Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

Elisa (ELISA FH) Finland

Henri Korpi (EVP Development) sells 20,000 shares at €41.55, reducing his holdings by -62%. This is his largest sale and his first since Jan 20 when he sold shares at €55. The sale is also a reversal from a small purchase in Apr 22 at ~€55. Smart Insider downgraded the stock on Oct 22nd, ranking it -N based on a €930,000 sale from Vesa-Pekka Nikula (EVP, Consumer Customers) at €46.44. That sale was his first since 2020. The stock has moved slightly lower since then; is now near a multi-year low and it is concerning to see additional selling and no insider buying. Smart Insider are downgrading the stock further, from -N to -1 (lowest rating).

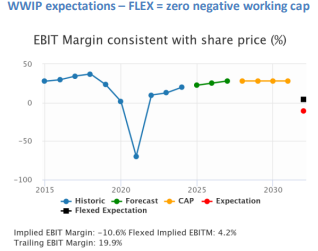

The last major news was OTB's Final Results for FY24 on Dec 3rd which looked great. Revenue was up 14%. Margins moved up by 170bp. And EBIT was up 22%. And the good news did not stop at the year end. Early trading for Sep 25 had revenues up 14% and bookings were strong. Even after the massive move in share price in the last few months, OTB has a basic implied to Y3 EBITM ratio that is negative. Willis Welby would prefer to use a flex with zero negative working capital and that flex above shows a ratio of just 15 for a company that is winning, has great financial productivity and double-digit growth. This share price could double.

Pernod Ricard (RI FP) France

A cash mirage - a closer look at the balance sheet shows a huge increase in the use of factoring in H1, benefitting cash flow by nearly €500m. Stripping out the sold receivables, “Trade receivables before factoring/securitisation” has moved up in the past 6 months from €2.6bn to €3.8bn. It is also higher than the same point in Jun 23 despite falling sales. This is concerning as it raises questions about collectability, particularly when one considers an existing red flag dating from the FY24 financial statements on ageing of receivables, which showed a sharp increase in receivables past due more than 30 days from 5% to 14%.

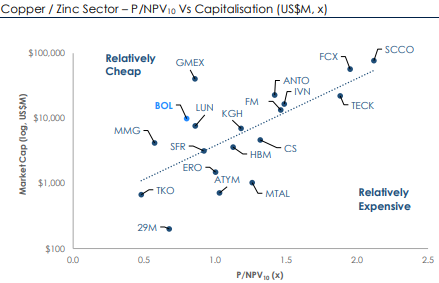

Boliden (BOL SS) Sweden

GMR continues to favour the outlook for zinc, where BOL is a large player (~0.5Mt/yr) and offers hard to find exposure. It is rare to find a company with several near-term events expected to support the business. These include a forecast recovery in Aitik grades; Tara moving back to full production rates; completion of the Odda expansion; Garpenberg throughput upside from permit revision; as well as plans to acquire Lundin’s Neves Corvo and Zinkgruvan mines. BOL is not expensive trading at 0.8x NPV10 and a prospective 2026E EV/EBITDA of 4.2x and FCF yield of 11%. Gearing is expected to peak in 2025 at ~22%.

BE Semiconductor (BESI NA) Netherlands

Q1 outlook below market expectations - one of BESI’s competitors was also cautious about the start of 2025, as most of the end-markets for the back-end equipment makers remains challenging. The growth of the semiconductors market is solely driven by AI applications, which still represents only a modest part of that industry, particularly in volume terms. While BESI is a great company, analysts at the IDEA! consider it to be heavily overpriced and the upcoming cycle has been more than fully reflected in the current share price.

North America

A search for big returns in small packages

Last Apr, KCR highlighted the remarkable opportunities in micro cap stocks. Their portfolio was a group of ignored and overlooked companies that typically had prodigious cash-flows and healthy growth runways, and despite delivering an impressive 21% return, KCR continues to source wildly mispriced (too cheap) stocks. Their Micro Cap Model Portfolio has a FCF Yield of 10% vs. the Russell 1000 Core ETFs’ holdings FCF Yield of <3%; suggesting powerful upside returns with a much higher margin of safety than the expensive and concentrated large cap index funds. A recent addition is ScanSource, which has transformed itself into a leading hybrid solutions provider by combining traditional technology hardware with cloud-based solutions. While headwinds have hampered sales recently, SCSC is generating solid cash flow and KCR thinks the stock can potentially double.

Event-Driven Legal℠ investment-research opportunities

MDC follows significant legal disputes to provide clients with actionable investment ideas that tend to be non-correlated with the market. They currently believe that the following companies will likely be involved in significant litigation in 2025 and 2026: Abbott Laboratories, Avadel Pharmaceuticals, Axsome Therapeutics, Bausch Health, Bayer, Burford Capital, Corcept Therapeutics, Exelixis, GSK, Harmony Biosciences, Johnson & Johnson, Liquidia, Live Nation, Reckitt and Sotera Health.

AI driven 10Q / 10K text analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) American Express - added several comments re. increased competition, as well as expansion through acquisitions. 2) Chipotle - aggressive goals for store openings; colour on new stores / pricing elasticity. 3) ePlus - decreased account profitability; government contract termination risks. 4) Microchip Technology - customers delaying orders; may continue to borrow to fund dividends. 5) PepsiCo - private label competition concerns.

The state of video gaming in 2025

Matthew Ball* joined Revelare for a discussion on the outlook for video gaming. He shared his in-depth analysis of waning growth trends for gaming spend and engagement, pricing power for video games, title development issues, Nintendo and the outlook for the Switch 2, as well as the potential impact of GenAI among other topics.

*Matthew is the CEO of Epyllion, which provides investment and strategic advisory services, produces television, films, and video games, and co-operates/owns the Roundhill Ball Metaverse ETF, which was the single largest sector ETF launch of 2021, among various other operating subsidiaries.

Ahead of the group's Q3 results in early Mar, Chuck Grom upgrades CASY to Buy. His increased optimism is driven by: 1) more optimistic view on near-term fuel margins; 2) sustainable foot traffic trends per GHRA’s Placer analysis; and 3) continued momentum on the digital front as their SimilarWeb data suggests app downloads and engagement remain robust even with a growing install base. Chuck increases his Q3 EPS estimate from $1.79 to $2.10 with his FY25 and FY26 EPS also moving higher to $14.30 and $16.20, respectively. His model now implies ~13.0% EBITDA growth vs. guidance of "at least 10.0% growth".

Verbatim Advisory Group

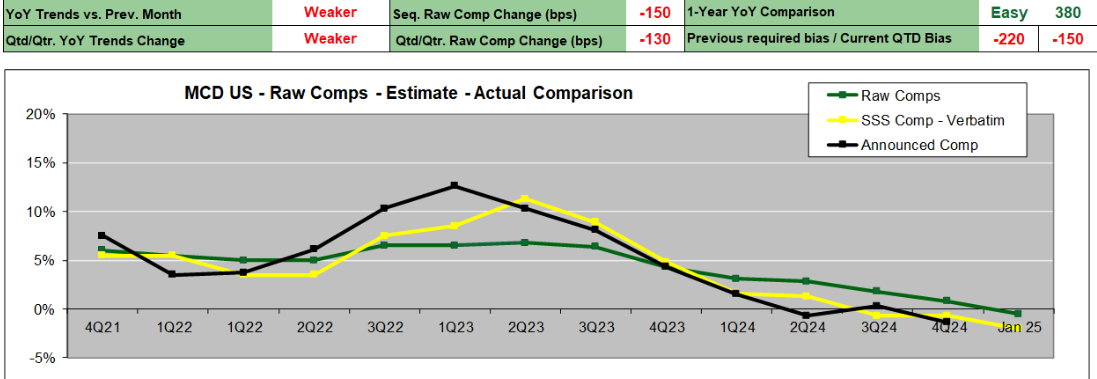

MCD US Jan sales trends are weaker than both Dec and 4Q24 trends, according to Verbatim’s latest channel survey. Traffic and sales remain sluggish mainly because of adverse weather, higher competition and a weaker macro environment. Prices have risen by 2% on average for Big Macs, Quarter Pounders and French fries. Staffing is easier Y/Y due to a higher number of applicants, with wages remaining steady. Online ordering continues to grow. Verbatim’s Jan Comp Estimate is -2.0% vs. 4Q24 (Oct-Dec) Actual Comp of -1.4%.

John Zolidis sees the potential for ~50% of the current m/cap to be returned to shareholders over the next 5 years, while YUMC simultaneously grows its EBITDA by nearly 50%. The company’s ability to grow while this capital return programme is underway highlights both the model and value creation from new unit openings. Its valuation has contracted while domestic restaurant stocks have seen valuation expansion establishing an extreme relative multiple discount. A 10.5x EV/EBITDA multiple generates a 34% 1-year return using 2026 forecasts. Over 4 years, a 12x multiple vs. John’s 2029 estimates produces a double, not including dividends. Downside is protected based on unit growth, cash flow, buybacks and the current 8.6x multiple.

Industrials Idea Forum

Given the market volatility and uncertainty, it was not surprising that MYST’s Industrials experts at their latest Buyside event, focused on sectors with good visibility and tailwinds, such as Aerospace and Power, in addition to inexpensive stocks and cyclical recoveries. Highlights include:

Allegiant Travel Co. (ALGT) - Simplified story & substantial LT earnings power upon completion of hotel sale. TP $225 (160% upside).

CRH (CRH) - Comically cheap vs. peers & fast-approaching Index inclusion catalyst. TP $150 (40% upside).

Solaris Energy Infrastructure (SEI) - Transformational pivot from legacy oilfield services to DC power generation. TP $52 (75% upside).

VSE Corp (VSEC) - Under-the-radar high-growth Aerospace aftermarket pureplay. TP $150 (45% upside).

AXON's impressive growth over the past several years has been a result of strong products, innovation, execution, acquisitions and partnerships. Unfortunately, it looks like one of those early partnerships has turned south and as Flock Safety emerges as a competitor to AXON in the ALPR, drone and RTCC space, it could impact the growth trajectory of AXON's recent Fusus acquisition. AXON's share price has surpassed Northcoast’s price target, and they are moving to a Neutral rating on valuation and concerns FY25 guidance will not live up to the Street’s lofty expectations.

DD is benefiting from the recovery in its electronics segment and steady growth across its other businesses. The group has consistently exceeded quarterly guidance and in a market where earnings misses are common, DD’s reliability stands out. Meanwhile, the company is preparing to spin off its world class electronics division. IndustrialsCo is trading at ~9x EV/EBITDA with a case to be made for a materially higher multiple when the actual split occurs. With positive growth trends and a significant value-enhancing transaction ahead, DD remains a compelling investment.

Field views have indicated that CRWD has executed very well to mitigate interruption to its bookings in the months since its crash. Recently, some contacts have told SPR that business continues to be strong, but think the vendor is setting itself up for a "reset" as a result of very aggressive efforts to pull business forward. The timing of a slowdown in bookings is uncertain. However, the channels who are predicting a reset have had very credible views in the past and SPR is now working hard to understand any changes to the vendor’s business. SPR expects a strong upcoming report and will continue to monitor for a slowdown if/when it arrives.

ETR

Technology Spending Intentions Survey: Tracking tech budget trends & vendor demand

ETR’s Jan TSIS, based on responses from 1,835 tech leaders, projects 5.3% Y/Y IT spending growth in 2025, the highest since Jul 22. 73% of organisations plan budget increases, driven by cloud expansion and project acceleration. Notably, only 6% cited new vendor adoption, while 12% focused on enhancing capabilities with existing vendors - reinforcing debates around platformisation vs. vendor sprawl. TSIS tracks hundreds of companies and each quarter ETR publishes 200+ vendor specific reports. In their most recent webinar, they highlighted 20 vendors including AWS, Google, Salesforce, Snowflake, Workday and Zscaler - 13 had positive outlooks, 2 were downgraded and 3 maintained their outlook.

Japan

Yuka Marosek examines what has motivated Symphony Financial Partners to invest in this geometry survey company and if there is more upside to the stock. Key points include: 1) Japanese construction consulting industry projected to grow from $449bn in 2023 to $571bn by 2030, driven by large-scale infrastructure projects and government initiatives. 2) Japan aims to increase wind power output from 4,000 GWh (FY21) to 51,000 GWh; Oyo leads in steel platform infrastructure for seabed surveys, giving it a competitive edge. 3) AI adoption can dramatically cut survey time - improving margins. 4) Overseas reorganisation to improve profitability. 5) Recent takeovers in the sector suggest Oyo could be a future acquisition target.

Emerging Markets

Management’s R106bn whitespace growth opportunity is overstated since a large part of the perceived opportunity is already well serviced by the likes of market leader, Shoprite, meaning BOX will have to compete aggressively for market share. Furthermore, targets of mid-teens turnover growth over the next five years are unrealistic (planned 70 new stores p.a. would need to increase to 100 stores p.a. by FY29 and to 145 stores p.a. by FY31), while BOX’s store expansion will be debt-funded, putting it at a disadvantage vs. peers. Primaresearch also flags succession risk, with the potential exit of more than half the management team by FY27. BOX’s premium valuation to SHP is unwarranted.

Ping An Insurance (2318 HK) Hong Kong

Ping An trades at record low valuations, offers a 6% dividend yield, is highly innovative and growing, but Erik@YWR notes that there is another kicker. Chinese pension reform. Individual retirement plans. This started as a pilot scheme in 2022, but in Dec last year the plan was officially rolled out nationwide. Erik thinks this is going to turn into a big story and will give Ping An a new growth driver which will rerate the P/E from 5.5x to over 10x. He targets a total return over the next 2 years of more than 130%.

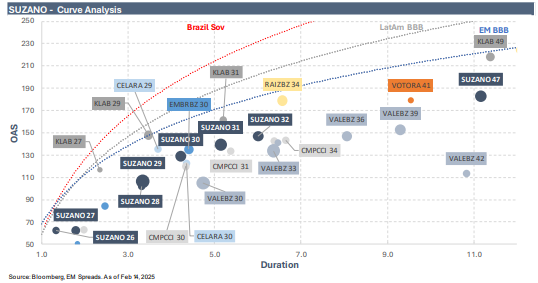

Suzano (SUZB3 BZ) Brazil

Despite additional industry supply, tight market conditions persist due to low stock levels, maintenance-related production cuts and operational disruptions. Healthy pulp prices, higher sales volumes, controlled costs and a focus on deleveraging should support Suzano’s cash generation and credit profile in 2025, with this trend likely continuing as no major new supply is expected. Within Suzano’s capital structure, EM Spreads prefers the 3.750% 2031 and 3.125% 2032 bonds, which compare favourably to select regional peers, the broader EM BBB Index, and the US BBB Index. Additionally, these notes trade below par at $90.1 and $84.6, respectively, while most of Suzano’s curve remains priced above par.

Macro Research

Developed Markets

Tactical trading will struggle in 2025

According to Paul Krake, the problem is that every trade of a tactical nature is influenced by Trump policy. In his latest report, he sets out his view over the next six months. Expect China to work on AI plays like Alibaba, Baidu and Tencent, as AI remains a leading driver of global beta. Investors can benefit from staying LONG commodities and infrastructure plays, especially electricity. Stick to the world’s best firms, many of which are US-based, whilst fading Germany in light of the inevitable EU recession. Stay away from rates and currencies as long as the Fed isn’t moving. Finally, when it comes to crypto, investors are looking at a clear Trump favourite and should see zero reasons to sell.

MSCI World hits a new high

There is a new high on the MSCI World Index, but not on US indices. Valerie Gastaldy points out that this seldom happens, but European Equities are responsible for this improvement. Bonds remain in medium-term bearish trends and may have reached their best level for the coming weeks. The Dollar still has a chance of resuming its rally, though it fell below the first key level and may simply resume the long, erratic evolution of the previous two years. Valerie’s MSCI World targets are still at 3960 and 4018, while the invalidation is unchanged below 3778.

Europe: Breaking free

The STOXX 600 is finally moving away from the 21-year ceiling of ~400. The minimum target for a breakout above a multi-year ceiling is a double – in this case 800+. The 9-month RSI is at 73, just below overbought 75. If Chris Roberts’ view is correct, RSI should have a high ceiling: 80+ (very overbought) should be achievable. The ROC indicator has been signalling a change since 2011, with the lows around -15% well above the 2002-09 lows that went below the -40% level. Chris will look to establish a LONG position into a corrective dip.

Blonde Money

Germany: What kind of coalition will follow?

Helen Thomas says predicting the outcome of German elections is complicated by two elements of the electoral system: the 5% threshold to gain electoral representation and the new fixed 630 seats for the Bundestag. These electoral quirks might have had only a small impact in a stable system, but the German electorate has become just as fragmented as any other in the western world. Support has been ebbing away from traditional parties and seeking out the new. More than a quarter of German voters claimed they were undecided with just over a week to go. Despite the uncertainty, the market appears relaxed, working on the blasé assumption that the old guard will band together. Yet the grand coalitions and three-party coalitions (CDU/CSU, SPD and Greens) of the last few parliaments have led to increased voter discontent and stagnation for the German economy.

Trades in divergence

While the inflation picture is somewhat similar across the main economies tracked by Andreas Steno, the growth picture is starting to diverge—especially between the US and Eurozone—creating a range of compelling macro trades. While growth has clearly strengthened in the Eurozone, Andreas’ US growth nowcast is softening significantly in the first half of February, a shift that markets have yet to fully price in. Even with US fiscal spending cuts in effect, markets are prepared for a broader slowdown in growth momentum and Andreas sees strong value in betting on lower US rates or a weaker USD as global business cycles start to diverge. It remains his best guess that markets are still net short US duration relative to European duration, suggesting that that the market has been caught wrong-footed in the latest move in USD bond yields, reinforcing the value in betting on higher EUR rates or lower USD rates.

The quiet signs of a market top

Bull markets rarely die with fireworks. Instead, remarks Jawad Mian, they fall in a slow, unravelling process. The reason is simple, not all sectors and styles peak at the same time. Looking at thirty bull-market tops since the mid-1920s, the average gap between the first sector peak and the final high has been seven months. A market can stop being a bull market long before the index starts to fall. Jawad recalls the strategy of Jesse Livermore in 1916, who noticed the signs of the market falling one after the other even as the bulls raged around him. A hundred years later, the game–and human nature—remains the same. Investors have been roaring bulls, but, like Livermore, they’re now watching for the shift. And it’s happening.

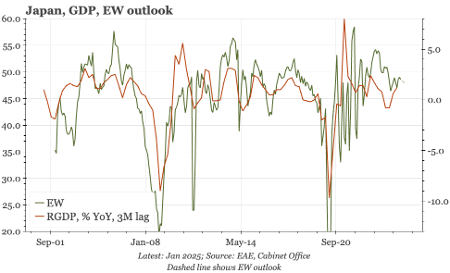

Japan: Wages support surprisingly firm consumption

Paul Cavey points out that the first estimate of Q4 GDP was solid, with growth of 2.8% QoQ annualised, much faster than market expectations of a 1% rise. That takes average growth in the three quarters from April 2024 to 2.5%, closing the gap with the growth path suggested by the Economy Watchers survey. RGDP is now once again back above the pre-pandemic level – though as that was now almost five years ago, this comparison shows how slow the economic recovery has been. The big driver of the strong result in Q4 was net exports, which on its own would have generated GDP growth of 3% annualised. While exports were strong, more surprising was the resilience of consumption in Q4. On a per capita basis, private consumption is now the highest since 2014.

Emerging Markets

Make Chinese equities investable again

There are many more reasons to be positive about Chinese equities again for both domestic and foreign investors. Continued regulatory easing to rekindle the spirits of the corporate sector; China’s manufacturing prowess which is often misjudged; a bottoming of the property sector; and resilient Chinese bonds and currency are all some of the main reasons outlined. Then there’s the fact that Chinese equities are not expensive, with the world still underweight Chinese assets (see graph). Chinese tech names are now a legitimate alternative to US names; the PE ratio of the US Mag7 is currently ~40x, why should investors not diversify into Chinese tech listed in Hong Kong, with a PE of 24x? As the Chinese economy rises from the bottom, expect USD/CNY to drift lower, not higher as most expect.

China: Jack Ma, the saviour?

Jack Ma’s meeting with President Xi is a sign that, after 4.5 years of stagnation, the Chinese state could be prepared to let the private sector have a much freer hand. This may be what is required to get technological innovation and investment going once again in China, and the stock market is already reacting. Currently, this is all talk, and it won’t be until we see any action that we will know whether this is a genuine change of heart or a plot to restore confidence; Richard Windsor sees it being the former. This is precisely what China needs if it is to come close to fulfilling its ambitions to be a leading technological and geopolitical power. The Chinese technology sector remains extremely cheap and if the state means what it says, there is a very long way to go in terms of upside in the shares of tech companies.

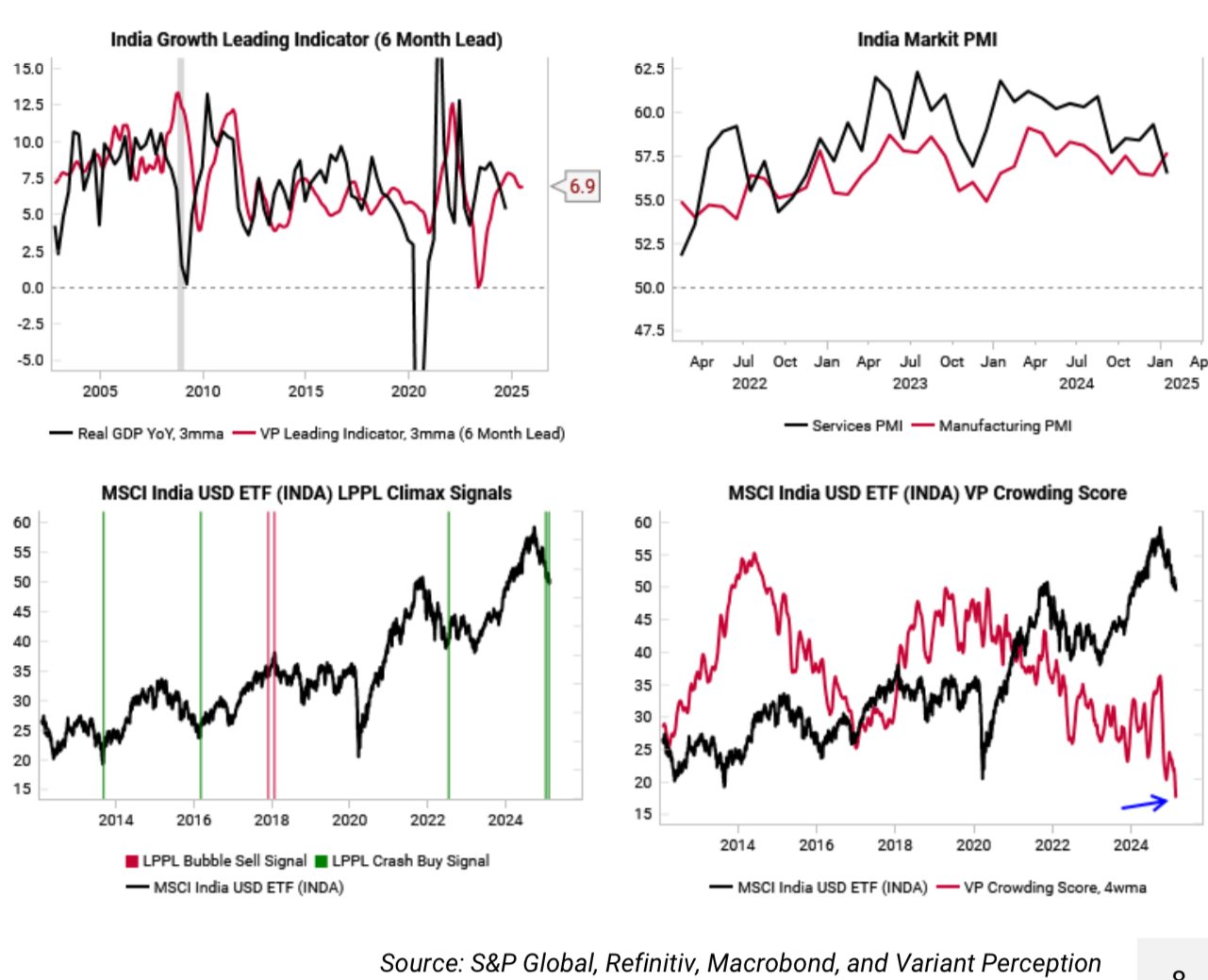

India: A contrarian view

The cyclical growth outlook in India is positive while inflationary pressures remain tame. The Variant Perception team’s main India growth leading indicator has a 6-month forward point forecast of 6.9% YoY real GDP growth (top left). Echoing this, Indian PMIs for services and manufacturing are both well above 50 (top right). Meanwhile, their Central Bank Regime model for the RBI has shifted dovish. Strong growth, rate cuts and the equity sell-off provides a compelling entry point. The LPPL and Crowding Score models are also flashing a clear buy, providing a contrarian indication of the potential for an equity rally. Add exposure to Indian equities.

Indonesia can’t hold pace

Indonesia's earlier upturn proved short-lived, and activity is weakening again. The latest data show a renewed slowdown in credit and retail spending, with our rough proxy index suggesting real growth of 3.5% or so going into 2025, i.e., neither a recession nor a boom. The pendulum swings back towards fixed income. With listed earnings flat and lacklustre growth momentum, Jonathan Anderson still doesn’t see Indonesia as an equity outperformer. Meanwhile, real rates remain high and BI is taking its time in the easing cycle, which makes carry and duration more interesting. The one potential issue is the rupiah, which has been a roller coaster over the past few quarters and still faces external deficits.

Mexico: The Art of (Trade) War

Over the last few weeks, Niall Ferguson’s team met with high level officials and representatives in Mexico. The trip emboldened their belief that President Sheinbaum will do “whatever it takes” to avoid tariffs and preserve USMCA, choosing to concede to American demands on security, the border and the trade deficit, including the trade relationship with China. This stems from a belief that the country will face an immediate recession should the trade war escalate. Despite Sheinbaum’s previous rhetoric against Trump, pragmatism will prevail to preserve USMCA and the economic benefits it has brought to Mexico.

What could derail Poland?

Poland is still outperforming its neighbours in terms of export dynamism, domestic activity also continues to rebound, and equity earnings and index performance have been solid. Jonathan Anderson asks, “what could get in the way?” The short answer appears to be "not much". Inflation is still a bit elevated, but real rates are moderate; the local economy is not meaningfully leveraged, and the external balance is still broadly supportive. The only wild card this year is the sharp fiscal deterioration, which may be something to watch in the medium term ahead.

ESG

Food inflation

One of Sustainable Market Strategies’ high-conviction calls for the coming decade is the high likelihood of strong, sustained food inflation. To put it simply, absent a massive productivity surge, it is unlikely that farmers will be able to feed the population the low-cost, high-calorie diet they have become accustomed to, especially as climate change wreaks havoc with growing seasons and creates the conditions for ever more animal viral outbreaks. Policy changes are set to disrupt things further. Investors should seek to buy companies in the consumer staples sector who have the greatest chance of passing through inflation to their consumers. Avoid the worst offenders in the unhealthy snack business, including Mondelez and PepsiCo.

Commodities

China opens up the flood gold gates

James Burdass notes that China’s policy change allowing insurers to invest in gold is a landmark moment that could unlock billions in new demand. The timing of this policy change also aligns with broader geopolitical shifts. The return of Donald Trump to the US presidency has introduced new uncertainties in global trade and economic policy. China’s move to allow insurers into the gold market could be viewed as part of a broader strategy to hedge against financial and geopolitical risks, including potential disruptions in US-China trade relations. While insurers are likely to be cautious in their approach, the sheer scale of potential inflows underscores gold’s growing importance in China’s financial system. As insurers gradually enter the market, this shift may provide long-term price support, further solidifying gold’s status as a critical asset in an increasingly uncertain global economy.

Ukraine/Russia and the impact on commodities

Kathleen Kelley notes that any peace agreement will open the door to resuming legitimate Russian commodity exports. The impact on supply and demand balances for these commodities will be nuanced thanks to lax sanctions implementation/cheating (oil), OPEC+ commitments (oil), lingering security concerns inherent in any dependence on Russian supply (natural gas) and the shift witnessed in traditional export destinations for these goods (grains, aluminium, nickel, copper, palladium). Russian gold faced Western sanctions, but gold is fungible. The real impact on gold came from the attempt at de-dollarisation and a workaround from global payment system exile, which drove central bank accumulation. Will negotiations involve Russia returning to the dollar with a greater allocation of dollars? Will that come at the expense of the euro or gold? The Trump administration seems likely to demand a move back towards the dollar from other BRICs and Russia is unlikely to get an exception.

Can Bitcoin reach $160,000?

Bitcoin prices have surged $50,000 since the BTC ETF launch, putting it on track to potentially reach the $140,000 - $160,000 target by the end of 2025. Markus Thielen points out that $142 billion has flowed into the crypto market, demonstrating how feasible this price movement is. However, despite bullish narratives around a potential strategic Bitcoin reserve or sovereign wealth fund acquisitions, Bitcoin’s upside remains tied to capital inflows. Matching this level of liquidity in 2025 will be challenging, which may limit BTC’s price trajectory within this range. Markus also calculates the Bitcoin Terminal Price at $190,847, advising investors to take profits should it reach this level.

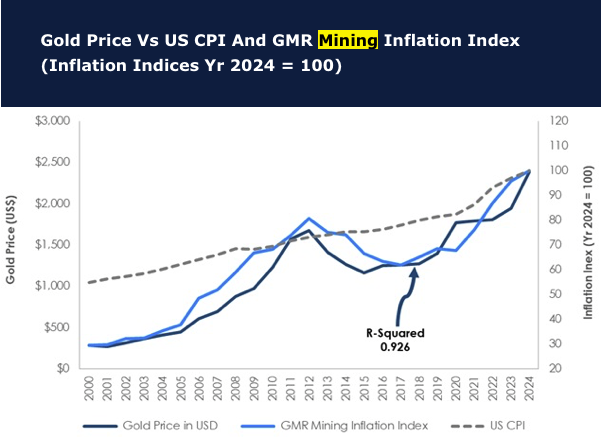

Gold: Limited downside?

As gold makes yet more record highs, Global Mining Research’s (GMR) latest report rationalises the moves to show that the correlation between the gold price and inflation remains true, using their own internal Mining Inflation Index. This is proven very useful in examining mining operating costs, commodity price moves and project capital cost escalation, and currently explains current gold prices. Whilst official inflation rates appear to contradict rising gold prices, GMR’s Index proves the relationship holds true, with the model holding a 2000-2025 R-squared of 0.926. A collapse in price is not imminent and may in fact have little material downside from present levels.