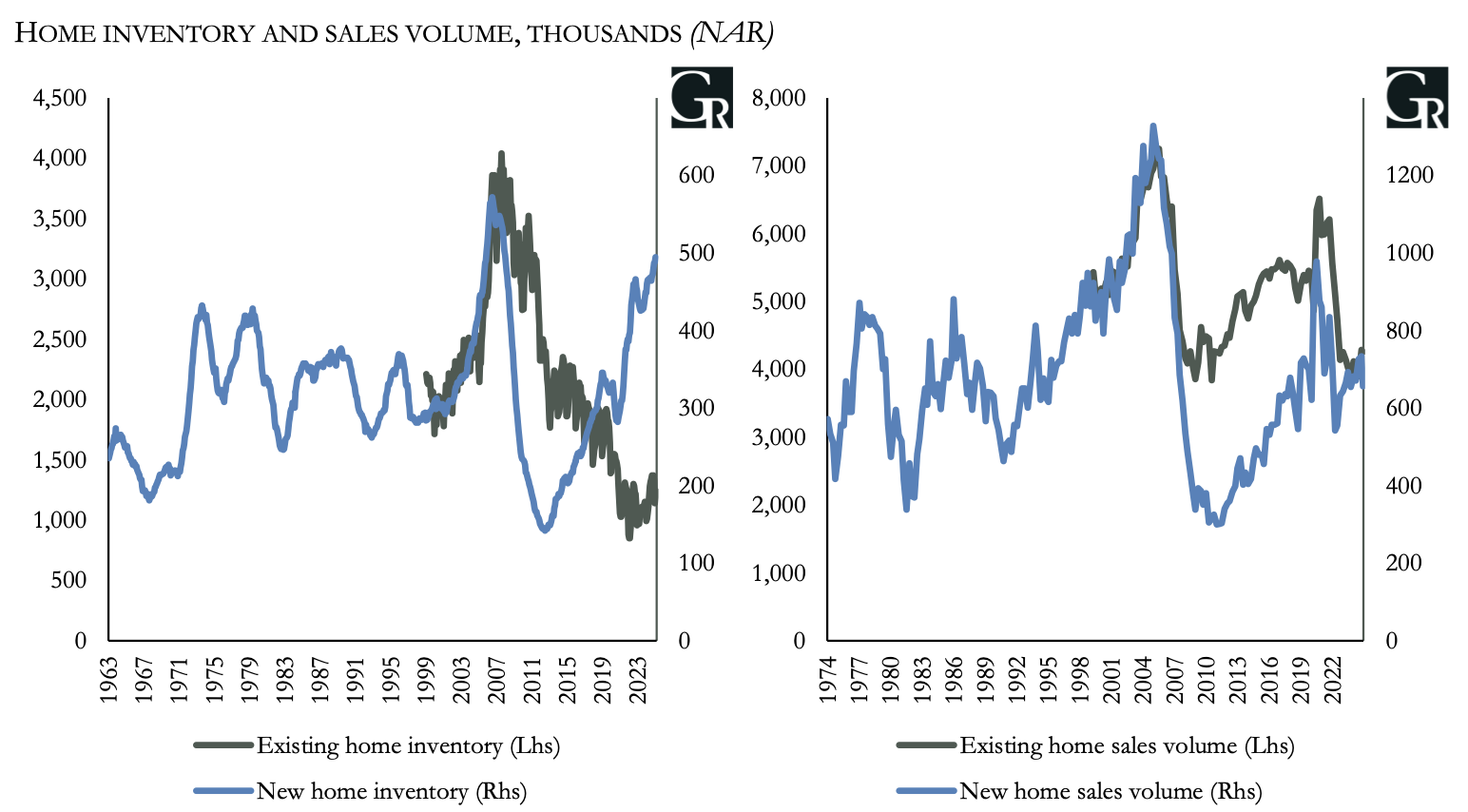

US: Housing hazards

Niall Ferguson points out the signs of weakness in the US housing market in his latest detailed report. Home inventories are high (see chart), whilst unaffordability prices out the median American from buying a home. A continually rising average mortgage rate, even in the best-case scenario, will increase net interest expense and put pressure on household budgets even as the prevailing new mortgage rate declines. Homebuilder-specific negative impacts from the Trump administration’s economic policy, namely reduced immigrant labour and higher prices for import-exposed building materials, all add to the case for bearishness.

US: Optimism amidst the pessimism

The expected fallout from Trump 2.0’s Reign of Tariffs undercuts Ed Yardeni’s former bullishness and dims the prospects of his base-case Roaring 2020s scenario for now. It has also drained confidence in the US economy on the parts of everyone from CEOs to consumers to investors. Recent data showing manufacturing faltering and purchasing managers paying higher prices suggest stagflation is already taking root. Ed is dropping the odds he assigns to his Roaring 2020s scenario from 65% to 55% and upping the odds of a stagflation scenario, which may include a recession, from 35% to 45%. That 45% is also the probability he sees that the stock market’s correction will deepen into a bear market in coming months. Yet Ed still expects an up year, with the S&P 500 rising above 6000 by year-end.

Hong Kong: Pulled in two directions

Hong Kong’s position as a small cog connecting between two larger ones (the USA and PRC) makes it doubly exposed to a changing world. If the two large cogs rotate in opposing directions, HK risks being shattered. The Hong Kong Dollar Peg is no more; the authorities are running countercyclical policies, the HKMA is running a currency target - and targeted regimes can be broken. Despite some signs of internal deflation, Hong Kong seems not to be improving its fundamental competitive position. The exchange rate is overvalued and therefore vulnerable. In the long term, the HKD is in any case an anachronism. As the PRC and HK economies become ever more integrated, the HKD’s raison d’etre will be diminished. Andrew Hunt asks, is now the time to short the HKD as the economy again softens? It still seems too soon, but in a world of uncertainty the opportunity may arrive soon.

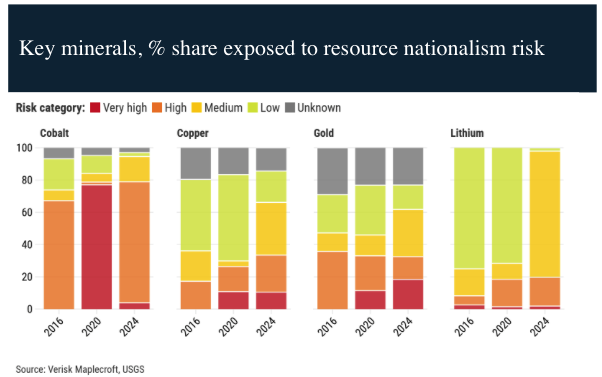

Emerging Markets

EM: Taking control

Emerging markets are home to a swathe of critical miners, including cobalt, copper, gold and lithium. According to Verisk Maplecroft’s Resource Nationalism Index (RNI), which measures government control of economic activity within mining and energy, 47 EM countries have registered a significant increase in the last five years. If this momentum continues, disruption to the supply of critical minerals for the renewables, tech and defence industries is probable. Some EMs will attempt to leverage their reserves in the wake of increasing geopolitical competition, implementing a wide range of measures including tax and rent hikes. Over the next few years, expect an increasing of number of related policy announcements in both producer and demand countries.

Brazil: Higher for longer

The country remains polarised at the political level, centred around the bitter fight between Lula and Bolsonaro. On the economic front, activity expanded in January after a strong performance in 2024, although Marcos Buscaglia expects a sharp deceleration this year. Downside in Q1 will be limited by agriculture and tourism. The labour market is showing strains already, and Marcos reiterates his view that credit will decelerate fast in the coming months, impacting employment and the wider economy. Inflation came in at 1.31% m/o/m in Feb, but decelerated to 0.64% m/o/m in March. Price pressures more linked to the cycle bring conflicting signals. Marcos expects the BCB to deliver a 50bp hike in its May meeting, then to remain on hold for the remainder of the year.

China: What to look out for

This cycle is different from previous rounds in the 2000s and 2010s, in that the downturn has been driven by a collapse in household spending. As a result, the most important indicators are those that highlight consumer and market sentiment. Jonathan Anderson says it is therefore important to watch property sales, equities and (especially) bond spreads. The three higher-frequency data series he watches are property sales, equity pricing - and especially bond spreads, a crucial gauge of where we are in the household "savings glut". All three indicators are now pointing solidly sideways. Property sales are still stuck at the trough, equities have been range-bound and bond yields are receding again after a mid-month jump. I.e., Chinese growth may have stabilized at a muted level, but there's no strong consumer recovery. There's more work to be done.

China: Market fears of recession remain intact

According to John Fagan, fears of Japanification have loomed large over China’s bond market in recent times, driven by persistent downward pressure on yields amid recessionary and deflationary worries reminiscent of Japan’s “lost decade.” In early 2025, China’s 10-year government bond yield sank to an unprecedented low of around 1.61%. However, sentiment began shifting from mid-February as a sustained sell-off in long-term bonds took hold, driven primarily by the PBoC’s steadfast commitment to defending the yuan, a move that tightened liquidity and lifted borrowing costs in both bond and repo markets. The dynamic pushed yields upwards to around 1.94%. Yet, recently, yields showed renewed weakness, with the 10-year yield retreating to approximately 1.87% this past Friday, despite aggressive governmental efforts to issue more debt aimed at stimulating economic growth and market stabilisation. Markets are indeed still worrying about recession and deflationary pressures.

Hungary: A stable but muted outlook

The economy is neither boom nor bust. Domestic activity is still recovering after the 2022-23 shocks, but rather draggy with no clear sign of acceleration. Meanwhile inflation has bounced back up, which keeps MNB from cutting rates further. This combination keeps the current account in mild surplus, and should be a source of support for the forint in the coming quarters. The other defining trend in Hungary in the past two years is the ongoing equity rally led by OTP Bank. However, most of this is due to a boom in operations in Russia and elsewhere, i.e., little to do with Hungarian macro per se. Not much to do at this point. Jonathan Anderson doesn’t mind the HUF carry trade, but on balance he remains on the sidelines.

The Philippines: Easing risks

According to Bob Herrera-Lim, a recent survey on the Senate race and the limited effect of the public protests in support of former president Rodrigo Duterte provide some evidence that his arrest has not yet resulted in a substantial increase in short-term political risk. US Defence Secretary Pete Hegseth affirmed Washington’s support for Manila in its territorial dispute with China, reducing the risk of a politically embarrassing about-face by the new US administration. Key factors to watch in the next few months include the April surveys for the senate, Vice-President Sara Duterte’s return from the Netherlands and the administration’s handling of economic and governance issues.

Commodities

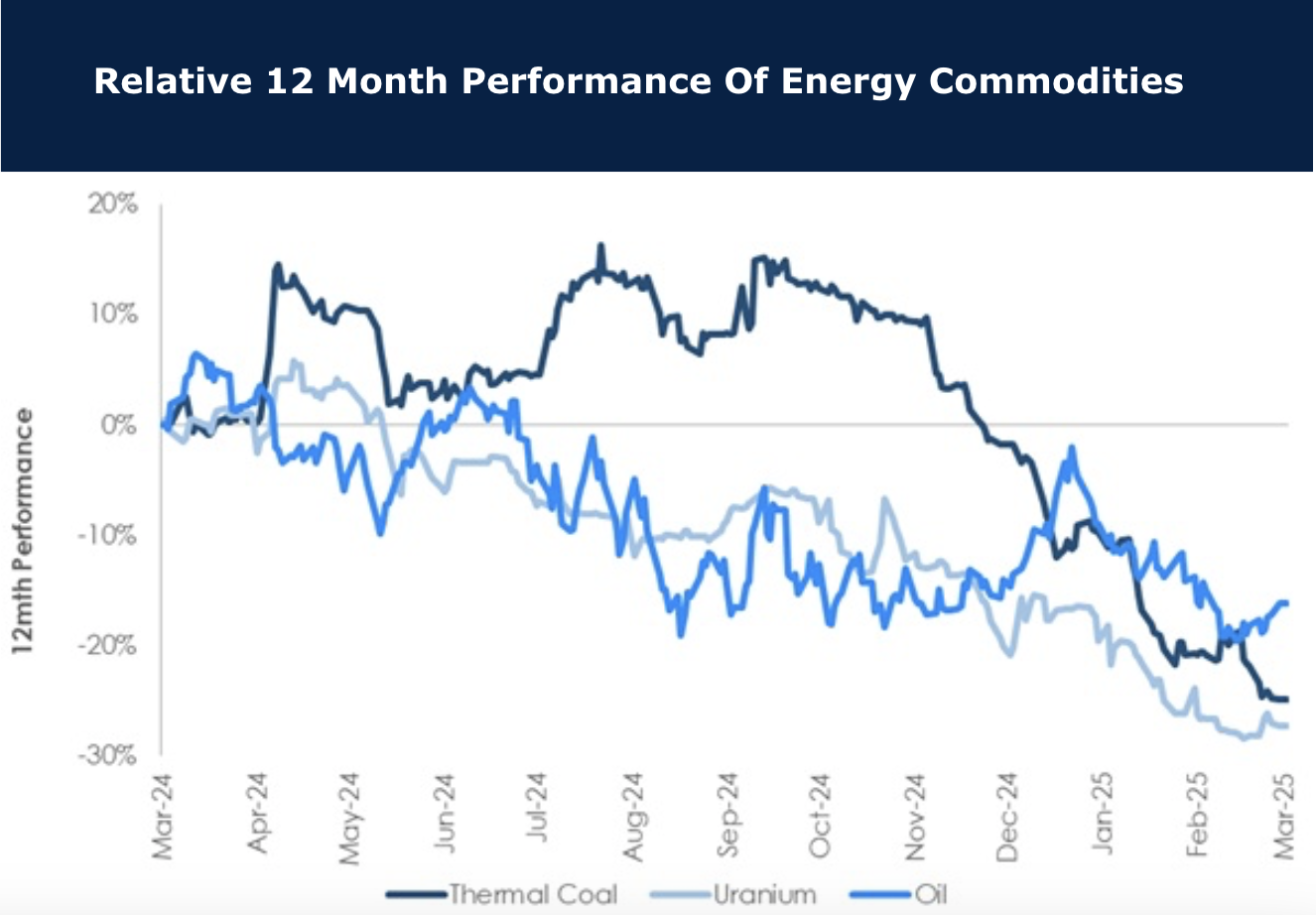

Thermal lost its spark

One of the worst performing commodities of 2025, thermal coal has been a drag on the coal miners. The reason is largely down to China and Australia’s strong production. Of course, there is a wider overlay of tariff concerns, recession fears and Deepseek disrupting the AI market. The chart shows how thermal weakness is not isolated, and has actually lagged the decline in both oil and uranium prices. Some coal producers are feeling the pain, although some producers have seen stronger share prices relative to the underlying thermal and met coal prices--they’ll need this strength going forward. The potential silver lining is that lower energy prices are deflationary, which can support remote miners reliant on diesel power generation. It’s bad news for the diversified miners producing coal such as Anglo American, BHP Group and Glencore, and also the pure play coal miners, but good news for much of the mining sector.

Gold: Divergence with the oil price is actionable

James Burdass notes that gold's ascent continues, fuelled by a confluence of macroeconomic and geopolitical factors, while crude oil faces persistent headwinds. This actionable divergence is something he has been commenting on for at least the last nine months. The divergence to oil represents one of the most actionable items in the sector. Potential headwinds in oil such as peak Asian demand, relaxation of OPEC+ quotas, new supply roll-out and the US energy dominance agenda are all significant, and investors can play geopolitical trends by investing in the yellow metal itself. Whilst USD strength held gold back during Q4/2024, Trump's unpredictability during Q1 justified James’s view of him as a "gold friendly" influence. The loss of momentum in the S&P 500 has caused more generalists to wake up and see what was once a stealth bull market in gold turn into more of a raging bull market.

A secular bull market story

The Bloomberg Commodity Index’s weekly chart features a 20-month Rectangle that started forming some 15-month after the index peaked at 140.58. The BCOM fell 34% between 2022 and 2024, and Chris Roberts continues to view the rectangle as a base that will be followed by the resumption of the secular bull market that started in 2020. The monthly MACD has finally started to turn up. A number of commodities have set new all-time highs in recent months, including cocoa, coffee, copper and gold. Chris already has long positions in the latter two and is patiently monitoring other markets looking for buy set-ups. He is adding to spot silver longs this week. If the BCOM breaks out from the Rectangle, the measured move target is around 126.00.

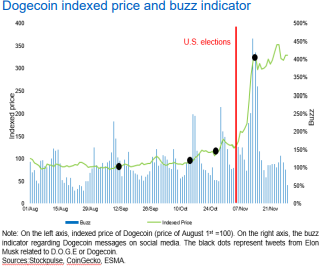

Meme coins expose close ties between crypto and social media

Stockpulse, whose platform provides real-time insights into social media sentiment, featured in an ESMA risk monitor recently with their data for crypto coins. Social media has been a key enabler of the growth of crypto assets and the recent boom of Dogecoin and other meme coins that originate from internet memes and jokes once again exposed this relationship. Musk’s influence on Dogecoin’s price is well known - he frequently tweeted about the coin in the past, often causing its price to surge (see chart). The growing role of social media and on-line communities in shaping market trends and investors’ sentiment is a source of concern for regulators because of the risks it raises to investor protection and market integrity.